This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

“As one of the fastest growing technology companies in the world, this cash injection – in addition to having the built-in option to expand the financing – will significantly accelerate the growth of our customer base, enhance SumUp’s technology leadership position, and drive the development of new services to support our merchants globally,” SumUp co-founder Marc-Alexander Christ said.

SumUp’s funding news comes at a time when the company is adding to its product portfolio in both Europe and the U.K. Much of this growth has come through acquisitions of POS software providers like London-based Goodtill, as well as Tiller, a digital service provider for gastronomy merchants. Separately, SumUp’s recent acquisition of Paysolut, a Lithuanian cure banking system provider will enable the company to fortify the banking services that it offers to its merchants.

SumUp supports more than three million merchants around the world. In addition to its expansion in Europe – going live in Romania to bring the total number of its European markets to 29 – the company has added to its interests in the Chilean market and launched operations in Columbia – the fourth largest economy in Latin America.

At the beginning of this year, SumUp announced that it was working with Shutterstock to give merchants the ability to add high-quality visual images to enhance their online storefronts.

“It’s important now more than ever that small businesses have the means to trade in the e-commerce space in order to take on larger competition,” SumUp European EVP Alex von Schirmeister said. “This partnership with Shutterstock will do just that, giving them more visibility to grow their customer bases.”

Founded in 2011, SumUp made its Finovate debut at FinovateEurope in 2013. Daniel Klein is CEO.

upSWOT, a fintech that helps bring business intel to small business owners, has raised $4.3 million in seed funding. Among Finovate’s newest alums, upSWOT offers a data aggregation and business finance management platform that leverages cash flow predictions and business insights to enable banks, insurance companies, and other institutions to better serve their small business and mid-market customers.

“Managing a portfolio of SMB clients is a challenge for every bank, lender, and servicer,” upSWOT CEO Dmitry Norenko said. “Amidst a global pandemic, the financial industry must find new and innovative ways to support this vital customer segment. Our white-label solution helps leading national and community banks gain granular insights into their SMB customers launched within six weeks, and with minimal strain on internal IT or overlap with legacy systems.”

upSWOT’s funding round was led by Common Ocean, a venture capital firm that specializes in early-stage fintechs that are innovating in the financial wellness space. Also participating in the round were CFV Ventures, ICBA, First Southern National Bank, and SpeedUp Venture Group, as well as previous investors. upSWOT said that it would use the funding to grow its business in the U.S., add talent to support “a growing list of deployments with Tier 1 and Tier 2 financial institutions,” as well as continue to add features and functionality to its data aggregation and BFM platform.

upSWOT leverages APIs to aggregate data from more than 120 widely-used business solutions such as Quickbooks, Salesforce, Amazon, and Shopify and provide business owners with predictive analysis and actionable insights. Via partnerships with financial institutions, upSWOT’s goal is to help SMEs that have been left to “fend for themselves” by giving them “modern day tools” to help support cash flow management, debt funding, financial planning and accurate cash reporting.

Founded in 2019, upSWOT demonstrated its white-label platform at FinovateWest Digital last year. A graduate of the Berkeley SkyDeck accelerator, the company includes Raiffeisen Bank International, Privat Bank, D&B, and Mastercard among its customers.

What happens after the newest cutting-edge banking technologies become table stakes? Banks move on to tackle another new technology.

In fact, in the past decade or so, banks have been constantly moving from one new technology to the next– from remote deposit capture to merchant-funded rewards, roboadvisory services, AI-informed marketing strategies, and finally on to complete digital transformation.

So now that 2020 served as the year of digital transformation, what’s next? How will banks use their limited resources to get ahead of the curve? Below are a few areas in which banks are focusing their attention to gain competitive advantage:

Communication

Last year we saw multiple financial services organizations update their communication technologies in tandem with digital transformation. But the game of facilitating customer communication is far from over. As Ron Shevlin pointed out in his piece, Every Bank Needs A Chatbot (Or Two) For Its Digital Transformation, chatbots are no longer simply a novelty. Instead, these tools offer fast turnaround for customer inquiries, provide additional data about consumers, and help firms hold personalized conversations with clients.

Another communication enhancement comes in the form of leveraging popular third party apps to communicate with customers. Axis Bank, for example, India’s third-largest private sector bank, recently announced a partnership with WhatsApp. Customers can now use WhatsApp to inquire about their account balance, recent transactions, credit card payments, deposit details, and block their credit or debit card.

Cryptocurrencies

Ready or not, crypto is here! In January, the U.S. Office of the Comptroller of the Currency (OCC) published an interpretive letter detailing that banks can transfer stablecoins to other banks. While banks haven’t been rushing to leverage this functionality, there have been a few moves that indicate financial services are slowly entering the cryptocurrency game.

First off, marketing services company Kasasaunveiled plans to help its bank and credit union clients provide bitcoin wallets to their consumers. Additionally, Mastercard recently announced it willallow merchants to accept payments in cryptocurrencies, and BNY Mellon agreed to begin custody of cryptocurrencies.

Payment tools

With so many payments moving online in the past year, banks need to be even more aware of their role in the online payments flow. In fact, the recent rise in embedded payments poses a risk to banks as third party apps such as Uber and DoorDash make the payment element of a transaction almost disappear.

There’s also been a lot of competition in the booming buy now, pay later (BNPL) space, and not just from third party fintechs like Klarna and Afterpay. Last year, Citi announced Citi Flex Pay, a product that enables cardholders to pay for select purchases over time at a lower interest rate than their card’s purchase rate. And in 2019, JPMorgan Chase launched My Chase Plan, an offering that allows cardholders to make equal monthly payments on purchases of $100 or more with no interest, just a fixed monthly fee.

Offering another tool to make payments more flexible, is U.K.-based fintech Curve. The fintech connects with consumers’ existing payment cards to offer rewards as well as a Go Back in Time feature that lets users switch payments from one card to another for up to 14 days after the purchase was made.

Sustainability

If you’re not green, you’re gone! O.K., maybe not quite, but in the past few months we’ve seen an increase in fintechs working toward a more sustainable future. In fact, just this month there have been multiple headlines that highlight fintech’s green future. First, U.K.-based digital bank Starling Bank launched recycled plastic debit cards. Second, Citi began restricting financing for companies expanding coal power. And finally, Menigapartnered with Iceland’s Íslandsbanki to integrate Meniga’s Carbon Insight into its digital banking solution.

Fintechs are also helping consumers do their part to minimize their impact on the environment. Aspiration, for example, ensures accountholders that their deposits won’t fund fossil fuel projects like pipelines, oil drilling and coal mines. The startup also works with reforestation partners to plant a tree when users roundup their purchase to the nearest dollar. And speaking of trees, Treecard offers a wooden Mastercard and donates 80% of its profits to reforestation efforts.

Ecommerce technology company Stripe announced over the weekend that it recently raised $600 million in funding. The Series H round brings the company’s total funding to $2.2 billion and boosts its valuation to $95 billion.

Investors in this month’s funding round include Allianz X, Axa, Baillie Gifford, Fidelity Management & Research Company, Sequoia Capital, and Ireland’s National Treasury Management Agency.

Stripe will use the funds to expand its Global Payments and Treasury Network and invest in its European operations to support increasing demand in the region. Specifically, the California-based company aims to boost its Dublin headquarters.

“We’re investing a ton more in Europe this year, particularly in Ireland,” said Stripe President and Cofounder, John Collison. “Whether in fintech, mobility, retail, or SaaS, the growth opportunity for the European digital economy is immense.”

Stripe has clients in 42 countries, 31 of which are in Europe. Among the company’s European clients are Deliveroo, Doctolib, Glofox, Klarna, ManoMano, N26, UiPath, and Vinted.

As Stripe pointed out in a blog post, only 14% of commerce happens online. That’s why, as the company’s CFO Dhivya Suryadevara notes, Stripe is “investing in the infrastructure that will power internet commerce in 2030 and beyond.” More specifically, the company is expanding its software and services and is making its technology available to millions more businesses in Brazil, India, Indonesia, Thailand, and the UAE.

“While Stripe already processes hundreds of billions of dollars per year for millions of businesses worldwide, the opportunity ahead is much larger for Stripe than it was when the company was started 10 years ago,” added Suryadevara.

This week for our Finovate Global Lists feature we congratulate the graduates of Startupbootcamp FinTech Dubai. Eleven startups successfully completed the MENA-based accelerator program in late February, wrapping up the three-month experience with a pitch opportunity before an audience of investors, corporate partners, mentors, and industry analysts.

“As the Demo Day has passed and the 11 startups of our third cohort continue their growth journeys – we are incredibly proud to welcome the 23 amazing founders of these startups as part of our global @sbcFinTech family!” Startupboootcamp Dubai announced via Twitter.

The graduates are:

Finllect: a UAE-based financial wellness app for Gen Zs.

Flaist: a digital transformation platform for banks.

Singular Capital: a digital asset mobile wallet based in Malaysia.

Open CBS: a Hong Kong-based, open and scalable, cloud-based core banking system for smaller FIs.

Absolute Collateral: a digital B2B capital markets trading platform based in the U.K.

Tajjir: a Jordanian startup that offers a stock trading software solution for retail investors.

Aura Technologies: an insurtech firm that enables non-insurance businesses to sell insurance to their customers.

CaaS (Compliance-as-a-Service): a regulatory reporting platform based in the U.K.

Stornest: a UAE-based digital legacy planner to support end of life planning.

Raseed: an investment platform that enables users in the UAE and Saudi Arabia to buy and sell U.S. stocks.

Kilde: a global private debt marketplace headquartered in Singapore.

Startupbootcamp FinTech is conducted in partnership with Dubai International Financial Centre (DIFC), Visa, HSBC, and Mashreq Bank. The program is open to fintech startups throughout the MENA region, as well as around the world, and offers expert-led Master Classes, tailored mentorships, as well as coworking space and living expense support for the duration of the program. Participants also benefit from access to corporate partners and an alumni growth program that helps startups remain networked after the program ends.

Since its launch in 2018, more than 30 fintech startups innovating in payments, lending, and Islamic digital banking count themselves as alumni of the accelerator. Startupbootcamp FinTech Dubai is part of an international network with more than 20 industry-focused programs for technology startups. The network boasts 950 startups accelerated – 41% of which were female-led – that have raised a combined $869 million (€ 727 million) in total funding.

Here is our look at fintech innovation around the world.

Supply chain financing expert Taulia is making a $6 billion credit facility available to its supplier clients this week. The funds were secured through a JPMorgan-led consortium that also includes UniCredit, UBS, and BBVA.

The news comes after Taulia partner Greensill Finance filed for insolvency earlier this week due to its largest client, GFG Alliance, defaulting on its debts. Taulia expects that the credit facility will help its clients that relied on Greensill Finance by offering them access to a different source of liquidity.

To be clear, the financing is not funding for Taulia itself; it is funding to help suppliers on its platform that are linked to Greensill Capital clients.

“Taulia’s priority, first and foremost, has been to enable businesses both large and small to unlock liquidity trapped in their supply chain in order to invest, operate and thrive,” said Taulia CEO Cedric Bru. “In the current environment, with the potential loss of a funder, our commitment to providing choice has become even more paramount.”

Today’s financing is the continuation of Taulia’s strategic partnership with JPMorgan that began in April of last year. Last July, the financier participated in Taulia’s $60 million financing round that boosted the San Francisco-based company’s total funding to $177 million.

Friday is the last day to save big on your ticket to this month’s all-digital FinovateEurope 2021. Register by March 12th and save GBP 100.00 off the price of our three-day, all-access pass.

Kicking off on Tuesday, March 23rd and running through Thursday, March 25th, FinovateEurope will feature a combination of innovative fintech demonstrations, insightful presentations, and an engaging new platform that makes digital networking as easy as an in-person meet ‘n’ greet. Morning coffee and afternoon cocktail not included.

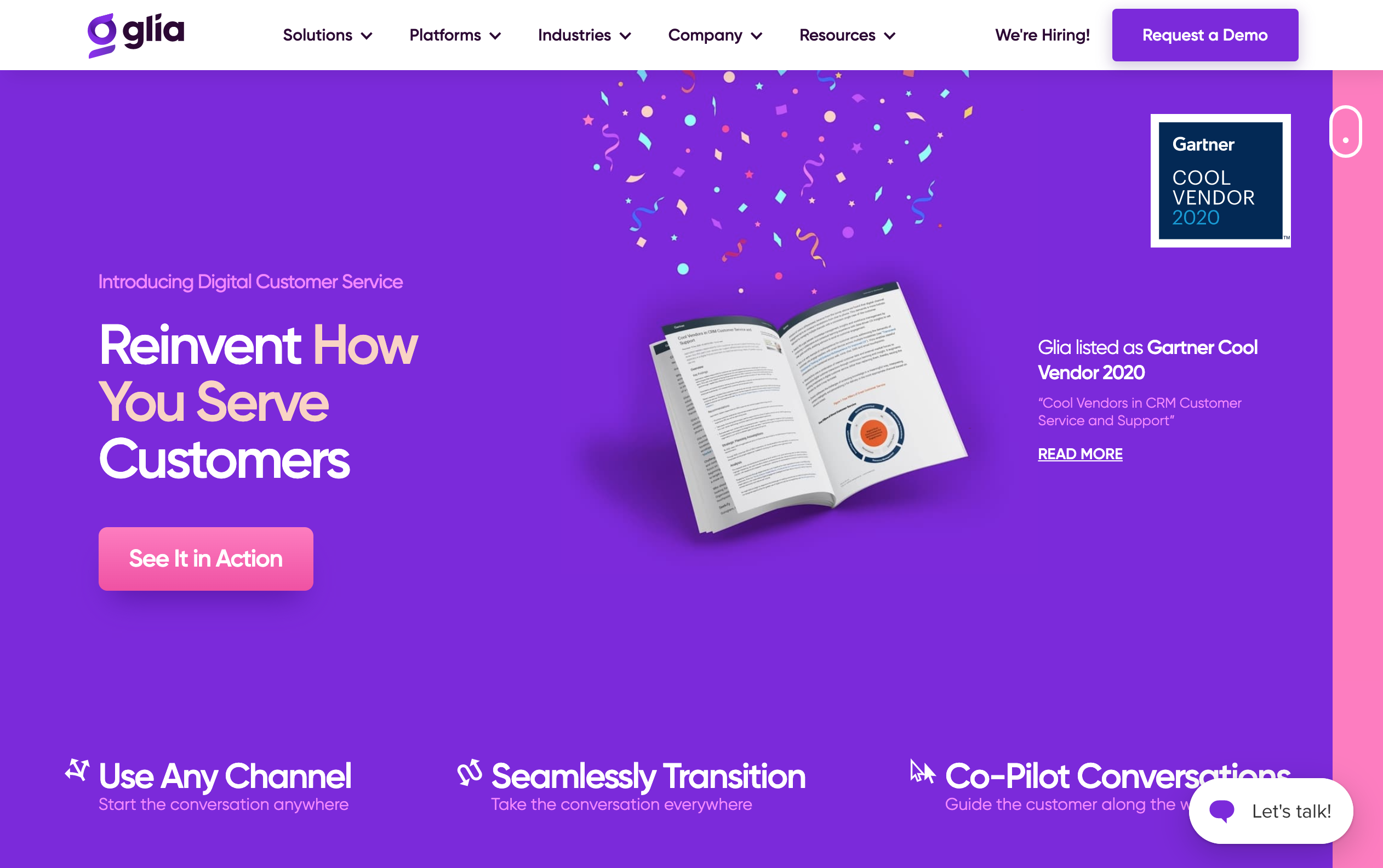

Glia is a digital customer service platform that connects financial institutions to their customers using chat, voice, video, co-browsing, and AI.

Features

Seamlessly move between modes of communication

Receive improved sales results and customer satisfaction via richer customer interactions

Deliver the best experience for customers and agents

Why it’s great Glia is seamlessly converting boring phone calls into exciting digital interactions and customer experiences.

Presenter

Dan Michaeli, CEO & Co-Founder Michaeli is the driving force behind Glia’s vision to combine the human touch with technology to create the best customer experiences. LinkedIn

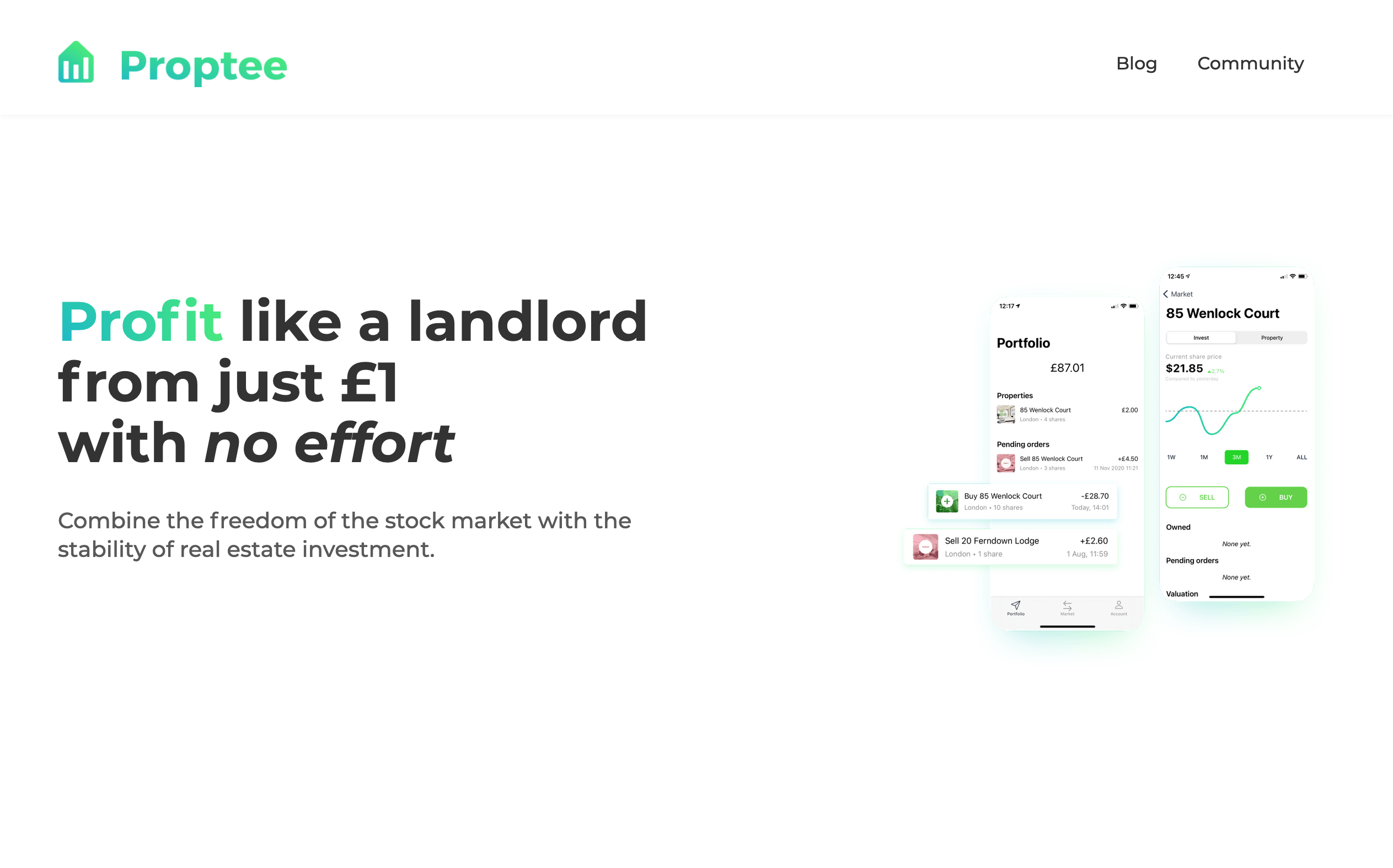

Proptee is a commission-free property stock exchange – the Robinhood of property investing.

Features

Invest in single properties with a tap of a button

Buy and sell shares just like on the stock market, completely free

Get paid a monthly dividend

Why it’s great Proptee – the future of property investing is here.

Presenters

Benedek Toth, CEO & Co-Founder Toth previously worked on PSD2 products at Intesa San Paolo. He founded and exited a honey manufacturing company at the age of 18 and graduated as an aerospace engineer. LinkedIn

Alexandru Rosianu, CTO & Co-Founder Rosianu was one of the first employees at Freetrade. He sold his first computer program at 12 and previously founded and exited Messenger For Desktop with more than 10 million downloads. LinkedIn

Cobase offers a multibank cloud solution for large corporates. The platform provides fully managed bank connectivity, a payment hub, and optional modules for cash management and treasury management.

Features

Single point of access to all banks and accounts for corporates

Cash visibility, control, and efficiency

Bank connectivity, payment hub, and optional cash and treasury management module

Why it’s great Banks can offer a white-labeled version to their clients under their own brand and use the technology to increase bottom line revenue without heavy investment.

Presenter

Jorge Schafraad, CEO Schafraad has worked in the transaction banking domain for more than 20 years. He has held various positions at different banks in channel management, IT, and innovation. LinkedIn

Luvleen Sidhu, CEO of BM Technologies (formerly known as BankMobile), is now one of the youngest female founders and CEOs of a public company.

Since she co-founded BM Technologies in 2014, the company has made major news headlines. We recently spoke with Sidhu to get the background behind some of those decisions and to get her opinion on what it takes to compete in the fintech world as an ethnic minority and a woman.

First off, give us some background on BM Technologies (BMTX) and how it differentiates itself from other challenger digital banking platforms.

Luvleen Sidhu: BM Technologies, Inc. (NYSE American: BMTX, BMTX.W) is among the first neobanking fintechs to go public and is one of the largest digital banking platforms in the U.S. (with over 2 million accountholders), providing access to checking and savings accounts, personal loans and credit cards. We are on a mission to utilize technology to provide millions of Americans with a better banking experience, especially around affordability, transparency and more consumer-friendly products. We are proud to share that we were named the “Most Innovative Bank” by LendIt Fintech in 2019 and we continue to stay true to our mission of being a customer-centric focused company committed to innovation, and financially empowering millions of Americans.

We are a profitable and high-growth company and have been able to build this strong foundation through our Banking-as-a-Service (BaaS) strategy, which enables the acquisition of customers at higher volumes and substantially lower expense than traditional banks. This allows us to provide low-cost banking services to low/middle-income Americans. Today, the BankMobile BaaS platform is provided to colleges and universities through BankMobile Disbursements and serves over two million account-holders, providing disbursement services at 722 campuses, covering one out of every three students in the U.S.

Additionally, BM Technologies executed an agreement with Google to introduce digital bank accounts, which will be available to its customers. We also expanded our white label strategy with T-Mobile for the launch of T-Mobile MONEY.

Tell us about why you chose to offer not only B2C banking products and services, but also banking-as-service tools?

Sidhu: When we launched our company over six years ago, we actually only had a B2C banking product. However, fairly early on, we realized we were not growing at the exponential rate that we had anticipated and our customer acquisition cost was high. This caused us to pause and reevaluate our strategy. We recognized that there was an opportunity to pivot our strategy to a B2B2C model where we could lower our customer acquisition cost to less than $10 and in return still deliver a tech-enabled banking experience to millions of Americans through our distribution partners. This has been critical in our growth and our success as a company.

BM Technologies has its roots in the traditional banking world, having been developed internally by Customers Bancorp. How did that relationship shape BM Technologies?

Sidhu: Customers Bancorp gave us an extremely solid foundation as a company. Even when we launched in 2015, Customers Bank had $6.5 billion in assets. My father, Jay Sidhu was then the CEO of Customers Bank and cofounded BankMobile with me. Richard Ehst, then President of Customers Bank, also helped guide me, along with other members of the company’s leadership team. Having the chance to work with banking veterans provided us with immense knowledge of the industry, which helped us be successful.

BM Technologies is one of the 11 financial institutions collaborating with Google to pilot its Plex bank accounts. What benefits does this partnership offer BM Technologies? Are there any challenges with the new partnership?

Sidhu: This collaboration is mutually beneficial and is differentiated from the others because of our unique college student acquisition funnel. This means we are bringing to Google Plex potentially millions of student customers.

For us, the collaboration offers additional brand equity since Google is one of the leading technology companies in the world and has chosen BM Technologies to work with.

Why did BM Technologies choose to go the SPAC route to become a public company? What opportunities will this offer?

Sidhu: We decided to go the SPAC route because it was a more efficient way for us to take the company public. Our ultimate goal is to add a new white-label partner and gain at least a million new bank customers each year and most importantly provide them with the most financially empowering banking experience. We also plan to use our new funds to continue to focus on innovations and expand our product offerings.

As not only an ethnic minority but also a woman, what have you learned about what it takes to compete in the fintech world?

Sidhu: It takes a lot of determination, flexibility and a “can-do” attitude. I have been raised by two parents who have always supported and encouraged me and given me the tools and resources to succeed. This has helped me throughout childhood and adulthood and has given me a strong foundation to launch my own company. “Never give up” is a motto that my father said to me since I was a young child and one that I truly believe in. There have been obstacles along the way, but by continuing on despite them and overcoming them, I feel I have been able to be competitive.

In general, what developments can we expect in the challenger banking space in 2021?

Sidhu: I think that challenger banks will continue to grow their customer base, becoming increasingly popular with consumers across the country. More and more people are turning to digital banking, and the pandemic accelerated this trend. Challenger banks are nimble and consistently creating new services, which are attractive to Americans. I also believe that more challenger banks will go public this year.

Consulting and IT services company NTT Dataannounced the launch of a new digital banking platform today. The new offering, Platea Banking, helps banks with digital transformation while maintaining their legacy technology.

Platea Banking helps retail banks take a platform-based approach to facilitate a customer-centric focus on the banking experience. The new platform offers banks access to NTT Data’s partner ecosystem and modules, including customer onboarding, lending, planning and financial management, card issuing and processing, payments, and others.

The open banking approach allows banks to select the features they need and move quickly through a platform-based approach that doesn’t tie them down to a single vendor.

“Technology plays a central role in helping banks innovate and deliver next-generation banking services to their customers,” said Global Head of NTT DATA’s Open Banking Practice Manuel Romero. “With consumers demanding digital banking experiences, it is imperative that banks act accordingly to respond [to] their needs. Platea Banking has been built to empower banks, providing them with a path to incorporate cloud-native technology to expand their business, as well as the ability to overcome obstacles such as scalability issues, legacy IT and compliance.”

Founded in 1988 and headquartered in Tokyo, Japan, NTT Data offers a range of IT services and solutions, including consulting, systems integration, and IT outsourcing, for multiple sectors. A Finovate alum, the company most recently demoed at FinovateFall 2019. Yo Honma is CEO.