Upgrade, the neobank launched by LendingClub founder Renaud Laplanche is celebrating the one-year anniversary of its flagship Upgrade Card – and a $50 million fundraising – with a new mobile checking account. Upgrade’s Unique Reward Checking Accounts offer 2% cash back on everyday and recurring expenses and 1% cash back on all other debit charges. Qualifying accountholders are eligible for up to 20% discounts on Upgrade loans.

“We asked our customers what would cause them to switch their primary checking account,” Laplanche said. “The overwhelming answer was attractive rewards on debit card purchases. While credit cards often provide decent rewards, it has been nearly impossible for consumers to earn a broad 2% cash back on debit charges.”

Upgrade’s Rewards Checking account, as well as all of the neobank’s banking services, are backed by Cross River Bank, chartered in New Jersey. Cross River founder, CEO, and chairman called the new accounts “everything mainstream consumers expect from a modern checking account with no fees, generous rewards, and access to affordable credit.”

The new offering comes as Upgrade enjoys strong adoption of its Upgrade Card, which offers access to installment financing online and at millions of points of sale via the Visa network. The company reported an annual rate of $1 billion in new credit lines already made available to consumers who are applying for Upgrade Cards or loans at a rate of more than one million a month.

Meanwhile in the wake of Brexit, European challenger bank Revolut is back in the market for a banking license in its home country. Revolut opted to secure its first banking license from the European Central Bank rather than pursue banking in the U.K. when anxieties over the future of a post-Brexit United Kingdom were at their peak. But now, with Brexit moving closer toward resolution, Revolut has returned with a bid to bring its digital banking services to the U.K.

“We want to be the best in class for customer experience, value and capabilities, and offering full bank accounts allows us to do just that,” Revolut founder and CEO Nik Storonsky said. “In the future, we want to offer many more innovative products to our UK customers and we are excited to continue driving innovation and competition in the banking industry. Becoming a fully licensed bank in the U.K. is a central pillar of that ambition.”

Toronto, Ontario-based challenger bank Koho announced this week that it has hired former Wayfair Director of Engineering Jonathan Klein as its new Chief Technology Officer. Klein takes over the CTO spot from Kris Hansen, who left the position back in August.

Founded in 2014 as the country’s first neobank, Koho has more than 120,000 accounts and reports $500 million in annualized transactions. The neobank offers full-service individual and joint bank accounts, along with a prepaid Visa card issued by People Trust Company. Koho has raised a total of $57.7 million in funding, most recently securing a $18.8 million Series B in the fall of 2019. Last year, Koho picked up an award for Best Prepaid Credit Card in Canada for 2021 from CreditCardGenius.

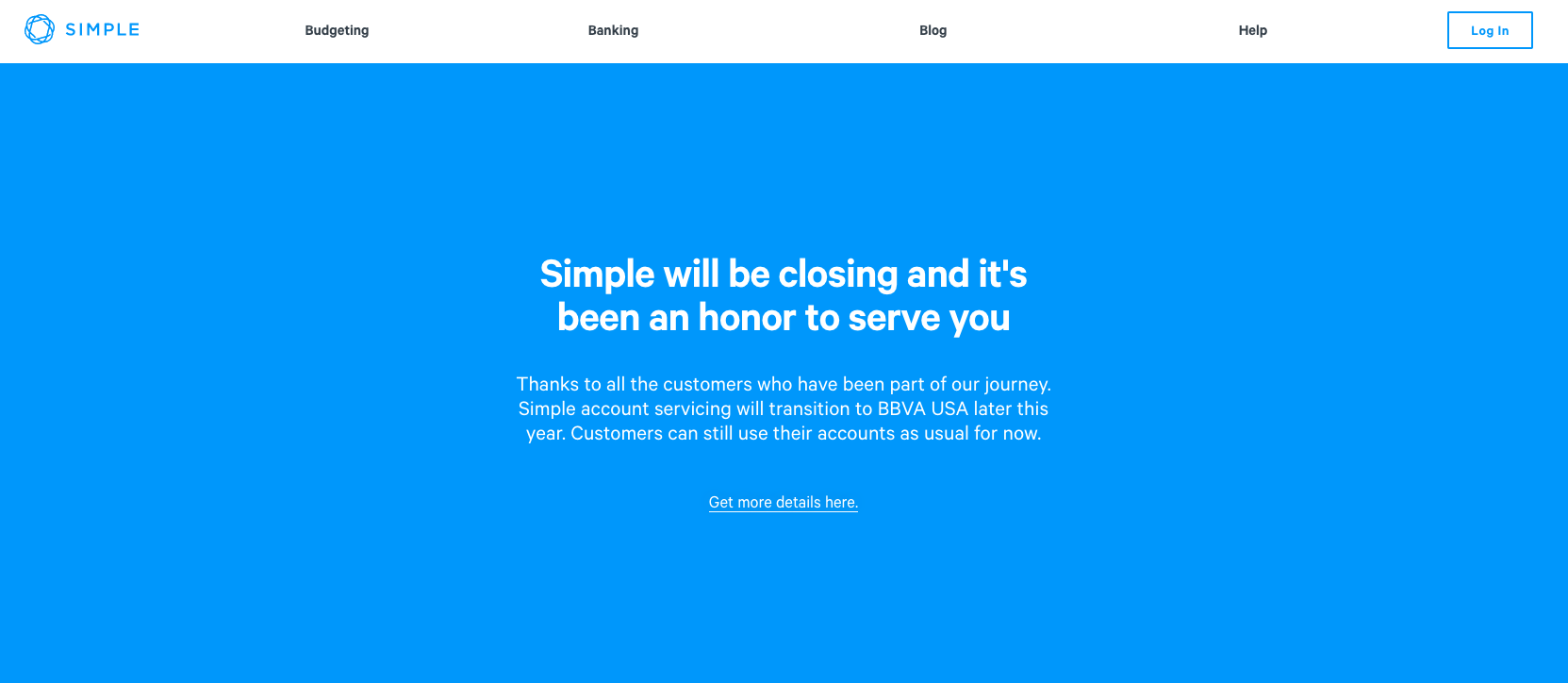

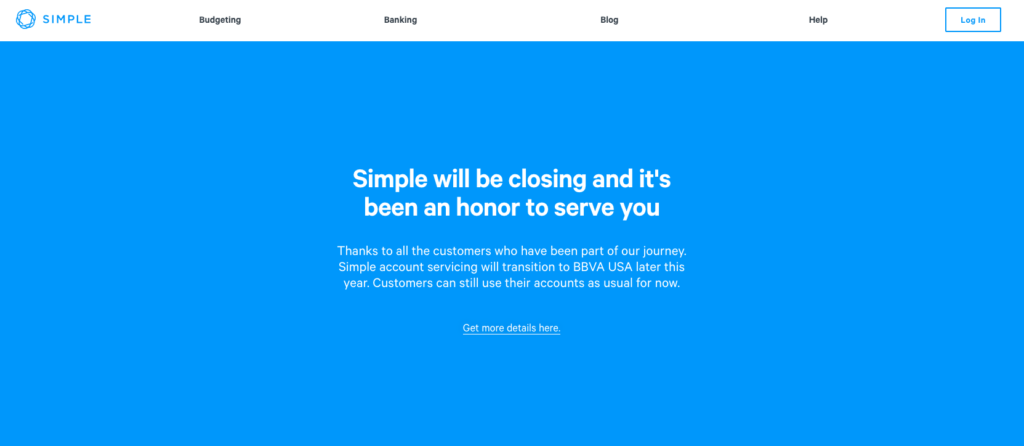

And for more from the neobank beat, check out our eulogy for Simple, the in-house challenger bank which was shuttered by BBVA after six years in operation.

Photo by Suzy Hazelwood from Pexels