This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

In an era when SPACs are the hip new way to take a company public, corporate expense management technology company Expensify is taking the old fashioned route.

The San Francisco-based fintech announced this week it has submitted an S-1 document– a key step on the road to an initial public offering to the SEC. The S-1 was submitted confidentially. Since Expensify is considered an “emerging growth company,” the contents of the filing do not need to be made public until 21 days prior to the road show for the IPO.

Expensify, which reached profitability at the end of 2018, has not yet determined the size and price range for the proposed IPO.

Founded in 2008, Expensify launched with its flagship receipt-scanning app and a simple motto, “Expense reports that don’t suck!” Since then, the company has gone on to launch a corporate payment card, offer a COVID-friendly virtual travel assistant, andexpand into billpay.

Expensify’s IPO is expected to commence after the completion of the SEC review process, subject to market and other conditions. The company has raised a total of $38.2 million. David Barrett, who Finovate interviewed about the company’s launch, is CEO.

In the age of “diamond-handed” growth investors and message board stock jockeys, does anyone even analyze stocks any more?

Israel-based online stock research firm TipRanks is betting that the answer is “yes.” The company, which offers solutions that enable investors to quickly analyze stock market data and the performance of market analysts, secured a $77 million investment in a round led by technology group Prytek last month. The funding will help the nine-year old fintech take advantage of the surging interest in trading and investing by retail customers.

TipRanks leverages Natural Language Processing technology to review and analyze data from a wide variety of sources including analyst forecasts, financial bloggers, insider activity, news sentiment, and both the collective wisdom of individual investors on the platform as well as the actual investments by top hedge fund managers. A two-time Finovate Best of Show winner, TipRanks offers quantitative tools like its Smart Score for stocks and its Star Ranking System for analysts to allow investors to quickly assess a stock’s prospects or the value of a given analyst’s opinion.

“In addition to being the only company that ranks analysts based on their performance rather than the prestige of the bank they work for, we are the only company that makes aggregated analyst ratings available to retail investors,” TipRanks co-Founder and CEO Uri Gruenbaum said. “We analyze all finance-related news, corporate filings, analyst research, and social media to provide retail investors with the same level of information that only institutional investors can afford. By doing so, we enable retail investors to make data-driven investment decisions.”

The investment takes TipRanks’ total funding to $80 million. The company will use the new capital to add to its workforce, having experienced a significant jump in demand for its solutions in 2020. TipRanks noted that it has more than four million monthly users in the wake of a 3x boost for its subscription-based services last year. Gruenbaum added that TipRanks also plans to expand its research coverage to include other asset classes and markets such as cryptocurrencies and exchange-traded funds (ETFs).

The new partnership will also give TipRanks access to Prytek’s tools and datasets which bring greater transparency to online investment advisory. Founded in 2017, Prytek is an Israel-based multinational technology group that specializes in investing in new technologies and delivering managing services to companies in financial services and other verticals via its Business Operating Platform-as-a-Service model (BOPaaS).

A look at the companies demoing at FinovateSpring Digital on May 10 through 13, 2021. Register today and save your spot.

Help With My Loan‘s software is helping banks, brokers, and consumers find the right loan. Its automated processing underwrites and matches at a 95% funding rate in commercial, residential, business, and personal loans.

Features

Improve front-end lending performance with back-end software

Save up to 80% in time on financial document analysis

Underwrite loans right from your website 24/7

Why it’s great The software’s AI ensures you navigate though market changes, uncertain economic changes, and helps lenders maximize their team’s performance.

Presenter

Chris Karageuzian, CEO & Co-Founder Karageuzian is the Co-Founder and CEO of Helpwithmyloan.com. He has over 20 years of experience working in sales and management for Coldwell Banker, Wells Fargo, JP Morgan Chase, and U.S. Bank. LinkedIn

Of all the trends accelerated by the global pandemic, enhancing customer engagement may be both the most critical and the most enduring as we transition toward a post-COVID world. In the latest edition of his Finovate Podcast, host Greg Palmer talks with Crayon Data founder and CEO Suresh Shankar about his takeaways from 2020 and what he expects from fintechs and their customers in 2021.

Shankar founded Crayon Data, a big data/AI startup, in 2012. The Singapore-based company helps businesses succeed by leveraging enterprise data to create digital-first customer experiences. Crayon’s flagship platform, maya.ai, enables businesses to boost revenues, reach inactive customers, and cut down on time and effort on low-ROI marketing campaigns – all by delivering highly relevant, highly personalized digital experiences to customers without compromising privacy. Crayon Data made its Finovate debut at FinovateEurope last year.

The Finovate Podcast is also a great source for 30,000 ft high observations on both the fintech landscape as well as the broader terrain of technological innovation. Greg Palmer’s recent conversation with futurist Nancy Giordano delves into what she calls the “Productivity Revolution” and its implications for fintech and financial services.

“There was a way we approached building the industrial era of the 20th century and prior that now no longer holds up and we have to have a really different way of thinking as we move into the future. ‘Leadering’ (the title of her new book) is the contrast to ‘leadership’. It’s a verb that’s dynamic and inclusive and caring and allows us to build the future that we really want to build … It sounds lofty, but it’s actually pretty practical.”

A guest lecturer at Singularity University, a ten-year TEDx curator, founder of Play Big Inc. consultancy, and one of the premier female futurists in the world, Giordano consistently underscores the role of the individual in times of rapid change and disruption. Her new book, Leadering: The Ways Visionary Leaders Play Bigger, connects the rise of innovative technologies with changing societal expectations to give individuals insight into what it takes to create human-centered solutions and long-term value.

For more from the Finovate podcast, check out our podcast archives.

Buy now, pay later (BNPL) company Sezzle is planning to strike while the iron is hot.

The Minnesota-based firm, which is already publicly-listed on the Australian Stock Exchange (ASX), is hoping to capture U.S. investors, now that the BNPL trend has exploded in this continent. Plans for the public listing are still in early stages. Details, such as the timing, price, and use, have not been revealed.

Prompting the plan to list is the company’s recent growth. According to its latest earnings announcement, Sezzle added 400,000 customers and recruited 7,300 active merchants in the first quarter of this year. This boost brings the firm’s total users to 2.6 million and total merchants to 34,000. Not surprisingly, the surge in usage helped increase the company’s first quarter income, which was reported at $22.3 million.

Sezzle initially went public on the ASX in July of 2019, raising $30 million on its first day of trading. The company now has a market cap of over $777 million. This figure is almost 5x higher than it was at the start of 2020. Sezzle’s move to the U.S. public markets follows its competitor, Affirm, which debuted on the Nasdaq at the start of this year.

Sezzle’s BNPL technology allows customers to split their ecommerce purchases into four installments with only 25% down and no fees. The offering is currently available to shoppers in the U.S., Canada, and India, and will soon be offered to residents in Brazil.

In February, Sezzle teamed up with Discover to work with select merchants on Discover’s network to help them provide their customers with additional payment options. Last September, the company launched a virtual payments card that helps customers benefit from Sezzle’s BNPL tech when they make purchases at brick-and-mortar stores.

Sezzle was founded in 2016. Charlie Youakim is CEO.

In a round led by Meritech and Greylock, Canada-based fintech Wealthsimple has secured $610 million (C$750 million) in funding. The investment takes the online brokerage’s total capital to more than $1 billion, more than triples the company’s most recent valuation to $4 billion, and represents one of the largest financings for a Canadian technology company to date.

“Seven years ago, we launched Wealthsimple with just four people and a mission that many thought was naive: use technology and innovation to revolutionize the finance industry so every Canadian could achieve financial freedom, no matter who they are or how much money they have,” Wealthsimple co-founder and CEO Mike Katchen wrote on the company’s blog this morning. “I’m happy to say that our mission doesn’t seem quite so naive anymore.”

Also participating in the round were DST Global, Sagard, Iconiq, Dragoneer, TCV, iNovia, Allianz X, Base 10, Redpoint, STEADFAST, Alkeon, TSV, and Plus Capital. A host of Canadian celebrities were also involved in the funding, including actors Ryan Reynolds and Michael J. Fox; athletes Kelly Olynyk, Dwight Powell, and Patrick Marleau; and singer Drake.

Since its inception in 2014, Wealthsimple has grown into a firm with more than two million users who enjoy commission-free stock trading, automated investing, as well as access to cryptocurrencies and tax services. This spring, the company introduced its cash app, which enables Canadians to send and receive cash “in seconds.” Free and requiring no minimum balance to use, Wealthsimple Cash has been likened to Venmo, a popular cash app in the U.S. The app currently has daily spending limits of $5,000 a day and $20,000 a month; Wealthsimple said that this is significantly more generous than what is available through the big banks.

Wealthsimple’s investment news comes as the Toronto, Ontario-based fintech pivots to pursue new opportunities in the Canadian market (the company sold its U.S. investment advisory business to Betterment in March). During the investing mini-mania surrounding Robinhood and shares of Gamestop earlier this year, investors in Canada were weighing in by making Wealthsimple’s trading app the number one app on Canada’s Apple App Store and on Google Play. This ratings boost was accompanied by a 50% gain in sign-ups and a 2x increase in trading volume. The environment created by the global pandemic, according to Wealthsimple’s Katchen, played a significant role in the company’s growth; 18% of the country’s new brokerage accounts in the first half of 2020 were opened on Wealthsimple’s platform.

Like a growing number of fintechs, Wealthsimple also plans to extend its offerings to include cash, checking, insurance, and mortgage products with the goal of becoming the customer’s “primary financial institution“. The company initially earned its unicorn status in October, after securing an investment of $93 million (C$114 million). Power Corporation of Canada is the company’s majority shareholder, with a 43% of the company post-financing.

From U.K.-based Standard Chartered to Germany’s Deutsche Bank, banks around the world are adapting to the post-COVID world with fewer branches. In separate announcements only a few days a part, two of the globe’s bigger banking presences (Standard Chartered is the 44th biggest bank in the world by total assets; Deutsche Bank is ranked 21st) have signaled that hybrid workplaces will join digital transformation as defining aspects of banking operations in the future.

Standard Chartered’s announcement comes as the firm reports better-than-expected profits for the first quarter. The bank plans to reduce the size of its branch network to 400 – and move to a hybrid remote working setup – as part of a cost-cutting maneuver. Standard Chartered also announced that it will look to automation to “enable the re-shaping of the workforce.” Standard Chartered has a strong presence in Asia, Africa, and the MENA.

As for Deutsche Bank, company CEO Christian Sewing cited fewer branch customers and a growing preference for digital options among the reasons driving the move toward a hybrid model. Deutsche Bank expects to close 150 Deutsche Bank and Postbank branches this year with an additional 50 Postbank branches to be closed in 2022. At the same time, the company said it will introduce a hybrid workplace model for its employees that will allow them to work remotely up to three days a week.

Hybrid workplaces aren’t the only things that financial services workers will be getting used to in 2021. If the new employee training initiative from Spain-based BBVA is any indication, bank workers may find themselves being reskilled and upskilled just by playing a game.

BBVA has announced a new global reskilling and upskilling experience, The Camp, that is designed to enhance the employability of its professional workers. Part of BBVA’s learning model, Campus BBVA, the new experience focuses on 14 strategic skills that are taught using a digital, gamified environment in which the workers are the primary actors who determine their own development.

“The challenge of ensuring the survival of organizations entails adapting and being flexible enough for teams to be able to navigate this uncertainty and constantly incorporate the skills that are needed to promote the strategy,” Global Head of Learning at BBVA Pilar Concejo said.

Each of the 14 strategic skills has a different training itinerary. And each itinerary has three levels of specialization that uses a mountain-climbing analogy to assess the employee’s progress. Starting out as a metaphorical hiker, the employee advances from the valley (basic level) to the mountain (intermediate level), earning status as an “explorer.” Successfully advancing from the mountain to the summit (expert level) gives the employee the rank of “alpnist” – the highest level of specialization in the knowledge category.

“Gamification is a very important element at Campus BBVA, and now also at The Camp, as it allows us to design experiences in which employees feel much more identified and increase their level of commitment to the learning process,” Concejo said. “In the end, we try to ensure that the employee is motivated enough to move forward with their development in a continuous and sustainable manner over time.”

Here is our weekly look at fintech innovation around the world.

Washington, D.C.-based digital banking infrastructure company Securrency announced plans to expand in the UAE in the wake of its $30 million fundraising.

Financial Times featured Fusion Microfinance, a company that specializes in providing microloans of between Rs10,000 ($136) and Rs60,000 ($816) to poor women in India.

“We have built a world-class financial technology partner ecosystem which our clients can tap into as they build a future-proof bank,” Thought Machine CEO Paul Taylor explained. “The firms we choose to partner with are those that have built meaningful, ultra-reliable products that ultimately improve the banking experience for customers. We look forward to working with Wise to bring its industry-leading payments solution to many more financial institutions, and customers, around the world.”

To ensure cross-system interoperability, Thought Machine and Wise have built an integration layer that cuts down on the amount of development work needed to plug into Wise’s API by as much as 60%. The partnership is a response to the growing demand for faster, more affordable, and transparent multi-currency banking, and comes amid a broadening trend away from reliance on legacy core banking technology and traditional correspondent banking networks.

“Though the internet has transformed much of the economy, the global banking system has lagged behind and moving money internationally has remained slow, difficult, and expensive for most,” Wise Platform & Wise Business Managing Director Stuart Gregory said. “Our mission is to change this 一 a goal we share with Thought Machine. Our integration today makes it quicker and easier for financial institutions and banks to enable faster and cheaper payments for their customers and brings us one step closer to our mission of building money without borders.”

Wise is actually the second money transfer company that Thought Machine has teamed up with in the first half of 2021. In February, the company announced that it was working with TransferGo, who will use Thought Machine’s Vault to provide advanced platform capabilities that will enhance the customer experience. The company also recently forged partnerships with German software engineering company GFT to launch challenger bank BankLiteX, and with full-stack fintech solution provider Vacuumlabs, which leveraged ThoughtMachine’s Vault to power a virtual bank in Hong Kong. An alum of FinovateEurope, London-based Thought Machine has raised more than $148 million in funding.

A Finovate alum since 2013, Wise moves more than $6 billion every month, saving its 10 million customers $1.5 billion in hidden fees every year. Rebranding as Wise in February, the company unveiled its product roadmap earlier this month, highlighting new initiatives in customer experience, spending and cards, expansion, small business services, and security. The company offers a multi-currency account that enables individual users to take advantage of real exchange rates in more than 50 international currencies. Wise Business provides payment services including invoice payments, debit cards, P2P payments, and cash management to more than 400 businesses. The firm includes companies ranging from fellow Finovate alum Xero to challenger bank N26 among its customers.

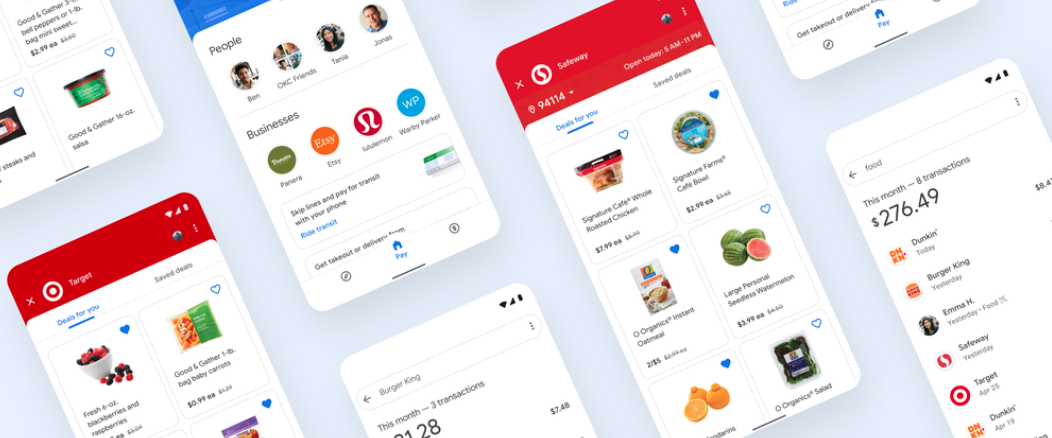

After reviving Google Pay in November of last year, Google made an announcement today that is sure to turn some heads in the fintech space. The two most relevant elements in today’s news release are new shopping options and spending insights.

To offer new shopping options, Google has partnered with Safeway and Target to help users browse weekly deals on groceries at Safeway and Target locations from within the Google Pay app. The app will enable shoppers to save their favorite items to purchase at a later date. Soon, users will be able to turn on push notifications to see deals from 500 Safeway stores and nationwide Target stores when they are nearby (if they have location services enabled).

The additional embedded shopping tools bring added stickiness to the app. However, Google will need to offer shopping experiences at more than just two stores to truly capture users’ attention.

Google Pay’s new spending insights tool comes a bit closer to what consumers may expect to see at their traditional bank. Via the Insights tab, users can see their account balance, view upcoming bill reminders, analyze weekly spend summaries, and receive alerts when large transactions are made. Under the Insights umbrella, Google also made it easy for users to view transactions by merchant or by category.

While the new spending insights may prove to be useful to shoppers, without more robust budgeting, planning, and forecasting tools Google Pay is unlikely to win consumers over from their traditional bank.

In today’s release, Google also added two more cities in which travelers can pay for transit. Via an integration with Token Transit, users in the San Francisco Bay area and Chicago can purchase and use mobile transit tickets through the Google Pay app. The two new cities join the list of 80 cities and towns across the U.S. that already offer travelers transit purchasing capabilities via Google Pay.

Regardless of the shortcomings of today’s new features, both banks and fintechs should be wary of Google Pay’s next moves. The app’s embedded finance capabilities, including grocery shopping and added transit ticket purchasing, are a signal of what is to come. Similarly, if Google Pay continues to add more personal financial management tools, such as budgeting and retirement planning, consumers may want to spend more time within the Google Pay environment and less time in their traditional banks’ app.

Our all-digital spring fintech conference is right around the corner. Here’s a look at some of the luminaries who will be sharing their insights at this year’s FinovateSpring, May 10 through May 13.

Seven in Seven

For years, we’ve put our demoing companies to the seven-minute test. Now its our experts’ turn on the clock. Our Seven in Seven main stage session on Tuesday, May 11, gives seven analysts, innovators, and executives seven minutes each to share their insights into the most critical issues facing banks and fintechs in 2021 and beyond.

Looking for a 30,000 foot view of the fintech landscape? Our mainstage, keynote addresses examine the terrain.

The Pandemic’s Lasting Impact on Financial Services and What Comes Next

The pandemic pushed financial services companies to innovate and accelerate their digital transformations overnight. Hitting the industry’s reset button has created growing pains and increased competition for some and opportunities for others, including new customers and partnerships– but what does this mean for the future of banking?

Melissa Manne, Marcus by Goldman Sachs – Session – Bio

Enabling a Data-Driven Enterprise

To streamline and automate compliance activities, leading firms are now implementing an enterprise data fabric to bring together data from across the enterprise, reducing manual effort, increasing accuracy, lowering latencies, and simplifying operations.

In this session we will present a subset of the research findings, describe what top analysts are calling “the future of data management,” and how it is being used to streamline both compliance initiatives and accelerate strategic business initiatives at top financial services firms.

A Digital Banking Roadmap For Community Banks & Credit Unions: Start With The Customer & Work Back

Rilla Delorier, Coastal Community Bank – Session – Bio

Power to the Panels!

From insights into customer engagement to expanding the role of women in fintech, our mainstage Power Panel discussions offer deep dives and diverse opinions on key issues in our industry.

Customer Insights – Sharing Real Life Examples Of Best Practice In CX And How To Blend Human & Digital CX

Tickets for FinovateSpring are available now. Book your reservation by April 30 (this Friday!) and save $100 on the price of your four-day, all-access pass!

Upcoming webinar Title: Innovating for success: How insurers can embrace innovation to drive growth Date: Tuesday, May 18, 2021 Time: 02:00 British Summer Time Duration: 1 hour

Technology and innovation are key to driving growth and creating scalable and agile business models in a challenging environment. It is an exciting time for insurers and many are seizing this opportunity to transform by investing in innovation, accelerating the evolution to digital, and evolving in ways that appeal to customers.

Join our latest webinar to explore:

Is innovation important and why?

Are insurers truly getting return from their investment in innovation?

What insurers can do so that their innovation endeavours lead to genuine growth?

Top tips that drive innovation – critical tasks and internal challenges?

How insurers can build an innovation funnel /roadmap?

Featuring Preetham Peddanagari, Digital Insurance Leader, EY EMEIA; Roy Jubraj, Chief Strategy & Transformation Officer, esure Group; Emmanuel Djengue, Innovation Director, RGAX Europe and Marcin Kurczab, Head of Innovation Lab, PZU Group.

We may still be enduring the absence of in-person networking, but there are a handful of ways to stimulate casual banter among conference participants.

At FinovateSpring, taking place digitally May 10 through May 13, we are making it as easy as possible for attendees and speakers to engage with each other through interactive roundtable sessions, networking “rooms” and a digital cafe.

One avenue we’ve found particularly useful to bring a personal element to the demo presentations is our curated set of 25-in-5 videos. In these videos, our team asks 25 rapid-fire questions in under five minutes to the demo companies at FinovateSpring.

My favorite part of these videos is that they bring a human element to each demo company. That’s because we ask the presenters off-beat questions that help you get to know them on a more personal level.

All of the 25-in-5 interview videos will be available as exclusive, on-demand content within the FinovateSpring Digital event platform. If you’re registered, keep an eye out for early access to schedule meetings and curate your event-day agenda with the sessions that most interest you.

And don’t worry about missing out. There’s still time to register, and with no need to buy a plane ticket and book a hotel room, FinovateSpring is more accessible than ever.