This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Financial data company Perfios has acquired Clari5 to enhance its fraud prevention and risk management capabilities using Clari5’s real-time financial crime management platform.

Clari5 offers AI-driven fraud detection tools, including customer-looped alerts, identity resolution, trade-based AML, and real-time transaction monitoring across multiple channels.

Perfios anticipates that the acquisition will strengthen its presence in India, the Middle East, North Africa, and Southeast Asia.

Financial data analysis company Perfios has agreed to acquire Clari5 (also known as CustomerXPs). India-based Perfios will use Clari5 to strengthen its own fraud and risk management capabilities. Financial terms of the deal were not disclosed.

Clari5 was founded in 2006 to help protect banks against fraud and money laundering. Among the company’s tools for fighting fraud are a customer-looped alert management service, payments fraud reporting, identity resolution, trade-based anti-money laundering, an inbound scam detection solution, and more. Additionally, Clari5 uses AI-driven analytics and machine learning to improve the detection of fraud patterns. The company monitors transactions in real-time across multiple channels to ensure that financial services organizations can quickly detect and prevent fraud.

“Joining forces with Perfios marks a new chapter of growth and innovation for Clari5,” said Clari5 CEO Rivi Varghese. “With Perfios’ deep expertise in the financial technology ecosystem and our advanced real-time financial crime management platform, we are creating a powerful synergy to redefine fraud prevention, risk intelligence, and AML compliance at scale. This partnership enables us to expand our reach, accelerate product innovation, and strengthen our ability to help financial institutions combat evolving financial crime with unmatched speed and precision. Perfios’ scale, global presence, and stability position us to serve the largest banks worldwide, enabling us to deliver impactful solutions to financial institutions of all sizes and complexities.”

Founded in 2008, Perfios builds customized solutions for financial services firms to make data-based, real-time decisions in lending, wealth management, embedded finance, insurance, and KYC. The company serves over 1,000 lenders in India, including each of the top 10 banks.

Perfios anticipates that adding Clari5 will help it build its leadership in the financial sector in India. The company also plans to use the move to strengthen its presence across its key geographies, including the Middle East, North Africa (MENA), and Southeast Asia (SEA).

“The acquisition of Clari5, a leader in EFRM and AML, marks a significant milestone in our journey to build the most comprehensive fraud and risk management ecosystem,” said Perfios CEO Sabyasachi Goswami. “Clari5’s real-time financial crime management platform, trusted by marquee financial institutions worldwide, perfectly complements Perfios’ mission to deliver secure, scalable, and tech-first solutions. Together, we are set to redefine fraud prevention, risk intelligence, and AML compliance, empowering financial institutions to stay ahead of evolving threats while powering financial security to billions across the globe.”

When regulatory changes are a moving target, it can be difficult for financial services companies to keep up. In 2025, several key regulatory updates across Europe will demand attention, from changes to MiFID II and PSD3 to new directives on anti-money laundering (AML) and artificial intelligence (AI). These shifts vary in scope by country, but all require companies to adapt to ensure compliance.

While many of these updates are an inconvenience and require organizations to implement new processes and workflows, they will ultimately improve transparency, security, innovation, and enhance the end user experience. Financial services companies that stay ahead of the curve will be better positioned to meet these challenges.

For deeper insights, FinovateEurope, which is taking place in London on February 25 and 26 (register today and save!), will host a diverse group of experts who will explore the region’s regulatory shifts in detail, offering valuable guidance on how firms can best prepare for 2025. Below, we’ve highlighted some of the most important changes that are likely to impact financial services organizations this year.

ESG compliance

The Sustainable Finance Disclosure Regulation (SFDR), which was introduced in 2021, required firms to complete more detailed and standardized reporting on sustainability practices. As a result, many needed to invest in systems to track and report ESG metrics more accurately and transparently. In 2025, the European Commission and European Supervisory Authorities (ESAs) is expected to update the legislation to improve definitions, simplify disclosures, add more mandatory disclosures, and more.

Additionally, in 2025, the Corporate Sustainability Reporting Directive (CSRD) is expected to see a significant expansion to its scope. More companies will be required to report under the CSRD, firms will be required to disclose detailed information about their sustainability impacts, the reporting measure will need to be fully integrated into a company’s business strategy and decision-making processes, and more.

While these shifts may be challenging, many organizations will likely benefit from improving their ESG transparency because it will help attract investors who prioritize sustainability and may improve their firm’s reputation.

Digital Operational Resilience Act (DORA)

The Digital Operational Resilience Act (DORA) went into effect in January of 2023 and began to require compliance last month. DORA aims to enhance the IT security of financial services companies including banks, insurance companies, and investment firms. The regulation requires firms to regularly test their systems, create contingency plans, and ensure that their third-party providers are also in compliance with security standards. The three European Supervisory Authorities– the European Banking Authority (EBA), the European Insurance and Occupational Pensions Authority (EIOPA) and the European Securities and Markets Authority (ESMA)– anticipate that DORA will reduce the risk of systemic disruptions and improve financial stability.

EU AI Act

Established in 2024, the European AI Office is implementing the EU AI Act to create regulatory framework for artificial intelligence in Europe. Ultimately, the regulation seeks to ensure that AI applications are transparent, accountable, and ethical. The first requirements under the EU AI Act went into effect earlier this month to ban the use of AI systems that involve prohibited AI practices. There are eight categories of prohibited practices, as law firm DLA Piper details in the graphic below.

European Data Governance Act (DGA)

The European Data Governance Act is designed to enhance consumer trust in voluntary data sharing to help businesses innovate and grow. The act establishes a framework for data sharing and sets standards for data altruism and data intermediaries.

In 2025, the primary update to the EU DGA is the upcoming enforcement of the Data Act, which will impact how businesses manage and share data and their personal information, by specifying data access and usage. The new legislation will take effect in September of 2025.

AML compliance

Anti-money laundering (AML) regulations are set to become even stricter with the introduction of new directives in 2025. Specifically, the EU AML Package, which is launching this year, establishes a new supervisory authority called the Anti-Money Laundering Authority (AMLA). Based in Frankfurt, the AMLA will implement stricter compliance measures for financial institutions, especially high-risk firms, to help combat money laundering and terrorist financing across the EU.

While complying with the AML regulations will require firms to rework their existing strategy and perhaps create new systems, it will help reduce financial crimes, protect firms from reputational damage, and reduce regulatory penalties.

Payment Services Directive 3

Payment Services Directive 3 (PSD3) is the third iteration of the EU’s Payment Services Directive. Changes to the directive coming in 2025 are expected to further enhance open banking capabilities and offer third-party providers greater access to consumer financial data while improving security and user consent mechanisms. The new iteration will also further protect consumers by providing clearer guidelines on payment methods, transaction rules, and dispute resolution processes. The updated standards are expected to increase the speed, transparency, and security of payments, while providing customers with a more seamless and trustworthy payment experience.

Crypto regulation and the MiCA framework

2025 will bring the full implementation of the Markets in Crypto-Assets (MiCA) framework, which will introduce regulation for cryptocurrencies and digital assets across the European Union. Financial services companies that engage with crypto will need to comply with new licensing and operational requirements.

Originally drafted and proposed by the European Commission in September 2020, MiCA aims to provide clarity for businesses and investors by establishing clear rules around the trading, issuing, and holding of crypto assets. This transparency is expected to provide stability and foster trust in the crypto market.

Anti-Tax Avoidance Directive (ATAD III)

The Anti-Tax Avoidance Directive (ATAD III), which aims to reduce tax avoidance by implementing stricter rules to combat aggressive tax planning and ensure that companies pay taxes, is slated to go into effect in 2025. The new directive requires financial services companies to adjust to their tax structures and increase their scrutiny of cross-border transactions. Ultimately, ATAD III should help promote fairness in the EU’s tax system by addressing loopholes used for tax avoidance.

Engagement Banking company Backbase has announced a strategic partnership with financial intelligence solutions provider Feedzai.

The partnership will integrated Feedzai’s Digital Trust solutions with Backbase’s Engagement Banking Platform.

Backbase most recently demoed its technology on the Finovate stage at FinovateFall 2021. Feedzai made its Finovate debut at FinovateEurope 2014 in London.

A newly announced strategic partnership between Backbase and Feedzai aims to bring advanced financial crime prevention technology to engagement banking. The integration of Feedzai’s Digital Trust solutions with Backbase’s Engagement Banking Platform will empower financial institutions to fight fraud more effectively while preserving the customer experience.

Feedzai’s Digital Trust platform analyzes user behavior, device health, and potential threats in real-time. The cloud-based solution operates in the background, enabling financial institutions, financial services organizations, and fintechs to detect and counter online identity impersonation and manipulation attacks, while allowing legitimate users to conduct their activities unimpeded. Feedzai’s Digital Trust is effective against account takeover (ATO) attacks as well as new account fraud attempts during onboarding. It combines behavioral biometrics, behavioral analytics, advanced malware detection, and network and device assessment to provide active and preemptive defense against threats. The integration with Backbase’s engagement banking platform will provide banks with real-time, AI-powered, proactive fraud prevention, plus lower operational costs thanks to AI-powered risk assessment that minimizes false positives.

“By combining Backbase’s engagement banking expertise with Feedzai’s advanced security capabilities, we’re giving financial institutions the complete package — superior customer experience and intelligent fraud prevention in one integrated platform,” Backbase CEO and Founder Jouk Pleiter said. “Together, we’re setting a new standard for how banks can build trusted digital relationships with their customers.”

Headquartered in San Mateo, California, Feedzai offers technology that leverages AI to help businesses fight fraud and financial crime. The company’s RiskOps platform uses machine learning and Big Data to detect and defend the world’s largest banks, payment providers, and merchants from malicious online actors. Founded in 2011 and now reaching 900 million people in 190 countries with its technology, Feedzai began 2025 by announcing a partnership with Credibanco to help the Colombian payment processing company strengthen its defenses against fraud.

“As the financial services industry evolves, security can no longer be an afterthought — it must be woven into the very fabric of the customer journey,” Feedzai CEO and Co-Founder Nuno Sebastiao said. “By partnering with Backbase, we’re empowering financial institutions to deliver a unified, seamless journey that not only protects customers from fraud but also ensures they feel valued, understood, and safe.”

Backbase has been a Finovate alum since 2009. The company has won Finovate’s Best of Show award four times, including back-to-back wins at FinovateEurope in 2017 and 2018. Backbase’s Engagement Banking Platform is a composable solution that empowers banks to accelerate their digital transformations by progressively modernizing each step of the customer journey, including onboarding, servicing, lending, and investing.

Backbase’s partnership news comes a few weeks after it announced it was teaming up with Alliant Credit Union, a digital-only financial institution with $20 billion in assets and more than 900,000 members. The company also recently partnered with Nordic digital transformation consultancy Knowit. Founded in 2003, Backbase is headquartered in Amsterdam.

The week begins with news of investment in insurtech, financial wellness, and risk management. We are also seeing a number of new partnerships in payments and fraud prevention. Check back here all week long at Finovate’s Fintech Rundown for updates on the latest fintech headlines.

Digital banking solutions provider Apiture and digital solutions company Omnicommanderteam up to help banks and credit unions better communicate with their customers and members.

Gold Coast Federal Credit Union enlistsTyfone to accelerate digital transformation.

Crypto / Defi

Ripplepartners with currency exchange provider Unicâmbio to bring crypto-enabled cross-border payments to Portugal.

Insurtech

Australian digital-first insurance broking firm UpCoversecures $19 million in Series A funding.

Via its brand Polly, European digital insurance broker CLARKlaunches its first fully digital underwriting solution in the UK.

Financial software and technology company CSI partners with Mitek Systems to launch its proprietary check fraud detection solution for NuPoint customers.

Backbase and Feedzaiteam up to integrate advanced security capabilities into Backbase’s Engagement Banking Platform.

Regtech and compliance

Sardine AIraises $70 million to make fraud and compliance teams more productive.

Investing / wealth management

Halal investment research platform Musaffalaunches new equity crowdfunding round.

BrightwaveintegratesQuartr’s global database of first-party information from public companies with its document analysis capabilities.

Datalignsecures $9 million Seed funding to accelerate AI-powered financial advisory solutions.

Lending and credit

FinastralaunchesAssist.AI, an AI-powered assistant to enhance the trade finance operations within its Trade Innovation solution.

Spreedly and Trustly have partnered to offer Spreedly’s merchant clients pay-by-bank capabilities through its Open Payments platform.

Adding the new payment option will help merchants enhance payment flexibility, conversion rates, and consumer insights.

Pay-by-bank adoption is growing in 2025 due to lower fees and faster settlement times for merchants. To encourage its use, some merchants offer monetary incentives at checkout.

Open payments platform Spreedly has teamed up with pay-by-bank expert Trustly this week. The two are collaborating to offer Spreedly’s merchant clients access to Trustly’s pay-by-bank capabilities.

Under the partnership, Trustly will take charge of the pay-by-bank tools in Spreedly’s Open Payments platform. Spreedly anticipates that merchants who use the new pay-by-bank tools will see improved conversion rates without having to overhaul their existing payments infrastructure. The company also envisions that the new capabilities will empower merchants with more payment flexibility and further insight into consumer habits.

“Our collaboration with Spreedly represents a significant step towards a unified payments experience becoming the industry standard,” said Trustly VP of Enterprise Growth Ross McFerrin. “By integrating Trustly’s pay-by-bank offerings with Spreedly’s orchestration platform, we’re providing merchants an all-in-one solution that allows them to choose the best payment methods to offer their customers while simplifying the complexity of payment integrations.”

Sweden-based Trustly’s pay-by-bank network currently processes over $42 billion in transaction volume each year. The company offers Trustly Pay for open banking payments and Trustly Payouts for payouts. It also provides open data tools like Trustly Connect for data retrieval, Trustly ID for identity verification, and Trustly Insights for real-time underwriting decisions. In 2018, Nordic Capital bought Trustly for an undisclosed amount, and since then, Trustly has acquired three companies of its own, including SlimPay, Ecospend, and PayWithMyBank. The company anticipates that partnering with North Carolina-based Spreedly will increase its market reach in the U.S.

Spreedly was founded in 2007 to help merchants build their payments stack on a single platform. The company’s payment orchestration stack offers merchants more than 140 gateway connections of more than 40 payment methods. Spreedly also offers fraud prevention, payment optimization tools, and more.

“Spreedly has long demonstrated its ability to securely vault and orchestrate payments across card networks, and by partnering with Trustly, we are excited to extend these benefits by embedding pay-by-bank flows directly into our Open Payments platform,” said Spreedly VP of Global Partnerships and Business Development Rose Francois. “Together, we’ll enhance payment flexibility and security, empowering merchants to meet the growing demand for efficient, data-driven payment solutions, while driving stronger outcomes for the broader payments ecosystem.”

Pay-by-bank has been cited by analysts as one of the top trends to watch in 2025 as consumer and merchant adoption continues to grow. Merchants often favor pay-by-bank because of the lower fees and faster settlement times. And while consumers may be hesitant to ditch their credit cards in favor of pay-by-bank, some merchants offer a monetary incentive at the point of purchase to promote using pay-by-bank.

This week’s edition of Finovate Global looks at recent fintech news and headlines from Australia.

Digital private equity manager Moonfare goes live in Australia

Eligible investors in Australia stand to benefit from the arrival of digital private equity investing platform Moonfare. The Berlin-based company announced that it is bringing its wealth management technology to what is now its 23rd country. Moonfare Asia Pacific head Adam Banks, who joined Moonfare in October, noted that the firm’s APAC investor relations team is already “in active discussions with potential clients” in Australia.

Founded in 2016, Moonfare enables eligible investors to access a selection of curated funds from managers such as KKR, EQT, and the Carlyle Group. The company’s proprietary portfolio investments provide diversification and low minimums across a range of strategies, including buyout, growth equity, venture, and infrastructure. Investors on the platform can also participate in secondaries, private credit, and co-investments.

“There is clearly a growing appetite for private equity investing in Australia,” Moonfare Founder and Co-CEO Steffen Pauls said. “But so far access has been limited, especially for people wanting exposure to non-domestic managers and strategies. Moonfare’s digital private equity platform plans to fill that gap by providing seamless access to globally leading top-quartile managers.”

Moonfare boasts more than €3.3 billion ($3.4 billion) in assets under management and access to more than 110 funds. The company began the year with the appointment of Heike Hövekamp as Chief Legal & Compliance Officer. Hövekamp joins Moonfare from Société Générale, where she was Head of Compliance.

Australian regtech Nuj raises $4 million in seed funding

Is there any debate that 2025 is shaping up to be the year of regtech? The fact that regtech increasingly seems to provide fertile ground for new fintech startups may be yet another indication of the growing importance of this subsector.

Australia’s Nuj is another fintech startup that is taking advantage of interest in regtech. The company announced that it has raised $4 million in equity and debt financing to develop its superannuation data platform. A superannuation is Australia’s pension program, created to benefit of employees. They are similar in many respects to an individual retirement account (IRA) or a 401(k) in the US.

Mimecast Co-Founder Peter Bauer led a $2 million seed round as part of an overall $4 million equity and debt package. He praised Nuj’s “powerful data platform that addresses an expensive challenge across the super industry — one of staying ahead in compliance with regulations.” Founded in 2020 by Matthew McKenzie, Nuj is a data platform and insights engine that sits between superannuation funds and the regulator. The technology provides real-time insights to superannuation trustees and executives, enabling them to better manage their risk programs. The company’s platform is used by institutions such as MUFG, AMP, and Equity Trustees.

The investment in Nuj comes as regulatory reporting requirements and calls for increased transparency for superannuation funds are growing. McKenzie noted that funding will help “fuel (the platform’s) capabilities for faster data processing and sharper insights, empowering funds to make informed decisions, and driving better financial outcomes.”

Headquartered in Sydney, Nuj was founded in 2020.

Ozone API and ProductCloud team up to help Australian firms meet open banking regulations

A new partnership between Ozone API and ProductCloud will help companies in Australia comply with Open Banking API regulations, specifically Consumer Data Right legislation. The partnership will provide Australian companies with a technology platform that enables them to quickly and securely deliver open APIs aligned to the most recent version of the Australian Consumer Data Standard.

“Our platform is already helping banks and financial institutions around the world to deliver standards compliant with open banking APIs, including in line with the CDR standard,” Ozone API Co-founder and CEO Huw Davies said. “We’re really excited to combine our global expertise in open finance with ProductCloud’s innovative product management platform. Together, our solutions remove the complexity of achieving and maintaining CDR compliance, allowing organizations to focus on their core business.”

Founded in 2017 and headquartered in London, Ozone API is a leading standards-based platform designed to take the complexity out of open banking and help companies meet regulatory and commercial requirements for open APIs. In addition to its partnership with ProductCloud, Ozone API also recently announced its collaboration with FinovateEurope 2024 alum ShareID to, in the words of ShareID CEO and Co-founder Sara Sebti, “enhance the Open Banking ecosystem” and, as Ozone API GM for Europe James Bushby put it, “strengthen trust in open finance.”

Melbourne-based ProductCloud offers a cloud-based, SaaS solution that streamlines product information management for financial institutions. Serving banks, neobanks, mutuals, and non-bank lenders, ProductCloud provides a single tool for both Open Banking Product Reference Data and Design and Distribution Obligation compliance. The company was founded in 2020.

“Since launching ProductCloud back when CDR kicked off, we had our sights on being the go-to Product Information Management and CDR Compliance platform for financial institution product managers,” ProductCloud Co-founder and CEO Mark Evans said. “Partnering with Ozone API is an exciting development because they have also been a pioneer in Open Finance. Collaborating with our respective SaaS platforms and out-of-the-box APIs will provide a unique offering for rapid and cost-effective open banking compliance.”

Here is our look at fintech innovation around the world.

Central and Eastern Europe

Romanian crowdfunding service provider, Venevo, partnered with regtech solutions hub iDenfy.

Lithuanian fintech ArcaPay agreed to be acquired by UK-based financial services provider Ebury.

International money movement firm TerraPay partnered with airport retailer Dubai Duty Free.

Central and Southern Asia

India-based payments and API banking firm, Cashfree Payments, raised $53 million in funding at a valuation of $700 million.

Egyptian fintech Halan Microfinance Bank expanded into Pakistan with a pledge to invest $10 million in 2025.

Indian fintech Cred became the first fintech platform to provide access to India’s central bank digital currency project.

Latin America and the Caribbean

Payment orchestration provider Yuno to launchMastercard Payment Passkey Service across Latin America.

Kuady teamed up with BridgerPay to enhance payment solutions throughout Latin America.

Latin American ecommerce company MercadoLibre now offers transactions using its payment processors in Argentina via Brazil’s instant payment system, Pix.

Its 2025, and while the concept of embedded finance is not new, it continues to evolve, offering fresh opportunities for growth. Embedded finance is making it easier for consumers and businesses to interact with financial services companies by helping to streamline payments, offer in-app credit, and provide insurance offerings within apps. Ultimately, embedded finance is creating convenience and efficiency for both end users and the financial institutions themselves. However, as this sector matures, so too do the complexities surrounding competition, partnerships, and regulatory compliance.

At this year’s FinovateEurope event, taking place February 25 through 26 in London (book now to save!), we’re bringing in experts to discuss a wide range of pressing topics impacting banks and fintechs across the globe. And since embedded finance is still high on the list of hot trends this year, we are featuring two sessions dedicated to exploring opportunities in the space.

In our executive briefing titled, “How financial institutions can capture the huge opportunity of embedded finance & embedded banking in both retail & commercial banking,” the panel will look at opportunities for banks to expand their distribution footprint, the role of non-banks, competition, risk, and more. Panelists include:

Rashee Pandey, Associate Director of Membership and Growth at Innovate Finance

Sadeque Ahmed, Executive Director of Product Management at J.P. Morgan

Vivien Cheung, Head of Financial Partnerships EMEA at Airwallex

Andrew Crocombe, Head of Embedded Banking Propositions at ClearBank

Jose Luis Navarro, Head of Open Banking Strategy at BBVA

Jakob Pethick, Chief Commercial Officer at YouLend

We’ll also host Mbanq Co-Founder Vladimir Lounegov, as he delivers a special address titled, “Want to print money? How embedded finance turns brands into banks.” Lounegov will share how embedded finance empowers non-financial brands to generate new revenue streams, build customer loyalty, and gain a competitive edge by integrating financial services seamlessly into their products or services.

Don’t miss these sessions, and others, at FinovateEurope. Whether you’re a bank, fintech, analyst, or VC, this show will be your opportunity to learn from top thought leaders in the space and shape your 2025 strategy. Register today and be part of the action!

Personetics unveiled a number of new features for its AI-powered flagship solution, Personetics Engage, this week.

The new features will help financial institutions build personalized digital experiences that encourage their customers to better manage their financial lives.

Headquartered in New York, Personetics made its Finovate debut at FinovateEurope 2016 in London.

Personeticsannounced a range of new features for its AI-powered flagship solution, Personetics Engage, this week. The new features are designed to help financial institutions create personalized digital experiences for their customers that empower and motivate them to better manage their finances.

“Financial institutions today need solutions that go beyond basic personalization and static insights,” Personetics Chief Product Officer Ron Agam said. “These new capabilities advance our mission of providing banks with a platform that dynamically responds to their customers’ changing financial needs, making them smarter about their money and motivated to act.”

The new features include an Activity Tracker that customers can use to see their spending, income, and cash flow for up to 12 months. This interactive overview gives customers enhanced visibility into their financial status, helping them track and manage their finances across multiple accounts from a single location. Personetics also introduced a Financial Recap feature that provides customers with an Instagram-like summary of their spending over the past seven days. The feature not only lists top merchants and categories of spending but also gives users a seven-day forecast of their projected cash balance and activities. Financial Recap helps contextualize spending for customers, making it easy to spot spending trends.

Personetics Engage will also now be equipped with Bank and User Categorization Control. This enables banks to manage transaction categorization mapping to improve accuracy. Institutions can review, recategorize, and rename categories — as well as create their own unique category designations. Customers also have the ability to recategorize transactions, increasing personalization and providing valuable feedback for their bank.

Personetics has also introduced a new level of interactive engagement between banks and customers courtesy of Custom User Journeys. This feature enables banks to build targeted, dynamic flows that collect customer preferences and adapt in real-time. These dynamic flows provide personalized financial guidance, as well as product recommendations that are based on direct customer input. To enhance engagement, the system uses customizable and interactive insights, questionnaires, and teasers..

“With these innovations, banks can move beyond static insights and truly monetize financial wellness,” Personetics VP of Strategy and Business Development Dorel Blitz noted on the company’s LinkedIn page, “inspiring customers to take action while driving meaningful business value.”

Personetics made its Finovate debut at FinovateEurope 2016 in London. Founded in 2011 and headquartered in New York, the company provides money management and personal financial management (PFM) solutions for banks and other financial institutions. Personetics’ technology leverages AI and its financial-data-driven platform to help FIs enhance customer engagement and boost revenue. Today, Personetics serves more than 135 million bank customers around the world, and includes six of the top 12 banks in North America and Europe as customers.

A look at the companies demoing at FinovateEurope in London on February 25. Register today using this link and save 20%.

Bitpowr Technologies

Through Bitpowr Technologies’latest products, fintechs and other companies can offer embedded stablecoin banking, payments, digital wallets, and card products in a safe, secure, and compliant way.

Features

Issue and enable stablecoin digital wallets to store and secure stablecoins

Process and receive global payments using stablecoins

Issue stablecoin-backed cards to users

Who’s it for?

Fintechs, neobanks, payment providers, and businesses.

ID-Pal

ID-Pal uses 100% AI-powered technology for real-time identity verification and AML screening, ensuring seamless customer onboarding, compliance, and zero access to customer data.

Features

Provides built-in AI document fraud detection

Delivers global coverage and streamlined AML compliance

Offers seamless integration options and full customization

Who’s it for?

Banks, neobanks, community banks, credit unions, payments providers, insurance companies, asset management companies, and financial institutions.

MDOTM Ltd

Sphere, MDOTM Ltd’s investment platform, leverages AI to deliver AI-driven investment insights, portfolio rebalancing at scale, and automated portfolio commentaries to institutional investors globally.

Features

Creates AI-driven investment insights

Provides portfolio rebalancing at scale

Uses GenAI for portfolio commentaries and reporting

Who’s it for?

Investment professionals and decision makers from banks, insurance companies, family offices, and asset and wealth management companies.

Moonjelly

Moonjelly is an enterprise-ready GenAI platform that retrieves information, derives insights, and completes tasks to increase day-to-day efficiency with complete transparency.

Features

Unlocks advanced insights with AI on trustworthy data across industries

Executes tasks in seconds to improve efficiency

Creates dashboards to track ROI and enterprise compliance

Who’s it for?

Small-to-medium-sized financial institutions.

PayIP

PayIP’s AI-powered billing platform optimizes banks’ payment network billing and interchange, providing fast, accurate alerts and insights to uncover immediate cost savings and revenue opportunities.

Features

Recovers and optimizes payment network fees and interchange for banks

Empowers banks to understand their payment network billing and interchange

Benchmarks and analyzes network billing

Who’s it for?

Banks, credit unions, fintechs and payment providers paying fees to payment networks and/or earning or paying interchange.

Worldpay plans to acquire AI-driven fraud detection company Ravelin.

The acquisition will help Worldpay enhance its e-commerce offerings by adding fraud prevention technology and improve business clients’ authorization rates.

Ravelin’s cloud-based platform helps merchants combat online fraud, secure accounts, and improve payment authorization rates through partnerships with data providers like Ekata and Ethoca.

Payments and banking services company Worldpayannounced plans today to acquire fraud detection company Ravelin. Financial terms of the deal were not disclosed. The acquisition is expected to close later this quarter.

“Our acquisition of Ravelin aligns with our strategy to invest in innovation and AI technology, enhancing the value we provide customers and accelerating our e-commerce growth,” said Worldpay CEO Charles Drucker. “In today’s online world, equipping merchants with next-generation AI-powered fraud prevention products is vital, and we believe Ravelin’s technology and expertise will significantly enhance Worldpay’s overall value proposition to the marketplace. We look forward to partnering with Ravelin’s leadership and their talented team to help our customers address their most complex challenges.”

Ohio-based Worldpay anticipates that buying Ravelin will complement and enhance its existing portfolio of solutions. The company will also leverage Ravelin’s cloud-based AI platform to help its merchant clients improve authorization rates.

Worldpay was founded in 1971 and enables merchants of all sizes to grow faster and protect their businesses as fraud activity accelerates globally. The company offers processing solutions that allow businesses to take, make, and manage a variety of payments, including online, in-person, and embedded payments. The company processes over 50 billion transactions each year across 146 countries and 135 currencies.

Fraud prevention and payments optimization company Ravelin helps ecommerce merchants combat online payments fraud, implement account security, accept returns while blocking fraudsters, and set limits on promotional redemptions. The company also performs 3D Secure identification. Ravelin works with third parties including Ekata, Ethoca, and Chargebacks 911 to bring a wealth of data and disputes, and can integrate with other external data sources, as well.

“Ravelin is thrilled to be joining Worldpay, a true global leader in the payments industry,” said Ravelin Co-Founder and CEO Martin Sweeney. “Worldpay’s scale and reach, including processing approximately $2.5 trillion in payments volume and more than 50 billion transactions in 2024, will be an immense asset as we accelerate Ravelin’s momentum and advance our mission to eradicate fraud from the internet. Together, we will be able to deliver innovation at scale, driving the adoption of our industry-leading fraud solutions to customers as they respond to increasingly sophisticated threats and rising fraud-related costs.”

In a world where consumers are demanding faster payments, fraud is taking place at a faster rate, as well. The methods of fraud are also evolving as AI tools become more advanced, making fraud more sophisticated and harder to detect. By integrating Ravelin’s fraud prevention tools with its payment processing services, Worldpay will provide businesses with the ability to protect themselves against fast-moving fraud.

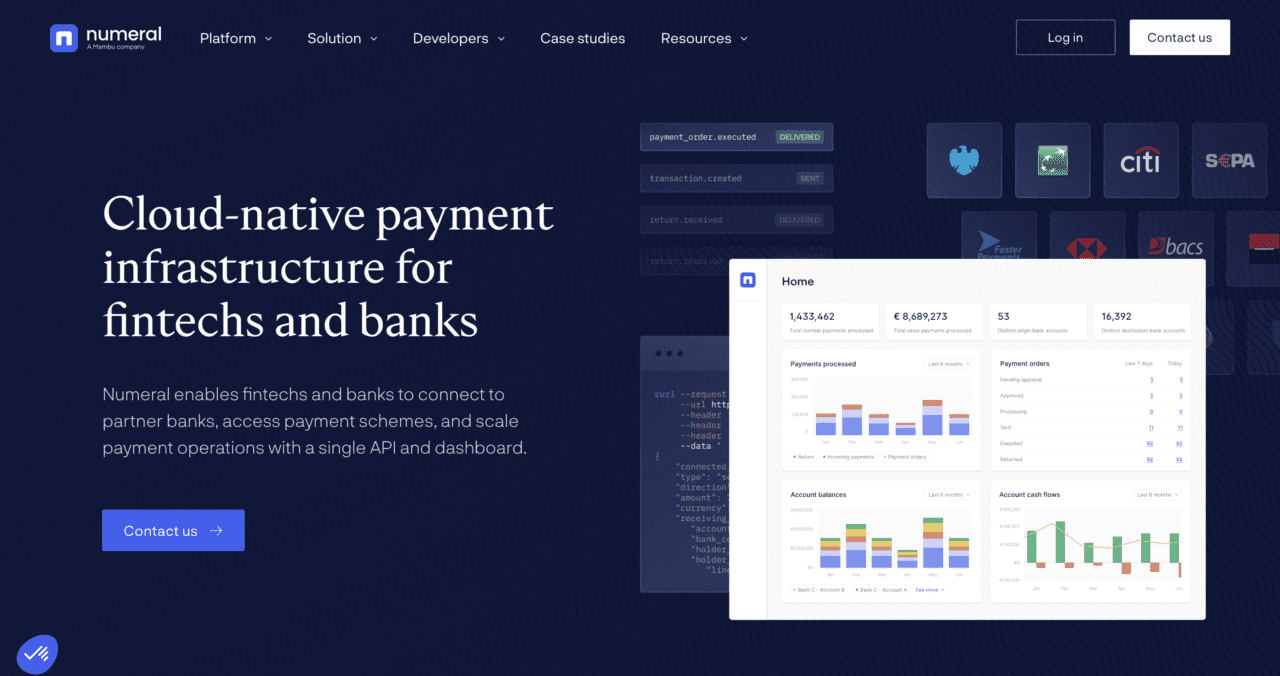

Payment technology provider for financial institutions, Numeral, unveiled its fully managed Verification of Payee (VOP) solution this week.

The new offering will help financial institutions in the European Union meet new VOP requirements months ahead of the regulator’s October 9 deadline.

Headquartered in France, Numeral made its Finovate debut at FinovateEurope 2023. The company was acquired by fellow Finovate alum Mambu in December.

Numeral, a payment technology provider for financial institutions, launched its fully managed Verification of Payee (VOP) solution this week. The technology will enable banks and other financial institutions to comply with the European Union’s VOP policy by October 9, the deadline set by regulators.

“At Numeral, our mission is to provide financial institutions with a future-proof and compliant payments infrastructure,” Numeral CEO and Co-founder Édouard Mandon said. “Given our fully managed payments hub offering, enabling our customers to comply with VOP aligns perfectly with our commitment to streamline payments infrastructures and operations. Our fully managed approach ensures they become and remain compliant without having to navigate the complexities of scheme adherence and ongoing operations.”

Numeral’s solution arrives as Europe searches for ways to fight payment fraud — especially authorized push payment (APP) fraud — and enhance payment security at a time when instant payments are becoming increasingly popular and available. To this end, new regulations for Verification of Payee (VOP) mandate that payment service providers (PSPs) give payers verification of payee details before making credit transfers.

Numeral’s VOP offering provides a managed approach that deals with all the regulatory and technical requirements involved in sending and responding to VOP requests. The solution supports the payment process from VOP scheme adherence to go-live readiness and enables account data synchronization through SFTP, API, manual upload, as well as real-time API connectivity. Numeral’s VOP technology also leverages a configurable matching algorithm that helps firms balance risk management and a seamless user experience. The company has also produced a publication, The Ultimate Guide to Verification of Payee, to help financial institutions better understand the VOP scheme.

“Account pre-validation and domestic verification solutions are extremely valuable for their intended use cases, but aren’t required to achieve VOP compliance,” Numeral Head of Product Marketing Matthieu Blandineau said. “The European Payments Council’s VOP scheme ensures interoperability across PSPs and countries by default, and our solution helps financial institutions comply with the scheme requirements on time, with minimal resources.”

Headquartered in Paris, France, Numeral made its Finovate debut at FinovateEurope 2023, where it demonstrated its API platform that enhances payment operations by automating bank payment processing. Specifically, Numeral showed how its platform automatically sends, receives, and reconciles SEPA payments and manages payment errors via SEPA R transactions.

Founded in 2021, Numeral was acquired by fellow Finovate alum Mambu in December 2024.

What makes an address “special”? This year at FinovateEurope 2025, the designation is going to speakers addressing an especially wide range of topics — from AI to quantum computing. Some of the presentations we’re highlighting today will be on the mainstage at FinovateEurope. Others will be offered as part of our focused tracks examining topics in payments, customer experience, AI, lending, and banking risk and regulation. All of them promise to be insightful discussions on key topics impacting fintech and financial services today.

Our slate of speakers for FinovateEurope is growing by the day. Visit our FinovateEurope 2025 hub for the latest updates on who’s speaking and when.

Mainframe modernization: the journey to agile digital services in 2025

Featuring Paul Holland (LinkedIn), CTO, Astadia: An Amdocs Company, this special address looks at how tools such as Generative AI (GenAI) can help accelerate digital transformation to unlock even further modernization. Holland will also lead a conversation on how financial institutions can complement existing capabilities to successfully modernize mainframe applications at scale. Tuesday, 25 February, 10:05 am.

An Amdocs company, Astadia is an industry-leading mainframe migration and modernization firm. Astadia’s core competencies include cloud migration, refactoring, replatforming, DevOps, and managed IT services. The company has conducted more than 300 successful migrations with world-class organizations.

Countdown to Q-Day: Why Banks Must Act on Post-Quantum Authentication Now

Featuring Petr Dvořák (LinkedIn), Founder and CEO, Wultra, this special address will examine the evolution of quatum computing and the potential challenges the technology will bring to digital banking. Dvořák will discuss the migration to post-quantum authentication (PQA) and the importance of transitioning to quantum-resistant authentication before “Q-Day” — when quantum computers are powerful enough to break contemporary cryptography. Tuesday, 25 February, 3pm.

Founded in 2014 and headquartered in Prague, Wultra helps banks and fintech brands build secure digital applications. The company offers modern, compliant authentication solutions that deliver security, easy access to financial services, and straightforward deployment.

Building Interactive Data Applications with Plotly: How AI Enhances the Delivery and Usage of Data Apps

Featuring Andy Wisbey (LinkedIn), European Sales Director, Plotly, this special address is part of FinovateEurope 2025’s Artificial Intelligence Track. Wisbey will lead a hands-on session that will demonstrate how to leverage Plotly’s advanced visualization capabilities to create an interactive data application that transforms complex financial data into actionable insights. Wednesday, 26 February, 10:50am

A Bronze sponsor of FinovateEurope 2025, Plotly is a leading provider of open-source graphing libraries and enterprise-grade analytics solutions. The company’s flagship solution, Dash Enterprise, enables organizations to build scalable and interactive data apps that drive impact decision-making.

Also providing special addresses at FinovateEurope this year are:

Pedro Andrade, Key Account Director, ORACLE MySQL

Vladimir Lounegov, Co-Founder, Mbanq

Waheed Mahmood, BFSI Lead, Rackspace

Be sure to check out the Finovate blog as more speakers for FinovateEurope are confirmed. And if you haven’t picked up your ticket yet, there’s no time like the present! Visit our FinovateEurope hub today and save your seat!