This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

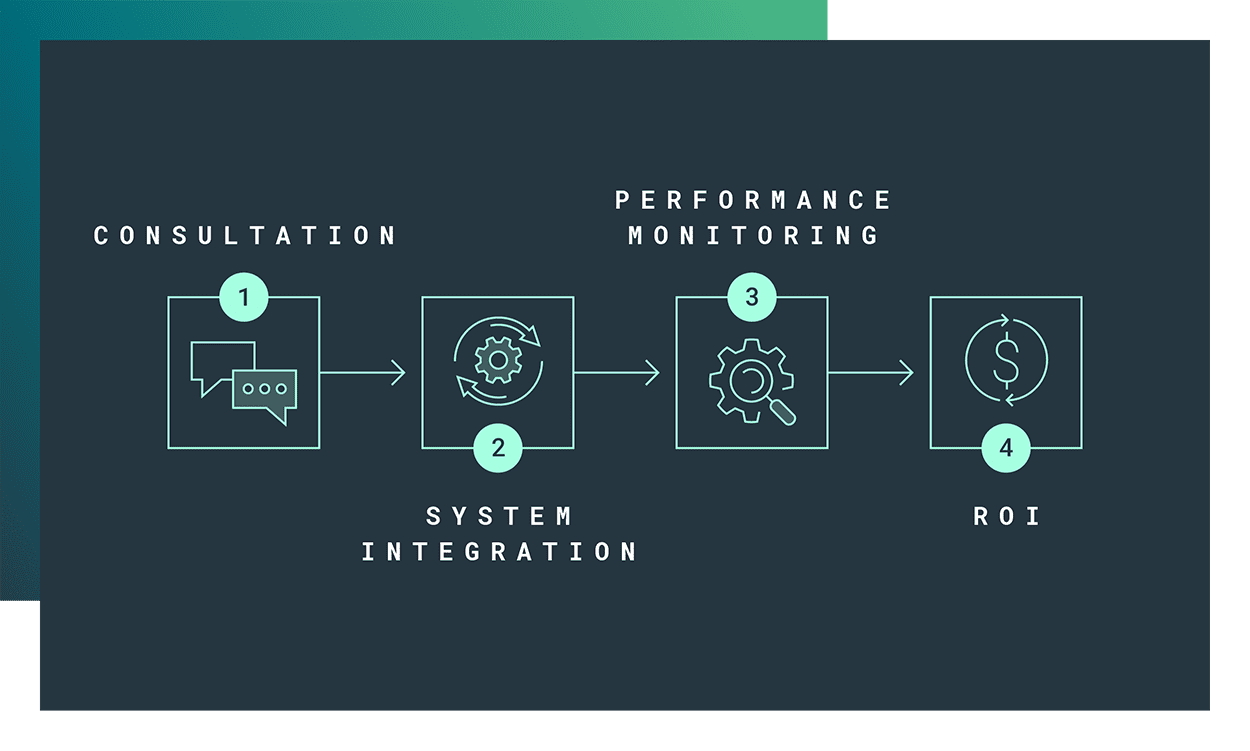

Today’s customers want personalized experiences, but how can companies drive meaningful one-on-one connections at scale?

Data wins!

Handled correctly, well-orchestrated data reaches customers the way they want to be reached: fast and seamless while facilitating loyalty and trust.

The next generation customer experience is made easier with LeanData, the leading Revenue Orchestration platform. LeanData connects the dots for over 1,000 companies, increasing speed-to-response and aligning go-to-market motions with efficiency.

90% reduction in data duplication

78% decrease in time needed to research records

5 hours per week saved by eliminating manual processes

Time-to-response decreased from 1 to 2 days to less than 1 hour

This week, Finovate Global looks at recent fintech developments in France.

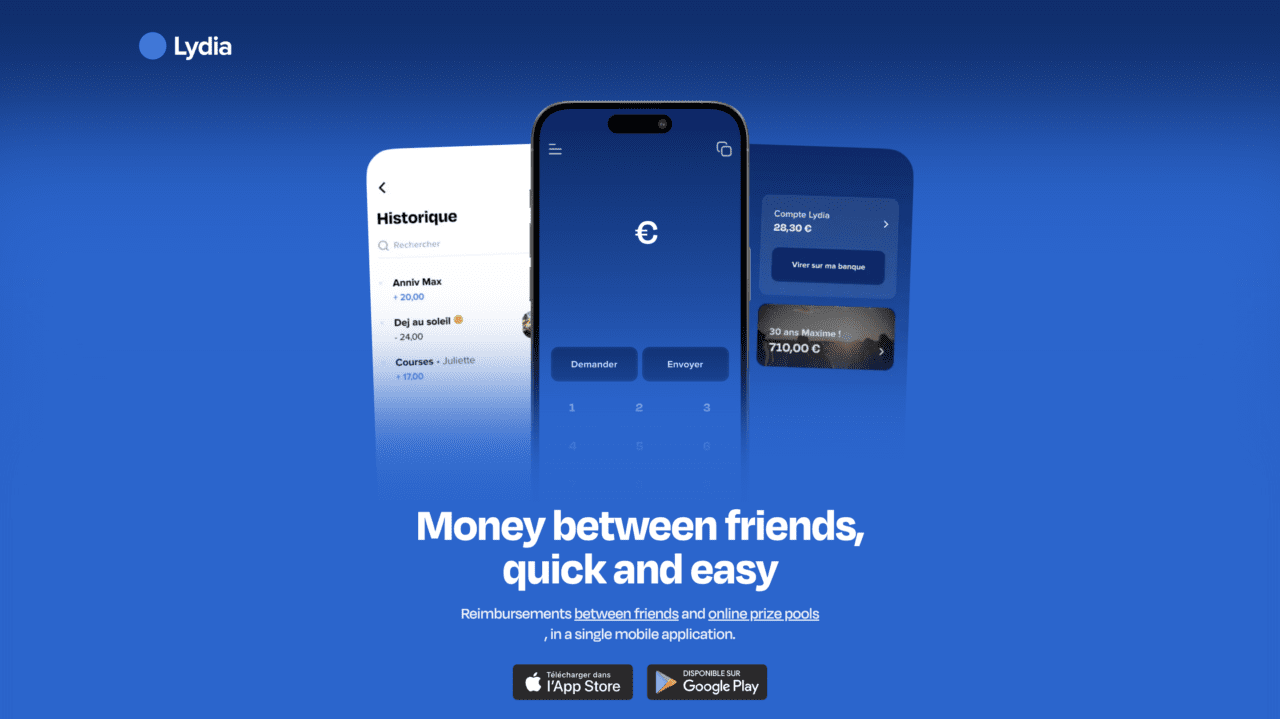

French start-up Lydiaannounced the launch of a new digital banking brand this week. Named Sumeria, Lydia plans to invest more than €100 million in the new initiative, as well as hire 400 people over the next three years. Sumeria, according to a post on LinkedIn, offers 4% interest and is designed to be a “simple and accessible banking super app.

“We are convinced that technology (cloud, mobile) is not an end in itself, but a way to simplify life, through everyday details,” the company noted in a statement on its website. Arguing that current accounts should be neither “trendy gadgets” nor make users captive to a given app, system, or institution, the company explained: “It should solve a real problem. This is why Lydia’s choices, with Sumeria, are motivated by common sense and its ambition to be universal: for everyone, for everything.”

Lydia’s brand announcement follows a decision by the company to split its digital banking app into two components. Originally launched in 2013 as a P2P payments app, Lydia’s solution scaled, adding more and more financial services features over the years. It was the launch of its Lydia Accounts offering convinced the company that a change was necessary to keep its early adopters – who relied heavily on the P2P service – onboard. The result was to offer the P2P services separately from Lydia’s digital banking proposition through the Lydia Accounts app. The original Lydia app will become Sumeria, with the new features mentioned above – such as stock trading, savings accounts and loans – to be ported to the new banking brand.

Headquartered in Paris, Lydia has raised more than $259 million in funding. The company’s investors include Accel and Echo Street Capital. In addition to the launch of Sumeria, Lydia is also seeking a credit institution license from the French Prudential Supervision and Resolution Authority.

Paris, France-based private wealth management startup RockFiraised €3 million in funding this week. The round was led by Varsity I and featured the participation of numerous business angels in technology and private management. The company plans to use the capital to grow its workforce by 3x by the end of 2024 so as to provide private banking and wealth management expertise to clients throughout France.

“Since the beginning of the year, we have seen strong client traction eager for a new model to manage their wealth,” RockFi Co-Founder and CEO Pierre Marin said. “With a market of €4.8 trillionin assets ahead of us and no tech leader yet in France and Europe, our ambition is very high for the coming years.”

RockFi’s model combines human expertise and technology to offer services including banking, wealth management, life insurance, and pension savings. The firm has a targetable clientele with assets of more than €100,000, representing six million households in France.

“Three months after our official launch this is an important step that anchors a strong momentum and allows us to further accelerate the construction of the new private management,” the company wrote on its LinkedIn page this week. “The ambition remains: to surround ourselves with the best talent and partners in each field and to deploy a tech ecosystem to unleash the potential of independent wealth managers at the service of their clients.”

Meet Finovate’s French Alums!

Over the years, Finovate has been proud to showcase a number of fintech innovators based in France. Here’s a look at some of French fintechs that have demoed their technology on the Finovate stage in recent years.

Aeropay raised $20 million in new funding for its pay-by-bank technology.

The round, which boosts Aeropay’s total funding to $25 million, was led by Group 11.

Aeropay also announced the launch of Aerosync, the company’s internally developed bank aggregator.

Chicago-based payments company Aeropayannounced today it has landed $20 million in new funding. The Series B round, which boosts the company’s total funds to $25 million, was led by venture capital firm Group 11 and saw participation from Chicago Ventures and Continental Investment Partners.

Aeropay was founded in 2017 to help businesses move money in a faster, less expensive way using Aerosync, the company’s internally developed pay-by-bank technology. Launching today, Aerosync is Aeropay’s bank aggregator that enables customizable integrations via open APIs.

“Payments in most verticals operate on archaic systems filled with excessive fees and risks,” said Aeropay Founder and CEO Daniel Muller. “We’ve built a bank-driven payments network that protects businesses against fraud, saves them money, and gives their customers an easy way to pay. Put simply, we are building the next-generation payments network.”

Aeropay will use the funds to expand into new markets, including financial services, wellness, utilities, QSR, and property management. The investment will also help fuel new product offerings, build on strategic partnerships, and explore new opportunities.

“For years, we’ve searched for a company advanced enough to solve the pains and inefficiencies of the card payment market, arguably the last bastion of the traditional financial services industry,” said Group 11 Founding Partner Dovi Frances. “Aeropay has tackled the most complex technological and compliance challenges, making them the most likely player to seize upon this massive addressable market.”

Pay-by-bank has seen rising popularity across the globe in the past few years, as open banking fuels new possibilities. The technology holds the promise of reducing transaction fees for retailers. End consumers, however, may remain skeptical of pay-by-bank’s security and user friendliness.

VantageScore launched its newest credit scoring model, the VantageScore 4plus.

The score combines consumer-permissioned open banking data with data from Experian, Equifax, or TransUnion to improve lenders’ underwriting efforts.

The new credit scoring model is available as a pilot for banks, fintechs, and government lenders.

Consumer credit score software company VantageScore unveiled VantageScore 4plus, its newest credit scoring model, today.

VantageScore 4plus leverages alternative data sourced through open banking that can be accessed via all major aggregator APIs. When consumers offer lenders access to their bank data, the lender can combine the data with traditional credit scoring information from Experian, Equifax, or TransUnion to make more informed underwriting decisions and potentially lend to more consumers who have thin credit files but demonstrate positive cash management.

“The use of consumer-permissioned bank account data is a huge step forward in creating a credit score that is more predictive and reflective of a consumer’s full financial profile, helping them build their credit and gain access to mainstream financial products,” said Credit Builders Alliance CEO Dara Duguay.

This new credit scoring model is available as a pilot for banks, fintechs, and government lenders. Because it uses the same 300 to 850 scoring range with aligned score-to-odds ratios as VantageScore 4.0, most lenders won’t need to adjust their credit or lending policies to use the new VantageScore 4plus credit score. And because the new score leverages real-time data, lenders will be able to view a consumer’s credit score adjustment within seconds, facilitating faster lending decisions.

The additional data from VantageScore 4plus not only helps lenders make informed decisions about new borrowers, but it also helps lenders identify existing borrowers whose habits have changed. The new score provides visibility into signs of financial distress months before the trouble is detected by traditional credit bureaus. which is critical in the current economic uncertainty.

“By harnessing the power of alternative open banking data, VantageScore 4plus is ushering in a new era of consumer credit scoring that is transformational for lenders,” said VantageScore President and CEO Silvio Tavares. “As the fastest growing credit scoring company in the U.S., with over 42% growth in 2023 and 27 billion credit scores used per year, lenders are recognizing the innovation and predictive power of VantageScore credit scores.”

The news comes shortly after Experian launchedCashflow Attributes, a tool also powered by open banking and consumer-permissioned data, that aims to offer lenders more data about underserved consumers.

Connecticut-based VantageScore was founded in 2006 as an independently managed joint venture of the U.S.’ three Nationwide Consumer Reporting Agencies (NCRAs) – Equifax, Experian and TransUnion. The company, which is committed to financial inclusion, saw the usage of its VantageScore increase by 42% in 2023, when it reported more than 27 billion credit scores. VantageScore helps 3,400+ institutions, including eight of the top 10 banks, to use the VantageScore credit score to underwrite credit cards, auto loans, personal loans, and mortgages.

Finovate’s David Penn interviewed Rikard Bandebo, VantageScore Executive Vice President and Chief Product Officer on the company’s approach to credit scoring in 2022.

With just a few days until FinovateSpring takes the stage at the Marriott Marquis in San Francisco, it is a good time to set your schedule in the event app. As usual, we have curated a lineup of keynote speakers who will be offering their expertise on some of the most pressing topics in fintech and banking.

Here’s a look at some of the keynote speakers taking the stage during the general session.

Brian Solis, Author at Mindshift: Ignite Change, Inspire Action, And Innovate For A Better Tomorrow

On Tuesday at 10:30 am, Solis’ keynote, The Cycle For Emerging Technologies: Which Will Really Matter To Financial Services Providers And Why? If You’re Waiting For Someone To Tell You What To Do, You’re On The Wrong Side Of Change will help financial services providers dig into the newest technologies and determine how to prioritize new, and rapidly approaching changes in banking and fintech.

Shirin Oreizy, Founder and CEO of NextStep

Oreizy’s keynote address is taking place on Tuesday at 12:45 pm. During her presentation, How Companies Can Leverage The Psychology Of Human Decision Making To Design And Scale Financial Products, Oreizy will consider how your consumers are really making their decisions, what motivates them, and how to design your UX to drive desired behavior.

Manas Chawla, CEO at London Politica

Chawla will take a look at the current geopolitical outlook in his keynote, The Global Economic & Geo-Political Outlook – What Are The Five Things You Need To Know? He takes the stage at 1 pm on Tuesday and will be looking at topics such as the interest rate environment, bank failures, wars, and political tensions.

Karl Alomar, Managing Partner at M13

In his quick fire keynote session at 3:35 pm on Tuesday titled, Major Banks Are Making Serious Plays In The Crypto & Digital Currencies Space – Why?, Alomar will consider the shortcomings of traditional currencies and will take a look at the rise of digital currencies, including CBDCs. He will also address the impact digital currencies will have on banks and how they should prioritize discussions.

Gary Rudman, Founder and CEO of GTR Consulting

Rudman will take the stage at 11:40 am on Wednesday to offer his keynote, ALT, SHIFT & CTRL: The 3 Keystrokes That Define the Gen Z Worldview – What Banks & Fintechs Need to Know. During his presentation, Rudman will describe how Gen Z differs from their predecessors and will discuss how banks can connect with the new generation.

Sam Kilmer, Managing Director, Fintech Advisory at Cornerstone Advisors

Kilmer’s quick fire keynote, which takes place at 9 am on Thursday, is titled, Focusing On The Three Pillars Of Banking: Deposits, Loans, and Money Movement – How Can Banks Innovate To Drive Revenue In A Challenging Economic Environment? The presentation will cover what Kilmer has determined are the three pillars of banking: deposits, loans, and money movement operations. Kilmer will also consider KYC, fraud detection, and authentication, and will discuss what banks should prioritize to add value.

James Robert Lay, Author of Banking on Digital Growth

In his keynote, Banking On Change – The Exponential Growth Journey, Lay considers how firms can maximize their digital growth using a future mindset. He also looks at how legacy systems limit digital growth potential. Lay’s presentation begins at 9:50 am on Thursday.

Sarah Welch, Managing Director at Curinos

In her quick fire keynote, How AI Is A Force Multiplier On Customer Loyalty, Welch will offer her take on AI in financial services and will consider how organizations can use the enabling technology to improve customer service and ultimately improve loyalty. Welch’s presentation begins at 10:05 am on Thursday.

Sam Maule, Head of Business Development at Moov

Maule’s presentation, The Next Chapter For Embedded Finance & The Digitisation Of Commerce. In An Age Of Re-Bundling Financial Product Experiences, How And Where Should Banks Play To Win? Why Retailers & Banks Need To Be Actively Partnering On Embedded Finance, takes place at 11:25 am on Thursday. Maule will consider how embedded finance is transforming the industry and will offer advice on where to steer.

Digital identity verification innovator Socure announced a partnership with identity-secured transactions company Proof.

The partnership will combine Proof’s Defend solution with Socure’s Sigma Fraud suite to help companies fight fraud and forgery in authorizations, agreements, contracts, and forms.

Founded in 2012, Socure made its Finovate debut the following year at FinovateFall in New York.

A new partnership between digital identity verification innovator Socure and identity-secured transactions company Proof will bring new tools to the fight against fraud and forgery in authorizations, contracts, and forms.

“With the explosion of new fraud vectors, our mission at Socure remains steadfast: use AI to deliver the most accurate anti-fraud and identity verification solutions in the industry,” Socure Founder and CEO Johnny Ayers said. “Partnering with Proof allows us to uniquely ensure identity-assured transactions for contracts, authorizations, forms, and high-risk financial events across various sectors.”

While there is widespread understanding about threats like money laundering that cost businesses $18 billion every year, the challenge from document fraud is significantly greater. A 2021 report from FINCEN revealed that false records and forgery are responsible for more than $45 billion in fraud activity annually. Fraudsters also have become more effective at leveraging AI to deploy deepfakes, synthetic identities, and – in the case of document fraud – falsified records.

The partnership will blend the strengths of Proof’s Defend solution with Socure’s Sigma Fraud suite. Defend leverages 100+ behavioral, fraud risk signals to detect fraud in online customer interactions. Businesses get a risk score for every transaction that highlights any fraud issues behind the authorization, signature, notarization, or identity verification.

Sigma Fraud analyzes historic behavioral patterns across channels to spot anomalies that may indicate fraudulent activity at the identity level. The suite also is backed by consortium data from the Socure Risk Insights Network, which draws from nearly 2,400 customers from the country’s largest banks, fintechs, payment platforms, and payroll providers.

“Adding Socure’s digital identity verification capabilities to Defend, our fraud detection and prevention product, allows customers to secure transactions at every stage, quickly and accurately,” Proof CEO Pat Kinsel said. “We can’t think of a better partner and are excited to introduce Socure to Defend clients.”

Founded in 2012, Socure made its Finovate debut at FinovateFall a year later. Most recently demoing its technology on the Finovate stage in 2017, Socure has since grown into a leader in digital identity verification with more than 2,300 customers. Last month, the company unveiled its new global watchlist screening and monitoring tool. The solution gives financial institutions the ability to screen, monitor, and assess new and existing customers against the Office of Foreign Assets Control (OFAC) sanction lists and politically exposed persons (PEP) databases, adverse media, and custom watchlists.

Socure began the year announcing a pair of new partnerships. In January, the company reported that auto finance company Exeter Finance would deploy the Socure ID+ platform to onboard new customers. In February, Socure teamed up with fellow Finovate alum Trustly to offer a Pay-by-Bank solution with streamlined onboarding.

As the banking sector stands at the precipice of a new era powered by fintech innovation, mastering the rapid deployment of AI technologies is not just beneficial—it’s imperative. At FinovateSpring 2024, Chris Brown, President of Intelygenz USA, will share pivotal insights during his keynote on “Accelerating Bank-Fintech Fusion: Deep Tech & AI Solutions in Action.” However, the core themes of his talk resonate beyond the conference, offering valuable lessons for all financial institutions navigating the complex terrain of digital transformation.

Chris Brown’s address will confront a stark reality in the fintech space: while many AI projects begin with promise, few successfully bridge the gap from development to production. An overwhelming 85% of these initiatives falter, yet Intelygenz has carved a niche in ensuring projects land within the successful 15%. This capability is not just a differentiator but a strategic imperative that positions banks to lead rather than follow in the digital age.

The keynote will explore three strategic areas where AI can significantly impact banking operations, tailored to both conference attendees and the broader industry audience:

Building Data-Driven Architecture with AI

Leveraging AI to enhance data architectures transforms the foundational operations of banking. By integrating predictive analytics for credit scoring, automated compliance monitoring, and real-time fraud detection systems, banks can enhance decision-making, ensure compliance, and secure transactions, streamlining operations while significantly improving risk management and customer trust.

Streaming AI to Automate Day-to-Day Operations

The deployment of streaming AI moves the technology from a conceptual stage to an operational necessity, automating critical operations such as transaction monitoring and customer interactions. This shift not only boosts operational efficiency but also enhances the quality of customer service, providing real-time, actionable insights that empower banks to make informed decisions swiftly.

Implementing Human Experience-Centric AI Solutions

At the heart of technological advancements lies the need to enhance human interactions. By focusing on AI-driven enhancements in customer service operations and user interfaces, banks can forge deeper connections with their customers, resulting in increased loyalty and satisfaction. From AI-enhanced financial wellness programs to advanced biometric authentication and accessibility improvements, these technologies are reshaping how banks interact with their customers.

These areas underscore Intelygenz’s expertise in rapidly transitioning AI projects from development to deployment, ensuring they not only meet but exceed their intended goals swiftly.

For those attending FinovateSpring, Chris Brown’s session will not only illuminate pathways to leveraging AI but also provide practical insights into overcoming the implementation challenges often encountered by financial institutions. For the broader audience, these themes serve as a blueprint for understanding and deploying AI technologies effectively within their organizations.

For a deeper dive into these transformative strategies, attend Chris Brown’s session at FinovateSpring, or reach out directly via his contact details for more personalized insights and solutions from Intelygenz.

By embracing these insights, banks and Fintechs can ensure they not only participate in the digital revolution but lead it, transforming potential technological disruptions into opportunities for significant growth and customer satisfaction.

About Intelygenz:

Intelygenz is a leading deep tech and AI services consultative company, specializing in delivering tailored solutions that leverage advanced technologies to drive business transformation in the banking and fintech sectors. With over two decades of expertise, Intelygenz specializes in enhancing operational efficiency and elevating customer engagement, thereby delivering measurable returns on investment. As a full-service end-to-end consultancy, Intelygenz collaborates closely with its clients’ internal teams from concept through to deployment, helping to develop, integrate, and maintain customized solutions.

Intelygenz’s key strength is its ability to facilitate rapid deployment, enabling its clients to realize tangible ROI within weeks, not months or years. Banks and fintech companies trust Intelygenz to tackle their most complex challenges, confident in the company’s capacity to support their teams in delivering critical AI-enabled projects on time and within budget.

Chris Brown, President at Intelygenz USA, is a seasoned leader in the AI and tech industry, specializing in transformative solutions for banking and fintech. Leading a team dedicated to innovation, Chris drives the development of tailored Deep Tech solutions to meet evolving client needs. LinkedIn

Layer has raised $2.3 million in pre-seed funding for its embedded accounting solution.

The round was led by Better Tomorrow Ventures, with participation from executives at Square, Plaid, Unit, Check, and other SMB software companies.

Layer will use the investment to expand its headcount across engineering and business operations.

Embedded accounting player Layerraised $2.3 million in a pre-seed round of funding today. The funds mark the first investment round the San Francisco-based company has seen since it was founded last March.

Better Tomorrow Ventures led the round, which also saw participation from executives at Square, Plaid, Unit, Check, and other SMB software companies.

Layer aims to simplify financial management for small businesses by enabling software companies– such as point-of-sale systems, neo-banks, and other software companies catering to small businesses– to embed accounting and bookkeeping solutions directly within their own platforms. This eliminates the need for small businesses to import data between their accounting software, such as Quickbooks, and the small business software provider. Because Layer allows software providers to combine their own data with data from customers’ external financial accounts, it helps offer the customers a more complete picture of their accounting.

“A common burden small businesses face today is keeping their accounting software in sync with their operations,” said Layer Co-founder and CEO Justin Meretab. “We believe our platform will now give SMBs a better solution for their accounting needs by embedding it into systems they use daily. Small businesses already have so much on their plate running and growing their operations, and accounting shouldn’t be another burden.”

Layer makes it possible for software companies to embed Layer through its API and pre-built Javascript UI components. The company will use the funding to expand its headcount across engineering and business operations.

“Accounting and bookkeeping are two of the biggest pain points small business owners face, and yet the existing products in the market are intimidating and can be time-consuming,” said Better Tomorrow Ventures Principal Nihar Bobba. “There are few products in the market that truly address these issues, which is why we’re excited to join Justin and Daniel in their journey to build and provide a powerful embedded accounting platform that enables all sorts of companies to solve the accounting needs of their customers.”

Identity verification solutions provider Data Zoo secured $22.7 million (AU$35 million) in Series A funding in a round led by Ellerston JAADE.

Data Zoo will use the capital to help foster broader adoption of its identity verification technology.

Headquartered in Sydney, New South Wales, Australia, Data Zoo was founded in 2011. Charlie Minutella is CEO.

International identity verification solutions provider Data Zoohas secured $22.7 million (AU$35 million) in Series A funding. The round was led by Ellerston JAADE, an Ellerston Capital fund; Data Zoo will use the capital to help drive broader adoption of its identity verification technology.

“There’s been a long-standing need for a more efficient and secure way to verify identities,” Data Zoo Founder and Chairman Tony Fitzgibbon said. “Data Zoo has spent years refining its solution – the result has been incredible innovation, UX optimization, and growth in a fiercely competitive market, putting us head-to-head with today’s most established identity providers.”

Data Zoo leverages direct access to authoritative data from more than 170 countries and advanced, logic-driven data sequencing to help institutions automatically verify identities based on the next best source. The company’s technology reduces dropout rates, lowers the total cost of ownership, and helps businesses boost customer approval rates and revenue realization. At the same time, Data Zoo prioritizes data protection and privacy by eliminating identity data storage.

Founded in 2011, Data Zoo is headquartered in Sydney, New South Wales, Australia. The company includes eToro, MoneyGram, and Experian among its partners, and competes in a crowded field of innovators including a number of Finovate alums such as Socure and Jumio. Earlier this year, Data Zoo announced the appointment of former London Stock Exchange executive Charlie Minutella as its new CEO. In a statement, Minutella spoke about the expansion opportunities this week’s investment will enable the company to pursue.

“Data Zoo is well-positioned to expand its footprint because of its patented ability to efficiently onboard a more diverse and global set of customers, meet compliance standards across jurisdictions, and enhance data privacy and protection,” Minutella said. “The investment from Ellerston JAADE will supercharge our capacity to operate in key markets, attract new business, and enter new strategic partnerships.”

For more coverage of fintech innovation around the world, check out our Finovate Global column published every Friday afternoon.

May is Asian-American and Pacific Islander Heritage month. And with FinovateSpring less than a week away, we wanted to take a moment to celebrate the Asian-American fintech innovators who will be demonstrating their latest technologies on the Finovate stage live in San Francisco, California on May 21 through 23.

Tickets for FinovateSpring are still available. Visit our registration page today and save your spot. We look forward to seeing you in San Francisco!

A former engineer at Dialpad, Dropbox, and Flexport, Ng is CEO and Co-Founder of Anvil. He is also a graduate of the University of Michigan and an alum of the Y Combinator Startup School Online.

Headquartered in San Francisco, California, Anvil was founded in 2018.

With experience in angel investments at 79 Studios, as a venture partner at Resolute, and a former I-banker at Chanin & CSFB, Saujin Yi is founder and CEO of LiquidTrust. Yi is a graduate of MIT and earned her MBA from UCLA Anderson, where she is a lecturer.

LiquidTrust was founded in 2019. The company is headquartered in Los Angeles, California.

A Venture Partner at JAZZ, Lin seeks to make everyone become “bionic” when it comes to investment research and analysis. Founder and CEO of Revelata, Lin is a graduate of Harvard University, earning his A.B. in Biochemical Sciences, as well as his S.M. and Ph.D. in Computer Science, at the institution.

Headquartered in Palo Alto, California, Revelata was founded in 2020.

Former Head of Operations for Juno Finance and Ownit, Chao is Co-Founder and Chief Operating Officer with Tennis Finance. Chao earned a B.A. in Economics and Psychology at University of California, Los Angeles.

San Francisco, California-based Tennis Finance was founded in 2022.

Klarna announced that 87% of its staff use its Generative AI engine, Kiki in their daily work activities.

Kiki was launched in June 2023 and uses OpenAI’s Large Language Models.

Kiki generates responses within one to five seconds and offers answers that are dependent on the user’s role and other context.

Global payments network and shopping platform Klarnaannounced today that 87% of its staff use Generative AI to complete their daily work activities. The employees are using Kiki, Klarna’s internal AI assistant.

Klarna launched Kiki in June of 2023, leveraging OpenAI’s Large Language Models (LLMs). Since it was released, Kiki has responded to more than 250,000 inquiries, which equates to roughly 2,000 inquiries per day. Today, more than 85% of all Klarna employees use Kiki.

“We push everyone to test, test, test and explore,” said Klarna CEO and Co-founder Sebastian Siemiatkowski. “As Klarna continues to discover applications for OpenAI’s tech, there’s the potential to take the business to new heights. We’re aimed at achieving a new level of employee empowerment, enhancing both our team’s performance and the customer experience.”

Overall, Kiki helps manage and distribute internal knowledge at Klarna, which helps to maintain a transparent culture. The AI assistant, which generates responses within one to five seconds, offers answers that are dependent on the user’s role and other context.

How do Klarna staff use Kiki? Employees can use the AI assistant to not only fetch information, but also to solve issues independently. For example, the company’s communications team uses the engine to evaluate whether press articles written about Klarna are positive or negative. The company’s lawyers use the tool to draft common types of contracts. “The big law firms have had a really great business just from providing templates for common types of contract. But ChatGPT is even better than a template because you can create something quite bespoke,” said Klarna Senior Managing Legal Counsel Selma Bogren.

Klarna also uses GenAI for external customer communications. The company states that, after one month, the AI customer service assistant handled 2.3 million conversations, equivalent to two-thirds of Klarna’s customer service chats.

The announcement comes as OpenAI, which powers Kiki, unveiledGPT-4o, the latest iteration of its GenAI chatbot. The new version is faster, has improved its non-English language text, and accepts input of any combination of text, audio, and images, while generating any combination of text, audio, and image outputs. “Because GPT-4o is our first model combining all of these modalities, we are still just scratching the surface of exploring what the model can do and its limitations,” states OpenAI’s announcement page.

Software solutions and engineering firm N-iXannounced today it has enhanced its partnership with digital identity verification tools company MitekSystems. Under the agreement, N-iX has tapped Mitek to enhance its digital identity verification and fraud prevention efforts.

Specifically, N-iX will leverage the Mitek Verified Identity Platform (MiVIP), a tool that allows organizations to aggregate multiple identity verification services using a low-code, no-code approach. MiVIP will help N-iX deploy the identity verification capabilities quickly, and will offer an easy-to-navigate experience for end users to maximize customer onboarding.

“By leveraging Mitek’s technologies, we are better positioned to meet the evolving needs of our clients in secure KYC, onboarding, and fraud prevention tools,” said N-iX Financial Services Client Partner Nataliya Maslak. “This partnership underscores N-iX’s ongoing commitment to fostering innovation and achieving excellence in the financial services domain and the digital security landscape.”

N-iX anticipates that Mitek’s MiVIP will enhance the service for end users while keeping digital transactions secure. With MiVIP, organizations can select a range of identity verification services and build multiple KYC processes with customizable workflows that will suit a range of risk profiles, products, and regulatory requirements. The technology guides end users throughout the onboarding process at their own pace and reengages them if they click out of the flow.

N-iX was founded in 2010 to offer technology to companies across financial services. The Florida-based company has been partnered with Mitek since 2016, using Mitek’s tools to develop customer lifecycle management and know your customer products. N-iX has built a cross-border payment engine for Currencycloud, a peer-to-peer lending platform for a U.K.-based fintech, instant money transfer solutions for Lebara, and a cloud-based Forex trading platform for Finatek.

Mitek was founded in 1986 and offers technology for mobile check deposit, new account opening, identity verification, and more. The company’s solutions are crucial to 99% of U.S. banks for mobile check deposits. Its technology is utilized by over 7,900 organizations, and its mobile check deposit and account opening tools serve more than 80 million consumers. Last year, Mitek formed partnerships with lending solutions company Abrigo and data and analytics company Equifax.

Mitek is publicly listed on the NASDAQ under the ticker MITK and has a current market capitalization of $633 million.