This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Eltropy is introducing a governed agentic AI platform built specifically for credit unions.

The new platform enables credit unions to create, deploy, and supervise AI agents within defined operational and compliance guardrails.

By centralizing agent deployment and governance, Eltropy positions credit unions to scale AI safely and competitively, narrowing the innovation gap between smaller institutions and large banks with larger technology budgets.

Member communications platform Eltropy is launching an agentic AI platform specifically for credit unions this week. The tool offers a single location for credit unions, fintechs, and core banking providers to work collaboratively on an agentic AI project.

The platform allows users to create, govern, integrate, and deploy AI agents. The tool offers credit unions visibility into what an AI agent did, why it did it, what data it used, and how it reached its decision. Every AI agent is subject to standard operating procedures and authentication protocols, so the agents are unable to take actions outside of the procedures or data boundaries.

Additionally, Eltropy’s agentic AI platform offers organizations control over which employees are able to access and control the agents. “This ensures Agentic AI is innovative but controlled, powerful but predictable, open but always safe,” said Eltropy CEO and Co-Founder Ashish Garg.

Offering credit unions the ability to build and govern AI agents in-house reduces vendor sprawl and creates a structured distribution channel for fintech partners. Rather than layering solutions across consumer touchpoints, credit unions can centralize automation under a governed agent framework.

Crucially, Eltropy’s agentic AI platform positions credit unions to compete more effectively with large banks that have significantly larger IT and R&D budgets. By embedding auditability, authentication protocols, and role-based controls, the platform lowers the regulatory and operational risk that often prevents smaller institutions from deploying advanced AI tools.

“This is just the beginning,” said Abhishek Tiwari, Chief Product Officer, Eltropy. “For us, agentic AI is not about automation for its own sake, it’s about delivering measurable business outcomes. Our AI agents already authenticate members and provide account information, and we’re rapidly expanding into payments, loan system updates, collections workflows, and more. The goal is simple—drive real operational impact across the credit union. This is how agentic AI becomes real.”

Eltropy’s Agentic AI platform helps shift agentic AI from experimental chatbot deployments to core operational infrastructure. With AI advancements moving rapidly and traditional financial institutions struggling to keep up, agentic AI platforms like Eltropy’s will be crucial fintech infrastructure as the industry continues to evolve.

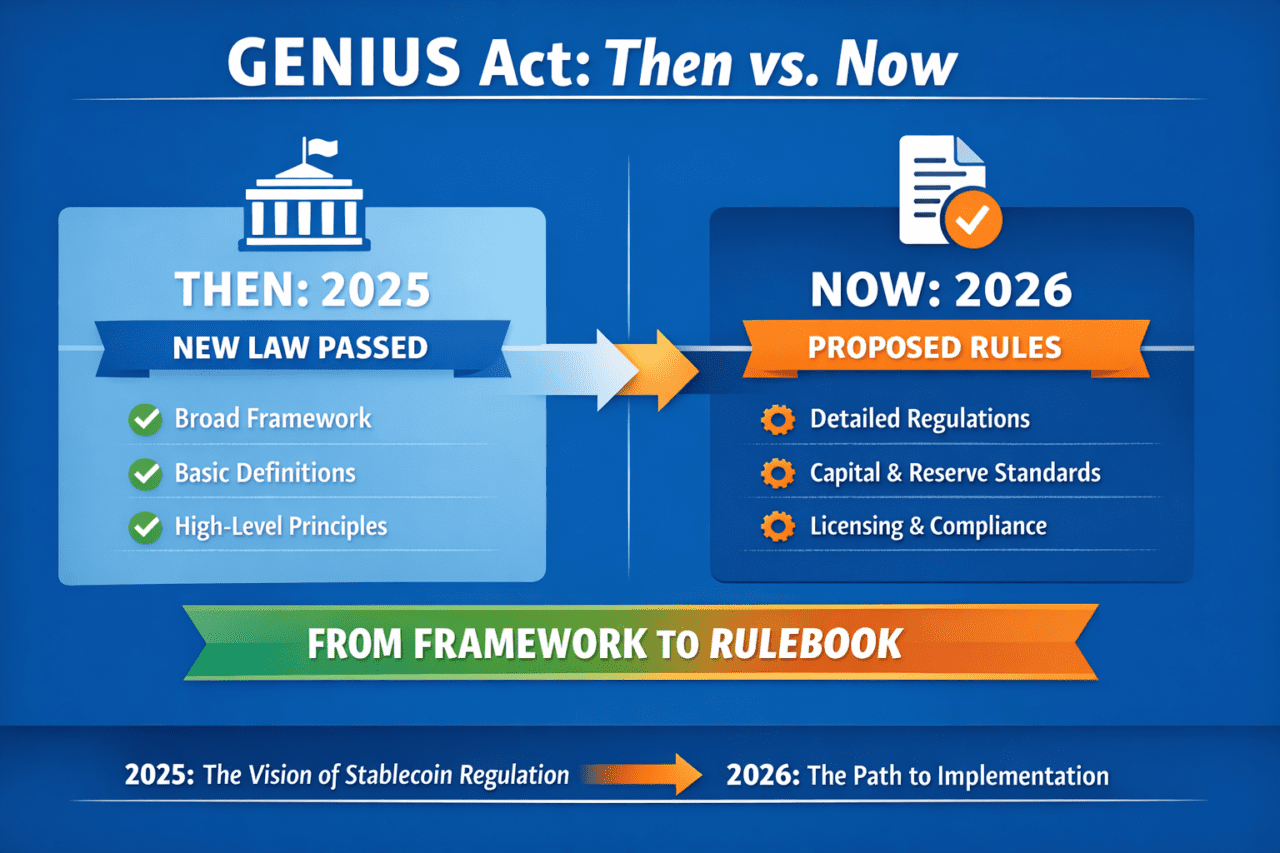

In July of 2025, the GENIUS Act, the first comprehensive federal framework for stablecoins, became law. Last week, the US Office of the Comptroller of the Currency (OCC) issued a notice of proposed rulemaking (NPRM) to implement the GENIUS Act’s requirements for payment stablecoin issuance and related activities.

While the new proposed rulemaking makes the GENIUS Act a reality instead of just a statute, it doesn’t change the intent of the GENIUS Act. It operationalizes the GENIUS Act by creating a dedicated regulatory section for issuers, establishing the licensing mechanics and timelines, forming the capital and operational requirements, and stipulating foreign issuer treatment.

2025 GENIUS Act

The 2025 GENIUS Act had a crucial role in setting the stage for the legality of stablecoin payments. It defined what a payment stablecoin is and who is allowed to issue stablecoins. It stipulated that stablecoins require full reserve backing with liquid assets, prohibited interest-bearing stablecoins, and created a federal and state regulatory structure. Overall, the purpose of the 2025 Act was to set guardrails. With this year’s notice of proposed rulemaking, the OCC is bringing a more procedure-focused approach.

New dedicated regulation

As mentioned above, the OCC is operationalizing the GENIUS Act in four major ways, the first of which creates a dedicated regulatory section (12 CFR Part 15) that establishes standards and requirements for stablecoin issuers. Creating the new part in the CFR changes the GENIUS Act from a written requirement into more enforceable supervisory standards.

New licensing

Additionally, new licensing mechanics come into play that create a defined pathway for entering the stablecoin market. Under the OCC’s proposal, prospective permitted payment stablecoin issuers (PPSIs) must submit a formal application outlining their business model, governance structure, reserve management approach, technology infrastructure, and risk controls. The proposal establishes what constitutes a “substantially complete” application and outlines supervisory review expectations. The new licensing process makes stablecoin issuance similar to applying for a bank charter, rather than launching a new product.

New capital and operational requirements

Similarly, the 2026 capital and operational requirements make stablecoin issuance look more like running a regulated financial institution than launching a new product. While the 2025 GENIUS Act focused primarily on reserve backing, the OCC’s 2026 proposal stipulates minimum capital thresholds, liquidity buffers beyond token redemption obligations, formal governance structures, internal control standards, and explicit third-party risk management expectations.

Established banks already have these processes embedded into their operating procedures. For fintechs, however, the new requirements may call for meaningful investment in governance, compliance documentation, and risk oversight infrastructure. These new formalities raise the cost of entry into the stablecoin issuance market.

New foreign issuer treatment

The OCC’s 2026 proposal incorporates foreign issuer rules directly into the scope of the plan, meaning that non-US players can no longer rely on regulatory ambiguity as a strategy to enter the market.

Just as the proposed framework requires US issuers, foreign issuers serving US users would still be required to apply for OCC registration, provide evidence of Treasury’s comparability determination, consent to US jurisdiction and OCC access to records, and meet requirements around US-available reserves (subject to any reciprocal arrangement).

This limits offshore entities operating in regulatory gray zones while marketing to US customers. The new rulemaking makes clear that global stablecoin players will need to align with US supervisory expectations, creating a more demanding roadmap for cross-border participation.

What this means for banks and fintechs

The proposed rulemaking makes clear that stablecoins are moving closer to the core of regulated banking activity and are increasingly being treated as part of the financial infrastructure rather than as a crypto experiment. As stablecoin issuance begins to resemble supervised activity, banks enter the conversation from a position of structural advantage. With governance frameworks, capital planning, risk management, and compliance processes already embedded in their operating models, traditional financial institutions may be better positioned than fintechs to comply with the regulatory demands of stablecoin issuance.

As compliance costs associated with stablecoin issuance rise, so does the barrier to entry. Not every fintech will have the appetite or resources to meet capital, liquidity, and supervisory expectations. The increased friction, however, brings institutional credibility to a payment type once considered adjacent to Bitcoin. This credibility lowers the risk for issuers as well as for end consumers and will ultimately transform stablecoins into an everyday tool.

Virginia-based cash handling company The Brink’s Company (Brink’s), has agreed to acquire NCR Atleos in a deal valued at around $6.6 billion.

The deal will combine Brink’s global cash management expertise with NCR Atleos’ ATM management and services as well as its ATM network and ATM-as-a-Service (ATMaaS) solutions. Adding NCR Atleos’ capabilities will allow Brink’s to offer complementary products, services, and software that provide banks and retail customers with an even broader variety of cash management solutions.

“This acquisition further supports Brink’s ability to deliver enhanced customer solutions and accelerates our value creation strategy,” said Brink’s President and Chief Executive Officer Mark Eubanks. “NCR Atleos is a partner we know well, and our business cultures are closely aligned around customer success, continuous improvement, and managing the interface between physical to digital payments to enable ease of cash acceptance and use. By combining our organizations, we gain critical scale and complementary, integrated capabilities to drive our ambitious growth strategy and provide new levels of service to our global customer base.”

Founded as NCR Corporation in 1881, the firm spun out NCR Atleos in October of 2023 to run as an independent company focused on ATMs. Today, NCR Atleos has an installed base of approximately 600,000 ATMs, 78,000 of which it owns and operates in high traffic retail locations. Headquartered in Atlanta, Georgia, NCR Atleos employs 20,000 people across the globe to facilitate hardware, software, and service for its line of ATM-related technology.

This is a massive win for Brink’s, and not simply because it is buying up one of the oldest firms in financial services. The acquisition offers the company a greater geographic footprint, tapping NCR Atleos’ client base located across more than 140 countries. Adding NCR Atleos’ ATM software, services, and installed ATMs to its own armored transport services will enable Brink’s to offer a more holistic and vertically integrated set of services and products.

Once combined, Brink’s anticipates it will generate approximately $10 billion in total revenue.

“This transaction represents a strategic opportunity for NCR Atleos,” said NCR Atleos CEO Tim Oliver. “The extraordinary efforts of the NCR Atleos team over the two years since our separation from legacy NCR have strengthened our leading ATM installed base, sustained best-in-class service levels and introduced innovative products. Combining the complementary service-led businesses of Brink’s and NCR Atleos will enable us to enhance offerings to financial institutions and retailers, and create more opportunities for our employees.”

DriveWealth will integrate Kalshi’s regulated prediction markets into its brokerage-as-a-service platform, enabling fintechs to offer event contracts alongside stocks and ETFs.

Kalshi, which processes over $100 billion in annualized volume, is expanding distribution through DriveWealth’s brokerage infrastructure.

As prediction markets move into the financial mainstream, event contracts are emerging as a new tradable asset class that could follow the adoption path of options and crypto.

Digital trading and brokerage company DriveWealth is teaming up with prediction market platform Kalshi in a move to capitalize on the growing interest in events contracts. The New Jersey-based company plans to integrate Kalshi’s event contracts into its brokerage platform.

The integration allows clients using DriveWealth’s brokerage-as-a-service platform to offer event-driven markets alongside more traditional equities, ETFs, and other traditional asset classes within the same interface.

Kalshi allows users to trade on the outcome of real-world events such as elections, economic indicators, weather, sports, and more in a fully regulated environment. Because it offers investment opportunities based on highly publicized events such as sporting and political events, Kalshi brings an approachable new asset class that has quickly become mainstream. Kalshi currently attracts over $100 billion in annualized volume.

Rather than operating purely as a standalone trading venue, Kalshi has increasingly positioned itself as infrastructure for fintech platforms seeking to add regulated event contracts to their product mix. “DriveWealth’s global reach and embedded brokerage infrastructure make them an ideal partner to Kalshi,” said Kalshi Co-founder and CEO Tarek Mansour. “Our goal is to provide leading fintech platforms with more access to regulated prediction markets.”

The new integration also places DriveWealth in the footsteps of Robinhood, which began integrating Kalshi’s prediction market platform into its investing app in August of last year. Other investment platforms leveraging Kalshi include WeBull and PrizePicks.

Offering an increasingly popular asset class like prediction markets enables DriveWealth clients to attract new users while deepening engagement with existing investors who may currently trade on external platforms. For end users, consolidating multiple investment opportunities within a single platform simplifies portfolio tracking and performance monitoring across markets. For DriveWealth clients, the addition modernizes their product offering while strengthening customer retention and growth.

As prediction markets gain regulatory clarity and mainstream traction, DriveWealth sees the Kalshi integration as a way to future-proof its brokerage infrastructure. “Our integration with Kalshi strengthens our ability to deliver cutting-edge market opportunities to our partners,” said DriveWealth CEO Naureen Hassan. “DriveWealth was built to power the future of global investing through scalable, API-driven technology, and Kalshi’s forward-thinking approach to market design makes for a natural fit. Together, we’re uniquely positioned to equip our partners with the latest financial innovations and next-generation market access for their clients.”

Overall, prediction markets are on a major growth trajectory this year. Prediction markets have evolved from niche academic tools and offshore betting platforms into regulated investing tools with growing institutional backing.

As retail investors increasingly seek alternative ways to grow their funds, prediction markets create a new category of tradable risk exposure. If distribution partnerships like those with Robinhood and DriveWealth continue to scale, event contracts could follow a trajectory similar to options or crypto that were once fringe, but are now embedded into modern product stacks.

If you missed out on FinovateEurope earlier this month, you don’t have to feel left out any longer. The 22 demo videos are now live (and free to watch!) on the Finovate website and on Finovate’s YouTube channel.

Each seven-minute video offers a fast and efficient way to catch up on the latest new launches in fintech. We’ve highlighted the three Best of Show-winning demos below to get you started.

For more coverage of on-stage content at FinovateEurope, check out our post-show analysis. And if you don’t want to miss out on the live action next time around, be sure to register for FinovateSpring, taking place on May 5 through 7 in San Diego, California. We’ll see you there!

Mambu is expanding its payments hub globally, launching in new markets across EMEA, Latin America, and Asia Pacific.

The global move comes in response to growing demand from banks and fintechs operating across multiple payment schemes and jurisdictions.

Mambu’s API-first payments hub extends the company’s composable core banking offering to help institutions modernize and scale payments alongside lending and deposits.

Cloud banking platform Mambu is expanding its payments hub into new global markets this year, with plans to launch in additional markets in EMEA, Latin America, and Asia Pacific.

Mambu said demand from global banks and fintechs operating across multiple payment schemes and jurisdictions drove this week’s expansion.

Mambu was founded in 2011 and emerged as one of the pioneering players to move banking software to the cloud. The company’s composable banking approach offers a plug-and-play approach to core banking that helps firms shift away from legacy platforms and build to scale.

As payments become a more central part of Mambu’s long-term platform strategy, the company is positioning its payments hub as a natural extension of its core banking business. “For years, Mambu’s core banking platform has long been the engine behind hundreds of the world’s most innovative financial players. Payments are now a cornerstone of our strategy as we help institutions navigate the industry’s growing complexity,” said Mambu VP of EMEA Leon Stevens. “We are poised to help modernize core infrastructure and accelerate innovation across the entire banking stack—from lending and deposits to payments and beyond.”

Launched in 2025 and fueled by the acquisition of payment gateway company and Finovate alum Numeral, Mambu’s payments hub aims to help firms modernize their entire payments stack with an API-first payments hub. With native straight-through processing, orchestration, liquidity, reconciliation, fully-managed connectivity to local and global payment schemes, and composable payment workflows, Mambu’s payments hub facilitates a faster, lower cost approach that can easily be scaled.

From an execution standpoint, Mambu sees growing complexity across global payment ecosystems as a key driver behind the expansion. “Payments are becoming more global and more local, more interconnected and more fragmented, and now move in real-time,” said Mambu VP Payments Edouard Mandon. “This complexity makes scaling payments across multiple markets challenging. To solve this, we have expanded our payments hub to give institutions access to local schemes while maintaining a consistent integration and operational experience. This continues our investment in connectivity at scale, which increasingly includes next-generation rails, to deliver payment solutions truly built for the future.”

Since launching, Mambu’s payments hub processed seven times as many payments in 2025 than what it did in 2024 when it was under the Numeral brand. Also in the nine months since launch, the company added European and global financial institutions, including Western Union, BCB Group, Flowe, and Spendesk.

As payments become increasingly global, the subsector is becoming a strategic battleground for banks as they seek to grow and modernize their technology stacks, especially as payments mix real-time, legacy, and new payment rails across multiple regions. Offering the ability to standardize integration while natively embedding payments into its composable banking platform will ultimately help Mambu’s clients scale faster while limiting complexity.

Mambu plans to continue expanding connectivity to major payment rails worldwide in an effort to help banks support payment schemes through a single platform. The company notes that its geographical expansion marks the next phase of its international growth, especially as it further builds out global core banking and payments infrastructure.

Experian has acquired AtData, US data and intelligence company.

The deal adds AtData’s more than 10 billion global email addresses to strengthen Experian’s identity and fraud capabilities.

Experian expects that integrating AtData’s real-time email intelligence into its broader consumer data and analytics platforms will support its clients’ AI-driven decisioning strategy.

Data analytics and consumer credit reporting company Experianannounced a key acquisition today. The Ireland-based firm has acquired US data and intelligence company AtData for an undisclosed amount.

AtData was founded in 1999 as TowerData, then combined with FreshAddress in 2021, and rebranded to AtData a year later. The company offers email address technology that helps thousands of organizations take control of their first-party email data collection to fuel marketing and minimize fraud.

Experian expects the acquisition to expand its existing data and identity assets by adding more than 10 billion email addresses of people across the globe. The company will combine AtData’s real-time data signals with its consumer data, analytics, and decisioning platforms to better allow its clients to identify, authenticate, and engage their customers across multiple channels.

For Experian, the acquisition is about strengthening identity resolution at a time when real-time signals and AI-driven decisioning are becoming table stakes. “Differentiated data and real-time identity signals are the ultimate advantage and increasingly important in the age of AI,” said Experian North America CEO Jeff Softley. “AtData brings deep email intelligence into our platform and further fuels our AI strategy. This isn’t just about adding capabilities; it’s about creating an integrated, durable identity solution that helps our clients deliver better experiences at every stage of the customer journey.”

Beyond expanding Experian’s identity stack, the deal highlights how the company is positioning itself amid an unsettled open banking landscape. As Section 1033 of the Dodd-Frank Act remains tied up in a legal and regulatory debate, and data-sharing standards continue to vary by institution and use case, financial services firms are seeking more resilient ways to identify, authenticate, and engage customers. By expanding its identity stack beyond traditional credit data to include real-time email intelligence, Experian is betting on first-party identity as foundational infrastructure for AI-driven decisioning even as open banking remains in flux.

The acquisition comes 15 years after the two companies first teamed up. For AtData, the deal represents a natural evolution of a long-standing relationship between the two companies. “Our goal has always been to help our customers optimize their first-party email data collection, accelerate their marketing performance, minimize the cost of fraud, and drive their data-oriented business strategies,” said Tom Burke, CEO of AtData. “Experian has consistently set the standard for using data to drive trusted outcomes for businesses and consumers. Joining Experian enables us to combine complementary strengths and deepen the intelligence capabilities that power confident, real-world decisions.”

Founded in 1980 and originally known for its consumer credit reporting, Experian has extensive access to data and has added fraud prevention offerings, identity theft protection, credit building tools, and a loan comparison marketplace. On the commercial side, Experian provides a range of services for small businesses, including business credit reporting, marketing products and services, debt collection tools, and more.

Experian is headquartered in Dublin, Ireland, and is listed on the London Stock Exchange under the ticker EXPN. The company has a market capitalization of $31.6 billion.

Spreedly is partnering with Paysafe to integrate Paysafe’s merchant acquiring capabilities into its global payments orchestration platform.

The partnership gives merchants more flexibility by combining Paysafe’s gateway and acquiring tools with Spreedly’s open payments architecture.

The move will help modernize payment stacks with a modular approach.

Open payments platform Spreedly is partnering with payments processing fintech Paysafe, integrating Paysafe’s merchant acquirer capabilities into its own global payments orchestration platform.

Paysafe will process credit card and debit card payments for Spreedly’s online merchant clients doing business across Europe, North America, and other geographies. Under the agreement, Paysafe is processing card payments for multiple online trading brokers and financial services companies and plans to onboard additional merchants launching before the end of 2026.

From Paysafe’s perspective, the partnership expands the reach of its gateway technology into Spreedly’s global orchestration layer, particularly among online trading brokers and financial services companies operating across multiple markets. “With the Paysafe Gateway, a trusted solution for card payments among forex and financial trading brokers and a wide range of other industries, we look forward to strengthening Spreedly’s Open Payment Platform and streamlining payments for its merchant users and their customers,” said Paysafe Chief Revenue Officer Rob Gatto.

This integration is meaningful for merchants operating across borders, as payments complexity continues to grow with gateway fragmentation and regulatory changes. Combining Paysafe’s tools into Spreedly’s offering brings a modular, open payments stack that allows merchants to adapt without rebuilding their infrastructure.

Spreedly’s Open Payment Platform is a payment orchestration stack that offers merchants more than 140 gateway connections to more than 40 payment methods. Integrating the Paysafe Gateway allows Spreedly to process online card payments for merchants and their customers.

For Spreedly, adding Paysafe reinforces the company’s broader strategy of giving merchants more choice and flexibility across payment providers and geographies without locking them into a single acquirer or gateway. “At Spreedly, we believe open payments drive better outcomes for merchants. Bringing Paysafe onto our Open Payments Platform expands optionality for our customers and reinforces our mission to provide a flexible, future-ready infrastructure for global commerce,” said Spreedly Partner Strategy Director Michael Rokos.

Founded in 1996, UK-based Paysafe has 30 years of experience providing online payments tools for forex and financial trading brokers, as well as merchants in iGaming, ecommerce, travel, and hospitality. The company connects businesses and consumers across 260 payment types in over 48 currencies around the world. Paysafe processes an annualized volume of $152 billion in transactions and is publicly listed on the New York Stock Exchange under the ticker PSFE with a market capitalization of $350 million.

Spreedly was founded in 2007 to help merchants build their payments stack on a single platform. The company’s payment orchestration stack processes over $60 billion in gross merchandise value on behalf of more than 400 customers across 100+ countries. Spreedly also offers fraud prevention, payment optimization tools, and more. Among the company’s clients are BMW, CLEAR, HBO Max, Hopper, Lemonade, Getty, Warner, The New York Times, and others.

It’s the last week of February, which means we have one more month to wrap up any Q1 goals. Below, we’ve aggregated the top news in fintech for the week. We’ll continue to add more announcements as the week progresses.

This article is brought to you in collaboration with Gregory.

AI is rapidly reshaping the competitive landscape in banking, and for many institutions, the real challenge lies not in experimentation, but in implementation. Richard Davies, CEO of Allica Bank, has been focused on exactly that: how to successfully deploy AI across an organization and drive meaningful adoption at scale.

Founded in 2020, Allica is a digital bank focused on established small and medium-sized businesses. To date, it has lent over £3 billion and been twice named by Deloitte as the UK’s fastest growing technology company. In 2025 the Financial Times identified it as the second fastest growing company in Europe.

Richard delivered a fascinating keynote address at FinovateEurope, titled: “Successfully Implementing AI & Scaling Adoption: What Are the Challenges Around Rolling Out to Production?”. Afterwards, we sat down with him to talk about what it really takes to embed AI into a bank’s operating model.

Tell us a little more about your role as CEO of Allica Bank and what you’re focused on at the moment?

Richard Davies: Allica is a fintech bank focused on established small and medium-sized businesses. We typically define that as businesses with five or more employees or at least £500,000 in revenue. So we’re not talking about the very smallest microbusinesses, but those that are at a point where things start to get more complex and there are multiple staff to support.

We find these businesses fall into a gap between the corporate banking divisions and retail banking divisions of the major banks. That’s the space we focus on.

We have been building Allica for five or six years now and provide a full stack of services, including current accounts, cards and all types of lending. Increasingly, we are moving into financial operations areas such as spend management and cash flow forecasting. Alongside that, we have been thinking hard about how we can apply AI to power many elements of what we do across the organisation.

In your keynote, you spoke about successfully implementing AI and scaling adoption. What do you see as the biggest challenges for banks when it comes to rolling AI out in practice?

Davies: I would group it into three main areas:

First, ensuring that AI adoption happens across the whole company, rather than sitting in an innovation lab or small specialist team. A big focus for us has been getting people bought in, upskilled and confident, and encouraging teams to create their own simple, agentic use cases. I am a big believer that bottom-up adoption tends to win over purely top-down mandates.

Second is software engineering and product development. Around a third of our staff are in engineering, and that is probably the area that has seen the greatest progress in AI tooling. We have focused on helping people move towards more T shaped or full stack roles, and ensuring our tech stack is AI enabled to unlock significant productivity gains. Depending on what you measure, we are seeing productivity improvements of two to ten times.

Finally, there are more complex agentic use cases. We have specialized teams working on these, and we have been learning a lot over the past two years about what it takes to get them live in production. It’s exciting because beyond engineering, you start solving real world problems that consume a lot of human time and can be inconsistent when done manually.

A lot of banks are investing in AI at the moment. How should they decide where it makes the most sense to focus first?

Davies: My view is that you should not overly narrow your focus. If you pick two areas, you are neglecting ten others, and those areas will fall behind.

Perhaps I have the luxury of leading a fintech organization that is naturally inclined towards this, but I think AI needs to be embraced across the company. Where you do need focus is on infrastructure, including data quality, enabling access to different AI models and ensuring that is done company wide.

If I had to pick one area with immediate and certain benefit, it would be engineering. The productivity unlock in software development is huge. If teams are still working in traditional ways, they need to move quickly, not just for the company’s benefit, but for their own careers. The industry is shifting rapidly, and people need the skills and experience to keep up.

Beyond the technology itself, what changes do banks need to make internally for AI to really become part of how they operate?

Davies: Culture is a big part of it. People need to lean into it. You need the infrastructure in place, as well as training and upskilling so people feel confident using AI.

At the same time, organizations need to remain risk aware. Different AI use cases carry different risks, and teams need to understand those.

In many ways, it’s similar to previous organizational transformations, such as moving from traditional waterfall practices to agile. The enablers are not conceptually different, but it does require deliberate leadership and a clear view of how you enable the organization to change.

From what you’ve seen at FinovateEurope so far, what themes or conversations around AI in banking have stood out to you the most?

Davies: Some of the most interesting conversations have been happening off stage. Recently, we have seen software company valuations come under pressure following major AI model releases, with the view that people can now build their own software more easily.

At the same time, traditional banks have re-rated quite significantly over the past year. In the UK, share prices are up roughly 80 percent. It creates an interesting dynamic.

Fintech has at times in the past been viewed by investors as a poor relation to software, but in reality, building a fintech is much harder than building a pure software company. You have complex regulatory requirements and balance sheet considerations that software firms do not.

It feels like there may be a shift happening in the relative valuation of where companies with real assets versus asset light software companies. For many fintechs, particularly those with strong fundamentals, that could ultimately be a net positive.

FinovateEurope 2026 wrapped up last week, but the fintech conversations are still flowing across social media. The two-day event was packed with meaningful conversations, fast-paced demos, a reunion of familiar faces, and new connections.

And while speakers and attendees were busy talking and learning about all things fintech and banking, Finovate’s photographer was capturing the event in more than 1,000 photos.

The photos are broken down into three categories, and we’ve pulled in a few photos as well as highlights to help summarize FinovateEurope via pictures. If you’re looking for a full content summary, check out our event summary blog post.

Some of the best discussions happen off stage. And with almost a dozen networking sessions baked into the event, there were a lot of valuable ideas exchanged in the hallways and on the networking floor. Heightening this experience were a live caricaturist and, even though fintech has a magic of its own, a magician.

Between panel discussions, fireside chats, and keynote presentations, the FinovateEurope stage hosted some of the brightest minds in fintech (and I’m not just saying that because I was on stage). We heard from founders on their biggest challenges, venture capitalists on the state of funding as we move into 2026, and bankers on how they actually measure the value of AI pilots.

The more than 20 companies that demoed their newest technology on stage showcased some of the most cutting edge ideas in fintech. From identity verification to core modernization, banks and fintechs face a lot of challenges. These fintechs took the stage to show their newest technology in under seven minutes.

If you attended FinovateEurope in London last week, you may have noticed that the energy of the event felt different.

In previous years, the conversation leaned heavily toward experimentation. This year, it shifted toward execution. Across the demo stage, panel sessions, and hallway conversations, it was clear that fintech is maturing. And that maturity is reshaping how banks create, partner, and serve customers.

AI moves from experimentation to operationalization

Agentic AI dominated the agenda in a pragmatic way that eschewed hype for reality.

Speakers discussed the importance of governed agentic AI that protect users with guardrails, auditability, and human oversight. Among these protective barriers, trust, explainability, and regulatory alignment were highlighted as central design principles when implementing agentic AI tools. It is clear that the conversation has shifted from “Can AI agents work?” to “How do we deploy them safely inside regulated institutions?”

Fraud and identity also pulsed throughout conversations about AI, as new technologies are evolving these elements from singular checks to continuous behavioral intelligence. The topics of responsible AI and the impact of AI on the future workforce were also front and center, with standing-room-only crowds on the AI stage discussing governance, skill atrophy, and ethical deployment.

As one attendee said, “When it comes to AI, speed may win attention, but trust wins the relationship.”

Customer experience: from product-centric to embedded

In the Analyst All-Stars session, much of the conversation centered on customer-centricity. Banks are moving from product-centric models to embedded, predictive, and contextual financial experiences.

In my panel discussions on embedded and challenger banking, we explored how digital lending is moving closer to the customer as part of the journey. Executing embedded lending is about being present at the moment of need in the correct channel.

Other panel discussions and keynotes offered more insights around improving the customer experience:

Customers compare bank journeys to every digital experience they have.

Onboarding remains a major friction point.

Personalization and channel choice are now expectations.

Balancing compliance, risk, and conversion requires smarter orchestration.

Challenger banks continue to influence customer expectations, especially when it comes to how they think about brand and community. Many conversations along these lines considered the benefits of collaboration. In fact, over 70% of fintech product launches now involve strategic partners, and panels on platform banking reinforced that partnerships are structurally necessary to compete.

Payments, tokenization, and agentic commerce

Many of the payments discussions highlighted the fact that instant payments are becoming mainstream, but geography and behavior matter. By increasing the speed of payments, fraud also accelerates. This shift is pushing institutions toward implementing “friendly friction,” with biometrics and AI-powered detection.

While not highlighted quite as much, the topic of agentic commerce was brought up in the payments track. If (or when?) bots become customers, banks must rethink identity verification and value-chain control. With ISO 20022 becoming the common language for blockchain-based value exchange, tokenization and programmable money will become key pieces of infrastructure.

Capital is maturing

Most of the investors on the networking floor and up on stage agreed that fintech funding rebounded globally in 2025. Today, capital efficiency and unit economics have returned to the center of strategy. To keep up, founders are tightening business models and refining their distribution strategies. Additionally, panelists mentioned that community-backed capital structures, which add accountability, are increasingly being used alongside traditional venture funding.

Beyond the stage

The Women in Fintech panel was one of the most popular sessions. The overflowing crowd was a reminder that inclusion plays a role in organizational growth. Geopolitical risk, national security strategy, and regulatory shifts also underscored the fact that financial services innovation does not happen in isolation.

Thanks to all of our speakers who braved the stage to share their insights, and to everyone who attended. You all make up such a great community and we truly could not do this without you all!