This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

You’ve likely been following the fallout from Synapse’s bankruptcy earlier this year. BaaS provider Synapse filed for Chapter 11 bankruptcy in April, leaving its clients, including Evolve Bank & Trust and multiple others, unable to verify and manage funds. In all, around $85 million in consumer funds are missing due to discrepancies in Synapse’s records.

Adding to the confusion, the dispute is ongoing in court, and because Synapse is a fintech and is thus unregulated, regulatory bodies are unable to protect consumers, many of whom are still missing their funds.

As a result of this nightmare, the FDIC has advanced a notice of proposed rulemaking for what it is calling Requirements for Custodial Deposit Accounts with Transactional Features and Prompt Payment of Deposit Insurance to Depositors. The regulatory body is currently taking public comment on the rule.

As it currently stands, the rule applies to bank accounts that fit into three categories:

The account is established for the benefit of beneficial owners

The account holds commingled deposits of multiple beneficial owners

A beneficial owner may authorize or direct a transfer through the account holder from the account to a party other than the account holder or beneficial owner

Here are five things banks with accounts that fit these categories should know about potential implications the rule may have on them.

Strengthened recordkeeping requirements

Advanced recordkeeping should already be part of a bank’s routine. However, the proposed rule is specific in its requirements, stipulating that banks working with non-bank entities (as in a BaaS partnership) must maintain accurate records that identify the beneficial owners of custodial deposit accounts that are held on behalf of consumers, which is typical in a BaaS agreement. Maintaining records of custodial accounts will help regulators ensure that deposit insurance can be quickly and accurately provided in the event of a bank failure.

Continuous third-party records access

The proposed rule states that if banks rely on non-bank companies to manage custodial deposits and their records, the bank must have continuous, direct access to records held at the third party organization. This requirement aims to prevent disruptions to operations, as what we saw in the Synapse bankruptcy case earlier this year. Ultimately, if banks have transparent access to third party records, they can help customers maintain access to their funds.

Annual compliance and validation

Under the new rule, FDIC-insured, BaaS-enabled banks will be required to conduct an annual, independent validation to verify that their third party partners are maintaining accurate deposit records. Banks will send the records, which must be accurate and compliant with the FDIC’s standards, to the FDIC and to the bank’s primary federal regulator. The purpose of this stipulation is to ensure consumers are able to access their funds without delays and to increase the reliability of custodial funds arrangements.

Consumer protection and transparency

Consumer protection is the underlying reason behind the new proposed rule. A large piece of this provides clarity about FDIC insurance. As such, BaaS-enabled banks will be expected to ensure that their consumers fully understand the coverage and protections of their deposited funds, particularly when dealing with non-bank custodians.

Heightened money laundering

The document also emphasizes that banks must exercise strengthened internal controls and anti-money laundering (AML) compliance requirements. Notably, the ruling also emphasizes that banks must ensure that their third-party partners do not facilitate financial crimes.

This week’s proposed rulemaking highlights two truths in financial services. First, the additional requirements can potentially add burdens on banks that are already weighed down by multiple reporting responsibilities. Yesterday, Vice Chairman Travis Hill voiced his concern, saying, “I recognize that certain types of pass-through arrangements have become much more complex in recent years, exacerbating the potential risks…” Hill said, however, that he is voting in favor of the proposal, explaining that, “improving recordkeeping and reconciliation practices (1) can reduce the likelihood of another Synapse-like disaster in the event of a third-party failure, and (2) may result in a more orderly resolution in the event the bank fails.”

The second truth today’s proposed rulemaking underscores is that the financial services industry needs a national fintech charter that can monitor, regulate, and enforce third parties that manage and handle consumer funds. Banks have long been subject to strict regulations and reporting requirements. But should banks that have conducted the proper due diligence be held responsible for the actions (or inaction) of their third party partners? It is time for fintechs to step up and share the responsibility.

Identity verification specialist ID-Pal announced a global strategic partnership with CLOWD9.

The partnership will integrate ID-Pal’s AI-powered identity verification technology into CLOWD9’s payment solutions portfolio.

ID-Pal made its Finovate debut at FinovateFall 2024 in New York.

Fresh off its Finovate debut at FinovateFall this month, identity verification specialist ID-Pal has announced a global strategic partnership with CLOWD9. Courtesy of the partnership, CLOWD9 will offer ID-Pal’s AI-powered identity verification technology via its payment solutions portfolio.

“This strategic partnership will allow CLOWD9 clients to access both a compelling end-to-end identity solution and an AML screening solution with advanced AI-fraud detection capabilities,” CLOWD9 CEO and Co-Founder Suresh Vaghjiani said.

Using a combination of document, database, and biometrics checks, ID-Pal enables businesses to verify the identity of their customers in real-time. Available via API, SDK, or through the Salesforce App Exchange, ID-Pal’s technology detects AI-generated documents, deepfakes, and injection attacks, providing advanced fraud detection without requiring direct access to customer data. ID-Pal also streamlines OFAC, AML, and KYC processes into a single compliant workflow to ensure a comprehensive audit trail.

“We’re delighted to be adding our award-winning identity verification solution to the CLOWD9 technology portfolio,” ID-Pal Enterprise Sales Manager Mark O’Hara said. “Together we can help financial institutions adapt and thrive in a new world of digital payments and enhanced security by democratizing secure, robust fraud prevention tools.”

The partnership with CLOWD9 advances the company’s mission to revolutionize the payment industry through a combination of advanced payment processing and AI-powered identity verification. Founded in 2021 and headquartered in London, CLOWD9 was among the first B Corp certified payments companies. The firm offers a cloud-native, decentralized issuer payments processing platform that serves challenger, consumer, and SME banks; e-wallets and crypto exchanges; virtual and corporate card programs; and more.

ID-Pal is not the only Finovate alum that CLOWD9 has teamed up with in 2024; the company announced a partnership with reconciliation and reporting services provider Kani Payments in June. Like ID-Pal, Kani is a relative newcomer to Finovate, debuting at FinovateSpring last year. Additionally, this week’s news from CLOWD9 comes just days after the company introduced new Chief Technology Officer Paul Hansford. Hansford comes to CLOWD9 after six years as head of software engineering for payment company Thredd.

Founded in 2016 and headquartered in Dublin, Ireland, ID-Pal made its Finovate debut at FinovateFall 2024. At the conference, company CEO and Founder Colum Lyons demoed ID-Pal’s technology that uses “pure AI, not people,” to provide real-time identity verification. In his remarks, Lyons highlighted the fact that many legacy vendors in the space rely as much on people for identity verification as they rely on technology. In contrast, he said, ID-Pal’s 100% AI-powered platform leverages 160+ trusted data sources and 7,000+ identity documents to provide more accurate results and greater efficiency.

Xero announced plans to acquire Syft Analytics, a collaborative reporting tool.

Financial terms of the agreement were not disclosed, but the deal is expected to close between October and December of this year.

Xero plans to integrate Syft’s technology into its existing accounting offering, and it will also continue to maintain Syft as a standalone company.

Small business accounting software company Xero has announced plans this week to acquire collaborative reporting tool Syft Analytics. Financial terms of the deal were not disclosed.

South Africa-based Syft was founded in 2017 to help small businesses leverage their financial data. In addition to automated, customizable reports, businesses can also create financial reports and disclosures. The tool can also consolidate financial information from any accounting software, trial balance, transaction list, or ERP.

“We’ve worked closely with Xero’s teams and customers over the past seven years,” said Syft CEO Vangelis Kyriazis. “Having met Xero’s senior leadership team over the past few months, we knew that joining Xero was a natural fit and would advance our shared goal of helping small businesses succeed.”

Xero has worked with Syft since February of 2018. The two first partnered when the New Zealand-based company added Syft to its App Store, which allowed Xero customers to leverage Syft’s custom reporting features.

Once the acquisition is finalized, Syft will continue to operate as a standalone offering for small businesses, accountants, and bookkeepers – regardless of whether they are Xero clients or not. Xero also plans to embed Syft’s functionality into its existing platform, aiming to enhance its own analytics and reporting capabilities.

“We look forward to bringing this exciting vision to life by strengthening our insights, advanced reporting and analytics offerings through capabilities such as benchmarking, long term cash flow forecasting and multi-entity reporting,” the company said in a blog post. “Our goal is to bring the power of premium insights and advanced reporting functionality to our customers so they can reap the value for their business.”

The acquisition is expected to close between October and December 2024.

Founded in 2006, Xero listed on the New Zealand Stock Exchange (NZX) in 2007 and the Australian Securities Exchange (ASX) in 2012. In January 2018, the company consolidated to list solely on the ASX and now boasts a market capitalization of $22.58 billion. The company counts 4.2 million subscribers.

Earlier this year, Xero launched new inventory management software called Xero Inventory Plus, which it anticipates will help goods-based small business owners track and manage their inventory across different channels.

MoneyLion will integrate TransUnion’s data and credit solutions into its hosted enterprise credit-decisioning platform and direct-to-consumer finance tools.

Leveraging TransUnion’s data will help MoneyLion deliver more personalized and relevant financial offers, and ultimately improve the user experience.

TransUnion also offers marketing, fraud, risk, and advanced analytics tools. The company showcased its Enchanced BreachIQ tool at FinovateSpring earlier this year.

Mobile banking platform MoneyLion will be adding personalized touches to its consumer-focused products and services thanks to a partnership with TransUnion.

Under the agreement, MoneyLion will integrate TransUnion’s data and credit solutions into its hosted enterprise credit-decisioning platform and direct-to-consumer finance tools. By using the data from TransUnion, MoneyLion will be able to deliver more personalized and relevant financial offers to its clients, which it expects will improve the user experience. For its part, TransUnion will see its credit solutions expand their reach into not only the MoneyLion platform, but also to its partner network.

TransUnion Executive Vice President and Head of Financial Services Jason Laky said that the partnership will drive efficiency and innovation in the industry. “By integrating our comprehensive credit data with MoneyLion’s innovative digital acquisition platform,” he added, “we can offer a more robust experience to consumers and our partners alike, ensuring informed decision-making and greater consumer satisfaction.”

TransUnion was founded in 1968 and entered into the consumer credit reporting industry in 1969. Since then, the Illinois-based company has expanded its services to offer marketing, fraud, risk, and advanced analytics. As part of its risk portfolio, TransUnion offers Enhanced BreachIQ, which it demoed earlier this year at FinovateSpring. The technology behind BreachIQ originated from Breach Clarity, a fintech founded by Jim Van Dyke that won Best of Show honors at FinovateSpring 2020.

New York-based MoneyLion, which was founded in 2013, offers both direct-to-consumer banking tools as well as a marketplace of embedded banking tools, called Engine, for businesses. This enterprise technology suite serves as a marketplace for financial products, enabling financial services and non-financial services companies alike to add embedded finance to their business leveraging MoneyLion’s API.

“This partnership with TransUnion exemplifies MoneyLion’s commitment to creating a dynamic digital consumer finance ecosystem where consumers can seamlessly access the financial tools and insights they need, while also enabling financial institutions to engage with customers more effectively,” said MoneyLion Co-Founder and CEO Dee Choubey. “By integrating our leading platform with TransUnion’s credit data solutions, we can offer consumers more personalized and relevant financial products that meet their unique needs at every stage of their financial journey.”

The Streamly Fintech Insights series provides analysis and discussion on major issues impacting banks, credit unions, fintechs, and financial services providers of all kinds.

Featuring senior leaders in fields ranging from banking to venture capital to media strategy, the Streamly Fintech Insights series offers a look into the innovative technologies that are helping financial institutions turn challenges into opportunities for themselves and their customers.

This week, we’re showcasing four new discussions from Streamly’s Fintech Insights series.

Embedded Finance with Eric McCabe, Head of Embedded Finance, Citizens Bank; and Amber Gerstung, Senior Managing Director, Head of Embedded Payments, SVB.

What’s Hot and What’s Not at FinovateSpring with Jason Henrichs, CEO, Alloy Labs; Alenka Grealish, Co-Lead Generative AI Research, Celent; and Charles Elkan, Professor of Computer Science, University of California.

Financial services software provider Finastra has teamed up with onboarding specialist Prelim.

Courtesy of the partnership, Finastra will integrate Prelim’s technology into its Finastra Phoenix core solution to enhance the account opening experience.

Finastra was formed via a merger between Misys and D+H in 2017. Prelim made its Finovate debut in 2022.

Financial services software company Finastraannounced a partnership with onboarding specialist Prelim. Finastra will integrate Prelim’s technology into its Finastra Phoenix core solution to enhance the deposit account opening experience for both retail and commercial accountholders.

“In a digital-first society, consumers and businesses expect their financial solutions to be agile and transform as needed to keep pace with their needs,” said Peter Longo, VP of Product Management for U.S. Mid-Market Banking Solutions at Finastra. “As we look to continuously enhance our offerings, Prelim is a trusted partner to support this transformation and our Open Finance ecosystem. We look forward to working together to deliver the innovations community banks and credit unions across the United States need to stay ahead of the competition.”

Prelim’s technology automates the application process, as well as internal processes such as reviewing, processing, underwriting, and servicing. This accelerates account opening and simplifies complex back-office operations. Prelim integrates seamlessly with Phoenix APIs, and newly created accounts are reflected in the digital banking solution, ensuring a cohesive, user-friendly experience.

“Customers expect an easy-to-use, real-time onboarding process when applying for a new financial product or service,” Prelim CEO and Co-Founder Heang Chan said. “We’re excited to be partnering with Finastra to help accelerate retail and commercial deposit account opening for financial institutions around the world.”

Finastra was forged in 2017 as a result of the integration between Finovate alum Misys and D+H. Headquartered in the U.K., the company provides financial services software applications for payments, lending, treasury, capital markets, and both retail and digital banking. Finastra has more than 8,100 clients in 130 countries, including 45 of the world’s top 50 banks.

In recent months, Finastra has forged partnerships with technology consultancy and digital solution provider Tech Mahindra, supply chain finance platform CredAble, and full-cycle verification platform Sumsub. The company’s technology powered new offerings like cloud-first ORO Bank of Bhutan and Bank Midwest’s digital-only OnePlace.bank. Finastra introduced Mike Stawchansky as its new Chief Technology Innovation Officer in March.

Prelim made its Finovate debut at FinovateSpring 2022. At the conference, the San Francisco, California-based fintech demonstrated its white-labeled platform that helps banks build more than 100 financial apps and digital experiences for customers and members. Prelim’s clients use the platform to add deposit accounts, treasury services, credit cards and more to their offerings. Point-to-point integrations enable Prelim to orchestrate and automate KYC, KYB, and AML in real time.

If you skipped FinovateFall last week, you missed out! Fortunately, I’ve compiled a written highlight reel to bring you up to speed.

Demos

With 66 demos on stage, the audience took in a variety of fintech solutions. There was one underlying, enabling technology that fueled the majority of the products and services. That enabling technology, AI, pulsed throughout not just the demos, but the entire event.

There were a wide variety of thought leaders on the Finovate stage last week. Among my favorites were Akeem Shannon, Founder and CEO of Flipstik, who not only brought a massive amount of energy to the stage, but also brought the story of how he launched his product. Perhaps not surprisingly, Akeem’s message centered around the importance of your brand or company’s story. During his presentation, Akeem shared both why crafting a story around your brand is so important, as well as how to build your own compelling story.

As always, I also loved the coverage from the Analyst All Star session, which featured seven-minute presentations from Tiffani Montez, Principal Analyst at EMARKETER; Philip Benton, Senior Analyst- Financial Services at Omdia; and Suraya Randawa, Head of Omnichannel Experience at Curinos.

Tiffani covered the growth of retail media networks in financial services. In addition to Chase Media Services and PayPal’s media arm, Tiffani covered others in the space and explained that financial media networks such as these are superior to retail media networks in that they have cross-merchant data. For his presentation, Philip highlighted the increase in SaaS adoption for banks and explained the implications of leveraging third party technologies. Suraya offered her presentation on how banks can deliver a better customer experience. Notably, she explained that there is no singular, happy path for customers. This variability is perhaps the factor that makes achieving a perfect user experience so difficult.

The conversations

My favorite part of every conference is the networking. This event was no different. I saw plenty of familiar faces and met multiple new ones. Many of my conversations centered around AI–specifically the regulation of AI in financial services.

I spoke with Katie Quilligan, Investor at BankTech Ventures, who sat on a panel discussion I led on creating value in leveraging AI. During our conversation, Katie remarked that all banks need to have a strategy around AI, even if they are not planning on using it directly. She added that banks don’t have the option to ignore the AI revolution, because not only are they falling behind by not leveraging the new technology, but also because their employees are using the technology, regardless of whether or not there is a formal policy around using it.

In a separate conversation with Jim Perry, Senior Strategist at Market Insights, Jim commented that he spoke with a bank recently that said that even though they put up a firewall blocking ChatGPT, one of their bank marketing employees felt they needed to leverage GenAI and was able to get around the firewall by walking across the street to Starbucks on their lunch break so that they could use Starbuck’s wifi to access ChatGPT and generate marketing copy.

The point of both of these conversations makes one thing clear– GenAI has arrived, and at this point ignoring it is not an option.

From hyper-personalization to compliance automation to product management, the digital transformation in retail bears many similarities to the digital transformation taking place in financial services.

In both instances, greater digitization and enabling technologies like AI and machine learning, are empowering businesses to better know and serve their customers, build innovative solutions and services, and secure their operations and their customers’ data against cybercrime.

We caught up with Lohith Kumar Paripati (LinkedIn), Product Lead at Walmart, to talk about the digital transformation in retail. In our extended conversation, we discuss Walmart’s efforts to make ecommerce more effective for merchants, the pain points retail customers are currently facing, and how innovations in AI and an emphasis on personalization are helping enhance the customer experience.

At FinovateSpring earlier this year, you were involved in a discussion on digital transformation in retail. What were some of your key takeaways?

Lohith Kumar Paripati: I was privileged to be part of this event as a panelist and speaker at FinovateSpring, where I discussed how AI and LLMs are revolutionizing retail through improved operational efficiency and personalized customer experiences. My reflections touched on the impact GenAI is having on the industry with its hyper-personalized recommendations as well as robust payment offerings, thus changing the purchasing experience.

What caught my attention was the buzz throughout. FinovateSpring has always been known for its exciting ambiance, and this year’s event was no different. There were live demos from various innovative companies that kept me tuned in while networking opportunities were unrivaled. From my fellow panelists, I heard insights about bridging ecommerce and in-store experiences for Gen Z consumers who want seamless technology-driven relationships.

The event reiterated that Finovate isn’t just about presentations but is also a forum where leaders in the industry converge towards innovation, networking, and learning.

You spearheaded the Walmart Seller Savings Platform. What are its goals? How do you measure success?

Paripati: The Seller Savings Platform has been built around the idea of seller success and offers financial incentives that promote best practices on the marketplace. The platform encourages sellers to offer affordable pricing and delivery speed, as well as maintain product listing quality, which are important drivers of sales growth for them.

Through the platform, we introduced a various programs such as Pro Seller, which gives visible importance and credibility through a badge and also reduces referral fees by 5%. Furthermore, with the Pro Listing program, sellers who have the ability to deliver their items fast and on time, or at low prices, can get an extra 10% discount. For new sellers, the New Seller Savings Program offers up to 25% fee reduction for the first 90 days while providing them with tools like Walmart Fulfillment Services and Sponsored Search ads that help them grow more quickly.

The key aim of this platform is to encourage sellers by offering resources and incentives that contribute towards better business outcomes. Success is measured by seller performance metrics: delivery rates, customer satisfaction levels, and program participation. At its core, however, it is all about helping sellers reach their goals, boost GMV figures, and improve overall marketplace experience for all.

How did your experience at technology companies like Microsoft, Intuit, and Samsung inform the work you did for Walmart?

Paripati: Microsoft, Intuit, and Samsung gave me a strong foundation in product management, strategic thinking, and customer-centric innovation skills that I’ve applied to multiple projects for Walmart. At Intuit, I developed deep expertise in fintech and commerce which has been invaluable in shaping initiatives like the Walmart Seller Savings Platform.

In my tenure with Microsoft, I was able to lead and drive solutions within large organizations structures. That experience empowered me to build comprehensive payments data infrastructure of Walmart sellers. From Samsung, I learned how to drive innovation in big firms so that every fresh thought is effectively integrated into previous systems. This enabled me to introduce more payment/billing options available to Walmart sellers in multiple geographies.

A combination of creativity, tactical planning, and working together are what have shaped my ambition for creating a suite of products and tools for merchants within the walls of Walmart Marketplace.

Were there any interesting challenges on the road to launching the platform?

Paripati: Managing the scale and complexity of Walmart’s vast marketplace was one of the greatest obstacles I faced when building the platform. We had to have a system that can manage personalized saving programs for thousands of sellers and millions of items while at the same time be accurate, transparent, and responsive in real-time, especially during peak times like holidays.

Also important was balancing technical requirements with wider business goals. We had to make sure that platforms like this supported objectives such as increased seller engagement or customer satisfaction without being too expensive. This meant working continuously with other people within finance, operations, and marketing–among others–ensuring that value is delivered at each level.

Another crucial aspect was building adaptability into our architecture. We needed an infrastructure that would not only satisfy today’s needs but also support future initiatives. The key takeaway points were learning about how scalability is important and how cross-functional collaboration can be powerful. Successful launch required seamless coordination between product, engineering, and business teams, resulting in both technological excellence and strategic impact.

You’ve been a Product Manager for technology companies for more than a decade now. How has that job changed over the years?

Paripati: Over the years, my role as a product manager has evolved from being feature-focused to becoming a central driver of business strategy. Early on, my work involved managing specific product features and ensuring their successful execution. As I progressed into leadership, my responsibilities expanded to include not just product development but also aligning those products with overall business objectives, balancing customer needs with strategic goals, and pivoting quickly when necessary to stay ahead in the market.

In the broader industry, product management has shifted from being a function focused on execution to becoming the core of business success. While stakeholder management and collaboration have always been key aspects, today’s emphasis is on creating a product-first culture. Product managers are now at the forefront of driving revenue, building scalable products, and contributing directly to the company’s financial success.

Today’s product managers must be agile, ready to pivot as market demands shift, and play a crucial role in shaping the company’s direction through data-driven insights and a deep understanding of customer needs. This evolution has made the role more dynamic, impactful, and integral to a company’s growth.

What role will enabling technologies – AI, machine learning, automation – play in the digital transformation of retail?

Paripati: AI, machine learning, and automation have altered retail by offering practical use cases that improve operations as well as customer interactions.

For example, AI-powered demand forecasting predicts product trends, thereby optimizing inventory levels and reducing costs. Inside stores, real-time shelf stock monitoring using computer vision driven by AI detects when items are running out, thus alerting attendants to restock before shelves go empty. Automated checkout systems make shopping faster by eliminating traditional checkout lines for frictionless shopping experiences.

Customer experiences are made more personalized by machine learning that result in product recommendations that continuously adjust prices. From the comforts of their homes, customers can virtually have a look at themselves with the help of AI-driven virtual try-ons.

In logistics, robotic automation accelerates order fulfillment, but delivery times are being reduced through automated delivery systems such as drones and autonomous vehicles. These technologies are revolutionizing retail, making it more efficient, agile and consumer-driven.

Where are the biggest pain points for retail consumers and how will this transformation in retail help resolve them?

Paripati: A major concern among retail customers is the disconnection between online and offline experiences. Several retailers find it difficult to provide customers with a seamless experience across all channels, even though that is what they expect today. Moreover, digital transaction fraud rates are very high, and payment security issues loom large as consumers become more concerned about security. Additionally, consumer retention becomes difficult when there are an overwhelming number of product choices due to a highly competitive landscape where retailers vie for customer loyalty.

The digital transformation of the retail industry addresses the problem by merging physical with digital channels to create an omni-channel experience. To achieve greater confidence from buyers, Artificial Intelligence (AI) and automation are used to secure payments while reducing fraud. In order to maintain customer loyalty in an extremely competitive market, retailers use their personalized offers alongside loyalty programs which improve shopping experience.

However, there are many countries where access to even basic goods remains an issue. It is an opportunity and a responsibility that retailers have to enlarge their reach and ensure that underserved consumers get hold of essential products. By using innovative distribution networks, technology can be employed by retailers to bridge this gap, provide more equitable access to goods, and ensure everyone benefits from the digital transformation in the retail industry.

What excites you most about what’s happening in the retail space right now that few people are talking about?

Paripati: Embedded finance has already been discovered as one of the greatest things happening in retail, even if it is not widely recognized. The ability to integrate financial services directly into the retail experience changes everything. On-demand lending at checkout, digital wallets, and buy-now-pay-later options are all instances of embedded finance which alters how consumers work with retailers.

The convergence of AI with physical retail is another area that fascinates me. Advancements in AI are enabling us to introduce new approaches to improving the shopping experience, such as using AI-based tools to customize product displays or optimize store layouts according to customer behavior. This blend of digital and physical is establishing a new frontier for retailers – a world that allows them unlimited space for innovation.

Fresh from FinovateFall in New York, we’ve got a raft of fintech news to share and catch up on. Be sure to check Finovate’s Fintech Rundown all week long for the latest in industry news, announcements, and headlines.

After two days of live demos from more than 65 fintech companies, the attendees of FinovateFall 2024 have made their decisions as to which of these innovators will take home Finovate’s coveted Best of Show awards. Featuring both Finovate newcomers and Finovate veterans alike, the winners of Best of Show for FinovateFall 2024 are listed below.

Bancography for its software tool that lets bankers predicate branch investments on sound market data, not intuition, preventing costly missteps and ensuring optimized investments.

CardLift for its solution that enables companies to build a co-branded browser extension for their partners that automatically finds and switches users’ card-on-file to their partners’ card.

Credit Mountain for its technology that helps organizations grow their businesses by retaining, nurturing, and cross-selling declined borrowers.

Delfi Labs for its technology that creates efficient risk management and hedging strategies in minutes, enabling clients to defend margins, enhance performance, and raise valuation.

Eko Investments for its platform that offers investments via a financial advisor to all clients–and not just the top 1%–starting from $10.

Illuma for its innovations in deepfake detection that enable community financial institutions to keep their members and customers connected with their funds in a convenient and secure manner.

Nest Bank & Efigence for their collaboration, N! Assistant, a virtual AI-powered assistant that revolutionizes finance.

Themis for its solution that enhances compliance efficiency, minimizes regulatory risk, and fosters seamless collaboration, empowering banks and fintechs to focus on growth and innovation in financial services.

Please join us in congratulating our eight, Best of Show-winning companies. Let’s also raise a glass to all of our demoing companies for their innovations in fields ranging from regtech and payments to lending, wealth management, and beyond. We are especially grateful for our attendees and sponsors, whose support continues make our Finovate conferences among the most anticipated events in our industry. We look forward to seeing you again next year!

Notes on methodology:

1. Only audience members NOT associated with demoing companies were eligible to vote. Finovate employees did not vote.

2. Attendees were encouraged to note their favorites during each day. At the end of the last demo, they chose their three favorites.

3. The exact written instructions given to attendees: “Please rate (the companies) on the basis of demo quality and potential impact of the innovation demoed.”

4. The six companies appearing on the highest percentage of submitted ballots were named “Best of Show.”

5. Go here for a list of previous Best of Show winners through 2014. Best of Show winners from our 2015 through 2024 conferences are below:

Today is the day! We are unveiling the 24 winners of the 2024 Finovate Awards. Each winning company, organization, or individual has proved their worth through a rigerous application process, competing with dozens of other highly qualified candidates.

The Finovate Awards honor both established institutions and rising stars that have made significant strides in delivering cutting-edge products and services to the financial sector. Each winner was selected from the a group of finalists that have each demonstrated exceptional contributions to society and developed groundbreaking solutions that have reshaped the fintech landscape.

Without further ado, let’s celebrate the visionaries and innovators who have earned their place in the spotlight as this year’s Finovate Award winners!

In the financial services sector, artificial intelligence (AI) is often heralded as a transformative force capable of revolutionizing everything from customer engagement to fraud detection. However, as the excitement around AI continues to grow, so do the challenges associated with its implementation. According to the latest McKinsey Global Survey on AI, AI adoption is accelerating, with 72% of organizations using AI in at least one business function in 2024, up from 50% in previous years. However, the challenges of achieving tangible business value remain substantial. The survey highlights that organizations need to focus on aligning AI projects with strategic business goals to achieve success (McKinsey, “The State of AI in Early 2024”).

The journey to successful AI implementation in financial services is not about jumping on the latest technology bandwagon; it is about identifying core business challenges, choosing the right AI strategy, and following a robust engagement methodology. Here’s how financial institutions can move beyond the AI hype and achieve real, measurable business value.

1. Start with the business challenge, not the technology

The key to successful AI deployment begins with a comprehensive understanding of the specific business problems that need to be addressed. Too often, organizations are drawn to AI’s potential without a clear roadmap for its application, leading to projects that flounder in development or fail to deliver a return on investment (ROI). McKinsey notes that “the business goal must be paramount,” emphasizing the importance of identifying the most promising business opportunities and working backward to potential AI applications rather than pursuing tech for tech’s sake (McKinsey, “The State of AI in Early 2024”).

For financial institutions, this means asking critical questions: What are the pain points that, if resolved, would yield the most significant benefits? Whether it’s enhancing customer engagement, improving fraud detection, or optimizing operational efficiency, defining the challenge upfront ensures that AI initiatives are grounded in strategic business needs rather than technological fascination.

2. Evaluate: build, buy, or partner

Once the business challenge is identified, the next step is to determine the most effective strategy for deploying AI. This involves a critical decision: whether to build a custom solution, buy an existing one, or partner with an AI expert.

Build: Custom solutions offer the highest degree of specificity and alignment with unique business processes, but they require significant time, resources, and in-house expertise. For institutions with complex, industry-specific needs, building an AI solution may be the most effective approach, but it also carries the highest risk.

Buy: Off-the-shelf solutions provide a faster route to deployment and can be cost-effective for common challenges. However, they may not offer the flexibility needed to adapt to specific business environments. McKinsey’s latest research shows that while 50% of organizations are using off-the-shelf generative AI models, the high performers are increasingly moving toward significant customization or developing proprietary models to meet specific needs (McKinsey, “The State of AI in Early 2024″).

Partner: Partnering with a specialized AI consultancy, like Intelygenz, allows organizations to leverage deep technical expertise and experience while focusing on rapid implementation. A trusted partner can guide institutions through the complexities of AI deployment, ensuring that the solution is tailored to deliver the maximum business impact. This approach combines the benefits of both build and buy strategies, mitigating risks and accelerating time to value.

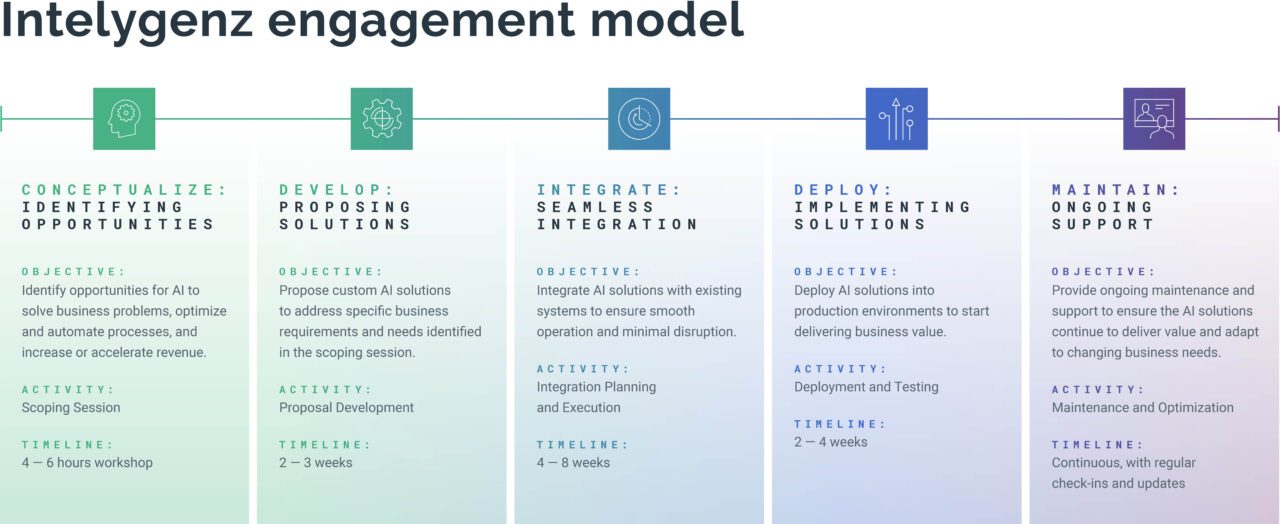

3. Implement with a proven engagement methodology

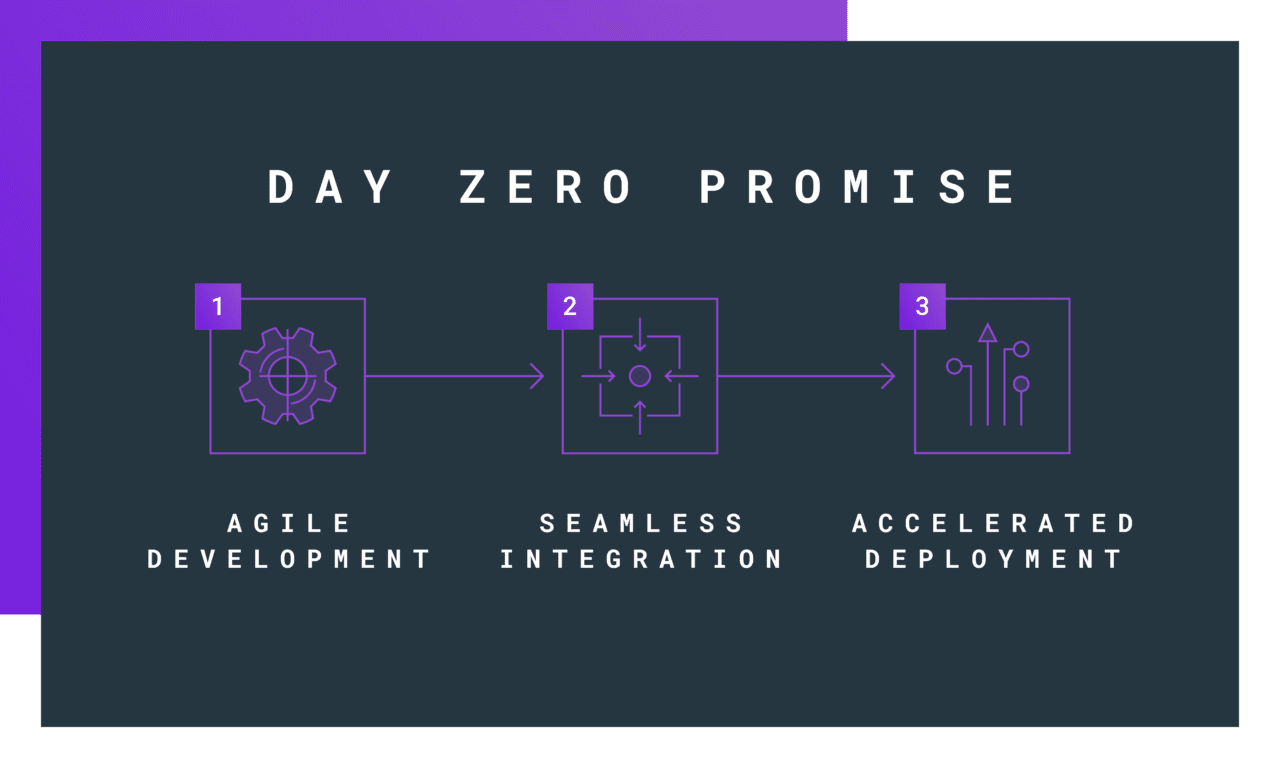

The pathway from AI concept to value realization is rarely linear. To navigate this complexity, financial institutions need a structured, end-to-end engagement methodology that enables rapid development and deployment while ensuring alignment with strategic objectives. Accenture’s “Tech Vision 2024” report emphasizes that adopting an agile, iterative approach to AI deployment enables organizations to see faster returns on investment and adjust quickly to evolving business needs (Accenture, “Tech Vision 2024″).

Intelygenz’s “Day Zero Promise” embodies this approach. Our methodology begins with a rigorous scoping session to align AI projects with strategic business outcomes from the very beginning. This is followed by:

Agile Development: An iterative approach that allows for continuous refinement and adaptation of AI solutions to evolving business needs.

Seamless Integration: Close collaboration with internal IT and business teams ensures that AI solutions integrate smoothly with existing systems and workflows.

Accelerated Deployment: Fast-tracking the time to value by deploying AI solutions in a matter of weeks, not months or years.

By maintaining a relentless focus on delivering measurable ROI, Intelygenz helps financial institutions avoid the common pitfalls of AI implementation and ensures that AI initiatives contribute directly to business growth.

4. Focus on flexibility and cost-efficiency

For many financial institutions, one of the barriers to AI adoption is the perceived cost and complexity. However, AI does not have to be prohibitively expensive or rigid. Intelygenz positions itself as a more flexible and cost-efficient alternative to top-tier AI companies. We deliver high-quality AI solutions without the overhead and rigidity often associated with larger providers, making us an ideal partner for organizations looking to innovate while managing costs.

5. A collaborative approach to AI success

AI projects are not just technical endeavors; they are fundamentally business transformations. A collaborative approach between the AI partner and the organization is crucial for success. At Intelygenz, we engage closely with our clients throughout the entire process, ensuring that every AI solution is not only technically robust but also aligned with the organization’s strategic goals. This partnership approach has led to real-world success stories where financial institutions have transformed AI from a buzzword into a business-critical capability.

Learn More at FinovateFall

For financial services leaders looking to leverage AI effectively, the path to success involves a thoughtful strategy that prioritizes business value over technology for technology’s sake. AtFinovateFall, Chris Brown, President of Intelygenz USA, will delve deeper into these themes during his keynote session, ‘Beyond the Hype: Delivering Real Business Value with AI in Financial Services’. Attendees will learn how to identify the right business challenges, evaluate strategic options for AI deployment, and implement solutions that drive tangible ROI.

Join us on day two of FinovateFall to gain actionable insights and see how Intelygenz’s expert consultancy and implementation services can help your institution harness the true potential of AI.