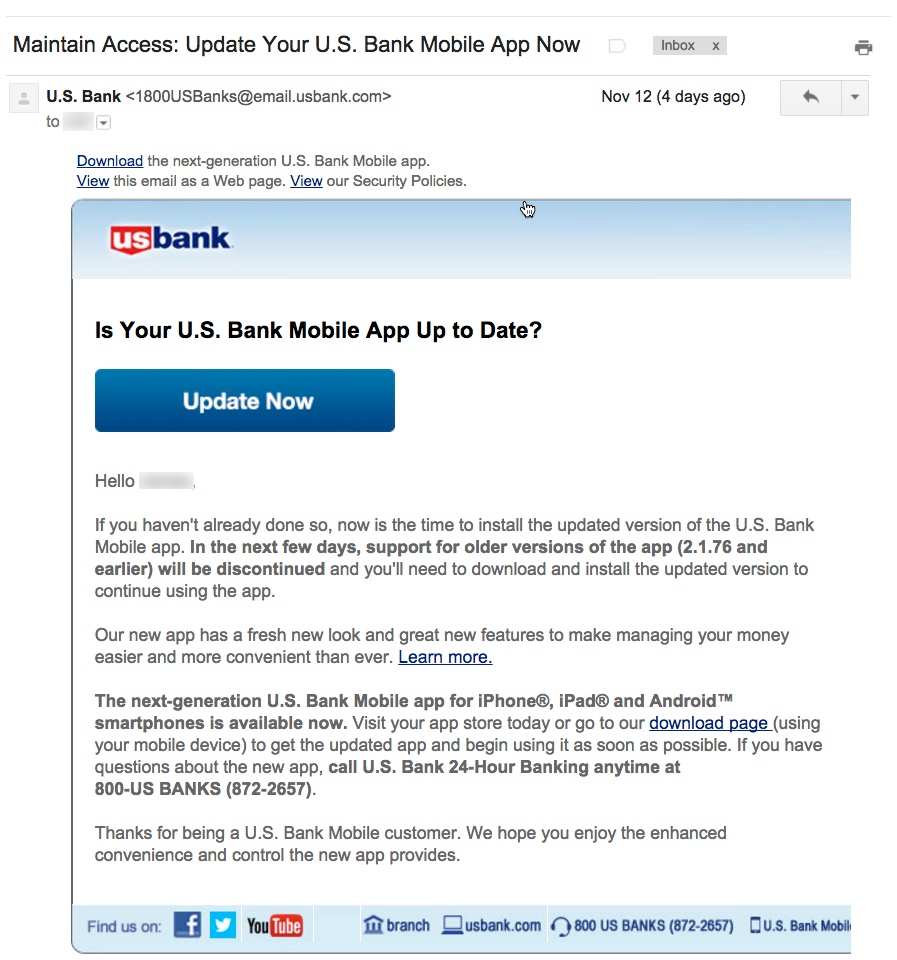

I know our readers have passed graduate level coursework in digital banking. But sometimes, even the PhD candidates need a refresher in the basics. Here’s a fundamental that too many financial institutions neglect:

I know our readers have passed graduate level coursework in digital banking. But sometimes, even the PhD candidates need a refresher in the basics. Here’s a fundamental that too many financial institutions neglect:

Make it super easy for visitors (non-customers especially) to find information about online and mobile banking

Just about every bank has an obvious login button in the top-right or top-left corners (or Chase who has it plastered in the middle). That’s fine for existing customers. But what about those simply shopping banks? You would think that online/mobile capabilities are pretty important to someone checking you out online!

The big-four U.S. banks do a good job exposing online and mobile features. Citibank is especially focused with its “bank online….make memories offline” tagline mid-page (screenshot below).

But finding the online banking features often requires menu hunting (see BofA, Chase, and Wells below) and/or promotion scanning (see Citibank, Wells and Atlantic Regional FCU below). And sometimes, it’s below the fold (Sterling Bank, BECU) or a screen away (see Comerica below).

Bottom line: You don’t want to get too cute with the fundamentals. That’s why we like the direct approach of both U.S. Bank and Bank of American Fork who position Online Banking as the first tab in their primary navigation (screenshots below). Alternatively, startups Moven and Simple use page-dominating screenshots of their mobile app to position themselves with mobile bankers (see below).

————————————-

Bank of American Fork

No, that’s not a typo. This community bank blankets American Fork, Utah, with its 13 branches. It places online banking in its own tab, plus it launches a huge mega-menu detailing all the personal and business online and mobile features. (Plus it has cookies, the kind you eat, in one of the four rotating promotions).

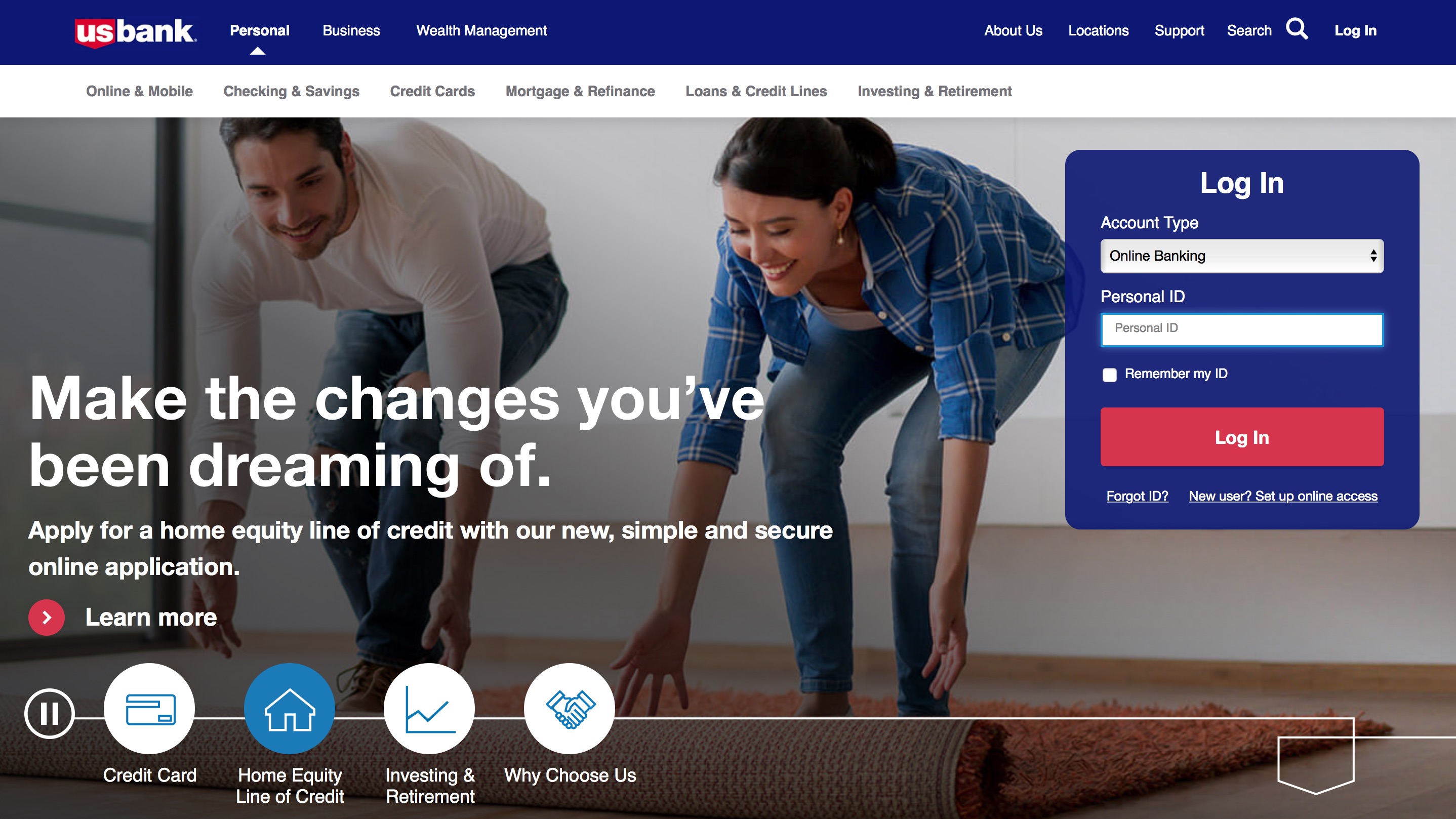

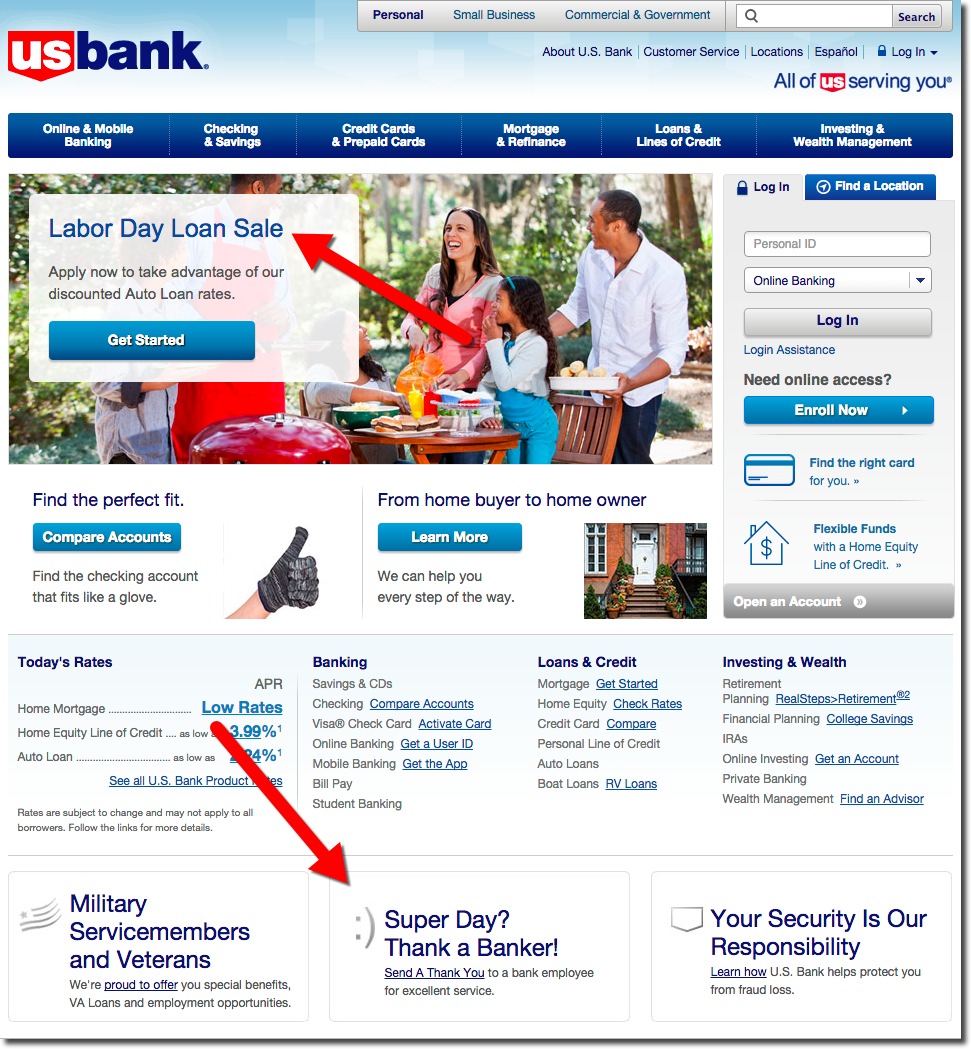

US Bank

US Bank is the only one with an “online banking” tab. And it’s positioned in the pole position. Mobile banking is listed in the mega-menu.

_____________________________

The big 4 (alpha order)

Bank of America

While it’s not in the main tab, both online and mobile are mentioned on mega-menu displayed when you hover over the “Bank” tab. And there is an online banking promo in the lower left.

Chase

Similar approach to Bank of America. However, online and mobile are buried pretty far down the popup mega-menu.

Citibank

Citi does not beat around the bush. Their entire homepage is devoted to driving users to online banking (first screenshot). And those that launch the mega-menu, see online banking, billpay & Popmoney at the top (second screenshot). However, the bank has no mention of “mobile” anywhere.

Wells Fargo

Online & mobile have the top position under “Banking” on the homepage. In addition, there are promotions and links scattered about the homepage.

_____________________________

Other examples

Atlantic Regional Federal Credit Union (link)

If you don’t have online banking in the main nav, you need to compensate elsewhere. Atlantic Regional’s BancVue-designed site uses the fashionable full-page graphic to draw attention to its four rotating promotions. Number 2 leads shown below leads directly to online banking info. The CU is also running a mobile banking announcement across the top of the page.

Bank Simple

Simple turns the double-play with an excellent welcome video and a snazzy shot of its iPhone app in action.

Moven Bank

Moven is all about the mobile, and visitors can’t miss that with the page-dominating visual.

Comerica

The bank currently has no mention of online banking on its homepage. However, once a visitor goes to the Personal or Small Business page, it is listed on the drop-down mega-menu.

—————————

Note: We cover financial website and mobile design issues periodically in our Online Banking Report (subscription).

A look at the companies demoing live at FinovateSpring on May 8 through 10, 2019 in San Francisco, California. Register today and save your spot.

Tory Passons, VP & Group Product Manager

Tory Passons, VP & Group Product Manager

In my annual look at holiday offerings from major banks, I found that Scrooge still roams the halls at many of the big names. Only eight of the 20 largest U.S. banks are using holiday-themed promotions or graphics (note 1). That’s one more than

In my annual look at holiday offerings from major banks, I found that Scrooge still roams the halls at many of the big names. Only eight of the 20 largest U.S. banks are using holiday-themed promotions or graphics (note 1). That’s one more than