This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Progress Bank, a $1.4 billion asset financial institution that serves businesses in Alabama and the Florida panhandle, has teamed up with Sensibill to offer its digital receipt management solution to its business customers. Sensibill leverages AI and machine learning to provide SKU-level transaction data to help businesses better manage their finances and enable banks to better customize offerings to their business customers.

“We have long been dedicated to providing a seamless, convenient experience for our busy business customers, and partnering with Sensibill directly supports that strategy,” Progress Bank SVP of Operations, Finance, and Technology Randy Tidwell said. “With Sensibill, we are modernizing and digitizing receipt and expense management, a traditionally cumbersome and time-consuming process. This ultimately helps our customers save time, reduce stress, and manage their personal and business finances more easily. As businesses look to navigate the pandemic’s lasting impacts, digital tools like these become even more critical to provide meaningful support.”

Progress Bank sees the addition of Sensibill’s technology as a way to reach out to businesses that cannot or prefer not to visit a branch. Progress Bank will run Sensibill’s solution via its FIS Digital One platform, enabling its business customers to capture and store receipts on their digital banking apps. Once digitized, receipt data can be readily analyzed to track spending and better manage overall finances.

“Relationship-focused institutions like Progress Bank understand the importance of providing customers with quick and intuitive digital tools to help them better manage everyday spend,” Sensibill CEO and co-founder Corey Gross said. “By leveraging our technology, the bank’s customers eliminate the time and hassle of keeping up with and analyzing paper receipts, leading to easier tax seasons and expense management.”

Toronto, Ontario, Canada-based Sensibill earned a Best of Show award in its Finovate debut at FinovateFall 2017. The company returned to the Finovate stage a year later for a demonstration in partnership with NatWest. Since then, Sensibill has partnered with JPMorgan to have its technology integrated into the Chase mobile banking app. The firm has also collaborated with Metro Bank, which went live with Sensibill’s digital receipt management solution over the summer. More recently, Sensibill earned a spot on The Globe and Mail’s Top Growing Companies in Canada list for 2020.

Founded in 2013, Sensibill has raised more than $55 million in funding from investors including Radical Ventures, Information Venture Partners, and First Ascent Ventures.

It’s Veterans Day in the U.S., a day dedicated to honoring the service of the country’s military veterans.

Given the long-running military conflicts in Iraq and Afghanistan, the Veterans Day holiday has taken on a special significance for Americans in recent years. And it could be argued that more military veterans have been “thanked for their service” in the past decade and a half than in the previous several put together. But beyond expressions of gratitude, what can financial services companies, financial institutions, and fintechs do to really show their appreciation for veterans? Here are five ideas:

Hire Them

The economic fallout from the global health crisis has had its impact on veterans as it has on everyone else. While the unemployment rate for veterans is better than the national rate – 5.5% for veterans compared to 6.9% for the U.S. population overall – some veterans still face unique challenges when it comes to returning to the civilian workforce.

One study published this week by the San Diego Workforce Partnership showed that many veterans lack the kind of business networks and networking opportunities that their non-veteran counterparts access. Respondents also felt they were unable to impress upon employers the value of skills they developed while serving in the military – such as discipline and reliability.

U.S. Veterans Magazine published a valuable primer in this regard last summer. For more on how to bring more veterans to your workforce – and how to make the most out of veterans you already have working for you, check out their 12 Tips for Effectively Managing Veterans in the Workplace.

Lend to Them

While there are many financial institutions and even insurers that make a point of serving veterans and their families, helping veterans buy first homes and fund small businesses is one of the best ways that fintechs can support the veteran community.

One fintech that has done much to help ensure veterans and veteran-run small businesses get the financial help they need is StreetShares. Founded in 2013 by U.S. Air Force veteran Mark Rockefeller and headquartered in Reston, Virginia, StreetShares offers a lending-as-a-service platform that enables banks, credit unions, and other organizations to offer small business loans. The company began, however, with a “first affinity” for providing financing for military veteran business owners who, the company noted in its Finovate debut in 2015, make up one in nine of all small businesses in the U.S.

Partner with Them

A growing number of companies are helping further the cause of diversity by seeking out partnerships with businesses run by women and members of underrepresented ethnic groups. For those interested in supporting veteran entrepreneurs and veteran-owned businesses, approaching veteran communities with the same enthusiasm and similar opportunities is a sound strategy.

Whether it’s via something as simple and straightforward as Veterans Day sponsorships or, ideally, a more enduring effort to seek out veteran business owners to discuss innovative collaborations, fintechs and financial institutions have as much to gain from the diversity of veteran-run businesses as these small businesses do.

Work for Them

As noted above, many veterans seeking work lack the networking opportunities many non-veterans have that can make the difference between a merely challenging job search and a brutally frustrating one. Similarly, not every veteran small business owner or entrepreneur has a Rolodex – or a LinkedIn account – full of talented and qualified potential employees. At the same time, some non-veterans may harbor negative stereotypes against veteran employers, and express some concern about working for them.

Understanding that the civilian workplace is different from the military workplace is a good place to start for everyone, including prospective employees of a veteran boss. In the same way that we correctly seek out diversity among those we live and work with to enhance our lives, improve our work, and support our communities, appreciating and learning from the life experience of military veterans can be similarly valuable for all involved.

And if you are a veteran, seeking out another veteran-run business is not only a way to support the veteran community, but also it might present a unique opportunity in which the veteran has a leg up over the non-veteran applying for the same job. It may be that many life-long civilians will not appreciate fully the “soft skills” developed through years of military service. But you can bet your bottom dollar that your veteran employer gets it.

Listen to Them

It is a cliche to say that many veterans bring valuable leadership skills to the private sector. But it is a cliche that endures for a reason: whether serving in peacetime or in conflict, the veterans of our armed forces have lessons and life experiences that not only have shaped them, but also can help guide us, as well. It is no surprise that, when surveyed, the U.S. military ranks consistently among the most trusted public institution. When respondents are asked why, the “competence with which they do their job” and “selflessness, bravery, and discipline,” were among the reasons.

And with more than a million men and women currently on active duty in the U.S. military, many of whom will become veterans in the next few years, “selflessness, bravery, and discipline” sound like a few good reasons to start adding more military veterans to your business network.

Small business financing and payment solution provider Behalf will partner with online, tech-based retailer NeweggBusiness to offer the firm’s business customers flexible, extended financing. NeweggBusiness gives its users access to a range of IT products – from laptops and desktops to servers and data storage solutions – at competitive prices. NeweggBusiness also supports smart purchasing by providing peer reviews, expert opinion, product tutorials, and the ability to network with other members of the NeweggBusiness community.

“Behalf is a great addition to our offering, as it gives NeweggBusiness customers greater flexibility in how they purchase and pay for the equipment that’s essential to their everyday operation,” VP of Business Development for NeweggBusiness Greg Fischer said. “Our commitment to deliver business-friendly solutions to our customers runs deep, not only in the products we offer, but also in the financing options that make those products more accessible to all business customers.”

Courtesy of the new partnership with Behalf, NeweggBusiness customers will be able to apply for a Behalf account directly from the NeweggBusiness website, and use Behalf’s financing for their NeweggBusiness purchases. Behalf offers an omni-channel digital payment platform that enables businesses to extend net terms and financing to their business customers. Once businesses sign up for net terms/financing with Behalf, they send their payments directly to Behalf who, in turn, pays the SME’s vendor by the next business day after the transaction is approved. Behalf helps accelerate receivables, boost inventory turnover, and gives small businesses greater control over their cashflow and access to more buying power.

“Financing has always been a challenge for small- and medium-sized businesses, and that is especially the case today due to COVID,” said Behalf CEO Rob Rosenblatt. “Access to capital is critical to the success of these businesses and Newegg is addressing the problem head on for its customers with Behalf.” Rosenblatt joined Behalf as CEO in August, replacing company co-founder Benji Feinberg.

Founded in 2011 and demonstrating its technology at FinovateFall three years later, Behalf announced a partnership in September with Georgia-based Priority Payments Systems and Priority Commercial Payments to offer flexible cashflow solutions for SMEs. The company has raised $310 million in funding from investors including Soros Fund Management, Viola Growth, MissionOG, and Spark Capital.

It looks like the Biden transition team aren’t the only ones being told to slow their roll by the Trump administration: the U.S. Department of Justice has filed a civil antitrust lawsuit to block Visa’s ability to acquire innovative fintech – and Finovate alum – Plaid.

“American consumers and business owners increasingly buy and sell goods and services online, and Visa – a monopolist in online debit services – has extracted billions of dollars from those transactions,” Assistant Attorney General Makan Delrahim of the Justice Department’s Antitrust Division said. “Now, Visa is attempting to acquire Plaid, a nascent competitor developing a disruptive, lower-cost option for online debit payments. If allowed to proceed, the acquisition would deprive American merchants and consumers of this innovative alternative to Visa and increase entry barriers for future innovators.”

The move by the Justice Department was anticipated. An investigation into the acquisition was launched in late October, after the department spent a year examining how the deal would impact the financial services market more broadly. And in its statement, the Department has concluded not only that the impact would not be good, but also that Visa’s motives for the acquisition are problematic, as well. DOJ accuses Visa of purchasing the fintech company as an “insurance policy” to defend its U.S. debit business. The statement indicates that Visa feared that, either by itself or in partnership with a competitor, failure to deal with the “threat” of Plaid could result in “potential downside risks of $300 million to $500 million” in its debit business.

Visa’s criticism of the lawsuit mirrors somewhat the broader critique that we often hear when politicians get involved in technology; namely, you just don’t get it. Specifically, Visa accused the government of not “understanding Plaid’s business and the highly competitive payments landscape in which Visa operates.” The company, which has 70% of the online debit transactions market compared to rival Mastercard with 25% share, added that rather than a competitor, it sees Plaid simply as a firm with complementary capabilities.

“Visa’s business faces intense competition from a variety of players,” the company’s statement read, “but Plaid is not one of them.” For its part, Plaid has not commented on the lawsuit at this point.

What are the odds of the Visa-Plaid acquisition emerging successfully from this legal challenge? While it is difficult to predict an outcome, what is catching the eye of some observers is the possibility that DOJ’s interest in Visa’s Plaid acquisition could be just the beginning. Citing language in the lawsuit that refers to Visa’s “long history” of aggressive action toward fintechs like PayPal, Bloomberg Law quoted former DOJ antitrust division attorney John Newman who said a “monopolization case” could be in the offing against Visa – even if the current case is limited to blocking the acquisition of Plaid.

FISPAN, Lendio, and Subaio are three of the ten fintech startups selected to participate in Mastercard’s upcoming Start Path accelerator program. The six-month accelerator will give startups the opportunity to collaborate with Mastercard on their solutions, as well as connect and network with members of Mastercard global ecosystem of banks, merchants, and technology companies.

“We all thrive when fintechs have access to the technology they need to reach scale and democratize finances,” Mastercard Chief Innovation Officer Ken Moore said. “We are partnering with the newest fintechs joining Start Path to drive inclusion, innovation, and trust with alternative ways to pay and authenticate, powerful solutions for small businesses, new ways to create efficiency for business payments, as well as address the wealth gap.”

Also participating in the program’s upcoming cohort are:

Carry1st

LISNR

Mocafi

Mo Technologies

Panda Remit

Paycode

Fanbank/Plink

All three Finovate alums shared the news Monday morning, either via social media or, in the case of Subaio, the company blog. “FISPAN is very proud and excited to work with Mastercard Start Path and start co-innovating,” the company announced on Twitter. “We’re excited to announce that Lendio is joining the Mastercard Start Path global network of fintech innovators!” tweeted Lendio.

FISPAN most recently demonstrated its cloud-based, API services management platform at FinovateFall last year. The Vancouver, British Columbia, Canada-based company was featured in our look at top Canadian fintechs over the summer. Look out for an upcoming Finovate interview with FISPAN Chief Technology Officer Clayton Weir on the company’s efforts to leverage open banking to help financial services companies better manage the economic fallout from the global health crisis.

A Finovate alum since 2011, Lendio has more than 75 lenders in its network who have facilitated more than 216,000 small business loans valued at more than $10 billion. Headquartered in Salt Lake City, Utah and founded in 2005, Lendio announced last month that it has processed more than $500,000 in microloans to women-owned businesses around the world. The initiative was launched via its Lendio Gives employee-contribution program, in partnership with international non-profit Kiva.

For its part, Denmark-based Subaio’s CEO Thomas Laursen added that joining Start Path would be a “huge opportunity to work together with Mastercard and validate(d) the potential within the subscription management service.” One of Finovate’s newest alums, demoing its technology at FinovateEurope in Berlin in February, Subaio offers a subscription management service that gives bank customers the ability to track and manage subscriptions and recurring payments. The company has eight partners in Europe and has processed more than five billion transactions since inception.

Founded in 2014, the Mastercard Start Path program has worked with more than 250 startups since inception. These companies have raised $2.9 billion in investments after leaving the program.

Embedded finance and payments platform Hydrogen announced a strategic investment today. FINLAB, a new incubator launched by EML Payments, completed what Hydrogen called an “initial investment” that will include a cross-platform integration that will make it easier for firms to offer smart apps linked to both physical and virtual payment cards.

“We are thrilled to be working with EML and have it as a strategic investor in Hydrogen,” company co-founder and CEO Mike Kane said. “Together, we’ll be able to bring innovative card offerings to the masses, making it easy for any organization to offer card capabilities. It’s embedded card services made easy.”

The terms of the investment were not disclosed. Hydrogen currently includes both SixThirty and Route 66 Ventures among its investors.

Hydrogen’s no-code platform enables financial and non-financial companies to offer fintech products and modules without needing to have any development experience. Those organizations with development teams can take advantage of Hydrogen’s low-code API option, which enables developers to build custom apps on top of REST-based APIs. Featuring orchestration, business logic, and data cleansing, the platform enables businesses to leverage a standardized data model that can help keep costs of integration low and the development time short.

“We love cementing deals and investing in payments trailblazers,” EML Managing Director and Group CEO Tom Cregan said. “Hydrogen, with the intensity of energy it has already infused into the industry, is no different. Our commitment is to assist this fast-growing entity in soaring within fintech via EML’s capabilities and FINLAB. It’s heartening to know Hydrogen feel in safe and trusted hands with the might of EML’s global reach.

Making its debut at FinovateEurope two years ago, Hydrogen announced in September that it was one of 20 companies selected to participate in Plug and Play’s 2020 Winter Fintech batch. Also that month, the company unveiled a partnership with fellow Finovate alum Dwolla and teamed up with market data and technology service provider Barchart.

Among its accolades, Hydrogen has been named FinTech Startup of the Year by KPMG Luxembourg and as a World Changing Technology by Fast Company. The company was founded in 2017 and is headquartered in New York City.

Putting artificial intelligence to work to help boost customer engagement in financial wellness, Personetics has announced a new partnership with Santander UK. Together, the two companies are offering a new digital solution, My Money Manager, integrated into Santander UK’s mobile banking app.

My Money Manager is designed to give users ready access to a variety of personalized, data-driven insights into their finances. The intelligent app learns as it is used, incorporating customer behavior, preferences, and feedback to provide alerts and tips to help keep users on track. Among the features of My Money Manager are expected deposit dates for recurring payments, push notifications for changes in scheduled payments, purchase analysis – including insight into category spending – as well as notification of expiring subscriptions and cards.

“We’re proud to be working with Santander to provide the technology to deliver personalized, proactive insights that significantly impact a customer’s financial confidence and ability to make lasting improvements to their financial situation,” Personetics CEO and co-founder David Sosna said. “Santander’s continued investment in customer-centric technologies demonstrates their innovative approach to customer engagement and digital innovation to better service their customers in a very tumultuous time.”

A Finovate alum since 2016, Personetics provides a customer engagement platform for financial services companies that enhances the financial customer journey with personalized insights, recommendations, and guidance. The platform leverages AI-driven chatbots to deliver contextual, financial advice and recommendations to help users reach their financial goals. Personetics notes that it’s technology has boosted digital engagement by 35% and saved new customers an average of $2,400 a year.

“My Money Manager is the result of a new kind of partnership between Santander and Personetics,” Santander UK Head of Customer Journey Design Andy Warren said. “Working collaboratively, the Personetics team is an extension of our internal teams, generating new use cases and co-creating beyond off-the-shelf solutions. Building long-lasting and meaningful relationships with our strategic partners is key to accelerate Santander’s digital transformation. We’re proud to bring innovation to our customers.”

Headquartered in Tel Aviv, Israel, and New York, Personetics announced an extension of its partnership with Discount Bank in August. The new agreement helped the bank launch Smart Save, an auto-savings solution. In April, the company teamed up with Hyundai Card to add personalized insights as part of a new service called “Spending Care by Personetics.” Also this spring, Personetics joined the Avaloq.one ecosystem.

The kids section of the fintech universe is making headlines as Strive – a U.K.-based challenger bank that helps parents preach financial literacy and practice smart financial behavior with their kids – made good on its acquisition of digital piggy bank GoSave. The company went live with the new functionality today in London.

“We’ve been working with GoSave for a period of time now with some of our clients, and the idea of a youth focused challenger bank kept coming up,” Strive CSO Ivan Muck said. “We see a real gap in the market to build a solution for parents that grows with the child, so it’s not just a debit card, it’s a whole 0-18 proposition that parents can start at any age.”

Strive is presently accepting “expressions of interest” of ahead of a Seedrs crowdfunding campaign “in a few months.” The company has pledged to donate a portion of sales of its digital piggy bank to help support financial literacy through youth charity MyBnk.

California-based GoSave was launched on KickStarter in 2018, and went on to earn recognition as part of VISA’s Everywhere Initiative later that year. The company is also an alum of Techstars Berlin (2019). Check out a profile of GoSave from February from our sister publication, Fintech Futures.

Courtesy of a partnership with Mastercard, Jassby’s virtual debt card gives kids a contactless and cashless way to spend money raised from chores, allowances, or gifts. The card can be used anywhere contactless payments are accepted via mobile device, and Jassby is offering the card with no fee for the first six months and no fee afterwards as long as the card is used once a month.

As with Strive, Jassby is also taking names for early registration for its “virtual debit card for families.”

“The Virtual Debit Card is another example of putting our customers first and delivering a product that meets a growing need in the market,” Jassby founder and CEO Benny Nachman said. “I started Jassby to prepare my kids for life in the real world and thousands of families have joined us for the same reasons. With continued support, we’re able to empower kids with the hands-on financial experience necessary for today’s new normal.”

Founded in 2018, Jassby scored $5 million in funding in March. The company includes Blumberg Capital and Correlation Ventures among its investors.

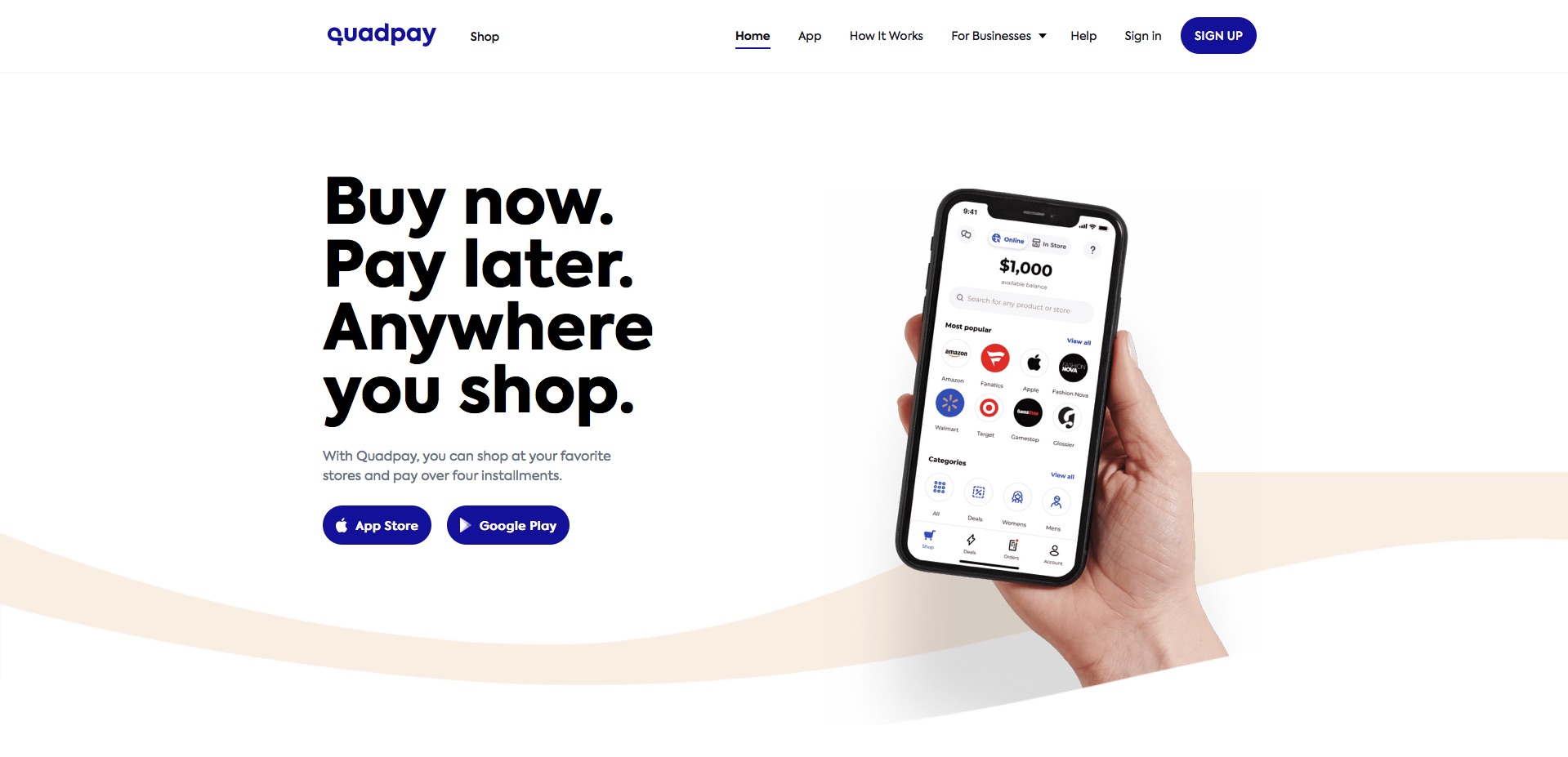

There were many themes that fintech analysts expected to dominate this year. But there were few among them who had “Buy Now Pay Later” (BNPL) on their 2020 bingo cards.

From big recent M&A in the BNPL space to the rash of installment payment offerings recently launched by both fintechs and incumbent financial services companies alike, it is clear that Buy Now Pay Later is one of the hottest trends in fintech and e-commerce right now.

We thought this would be a good time to catch up with one of the leaders in the BNPL movement. QuadPay co-CEO and co-founder Brad Lindenberg shared with us his insights into what’s driving interest and excitement in the Buy Now Pay Later space, and what we can expect to see in the months and years to come.

Finovate: The Buy Now Pay Later phenomenon is one of the more unexpected developments in e-commerce this year. From the perspective of a company that’s been active in this space for years, what made the difference in 2020?

Brad Lindenberg: There are a number of factors in play that have led to the rapid ascent of buy now, pay later (BNPL) globally in 2020. First, consumers – particularly millennials – are wary of high interest credit cards and accruing additional debt. This concern was prevalent before 2020, as many millennials are saddled with student loan debt, but now has been heightened by the economic impact from COVID-19. The BNPL industry has been a major disruptor to credit cards and companies like QuadPay represent the new world of interest-free, transparent digital payment products.

Secondly, BNPL empowers retailers to provide their customers with flexibility to pay over time, which ultimately fosters customer loyalty, increases conversions, and a better customer experience. In the case of QuadPay, merchants that have implemented our BNPL product for e-commerce have seen a 20 percent increase in conversions and 60 percent increased average checkout value.

I would also point out that for QuadPay the BNPL phenomenon is not solely within e-commerce. With QuadPay, consumers can use BNPL to shop everywhere for everything – whether it’s online or in the-physical retail locations of the thousands of merchants on the QuadPay app. QuadPay has direct partnerships with 7,200 world-class retailers that are promoted within the QuadPay app to our four million and growing customer base in the U.S.

Finovate: We can’t talk about 2020 without talking about COVID. How has the pandemic affected both your company, and your company’s relationship with its customers?

Lindenberg: In many ways, QuadPay is the right company at the right time. Almost overnight the industry witnessed a drastic shift in consumer spending to focus almost exclusively online with retailers responding in kind to support that demand and QuadPay was able to facilitate those needs on both sides. We have built a digitally-forward payment product that fits the mobile-first lifestyle of today’s budget conscious consumers that can also be quickly and efficiently implemented by merchants across industries and of all sizes trying to adapt. We have experienced an uptick in interest in BNPL overall, but particularly from small and medium businesses – this has by far been our fastest growing vertical since the pandemic.

Finovate: In this increasingly competitive space, what does QuadPay offer that its competitors don’t?

Lindenberg: Competition is inevitable in a fast-growing and successful category like BNPL and serves as validation that the credit card industry is badly broken. The entry of new players has not changed our strategy or lessened our opportunity. We remain laser-focused on providing our users the best possible products fueled by our drive to innovate. Our recent merger with Aussie payments pioneer Zip Co. (ASX: Z1P) forged a $1 billion global fintech alliance and has us solidly positioned to continue our leadership position in this category.

QuadPay’s true differentiator remains innovation – we are the only installment platform that gives consumers the power to shop anywhere – at any retail location, on any website and with QuadPay’s integrated merchants on the app – and that’s a substantial advantage. We believe our recent partnerships with Fiserv, MasterCard Vyze and GameStop are key indicators of our continued mission to forge the future of BNPL.

Finovate: How easy is it for consumers to qualify for BNPL compared to traditional consumer financing options? Who is left “holding the bag” if the consumer does not hold up their end of the bargain?

Lindenberg: The BNPL qualification process is drastically modern compared to that of traditional consumer financing options. We leverage proprietary technology and algorithms to assess the eligibility of each applicant across a variety of variables and approval can happen within minutes. There is no hard inquiry to the consumer’s credit history. It is in our own interest to approve consumers for an amount commensurate with eligibility. Our platform caters to purchases between $35 – $1,000 so the risk is relatively small. Less than 2 percent of our customers are late to make repayments in any given month – far below the national average for delinquent credit card payment. And in the event they are unable to pay, they can no longer make purchases on the QuadPay platform.

Finovate: Some critics of BNPL say that, unlike old-fashioned layaway programs, Buy Now Pay Later encourages consumption at the expense of saving. How do you think we should understand BNPL in the overall context of individual financial wellness?

Lindenberg: Financial responsibility is built into our model. Our mission is to provide consumers a transparent, financially responsible way to expand their spending power without the debt-spiral of credit cards. Installment payments are set to be charged automatically on the due date, so customers can just sit back and relax without worrying about missing a payment. QuadPay sends SMS and email reminders before installments are due so customers can make sure they have enough funds available to cover an upcoming installment.

In the event a customer can’t make a payment, we can adjust their payment schedule at their request. And if they stop making payments all together, they can no longer use the platform for purchases until the balance is paid. It’s really that simple and easy. There’s no impact on the consumer’s credit score and no interest accrues which is the real driver of most debt. We are here to help, not hurt, consumers. In fact, we have seen many consumers leverage QuadPay to expand their spending power for things like groceries, personal care, and other essentials particularly during COVID-19.

We very much see QuadPay as a critical first step for many consumers to learn and implement overall healthier budgeting habits which could ultimately improve savings.

Finovate: You recently announced a partnership with Gamestop. What is the significance of this relationship?

Lindenberg: The GameStop partnership was rolled out just ahead of the highly-anticipated release and pre-order availability of the new Sony PlayStation 5. It serves as a great example of how retailers can really leverage flexible payment solutions like BNPL to get the latest and greatest products into the hands of an enthusiastic customer-base ahead of the 2020 holiday shopping season.

We are thrilled to be partnered with GameStop, the world’s largest video game retailer, as they look to provide their customers with a simple and flexible way to pay over time both online and at the point of sale inside their more than 3,300 U.S. retail locations.

Finovate: QuadPay has also received significant backing from Goldman Sachs and Oaktree recently. What does this relationship do for QuadPay going forward?

Lindenberg: QuadPay has secured a committed revolving line of credit of up to $200 million from Goldman Sachs, with mezzanine financing provided by Oaktree Capital. The support of two strong institutions like Goldman Sachs and Oaktree is a testament to QuadPay’s leadership position within the BNPL industry.

Finovate: What is the future of Buy Now Pay Later? As a consumer financing option, what innovations have yet to be brought to this space that we might see in the next few years?

Lindenberg: The future for BNPL is very bright. We are only in the nascent stages of adoption in the U.S. market and expect installment payments to become as ubiquitous as “Visa accepted here” logos at checkout or at the register in-store. Consumers will begin to expect merchants to offer interest-free, installment payments as an alternative to high interest credit cards. We also believe that as contactless payments become more widely accepted, BNPL will continue to flourish.

On our part, we will continue to introduce new features and capabilities that make it easier to search and find particular types of items across retailers so shoppers can find the best deals on the items they want. We recently acquired Urge, a retail search engine providing shoppers access to all the world’s leading brands, stores and online retailers in one place which will change the game for BNPL globally.

How have the major secular trends in fintech been impacted by the COVID-19 crisis?

In his afternoon presentation at FinovateWest Digital, November 23 through 25, Jacob Jegher, President of Javelin Strategy and Research, will take a close look at which innovations in fintech are moving the needle in terms of boosting customer engagement, creating efficiencies, and helping financial institutions and financial service providers grow revenues.

Formerly Vice President of Global Solution Marketing and Head of Analyst Relations at FIS and, before that, serving for more than a decade as Research Director for Celent, Jegher brings a wealth of knowledge and experience in the banking technology industry. In addition to being widely cited in both mainstream and financial media – including The Wall Street Journal, The Globe and Mail, Bloomberg, and The New York Times – Jegher is a judge and coach at the Innotribe Startup Challenge.

“There are so many different pieces that (fintechs and financial institutions) have to watch out for in changing times,” Jegher told Finovate VP Greg Palmer during the Finovate Podcast earlier this year. “Pitfalls today include: how do you manage your budget and your cash flow associated with investment? What are you going to decide to keep pushing the envelope on and what’s going to get cut back? It’s just a realistic point of view given what’s taking place with company budgets – whether they are fintechs or financial institutions.”

To catch Jegher’s presentation at FinovateWest Digital – as well as the rest of our three-day, all-digital fintech event – visit our FinovateWest Digital hub and save your spot today. Take advantage of Early Bird discounts when you buy your ticket by November 13.

Small business banking solution provider BlueVine announced late last week that its BlueVine Business Banking offering is now generally available for small businesses looking for an integrated banking, payments, and lending solution. BlueVine Business Banking gives SMEs online services and tools to help them manage their finances, deposit checks, transfer funds, and make bill and vendor payments. The solution includes BlueVine’s Business Checking product, which the company said had seen “rapid adoption” by its customers during the recently-concluded beta testing period.

“Now more than ever, small businesses need simple, easy-to-use financial solutions, services, and guidance that support – not nickel-and-dime – them on their path to recovery amid the pandemic,” BlueVine CEO and co-founder Eyal Lifshitz said. “Over the last year, we have worked tirelessly behind the scenes to innovate and iterate on our BlueVine Business Checking product based on tremendous beta customer reception and feedback. We are thrilled to provide all small business owners with access to sign up for an account today, to help them achieve a better financial tomorrow.”

BlueVine Business Checking offers 1.0% interest on balances of $1,000 or more. Beginning this month, the company will offer 1.0% interest with no minimum balances – up to $100,000. The accounts include two free checkbooks, and no monthly ATM, NSF, or incoming wire fees. SMEs get unlimited transactions with no minimum balance requirements, and business owners can apply for the accounts in as little as 60 seconds.

BlueVine notes that more than 20,000 small businesses have signed up for the company’s Business Banking Accounts, which will also now feature BlueVine Payments. This enhanced billpay functionality enables businesses to pay vendors and bills from a directory of more than 40,000 common billers and registered payees – as well as setup their own payee. Businesses can pay by bank account or debit card, and the company’s payment is then sent to vendors by ACH, wire, or check. BlueVine added that payment by credit card is currently in beta testing.

The new product launch was also an occasion to announce a new partnership. BlueVine said that it has teamed up with fellow Finovate alum – and Visa acquisition target – Plaid to enable its small business banking customers to access external accounts when making payments or other transactions via the BlueVine dashboard. The partnership will also add BlueVine as a supported bank account on the Plaid Exchange Network.

Founded in 2013 and making its Finovate debut one year later at FinovateFall, BlueVine has raised more than $767 million in equity funding, most recently announcing a $102.5 million investment in November 2019. The company picked up a debt financing with Atalaya Capital Management that enabled them to secure a $75 million revolving credit facility in September. In August, BlueVine teamed up with DoorDash to help restaurant owners apply for Paycheck Protection Program (PPP) loans.

BlueVine’s participation in the PPP this year has been notable. The company said that it processed more than 155,000 emergency government loans for SMEs, valued at more than $4.5 billion, as part of the relief effort.

Just a few months after buying U.K.-based financial service price comparison site Know Your Money, NerdWallet is back at the register with another big purchase. The company announced late last week that it had agreed to acquire online, small business lending marketplace Fundera. Terms of the transaction were not disclosed.

The acquisition enables NerdWallet to expand its offerings for small business owners, and adds to the financial wellness platform’s content and marketplaces for products including student loans, insurance, mortgages, and investments. Founded in 2013 by Jared Hecht, Andres Moran, and Rohan Deshpande, Fundera will become a NerdWallet subsidiary as a result of the transaction, with all of Fundera’s employees joining NerdWallet.

In a statement, NerdWallet co-founder and CEO Tim Chen pointed to the small business market as an area of “tremendous opportunity” that the acquisition will enable his company to pursue.

“Although we offer free tools and content, we’ve never been able to fully support small business owners — that changes today,” Chen said. “Fundera has been one of our partners for several years and their deep understanding of the SMB market, the long-standing, trusted relationships they’ve built with both lenders and business owners, and their commitment to putting the needs of small business owners first is really unique and impressive.”

Founded in 2009 and headquartered in San Francisco, California, NerdWallet offers personalized, objective, actionable financial guidance to help consumers make intelligent financial decisions. Via its website and app, NerdWallet provides consumers with free access to its expert content and comparison shopping marketplaces to enable them to save time whether they are looking for insights into the best credit card for their needs or assistance in buying a first home.

NerdWallet has raised $105 million in funding. The company includes Camelot Financial Capital Management and Institutional Venture Partners (IVP) among its investors.