This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Have you listened to the latest episodes of the Finovate Podcast?

Over the past few weeks, Greg Palmer and the Finovate Podcast have hosted some of the most interesting innovators in fintech. Alan Bekker of eSelf on the future of AI in financial services, The Clearing House’s Jim Colassano on real-time payments, financial inclusion and wealth-building with Rodney Williams of SoLo Funds … these are just a handful of the interviews Greg Palmer and the Finovate Podcast have featured in recent weeks.

Don’t miss another conversation! Join Greg Palmer and his guests on the Finovate Podcast today!

Greg Palmer interviews Alan Bekker, co-founder and CEO of customer engagement innovator, eSelf. The two discuss the role of AI in fintech and financial services, and the future of face to “face” interactions. eSelf won Best of Show in its Finovate debut at FinovateFall 2023. Episode 208.

The rise of real-time payments, especially in the U.S., is creating opportunities and challenges for fintechs and financial services companies alike. Greg Palmer sits down with Jim Colassano, SVP of Product Development and Strategy with The Clearing House, to discuss what institutions need to do in order to take advantage of one of the latest innovations in payments. Episode 207.

Greg Palmer catches up with Jack Spiers, Sales Director at Tink, to discuss the findings of a new report from the Best of Show winning company that details how to enhance affordability assessments with enriched data. Episode 206.

Dr. Adam Lowe, Chief Product & Innovation Officer with CompoSecure, talks with Finovate Podcast host Greg Palmer on how to think about fraud prevention as an asset, and the importance of balancing security and customer experience. Episode 205.

As part of the Finovate Podcast’s commemoration of Black History Month, Greg Palmer and Rodney Williams, co-founder, chairman, and President of SoLo Funds, talked about the challenges of creating wealth-building products for underserved communities. Episode 204.

Last month at FinovateEurope, I had the pleasure of conducting interviews with 14 professionals, entrepreneurs, and authors from the world of fintech and financial services. A few days ago, I shared videos of my conversations with Moneyhub’s Samantha Seaton and Finthropology’s Anette Broløs.

Today, I’m unveiling another pair of interviews from FinovateEurope. First, I sit down with Edwin Van Bommel, Head of Strategy and Innovation with ABN AMRO Bank. In his role with the bank, van Bommel is responsible for introducing new products and services to clients in the areas of artificial intelligence and distributed ledger technology.

In our conversation, van Bommel and I talk about the different ways ABN AMRO Bank is leveraging enabling technologies like embedded banking, generative AI, and distributed ledger. We also talk about the challenge of legacy systems and why they will still “play an important role in the future” of financial services.

In our second video interview, Indrek Vainu, Head of Conversational AI at Zurich Insurance Group, and I talk about the challenge and opportunity of artificial intelligence in financial services. We discussed ways that generative AI, for example, is bringing innovation to both the front and back office. Vainu also shared what he believes are the next steps in AI adoption in fintech and financial services.

In his role as Head of Conversational AI at Zurich Insurance Company, Vainu leads activities globally that are related to Generative AI and chatbots. He co-founded AlphaChat, a chatbot startup that was acquired by Zurich Insurance Group in 2021.

March 10th marked the one-year anniversary of the collapse of Silicon Valley Bank (SVB). While the event isn’t necessarily something to celebrate, it is a great time to reflect on what the industry has learned and how things have change.

Looking back on the aftermath of SVB’s liquidity crisis, we have seen shifts in behavior and strategy that are starting to reshape the landscape for both banks and fintechs. I had the privilege to speak with Law Helie, General Manager of Consumer Banking at nCino, to gain insights into these changes and how institutions are adapting to meet evolving consumer expectations and regulatory demands.

Finovate: We’re approaching the one-year anniversary of SVB’s liquidity crisis. In the past 12 months, how has the industry responded? Have you seen any changes in behavior from banks or fintechs?

Law Helie: Regardless of size, a consistent banking trend is the re-emphasis on building up deposits. After the liquidity crisis last year, banks became more risk-averse and leaned on their deposits as a shield against volatility.

Another trend is the shift to relationship banking via technology. Banks are leveraging cloud-based tools to unlock more data within their organization to better inform and tailor their services to customers for core offerings, including loans, CDs, high-yield savings and more. We expect intense competition around these services as banks prioritize opening multiple service streams with customers to deepen the relationship and hold onto deposits.

Finovate: How will banks approach their spend on fintech following the SVB crisis?

Helie: Expect banks’ spending on fintech tools to grow exponentially. This isn’t a new phenomenon, but the pace of acceleration since SVB is significant as banks seek ways to better compete in a crowded market.

Banks are deploying technology to help understand their cost of funds base, attract deposits, drive internal efficiencies and, most importantly, to help create a sense of stability. As we await more certainty from the Fed around economic forecasting, we expect to see an increase in tech spending, especially at a time when banks’ appetite for increasing efficiency continues to grow at a rapid pace.

Finovate: How about end consumers—both retail and commercial bank customers—have they changed their attitudes and behavior?

Helie: Post-SVB, end consumers in all lines of business are more aware and educated on deposit limit risks that come with over-exposure. Our FIs have told us that their customers are searching for ways to have more security, including wanting to know how they can limit their risk of exposure and how to structure their accounts for FDIC limits. In addition, some of our customers have incorporated the use of CDARS, a Certificate of Deposit Account Registry Service, that can help customers disperse funds into multiple accounts.

The overall attitude and behavior of end consumers is now that they need to pay attention to FDIC limits, disburse their deposits, and have an increased focus on their wealth management. This shift underscores a proactive approach among consumers toward safeguarding their financial assets.

Finovate: Given these behavioral and attitude shifts, how can banks and fintechs adapt to these changes?

Helie: Most banks have siloed systems, meaning there is no singular source of truth for their data. Yet customers don’t think this way – they look at their needs holistically. Serving these customers requires a client-centric model that is efficient and driven toward self-service.

And the more products a customer has with a bank, the stickier they are. In order to retain existing and new depository relationships, banks can best position themselves by providing a wide suite of banking offerings and services, in particular digital offerings.

Banks also have an opportunity to leverage fintechs to gather a 360-degree view of the customer, allowing them to understand what is going on across all accounts. With that information, banks can leverage relationship banking techniques to provide customers with the tailored products and services that they want and need.

Finovate: What impact has SVB’s liquidity crisis had on regulations so far and how are banks and fintechs responding?

Helie: Regulations have been put in place to try and mitigate the risk of another SVB collapse. Despite NYCB’s recent issues, we are not seeing the same level of concern spread to other financial institutions as it seems the public has a better understanding of the underlying reason for the issues NYCB is currently having.

Financial institutions are actively pursuing ways to strengthen their deposits bases by reviewing FDIC limits. Notably, some FIs have taken measures to impose restrictions on the maximum amount of cash that can be held in an account, aligning with the FDIC limit. Fintechs are helping FIs by not only providing the framework for streamlined experiences that help meet customer needs, but also allowing them to responsively acquire new funds for those customers looking to diversify their deposit base.

Finovate: Looking ahead, what advice do you have for banks and fintechs navigating the ever-competitive game of increasing deposits?

Helie: The market expects the Fed to reduce interest rates one-to-three times this year. Americans are waiting on the sidelines for better rates so that they can shop for refinancing or fresh loan opportunities.

Banks that are well-prepared have a tremendous opportunity to help people get a better handle on their finances and position themselves as a partner for life. Those that struggle to quickly evaluate inquiries or match competing offers could frustrate customers that want to take advantage of the improving environment.

Cloud-based tools that utilize data and AI to help banks evaluate a fresh loan or refinancing request quickly are at a tremendous advantage. Institutions that maintain the sleepier pace of the past year will be rapidly outpaced by their peers and they will have few opportunities to make up the gap.

This year at FinovateEurope (27-28 February) I will be interviewing 15 fintech entrepreneurs, CEOs, analysts, authors, and thought leaders on what they believe are the most important topics and trends in fintech and financial services. Here’s a preview of the people I’ll be speaking with, a note on what they will be presenting at FinovateEurope, and a sense of the questions I’ll be asking them next week.

Be sure to stay tuned immediately after the event as we begin to roll out our Finovate TV interviews from FinovateEurope.

Anette Broløs – Director and Founder, Finthropology

Anette will be a part of our Wednesday afternoon Power Panel: From Open Banking To Open Finance & Beyond – How Can Banks Seize The Opportunity To Generate Returns?

I will ask Anette about the challenges that financial institutions face when trying to become more customer-centric. We’ll also discuss her new book, Customer-Centric Innovation in Finance, which explains how to turn human insights into product innovation.

Nina Schick, Author, Generative AI Expert, Founder, Tamang Ventures

Nina will deliver our Out of the Box Keynote Address Tuesday morning titled Will AI Be More Profound Than The Invention Of The Internet? What Do Financial Institutions Really Need To Understand About Generative AI?

I’m looking forward to learning more about what financial services need to know about de-risking the adoption of enabling technologies like AI. I’m also curious what other enabling technologies Nina thinks should be on our radar.

Indrek Vainu, Head of Conversational AI, Zurich Insurance Company

Indrek will be a part of our Wednesday afternoon Power Panel: AI In Action & Real User Cases: How Smart Players Are Using AI To Solve Pain Points For Their Customers & Their Business. He will also deliver a keynote address – How Financial Institutions Can Harness The Era of Generative AI – as part of our invitation-only session Monday evening for financial institutions.

In our conversation at FinovateEurope, I want to hear about the challenges Indrek and his team have faced as they implemented generative AI applications at their firm. What lessons and insights can he share with other financial services as they embark on their AI journeys?

Ville Sointu, Chief Strategist, Digital Currencies, Nordea

Ville will be a part of our Wednesday afternoon Power Panel: Digital Payments Are Eating The World – How Will New Competitors & New Business Models Shape The Future?

I’m curious to learn from Ville about how embedded payments are spreading throughout Europe. I’m also interested in learning about his interest in super apps, which he mentioned last year. How might the rise of super apps impact the payments landscape?

Janine Hirt, CEO, Innovate Finance

Janine will be a panelist on our Tuesday evening Executive Briefing: What Embedded Finance & Banking As A Service Mean For Banks – Can You Afford to Hold Back?

I will ask Janine about the future of Banking-as-a-Service and embedded finance in Europe. I’m looking forward to hearing her take on how the competitive landscape for service providers – beyond retailers and Big Tech – will evolve in this context.

Ken Hughes, Consumer Behaviouralist, The King of Customer Experience

Ken will deliver an Out of the Box Keynote Address Wednesday morning titled, Financing the Future: Preparing For The Customer Of Tomorrow.

I want to ask Ken about the Customer of Tomorrow. In what key ways will the customer of tomorrow differ from the customer of today?

I’m also looking forward to hearing his thoughts on customer-centric innovation and how traditional brands are adapting to new challenges and opportunties.

Valentina Kristensen, Director of Growth & Communications, OakNorth

Valentina will be part of our special panel titled, Women in Fintech: How Can We All Make Sure We Are Moving The Needle?

I would like to hear from Valentina on the evolution of DE&I initiatives in recent years. How effective have these efforts been in terms of attracting and retaining female talent, in particular?

I also want to learn from Valentina about how financial institutions can be more responsive to their female professionals as they move through various stages of their careers.

Manas Chawla, CEO, London Politica

Manas will provide a Keynote Address Wednesday morning titled, The Global Economic & Geo-Political Outlook – What Are The Five Things You Need To Know?

He will also deliver a special Fireside Chat: The Escalation of Geopolitical Risk – What Does It Mean for Banks And Their Customers? as part of our invitation-only session for financial institutions Monday evening.

Always an engaging interview, Manas is likely to have a lot to say about the myriad geopolitical issues that are dominating headlines in 2024. How will these various crises – from Europe to Asia to the Middle East to the American border – impact banks, fintechs, and financial services companies? I’m eager to hear what Manas has to say about all of it at FinovateEurope next week.

Jurgen will be a part of our Wednesday afternoon Power Panel titled, Tales From The Frontline – How Can Financial Institutions Deliver Excellent CX By Blending The Human & The Digital?

I want to talk with Jurgen about the impact of enabling technologies in the wealth management space. I’m curious how everyoneINVESTED is innovating in this area and what innovations in the investing experience are most compelling for customers in wealth management.

Nadia Edwards-Dashti, Co-Founder & Chief Customer Officer, Harrington Star Group

Nadia will moderate our Wednesday morning panel titled, Women in Fintech: How Can We All Make Sure We Are Moving The Needle?

In our Finovate TV conversation, I want to talk with Nadia about how many of the people she talks with in her podcast, Women of Fintech, are driving positive change in fintech and financial services.

I would also like her opinion on what it takes for companies to create more inclusive workplaces for their employees.

Samantha Seaton, CEO, Moneyhub Enterprise

Samantha will deliver a Special Address Wednesday morning titled, Your Product Isn’t The Hero – Your Customer Is.

I’m eager to hear from Samantha about how companies in financial services can pivot from an emphasis on the product to a more customer-centric approach.

I’m also curious how she sees the impact of technologies like AI and the role they may play in helping financial services companies make this pivot. I also will ask Samantha about her overall sense of the state of fintech right now.

Stephen Hutchinson, Head of Operations, IFX Payments

A few years ago a venture capitalist reminded us from the Finovate stage that “payments are the gift that keeps giving.”

With that in mind, I’m looking forward to talking with someone who walks the payment talk in Stephen Hutchinson, Head of Operations at IFX Payments.

I will ask Stephen what payment trends he finds most exciting and how he believes those trends will impact IFX Payments. We will also talk about some of the key targets and goals for IFX Payments in 2024.

Jose Luis Navarro, Head of Open Banking Strategy, BBVA

Jose will be a panelist on our Wednesday afternoon Power Panel titled, From Open Banking to Open Finance & Beyond – How Can Banks Seize The Opportunity To Generate Returns?

Given the success of open banking and open finance in Europe compared to many other parts of the world (I’m looking at you, US of A!), I’m eager to learn from Jose about what’s working in Europe and how BBVA has managed to capitalize on current trends in open banking and open finance.

I also will ask about the regulatory risks of open banking and open finance, and what institutions need to know in order to navigate these issues.

Edwin van Bommel, Chief Strategy and Innovation Officer, ABN AMRO Bank

Edwin will be part of our Wednesday morning Power Panel: Finding New Opportunities Through Digital Transformation – Success Stories & Insights To Help Financial Institutions Find Growth, Drive Revenue & Future Proof Their Business.

In my conversation with Edwin, I’m looking forward to learning more about AMRO Bank’s product roadmap, and the degree to which he sees AI becoming a greater part of financial services overall. I also want to talk with Edwin about the challenge traditional banks have when it comes to overcoming legacy systems.

Katharina Lueth, Chief Client Officer and Managing Director, Raisin

Katharina will be part of our Wednesday morning Power Panel: Why Fintech Will Revolutionize Customer Experience & How Financial Services Providers Can Compete In A Hyper Personalized World. What Are They Key Lessons To Learn From Other Industry Verticals & From How Big Tech Companies Build Customer Trust?

How can a financial services company that operates in multiple geographies successfully provide personalized services in these different regions? What are some of the key trends in fintech that are impacting what Raisin’s customers want and how is Raisin adapting to meet these trends?

These are a few of the questions I’m looking forward to asking Katharina next week at FinovateEurope.

There’s still time to pick up your ticket and join us for one of the most loaded FinovateEurope conferences to date! Visit our FinovateEurope page and register today!

We’re starting off our Women in Fintech series this year with a conversation with Erin Wynn. As Executive Director of Product Management at NCR Voyix, Wynn helps both community banks and credit unions form strategies to implement their digital transformation and product roadmap initiatives.

Wynn also works as a mentor and coach for the company’s internal pre-sales teams. In this role, she helps ensure that sales engineers, solution architects and business analysts are supporting NCR Digital Banking’s vision and solutions.

We caught up with Erin Wynn to talk about her own beginnings in fintech, as well as what she is learning from her customers and clients about the most important trends in our industry.

NCR Corporation changed its name to NCR Voyix in the fall of 2023 as the company spun-off its ATM-based business, known as NCR Atleos. Headquartered in Atlanta, Georgia, the company has 35,000 employees globally, and trades on the NYSE under the ticker symbol “VYX.” NCR has been a Finovate alum since 2015.

How did you get started in fintech? What has led you to where you are today in your career?

Erin Wynn: I began my career in 1998, working at a bank, where I got my first taste of fintech. I worked so closely with one of our vendors, Digital Insight, that I even went to work for them for a few years before a different opportunity presented itself. In the long run, however, I knew Digital Insight was my home, and I returned to them in 2012. Digital Insight was acquired by NCR Voyix’s Digital Banking platform in 2014, but has managed to keep the familial relationship that drew me back here.

My dedication to being a lifelong learner has led me to amazing opportunities, holding various positions within NCR Voyix. I look at every experience as a chance to be curious and learn something new. Whether it be from a client, a colleague, or a partner, I believe everyone has something valuable to share and learn from.

My passion and deep understanding for how our products work and helping financial institutions achieve success have been central to my growth. As the executive director of product management for Digital Banking at NCR Voyix, I lean into my banking experience to help community financial institutions develop strategies for implementing digital transformation and better support their consumers and communities. I empower them to help customers and members improve their financial wellness — a topic I’m especially enthusiastic about (and one that’s driven my career in banking!).

Which digital banking features and capabilities are most resonating with clients? What trends are top of mind for customers?

Wynn: A significant trend we’ve seen is centered around personalization, which really means reminding the consumer that you know and care about them; they’re not just another number. This means creating digital experiences that feel like they’re catered to each user. Financial institutions are realizing that they can’t just compete on low loan rates or high deposit rates. Even if that’s what got the consumer in the door, it won’t be what keeps them there. The financial institutions that emphasize building and maintaining relationships, as well as providing meaningful tools and support (such as financial wellness resources), will be better positioned for loyalty and success.

Another major trend I’ve seen is finding ways to increase overall efficiency. This can mean embracing more automation or researching ways to better maximize current staff and technology. Our clients, like most people, are looking for ways to simplify processes and quickly solve problems. For example, NCR Voyix can support marketing automation, an area of typically high turnover within institutions, helping banks and credit unions make every interaction count.

What has been the impact of AI on banks and credit unions and their accountholders? How should financial institutions begin to incorporate AI into their organizations?

Wynn: AI has notable potential. It can create personalized interactions with each consumer at scale and significantly increase efficiencies. AI can help institutions approach certain processes in different ways. For example, more institutions are using AI when it comes to lending decisions instead of solely relying on traditional factors.

However, when it comes to AI and, especially, generative AI, banks and credit unions should know that the technology is only as strong as the data and information behind it. There is a lot of work to train AI to make AI effective; it’s not a magic bullet. You must give it the right data and training to effectively work, while continuing to provide human oversight.

My advice for banks and credit unions who are considering how to use AI is to first ask themselves what they’re trying to accomplish. For example, is there more of a need to enhance back-office efficiencies? Or are they trying to offer different ways to support users? Don’t try to do everything all at once; it will be too much. Understand that it won’t be perfect from day one. You’re going to have to experiment and improve the AI along the way.

What does it mean to effectively humanize digital experiences? How can banks and credit unions accomplish this?

Wynn: Effectively humanizing the digital experience means leading with empathy throughout the user experience on their phone or online. This could be something as simple as analyzing the language used in an error message. Evaluate everything with a person in mind; are you providing them with relevant information in a human way, making them feel comfortable and supported along the journey? Of course, personalization is also a major factor here, as well. Money and finances are extremely personal, and they need to be treated with care.

Data is a core factor when it comes to humanizing digital. Effectively leveraging data can uncover crucial consumer behaviors, channel preferences, transactional patterns, and key events in the consumer journey. Employing technologies like AI enables financial institutions to analyze this data more effectively, anticipating member behaviors and offering contextual assistance, such as tailoring their website content to specific needs.

Looking ahead, I expect banks and credit unions to prioritize looking for ways to incorporate more empathy and personalization within their platforms, which will drive relationships and loyalty with their consumers.

Are there any leadership tips that you would like to share with other strong females in a male dominated industry?

Wynn: It all comes down to confidence. Knowing your worth and intelligence goes a long way. Surround yourself with a strong group of women who lift you up and encourage you. When you start to see yourself the way others see you, you are more likely to take a risk in your career or feel more confident to speak up. Also, recognize what motivates and drives you, and know that it’s okay if those things change over time. Everyone constantly evolves in their journey, and you’re sure to learn something every step along the way.

Headlines announcing layoffs in fintech and banking have been pulsing throughout the news cycle since the start of last year. And according to one fintech expert, we may see more throughout 2024.

And while there is no doubt that layoffs and job losses are personally devastating to those involved, there may be a silver lining. Freeing up talent– especially experienced and/or technical talent– allows other organizations in the sector the opportunity to capture new, experienced professionals while offering individuals the chance to level up their career.

In a series called Fintech Founders, our sister publication Fintech Futures recently produced five videos on hiring. The videos capture founders’ thoughts on their internal hiring process, how they intentionally build their company culture, their hiring strategy, how they create a versatile team, and upcoming industry trends.

This week on the Finovate Podcast, Finovate VP and podcast host Greg Palmer sat down with fintech strategist, host of the Cyber Insiders Podcast, and owner of PR firm KCD PR, Kevin Dinino.

Dinino is founder and President of KCD PR, one of the top ranked public relations and marketing firms with an emphasis on financial services, fintech, technology, and transportation. He manages the day-to-day business operations for the firm, and leads business development while providing strategic counsel to clients on high profile issues.

Dinino is also host of Cyber Insiders, an iHeartRadio podcast series that features industry leaders involved in the cybersecurity industry.

In his Finovate Podcast interview, Dinino talks with host Greg Palmer about the “wonders and blunders” from 2023. Dinino also shares his ideas about what to expect from the world of fintech and financial services in 2024.

Last year was really quite an eventful year in terms of fintech and banking. Look at the Super Bowl last year to kick of 2023. We had TV commercials with the amazing Larry David in it for FTX and, in the ad, the irony of the campaign was that it was called Don’t Miss Out. And his character was like, ‘Eh, maybe I don’t want to do that’.

So it’s hard not to lump in what happened with crypto in general last year. Various scandals, FTX, and everything that happened with SBF probably being among the bigger ones, for sure. There was plenty on the ‘blunder’ side with that.

Check out Episode 201 of the Finovate Podcast and the rest of the conversation featuring Greg Palmer and Kevin Dinino of KCD PR.

U.S. Bank’s innovation team recently attended the Consumer Electronics Show (CES) in Las Vegas last week on what it called a “Future Safari.” After attending the show in 2023, the team was back on the lookout for emerging tech trends with the potential to impact the financial services industry, emphasizing AI, autonomy, embedded financial services, and the intersection of physical and digital realms.

We interviewed U.S. Bank’s innovation team to get a view of CES under a fintech lens, as well as to get a peek at U.S. Bank’s tech-forward initiatives in 2024 and beyond.

U.S. Bank’s innovation team attended the Consumer Electronics Show in Las Vegas last week. What was the team looking for?

U.S. Bank Innovation Team: We look for several things. First and foremost, we are looking for emerging tech and trends that may have an impact on the financial services industry and/or our customers.

We also look at trends and activity across several technology verticals to see if there is technology that we need to get ahead of.

Another thing we look for is specific new tech we might be able to test and pilot. And, of course, it’s great to see what other industries are doing with the technology that is coming to market.

In general, what are some fintech trends U.S. Bank is currently exploring or excited about?

U.S. Bank Innovation Team: At U.S. Bank, we cover a broad range of technologies, domains, client segments, and industries as part of how we try to develop and deliver the future now. Some of the broad trends we’re exploring at the show include AI and autonomy, of course, and how these technologies can change peoples’ lives; the embedding of financial services into all manner of products, services, experiences; how devices are proliferating and what that means for how we help people optimize their financial lives; and how the physical and digital parts of life are changing thanks to new technologies. We’re exploring dozens of trends in many sectors, but those are a few at a high-level that our Future Safari to CES helps us to gauge.

As a large bank, how does U.S. Bank make the decision whether to build or buy new technologies?

U.S. Bank Innovation Team: As a large bank, we like to focus on our core competencies and make decisions that reduce risk. Particularly in tech areas outside of our expertise (technical or business), we will look first to partner.

For example, we aren’t going to try to build our own quantum computer any time soon. We did build our award-winning mobile app, and we do build the majority of our digital customer facing experiences. Some components of those experiences may be provided by fintechs that we partner with when there is a time to market/cost/economic advantage or they have expertise outside of the banking/financial services realm that will improve our customers’ experience. At the end of the day, it is all about the customer experience.

What are some tech-forward initiatives we can expect to see U.S. Bank come out with this year?

U.S. Bank Innovation Team: While I can’t preview any planned announcements for later this year, we use Future Safaris like these to inform insights that help us create amazing experiences for our clients.

One example of how we’ve used these Future Safari insights in the past is that we were able to be the first bank to integrate with all three virtual assistants – Siri, Google, and Alexa. That work later informed the launch of our own industry-leading virtual assistant, U.S. Bank Smart Assistant, which built the foundation for when we created our Spanish Smart Assistant – the nation’s first Spanish-language voice assistant for banking. All of these were informed by early innovations in voice technology that we were seeing at CES. It gave us early signals into what would be important to people and allowed us to envision how we might integrate these kinds of emerging technologies into how we serve our clients.

What was your favorite non-fintech innovation you saw at the show?

U.S. Bank Innovation Team: We really liked the Genesis Systems WaterCube 100. It is a cube about the size of an air conditioner that pulls water from the air. It runs on low enough power to operate on solar panels and can be dropped in to emergency areas in need of clean water, or it can be used for off-grid and remote applications for both commercial and consumers.

The Federation of International Drone Soccer League out of Korea was very cool! The drone soccer league had a big space where they were demonstrating drone soccer – for Harry Potter fans, it looks a lot like quidditch. We thought it was great as it turns a fun solo activity that kids are into these days into an in-person competitive event. Also, it looks like tons of fun!

We are always amazed by the advances in big farm technology. In the John Deere booth, we saw their latest line of tractors that can be operated manually, remotely, or autonomously. They showed their custom GPS, which can get the behemoth tractors to plow and deliver seeds within one-inch accuracy.

We also noticed a trend of high-end, battery powered campers from the super-luxury concept at LG with built-in bars and entertainment, to Jackery and Goal Zero camper concepts with built-in solar batteries and rooftop tents with low-power fridges and a plethora of glamping features. Going off-grid and connecting to nature may also have plurality creature comforts in the future.

Companies and innovators are raising the bar across all industries, and we continue to push ourselves to do the same.

Group photo left to right: Todder Moning, Head of Applied Foresights; Rosa Dunn, Assistant Vice President, Digital Innovation; Cynthia A. Jackson, Vice President, Digital Innovation; Andrew Cantrell, Sr. Applied Foresights Strategist; Don Relyea, Chief Innovation Officer

Our final Finovate Global column of 2023 celebrates the conversations we’ve had this year with fintech innovators from around the world.

Stay tuned in 2024 for more interviews with some of the most interesting founders, entrepreneurs, and thought leaders in fintech and financial services.

“We developed BehaviorQuant because every financial decision is ultimately made by a person or a team. BehaviorQuant solves a core problem that underlies the entire investment industry: we don’t have systematic knowledge about the people and teams behind investment decisions. And that’s true for financial professionals and clients alike.” Dr. Thomas Oberlechner, founder and CEO of BehaviorQuant. Interview.

“Moniepoint solves the problem of fragmented, inaccessible, and low-quality financial services for businesses in emerging markets. It is a full-service business banking platform seeking to provide all the digital financial services a typical business needs.” Tosin Eniolorunda, founder and CEO of Moniepoint. Interview.

“Eight hundred million voice conversations are recorded daily in Europe and many more worldwide. A tiny 1% of these conversations are checked for quality control, employee training, and business results improvement. Ender Turing is a conversations intelligence and automation platform to close 99% of the conversation gap for business growth.” Olena Iosifova, CEO of Ender Turing. Interview.

“Capital raising is broken. Private companies spend months and even years in the fundraising process, learning how to raise capital and repeating the same mistakes, approaching the wrong investors and often spamming them with irrelevant investment opportunities.” Ulyana Shtybel, CEO of Quoroom. Interview.

“At Refine intelligence, our mission is to help banks regain that superpower of really knowing their customers’ life stories, so their financial crime teams can quickly clear AML or scam alerts triggered by legitimate customer activity. We work with Risk, Financial Crime, BSA and AML teams. Fraud teams look at our technology to help with scam operations.” Uri Rivner, co-founder and CEO of Refine Intelligence. Interview.

“It was an honor to be ranked by CB Insights in its Fintech 250 list and, as one of only seven African start-ups featured, it speaks to the pioneering approach we are introducing to the world – revolutionizing payments and creating a financial services ecosystem for Africa.”

“As sub-Saharan Africa gains recognition on the global stage, we are seeing innovative and pioneering products emerge and rise in popularity amongst consumers, diversifying the products they can choose from.” Tayo Oviosu, founder and CEO of Paga. Interview.

Here is our look at fintech innovation around the world.

Asia-Pacific

Singaporean fiat-to-crypto payment gateway Alchemy Pay forged a partnership with Worldpay from FIS.

Indonesian P2P fintech JULO added insurance coverage with the launch of its JULO Cares solution.

Hungary’s OTP Bank partnered with Intellect Global Consumer banking (iGCB), the consumer banking arm of Indian banking technology copany Intelltect Design Arena.

The Fintech Founders series, presented by our sister publication Fintech Futures, features fintech and financial services veterans sharing their insights and experiences on a range of topics important to businesses in our industry.

Today we share five conversations on fintech funding featuring our panel our fintech experts. As part of our Funding Series of discussions, our panelists talk about issues such as: bootstrapping versus external funding, finding the right investment partners, the importance of producing significant growth, as well as tips for entrepreneurs and surprises our panelists encountered in their own journeys in fintech and financial services.

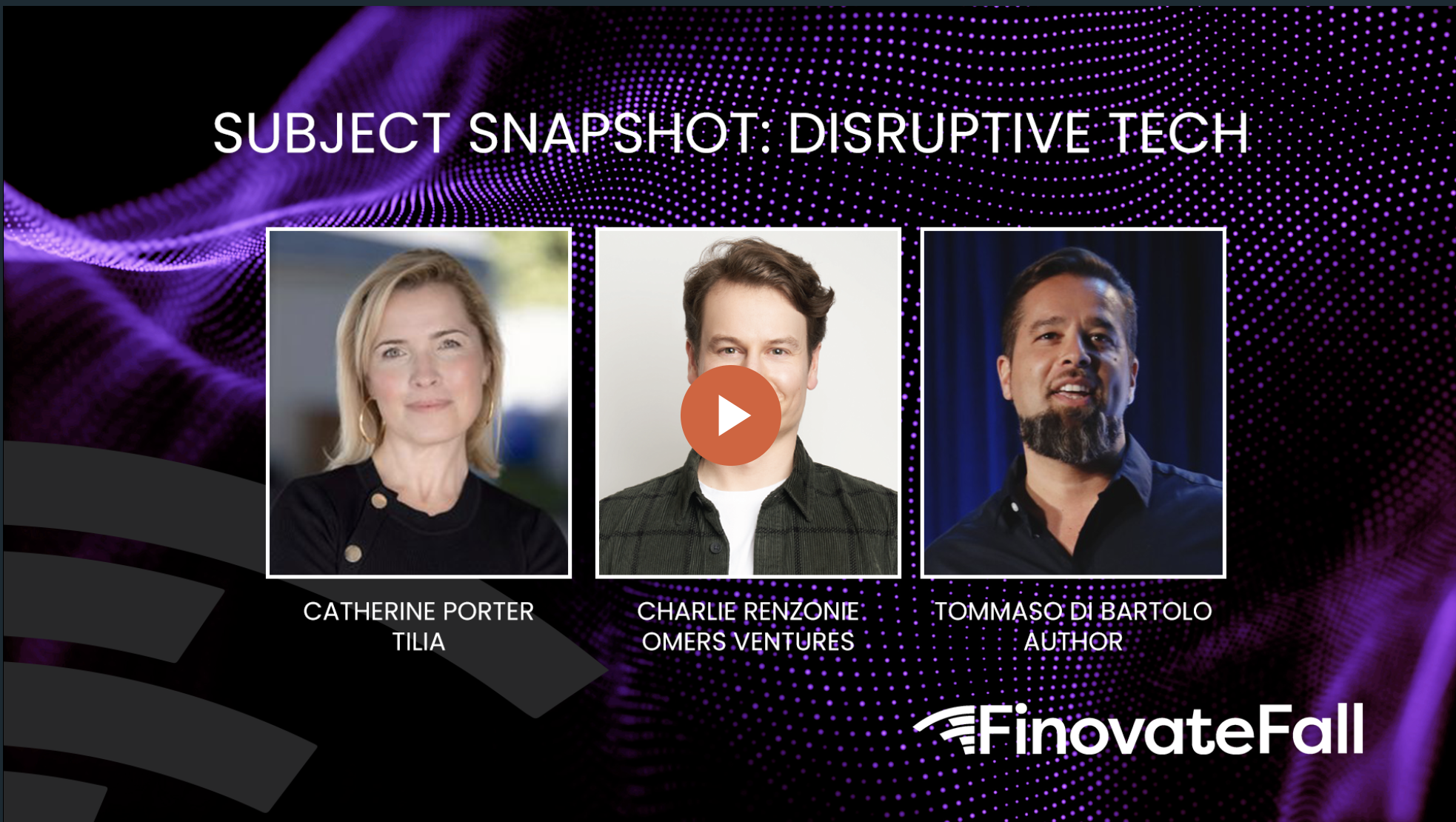

How will disruptive technologies like Generative AI change the financial services landscape. How will these technologies impact our ability to expand financial wellness and promote financial inclusion?

The rise of disruptive technologies has created new opportunities for banks and financial services companies to bring new and better services to consumers and businesses. Here’s a look at what our fintech experts told us this year at FinovateFall about how disruptive technology will shape the future of finance.

This year at FinovateFall we heard from fintech analysts and financial services professionals on what financial institutions can and should do in order to bring better financial services to more individuals, families, communities, and businesses. Here’s a brief Streamly Snaphot sharing what our experts had to say.