The coffee shop where I do much of my writing held a huge sale yesterday. But you wouldn’t have known it from the sparse late-July mid-day crowd. The event took place entirely online through local deal-of-the-day marketer, Groupon.

The coffee shop where I do much of my writing held a huge sale yesterday. But you wouldn’t have known it from the sparse late-July mid-day crowd. The event took place entirely online through local deal-of-the-day marketer, Groupon.

The day-long sale resulted in nearly 3,000 half-price $10 coupons being sold, a huge influx of customers for a 3-location coffee shop (see screenshot below). I’m working somewhere else tomorrow when the coupon buyers start coming in.

Groupon is the leader in the burgeoning field of localized flash marketing (aka social/group buying) having taken more than $170 million in VC funding to expand to more than 150 cities.

Groupon is the leader in the burgeoning field of localized flash marketing (aka social/group buying) having taken more than $170 million in VC funding to expand to more than 150 cities.

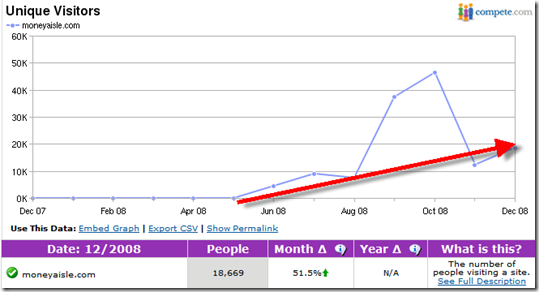

The other major player is Living Social, which I’ve successfully used a few times to buy gifts. LivingSocial has raised $50 million and recently expanded to 52 cities. Both companies have nearly 5 million unique monthly U.S. visitors (see below). And with minimal barriers to entry, there are dozens of copycat sites in operation.

There’s another sub-category in flash marketing, companies that specialize in certain types of merchandise. The pioneer here is the geeky and irreverent gadget and T-shirt marketer, Woot with 2.3 million monthly visitors. The site was scooped up by Amazon for $170 million last month. In women’s fashion, Gilt Groupe has a cult following and nearly 1 million monthly visitors.

U.S. traffic at Groupon (blue), Living Social (green), Woot (orange), Gilt Groupe (red)

Source: Compete (link)

Flash marketing is not a new concept, and it’s not much different than the $299 laptop on the cover of the Best Buy circular. Savvy shoppers know to show up early at the store if they want to claim one of the few loss leaders in stock.

Web-based flash marketers use email, Facebook and Twitter to inform potential customers of the latest deal. There is usually a time limit, typically a single day, and/or a limited number for sale. All the Groupon deals expire at midnight local time. Woot runs all its deals for 24 hours, or until they sell out, beginning at midnight Central Time.

Opportunity for Netbankers

While I haven’t seen a financial product sold on Groupon or LivingSocial yet, there’s no reason it wouldn’t work. In a quick search, the only financial institution participant I found was First Tech Credit Union, a recent recipient of sponsorship recognition in a LivingSocial deal for half-off tickets to the 2010 Bellevue (WA) Jazz Festival (see second screenshot).

But the promotions can be costly. The flash marketing companies typically take 50% of the sales price and require a deep discount, usually 50% or more off list prices. So retailers are getting as little as 25 cents on the dollar in the promotions (see note 1). Quantities can be limited to protect against too many takers.

While financial services don’t lend themselves to online flash sales as well as spa visits or fine dining, there are fee-based services that could work. For example:

- Checking account: $15 annual fee (first year) instead of $96 list price (note 2)

- Credit monitoring: One year for $50 instead of the $150 list

- Credit report: One 3-bureau report for $10 instead of the $30 list

- Financial plan: $50 instead of $200 list

- Prepaid MasterCard/Visa: One $25 card for $15 instead of the $29.95 list (assuming $4.95 issuing fee)

- Savings account: $50 initial deposit for $15 fee (note 2)

- VIP banking package: $25 annual fee instead of more than $100 if bought separately (rewards card, premium service, free VIP online banking, credit report, rate discount, etc.)

Or FIs could go the First Tech route and work with local restaurants, theatres, or nonprofits to sell a product bundle. For instance, a $20 dining certificate, 50% off on theatre tickets and a $10 Visa card for $20.

Groupon Seattle deal-of-the-day at Zoka Coffee Roasters (26 July 2010)

First Tech Credit Union gets top billing on recent LivingSocial deal (link)

Notes:

1. That assumes all coupons are redeemed. But typically a large portion, as much as 50%, go unredeemed. That means fewer new customers in the door, but it also helps limit the amount of discounts that must be honored.

2. The problem with many financial product offers is that not all customers will be approved. But you could offer refunds for anyone declined for a checking account.

3. For more info on selling online, see our Online Banking Report on Lead Generation.

Next up is

Next up is