This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Intelligent conversational chat technology is on its way to the 174,000+ members of Michigan-based United Federal Credit Union. The institution, which serves customers in neighboring Indiana and Ohio as well as in Arkansas, North Carolina, and Nevada, has teamed up with Finn AI to add the chatbot service to its suite of digital banking offerings.

United FCU will integrate the technology into its LivePerson-based live chat system, which provides credit union members with immediate assistance for routine queries. The integration will enable human agents to spend more time on complex customer services issues and allow the automated technology from Finn AI to handle everything from account access problems to forgotten passwords.

“The pandemic has increased the need for financial services companies to provide a superior customer experience,” said Finn AI CEO Jake Tyler. “United realizes the importance that digital and AI have in delivering on this promise. We look forward to partnering with them as they lay out the future of their customer service offering.”

A two-time Finovate Best of Show award winner, Finn AI leverages artificial intelligence to deliver an intelligent chatbot solution that provides optimized, out-of-the-box support for 500+ of the most commonly-requested banking queries and questions. Finn AI’s chatbot technology can interact with customers over a wide range of channels: from websites and native apps to popular messaging platforms such as WhatsApp and Facebook. With Finn AI, institutions can inexpensively expand service availability, onboard more customers faster by streamlining basic processes, improve customer engagement, and reduce handling time.

Founded in 2014, Finn AI is headquartered in Vancouver, British Columbia, Canada. Over the summer, the company announced a partnership with Genesys to add its banking chatbot to Genesys’ AppFoundry marketplace of customer experience solutions. Finn AI includes ATB Financial, Fidor Bank, and fellow multiple-time Finovate Best of Show winner MX among its customers and partners.

When it comes to taking advantage of the best that the world’s fintech has to offer, you won’t find financial services companies in Canada sleeping on the job. This week in the country’s payments space, Toronto, Ontario-based Versapay announced its acquisition of Solupay, a contactless payments company based in Ohio. We also learned that FinovateEurope alum unblu, which offers a digital conversational platform for FIs from its headquarters in Basel Switzerland, had teamed up with Calgary, Alberta-based digital technology solutions provider Celero.

By the end of the week, Canada’s largest credit education company, Borrowell, announced that it was partnering with multiple Finovate Best of Show winner MX. Borrowell, the first company in Canada to offer free credit scores via its partnership with Equifax, has launched a new bill tracking feature called Boost on its app. The company will use MX’s data cleansing technology to improve Boost’s analysis of user spending behavior to help users make better financial planning decisions.

“With MX, Borrowell is giving its customers greater clarity into how they can become more financially strong as a means to increasing credit strength,” MX Chief Customer Officer Nate Gardner said. “It is exactly this kind of innovation, partnership and money experience that MX loves to enable through our powerful data platform.”

Last week we featured an extended Q&A with Eric Rosenthal, Vice President and Managing Director for the Americas with Rapyd. If you’re interested in learning more about the fintech ecosystem in one of the most overlooked regions of the world, our conversation with Eric Rosenthal is a great place to start.

With that in mind, congratulations to Mexican challenger bank Klar, which raised $15 million in Series A funding in a round led by Prosus Ventures this week. Founded in 2019, Klar now has approximately $72 million in total debt and equity financing, and noted that the new capital will help the company build its engineering capabilities in its hubs in Berlin and Mexico.

“Klar is making credit accessible to all Mexicans, including those with no credit history,” Klar co-founder and Chief Financial Officer Daniel Autrique said. “We help people build credit by looking at how and where they spend their money, instead of being stuck with traditional credit scores that are backward looking and obsolete.” The company said that, since inception, it has issued more than 25,000 lines of credit among its 200,000 customers.

Here is our look at fintech around the world.

Sub-Saharan Africa

Stripe makes inroads in Africa with acquisition of Paystack.

A partnership between Standard Bank, Mastercard, and Google will help SMEs in Africa offer their services online as well as accept digital payments.

Trading Technologies teams up with Cape Town-based Applied Derivatives, which will distribute the TT platform from South Africa.

Central and Eastern Europe

PayRay, a factoring company based in Lithuania, receives banking license and begins banking operations in its home country.

Lithuanian online payments firm Interpaylink partners with iDenfy to provide remote user identification.

Advapay, a digital core banking platform provider based in Estonia, teams up with U.K.-based identity verification platform Sumsub.

Middle East and Northern Africa

Cairo, Egypt-based financial wellness platform NowPay raises $2.1 million in seed funding.

Central Bank of Bahrain launches the region’s first digital fintech lab, FinHub 973.

Commercial Bank of Dubai introduces cards and accounts for low-income consumers courtesy of partnership with Now Money.

Central and Southern Asia

Indian payments processor Razorpay secures $100 million in Series D funding, earning a valuation just over one billion.

Mastercard announces partnership with Indian regtech Signzy to bring the company’s video KYC technology to its banking customers.

Indian fintech Open partners with Equitas Small Finance Bank and Visa to offer business debit card.

Latin America and the Caribbean

Brazilian payment solutions provider Ebanx announces expansion of operations into five countries in Central and South America.

Venio, a mobile app that provides financing to the unbanked, goes live in Mexico.

Chile’s third largest bank, Banco de Crédito e Inversiones (BCI), partners with Temenos to launch new corporate bank in Peru.

Asia-Pacific

The People’s Bank of China holds lottery to distribute millions in digital yuan valued at $1.5 million.

Vietnamese online payment portal AppotaPay scores payment intermediary license from State Bank of Vietnam.

PayMaya, a mobile payments platform based in the Philippines, launches new mobile payment device PayMaya One Lite, that enables acceptance of a range of digital payment types.

In a venture round featuring Motley Fool Ventures and Ally Ventures – the strategic investment arm of Ally Financial – as well as individual angel investors, Streetshares has secured $10 million in new funding. The company said that it will use the capital, which takes the company’s total to more than $279 million, to drive future product development with an eye on serving small businesses in the post-PPP market.

“We’re seeing exciting digital adoption by banks and credit unions in response to COVID-19,” said StreetShares CEO Mark L. Rockefeller. “But equally important to us is the practical impact our technology is having in helping their customers, especially underserved business owners, get the funding they need to succeed.”

Founded in 2013 and launched a year later as an affordable digital lending alternative for veteran-owned small businesses, StreetShares unveiled its lending-as-a-service platform last year at our annual fintech conference FinovateFall. The platform enables banks to lend up to $250,000 to SMEs, and features a digital loan application, instant underwriting, loan servicing, and tracking. The company’s offering came in handy this year when the coronavirus struck and businesses across the country were shut down and starving for financial assistance. StreetShares’ technology was leveraged widely by community lenders in order to make Paycheck Protection Program funds available to SMEs.

As such, so far this year, a total of 53 financial institutions currently use the StreetShares platform. The company said that it is now expanding its platform into a suite of small business banking solutions that will be especially helpful for community banks, credit unions, and their small business clients as digital transformation initiatives continue in the wake of COVID-19.

“We’re seeing years of digital adoption by banks condensed into weeks,” said Ollen Douglass, Managing Director of Motley Fool Ventures. “Beginning with PPP, and now on to a full-suite of products, we believe StreetShares is positioned perfectly to power banks in their digital transformations.”

StreetShares is headquartered in Reston, Virginia. Read our profile of the company from last summer as StreetShares was stepping up to help bring needed financing to SMEs at the onset of the COVID-19 crisis.

Another day, another acquisition in the payments space: U.S. payment processor PaymentCloud announced this week that it has acquired contactless payments provider Paysley. Payment Cloud purchased the majority share of the Los Angeles, California-based company; the amount of the transaction was not disclosed.

Paysley’s technology enables customers to use their smartphone as the point of sale device – without having to set up an account with the merchant in advance. Paysley leverages QR code technology – an approach common to payments in South Africa where the company’s founders are from – to power secure mobile payments directly from the user’s card, Apple Pay, or Samsung Pay account.

And with one-click payment verification, Paysley’s solution works well with the kind of transactions that are increasingly popular in our post-COVID, gig economy, subscriber-based, P2P world.

“The future of payments is already shifting toward contactless means and now, with the acquisition of Paysley, we will be at the forefront of this shift,” PaymentCloud CEO Shawn Silver said. “I’m eager to bring this innovative solution to fruition at such a pivotal time.”

Currently in the process of relocating its 55 employees to new offices in Encino, California, PaymentCloud processes credit cards for thousands of clients around the country. The firm also works with more than 80% of the top digital independent sales organizations (ISOs) to help them boost approval rates, onboard merchants quickly, and limit attrition.

Named to Digital.com’s list of the Best Credit Card Processing Services of 2020, and ranked #295 on the Inc. 5,000, PaymentCloud was founded in 2016.

The growing presence of BigTech in the fintech ecosystem is one of the stories of 2020 that will likely be among the top stories of 2021, as well. As companies like Apple, Google, Amazon, and Microsoft look to fintech for new markets and opportunities to innovate, how will their relationship with the fintech ecosystem evolve and change?

For a few answers to this and other questions, check out our interview with Microsoft’s Sandeep Mangaraj and Tom Feher, industry executives, Digital Transformation, Financial Services. Both Mangaraj and Feher participated in our all-digital fintech conference, FinovateFall Digital, in September.

What is the value of partnership as BigTech becomes more involved in fintech?

Mangaraj: Microsoft leads with partners. That’s been true throughout our history and especially given what we are facing now, all the uncertainty and challenges that our partners are facing. I don’t see that changing. Our partners were quick to respond to what happened with COVID. They leveraged the power of our platform, and they were there immediately with creative and innovative solutions.

That has been the story of Microsoft. What is it that we provide? We have a secure, compliant, scalable platform that they can innovate on, and we are here to help them and support them, and make sure that they take advantage of the full power of what we offer, what they offer, and what our other partners offer, to take to their clients.

Feher: Partners are key to our success. We have several programs to help incubate and expand our fintech ecosystem. This includes everything from Microsoft for Startups, a program that assists startups in building solutions on our platform, to our M12 Ventures program that invests in a portfolio of fintechs in the industry. We also have our worldwide partner organization that focuses on strategic alliances and partnerships with fintechs that enable us to bring net new solutions to market on our platform that accelerate our clients’ innovation and well as helping them drive business outcomes.

The following is a guest post from RJ Sherman, VP of Innovation, Citizens Bank.

The word innovation is often thrown around casually to describe anything new that an organization is doing. However, for an organization to be truly innovative, it must adopt an “innovation mindset.”

Broadly, this means the organization needs to: take an empathetic approach to customer research to fully understand the customer’s needs; think longer term to identify potential disruptors that are further out on the horizon; and “test and learn, fast and cheap” by quickly exploring new ideas in a calculated manner to understand their value.

Innovation is more than simply creating new products or exploring emerging technologies. Innovation means acting on ideas that accelerate growth and challenge the status quo.

Here are five specific ways an organization can foster innovation:

Focus on the customer experience

Innovation starts with a deep and nuanced understanding of the customer journey and the associated pain points. Innovating for the sake of innovation doesn’t work – instead, use your customer’s pain points as a ‘North Star’ and design a compelling offering around them. Don’t be afraid to iterate in partnership with your customers (the solution is for them, after all). Despite the pandemic, there are still many ways to collaborate and co-create with customers, it just requires us to be more creative with how we conduct research.

Take a balanced approach to building the innovation portfolio

A balanced innovation portfolio is made up of opportunities from all areas of the business, including internal (organization-facing) and external (customer-facing) opportunities. This is critical as it signals to colleagues that all aspects of the business play a role in positioning the organization to win in the future. Continuously monitor your balance and partner with executive leaders across the organization to identify and explore strategically aligned opportunities (especially in underrepresented business areas).

Partner with fintechs when and where appropriate

While fintechs can pose a threat to financial incumbents, there is a significant opportunity for banks and traditional financial institutions to join forces to better serve the customer. Fintechs have a significant advantage when it comes to designing great customer experiences, but lack the customer relationships, scale, expertise, or risk management muscle needed to operate as broad-based financial services institutions. Fintechs can help power and accelerate a smart, data-enabled strategy, and offer a quick and relatively low-risk way to support business strategies.

Create the appropriate organizational mechanisms to explore early stage ideas

Citizens is investing in innovation using an Innovation Fund as part of its annual Tapping Our Potential (TOP) program. The fund operates like an internal venture capital firm, placing small-scale investments in colleague ideas. It is a great way to generate a grassroots movement around innovation and invest in the ideas of colleagues.

Encourage idea generation from everyone in the enterprise

When someone asks me “how big is the innovation team at Citizens?” I say 18,000 colleagues because every person at our organization has a role to play in innovation. Encouraging colleagues to participate in innovation begins at the top and, if done successfully, colleagues will buy-in and it will be embedded into everything you do. That way, when it comes to evaluating new opportunities or reimagining traditional business lines, innovation will always have a seat at the table.

To sum up, there isn’t a single “one size fits all” innovation model that will work for every financial institution to bring new ideas to life. Instead, leaders must create a bespoke solution for their organization, establishing mechanisms to leverage the cumulative power of their colleagues to identify and solve for the most pressing customer problems.

It is a truism that many of our greatest technological innovations have come as a result of trying to empower people challenged with physical limitations. Whether the circumstances are sensory, mobility-oriented, or cognitive, the role of technology for many of us is to make the phrase “differently-abled” something more than a politically-correct euphemism.

The rise of mobile banking itself has been a tremendous boon for many disabled customers, rendering unnecessary those often-expensive, time-consuming, and potentially dangerous regular visits to physical bank branches. Technologies that turn text-into-speech or that enable speech to drive digital processes have revolutionized access to financial services for those with sensory limitations. Even more modest innovations that enable seamless debit card spending controls and transaction monitoring are valuable tools not just for small business owners, but for caretakers of adults with limited cognitive capacity, as well.

In financial services, there have been even more focused efforts to serve the adults with disabilities. One is to build institutions that are dedicated to serving populations that have been overlooked in general because of “able-ism.” Purple is a challenger bank that was launched over the summer by a company called youBelong, who built the first social network for “people with special needs.” The bank is the evolution of youBelong’s mobile bank for families with special need children, youBelong Cash, and emphasizes financial literacy and education as a strategy for helping people with disabilities enjoy security and independence.

Founded by CEO John Ciocca, Purple offers a digital savings account with no hidden fees and no minimum balance. Account holders can set up their accounts to receive any Social Security Insurance and Disability payments they are eligible for. Access to PFM features such as money transfers and transaction tracking are included in Purple’s banking app. The accounts come with a Purple Mastercard Debit card, and Purple donates a portion of its revenues to the Special Olympics with every card transaction.

Among fintechs, True Link Financial is a company that has dedicated itself to improving the financial well-being of people with disabilities as well as vulnerable older adults. Payment cards that can be administered by a responsible family member or guardian on behalf of an intellectually-challenged adult, for example, are among True Link’s offerings. The company announced a $35 million Series B round over the summer and its founder and CEO, Kai Stinchcombe, highlighted the way the platform can serve people with disabilities.

“When we launched the True Link Card, it quickly became clear that its features could protect a wider range of people who weren’t being served by traditional financial institutions,” Stinchcombe wrote. “We found that people with disabilities and individuals in recovery from addiction could use our product to meet their unique needs and circumstances.”

Other Finovate alums – from Best of Show winner Golden to Eversafe – also have platforms geared toward helping vulnerable seniors that can be similarly leveraged to benefit members of the disabled community and their families.

Still there are significant challenges. According to a Pew Research Center study from 2017, the rate of technology adoption among the disabled across age groups lags behind those without disabilities – and significantly so in some areas. The home broadband gap between seniors with disabilities and seniors without disabilities is more than 20%. The smartphone gap between non-seniors (ages 18 to 64) with disabilities and non-seniors without disabilities is 17%. If anything, the research suggests that an emphasis on not just the disabled, but disabled seniors in particular – where smartphone and home broadband adoption rates are below 40% – would go a long way toward helping the neediest among those with disabilities.

A new merger in the payments space will bolster the accounts receivables and payments solutions available to small and medium businesses. Versapay, a customer-centric order-to-cash solution provider based in Canada, announced this week that it has completed its merger with Twinsburg, Ohio-based, payment services provider Solupay. The combined entity will operate as Versapay in name and will be led by the company’s current CEO Craig O’Neill.

Financial terms of the deal were not disclosed. But the merger does include a pair of Solupay subsidiaries: payment processors ChargeLogic and 2CP. Solupay’s technology simplifies payment acceptance, provides click-to-pay invoicing, and automates AR processes, and will give Versapay additional opportunities to serve its SME customers.

“Simplifying invoice presentment and reducing the cost of accepting digital payments are the building blocks for a customer-centric order-to-cash process,” O’Neill said. “We’re excited to welcome the complimentary capabilities of the Solupay team and its innovative integrated payments and AR automation technology as we seek to better serve businesses through their digital payments transformation.”

Founded in 2006 and headquartered in Toronto, Ontario, Canada, Versapay has a worldwide network of 8,000 customers and 50,000 users, accounting for $10 billion in payment volume a year. The company’s solutions help businesses accelerate cash conversion, automate manual processes, as well as reduce costs and boost efficiency.

Versapay was acquired by Great Hill Partners in February in a deal that valued the company at $96 million (CAD $126 million).

A pair of partnerships this month have helped Unblu bring its digital conversational platform to a larger number of financial services customers. The company announced at the beginning of the month that digital technology solutions provider Celero will use Unblu’s conversational platform to enable its credit union customers to leverage digital channels to better engage with their members. The integration adds to Celero’s digital banking platform, Celero Xpress, which is powered by another Finovate alum, ebankIT.

“Our new digital platform offers credit union members an intuitive, engaging and secure digital banking experience,” Celero General Manager for Digital Banking Dean Rathwell explained. “By integrating Unblu, our clients can ensure these digital experiences also deliver a personal connection, which is core to the credit union difference.”

Set to launch later this year, the enhanced Celero Xpress platform will provide must-have communication functionalities such as live and video chat, as well as messaging and collaborative co-browsing. The platform is connected to Celero’s digital ecosystem, Celero Xchange, which leverages modern APIs to enable institutions to integrate their own or third party applications. Headquartered in Calgary, Alberta, Canada, Celero was founded in 2003 and counts more than 110 credit unions and financial institutions in Canada as its customers.

Unblu’s partnership with Celero came just a week after it announced that it had teamed up with Luzerner Kantonalbank (LUKB), the leading retailing banking group in the Swiss canton of Lucerne with more than $46 billion (CHF 42 billion) in assets as of 2019. LUKB has begun a pilot project to test an online customer advice feature powered by Unblu’s conversational platform. The feature uses a hybrid approach, with customers engaging with a live LUKB agent who works in tandem with the customer by way of Unblu’s screen sharing technology.

“With this new online function, LUKB’s advisors can make the documents on their screens visible on their customers’ devices. That way, the documents or online applications can be clearly explained in a conversation,” LUKB Head of Digitization and Multichannel Management Stefan Lüthy said. He added that while the new solution will save customers a trip to the branch, it is not intended to replace in-person meetings and consultations.

Headquartered in Basel, Switzerland, Unblu made its most recent Finovate appearance at our European conference in Berlin earlier this year. Unblu was founded in 2012. Luc Haldimann is CEO.

Even before the onset of the global health crisis, banks and other financial services companies were moving in the direction of greater digitization to improve efficiency, cut costs, and most importantly, deliver new and enhanced products and services to an increasingly-tech savvy – and tech-dependent – consumer.

But do firms in the financial services space need to do more than just digitally transform themselves? What strategies do these businesses need to adopt in order to further differentiate their offerings from rivals? How can they provide their customers with the kind of personalized, low- to no-latency, access anywhere, digitally-oriented service their customers have come to expect from all institutions – public or private, large or small, financial or not?

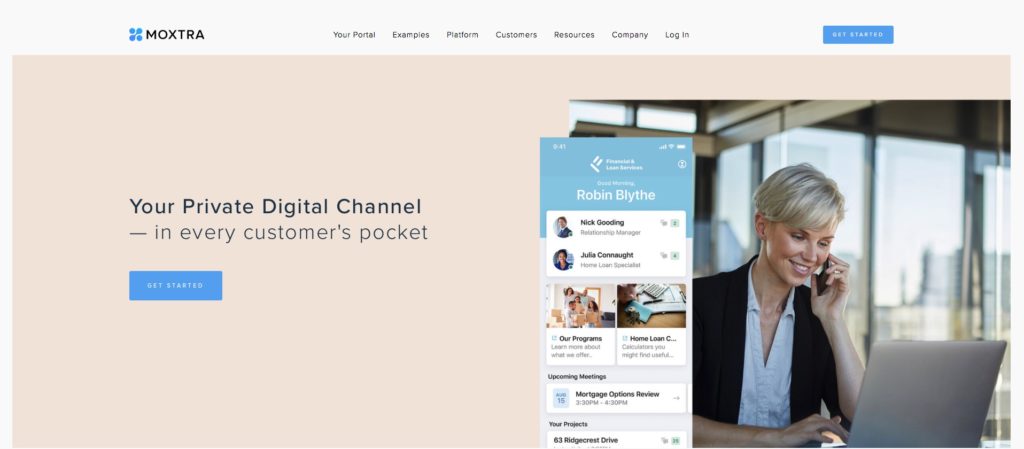

For this week’s Finovate Alumni Profile, we caught up with Stanley Huang, Chief Technology Officer for Moxtra, to discuss these challenges. Specifically, we talk about what he calls the “marketing mindset” that financial services businesses need to adopt in order to not just survive, but thrive in these uncertain times. A leading business collaboration platform designed for the mobile era, Moxtra offers an embeddable omni-channel client engagement solution for financial services companies. The company, founded in 2012 and headquartered in Cupertino, California, has been a Finovate alum since 2016.

Finovate: Digital transformation is the major buzzword for companies right now – understandably. However, would you say that there is more to making it through the current crisis – to say nothing of coming out better on the other side – than just digital transformation? What else do companies need to do?

Stanley Huang: Digital transformation is inevitable but it’s more about the overall industry transformation that needs to take place, especially in an industry like finance and banking which has been slower to adopt more modern, digital solutions. We encourage our customers to leverage this crisis in order to finish the long-term business service model transformation. It’s like shifting from using taxis to Uber.

Consumers have grown accustomed to and reliant on mobile in their interactions with businesses for more than a decade now, and that has raised customer expectations of all businesses fundamentally. It’s simply the reality, and it’s time for laggards to embrace that reality. In order to compete today, you need to place a premium on providing on-demand service with instant response and serving every client as a high-touch customer. The mobile era has created a level of service that customers are accustomed to – so getting ahead of the expectations and needs of customers is vital to better ensure loyalty during the entirety of the customer lifecycle, which in the financial industry is a lifetime if done right.

The silver lining of seemingly being forced into digital transformation during this unique time is that it’s serving to benefit not just some, but all customers in this time capsule we’re experiencing. Now is the time to ensure that no age demographic is left behind in the pursuit of digital adoption, for example. For financial institutions that previously didn’t have something like a OneStop Customer Portal to serve customers virtually, that was a missed opportunity to attract the younger generations who have grown up with mobile and digital solutions as an expectation, not a luxury.

And for financial institutions that had a digital solution headed into the pandemic, this period of time serves as a unique environment to bring older generations into the fold that previously may have been hesitant to do business virtually. Show them what they can do — safely — both physically and from a cybersecurity standpoint, with a OneStop Portal solution. Ensuring they feel comfortable to be served via this new channel with both a secure and user-friendly interface will make them a lifelong virtual banker, benefiting both parties long term.

Finovate: You’ve discussed a concept called a “marketing mindset” that you think more businesses need to adopt in order to survive and thrive in the current environment and beyond. What is a marketing mindset? Why do companies need it and how do they get it if they don’t have it? How did you come to this insight?

Huang: When we talk about doing business with a marketing mindset, it goes back to the shift in importance to how you provide service vs. what you offer – it’s evolving from a “product mindset” to a “marketing mindset”. By that, we mean creating a customer experience that is centered around brand consciousness. Marketers are naturally focused on this concept of brand consciousness in their role as they own the responsibility of overseeing the execution of how the brand is presented to customers as well as the messaging that is circulated. Oftentimes, banks aren’t as self-aware of their brand identity when interacting with customers on a day-to-day basis as they really should be.

Banks must have a marketing and customer-centric mindset to succeed in a digital age that has heightened consumer expectations for the type of experience they expect to receive, especially by an institution that is responsible for something so personal and important to them as managing their money.

When customers have other options for who they bank with, financial leaders — no matter their role — should consider leading with a marketing and customer-centric mindset to appeal to and retain customers. If this frame of mind and way of doing business isn’t innate within the company, it is up to bank employees to educate and promote the benefits of this new approach to banking. Especially during the early adoption phase of digital banking, a thought-out, handshake-replacing approach to doing business digitally is what will help banks gain customer confidence and trust to earn their loyalty long-term. If approached with a marketing mindset, your advocacy and education about this new approach to doing business will aid in customer adoption, comfort and, ultimately, loyalty.

Finovate: What industries or companies are doing the best job of embracing this mindset? Is there a reason why these businesses are better able to adopt a marketing mindset compared to other businesses/industries?

Huang: Industries embracing this mindset best are those that have the greatest reputations to uphold in comparison to other top-notch brand experiences, such as in retail and CPG (consumer packaged goods). While antiquated government institutions and utility companies can coast by with a lower caliber of service, retail and CPG brands can’t afford to slip up on the customer experience advertised — especially with all of the options available to consumers and the likes of Amazon coming for their customers.

That’s why retail banks serving your everyday consumer such as Citibank came to us to ensure the experience it offers its customers is thoughtful, thorough and robust to match their in-person banking experience, and in some ways surpass it with on-demand relationship managers.

High-touch businesses like Citibank are our sweet spot of service, because their OneStop Digital Branch requires comprehensive, collaborative capabilities — both on the front end and back end — that can manage a more complex level of services than a simple e-commerce site or app by a retailer needs. Banks need capabilities like secure messaging, digital signature, and a seamless tracking of finances, transactions, and banking communications in real-time.

High-touch businesses, such as those in the financial industry, law, real estate, education, event planning, etc. are the type of companies and organizations that may be slight laggards with digital transformation not because they don’t value their customers, students and other stakeholders, but because ten years ago the technology wasn’t out there to facilitate the complex facets of their business virtually in the way that a simple online clothing retail operation can pull off. We are working to fill that need at Moxtra with our Digital Branch Solution.

Heading into the new year, many fintech observers believed that customer experience would be as big a theme in 2020 as it was in 2019. And while the specific circumstances of that bigness (i.e., a generational global health crisis) were not anticipated by anyone, the importance of the customer remain as key theme this year as many thought it would be – if not more so.

This makes our upcoming conversation at FinovateWest Digital about the customer experience in 2020 and beyond so compelling. Joining us on Day Two of our all-digital, fintech conference next month are Sunil Dixit, Managing Director at BBVA, and Jeremy Balkin, Head of Innovation with HSBC. The two will take on the topic of how to create a customer experience that goes beyond insights to actually “surprise and delight” consumers.

Sunil Dixit leads the delivery of digital transformation of the consumer/retail bank for BBVA’s Global Client Solutions division. Based in Madrid, Spain, Dixit joined the company in 2017 after a tenure at Barclays where he led on strategy, embracing disruptive technologies, and the start-up ecosystem. Most recently, he has led development of BBVA’s open banking strategy and governance worldwide.

No stranger to Finovate audiences, Jeremy Balkin is Head of Innovation with HSBC Bank USA. The New York-based analyst serves on the bank’s retail bank management committee and manages the fintech innovation and exponential growth strategy for North America. Balkin is also the author of Investing with Impact: Why Finance is a Force for Good and Millennialization of Everything: How to Win When Millennials Rule the World.

Together Dixit and Balkin will address how financial services companies can avoid the dead-end of price competition and instead add new services, products, rewards, and benefits to differentiate their offering and improve the customer experience. They will look at how COVID-19 has impacted consumer preferences and what data science and other enabling technologies can be employed to help firms gain and act on insights into their customers’ preferences.

Learn more about our upcoming presentation on Customer Experience in the Post-COVID era. And visit our FinovateWest Digital hub to register today and save your spot.

Two of the biggest phenomena in fintech worldwide: the rise of open banking and the growth of digital-first (and digital-only) banking, continue to make an impact on fintech as well. One example of that is today’s news that NYMBUS has partnered with PeoplesBank to help the Massachusetts-area financial institution launch its digital-only extension, ZYNLO.

“Only NYMBUS provided us a comprehensive strategy to quickly introduce a new digital-only effort,” PeoplesBank Brian Canina, Chief Financial Officer said. “Backed by and running in parallel to our established institution with 135 years of experience in creating satisfied customers, ZYNLO delivers the ideal combination of digital banking convenience and security that today’s consumers depend on.”

PeoplesBank’s new offering is a no-fee savings account that includes features like Zyng, a round-up savings benefit that rounds up debit card purchases to the nearest dollar and adds the difference to the customer’s ZYNLO account. The company is currently offering a 100% round-up match for the first 100 days, with a 10% match on debit card transactions afterwards. ZYNLO also offers Early PayDay and daily balance and payment alerts, and all deposits are insured via FDIC and DIF.

Today’s news represents an extension of the partnership between the two companies. At the beginning of the year, PeoplesBank announced that it would deploy NYMBUS’ SmartMarketing and SmartOnboarding platform to boost revenue growth and enhance customer engagement. With more than $3 billion in assets under management PeoplesBank is the largest community bank in Western Massachusetts, with 20 banking centers in Massachusetts and Connecticut.

Founded in 1885 and headquartered in Holyoke, Massachusetts, PeoplesBank recently announced that its latest new branch in South Hadley will feature VideoBanker ITMs, a combination of an ATM and a virtual teller that Canina said mitigates the need for drive-up teller windows. The innovation became a necessity when the municipality issued a zoning restriction that required the new branch building to be located closer to the street, making a traditional drive-up window problematic.

Most recently demonstrating its SmartLaunch digital banking solution at FinovateFall last year, NYMBUS has since inked partnerships to deploy the technology with Centier Bank, BankMD, and Pacific National Bank. Over the summer, NYMBUS secured $12 million in growth funding, taking the company’s total capital to more than $45 million. That same month, NYMBUS added Jim Modak as President and Chief Financial Officer.

In September, the company named former Kony DBX DVP and General Manager Jeffery Kendall as CEO. Kendall replaced former CEO and company founder Scott Killoh, who will continue with NYMBUS as executive chairman of the company’s board of directors.