This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Non-fungible tokens (NFTs) are the hottest fintech trend that nobody saw coming. And today, payments infrastructure firm Circle is extending its services to help support NFT marketplaces.

Circle’s new payments solution enables NFT marketplaces to accept both traditional payment cards and crypto payments. The Masachusetts-based company anticipates that the support will not only offer a more seamless user experience for NFT marketplaces, but will also support engagement by offering more payment options.

“This is not only an important and valuable trend for marketplaces and creators, it represents incredible demand from customers – for collectibles, artwork, moments, and really anything that can be tokenized on the blockchain,” said Circle Co-founder and CEO Jeremy Allaire. “Circle looks forward to supporting the industry – creators, platforms, marketplaces, storefronts and customers – with our solution for enabling a user-friendly, mainstream payments experience with the power of crypto connectivity and USDC.”

In the coming months, Circle will also add support for BTC and ETH payments; allow for the storage, custody, and transfer of NFT assets; and provide treasury and yield services.

Today’s news comes at a time when public awareness of NFT marketplaces is at an all-time high. One such platform, NBA Top Shot, has seen a 400% increase in sales over the past 30 days. Overall, sales volumes across major NFT marketplaces grew nearly 800%, to more than $200 million last month alone.

Since it was founded in 2013, Circle has supported over 100 million transactions worth tens of billions of dollars. The company, which counts almost 10 million retail customers and almost one thousand business clients, stores more than $5 billion in digital currency assets.

The post-COVID era of fintech will be defined by a renewed commitment to the customer experience – both digital and in-person. Add to this an eagerness to find and work with new partners, new markets, and new communities and you have a glimpse at what we saw in fintech’s future at FinovateEurope this month.

Among our demoing companies we saw innovators like Meniga that have developed solutions to help financial institutions better engage their increasingly climate-conscious customers. iProov, a multiple-time Best of Show winner, followed up a demonstration of its biometric authentication solution with a post-Demo Q&A conversation on how the technology is being applied in the fight against COVID-19. Finovate newcomer Cobase, which provides bank connectivity and treasury management solutions to corporates, shared insights into its decision to pivot toward also offering a white-label version of its platform to banks.

There was a moment, before COVID, when fintech’s perennial “Year of the Customer” declaration was in danger of becoming a bit of a cliche. Clearly, COVID turned that potential cliche into a real crisis in financial services as institutions were, due lockdowns and quarantines, literally cut off from their customers. Customer service strategies that had been perfectly appropriate – even innovative – a year ago, were obsolete in a matter of weeks.

How fintechs and financial services companies, internally, with their customers and members, and with each other, responded to this challenge was understandably the overarching theme of FinovateEurope. What we learned was that, in virtually every case, it was an embrace of both digital and human capital that enabled companies large and small to continue to serve their customers. And by taking advantage of a widening range of channels including voice and chatbot, and upgrading their capacity to effectively manage a higher volume and sophistication of digital transactions and activity, these institutions are well-positioned to outperform as the threat of the pandemic subsides.

A large part of this outperformance may well come from a renewed sense of the power of partnerships. The collaborations between financial institutions and fintechs to help facilitate relief funding to small businesses and individuals during the COVID crisis are not likely to be forgotten when the days of mask-wearing and social distancing are gone. And as the Meniga example shows, we should be equally observant to those heterodox partnerships; ones, for example, that add lifestyle offerings rather than just traditional financial solutions. As competition grows – including competition with Big Tech – these brand-redefining partnerships may become a more common response for fintechs and financial services companies, in Europe as well as in the rest of the world.

Avanti Financial Group has put the final touches on a deal that will bring the firm that much closer to its goal of launching a digital asset bank.

Late last week, Avanti announced that it had closed a Series A round, raising $37 million from a wide swathe of institutional investors, cryptocurrency companies, family offices, and angel investors.

The investment takes Avanti’s total capital to $44 million. Launched last year, Avanti secured $5 million in angel funding last June in a round led by the University of Wyoming Foundation and featuring participation from Morgan Creek Digital, Blockchain Capital, and Digital Currency Group. The new financing will fund the necessary regulatory capital for Avanti’s digital asset bank, as well as support engineering and operating expenses.

“Our roadmap includes offering API-based U.S. dollar payment services for wires, ACH, and SWIFT; issuance of our tokenized, programmable U.S. dollar called Avit; and custody and on-/off-ramp services for bitcoin and other digital assets,” Avanti founder and CEO Caitlin Long said. Long highlighted the number of customer inquiries (2,500+) that Avanti had received since it secured a bank charter back in the fall of 2020 and said that those looking to become a part of the firm’s digital asset bank should expect a launch “soon.”

Headquartered in Cheyenne, Wyoming, Avanti sees itself as a bridge between traditional banking and a world in which digital assets are bought, sold, and trusted as thoroughly as fiat currencies. A software platform with a bank charter, Avanti gives customers a strong regulatory environment compared to other digital asset companies, including a full-reserve requirement for dollar deposits and resources like its tokenized dollar, Avit, to help solve painpoints in the payments process.

Trace Meyer, who formed the consortium that led Avanti’s Series A, praised Avanti’s “potent, institutional-quality human capital.” A Bitcoin investor and early adopter, Meyer emphasized that both smart regulation and “experienced, competent operators” are critical to the institutionalization of digital assets, and said that Avanti was “well-positioned to competently answer questions that most in the industry have not even thought about.”

Financial services technology provider Fiserv made its latest acquisition this week. The Wisconsin-based company has agreed to purchase payment processing and payment acceptance startup Pineapple Payments.

Financial terms of the deal, which is expected to close next quarter, were not disclosed.

Under the agreement, Fiserv will continue to provide processing services to Pineapple’s 25,000 merchants. Fiserv anticipates the purchase will expand the reach of its own payment solutions, including the CoPilot partner platform, Clover, and Clover Connect.

“With Pineapple Payments already operating as a key distribution partner of Fiserv, we expect to accelerate the delivery of new and innovative capabilities to a host of new merchant clients,” said Fiserv President and CEO Frank Bisignano. “Together, we will provide omni-channel payments technology and services to enable merchants to maximize the potential of electronic payment processing. We look forward to welcoming Pineapple Payments to the Fiserv family and continuing to provide the best-in-class solutions and service that merchants and their customers expect.”

Headquartered in Wisconsin and founded in 2016, Pineapple Payments provides payment processing and omni-channel payment acceptance solutions for integrated software vendors and SMBs.

Today’s deal is Fiserv’s 35th acquisition. Prior to today, the company most recently bought up digital card services platform Ondot in a deal announced last December.

Last week, we leveraged the occasion of French alum Ledger’snew, cryptocurrency-focused, business division to bring readers up to speed on the latest in French fintech. This week, news from Fabrick, a financial services company based in Milan (and a sponsor of the just-concluded FinovateEurope Digital) offers us a similar opportunity to catch up with innovations in fintech in Italy.

Fabrick announced this week that it had forged a partnership with Microsoft Italia. The collaboration will enable the open banking financial services provider to leverage cloud computing and other new technologies to develop solutions that help accelerate digital transformation in financial services. As part of the alliance, Fabrick’s offering will become a part of the Microsoft Commercial Marketplace and enable the company to better market its technology to the enterprise sector. Fabrick’s personal financial management solution is already available on Microsoft’s marketplace.

“For us, the partnership with Microsoft represents an extraordinary opportunity to grow and strengthen our positioning in the market,” Fabrick CEO Paolo Zaccardi said. “We have found a valuable ally who, like us, has seen in technological evolution and Open Finance a new way to innovate the delivery of corporate services for the end user.”

Founded in 2017, Fabrick is an open banking ecosystem and a regulated TPP. Within digital payments, channel innovation, and open banking, Fabrick helps enrich the offerings of banks, processors, and fintechs. With customers including Bankart, HDI Assicurazioni, and illimity, Fabrick made fintech headlines earlier this year via collaborations with DizmeID Foundation for a hackathon based on innovations in digital identity, and with Banca Progetto and Faire to help the Italian challenger bank offer an instant lending service for small and medium-sized businesses.

“We are particularly enthusiastic about this collaboration because it testifies to the validity of the ecosystem proposed by Fabrick,” Zaccardi said when the partnership was announced last month. “On the one hand (we have) the capacity of our platform, through which the service will be implemented, and on the other the important synergies that arise within our community Fintech District, of which Faire is part and through which we have begun to collaborate with them.”

Like France, which we looked at last week, Italy has a fintech industry that is often overlooked in the broader conversation on European financial technology. To this end, this week’s Finovate Global Reports turns to the Fintech District and its The Italian Fintech Guide 2020 for a peek into “the most promising fintech companies operating in Italy.”

According to Fintech District, Italy had 345 fintech startups as of the end of 2019. It is a young industry – with most startups at an intermediate stage of growth and with less than one million in capital raised. Additionally, these fintech teams have members who are, on average, less than 32 years old. As with most regions, fintechs in Italy have increasingly been looking to enhance the digital capabilities of incumbent banks and insurance companies – as well as developing B2C solutions for Italian consumers. Open banking has helped accelerate this trend, and companies like Fabrick have been among those helping banks and third party solution providers connect and innovate together.

In recent years, our FinovateEurope conferences have featured a number of alums headquartered in Italy, as well. Ten of these companies, along with the year of their most recent Finovate appearance and their home city, are listed below.

Jeff App, loan brokerage platform the the underbanked, received a $1 million investment that will help the Latvia-based company continue its expansion in Vietnam, its first market.

Kona, an Uruguayan company that leverages AI to enhance the customer experience, has been acquired by Miami-based fintech Technisys to bolster its digital banking offering.

Asia-Pacific

Gimo, a fintech startup that serves underbanked workers in Vietnam, received seed funding from ThinkZone Ventures, BK Fund, and others strategic investors.

Our first all-digital European fintech conference is in the books. And given a little extra time to resolve a truly historic number of tied votes, our attendees have decided which companies will take home our Best of Show trophies for FinovateEurope 2021.

This year’s winners are:

Dbilia for its digital memorabilia that leverages blockchain and NFTs to enable fans to invest in creatives. Video.

Proptee for its global property app that helps reinvent the way people invest in real estate. Video.

Quantum Metric for its technology that helps retail banks differentiate on the digital experience, improve digital adoption, and enhance internal efficiencies. Video.

Thanks to all of our demoing companies, our partners and sponsors, and to you, our attendees in the fintech and financial services community. Be sure to stay in touch with the Finovate blog in the days and weeks to come for more information on our “Spring Collection” of webinars, networking opportunities, and upcoming conferences – including FinovateSpring in May.

Notes on methodology:

1. Only audience members NOT associated with demoing companies were eligible to vote. Finovate employees did not vote.

2. Attendees were encouraged to note their favorites during each day. At the end of the last demo, they chose their three favorites.

3. The exact written instructions given to attendees: “Please rate (the companies) on the basis of demo quality and potential impact of the innovation demoed.”

4. The three companies appearing on the highest percentage of submitted ballots were named “Best of Show.”

5. Go here for a list of previous Best of Show winners through 2014. Best of Show winners from our 2015 through 2020 conferences are below:

It’s hard to believe it’s only been one year since FinovateEurope 2020 wrapped. What a year it’s been! Looking back on the 2020 demo and speaker videos feels notable precisely because of how “normal” they all look. So much of the past year has been spent dealing with specific challenges and simply trying to weather the storm. It almost seems bizarre to see innovations that don’t specifically address COVID-related problems. But that’s exactly what we have to start doing again.

As we inch towards a gradual re-opening process and, with any luck, a new, more sustainable status quo, it’s vital that we don’t forget one of the biggest lessons of 2020: to prepare for the future, we have to look beyond the problems we can already see.

Fintech is an industry that rewards those who see problems before they arise, and there are no shortage of opportunities waiting just around the corner. Now is the time to look upstream and maybe even dust off projects you shelved a year ago. Put simply, it’s time to stop playing defense all the time and approach fintech with optimism again.

The writing is on the wall – we are going to return to “normal” again. Now it’s up to all of us to imagine how good “normal” can be.

Not letting any grass grow beneath its feet in the wake of the U.S. Justice department’s decision to block its acquisition by Visa, fintech infrastucture company Plaid has since launched its FinRise incubator to support early-stage founders who are members of ethnic minority groups.

“While technology has come a long way to level the playing field, the reality is that many minority-owned businesses are still frequently denied access to some of the most basic resources needed to start and grow their businesses,” Nell Malone and Bhargavi Kamakshivalli wrote on the Plaid blog when the program was announced in January. Highlighting in particular the plight of African-American owned businesses as noted in a report from the Small Business Administration, Malone and Kamakshivalli wrote: “It is a shared responsibility to help power a financial system that works for everyone, and we recognize that one way to achieve that is to support and promote a diverse ecosystem of entrepreneurs.”

All this makes today’s announcement that FinRise has chosen the first companies to participate in its accelerator program that much more exciting for supporters of financial inclusion and diversity. Out of more than 100 applications, five early-stage fintechs were selected, offering solutions in everything from identity verification and authentication to financial wellness and lending.

The qualifications for consideration were startups with at least one founder who is African-American, indigenous, or a “person of color,” has two or more employees, and is post-seed, pre-Series B in its funding status. The members of the incoming class are below:

Global Data Consortium: a global identity verification API that provides KYC and eKYC services for businesses

Guidefi: a financial wellness marketplace to help members of ethnic minority groups connect with “vetted, culturally-attuned” financial advisors

OfColor: a financial wellness program that offers personalized PFM and loans to help ethnic minority employees maximize their 401(k) contributions

Walnut: a point-of-sale lending platform that works with healthcare providers to make it easier for patients to pay for their medical bills

Zeta: a financial wellness company that specializes in PFM solutions for couples and families

FinRise begins with a three-day bootcamp of workshops covering issues ranging from regulatory and policy concerns to marketing and communications strategy. After the bootcamp, startups will be paired with Plaid mentors to help them further develop and scale their products. The nine-month program consists of workshops and networking opportunities with accelerator partners, as well as discounts on services offered by Plaid network partners. Even those startups not selected for the accelerator this session will be eligible for discounts and credits from companies supporting the program.

FinRise’s network partners include: Alloy, AWS Activate, Brex, Fintrail, FS Vector, Hummingbird, Very Good Security, and Zendesk.

On the heels of its FinovateEurope demo this week, digital banking player Meniga has raised $11.8 million (€10 million). The investment brings the company’s total funding to $55.7 million.

Velocity Capital and Frumtak Ventures led the round, followed by Industrifonden and Meniga customers UniCredit, Swedbank, Groupe BPCE, and Íslandsbanki.

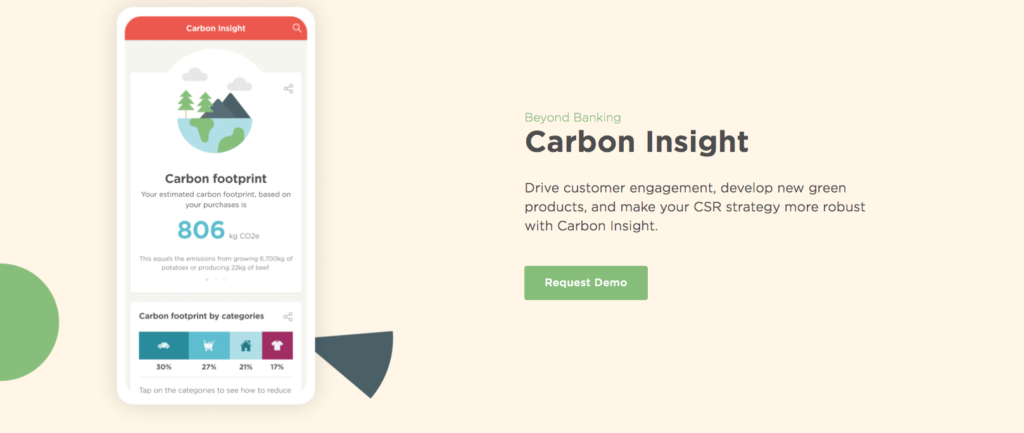

“Meniga has established itself as a trusted strategic partner to top-tier banks around the world for Personal Finance Management and Business Finance Management tools, which are built on top of its market-leading data consolidation and enrichment technologies,” said Willem Willemstein, General Partner & Founder at Velocity Capital Fintech Ventures. “We’re extremely excited about the growing demand for the personalised banking experiences that Meniga delivers, such as its new product, Carbon Insights, which uses transaction data to measure a bank customer’s carbon footprint.”

Meniga will use the funds to increase its R&D efforts and further build its sales and service teams. The company also said it will use the funds to bolster its green banking products.

The latter point is notable because Meniga has been making a name for itself in the green banking arena since the launch of its Carbon Insights tool. While multiple digital banking providers, such as Aspiration and Treecard, have launched in an effort to promote ESG banking for individual consumers, there have not been many players helping incumbent banks to compete by offering their own green banking products.

Launched last year, Carbon Insights enables banks to inform customers about their carbon footprint based on their spending habits and offers them the ability to reduce or offset it. Earlier this month Iceland’s Íslandsbanki became Meniga’s first client for Carbon Insights.

During the company’s FinovateEurope demo, Meniga CEO and Co-founder Georg Ludviksson noted that the company is currently implementing Carbon Insights with banks in four separate countries. “The demand is growing fast,” he added. “Carbon-concious consumers are here to stay.”

Founded in 2009, Meniga powers banking apps used by more than 100 million people in more than 30 countries. The company is headquartered in the U.K. with offices in Reykjavik, Stockholm, Warsaw, Singapore, and Barcelona.

Financial crime fighter Feedzai has secured a growth investment of $200 million. Product development, partner strategy, and global expansion are three Feedzai priorities that will be accelerated by the new investment.

The Series D round was led by KKR, and featured participation from existing investors Sapphire Ventures and Citi Ventures. The company’s total capital now stands north of $277 million, having most recently raised $50 million in a 2017 Series C round.

“This new investment delivers on our mission to keep commerce safe by further developing our single machine learning cloud platform for all four stages of the customer risk journey: prevention, detection, remediation, and compliance,” Feedzai CEO Nuno Sebastiao wrote on the company blog this week. “Focusing on the entirety of the risk lifecycle,” he added, “allows us to partner with financial services in a radically new way at every step of the journey.”

The funding also gives the risk management platform a valuation “well over $1 billion” the company noted in its funding announcement.

Partnered with some of the largest financial institutions in the world – including four of the five largest banks in North America, Feedzai leverages its risk management platform to monitor activity at companies with more than 800 million customers in 190 countries. The firm’s platform leverages machine learning and AI to help companies defend themselves from financial crimes including money laundering, detecting fraud in less than three milliseconds.

A Finovate alum since 2014, Feedzai unveiled its Feedzai Fairband solution earlier this month. Feedzai Fairband is an AutoML algorithm-based technology that automatically discovers less biased machine learning models while increasing model fairness by as much as 93% on average. Dubbed “the world’s most advanced AI fairness framework,” Feedzai Fairband enables financial institutions to accommodate their customers fairly and without the bias that even the most carefully-designed AI models may still hold.

“Feedzai Fairband is one of the biggest milestones in the financial services industry as it presents a low-cost, no-friction framework to address one of the biggest problems of our era – AI bias,” Feedzai Chief Scientist Dr. Pedro Bizrro said. “By creating the most advanced framework for AI fairness, Feedzai is allowing financial institutions to incorporate a critical piece of technology that addresses a problem under close public scrutiny with proven damaging effects across the globe. Building accurate and fairer models will be less challenging from now on.”

Named to Techround’s roster of the top 50 fintech companies in the U.K. in February, Feedzai highlighted the “skyrocketing” rise in fraud attacks in 2020 in its Financial Crime Report Q1, 2021, released earlier this month.

“2020 was a year of rapid growth in financial crime. Fraudsters tried to take advantage of the convergence between a fast-paced digital environment and a new wave of inexperienced consumers to perpetrate a multitude of attacks that created a significant uptick in fraud,” Jaime Ferreira, Senior Director of Global Data Science at Feedzai said in the report. “Financial institutions need to further invest in technologies to protect their customers while developing educational approaches. Robust technology and informed consumers are a powerful combination when fighting financial crime.”

Feedzai began the year with an announcement that Latin America’s largest investment bank, BTG Pactual, will implement Feedzai’s financial crime management technology.

Germany-based digital bank N26 announced today it is bringing on Gilles BianRosa as its new Chief Product Officer.

In this new role, Gilles will be responsible for leading product teams in Berlin, Barcelona, Vienna, and New York. He will also define, guide, and implement N26’s product strategy. To support these efforts, Gilles will bring on new team members and build N26’s product innovation.

“Gilles has a track record of delivering consumer-facing innovation that truly engages, excites and entertains customers,” said N26 co-founder and CEO, Valentin Stalf. “Today, N26 has revolutionized how people relate to their banking experience on an everyday basis. With Gilles on board, we will expand our experience further to being banking that easily connects an account with one’s lifestyle in an even more tangible way.”

Gilles brings with him decades of experience as CPO at tech companies including SoundCloud and Samsung Electronics. He also has entrepreneurial roots, having served as the co-founder and CEO of two Silicon Valley startups.

N26 is one of the most well-known players in the ever-growing digital banking realm. Founded in 2013, the startup offers its digital banking services in 25 countries, including the U.S., where it launched in 2019 and has since accumulated 500,000 customers in the area.

Today’s news comes about a month after N26 received a $35 million (€30 million) investment, bringing its total raised to $819 million. And it’s not the first C-level hire that N26 has initiated this year. In January, the company brought on Jan Kemper as Chief Financial Officer. Kemper holds experience in leading companies to go public, which may be an indication of N26’s intentions. In fact, Bloomberg expects the startup to IPO within the next two years.

In the biggest fundraising for an identity verification company to date, Jumio has locked in an investment of $150 million. The funding comes courtesy of Great Hill Partners, a private equity firm that specializes in investments in “high-growth, disruptive companies.” The investment takes Jumio’s total funding to more than $255 million, according to Crunchbase.

“Jumio’s innovations helped establish the identity verification market, and the need to establish someone’s digital identity remotely has never been greater,” Jumio CEO Robert Prigge said. The company plans to use the new capital to automate its identity verification solutions, expand the breadth of its Jumio KYX Platform, and further build out the platform’s suite of AML compliance solutions.

As part of the investment, Great Hill Partners’ Nick Cayer and Matt Vettel will join Jumio’s Board of Directors. Cayer, who has been with Great Hill since 2006, praised the company as “the de factor global leader in online identity verification, fraud detection, and compliance.” He added that given the mandate many institutions have to digitize processes such as onboarding and KYC monitoring, firms like Jumio can play a key role in helping them keep pace with the growing volume of digital and mobile-based transactions.

Making its Finovate debut in 2013 and being acquired by Centana Growth Partners in 2016, Jumio has verified more than 300 million identities issued by 200+ countries and territories since inception in 2010. With customers and partners in a wide range of verticals – from financial services and the sharing economy to retail, travel, and online gaming – Jumio leverages AI, biometrics, machine learning, and certified liveness detection to help ensure that customers are who they claim to be. Jumio’s KYX Platform, launched last fall, provides organizations with an end-to-end identity verification and eKYC solution that enables them to onboard new accounts safely and accurately, keep existing accounts secure, and meet their compliance obligations with regards to KYC, AML, and GDPR.

“Digital transformation is more than a buzzword. It’s today’s business imperative,” Prigge said. “To succeed, organizations must transform quickly and do it in ways that build trust, security, and satisfaction. Businesses can tailor the Jumio KYX Platform to fit their unique needs and risks and tap into services that accelerate digital transformation without sacrificing security and convenience.”

Learn more about how Jumio fights deep fakes and bots in our interview from last summer featuring company VP of Marketing, Dean Nicolls.