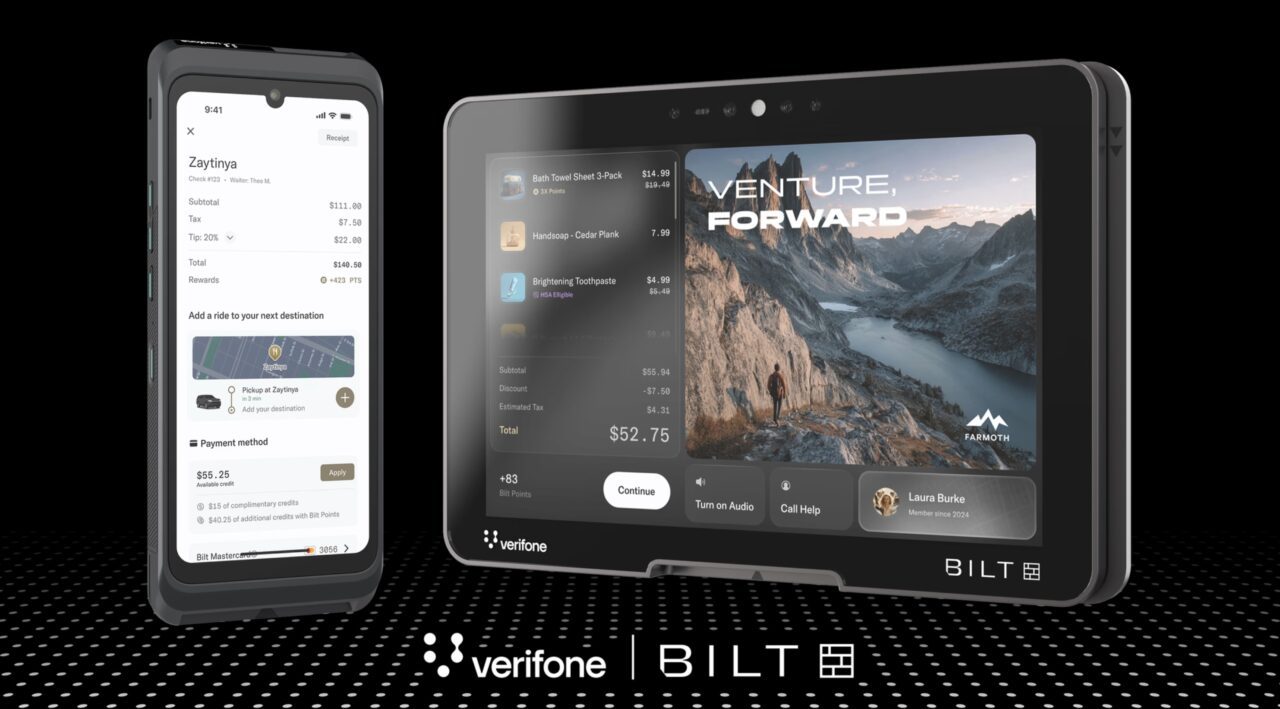

- Bilt is partnering with Verifone to embed its loyalty and customer experience platform directly into Verifone Victa point-of-sale devices and will allow merchants to recognize and engage members at checkout with personalized experiences.

- The integration requires no new hardware and works across multiple payment providers.

- For Bilt, the deal creates a scalable distribution channel through Verifone’s point-of-sale devices, significantly expanding its merchant reach.

Loyalty platform Bilt announced it is teaming up with Verifone this week. The partnership will integrate Bilt’s experience and loyalty platform into Verifone’s Victa point-of-sale hardware devices.

The nine Verifone Victa point-of-sale devices range from enterprise-grade registers to small mobile and portable devices. Integrating Bilt’s loyalty tools into these devices will help merchants engage customers at point of sale by embedding personalized experiences and member identity into the payment experience.

The native integration, which won’t require additional hardware investment or changes to existing workflows, is designed to be easy for merchants to adopt. It works across multiple payment providers as an out-of-the-box tool that has already been tested and certified, which lowers implementation risk and shortens the time it takes for businesses to go live with Bilt’s customer experience tools.

“By embedding Bilt’s loyalty technology directly into the Verifone platform, delivered through Victa, we’re enabling merchants to elevate customer engagement without adding hardware or disrupting existing workflows,” said Verifone CEO Himanshu Patel. “Through the Verifone gateway, merchants get a pre-certified, enterprise-grade integration that accelerates time to market and is already proven at scale—while unlocking access to Bilt’s member base.”

Bilt was founded in 2021 to offer a loyalty rewards program and credit card that allows renters to earn points when they pay their rent, building credit with every payment. With no annual fee, the Bilt Mastercard credit card also allows cardholders to earn points on select dining experiences, rideshare purchases, and travel purchases. These points can be redeemed for travel, fitness classes, home decor, and even a down payment on a future home.

For Bilt, today’s partnership has the potential to massively increase its merchant footprint by placing its loyalty and customer experience tools directly into widely deployed point-of-sale hardware. By meeting merchants where transactions already occur, Bilt can scale distribution without requiring merchants to adopt new systems or change how they operate.

This is big news for Bilt. The partnership has the potential to move Bilt from a card-centric loyalty program into embedded commerce infrastructure that meets consumers and merchants directly at the point-of-sale.

“Partnering with Verifone—the gold standard in payment hardware—means our merchant partners get best-in-class customer experience technology that’s already delivering better reviews, faster operations, and happier customers,” said Bilt Founder and CEO Ankur Jain. “This partnership with Verifone brings our proven membership and loyalty tech right to the point-of-sale—dining, fitness, retail, you name it. Together, we’re completely changing how merchants connect with their customers. Now they can automatically recognize and reward people at checkout, which means every transaction becomes a chance to build real relationships and unlock new revenue with personalized offers.”

Bilt will begin rolling out the Verifone integration with select restaurant groups, and will make its tools more available to a broader set of merchants throughout 2026.