This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Payments optimization platform Spreedly has acquired fraud prevention company Dodgeball. Terms were not disclosed.

The acquisition will combine payments optimization and fraud prevention into a single platform.

Founded in 2008 and headquartered in North Carolina, Spreedly has been a Finovate alum since 2013.

Open payments platform Spreedlyannounced its acquisition of fraud orchestration company Dodgeball. Terms of the transaction were not disclosed. The acquisition combines payments optimization and fraud prevention in a single platform and helps bolster Spreedly’s strategy for both AI and open payments.

“For most merchants, payments and fraud aren’t separate challenges—they’re two sides of the same coin,” Spreedly CEO Justin Benson said. “You can’t optimize payments without addressing fraud, and you can’t fight fraud without understanding the payment flow. This acquisition brings these critical functions together, allowing us to deliver immense value to our customers and accelerate our vision for an AI-powered, open payments future.”

The acquisition is designed to give Spreedly’s customers additional reliability, as well as insights to help eliminate fraud and make more intelligent e-commerce decisions. The company noted that the acquisition will also enhance Spreedly’s workflow engine and help build the foundation for an AI-powered payments copilot. Post acquisition, the Dodgeball brand, as well as the Dodgeball team, will be integrated into Spreedly. This will not only enable Spreedly to maximize the benefit of Dodgeball’s expertise, but will also help ensure a smooth transition for customers with no service interruption and complete access to Spreedly’s global support and account management teams.

“We leapt at the opportunity to join forces with Spreedly, in order to help more merchants build best-of-breed fraud management solutions while still promoting growth,” Dodgeball CEO Adam Hiatt said. “The partnership will also help us provide much greater value to our existing customers. All of us at Dodgeball are excited to get started on integrating our offering with Spreedly’s.”

Most recently having demoing its technology on the Finovate stage at FinovateFall 2018 in New York, Spreedly has been a Finovate alum since 2013. The company, founded in 2008 and headquartered in Durham, North Carolina, counts major brands such as BMW, HBO Max, Priceline, The New York Times, and others among those that use its payments technology. Spreedly processes more than $50 billion in gross merchandise value (GMV) on behalf of more than 400 customers in 100+ countries.

Spreedly’s acquisition announcement came shortly before the company released its State of Checkout 2025 Survey, conducted by Talker Research on Spreedly’s behalf. The survey noted that many US executives remain concerned that AI could bring greater complexity to what they consider to be fragile checkout flows, leading to greater challenges and even financial losses.

“AI has incredible potential to transform payments,” Spreedly President Peter Dougherty said. “But executives in the survey also revealed they’re already paying a steep ‘engineering tax’—with as much as a quarter of their engineering teams dedicated to maintaining fragile checkout flows. AI should be layered thoughtfully to strengthen these payment systems, not replace them entirely and introduce new risks.”

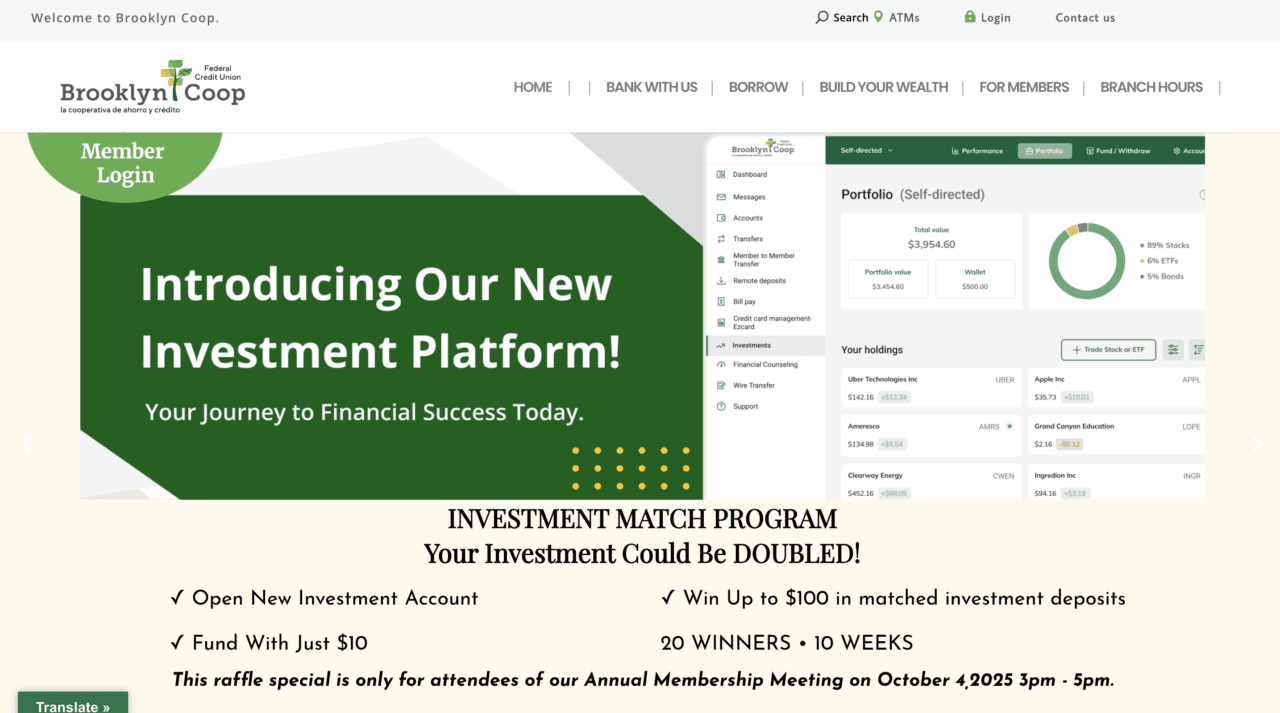

Eko Founder and CEO Mart Vos doesn’t care if you call his company “echo” or “eco.” But what he does care about is making it easier for community banks and credit unions to offer easy-to-use investment solutions to their customers and members—before they become enamored of the offerings by the new crop of digital investment brokers and platforms.

“I’m from the Netherlands,” Vos said to the FinovateFall 2025 audience last month in New York. “Back in the Netherlands, everybody invests their money with their trusted bank. And maybe it sounds weird. But to me, it’s very normal. If I want to invest my money, I’m going to go with a place that I know and trust. I know my bank. I trust my bank. So where else am I going to go than my trusted bank?”

This is the lens through which to view Eko’s latest partnership announcement, teaming up with the Brooklyn Cooperative Federal Credit Union. The partnership, announced last week, will enable Coop members to invest directly from their credit union’s platform. Members can start with as little as $10 and investment services are available in both English and Spanish. A certified CDFI (community development financial institution) and a Minority Depository Institution, Brooklyn FCU began operations in 2001 and serves central and eastern Brooklyn communities such as Bushwick, Bedford-Stuyvesant, and Crown Heights. The credit union is the third largest in its county, despite its relative youth, and currently has more than 7,200 members and $50 million in assets.

In a statement on LinkedIn, Vos noted that the full integration of Eko’s “one-stop investments shop” was completed in three weeks. Coop members will benefit from a seamless, integrated investing experience that sits within their current digital banking portal and/or app, flexible portfolio options including pre-built and hybrid investment pathways, and low barriers to entry with a streamlined onboarding process and the ability to start investing with as little as $10. The partnership news follows Eko’s second consecutive Best of Show win at FinovateFall (the company won its first Best of Show award at FinovateFall 2024), as well as recognition as “Best Fintech” at the Tennessee Credit Union League annual conference.

“This launch feels extra special to me personally: Brooklyn Coop is literally the credit union next door here in New York! Really proud to support Brooklyn Coop in making investing simple, affordable, and accessible for all members,” Vos said.

An embedded investment platform for banks and credit unions, Eko won Best of Show in its Finovate debut at FinovateFall 2024 and won again the following year at FinovateFall 2025. Headquartered in New York and founded in 2021, the company’s white-label solution integrates directly into digital banking infrastructures to enable customers and members to invest in pre-built portfolios, IRAs, cryptocurrencies, and more, as well as engage in hybrid investing and self-directed trading.

In its most recent Finovate appearance, the company demonstrated how its embedded AI assistants support investors by answering financial planning questions, providing investment research, and helping with tasks like setting up recurring deposits and rebalancing portfolios.

Fraud and financial crime prevention platform Feedzai has secured $75 million in funding at a valuation of $2 billion.

The company also announced that the European Central Bank (ECB) has selected it as the first-ranked provider for fraud and risk management for the digital euro, slated to be launched by 2029.

Founded in 2011 and headquartered in Portugal, Feedzai made its Finovate debut at FinovateEurope 2014.

In a big start to the month of October, fraud and financial crime prevention platform Feedzai has announced both a major funding round and a deal with the European Central Bank (ECB) to safeguard the digital euro.

First up, the funding. Feedzai has secured $75 million in a round that featured participation from new institutional investors Lince Capital, Iberis Capital, and Explorer Investments, as well as existing investors Oxy Capital and Buenavista Equity Partners. The funding, which takes Feedzai’s total capital raised to more than $352 million according to Crunchbase, gives the Portugal-based fintech a valuation of $2 billion.

In a statement, Lince Capital CEO Vasco Pereira Coutinho praised Feedzai for its use of AI and the company’s “end-to-end approach to risk operations.” Coutinho also underscored Feedzai’s ability to “execute across multiple product lines while scaling globally.”

Feedzai CEO and Co-Founder Nuno Sebastião spoke to the strong pace of innovation in the fraud prevention space, and pointed to the importance of future-proofing financial crime fighting technology. “This new investment round enables us to continue driving innovation to defend against whatever comes next, so that every form of payment, even those yet to be imagined, can be trusted and adopted safely,” Sebastião said.

Second, the ECB deal. The same day that Feedzai announced its major funding, the company also reported that the European Central Bank (ECB) has selected it as the first-ranked tenderer in its framework agreement to provide the central fraud detection and prevention solution for the to-be-launched digital euro. The framework agreement outlines the providers for five different digital euro components and related services: alias lookup, risk and fraud management, app and software development kit, offline solutions, and secure exchange of payment information. Feedzai is one of two providers in the risk and fraud management component; Capgemini Deutschland is the designated second provider. Service requests, according to the framework, will be initially directed to first-rank providers with second-rank providers contacted only as needed.

The framework agreement for the risk and fraud management component for the digital euro has been valued at €79.1 million ($92.8 million), with a maximum value of €237.3 million ($277.3 million). For its part, Feedzai is partnering with subcontractor PwC to deliver a state-of-the-art central fraud detection and prevention mechanism that complies with EU security, privacy, and data protection standards.

“Being selected as the first-ranked tenderer in the framework agreement to secure the digital euro is both an honor and a responsibility,” Feedzai’s Sebastião said. “With tens of billions of transactions expected across the eurozone, success depends on AI that can adapt as quickly as fraud evolves. Our role is to provide the intelligence that keeps even the most sophisticated fraud out, ensuring trust in every digital euro transaction from day one.”

Founded in 2011 and headquartered in Lisbon, Portugal, Feedzai made its Finovate debut at FinovateEurope 2014. Today, the company defends 900 million people in 190 countries from fraud with an end-to-end financial crime prevention platform that features AI-native solutions. Over the past year, Feedzai has launched a number of key products including its Feedzai Orchestration and Feedzai IQ, which empower financial institutions to make better, faster risk assessments. Feedzai has also introduced the TRUST Framework to embed fairness, explainability, and security into every component of GenAI model development.

In April, Feedzai acquired data management platform and fellow Finovate alum DemystData in a deal valued at $157 million.

Coupa has acquired AI-powered supplier discovery platform Scoutbee to enhance transparency and efficiency in supplier sourcing, onboarding, and transactions.

The move expands Coupa’s procurement ecosystem, adding Scoutbee’s collaborative tools and AI-driven supplier intelligence to Coupa’s $8 trillion spend management platform.

As competition in AI-enabled procurement heats up, Coupa’s acquisition positions it to better compete with SAP’s Ariba and JAGGAER in building a dynamic, resilient global supply chain network.

Spend management platform Coupa revealed today that it has acquired supplier discovery platform Scoutbee for an undisclosed amount.

Coupa anticipates that integrating Scoutbee’s tools into its platform will offer business clients greater transparency and efficiency in supplier discovery, onboarding, and transactions.

Scoutbee was founded in 2015 to connect buyers and suppliers through its AI-powered procurement platform, which includes a robust supplier database and collaboration tools. The California-based company has raised $76 million in funding to help organizations discover new, relevant suppliers and unlock new opportunities.

“We founded Scoutbee with the premise that AI can transform real-time sourcing and procurement by enabling buyers and suppliers to seamlessly connect, collaborate, and transact,” said Scoutbee co-founder and CEO Gregor Stühler. “Joining Coupa allows us to bring our mission to a global stage, and provide an exceptionally data-rich and comprehensive buyer-supplier network and B2B marketplace at scale.”

Coupa launched its AI platform for total spend management in 2006. The company’s platform contains a community-generated, $8 trillion dataset and brings autonomous AI agents, 10 million buyers and suppliers, and apps to automate the buying process. In 2022, Coupa was acquired by Thoma Bravo for $8 billion in cash.

“Coupa and Scoutbee share a fundamental belief that better data leads to better AI, better decisions, and ultimately, a better world through more resilient supply chains,” said Coupa Chief Product and Technology Officer Salvatore Lombardo. “Together, we are creating the world’s most comprehensive, dynamic, and data-rich network. This acquisition enables us to deliver a truly effortless buyer-supplier matching experience and further enhances our network that will power the future of global trade.”

Bringing Coupa and Scoutbee together under a united front will help fortify Coupa’s position in the race to dominate the AI-powered procurement and supplier intelligence space. With rivals like SAP’s Ariba Network doubling down on AI-enabled sourcing and JAGGAER investing heavily in autonomous commerce, Coupa’s move will deepen its supplier intelligence capabilities, reinforcing its position as a data-rich, network-first procurement ecosystem.

Each year, FinovateEurope brings together the brightest innovators in fintech to demo the future of financial technology. But for many companies, demoing their technology on the Finovate stage is more than just a moment in the spotlight, it’s a launching pad for growth.

Over the past 15 years, dozens of FinovateEurope alumni have captured the attention of major industry players, leading to high-profile acquisitions and partnerships. Below, we highlight some of the companies that turned their Finovate demo into their next big deal.

These success stories underscore how FinovateEurope has helped fintechs showcase their newest fintech innovation and connect it with the institutions and investors ready to scale it. From early-stage disruptors to industry leaders, the companies that have taken the Finovate stage prove that a seven-minute demo can spark partnerships, acquisitions, and growth.

As we look ahead to FinovateEurope 2026, we’ve already started to help the newest wave of fintechs prepare to take the spotlight. If the past 15 years are any indication, the ideas you will see on stage next February could be the ones reshaping fintech in the years to come.

Join us for FinovateEurope 2026 on February 10 through 11 in London. Tickets are available today at a discount, so register today and save!

BILL has launched a high-yield Cash Account for its SMB clients, offering 3% returns with no fees or minimum balance requirements.

The account provides enterprise-grade features like FDIC insurance up to $200 million, next-day ACH payments, and integrated cash management tools.

With nearly 500K small business clients and $266 billion in processed payments, BILL aims to help SMBs grow funds and optimize cashflow.

Small business financial software provider BILLlaunched a cash account that will offer high-yield savings opportunities to its small-and-medium-sized business clients. The BILL Cash Account will help SMBs earn a higher yield on their idle cash.

The California-based company is launching the new account to help its nearly half a million small business clients use manage their money with higher returns and stronger cashflow.

“Idle cash sitting in low-or no-yield checking accounts not only costs businesses time and money—it costs them opportunity to grow,” said BILL EVP, GM of Payments and Financial Services Mary Kay Bowman. “With Cash Account, we’re bringing growing businesses the same enterprise-grade capabilities normally reserved for Fortune 500 companies—combining high APY on an operational account with fast speed, seamless software integration, and security all in one simple account.”

BILL’s new Cash Account offers enterprise-grade tools to help businesses grow their funds confidently, with FDIC insurance coverage of up to $200 million. The high-yield account pays 3% returns, which is 42 times the national average of 0.07%. Unlike many competitors, BILL doesn’t require businesses to hold a minimum amount of funds in their accounts and does not charge fees. Users also benefit from next-business-day ACH payments and cash management tools.

Founded in 2006, BILL helps its small business clients automate their financial operations and has processed $266 billion in payments volume. The company, which trades on the New York Stock Exchange under the ticker BILL, went public in 2019 and has a market capitalization of $5.54 billion.

Dutch insurtech RISK has acquired Amsterdam-based savings app Dyme. Terms of the transaction were not disclosed. The deal will enable Dyme to boost its presence in the Netherlands as well as enter the German market. Courtesy of the agreement, both Dyme’s brand and management team will remain intact.

“From being featured on Dragon’s Den to becoming one of the largest finance apps in Europe and reaching profitability, our mission has always been the same: helping people take control of their money,” Dyme noted on its LinkedIn Page. “This step opens up some great opportunities for Dyme and its customers: expand the product, especially with great insurance packages and service, reach millions more people through the RISK ecosystem, and take Dyme international, beginning with Germany.”

Dyme currently has more than 600,000 consumers who have linked their bank accounts to the Dyme platform. The company’s app serves as a personal financial assistant to help users lower costs, and uses smart algorithms to automate subscription cancellations and provide financial guidance. Dyme announced its first profitable quarter in 2024, and has said that it has helped users save more than €40 million since inception. The acquisition will combine RISK’s market expertise and technological platforms with Dyme’s user-friendly financial solutions that enable users to easily manage their expenses, budgets, and more.

RISK offers an advanced IT platform, SureBase, that assists financial advisors, online labels, and insurers in product comparison and distribution. SureBase, according to RISK CEO Harm Vollmuller, will serve a key base for the new synergy between RISK and Dyme. “By combining that with our platforms and market knowledge, we can reach people at a time when financial breaking space is more important than ever,” Vollmuller said.

“This new facility is a testament to the trust and confidence Brand New Day Bank has placed in Factris and our vision for SME financing,” Factris CEO Brian Reaves said. “As we continue to scale across Europe, this partnership ensures we can meet the increasing demand for alternative financing and provide SMEs with the liquidity they need to thrive.”

Founded in 2017 and headquartered in Amsterdam, North Holland, Factris specializes in invoice factoring for small and medium-sized enterprises. The company offers selective factoring to enable companies to decide which specific invoices to factor, fund availability within 24 hours of invoice submission, credit insurance to protect against customer non-payment or bankruptcy, and debtor management for collections and account receivables.

Brand New Day Bank is a Netherlands-based digital-first, challenger bank and fintech that began operating in 2010. The financial institution serves both individuals and small-to-medium sized businesses with savings accounts, investment and pension products, tax-advantaged savings and investment solutions, and annuity payment services. Brand New Day Bank has more than €8 billion in assets.

Digital banking experience platform Plumeryannounced a suite of new features and integrations designed especially for credit unions in Canada. These new capabilities will give these institutions the ability to provide personalized, compliant, and modern digital banking experiences for their members.

The Amsterdam-based fintech leveraged a collaboration with Aequilibrium, a digital services and technology consultancy headquartered in Vancouver, British Columbia, to make sure its Canadian-ready platform is built based on the way that Canadian credit union members prefer to bank. This includes not just hyper-personalized, mobile-first, and intuitive digital journeys, but also support for everyday payments and transfers including billpay and Interact e-Transfers, and Canadian savings and lending products like GICs.

Plumery’s move comes as Canadian banks and credit unions face a range of challenges including evolving customer expectations, fintech competition, and the pressure to modernize their legacy systems. More immediately, Canadian credit unions are scrambling in the wake of Central 1 Credit Union’s announcement that it will wind down its digital banking platform Forge (formerly MemberDirect). More than 170 credit unions across Canada had been relying on the technology.

“With Forge winding down, Canadian institutions have a rare opportunity to modernize on their own terms, rather than being tied to outdated systems,” Plumery CEO and Founder Ben Goldin said. “Our platform provides an immediate, future-ready option that puts control back in the hands of credit unions. By working with Aequilibrium, we are combining global banking innovation with local expertise to deliver experiences that meet the unique needs of Canadian credit unions’ members.”

Founded in 2016, Plumery enables financial institutions to offer unique mobile and online experiences on top of either their modern or legacy core banking platforms up to 80% faster. Plumery’s technology features foundations that are pre-integrated into its digital banking journeys that accelerate app development and shorten time-to-market while maintaining complete control over both design and functionality.

India’s Bank of Baroda launched its eRUPI Person-to-Person (P2P) gifting solution.

TBC Uzbekistan extended financial services to non-residents.

Indian fintech Kiwi unveiled its interest-backed EMI on UPI.

Latin America and the Caribbean

Brazilian digital banking giant Nubank has applied for a US national bank charter.

Unlimit announced securing Principal Membership with Mastercard and Visa in Peru.

Brazi-based proptech Lastro raised $15 million in Series A funding in a round led by Prosus Ventures.

Asia-Pacific

Cambodian MSME-focused bank Chief Bank teamed up with payment solutions provider BPC to launch its new Chief Mobile 3.0 mobile app.

The People’s Bank of China opened a digital yuan operation center in Shanghai.

The Hong Kong Monetary Authority (HKMA) and the Hong Kong Science and Technology Parks Corporation (HKSTP) launched IADS Developer Hackathon to promote bank-fintech collaboration.

Mastercard Commerce Media has launched to leverage consumer-permissioned transaction data, giving 25,000 advertiser partners smarter targeting and delivering up to 22x ROAS across industries like retail, travel, and dining.

Mastercard’s partnerships with Citi, American Airlines, Microsoft, and WPP will expand scale, reach, and brand integration.

Retail media networks are surging, with spending projected to hit nearly $100 billion by 2028. Chase Media Solutions, which launched in 2024, is an example of how financial institutions are monetizing first-party data to serve personalized offers.

Mastercard announced that it will begin leveraging consumer-permissioned data via its new digital media network, Mastercard Commerce Media. The new media network will give Mastercard’s 25,000 advertiser partners access to transaction data from the 500 million enrolled consumers in order to power smarter, personalized commerce.

Through Mastercard’s proprietary Offers platform, advertisers can deliver tailored campaigns, such as cashback, discounts, and incentives, to audiences defined by their business goals. Using insights from consumer-permissioned data, Mastercard identifies the right customers and delivers relevant advertising content. Consumers can then activate offers on their enrolled card and complete the purchase, with Mastercard directly attributing the transaction to the campaign.

Beyond traditional cashback, Mastercard Commerce Media helps publishers strengthen brand loyalty by enabling programs where consumers earn rewards in a brand’s own cash currency, giving shoppers more purchasing power and brands deeper engagement. Looking ahead, Mastercard plans to expand distribution to new channels and deepen integrations across its broader services portfolio beginning in 2026.

Mastercard processed more than 160 billion transactions in 2024, and its new media network will deliver proprietary insights from transactions like these processed by Mastercard. Mastercard Commerce Media currently delivers a return on ad spend (ROAS) of up to 22 times for advertisers across retail, travel, entertainment, dining, and more.

“We understand how to connect advertisers to consumers and consumers to the products, services and experiences they value,” said Mastercard Chief Services Officer Craig Vosburg. “Mastercard Commerce Media is a natural extension of the trusted connections we’re known for and the work we already do across our unique suite of services. That means we’re not just well-positioned to bring a full-scale commerce media network to life—we’re best-positioned.”

Mastercard Commerce Media is launching in partnership with Citi, which will help the program grow faster, reach more users, and deliver more value. Mastercard already has ongoing ties with Citi, which will give Mastercard’s media network a head start in leveraging Citi’s infrastructure, customer base, and channels. Mastercard is also partnering with American Airlines, Microsoft, and WPP, which will help extend its footprint and connection to brands in the traditional media space.

As the use of consumer-permissioned data gains popularity across fintech subsectors, so too has the adoption of retail media networks. These networks allow institutions to monetize their first-party data by connecting brands with highly targeted audiences through trusted digital channels.

According to eMarketer, retail media networks will expand in the coming years. The firm estimates that retail media network spending will reach nearly $100 billion through 2028, reflecting both advertiser demand and consumer engagement with personalized content. An early trailblazer in the space is Chase Media Solutions, which launched in 2024 to leverage its transaction and cardholder data to serve personalized offers and marketing to its 80 million customers.

Account holder engagement specialist Larky has announced a strategic partnership with digital banking solutions provider Tyfone.

Courtesy of the partnership, Larky will integrate its nudge engagement platform into Tyfone’s nFinia digital banking solution.

Tyfone made its Finovate debut at FinovateSpring 2008. Larky first demonstrated its technology to Finovate audiences at FinovateFall 2014.

Proactive account holder engagement company Larky has inked a strategic partnership with digital banking solutions provider Tyfone this week. The agreement will integrate Larky’s nudge platform directly into Tyfone’s nFinia digital banking solution.

“At Tyfone, we believe that elegant user experiences are only the starting point,” Tyfone CEO Siva Narendra said. “What truly sets us apart is our commitment to innovation, collaboration, and execution. Partnering with Larky extends that commitment, helping our clients engage their customers and members in meaningful ways that strengthen relationships and deliver lasting value.”

Larky’s nudge platform provides real-time personalized notifications to enhance the ability of financial institutions to connect with their account holders. The solution enables financial institutions to increase deposits and new loans, and prevent fraud with tailored, turnkey push notifications. Financial institutions using nudge leverage data-driven and location-aware messaging to secure customer and member engagement rates that are seven to ten times higher than with traditional marketing channels.

Via a pre-built integration with Tyfone’s digital banking technology, Larky’s notification capabilities are seamlessly embedded, empowering banks and other financial institutions to bring additional value by way of the mobile channel that customers use and trust. Financial institutions will be able to choose from either a library of pre-built campaigns or deploy Larky’s AI-powered solutions to create messaging that is customized for their specific audiences. This messaging can help banks and other financial institutions to encourage debit card use, boost fraud prevention awareness, announce the launch of new solutions, and more.

“We’re thrilled to launch our partnership with Tyfone and bring our nudge platform to more community financial institutions,” Larky CEO Gregg Hammerman said. “Tyfone’s focus on meaningful digital relationships aligns perfectly with our mission to help account holders receive relevant, timely engagement where it matters most.”

Founded in 2012 and headquartered in Ann Arbor, Michigan, Larky made its Finovate debut at FinovateFall 2014. More recently, the company has forged partnerships with core banking solutions provider VisiFi, and began this year teaming up with data analytics and business intelligence solutions company for credit unions Trellance. Larky has raised more than $4.5 million in funding, according to Crunchbase, most recently securing an investment from Reseda Group in 2023.

Portland, Oregon-based Tyfone has been a Finovate alum since its debut at FinovateSpring 2008. The company’s nFinia digital banking platform offers account management, fund transfers, and billpay services, as well as payment solutions and personal finance management (PFM) tools. The platform also features Penni AI integration that delivers conversational banking capabilities including smart tools and intelligent, personalized support, 24/7.

Tyfone’s partnership news with fellow Finovate alum Larky comes just days after the company reported collaborating with another Finovate alum, BioCatch. Last month, the two companies announced a strategic partnership that integrated BioCatch’s Account Takeover Protection solution into Tyfone’s nFinia platform.

“Account takeover fraud is one of the most pervasive threats in digital banking,” BioCatch Senior Director of Global Integration Partners and Alliances Jay Whoriskey said. “By embedding our behavioral intelligence into Tyfone’s digital banking platform, community financial institutions gain real-time protection, identifying and stopping fraud before any money leaves the would-be-victim’s account without compromising the user experience.”

Founded in 2004, Tyfone has raised more than $38 million in funding, according to Crunchbase. This figure includes the company’s $25 million venture round in 2023.

How is AI helping lenders make better loans to more qualified borrowers? How can stablecoins promote cross-border trade and help local merchants make more sales in more markets? How can banks overcome the limitations of their legacy systems and confidently embrace modernization? The latest round of interviews from Finovate VP Greg Palmer and the Finovate Podcast cover all these issues and more.

Here’s a look at the Finovate Podcast’s recently completed September slate. By the way, the first few podcast interviews with FinovateFall Best of Show winners have just begun to drop. If you want to get an early listen, check them out on our Finovate Podcast page.

Greg Sullins (LinkedIn), Head of the US Banking Center of Excellence for Newgen Software, talks with Greg Palmer about how AI is revolutionizing the lending process. Sullins explains why AI is especially valuable in the lending business, in part because it sits at the intersection of data intensity, risk management, and the customer experience. Episode 271.

Founded in 1992, Newgen Software offers lenders a low-code platform that provides end-to-end automation, AI-powered decisioning, configurable workflows, and enhanced customer experience capabilities. The company’s technology enables business analysts rather than programmers configure workflows and deploy changes quickly. This helps financial institutions modernize their legacy systems faster while remaining compliant.

Bridgit Antwi (LinkedIn), Head of Strategy and Planning at Flutterwave, talks with Greg Palmer about the rise of stablecoins, the importance of building strong relationships across the financial ecosystem, and what Flutterwave is doing to help local merchants expand their reach across borders. Episode 270.

Africa’s leading payments company, Flutterwave was founded in 2016 by Olubenga “GB” Agbola. The firm offers a single API platform that enables merchants to seamlessly collect payments across multiple countries, currencies, and payment methods. Flutterwave operates in more than 30 countries, holds licenses in 14 African nations, and maintains 35 money transfer licenses.

Rouzbeh Rotabi (LinkedIn) Chief Revenue Officer at Qolo and Greg Palmer talk about the challenge and opportunity of payment infrastructure modernization. With more than 20 years of experience in fintech and payments, Rotabi explains how the need to increase deposits, infrastructure limitations of legacy systems, and evolving consumer demands are pressuring banks to embrace new technological solutions. Episode 269.

Founded in 2018 and headquartered in Fort Lauderdale, Florida, Qolo offers an all-in-one platform for card issuing, ledger management, and payment processing. The company helps businesses launch faster, lower costs, and secure real-time visibility into the payment flow.

Bill Harris, fintech pioneer and former CEO of Intuit, PayPal, and founder of Personal Capital, has unveiled a new digital RIA focused on affluent and high-net-worth investors.

Evergreen Wealth combines agentic AI advice with fiduciary advisors, offering Dynamic Portfolios designed for hyper-personalization and advanced tax optimization.

Moving beyond early roboadvisors, Evergreen Wealth blends human expertise, AI analytics, and tax-efficient strategies to meet changing expectations of younger, affluent clients.

Serial entrepreneur Bill Harris unveiled his newest fintech yesterday. The new wealthtech, Evergreen Wealth, is a digital Registered Investment Advisor (RIA) that provides investment management with a tax-forward mindset.

The launch builds on Harris’ long track record in both wealth management and tax innovation. On the wealthtech side, he founded Personal Capital in 2009, one of the first hybrid roboadvisors, which grew to manage $23 billion in assets before selling to Empower in 2020 for $825 million upfront. On the tax side, Harris led TurboTax and later served as CEO of Intuit in the late 1990s. He also briefly served as an early CEO of PayPal in 1999, cementing his reputation as a serial fintech entrepreneur.

Harris said that the launch comes at a time of changing market environment and consumer expectations. “Younger, affluent investors want more than traditional products and quarterly meetings—more than half don’t want their parents’ advisors,” said Harris. “They demand sophisticated tax and investment services, available on their schedule. We built Evergreen Wealth for this generation of investors.”

As a new wealthtech in the AI era, Evergreen Wealth offers agentic AI-powered financial advice to affluent and high-net-worth clients. The company is differentiating itself with its Dynamic Portfolios that contain hundreds of individual securities that can be tax-optimized and hyper-personalized to match the clients’ goals.

Tax optimization is a key focus for Evergreen Wealth. The company leverages multiple tax strategies, such as direct indexing, to help offset, reduce, defer, and even eliminate taxes on their investments. This is important for high-income taxpayers in high-tax states when they are trying to beat the market.

Along with its emphasis on tax efficiencies, Evergreen Wealth also focuses on offering a high-touch approach. The company’s advisors are fiduciaries that leverage research from Evergreen Intelligence, the company’s financial knowledge base, in order to deliver personalized advice to their clients. These tools allow advisors to offer each client personalized insights and advice.

“We combine human expertise with AI analytics to create a new model for financial advice,” said Harris. “It’s the best of both worlds—experienced advisors plus advanced technology.”

Today’s launch solidifies an era of change in the wealthtech space. While early wealthtechs leveraged the roboadvisory strategy, today’s consumers want an even deeper approach when it comes to managing their wealth. By offering a tax-forward mentality combined with agentic AI tools and a high-touch, personal approach, Evergreen Wealth is adapting to consumers’ changing preferences.

Sales platform Xaver unveiled a range of new features that arm financial advisors with an Agentic AI workforce that “assists, advises, and acts.”

The new functionality reduces the number of hallucinations, features 24/7 call answering with AI-native advisors, and provides greater accuracy compared to popular Large Language Models (LLMs), the company said.

Founded in 2023, Xaver made its Finovate debut at FinovateEurope 2025 in London. Co-founder Max Bachem is CEO.

White-label, omnichannel sales platform Xaver has introduced a range of new features the company pledges will “open a new chapter for financial advisory with an AI workforce that doesn’t just assist, it advises, and acts.”

The new functionality includes three elements in particular that respond to key barriers that regulated businesses and organizations can face when looking to adopt AI-powered solutions. To start, Xaver has leveraged context engineering, a model-independent data ingestion layer, and multi-agent orchestration to reduce the number of hallucinations by 80%. This “safer by design” strategy makes the technology more appropriate for operation in high-risk, regulated environments with both auditability and human oversight.

Second, the company has shown through independent testing that its AI agents outperformed leading LLMs when it comes to regulated financial-advice accuracy. This is important insofar as companies in regulated industries have expressed concerns about AI being able to consistently achieve this level of accuracy. Third, Xaver has introduced 24/7 call answering with voice-native AI advisors who can resolve incoming questions, qualify interest into warm leads, and seamlessly transfer calls to a human agent, when appropriate.

“Powered by Xaver’s MCP-enabled investment infrastructure rails, our AI advisors do things no other AI can today,” the company noted on its LinkedIn page.

Pictured (left to right): Nigel Jankelson (COO) and Max Bachem (CEO & Co-Founder), Xaver

Xaver’s enhanced offering enables financial advisors to use the AI agents as “prep partners” to provide instant briefs, conduct prospect research, suggest next-best actions, and build both tailored playbooks and compliant document packs. The AI agents run in parallel to the client journey, “like a personal AI advisor at your side. Always on, cost-efficient, infinitely scalable,” the company explained. The new features also include the ability to conduct phone, email, and WhatsApp campaigns—including automated follow-ups—from first touch to booked meeting or sale.

Xaver made its Finovate debut at FinovateEurope 2025 in London. At the conference, the company demonstrated its sales platform that leverages specifically trained and compliant AI agents to handle a variety of tasks including financial analysis, data extraction, and the creation of personalized customer journeys. Fully ISO27001, GDPR, and EU AI Act-compliant, Xaver’s platform orchestrates multiple LLMs to deliver 24/7 AI-powered guidance via chat and voice. At the same time, the technology is able to introduce human advisors into the workflow as needed.

“This platform has four main components,” Xaver co-founder and CEO Max Bachem explained from the Finovate stage earlier this year. “First of all, we are providing AI-generated, tailored, personalized online journeys for each customer. Second, we have AI advisors who can compliantly advise customers and do conversational sales. But we have an omnichannel approach so, number three, we do seamless handovers from these digital channels … to your in-person financial advisor. And, number four, when you are with the in-person financial advisor, the AI is then acting as a co-pilot for that advisor.”

Bachem co-founded Xaver with Ole Breulmann (CPTO) in 2023. The company is headquartered in Cologne, Germany.