This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

2024 marks the 90th anniversary of the Federal Credit Union Act. Signed into law by President Franklin Delano Roosevelt in the summer of 1934, the Federal Credit Union Act authorized the formation of federally chartered credit unions in every state.

How are credit unions faring 90 years later? Today, total assets in federally insured credit unions sit at more than $2.3 trillion as of the first quarter of this year. That figure represents a year-over-year increase of 4.4%. Membership in federally insured credit unions has also picked up year-over-year, with membership topping the 140 million mark in Q1 of 2024.

But credit unions face significant challenges. Digital transformation is neither cheap nor easy. Competition with larger financial institutions–as well as Big Tech and Big Retail–has forced credit unions to seek new ways to better serve and engage their members.

FinovateFall 2024’sCredit Union Spotlight, presented by Curql, is designed to help credit unions overcome these challenges, offer new innovative solutions, and grow their membership ranks. The session, Wednesday afternoon, on September 11, will enable credit union executives to connect and speak intimately with a small, curated group of fintechs who are specifically focused on serving credit unions. The session will feature a series of rotating roundtables to give participants an ideal opportunity to interact, ask questions, and share best practices.

“It’s an exciting time to be a credit union looking at fintech,” said Greg Palmer, host of Finovate. “More and more innovators are creating solutions with credit unions in mind, and we’re delighted to be able to showcase some of those solutions to a room full of people who can start using them right away.”

Curious? Here are three reasons why you should attend our Credit Union Spotlight if you care about the future of credit unions in America.

Transformation

Digital transformation is reshaping businesses across industries. Credit unions are no exception. Moreover, many of the forces that are driving digital transformation in other industries are especially relevant to credit unions. Digital technology enables credit unions to offer more personalized services and better engage members. It also enhances processes to ensure that members’ data is secure, making the organization more efficient and capable of serving their current members more comprehensively.

And while every credit union is unique, there are commonalities when it comes to the digital transformation journey. Here, the lessons of those institutions that have already undergone this process can be invaluable for those institutions that have just begun–let alone those credit unions encountering challenges on their path to greater digitalization.

Competition

The opportunity to grow, accelerated by digital transformation, also means that credit unions are facing and will continue to face greater competition than ever before. Personalization makes it easy for larger financial institutions to customize their offerings and compete with credit unions when it comes to deeply engaging with individual needs and preferences. Larger financial institutions also often have resources to take advantage of technologies faster and more thoroughly than most credit unions. This can make it easier for these bigger rivals to offer innovations to their customers before credit unions can provide similar solutions for their members.

This is to say nothing of the non-financial entities in Big Tech and Big Retail, for example, who, through innovations such as embedded finance, have begun to offer a variety of financial and banking services to their customers.

Learning more about ever-evolving member preferences is an important initial step. But following up with new initiatives, new services, and new solutions can be a key hurdle early in the process. To this end, credit union professionals owe it to themselves to learn and share strategies that have helped credit unions of all sizes better understand their members, deploy new products that are eagerly adopted, and boost engagement.

Collaboration

One of the ways that credit unions are dealing with the challenge of competition–with Big Banks, Big Tech, Big Retail–is by embracing opportunities to collaborate with innovative fintechs, many of whom specialize in serving the credit union industry. This is important. For credit unions looking for partners to help them improve back-office operations, offer a new rewards program, or fortify their defenses against fraud, teaming up with fintechs that have demonstrated interest and experience in partnerships with credit unions can make the difference between achieving digital transformation goals that may have seemed unreachable–and falling short.

To facilitate these kinds of partnerships, credit union professionals need a forum that focuses exclusively on credit unions and the fintechs that serve them. Our Credit Union Spotlight, taking place next month at FinovateFall in New York, is that forum. To learn more about joining us and participating in the session, email our registration coordinator at [email protected].

Headquartered in Littleton, Colorado, CPI Card Group offers a range of credit, debit, and prepaid solutions, as well as complimentary digital solutions and Software-as-a-Service (SaaS) instant issuance. The company’s partnership with Rippleshot will enable its customers to take advantage of the fraud prevention firm’s technology that leverages AI, machine learning automation, and predictive analytics to identify and stop credit and debit card fraud.

“Our partnership with CPI furthers our commitment to collaborating and helping financial institutions better protect their revenue and their account holders,” Rippleshot Co-Founder and CEO Canh Tran said. “Keeping up with evolving fraud trends is complex, labor intensive, and impossible to tackle alone. We’re excited to team up with CPI and their partners to help financial institutions proactively transform fraud prevention with a data-driven fraud management approach.”

Rippleshot’s fraud analytics platform spots fraud patterns and creates intelligence and rules to proactively identify emerging fraud risks and stop fraud incidents before they take place. With the backing of an expansive data consortium of 5,000+ financial institutions, the platform also enables banks and financial institutions to block merchants deemed “high risk” and limit the potential damage from major data breaches.

Rippleshot clients using the platform on a consistent basis have experienced a decrease in fraud activity of up to 35% a year. These clients have also identified 10x more compromised incidents compared to average network alerts. Thanks to Rippleshot’s risk score-based reissuance strategies, the fraud prevention process does not create additional friction for the client; institutions report 5x less disruption to customers’ transactions with Rippleshot’s technology.

“Rippleshot is a technology-forward solutions provider with a human-centric approach to decreasing fraud,” CPI Card Group VP of Business Development and Digital Solutions, Rob Dixon, said. “Through this partnership, our customers will be able to reduce costs associated with fraud loss, chargebacks, and manual monitoring while increasing profits and retaining top-of-wallet status with their cardholders.”

Founded in 1982 as Colorado Plasticard, CPI Card Group today is the largest manufacturer of credit, debit, and prepaid cards. The company went public in 2015, trades on the NASDAQ under the ticker PMTS, and has a market capitalization of $303 million. CPI Card Group began the year with the appointment of its new President and CEO John Lowe.

Headquartered in Chicago, Illinois, and founded in 2012, Rippleshot made its Finovate debut at FinovateSpring 2014. The company returned later that year to demo its fraud prevention technology at FinovateFall in New York.

Next-generation banking technology company Zeta has partnered with India’s HDFC Bank to power its Credit Line on UPI (CLOU) solutions.

The bank will leverage Zeta’s Digital Credit as a Service technology, which enables banks to manage a credit product from origination through processing without requiring multiple integrations.

Zeta won Best of Show in its Finovate debut at our all-digital fintech conference in 2020.

Banking technology provider Zeta has inked a partnership with India’s HDFC Bank to power its new Credit Line on UPI (CLOU) solutions. Announced by India’s National Payment Corporation of India (NPCI) in 2023, the CLOU scheme will make it easier for individuals to access credit and help banks leverage the UPI ecosystem to reach a significantly wider audience. HDFC’s partnership with Zeta will enable the bank to use the CLOU scheme to launch a range of new credit products by connecting pre-approved credit lines to the UPI user base.

Zeta Co-Founder, Global CTO, and CEO APAC Ramki Gaddipati referred to CLOU as “a credit superhighway.” He added, “Our solution is architected to leverage its innovative capabilities across the entire credit distribution lifecycle spanning underwriting, origination, distribution, usage, repayments, collections, and more.” Gaddipati emphasized that Zeta’s solution was built to fit the new technology, saying it would deliver a “UPI-first, mobile-first, and cloud-native credit products ecosystem.”

HDFC’s CLOU offerings will be powered by Zeta’s Digital Credit as a Service (DCaaS) solution. Unveiled earlier this year in India, Zeta’s technology enables banks to manage a credit product from origination to processing–as well as rewards, customer services, and more–without having to integrate multiple software packages and services. DCaaS also provides specific product blueprints to streamline the development of different types of credit lines on UPI products.

The technology was developed as Zeta recognized that the growing popularity of UPI was putting a strain on core banking systems–and that this strain could impact credit lines on UPI, as well. The company believes that CLOU will become a $1 trillion opportunity for banks by 2030.

The CLOU announcement is only the latest achievement of the partnership between Zeta and HDFC Bank. This spring, the bank announced that its PayZapp mobile app–developed in partnership with Zeta–had won the Celent Model Bank Award 2024. The app notched more than seven million customers since its launch in March 2023, and is among the top-rated apps in the Finance section on Indian app stores.

“We are glad to develop the Credit Line on UPI offering with Zeta enabling our customers to enjoy the benefits of an affordability program combined with the ease of doing a UPI transaction,” HDFC Bank Sr. EVP Rajanish Prabhu said.

HDFC Bank offers a wide range of banking products and solutions, including consumer, commercial, private, and investment banking; investment, asset, and wealth management; insurance; credit cards; and more. As India’s leading private sector bank, the Mumbai-based institution is the 10th largest bank by market capitalization ($145 billion), and the 16th largest employer in India.

Founded in 2015 and headquartered in San Francisco, California, Zeta won Best of Show in its Finovate debut at our all-digital conference in 2020. The company returned the following year to demo its modern, cloud-native, omni stack banking platform at FinovateFall 2021. Zeta achieved unicorn status that year courtesy of a $250 million round led by SoftBank.

In a recent post about the themes of FinovateFall 2024 (New York City, September 9 – 11), we recognized just how much our demoing companies were leveraging AI to help build innovative financial solutions in everything from payments and lending to cybersecurity and regulatory compliance. Financial services and fintech have truly entered the AI era.

And while our demoing companies showcase ready-to-go AI-powered tools and platforms, our keynote speakers are doing their part to help fintechs, banks, credit unions, lenders, and other financial services organizations figure out how to make AI work for their businesses and their customers.

Below is just a sample of the AI-in-financial-services content we have in store for you in less than two weeks time. If you haven’t picked up your ticket yet, you’re in luck: registration is still open and spaces are still available. Visit our registration hub today and we’ll see you in New York in September!

Conversational Banking: Get Value from Generative AI

Wulfraat is a seasoned industry leader bringing more than 20 years experience in solutioning and selling automated customer and employee experience solutions to many of the world’s most prestigious brands. At Kore.ai, he leads global direct sales, and is responsible for revenue performance across product offerings and regions. LinkedIn.

Unifying and Personalizing the Customer Journey through a Digital and AI-First Strategy

Kumar is focused on driving thought leadership and industry specific innovation to position Talkdesk as a leader in the market. He advises all components of digital transformation within the financial services industry on business strategy and adoption of new business models to support growth plans. In his 15 years in financial services, Kumar has helped multiple credit unions and community banks ideate and execute large scale digital transformation program. LinkedIn.

AI as a Co-pilot in Financial Services – How Every Function is Being Reimagined by Automation, AI Data Mining & AI-Generated data

Dan Latimore – Chief Research Officer, The Financial Revolutionist

Latimore is Chief Research Officer at The Most Impactful, a leading research-based recognition program created by The Financial Revolutionist to identify companies in financial services making the greatest difference. Latimore’s focus is on innovation in financial services and fintech, with a keen interest in consumer behavior and technology-enabled strategy. Most recently, he was the Chief Research Officer at Celent, a leading research firm focused on technology for financial services. LinkedIn.

Beyond the Hype: Delivering Real Business Value with AI in Financial Services

Brown is a seasoned leader in the AI and tech industry, specializing in transformative solutions for banking and fintech. Leading a team dedicated to innovation, Brown drives the development of tailored Deep Tech solutions to meet evolving client needs. At Intelygenz, he focuses on pushing AI technology boundaries, specializing in data-driven architecture, streaming AI, and human-centric solutions. LinkedIn.

What Does the Era of Generative AI Mean for Financial Institutions? What are the Real Use Cases for GenAI in Financial Institutions and Banks?

Subbarao leads Financial Services and Strategic Parnterships at Instabase. She is responsible for setting and implementing Instabase’s Financial Services product and market roadmap, enabling organizations across the world to drive bottomline efficiencies and transform customer journeys through the automation of critical processes underpinned by unstructured data. LinkedIn.

Alwell leads the Financial Services Solutions engineering team at GitHub and has worked in AI for the last decade. He has spoken at Microsoft events such as Build and Innovate as well as every GitHub Galaxy event including the keynote of 2022. His developer tools journey started in communications, digital media, then consulting, and now his focus is on serving GitHub’s financial services customers. LinkedIn.

Leveraging Advanced AI to Deliver Accurate and Adaptive Customer Service

Misra is Senior machine Learning Engineer at Truckstop and an AI Consultant at Sentick, where she focuses on assisting startups with their AI strategy and building solutions. She leverages her extensive experience in machine learning and a Master’s degree from the University of Waterloo, where her research bridged driving and machine learning to offer valuable insights. LinkedIn.

Governance, risk, and compliance platform Themis has partnered with regulatory compliance company Sei.

The partnership integrates Sei’s marketing compliance engine into Themis’ platform to enable financial institutions to maintain marketing compliance across all channels.

Themis won Best of Show in its Finovate debut at FinovateFall 2022. Neepa Patel is founder and CEO.

A partnership between regtech Themis and AI-powered regulatory compliance company Sei will provide financial institutions and fintechs with new tools to manage their marketing compliance operations. Integrating Sei’s marketing compliance engine into Themis’ platform will help institutions remain compliant across multiple marketing channels.

Sei’s technology leverages Large Language Models (LLMs) to convert regulations into actionable code. This can be used by compliance and risk teams to automate a variety of complex tasks. The integration of Sei’s AI agents into Themis’ platform will enable companies to screen partner websites and social media, automate the review of marketing content before it is shared with the public, and identify potential compliance issues.

Financial institutions and fintechs will benefit from access to advanced AI models that detect compliance issues across text, image, audio, and video. Sei’s AI agents support multiple languages, and are enabled with contextual understanding to ensure that only the most relevant issues are flagged.

“We’re thrilled to partner with Themis, the leading GRC platform for banks and fintechs, to offer Sei’s Marketing Compliance AI agent,” Sei founder Pranay Shetty said. “Together, we aim to improve consumer protection and help companies navigate an increasingly complex regulatory environment.”

Backed by Y Combinator and PayPal, Sei offers AI agents that work with risk and compliance teams to boost their efficiency, impact, and ability to scale. Founded in 2023 by Ramkumar Venkataraman, the New York-based company serves customers across three continents with solutions for marketing, customer support, and communications compliance, and regulatory change management.

Headquartered in New York and founded in 2021 by CEO Neepa Patel, Themis made its Finovate debut at FinovateFall 2022. The company won Best of Show for its demo of its GRC solution that serves as a one-stop shop for compliance. In addition to managing internal compliance workflows, Themis’ GRC solution can also be used to help banks and other financial institutions accelerate their partnerships with fintechs by examining their compliance controls in real-time.

As summer draws to a close, there may be a big acquisition on the horizon in the fraud and financial crime prevention space. Be sure to check in with Finovate’s Fintech Rundown all week long for the latest in fintech news.

This week’s edition of Finovate Globalfeatures an in-depth interview with Nacho Díaz de Argandoña, Chief Product Officer with Spain-based fintech, GPTAdvisor.

Founded in 2023 and headquartered in Madrid, GPTadvisor made its Finovate debut earlier this year at FinovateEurope 2024 in London. GPTadvisor offers a Gen AI platform that is specifically built to boost the productivity of financial advisors and wealth managers, as well as enhance client engagement.

This year, GPTadvisor announced that it has successfully completed a capital expansion round that featured support from two major Spanish venture capital firms, Kfund and JME Ventures. The company also announced that has launched a version of its GPTadvisor solution in the GPT Store by OpenAI. This launch made GPTadvisor the first portfolio management app available in the OpenAi store.

We caught up with Nacho to talk about current trends in wealth management and what AI can bring to the industry.

What problem does GPTadvisor solve and who does it solve it for?

Nacho Díaz de Argandoña: GPTadvisor addresses a critical challenge in the wealth management sector: the need for increased efficiency and productivity to remain competitive in an increasingly complex financial landscape. Financial advisors often face time-consuming, repetitive tasks such as investment research, portfolio management, and compliance. These tasks can detract from their prime objective, which is increasingly harder to accomplish: to nurture strong relationships with their clients and provide them with truly personalized and strategic advice.

GPTadvisor solves this context by providing advanced AI-driven tools that automate and streamline many of these processes, in a secure, private and controlled environment. Our wealth management platform uses the latest generative AI technology to assist financial advisors in quickly finding the right investment product, analyzing and comparing portfolios, elaborating comprehensible narratives to excel in client engagements and, ultimately, helping their clients reach their financial goals. By dramatically improving productivity, GPTadvisor allows advisors to focus more on client relationships and strategic decision-making.

The primary beneficiaries of our solutions are wealth management entities, including financial advisory firms and independent financial advisors. We see this product as a truly global proposition, where advisors anywhere around the globe can really start engaging in a new way of working.

How does GPTadvisor solve this problem better than other companies or solutions?

Díaz de Argandoña: GPTadvisor emerged during the generative AI wave with a clear objective: to apply this groundbreaking technology specifically to the wealth management sector. This focus distinguishes us from many other tech companies that, while experienced in general AI, are now struggling to adapt to the fundamentally different approach required by generative AI. Our foundation in this new paradigm allows us to harness its full potential in ways that others find challenging.

Having said that, we take AI very cautiously. We acknowledge there is a lot of noise and over-reliance in the industry where we expect AI to solve all our problems, and that is not the case. We focus on the use cases that provide the biggest gains in productivity, but without putting compliance at risk. This is why we proactively collaborate with regulators – FCA in the UK and CNMV in Spain – to explore the risks this technology involves and frame the guidelines to follow in order to successfully implement these capabilities.

Our core team brings over 40 years of collective experience in the wealth management industry. This deep expertise has enabled us to develop an innovative product from the ground up, in close collaboration with key industry partners. We work closely with numerous wealth management entities worldwide to ensure that our solutions are aligned with industry needs, making them both relevant and impactful.

Who are GPTadvisor’s primary customers. How do you reach them?

Díaz de Argandoña: GPTadvisor’s primary customers range from big commercial banks, private banks, and wealth management firms, to financial advisory entities and independent financial advisors. We work with entities that are seeking innovative solutions to enhance their productivity, streamline their processes, and ultimately provide more value to their clients by leveraging the latest technology in the market.

Interestingly, we’ve been receiving considerable inbound interest from various industry entities, driven in part by the growing enthusiasm for generative AI. As a result, we are actively engaging these entities and incorporating them into our aggressive generative AI product roadmap. This roadmap is designed not only to meet current market demands, but also to anticipate and continuously bring the benefits of this technology that is moving at unprecedented velocity.

We’ve also had the opportunity to pitch and present our work in numerous industry events, just like what we did with you last February at FinovateEurope in London. These platforms allow us to demonstrate the unique capabilities of our solutions to a wide audience that has generated very interesting conversations for us.

By capitalizing on the current momentum around generative AI and maintaining a strong and cold focus on the needs of wealth management professionals, I think we are successfully positioning GPTadvisor as the go-to solution for entities looking to stay ahead in this rapidly evolving landscape.

Can you tell us about a favorite implementation or deployment of your technology?

Díaz de Argandoña: One of our most exciting recent implementations is our quick portfolio analysis tool. This innovative function allows advisors to simply take a picture of a client’s portfolio with their phone and receive an instant, comprehensive analysis, thoroughly explained. The analysis includes generated insights on performance, risk, fees, and even comparisons with model portfolios. All in one go. This feature exemplifies the kind of intuitive, productivity-boosting tools we aim to deliver, making sophisticated portfolio analysis as simple as taking a photo.

Another feature we’re particularly proud of is our fund documentation auto-read feature. This tool is going to be a game-changer for GPTadvisor users globally, as they are now going to be able to instantly find and chat about key data and information in the documentation of thousands of investment funds. Whether they need details on fund performance, fees, or any other critical information, this tool streamlines the process, saving valuable time and enhancing decision-making capabilities.

These features are just the tip of the iceberg. We’re seeing new productivity functions like these arise on a weekly basis, as our team is able to move in sync with the fast-paced advancements in generative AI. Our ability to rapidly bring ready-to-use features to the wealth management space is one of the key strengths that sets GPTadvisor apart. It’s incredibly rewarding to see these innovations in action, transforming how wealth managers spend their valuable time and providing them with the tools they need to stay competitive.

What in your background gave you the confidence to tackle this challenge?

Díaz de Argandoña: The confidence to tackle challenges at GPTadvisor stems from the extensive experience and proven track record of our CEO, Salvador Mas. Before founding GPTadvisor, Salvador served as the Chief Digital Officer at Allfunds for five years, where he played a pivotal role in the company’s digital transformation and its successful public offering. Prior to his tenure at Allfunds, Salvador founded several startups at the forefront of innovation in wealth management. His most recent venture, Finametrix, a portfolio management platform, was eventually acquired by Allfunds.

This entrepreneurial experience, coupled with his leadership in a global financial powerhouse, has provided Salvador with deep insights into the challenges and opportunities within wealth management. It has also equipped him with the expertise to leverage technology in creating innovative solutions that address real-world problems in the sector.

Under Salvador’s leadership, we have fostered a highly talented, agile, and focused team at GPTadvisor, which has successfully grown the product and its capabilities since its inception just over a year ago.

With this strong foundation, we are confident that we are well-positioned to lead the way in bringing cutting-edge generative AI solutions to the industry.

What is the fintech ecosystem in Spain like? What is the relationship between fintechs, banks, and traditional financial services companies in the country?

Díaz de Argandoña: The relationship between fintechs and traditional financial services companies in Spain is characterized by a mix of competition, collaboration, and co-opetition.

In the specific case of wealthtech, traditional institutions have maintained their market share despite some success stories (such as the robo-advisor Indexa Capital and the neobank MyInvestor). However, the majority of advisory services continue to be provided by traditional institutions like Santander, BBVA, or CaixaBank, which have successfully embraced digital transformation.

At GPTadvisor, we are collaborating with both types of entities, introducing generative AI in both traditional and disruptive institutions.

Left to right: Nacho Díaz de Argandoña and GPTadvisor CEO Salvador Mas at FinovateEurope 2024.

You demoed at FinovateEurope earlier this year. How was your experience?

Díaz de Argandoña: FinovateEurope was an excellent experience for us. The event was professionally and thoughtfully organized, making us, as demo participants, feel like true protagonists. It provided a valuable platform to connect with a wide range of wealth management professionals, investors, and industry stakeholders, which allowed us to test our proposition with real prospects in London—one of the world’s premier fintech hubs.

As we prepare to demo our solution again, this time in New York, it feels like a natural next step in our journey. Entering the U.S. market is a key priority for us, as we believe our solution can significantly enhance the day-to-day operations of financial advisors across the country.

We’ve been steadily growing our platform, adding a host of new features and enhancements, and we can’t wait to showcase these developments on stage. We’re confident that the New York demo will be another great experience for us, helping us to further expand our presence in a critical market.

What are your goals for GPTadvisor? What can we expect to hear from you in the months to come?

Díaz de Argandoña: Over the past year, we’ve focused intensely on refining and validating our proposition in the market. We’ve been building a next-generation AI-native platform from the ground up, one that evolves in tandem with the rapid advancements in AI technology. Our approach has involved close collaboration with leading financial entities worldwide, ensuring that we stay connected to the real-world challenges and opportunities that need solving.

I believe we’re now at a tipping point where the product is ready for greater scale. GPTadvisor is now ready to support thousands of financial advisors work more productively and deliver more value to their clients. Our plan is launching our SaaS model at global scale through the second half of the year to reach more clients and gain more leadership in the market.

As we continue to explore the full potential of generative AI and its applications within our sector, I can’t imagine a more exciting time to be involved in shaping the future with GPTadvisor. We’re just getting started, and there’s much more to come.

InvoiceASAP has partnered with global payments platform Adyen to facilitate instant access to deposited funds.

The partnership combines InvoiceASAP’s Invoice to Pay solution with Adyen’s Instant Payouts and Cash Out functionality to enable businesses to better manage cash flow.

Oakland, California-based InvoiceASAP made its Finovate debut at FinovateSpring 2013.

A partnership between invoicing and payments solutions provider InvoiceASAP and business payments platform Adyen will enable InvoiceASAP to offer its users instant access to deposited funds. This is a critical issue for InvoiceASAP’s small- and medium-sized business customers, who often require quick and ready access to capital to better manage their expenses.

“InvoiceASAP is building the most advanced Invoice-to-Pay solution,” company CEO Paul Hoeper said. “Adyen gives us access to the most advanced payment products and tools, including FedNow for Instant Deposits. We are fully focused on providing the fastest velocity of bank deposits for our over 23,000 merchants. By combining Adyen’s Instant Payouts and new Cash Out functionality, we can provide our users with unmatched velocity.”

InvoiceASAP will take advantage of Adyen’s global solution – Adyen for Platforms. The offering enables users to sign up, sell, and get paid through a single solution. The company will also leverage Adyen’s Cash Out feature to provide its users with instant access to pending funds, without having to wait multiple days.

“Our partnership with InvoiceASAP underscores Adyen’s commitment to continued innovation,” Adyen North America President Davi Strazza said. “Our FedNow certification allows for instantly-available deposits and cash advances, enabling InvoiceASAP users to better manage cash flow, scale operations, and invest in the tools they need to thrive.”

With customers ranging from Microsoft and Meta to Uber and H&M, Adyen provides end-to-end payments capabilities, data-driven insights, and financial products to businesses around the world. Headquartered in Amsterdam, Adyen processed more than €970 billion in payment volume in 2023. This month, in addition to its partnership with InvoiceASAP, Adyen announced a collaboration with PayPal to offer its Fastlane product on the Adyen platform. Also in August, Adyen reported that it has extended its partnership with BMW and expanded its operations in India. The publicly traded firm has a market capitalization of $45 billion.

Founded in 2010 and headquartered in Oakland, California, InvoiceASAP made its Finovate debut at FinovateSpring in 2013. In the years since then, the company has grown into a major, fully-integrated mobile invoicing solution provider with more than 400,000 customers in 120+ countries. InvoiceASAP enables merchants to generate and pay invoices on the go using either a smartphone or a tablet. The company’s technology connects with major accounting platforms, including QuickBooks and Xero, to ensure compatibility with the merchant’s accounting software.

Consumer-permissioned data platform Truv announced an integration with mortgage point-of-sale (POS) and automation software provider LenderLogix.

The integration will enable mortgage lenders to more easily verify income and employment data from mortgage applicants.

Truv was founded in 2020 and made its Finovate debut at FinovateFall 2022.

Making it easier for lenders to access the data they need in order to provide credit to worthy borrowers is one of the key promises of open finance. A new integration between consumer-permissioned data platform Truv and mortgage point-of-sale (POS) software provider LenderLogix will leverage open finance to enable lenders to more easily and accurately verify income and employment information from mortgage applicants. The integration will enable mortgage lenders to access Truv’s platform via LenderLogix’s point-of-sale system LiteSpeed to secure direct-to-source income and employment verification.

“With the integration of Truv’s verification capabilities and LiteSpeed, lenders can now enjoy a streamlined workflow that reduces administrative tasks and frees up resources for improved customer service,” LenderLogix Co-Founder and CEO Patrick O’Brien said. “This powerful combination eliminates the need for third-party verification services, leading to significant cost savings and lower overall loan processing expenses. Additionally, the automation speeds up loan approvals, allowing lenders to close loans faster and optimize their operational throughput.”

Lenders will benefit from Truv’s coverage of 96% of the U.S. workforce and the immediate access to data through LenderLogix’s LiteSpeed. This will accelerate the mortgage application process by removing manual document collection and by being able to access more data-rich, complete loan files at the point of application. For borrowers, the partnership will provide an application process that is faster and more straightforward, with fewer touchpoints.

“Our integration with LenderLogix marks a significant advancement in our mission to revolutionize the mortgage origination process,” Truv CEO Kirill Klokov said. “By combining our strengths, we are providing mortgage lenders with the tools they need to deliver exceptional service to their clients while improving operational efficiency.”

Founded in 2020, Truv made its Finovate debut at FinovateFall 2022. At the conference, the company demonstrated its income and employment verification and direct deposit switch technology. The company’s income and employment verification solution delivers verified identity, income, and employment data points within 60 seconds. Truv credits its direct deposit switch solution for enabling institutions to increase direct deposits by up to 65%.

This spring, Truv teamed up with digital mortgage automation solutions provider Floify and with point-of-sale (POS) mortgage lending platform – and fellow Finovate alum – BeSmartee. Truv has raised more than $28 million in funding from investors including Kleiner Perkins and NYCA.

Are you an innovative fintech with new technology that’s ready for prime time? Join us in New York next month for FinovateFall and take advantage of the opportunity to showcase your solution before an audience of 2,000+ decision-makers.

International payouts orchestration company, PayQuicker, has forged a partnership with cross-border payment infrastructure firm Thunes to expand its e-Wallet payout capabilities around the world.

The integration is designed to better serve the growing demand for diverse and flexible payout methods. This demand is especially acute in emerging markets, where access to traditional banking is limited and tools like e-Wallets play a major role in helping individuals manage finances and make payments. McKinsey estimates that up to 60% of those in emerging markets prefer to use e-Wallets instead of traditional banks.

Integrating enhanced e-Wallet capabilities into its global payouts solutions mix will help PayQuicker fulfill its objective of providing faster, easier payouts around the world. The company said that it will offer access to more than 120 e-Wallets in key emerging markets, courtesy of the new partnership. Among the e-Wallets that will be accessible are popular e-Wallets such as the Philippines’ GCash, China’s Alipay, and both Orange Money and M-Pesa of Africa.

“Digital wallets are transforming the way people manage their finances, especially in regions where traditional banking infrastructure is lacking,” PayQuicker CEO Paul Beldham said. “By teaming up with Thunes, we’re further enabling millions of people around the world to receive their funds faster and more securely, providing the flexibility of a bank alternative. This not only empowers individuals to better manage their day-to-day finances but also supports the economic growth of emerging markets by facilitating more reliable transactions.”

Headquartered in Rochester, New York, PayQuicker made its Finovate debut at FinovateFall 2022. At the conference, the company demoed its Payouts OS solution, which packages the company’s payments technology into a payouts payment orchestration platform that intelligently determines and facilitates the fastest, most cost-effective payouts across 200+ countries in 40+ currencies.

Thunes was formed in 2019 when Finovate alum TransferTo rebranded as two separate businesses: one, Thunes, focusing on cross-border payments and the other, DT One, focusing on mobile top-up and rewards. Earlier this month, Thunes announced a partnership with Alipay+ to enable merchants in Paris to accept payments from 15 international e-Wallets and mobile partnerships. In July, Thunes added cross-border payment service provider LianLian Global to its global network.

Conversational AI technology company Gridspace announced new emotional intelligence capabilities for its virtual voice agent Grace.

The update enables Grace to respond more swiftly and empathetically, and enhances the agent’s ability to express its own emotional states.

Gridspace made its Finovate debut at FinovateFall 2022 in New York.

Voice technology and AI software innovator Gridspaceunveiled new emotional intelligence capabilities for its virtual voice agent Grace. The new capabilities enable Gridspace’s voice agent for business to respond faster and more empathetically to the speaker’s emotions. The enhancements also improve Grace’s ability to express its emotional states.

“Grace’s new emotional intelligence capabilities make voice calls with Grace even more natural,” Gridspace CEO Evan Macmillan said. “We are excited to further advance customer satisfaction with voice agents and make it even easier for businesses to deploy them.”

Bringing emotional intelligence capabilities to voice agents is a major advance in spoken dialog systems, according to Gridspace. Because so many contact center interactions involve customers experiencing frustration, being able to respond appropriately is paramount. Grace’s enhancements will enable the voice agent to manage more complex interactions with greater nuance, and also act as a buffer for high-volume contact centers. To this point, human agents working with Grace have reported not only being able to spend more time on complex calls, but also are experiencing less stress, lower burnout rates, greater productivity, and higher job satisfaction.

Founded in 2012, Gridspace made its Finovate debut at FinovateFall 2022. The California-based company was created through a collaboration between SRI Speech Labs – the entity behind Siri – and a diverse team of designers and engineers. Gridspace has been innovating in fields such as high-performance voice telephony, automated speech recognition (ASR), hyper-realistic TTS (text-to-speech), low-latency spoken dialog systems, as well as tools and solutions to help institutions deploy and manage conversational AI.

Gridspace has raised more than $27 million in funding and includes Private Investors and USAA among its investors.

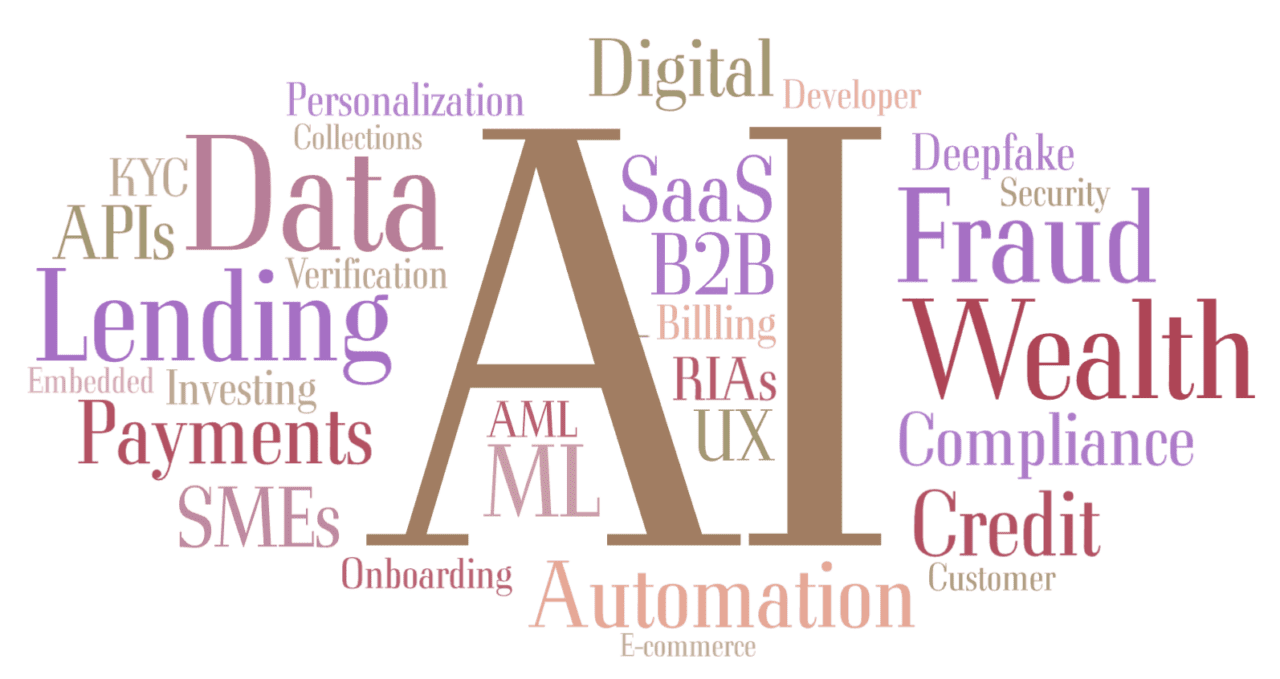

What themes will dominate the conversation at FinovateFall next month in New York (September 9-11)?

Many of the popular themes in recent years still endure. The customer is still king. Data and personalization matter. And payments, in the words of one clever panelist many Finovates ago, continues to be the “gift that keeps on giving.”

But in some ways these issues have been, if not eclipsed, then perhaps subsumed by enabling technologies like AI, machine learning, and what I call “Automation 2.0” – the leveraging of AI technology to automate a growing range of business operations and manual tasks.

These technologies have brought new energy to sectors such as lending and payments. They have raised the stakes on what it means to provide truly personalized financial services. And when it comes to the customer, these enabling technologies promise new and exciting ways to engage them and deliver digital experiences that would have been hard to imagine even a few years ago.

In fact, I’d argue that some of the themes we see in the word cloud above, such as “compliance,” “security,” and “fraud,” are more prominent than before not simply because of the growing impact of financial crime or fresh concerns over regulatory priorities, but also because of the way that enabling technologies such as AI, machine learning, and automation have given fraud fighters and compliance teams new tools to keep consumers safe and company operations compliant.

If these themes resonate with you, then remember that at Finovate, what you see is what you get. Each of these themes has at least one, if not two or three, innovative companies who will be demoing their response to these challenges and opportunities live on stage next month at FinovateFall in New York. Check out our Finovate Sneak Peek series, as well as our evolving FinovateFall agenda, to learn more.