This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Verification provider Sumsub announced a partnership with blockchain data platform Chainalysis this week.

The integration will bring automated crypto transaction monitoring and secure data storage, as well as ensure regulatory compliance.

Sumsub made its Finovate debut at FinovateEurope 2020 in Berlin, Germany.

Full-cycle verification provider and FinovateEurope alum Sumsubannounced an integration with blockchain data platform Chainalysis this week. The partnership brings Sumsub’s Transaction Monitoring and Travel Rule solutions to the Chainalysis platform. This will enhance regulatory compliance and secure data storage, as well as provide automated crypto transaction monitoring for Chainalysis’ clients.

In a statement, the companies suggested that the partnership will help encourage greater digital compliance for businesses in the crypto space with functionality like unified workflows and automated transaction monitoring. Sumsub’s Transaction Monitoring solution is designed to help firms deal with the estimated $48+ billion in total fraud losses last year alone. The solution gives fraud and risk teams a single tool to manage the transaction monitoring process with provides fewer false positives and more efficient case management.

Additionally, the technology enables real-time fraud detection, and users can connect KYC, AML, and KYB verification with transaction monitoring for further vigilance against suspicious activity. With Travel Rule, Sumsub automates data transfers with counterparties to make sure firms remain compliant with regulatory obligations in different jurisdictions around the world.

“This partnership enables us to offer access to over one billion mapped addressses across multiple blockchains to those customers who use Sumsub’s Transaction Monitoring and Chainalysis crypto risk solutions,” Sumsub co-founder and Chief Innovation Officer Jacob Sever explained. “Sumsub’s solution’s enhanced capabilities, integrated with Chainalysis’ analytics and key management model, are reshaping the landscape of crypto compliance and security in the digital realm.”

Sumsub made its Finovate debut at FinovateEurope 2020 in Berlin, Germany. The company currently has more than 2,000 clients in fintech, crypto, e-commerce, transportation, gaming, and more. Businesses working with Sumsub have experienced 2.4x return on investment (ROI), $3.2+ million in net present value (NPV), and a payback period of less than six months.

So far in 2024, Sumsub has forged partnerships with B2B Gaming Services and embedded finance integrator AAZZUR. The company began the year teaming up with digital banking technology firm Plumery. In February, Sumsub launched its deepfake detection solution for video identification, an industry-first, and made its non-doc verification solution available in the U.S.

Headquartered in London, Sumsub – which stands for “Sum & Substance” – was founded in 2015. Co-founder Andrew Sever is CEO.

The EU Parliament approved the Artificial Intelligence (AI) Act today. Member states agreed upon the regulation in December 2023. Today, members of the European Parliament endorsed the act, with 523 voting in favor, 46 voting against, and 49 abstaining from the vote.

It’s no secret that AI is a double-edged sword. For every positive use case, there are multiple ways humans can use the technology for nefarious purposes. Regulation is generally effective in creating safeguards for the adoption of new technologies. However, delineating the boundaries of AI’s applications and capabilities is challenging. The technology’s vast potential makes it difficult to eliminate negative uses while accommodating positive ones.

Because of this, the European Union’s new Artificial Intelligence Act will have both positive and negative impacts on banks and fintechs. Organizations that learn to adapt and innovate within the boundaries will see the most success when it comes to leveraging AI.

That said here are four major implications the new law will have on banks:

Prohibited AI applications

The new law prohibits the use of AI for emotion recognition in the workplace and schools, social scoring, and predictive policing based solely on profiling. This will impact how banks and fintechs use AI for customer interactions, underwriting, and fraud detection.

Compliance and oversight

The ruling specifically calls out banking as an “essential private and public service” and categorizes it as a high-risk use of AI. Therefore, banks using AI systems must assess and reduce risks, maintain use logs, be transparent and accurate, and ensure human oversight. The law states that citizens have two major rights when it comes to the use of AI in their banking platforms. First, they must have the ability to submit complaints, and second, they have the right to receive explanations about decisions made using AI. This will require banks and fintechs to enhance their risk management and update their compliance processes to accommodate for AI-driven services.

Transparency

Banks using AI systems and models for general purposes must meet transparency requirements. This includes complying with EU copyright law and publishing detailed summaries of training content. The transparency reporting will not be one-size-fits-all. According to the European Parliament’s explanation, “The more powerful general purpose AI models that could pose systemic risks will face additional requirements, including performing model evaluations, assessing and mitigating systemic risks, and reporting on incidents.”

Innovation support

The law stipulates that regulatory sandboxes and real-world testing will be available at the national level to help businesses develop and train AI use before it goes live. This could benefit both fintechs and banks for support in testing and launching their new AI use cases.

Overall, the EU AI Act isn’t requiring anything outside of banks’ existing capabilities. Financial institutions already have processes, documentation procedures, and controls in place to comply with existing regulations. The act will, however, require banks and fintechs to either establish or reassess their AI strategies, ensure compliance with new regulations, and adapt to a more transparent and accountable AI ecosystem.

The Harbor Bank of Maryland has partnered with digital account onboarding specialist Prelim.

Courtesy of the partnership, the Baltimore, Maryland-based financial institution will leverage Prelim’s technology and expertise to enhance its account opening services.

Headquartered in San Francisco, California, Prelim made its Finovate debut at FinovateSpring 2022.

Digital account onboarding specialist Prelim and the Harbor Bank of Maryland have teamed up to bring digital account opening services to the customers of the Baltimore, Maryland-based financial institution.

Founded in 1982 with $2.1 million in assets, Harbor Bank of Maryland serves the Baltimore, Maryland metropolitan area with seven branch locations and a loan office in Silver Spring, Maryland. The bank offers a wide variety of banking services, including checking, savings, time deposits, credit and debit cards, and commercial real estate, as well as personal, home improvement, and other installment and term loans. With total assets of $377 million, Harbor Bank of Maryland is a designated Minority Depository Institution (MDI) and the first community bank in the U.S. to have an investment subsidiary, Harbor Financial Services.

San Francisco, California-based Prelim made its Finovate debut at FinovateSpring in 2022 and returned again the following year for FinovateSpring 2023. Co-founded in 2017 by Heang Chan (CEO) and Chris Blaser (CTO), Prelim offers a white-label platform that empowers banks to digitize their business banking operations. Via API, Prelim enables financial institutions to automate their business account onboarding, as well as connect to third party providers to meet AML, BSA, and CIP requirements. The platform also helps FIs launch other financial services and banking products from lending to merchant services.

In addition to its partnership with the Harbor Bank of Maryland, Prelim last month announced a collaboration with Movement Bank. Headquartered in Danville, Virginia, Movement Bank was launched in 1919 by a team of African American doctors, teachers, farmers, and preachers. From humble origins in a church basement and $6,500 in capital, the financial institution has grown into a major community resource. The bank was among the first to reopen during the Great Depression after banks were forced to close. The institution was also one of the first banks in Virginia to issue Federal Housing Administration (FHA) loans back in 1934. Movement Bank currently has $150 million in total assets.

Interested in demoing at FinovateSpring in San Francisco in May? We are happy to read applications from innovative companies with new solutions that are ready to show. Visit our FinovateSpring hub today to learn more.

A pair of Canada-based Finovate alums – Coconut Software and PayTic – have earned spots in the first cohort of the UK Fintech CTA program. The program runs for eight-weeks, much of it conducted online, and includes a needs assessment and company analysis, participation in the Innovate Finance Global Summit, virtual market briefings, mentor-matching and coaching, as well as strategic business-to-business introductions.

In addition to the digital sessions, participants in the program will be invited to attend local events in the U.K. that will help the firms build and grow their in-market presence and their network. This will enable them to introduce their value proposition to key market participants, investors, as well as potential customers.

Joining Coconut Software and PayTic are a number of other Canadian startups including Symend, OneVest, VoPay, Four Eyes Financial, Octav, and Sibli.

“We are so excited to be selected for the first cohort of the UK Fintech CTA, proudly representing our country’s growing payments landscape as we expand our efforts in the U.K.,” PayTic noted on LinkedIn last week. “Thank you Canadian Technology Accelerators | Accélerateurs technologiques canadiens for this recognition and opportunity to scale!”

Headquartered in Charlottetown, Prince Edward Island, PayTic made its Finovate debut last year at FinovateSpring. The company offers a SaaS solution that manages all of the significant aspects of program management for card issuers and BIN sponsors in a single interface. PayTic’s technology serves as a central hub within the payments ecosystem, enabling users to automate reconciliation, network report generation, dispute submission, fraud detection, network fee analysis, and robust business intelligence.

At FinovateSpring, PayTic founder and CEO Imad Boumahdi and Director of Product Kate Firuz demoed how PayTic’s platform can help banks, card issuers, BIN sponsors, and fintechs save significant amounts of money by analyzing and optimizing network fees against program activity. The technology enables users to instantly reconcile data across the payments ecosystem from the program and account level to the transaction level. This empowers users to identify exceptions in real-time, generate accurate reports, and remain compliant.

Founded in 2020, PayTic has raised $4 million in funding. Visa Accelerator and Outlierz Ventures are among the firm’s investors.

More than 4,000 kilometers to the west via the Trans-Canada Highway (44 hours if you’re driving), Saskatoon, Saskatchewan-based Coconut Software is the other Finovate alum that will be joining PayTic as part of the UK Fintech CTA program. Founded in 2007, Coconut Software offers a customer engagement platform to help financial institutions better schedule, manage, and measure customer, prospect, and employee interactions.

Coconut Software made its Finovate debut as part of our special all-digital FinovateSpring conference in 2021. At the event, Senior Solutions Engineer Andre Doucette demoed enhancements to the firm’s appointment scheduling and lobby management technology. These upgrades improved the platform’s online queuing and lobby management capabilities.

Named to the 2023 Technology Fast 50, Coconut Software counts a number of North American financial institutions among its customers, including RBC, Arvest Bank, Vancity, and Rogue Credit Union. The company has raised more than $35 million in funding from investors including Klass Capital and Information Venture Partners. Katherine Regnier is founder and CEO.

Interested in demoing at FinovateSpring in San Francisco in May? We are happy to read applications from innovative companies with new solutions that are ready to show. Visit our FinovateSpring hub today to learn more.

U.K.-based business banking platform Tide is expanding into Germany.

Tide didn’t release an exact timeline, but said that customers on its waitlist will be able to begin using a limited release of the company’s business banking tools “in the coming months.”

Germany is Tide’s second international market. The company launched in India in 2022.

Business banking platform Tide is expanding across international borders for the second time. The U.K.-based fintech announced today it will soon begin serving clients in Germany.

Tide did not offer an exact timeline for its expansion into Germany, but the wait list is currently open and the app will be available “in the coming months.” After Tide’s launch in Germany later this year, the company’s members will initially be limited to the app’s business account and card products. Access to Tide’s other features, including cash flow forecasting, will be rolled out in phases.

Among the reasons why Tide selected Germany as its next market is because large, traditional banks provide the bulk of services to small businesses in the region. Tide wanted to offer business owners a more simple, innovative platform to help them manage their business.

“Looking at what is on offer for SMEs in Germany, we believe there is a huge opportunity for Tide,” explained company CEO Oliver Prill. “Across all our markets, we continue to add to the services and products we offer to our members, as part of our mission to be the leading international financial platform for small businesses.”

Tide launched in 2015 to help small businesses save time and money on banking and administrative tasks. The business bank accounts offer accounting tools, expense cards, invoicing, payment collection capabilities, business loan comparisons, and cashflow insights. In 2022, Tide acquired lending marketplace Funding Options for an undisclosed amount. Tide currently counts more than 775,000 sole traders, freelancers, and limited companies as clients.

“Our success in the U.K. has been built on having a deep understanding of the pain points of small businesses, the self-employed and freelancers. Our goal is to help reduce the financial and administrative management burdens with our advanced business financial platform,” added Prill.

Today’s launch isn’t Tide’s first foray into international markets. The company expanded into India in 2022 and has since added more than 200,000 members in the region. Tide now employs 1,600 people in offices across India, Bulgaria, as well as its headquarters in London.

March 10th marked the one-year anniversary of the collapse of Silicon Valley Bank (SVB). While the event isn’t necessarily something to celebrate, it is a great time to reflect on what the industry has learned and how things have change.

Looking back on the aftermath of SVB’s liquidity crisis, we have seen shifts in behavior and strategy that are starting to reshape the landscape for both banks and fintechs. I had the privilege to speak with Law Helie, General Manager of Consumer Banking at nCino, to gain insights into these changes and how institutions are adapting to meet evolving consumer expectations and regulatory demands.

Finovate: We’re approaching the one-year anniversary of SVB’s liquidity crisis. In the past 12 months, how has the industry responded? Have you seen any changes in behavior from banks or fintechs?

Law Helie: Regardless of size, a consistent banking trend is the re-emphasis on building up deposits. After the liquidity crisis last year, banks became more risk-averse and leaned on their deposits as a shield against volatility.

Another trend is the shift to relationship banking via technology. Banks are leveraging cloud-based tools to unlock more data within their organization to better inform and tailor their services to customers for core offerings, including loans, CDs, high-yield savings and more. We expect intense competition around these services as banks prioritize opening multiple service streams with customers to deepen the relationship and hold onto deposits.

Finovate: How will banks approach their spend on fintech following the SVB crisis?

Helie: Expect banks’ spending on fintech tools to grow exponentially. This isn’t a new phenomenon, but the pace of acceleration since SVB is significant as banks seek ways to better compete in a crowded market.

Banks are deploying technology to help understand their cost of funds base, attract deposits, drive internal efficiencies and, most importantly, to help create a sense of stability. As we await more certainty from the Fed around economic forecasting, we expect to see an increase in tech spending, especially at a time when banks’ appetite for increasing efficiency continues to grow at a rapid pace.

Finovate: How about end consumers—both retail and commercial bank customers—have they changed their attitudes and behavior?

Helie: Post-SVB, end consumers in all lines of business are more aware and educated on deposit limit risks that come with over-exposure. Our FIs have told us that their customers are searching for ways to have more security, including wanting to know how they can limit their risk of exposure and how to structure their accounts for FDIC limits. In addition, some of our customers have incorporated the use of CDARS, a Certificate of Deposit Account Registry Service, that can help customers disperse funds into multiple accounts.

The overall attitude and behavior of end consumers is now that they need to pay attention to FDIC limits, disburse their deposits, and have an increased focus on their wealth management. This shift underscores a proactive approach among consumers toward safeguarding their financial assets.

Finovate: Given these behavioral and attitude shifts, how can banks and fintechs adapt to these changes?

Helie: Most banks have siloed systems, meaning there is no singular source of truth for their data. Yet customers don’t think this way – they look at their needs holistically. Serving these customers requires a client-centric model that is efficient and driven toward self-service.

And the more products a customer has with a bank, the stickier they are. In order to retain existing and new depository relationships, banks can best position themselves by providing a wide suite of banking offerings and services, in particular digital offerings.

Banks also have an opportunity to leverage fintechs to gather a 360-degree view of the customer, allowing them to understand what is going on across all accounts. With that information, banks can leverage relationship banking techniques to provide customers with the tailored products and services that they want and need.

Finovate: What impact has SVB’s liquidity crisis had on regulations so far and how are banks and fintechs responding?

Helie: Regulations have been put in place to try and mitigate the risk of another SVB collapse. Despite NYCB’s recent issues, we are not seeing the same level of concern spread to other financial institutions as it seems the public has a better understanding of the underlying reason for the issues NYCB is currently having.

Financial institutions are actively pursuing ways to strengthen their deposits bases by reviewing FDIC limits. Notably, some FIs have taken measures to impose restrictions on the maximum amount of cash that can be held in an account, aligning with the FDIC limit. Fintechs are helping FIs by not only providing the framework for streamlined experiences that help meet customer needs, but also allowing them to responsively acquire new funds for those customers looking to diversify their deposit base.

Finovate: Looking ahead, what advice do you have for banks and fintechs navigating the ever-competitive game of increasing deposits?

Helie: The market expects the Fed to reduce interest rates one-to-three times this year. Americans are waiting on the sidelines for better rates so that they can shop for refinancing or fresh loan opportunities.

Banks that are well-prepared have a tremendous opportunity to help people get a better handle on their finances and position themselves as a partner for life. Those that struggle to quickly evaluate inquiries or match competing offers could frustrate customers that want to take advantage of the improving environment.

Cloud-based tools that utilize data and AI to help banks evaluate a fresh loan or refinancing request quickly are at a tremendous advantage. Institutions that maintain the sleepier pace of the past year will be rapidly outpaced by their peers and they will have few opportunities to make up the gap.

This week marks both the one-year anniversary of Silicon Valley Bank’s collapse and St. Patrick’s Day. Let’s see if this week’s news projects a luckier year for fintechs. Check back for real-time updates on how the fintech landscape evolves this week.

N26launches its Instant Savings accounts in 13 new markets in Europe.

Backbase and West Monroe team up to combine Backbase’s Engagement Banking Platform with West Monroe’s financial services advisory and digital experience capabilities.

Cryptocurrency

Blockchain data platform Chainalysisintegrates with verification provider Sumsub to enhance regulatory compliance, and provide automated transaction monitoring for its clients.

Funding search engine Fundica announced a collaboration with Visa last week.

The partnership will make it easier for entrepreneurs to access government funding.

Headquartered in Montreal, Quebec, Canada, Fundica made its Finovate debut last year at FinovateSpring 2023.

A newly announced collaboration between North American funding search engine Fundica and Visa will democratize the process of securing government funding for SMEs, especially those founded and led by members of underrepresented communities. Together Fundica and Visa will offer an intelligent solution that helps SMEs and entrepreneurs find relevant government funding and private sector grants based on their individual business’ needs and goals.

“We are thrilled to be working with Visa to further democratize access to government funding for small businesses across North America,” Fundica co-founder and CEO Mike Lee said. “Visa and Fundica are both deeply committed to fostering accessibility and inclusion in business communities – making this collaboration a great fit.”

Fundica’s platform enables small businesses to identify and apply for relevant government and private sector funding, while giving financial institutions the ability to promote inclusion and serve as a more comprehensive financial advisor to its SME clients. The technology aggregates data from tens of thousands of funding programs, leveraging strategies from discovery and tracking bots to funders, collaboration partners, and its own internal research team.

The search experience for the business customer is straightforward; companies enter basic information about their business and Fundica displays appropriate funding options in order of relevance. The solution presents each opportunity in a detailed, one-page summary, making it easy for business customers to confirm their suitability for the funding and to begin the application process. Funding sources include grants, tax credits, government loans and loan guarantees from federal, state, provincial, and municipal entities – as well as the private sector.

On the backend, FIs can see the profiles of the companies looking for funding and make informed connections with qualified leads and clients. The platform also enables institutions to identify key business behavioral trends. Some of the largest FIs in North America license Fundica’s AI-powered funding search engine to help them acquire and retain business customers.

Headquartered in Montreal, Quebec, Canada, and founded in 2017, Fundica made its Finovate debut at FinovateSpring 2023. At the conference, Fundica’s Lee demonstrated new enhancements to the platform’s front- and back-ends. These enhancements included a traffic augmentation solution, improved traffic conversion, and improved user engagement.

A Finovate alum for more than a decade, Visa made its Finovate debut at FinovateSpring 2010 in San Francisco. The company is also an alum of our developers conference, participating in FinDEVr Silicon Valley in 2014.

Interested in demoing at FinovateSpring in San Francisco in May? We are happy to read applications from innovative companies with new solutions that are ready to show. Visit our FinovateSpring hub today to learn more.

Griffin was granted approval from the U.K.’s Prudential Regulation Authority (PRA) and Financial Conduct Authority (FCA) to offer banking services in the region.

Along with announcing the banking approval, Griffin also unveiled it has secured a $24 million (£19 million) Series A extension round to fuel the launch of banking services.

Initially, Griffin does not plan to offer direct-to-consumer banking accounts, but will offer business bank accounts to help organizations manage their own finances and hold client funds.

U.K.-based BaaS fintech Griffin has been granted approval to launch as a fully operational bank. The company announced yesterday that the U.K.’s Prudential Regulation Authority (PRA) and Financial Conduct Authority (FCA) granted Griffin approval to offer bank services in the U.K.

Fueling the launch is a $24 million (£19 million) Series A extension round. Crunchbase reports that the investment will boost Griffin’s total funding to $66.7 million (£52.1 million), while TechCrunch stated the total as $52 million (£40.6). The new round was led by MassMutual Ventures, NordicNinja, and Breega. Existing investors Notion Capital and EQT Ventures also participated. Griffin will use the funds to scale the bank and enhance its infrastructure.

With the proper approvals in place, Griffin can now offer banking, payments, and wealth management accounts to third party organizations. Interestingly, Griffin is not launching direct-to-consumer bank accounts, but will offer business bank accounts to help organizations manage their own finances and hold client funds.

The authorization comes after Griffin’s year-long mobilization period during which it was allowed to test and refine its products, build banking integrations, and develop its systems in preparation for the debut as a full bank.

“Today’s announcement is a culmination of years of hard work by the incredible team at Griffin,” said company CEO David Jarvis. “I’m particularly grateful to our pilot customers for placing their trust in us, and look forward to helping them continue to scale innovative products at the intersection of technology and finance.”

Founded in 2017, Griffin offers BaaS tools that include client onboarding, regulatory compliance safeguards, client money accounts, and payments. The company plans to launch branded debit, prepaid, and digital cards soon. Griffin’s direct banking tools, launched this week, include operational accounts, credit, and lending.

“As the UK’s first full-stack BaaS platform with a banking license, Griffin is the partner of choice for fintechs and brands to build innovative financial products with a seamless client experience,” said MassMutual Ventures Managing Partner Ryan Collins.

Sila has partnered with Trice to leverage the company’s safeguards for instant payments.

Trice will help Sila’s customers eliminate insufficient funds and unauthorized debit for ACH transactions.

Sila combines FedNow and The Clearinghouse’s RTP to allow ACH transactions to be settled in seconds.

There has been some movement in the instant payments world this week. Banking and payment infrastructure-as-a-service company Sila has partnered with instant payments platform Trice.

Under the agreement, Sila will leverage Trice’s built-in safeguards for instant payments. Founded in 2022, Trice offers the ability to eliminate ACH return codes R1 and R5. For those unfamiliar with ACH return codes, R1 typically refers to “insufficient funds,” while R5 refers to “unauthorized debit to consumer account using corporate SEC code,” meaning the accountholder did not authorize the transaction. By eliminating these return codes, Trice will help Sila lower costs, reduce losses, decrease fines, and ultimately improve the customer experience.

“This partnership reflects our dedication to simplifying financial transactions and making money movement more accessible, reliable, and cost-effective for businesses of all sizes,” said Sila Co-Founder and Chief Strategy Officer Shamir Karkal. “Trice’s innovative instant payment solutions align perfectly with our mission, and together, we aim to set new industry standards for secure and efficient money transfer services.”

Oregon-based Sila launched its ACHNow product in 2018. The tool combines The Clearing House’s RTP, the U.S. Federal Government’s FedNow, and Sila’s own instant settlement product that allows all ACH transactions to be settled in seconds. When businesses submit a standard NACHA file, ACHNow routes each transaction to either RTP or FedNow. In the event the transaction cannot be routed on either of those rails, Sila uses its own instant settlement product to clear the transaction.

“With new faster payment systems becoming available, Sila is currently in a great position to create excellent payment experiences to surprise and delight their customers,” said Trice Co-Founder and CEO Doug Yeager. “Together with Sila, we’re excited to bring these groundbreaking solutions to businesses and financial institutions, further enhancing the financial ecosystem with the promise of smarter, faster, and more secure money movement.”

This week’s edition of Finovate Global takes a look at recent fintech developments in Latin America. The region was one of the few places in the world to see significant fintech funding in Q2 of 2023. Further, fintech in Latin America will be the focus of a special panel at FinovateSpring in May.

Here are a handful of headlines to help you get up to speed on the variety of fintech innovation happening in countries like Mexico and Colombia.

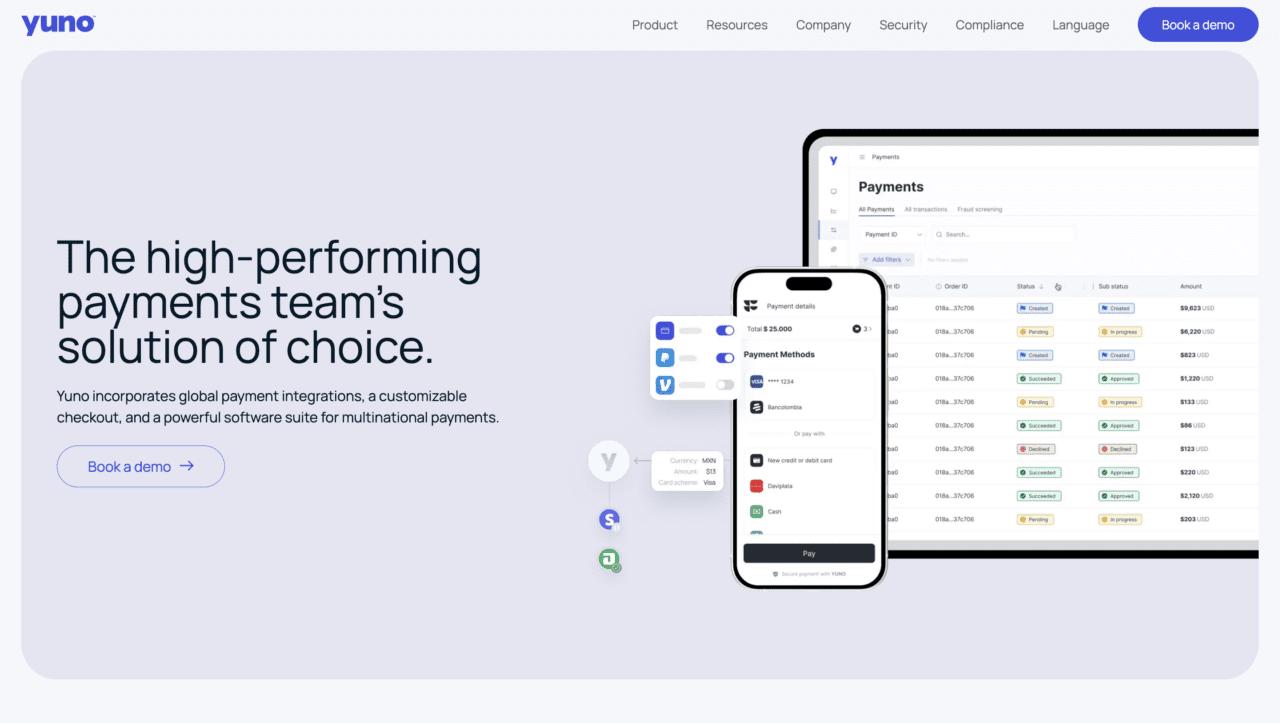

Colombian payments orchestration platform Yuno raises $25 million

Payments, as we say in the fintech business, is the gift that keeps giving. And this week, Colombian payments orchestration platform Yuno is on the receiving end. The company announced this week that it has raised $25 million in funding from a consortium of investors including DST Global Partners, Andreessen Horowitz, Tiger Global, Kaszek Ventures, and Monashees.

With customers ranging from McDonald’s to Avianca, Yuno offers fast and reliable payments orchestration for businesses in industries like e-commerce, retail, and mobility. The company’s platform offers features such as one-click checkout modifications and smart routing. Yuno also integrates data from all payment processors and anti-fraud tools into a single, unified interface. The company will use this week’s investment to support its operations in both North and South America. The investment also will help fuel Yuno’s expansion to new markets in Europe, Asia, and Africa.

“This financial backing validates our vision and our ability to take the global payments industry into the future, helping fuel positive change across many different sectors of the economy. We are thrilled to bring our cutting-edge solutions to new markets,” Yuno CEO and co-founder Juan Pablo Ortega said.

Mexico’s Ziff acquires digital lender Arrenda

Meanwhile, a few miles north, Mexican revenue-based financing company Ziffhas acquired Arrenda, a Mexico-based digital lending startup. Terms of the transaction were not disclosed. Arrenda founder and CEO Joe Merullo will take the position of Chief Technology Officer in Ziff’s C-suite.

Ziff founder and CEO Gerardo Name said the acquisition will boost the company’s product offering and “enable us to rapidly penetrate new market sectors.” Currently, Ziff’s revenue-based financing solution provides liquidity to Mexican SMEs – which often have little to no credit histories – by funding up to 36 months of receivables. The acquisition will enable Ziff to leverage Arrenda’s Adelanta digital lending platform, which enables Mexican property owners convert future rental payments into cash within 24 hours. Name added that he hopes to see Ziff distribute more than $1 billion pesos to Mexican SMEs by the end of 2027.

BBVA Technology expands to Latin America

Created in 2023, BBVA Technology announced its expansion to Latin America this week. To be headquartered in Mexico, the new entity – officially titled “BBVA Technology en América” – represents the merger of a number of technology companies that previously operated under the name BBVA Axial Tech. The goal of the nearly 600-strong body is to help advance BBVA Group’s digital transformation objectives. The company noted that in addition to a regional expansion, the creation of BBVA will help boost career opportunities for BBVA’s tech talent.

From Mexico City, Mexico, BBVA Technology will provide technology services to BBVA firms operating in Argentina, Colombia, Mexico, Peru, Uruguay, and Venezuela. Former BBVA Axial Tech CEO Robert Altes will serve as CEO of the new company.

Note that BBVA has also set up a companion entity in Europe – “BBVA Technology in Europe” – led by CEO Ricardo Jurado and headquartered in Spain.

Here is our look at fintech innovation around the world.

Asia-Pacific

Savis and Open Banking advisory firm Konsentus announced the creation of an operational structure for open banking in Vietnam.

New Zealand-based Kiwibank went live with ACI Worldwide’sEnterprise Payments Platform.

Hong Kong’s Mox partnered with Wise to enable low-cost, international payments directly from the Mox app.

Sub-Saharan Africa

South African payroll and HR software company PaySpace agreed to be acquired by HR startup Deel for $100 million.

Kenya’s Equity Bank launched instant withdrawals courtesy of a partnership with PayPal.

A partnership between Mastercard and Ethiopian commercial bank Awash Bank will bring new payment solutions to consumers in the country.

Currencycloud was offered In-Principle Approval to serve as a Major Payment Institution license holder in Singapore.

If granted the license, Currencycloud will be able to offer its full suite of intra-regional and international money movement services to Singapore businesses.

“Having the license would allow us to integrate with the robust financial network in Singapore and collaborate with valuable industry players,” said the company’s Managing Director of APAC Rohit Narang.

B2B cross-border payments fintech Currencycloud announced this week that the Monetary Authority of Singapore (MAS) offered the company In-Principle Approval (IPA) to serve as a Major Payment Institution (MPI) license holder in the region.

If the MAS grants Currencycloud the MPI license, the company will be able to offer its full suite of intra-regional and international money movement services to Singapore businesses. These additional capabilities will allow the U.K.-based company to process intra-Asia and east-to-west payments more quickly, efficiently, and seamlessly.

The MPI license will also impact Singapore-based businesses, which will be able to leverage Currencycloud to help their customers make conversions and payouts in their own time zones and local currencies. Ultimately, the license will help these local businesses launch new financial services quickly by leveraging local networks combined with its multi-currency account capabilities.

“The IPA for a Major Payment Institution License is testament to the strength of the Currencycloud brand,” said Currencycloud Managing Director of APAC Rohit Narang. “Having the license would allow us to integrate with the robust financial network in Singapore and collaborate with valuable industry players. The payments opportunity in Asia-Pacific is significant, and Singapore’s excellent infrastructure, world-class regulatory system, and strategic geographical location serve as an ideal base for accelerating future payments innovation across the region.”

Founded in 2012, Currencycloud facilitates cross-border, multi-currency transactions. In addition to offering virtual wallets, the company also enables banks, fintechs, and FX brokers to offer their users the ability to send, receive, and manage their multi-currency payments. Among the company’s clients are Starling Bank, Revolut, Penta, and Lunar.

Currencycloud was acquired by Visa in 2021. Mike Laven is CEO.