This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Financial crime compliance company Napier AI has partnered with Romania’s Salt Bank.

Salt Bank will deploy Napier AI’s transaction screening solution to protect transactions against a variety of fraud risks.

Napier AI made its Finovate debut at FinovateEurope 2018 in London.

Romania’s first neobank, Salt Bank, has teamed up with financial crime compliance company Napier AI. Salt Bank will deploy Napier AI’s Transaction Screening solution to ensure that the hundreds of millions of transactions Salt Bank handles are safe from fraud risks.

“We chose the Napier AI platform because it offered NextGen technology which enables us to strengthen our financial crime controls and matches our drive to offer clients a seamless digital experience, within a robust regulatory environment,” Salt Bank CEO Gabriela Nistor said.

Salt Bank sought out Napier AI’s technology to ensure that it is able to keep pace with evolving money laundering, terrorist financing, and fraud risks on the one hand, and consumer demand for a seamless digital experience on the other. Napier AI’s Transaction Screening product features a user friendly interface with customizable workflows, a cloud-based deployment, a sandbox environment for optimizing screening configurations, and a configurable dashboard with no-code rule building and AI insights.

“Napier AI’s industry-leading Transaction Screening solution is set to help Salt Bank succeed in setting a new standard for banking in Romania,” Napier AI CEO Greg Watson said. “It is an exciting time for the industry and market, and I am excited to see how we work together to bring best-in-class financial crime compliance to the next generation of digital banking users.”

Founded in 2015 and headquartered in London, U.K., Napier made its Finovate debut at FinovateEurope in 2018. At the conference, the company demoed its Customer Screening and Transaction Monitoring Enhancement software. By addressing gaps in current legacy systems’ AML and client screening solutions – and extending their shelf life – Napier’s technology enables organizations to enhance the performance of their current fraud prevention processes.

Napier AI’s partnership news comes one month after the company teamed up with impact asset manager Finance in Motion. Finance in Motion will deploy Napier AI Continuum – including its Client Screening solution and Client Risk Assessment module – as its AML and counter terrorist financing platform. Earlier this year, Napier AI secured an investment of $56.6 million (£45 million) from Crestline Investors.

“We are excited to work with the Napier AI team and believe their market-leading, AI-powered technology platform is well-positioned to help financial institutions and other regulated companies excel in an environment with rapidly expanding transaction volumes and increasing regulatory requirements,” Crestline Managing Director Will Palmer said when the investment was announced in February.

The week begins with a few research-related announcements in the fintech and financial services space. CB Insights announced the availability of its State of Insurtech report for the first quarter of 2024, and the Federal Reserve Board issued a summary of climate risk resiliences exercises conducted recently by a handful of big banks. While the focus on this column in on the former, the publication of the latter shines some light on potential answers to the problems raised in CB Insights’ report.

With regards to the state of insurtech, there is still a great deal of hesitation among investors. CB Insights noted that quarterly funding for Q1 of this year was only $0.9 billion, the lowest level since 2018. Property & casualty insurtech suffered the most, with a quarter-over-quarter decline of 25%. Q1 2024 was also the first time since 2018 that there were no “mega-round deals” – investments of $100 million or more. There was some good news in Europe, as the number of deals increased slightly, as did the median insurtech deal size. But the overall message continues to be caution when it comes to investor attitudes about investech.

What Ails Insurtech?

Digital disruption: The challenge of digital disruption is one that the insurtechs share with the broader fintech community. The rise of enabling technologies such as AI will both steepen customer expectations as well as accelerate competition between companies to effectively deploy new, innovative solutions.

The insurance business is ripe for innovation. From the massive volume of manual processes and the document-intensive nature of the business to the challenges of underwriting and refining statistical models, the idea that AI will be a powerful ally in the insurance business is a no-brainer. One firm, Zippia, has predicted that as much as 25% of the insurance industry could be automated via AI by 2025.

There are obstacles. The disposition of regulators toward change in the industry is a major concern as new technologies are introduced to enhance operations like underwriting and statistical modeling. A regulatory authority that is indifferent, or hostile, to new technologies or their application in certain use cases can send a powerful signal that innovators are better off deploying their solutions in other industries or other geographies. Looking at the U.S., if the behavior of regulators toward innovators in the crypto space and the Banking-as-a-Service space is any indication, then we can expect to see insurtech and their investors to tread cautiously.

There are also challenges with regard to talent. Now that almost every company in every industry is looking to up their AI game, the fight over top talent in AI and automation has become all the more competitive.

Nevertheless, there is no doubt that AI promises to revolutionize many key processes that insurers rely on. And as those processes become more efficient – and as those companies best exploiting those AI-enhanced processes take greater market share – it is easy to see investment dollars returning to insurtech as investors begin making their bets on winners and losers in the space.

Climate change: The impact of climate change is another instance in which challenge and opportunity go hand-in-hand for insurtechs. The growing incidents of extreme weather – from temperature extremes to increasingly powerful hurricanes, floods, and other phenomena – have put a major strain on both property and casualty (P&C) insurers as well as those homeowners and individuals who rely on their protection. Note that CB Insights reported the biggest quarterly drop in funding this year was among P&C insurtechs. And of the top 10 P&C insurtech deals of Q1 2024, only three were U.S. based companies.

While many fintechs involved in climate change and sustainability have focused on helping businesses and institutions measure and better manage their carbon footprints, there is a need for technology companies in the insurance space that can help these firms build the models they need to better anticipate climate change-related risk. I mentioned the Federal Reserve report on climate resiliency earlier. The Fed’s report was a summary of an exploratory pilot Climate Scenario Analysis (CSA) exercise held by six U.S. banks: Bank of America, Citigroup, Goldman Sachs, JPMorgan Chase, Morgan Stanley, and Wells Fargo. Among the conclusions that are especially relevant to this conversation were these two:

The role of insurance in mitigating climate change risks for consumers, businesses, and banks was emphasized, with a call to monitor changes in insurance costs and their impacts on specific markets and segments.

and

Participants expressed the high uncertainty and difficulty in measuring climate-related risks, making it challenging to incorporate them into risk management frameworks on a routine basis.

Insurtechs – and fintechs, for that matter – who are able to help financial institutions resolve these two issues, will find their services in demand as companies seek ways to quantify their own exposure to climate change risk. It is easy to envision other enabling technologies, such as quantum computing, also playing a part. Together, they could provide the kind of powerful modeling that would accurately gauge the risks of climate change and its potential impact on markets, communities, businesses, and families alike.

Temenos has launched Responsible Generative AI Solutions for financial services.

The GenAI tools allow bank employees to use natural language to query the engine, which will leverage banks’ data to generate unique insights and reports.

At launch, the new GenAI tools will be available within Temenos Wealth and Temenos Digital products.

Banking technology provider TemenoslaunchedResponsible Generative AI Solutions for financial services this week. The Switzerland-based company is making the solutions available as part of its AI infused banking platform, starting with its Temenos Wealth and Temenos Digital products.

Temenos’ new offering aims to change the way banks leverage their data, and the company anticipates they will ultimately improve banks’ productivity and profitability. Temenos’ new Responsible Generative AI solutions work similarly to other GenAI engines, such as ChatGPT, in that they allow bank employees to use natural language to query the engine, which will leverage banks’ data to generate unique insights and reports. Banks can use the new tools in processes ranging from managing existing accounts to brainstorming new products and mitigating financial crime.

“We all use AI in our daily lives and benefit from the personalized services and insight,” said Temenos President Product and COO Prema Varadhan. “Temenos Explainable AI offers transparent, auditable insights while our Generative AI infused platform delivers these insights instantly in an intelligent and personalized way. Temenos ensures responsible AI practices by providing explainability, security, safe deployment, and banking-specific capabilities. With our AI platform, banks can rapidly implement real-world use cases that enhance efficiency, boost profitability, and create hyper-personalized customer experiences.”

The “responsible” part of Temenos’ new tools lies in its transparency and explainability. Users and regulators will have visibility into the process and will be able to verify the results produced by the engine. The Responsible Generative AI solutions also have a permissions and access security framework to address data security and privacy concerns.

Banks can deploy the newResponsible Generative AI Solutions as standalone solutions or connect them with their existing core systems on-premise, on public or private clouds, or delivered via Temenos SaaS.

Temenos was founded in 1993 and offers solutions for retail and commercial banking, wealth management, payments, fund administrators, insurance companies, and more. The company has clients in 150 countries and offers solutions that touch 30% of the world’s banking population, equivalent to 1.2 billion people.

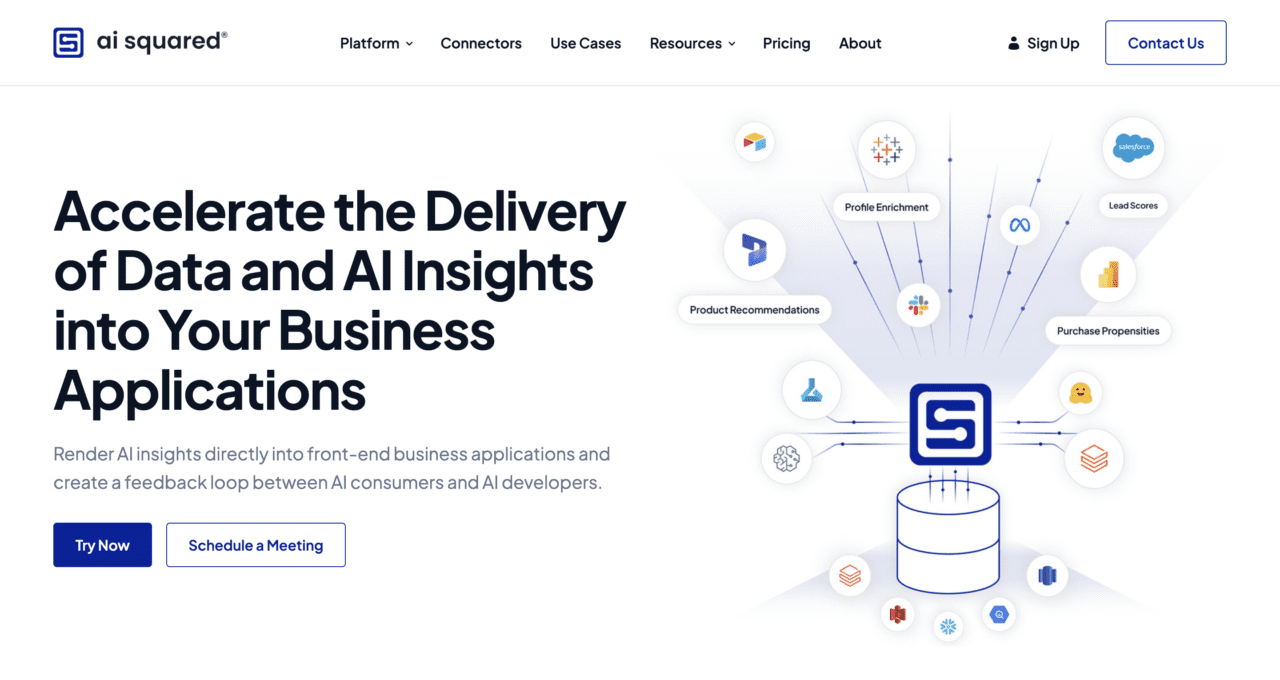

AI integration specialist AI Squared acquired open-source Reverse ETL (rETL) company, Multiwoven. Terms were not disclosed.

The acquisition follows AI Squared’s $13.8 million Series A funding round in April.

AI Squared made its Finovate debut at FinovateSpring 2023.

AI integration platform AI Squared has acquired open-source Reverse ETL (rETL) company Multiwoven. The transaction fortifies AI Squared’s ability to help organizations more easily move data and AI-based insights into business applications.

In a statement, AI Squared Founder and CEO Benjamin Harvey praised both Multiwoven’s technology as well as its open-source approach to innovation. “From my experiences as a data-science executive at the National Security Agency and as an early employee at Databricks, I recognize and respect the critical role that the open-source community plays in fueling innovation,” Harvey said. “Now as a singular organization, AI Squared and Multiwoven will continue to lead the way in open-source rETL, while simultaneously bringing critical data-movement functionality to our customers.”

Multiwoven is an open-source, reverse ETL platform that facilitates secure data segmentation, synchronization, and activation. The company’s technology makes it easier for firms to deploy this organized data into applications and business tools for sales, marketing, and advertising operations. By integrating Multiwoven’s rETL capabilities into its platform, AI Squared will be able to help organizations efficiently integrate robust data and AI insights into their applications.

“With our new combined team, we will be able to accelerate the development and growth of Multiwoven open-source, which will remain free to use,” Multiwoven Co-Founder and CEO Sojoy Golan said. “We are also excited to now introduce advanced capabilities to activate AI/ML data, together with AI Squared.”

AI Squared also will continue to support development of Multiwoven’s open-source technology. Golan called open-source “a wonderful enabler” that has helped uncover insights not only for Multiwoven’s own users and open-source contributors, but also for “the data practitioners on our Community Slack, and all the other generous people in the open-source community.” As part of the transaction, Multiwoven’s team will join AI Squared. Golan has been named Chief Product Officer; Multiwoven Co-Founders Nagendra Dhanakeerthi and Subin Thattaparambil will serve as Chief Technology Officer and SVP of Engineering, respectively.

Headquartered in Washington, D.C., AI Squared made its Finovate debut at FinovateSpring 2023 and returned to the Finovate stage later that year for FinovateFall in New York. In its most recent appearance, AI Squared demonstrated how adding Generative AI to the platform’s Predictive AI capabilities enables users to build tools such as chatbots to help them more efficiently query their data.

AI Squared was founded in 2019. Learn more about the company in our feature interview with AI Squared’s Benjamin Harvey.

Last week brought a small uptick in fintech funding and drama ensued when Tabapay renounced its agreement to purchase Synapse’s assets. Stay tuned to this week’s news for updates as this situation– and others– evolve throughout the week.

TangolaunchesGlobal Choice Link, to offer its business customers an easy platform to send rewards, incentives, and payouts to recipients across the globe.

REPAYbecomes a Certified Integration Partner with Corelation’s KeyStone platform.

U.K.-based challenger bank Monzo secured an additional $190 million (£150 million) in funding this week, adding to the $426 million (£340 million) raised just a few days ago. The Series I round, totaling $616 million (£490 million) gives the digital bank a valuation of $5.2 billion (£4.1 billion) and represents one of the biggest fundraising rounds for a European fintech since 2023.

The bank’s financial backers included Hedosophia and CapitalG, Alphabet’s growth fund. CNBC’s coverage of the funding notes that Singapore-based sovereign wealth fund GIC was also a participant in the funding, but GIC has yet to confirm the report.

Monzo will use the funds both to build new products as well as move forward with its international expansion plans. Expansion to the U.S. is near the top of the company’s wish list, having resumed efforts to secure a banking license in the country after retreating from a previous attempt three years ago. Monzo hired Conor Walsh, former Head of Product for Cash App, as its U.S. CEO in 2023.

“At the heart of it, we are a mission-oriented company that’s looking to build the single place where people can meet all of their financial needs,” Monzo Co-Founder and CEO TS Anil told CNBC. “What’s exciting to me is that, as we pursue that mission of changing people’s relationship with money, we’ve built a business model that is congruent with that, as well, with this model that is built entirely around the customer.”

Founded in 2015, Monzo has more than nine million retail customers and 400,000 business customers in the U.K. The challenger bank offers current and joint accounts, as well as an app to enable customers to see all their accounts and control spending. The company launched its first business bank accounts for SMEs and self-employed workers in 2020 and, later that year, unveiled its first loan products for its personal current account customers. In 2023, Monzo announced that it had achieved profitability for the first time.

As part of its expansion plans, Monzo is looking to begin offering mortgage and pension products, with the latter being available as early as six to nine months from now. Last year, Monzo launched an investment product, giving customers the ability to invest in a trio of funds offered by BlackRock.

Banked and NAB Promote A2A Payments in Australia

A new partnership between international payments network Banked and National Australia Bank will make it easier for merchants in Australia to adopt account-to-account (A2A) payments solutions. Specifically, the two entities are seeking to encourage the adoption of Pay by Bank technology via Australian Payments Plus (AP+) services.

Pay by Bank enables merchants to send PayTo Agreements to customers, and then initiate payments and refunds based on those agreements – which cover a variety of transaction experiences including online payments, and recurring payments with fixed, variable, or split payment amounts. Partnering with NAB gives Banked a partner with both an established presence in the Australian market, as well as a comprehensive knowledge of the needs of merchants in the country.

“The nascent A2A payments industry in Australia presents an incredible opportunity for Banked,” Banked CEO Brad Goodall said. “Local regulators have developed well-constructed mandates and the banking industry is primed for innovation, all of which sets the stage for rapid growth in real-time payments.”

An initial set of NAB business customers from industries such as e-commerce and retail, as well as non-bank lenders, is scheduled go live with A2A payments in the first half of 2024.

With offices in both Palo Alto, California and London, U.K., Banked was founded in 2018. Earlier this year, the company announced a partnership with FIS to promote use of Pay by Bank.

Meet FinovateSpring 2024’s International Alums

FinovateEurope typically gets top billing as our most international fintech conference. But FinovateSpring has showcased a sizable number of fintech innovators from around the world, as well. And this year’s FinovateSpring is no exception.

Here’s a look at seven companies demoing at FinovateSpring, May 21-23, that hail from outside of the United States.

There’s still time to pick up your ticket and save your spot for our annual Spring fintech conference in San Francisco, May 21-23. Visit our FinovateSpring hub to register.

Here is our look at fintech innovation around the world.

Sub-Saharan Africa

Nigerian fintech and non-bank credit card issuer O3 Capital partnered with American Express to issue four new AMEX credit cards.

South African fintech Lesaka acquired South African payments company Adumo in a deal valued at $85.9 million.

SasaPay, a fintech headquartered in Kenya, announced a partnership with investments solutions provider Etica Capital.

Central and Eastern Europe

Swiss Bitcoin Pay teamed up with Lithuanian regtech iDenfy to enhance its risk management and onboarding processes.

Latvian fintech Huntli partnered with U.S.-based Payall to improve security for cross-border payments.

Lithuania-based TransferGo secured $10 million in funding from Taiwania Capital Management.

Middle East and Northern Africa

Digital payments company Wink Pay launched in Lebanon in partnership with Visa and Codebase Technologies.

Saudi Arabian insurtech Rasan to sell 30% of its stake in a Riyadh IPO.

Central and Southern Asia

Nepal Clearing House inked a memorandum of understanding (MoU) with Ant International to enable QR payments via Alipay+ for visitors to Nepal.

Finovate Best of Show winner Zetalaunched its Digital-Credit-as-a-Service solution for banks in India.

Saudi Arabia’s Alraedah Digital Solutions forged a strategic partnership with Pakistan-based fintech ABHI to launch new financial services in the kingdom.

Latin America and the Caribbean

Brazilian digital bank Nubanktops 100 million customer mark.

Experian launched Cashflow Attributes, a tool to offer lenders more data about underserved consumers.

Cashflow Attributes offers lenders visibility into more than 900 consumer attributes that reflect consumers’ cashflow and affordability.

Lenders can use the insights to aid in their underwriting decisions, drive more personalized experiences, and help improve financial management tools.

Information services company ExperianunveiledCashflow Attributes yesterday, a new solution that leverages open banking to help underserved consumers access fair and affordable credit.

Cashflow Attributes uses more than 900 income, cashflow, and affordability attributes to allow lenders to integrate applicants’ banking data into the decision-making process. Experian expects the new solution will help some of the 106 million U.S. consumers who are considered credit invisible, unscoreable by conventional credit scores, or have a subprime or below credit score and are therefore unable to secure credit at mainstream rates. Credit Attributes layers traditional credit report data with cashflow insights to create a more detailed view of a consumer’s financial health and creditworthiness.

“Supporting financial inclusion and creating an equitable path to credit is ingrained in our DNA,” said Experian Financial and Marketing Services Group President Scott Brown. “We believe banking information holds untapped potential and that our new Cashflow Attributes represent an exciting step forward that can easily be integrated into lending decisions. As we look ahead, we will continue to leverage our core credit data, new data elements and our analytics expertise to unlock new opportunities for both consumers and businesses.”

To use Cashflow Attributes, lenders first provide Experian with depersonalized transaction information from their existing customers or from customers at other banks, as long as they have consumer-permissioned account access. Experian uses its categorization model to analyze and categorize the consumer transaction data and sends the lender the transaction categories and predictive attributes. Lenders can use these categories and attributes to aid in their underwriting decisions, drive more personalized experiences, and help improve financial management tools.

Founded in 1980 and originally known for its consumer credit reporting, Experian has extensive access to data and has added fraud prevention offerings, identity theft protection, credit building tools, and a loan comparison marketplace. On the commercial side, Experian provides a range of services for small businesses, including business credit reporting, marketing products and services, debt collection tools, and more. The company is headquartered in Dublin, Ireland, and is listed on the London Stock Exchange under the ticker EXPN and has a market capitalization of $39.5 billion.

Nubank has surpassed 100 million customers, stating that it is the first digital banking platform outside of Asia to reach this customer milestone.

Nubank serves 92 million customers in Brazil, over 7 million in Mexico, and close to 1 million in Colombia.

In 2023, Nubank achieved record financial results, reaching more than $1 billion in net profit and over $8 billion in revenue.

Brazilian challenger bank Nubankannounced this week it has surpassed 100 million customers across Latin America. The fintech estimates it is the first digital banking platform outside of Asia to reach this customer milestone. Nubank is currently active in three countries, serving 92 million customers in Brazil, over 7 million in Mexico, and close to 1 million in Colombia.

The company has a mission of “fighting complexity to empower people,” offering users a digital bank account, credit card, mobile phone insurance, life insurance, personal loans, and investing tools. The company launched business accounts in 2019 to offer small business users a bank account, credit card, and a phone-based payment acceptance app.

“In 2013, we had set ourselves the ambitious goal to reach one million customers in five years, which seemed almost impossible at the time,” said Nubank Founder and CEO David Vélez. “In a decade, we have surpassed 100 million, which is a testament to the trust our customers place in us and to the power of a truly customer-centric business model. These 100 million customers have written their stories together with ours, and we want to honor them in a special way.”

Since its inception, Nubank has been instrumental in helping its customers save more than 440 million hours of waiting in service queues. Additionally, the company estimated that it helped users save 11 billion dollars in banking fees in 2023.

Perhaps more notable than savings consumers on fees and their time waiting in line, Nubank has also been instrumental in promoting financial inclusion in Brazil, a region notorious for its high rate of unbanked adults. Between July 2021 and July 2022, Nubank added 5.7 million credit cardholders to the country’s credit card market. In a survey it conducted of accountholders from 2021, Nubank found that 60% of Brazilian customers improved their financial journey in the first 24 months, citing frequent and responsible use of credit cards and other financial products.

“Being customer-centric has been guiding us since the very beginning,”said Nubank Co-founder and Chief Growth Officer Cristina Junqueira. “Today, we want our customers to see themselves the way we see them: at the center of everything. In reaching this milestone, we want to focus on the real people and individual stories of empowerment and advance our mission to help improve people’s lives.”

From a U.S. perspective, Nubank’s customer number is not the only impressive metric surrounding the fintech. The company closed last year with record financial results, recording more than $1 billion in net profit and over $8 billion in revenue. The positive financials are especially admirable, given that many U.S.-based challenger banks are still seeking to reach the break even point.

Finovate’s Credit Union Spotlight is back! This month at FinovateSpring – May 21 through May 23 – Finovate will host a special session to give leaders and professionals working at credit unions an opportunity to meet and network with their peers as well as with fintech innovators who are building solutions specifically for credit unions.

Coordinated by Finovate Vice President and Director of Fintech Strategy Greg Palmer and Sam Das, Managing Director of TruStage Ventures, the Credit Union Spotlight gives those running credit unions the opportunity to speak freely and candidly about the challenges – and opportunities – facing credit unions and their members today.

We caught up with Greg Palmer to talk about the state of credit unions in 2024 and what the Credit Union Spotlight at FinovateSpring this year hopes to achieve.

What challenges are credit unions facing right now?

Greg Palmer: Credit unions are facing a myriad of challenges at the moment. High interest rates and economic uncertainty are putting pressure on everyone, but local financial institutions like credit unions are particularly vulnerable. The good news is that the fintech industry is increasingly aware of what CUs are going through, and we’re seeing more and more technologies built with CUs in mind. These technologies are arriving just in time, and it’s about to get a lot easier for smaller FIs to compete with the multinational banks that tend to dominate the headlines.

How can better, deeper relationships with fintechs help credit unions overcome these challenges?

Palmer: It’s difficult for CUs to compete with larger financial institutions with bigger budgets, more marketing power, and teams of technologists creating new innovations in-house. These same factors, though, are also making it more difficult for fintech companies to sell their solutions into those big banks. The result is that a lot of newer fintech innovators are looking at credit unions as a target demographic. CUs both need the technologies they can provide and are less likely to be able to create their own alternatives, which is why it’s so imperative for us to bring both groups together.

How important is it to give credit unions the opportunity to network more exclusively with fintech providers, as well as with each other?

Palmer: Credit unions are fundamentally different from for-profit financial institutions, and they look at new technologies through a slightly different lens. That’s why it’s so important to separate out CU executives into their own space where they can network with each other, share experiences, and view new technologies together.

Finovate’s Credit Union Spotlight will take place on May 23, Day Three of FinovateSpring. The session will be held around midday and will last for approximately 90 minutes.

Read more about the Credit Union Spotlight at FinovateSpring in this feature at Finopotamus and don’t forget to take an early look at our demo companies in our Sneak Peek series. And if you haven’t picked up your ticket yet, Friday is the deadline to take advantage of big, early-bird savings. Visit our FinovateSpring hub today and save your seat!

FIS unveiled its embedded finance platform, Atelio by FIS, this week.

The platform leverages FIS’ existing technology to enable businesses to embed a variety of financial products and services into their offerings.

FIS made its Finovate debut at FinovateSpring in 2013. Stephanie Ferris is CEO and President.

FIS is the latest company to introduce a platform to make it easier for businesses and software developers to embed financial services and fintech solutions into their products and services. Atelio by FIS, launched this week, is one of the first banking-as-a-service offerings from a major core provider. The technology will serve B2C fintechs and enable financial and non-financial services companies alike to implement embedded finance into their existing offerings

“Welcome to the future of financial services,” FIS President of Platform and Enterprise Products Tarun Bhatnagar said. “Atelio by FIS is our vision to lead where fintech is going, which is outside the boundaries of how businesses enable, and their customers consume, financial services today.”

Atelio leverages FIS existing technology by way of easily embeddable and consumable components. The platform enables non-financial companies to offer their customers a wide variety of financial experiences: collecting deposits, moving money, issuing cards, sending invoices, and more. Atelio also provides tools to help companies fight fraud, anticipate cash flows, and gain insights into consumer preferences and behaviors.

FIS’ latest offering comes at a time when growth in embedded finance is expected to soar. In its product announcement, the company pointed to research from Bain Capital that indicated that embedded finance will represent 10% of all transactions by 2026. The firm values these transactions at $7 trillion, or more than $50 billion in total revenue. Additionally, research from S&P Global Intelligence showed that banks that offered embedded finance solutions outperformed their peers in terms of deposit growth.

“More than just a new solution, Atelio is built to lend the expertise, tools, and distribution so that our users and clients can focus on creating,” Bhatnagar said. “Our scale, distribution and continued investment in technology have given us the foundation to unlock our financial capabilities to a wider audience and power the next generation of financial innovation.”

Three FIS clients – KeyBank, private student loan provider College Ave, and payment system and billing platform Royal Pay – have already deployed Atelio and are building solutions on the platform.

Jacksonville, Florida-based FIS made its Finovate debut at FinovateSpring 2013. Currently, the company enables 95% of the world’s banks, moves more than $1 trillion a month, and processes $50 trillion via its asset management technology every year. The company’s new product announcement came one day after FIS announced first quarter 2024 results which included the firm’s “fifth straight quarter of exceeding our financial outlook,” according to FIS CEO and President Stephanie Ferris.

In the fast-evolving world of fintech, founders are a breed apart, characterized by their unique blend of grit, determination, and adaptability. Their journeys are often marked by challenges, triumphs, and invaluable insights. In this series of interviews, we delve into the minds of five fintech founders to uncover the lessons they’ve learned, the key traits they believe are essential for a successful founding team, and the distinctive challenges and opportunities they’ve encountered on their entrepreneurial paths. Join us as we explore the stories and experiences that have shaped these innovative leaders in the fintech industry.

Expensify is teaming up with Spotana to launch Expensify Travel, a business travel booking platform based on Spotanas Travel-as-a-Service offering.

The new travel service will offer Expensify’s business users access to global travel inventory, lower fares, and servicing.

Expensify’s new launch makes it a direct competitor with California-based Navan, a corporate travel and expense management platform that launched in 2015.

Business expense management company Expensify announced the upcoming addition of a new set of capabilities today, which will make it a more robust platform to help businesses plan and manage their expenses. The company is launching Expensify Travel.

Expensify Travel will allow the company’s business users to access global travel inventory, lower fares, and servicing. Expensify Travel will be built on top of New York-based Spotana’s cloud-based Travel-as-a-Service platform, which will help clients manage flight changes, cancellations, and unused ticket credits, as well as offer comprehensive travel management capabilities.

“Book your trip in minutes, we’ll handle the rest. We’ve made it effortless for members to search and book flights, hotels, cars, and trains — all at the most competitive rates available,” said Expensify CEO David Barrett. “Our early release will let business travelers manage it all in one place, with real-time support, customizable rules, and the option to assign virtual travel cards to employees. We couldn’t be more excited for the future of Expensify Travel in partnership with Spotana.”

Expensify plans to have the early release of Expensify Travel next week, offering booking and management capabilities, as well as 24/7 Expensify support. In the future, the new travel offering will be directly integrated into New Expensify, the company’s new super app. When booking their travel in the new chat-based app, customers will be able to book and manage trips, manage travel expenses, chat with colleagues, and more. “Through our partnership, Expensify has created a one-stop shop for travel and expense management for their customers with a seamless user experience,” said Spotnana Founder and CEO Sarosh Waghmar.

Expensify’s new launch makes it a direct competitor with California-based Navan, a corporate travel and expense management platform. Formerly known as TripActions, Navan was founded in 2015 and offers expense management tools such as employee spending controls, automated expense management tools, reporting capabilities, and more.

There are key differences between Expensify’s and Navan’s expense management tools, however. While both companies allow clients to use their own existing corporate expense cards with their expense management tools, Expensify also offers users its own branded debit card. Also, Expensify’s interface is focused on being user friendly to serve small and medium sized businesses, while Navan offers features that are tailored to meet needs of a variety of sizes.

It is more difficult to assess the differences between the companies’ travel booking tools, given that Expensify’s tools have yet to launch. However, it appears that the two will differentiate themselves with tools that serve their individual target markets. For instance, Navan offers a high-touch, premium travel experience, the ability to book meetings and events, and consulting services aimed at larger, corporate clients. Expensify’s tools will likely root in the company’s user-friendly, simplified approach.