This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

This week’s edition of Finovate Global showcases fintech innovation in Indonesia.

Thought Machine helps modernize Islamic finance

Core banking and payments technology company Thought Machinehas partnered with BCA Syariah to bring digital, Sharia-compliant financial products and services to its customers. The bank, a subsidiary of Bank Central Asia (BCA), has deployed Thought Machine’s core banking platform, Vault Core, which has enabled the institution to launch a number of new solutions. These offerings include Wadiah savings, a top-up e-wallet, and an online service Hajj Fee deposits. BCA Syariah also plans to launch term deposit products and gold financing “soon.”

“(Vault Core’s) Universal Product Engine allows us to create Sharia-compliant products with precision and swift responsiveness to evolving customer needs,” BCA Syariah Director Lukman Hadiwidjaja said. “Our successful go-live marks an important milestone in our mission to contribute significantly to the development of Sharia banking in Indonesia.”

Thought Machine’s Universal Product Engine features out-of-the-box Sharia-compliant products, enabling institutions to develop and customize a broad range of integrated financial solutions on a unified platform. In operation since 2010 and headquartered in Jakarta, Indonesia, BCA Syariah was named “Best Performing Sharia Bank in 2024” at the 13th Infobank Sharia Awards in October.

“BCA Syariah has demonstrated exceptional foresight in leveraging modern technology for enhanced user experiences,” Thought Machine CEO and Founder Paul Taylor said. “This milestone underscores our unwavering commitment to empowering financial institutions to innovate, grow, and outperform in their markets.”

Founded in 2014 and headquartered in London, Thought Machine made its Finovate debut at FinovateEurope 2018. At the event, the company demonstrated its Vault core banking product, which today is used by institutions ranging from global Tier 1 clients such as Standard Chartered and Lloyds Banking Group to fintechs and challenger banks like Trust Bank and Atom Bank.

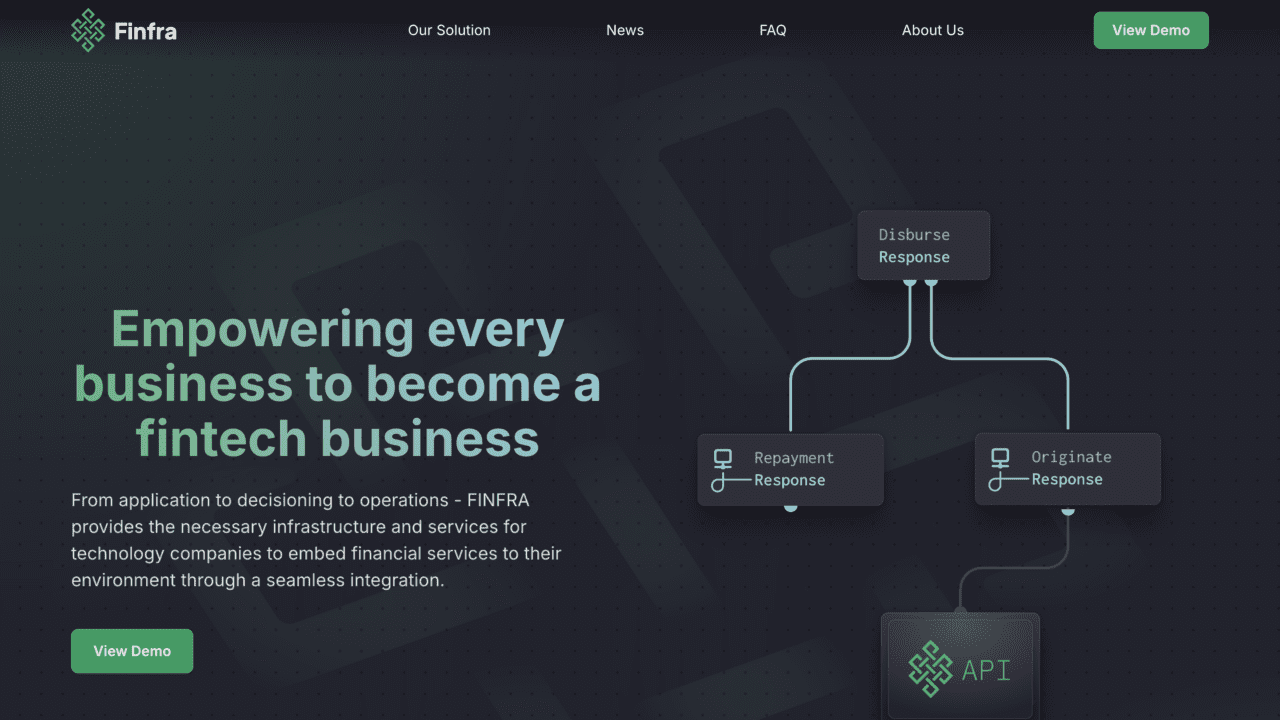

The investment is a $2.5 million fundraising led by Cento Ventures and featuring participation from Accion Venture Lab, Z Venture Capital, and Avafin founder Matiss Ansviesulis. In a statement on LinkedIn Finfra CEO Markus Prommik, thanked his team and the company’s shareholders for their support and “for believing in this mission.”

Finfra also announced a new strategic partnership with Tyme which will bring the company’s embedded lending infrastructure to India. This, according to Prommik, will “unlock new opportunities for SMEs to access finance and drive meaningful impact. This partnership is more than a business collaboration; it’s a validation of our vision for Finfra and the future of lending!”

Founded in 2022 and headquartered in Singapore, Finfra enables technology companies to seamlessly embed financial services — from application to decisioning to operations — into their platforms. Finfra offers invoice, payroll, and working capital financing, as well as healthcare financing to give patients an alternative way to pay for medical procedures. The company’s technology has disbursed more than 325,000 loans to date, valued at more than $50 million. Prommik noted in his statement that Finfra has doubled its gross profit year-over-year, as well as its client base.

Here is our look at fintech innovation around the world.

Sub-Saharan Africa

Konsentus forged a collaboration with the Bank of Namibia to support the bank’s open banking initiatives.

Brokerage-as-a-Service fintech DriveWealth secured a brokerage license from the Bank of Lithuania.

Borse Stuttgart Digital turned to Fenergo to scale compliant crypto solutions across Europe.

Middle East and Northern Africa

International money movement firm TerraPay teamed up with Suyool to enhance financial accessibility in Lebanon.

Mastercardpartnered with Arab Regional Payment System, Buna, to reduce friction in cross-border payments.

Open API banking solutions company Codebase Technologies and AI-based identity verification specialist IDWise announced a collaboration to help banks in the MENA region fight financial crime.

This week’s edition of Finovate Global features news from the fintech industry in Nigeria.

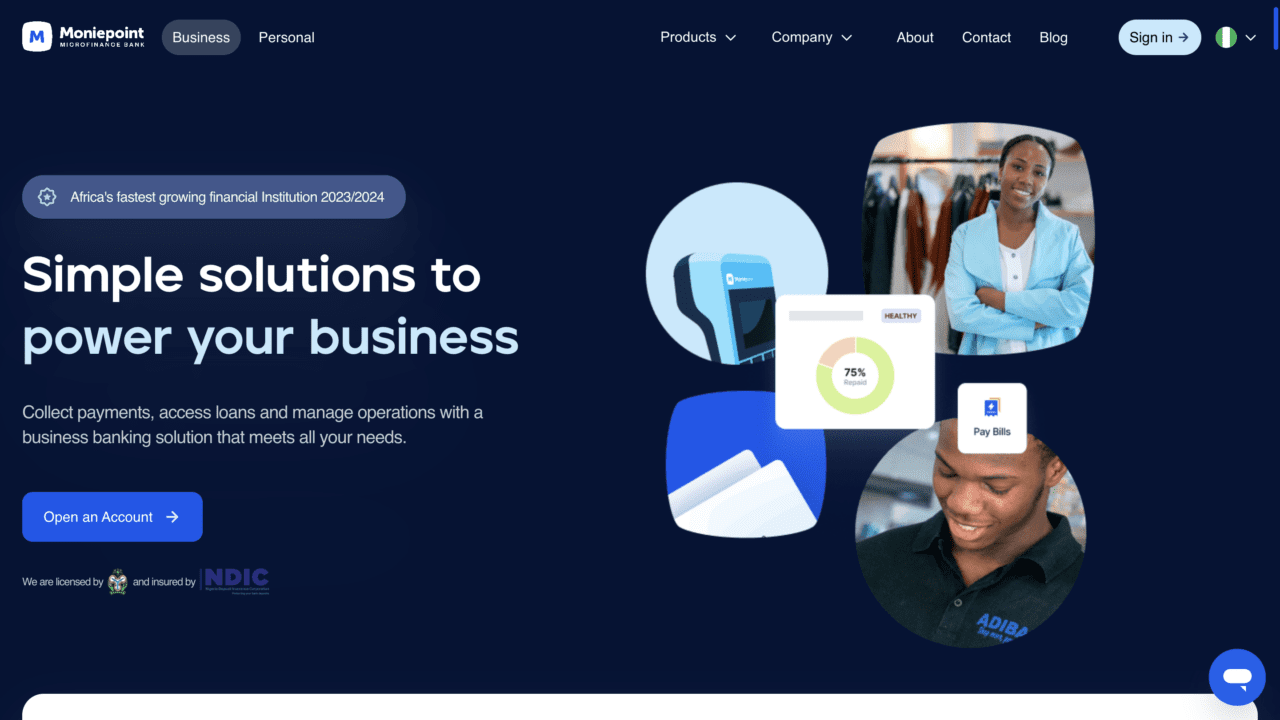

Africa’s newest fintech unicorn raises $110 million

African fintech Moniepoint is the continent’s latest fintech unicorn. The firm, Nigeria’s largest merchant acquirer, announced this week that it has raised $110 million in a funding round led by private equity firm Development Partners International (DPI). The round also featured participation from Google’s Africa Investment Fund, Verod Capital, and Lightrock. The infusion of capital boosts Moniepoint’s valuation above $1 billion, and is providing a positive light at a time when many fintechs in Africa are struggling to secure funding.

The funding takes Moniepoint’s total capital to more than $180 million.

Formerly known as TeamApt, the nine-year-old fintech will use the capital to accelerate the company’s growth across the continent. Moniepoint is building an all-in-one, seamlessly integrated platform for African businesses that features services including digital payments, banking, foreign exchange, credit, and business management tools. Speaking on behalf of DPI, Adefolarin Ogunsanya praised the company for its “combination of innovative technology, fast growth, and positive impact on the continent.”

CEO Tosin Eniolorunda co-founded the company in 2015. In the years since then, Moniepoint has grown into an all-in-one financial ecosystem that serves 10 million businesses and individuals. The company powers most of the point of sale transactions in Nigeria and, via its subsidiaries, processes $17 billion a month for its customers. Headquartered in London, Moniepoint maintains offices in Lagos, Nigeria; and Nairobi, Kenya, as well as in the U.S.

“This milestone validates the work we’ve put in for almost a decade,” the company noted in a post on its LinkedIn page. “And with this raise, we’ll be making financial happiness a reality for every African, everywhere. This is just Day One, and we’re excited for where this takes us.”

CB Insights also named Moniepoint to its 100 most promising startups roster for 2024. The Nigerian fintech is one of seven African startups to make this year’s list.

MTN Nigeria aims for higher quality mobile wallet users

There’s good news and bad news in the latest financial report from African telecommunications company MTN Nigeria. The bad news is that the company reported a significant after-tax loss of $312.7 million (₦514.9 billion), due largely to volatility in the currency market. MTN also noted that though active data users grew by more than 5% to 45.3 million, the company’s mobile money wallet business declined by more than 21%.

The good news? MTN’s fintech division grew revenues by 18%, with much of the gains coming from its mobile money service, MoMo. The decline in active mobile money wallets noted above was attributed in part to a shift in the company’s sales strategy to focus more on “high-quality wallet users” rather than just maximizing the number of users in general. MTN Nigeria also noted that its MoMo service has recently added functionality to support cross-border transactions.

“In the fintech business, we focused on executing our growth strategy, prioritizing increasing wallet quality, focusing on advanced services, and the MoMo PSB app to enhance the user experience and engagement,” MTN Nigeria CEO Karl Toriola explained. “We have introduced cross-border remittances with 13 fellow African countries to boost adoption and monetization. Taking advantage of their interoperability, we are now leveraging the existing network of agents and merchants … in the industry to bring our services closer to our customers.”

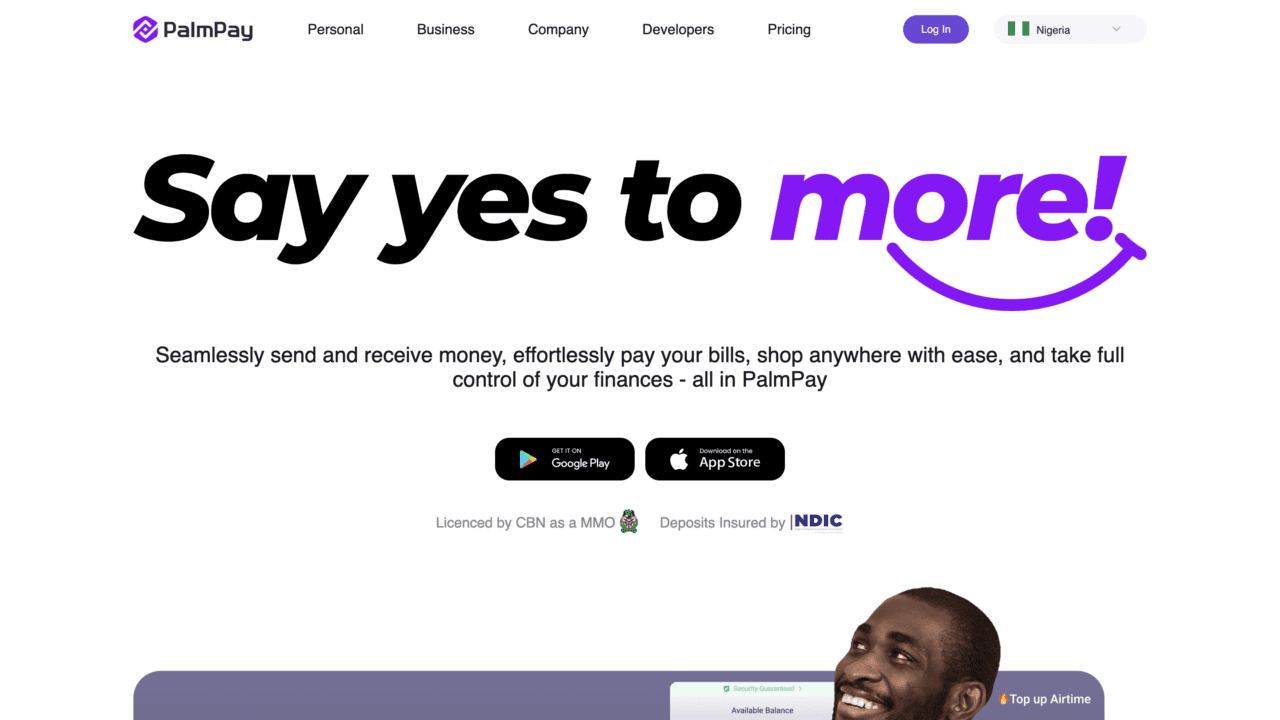

PalmPay wins recognition for financial inclusion

Lagos, Nigeria-based fintech platform PalmPay was recognized as the “Most Outstanding Fintech Driving Financial Inclusion” at the 2024 BrandCom Awards held late last month. Sponsored by Brand Communicator, the award acknowledges the fintech’s work in bridging financial gaps and promoting financial inclusion in Nigeria.

“At PalmPay, we believe financial inclusion is the foundation for economic empowerment, and we’re dedicated to ensuring that every Nigerian has access to secure, user-friendly, and reliable financial services,” PalmPay Head of Marketing and Communications, Hanson Femi said.

Founded in 2019, PalmPay has more than 35 million users. The company connects more than one million businesses via its mobile money agent and merchant network, and provides services ranging from instant transfers and billpay to its new USSD feature. This feature enables customers to perform a variety of banking transactions without needing internet connectivity by dialing *861# on their mobile phones.

“We aim to bridge the gap in digital access, and the introduction of our USSD service aligns with that mission,” PalmPay Managing Director for Nigeria, Chika Nwosu, said when the service was launched in September.

Here is our look at fintech innovation around the world.

Asia-Pacific

South Korean fintech unicorn, Viva Republica, which operates the mobile financial super app Toss, announced plans to debut in the U.S. market.

Singapore has established a “Global Finance & Technology Network” (GFTN) to support the region’s reputation as an international fintech hub.

Wise became the first non-bank operating in Japan to earn approval to join the country’s domestic payment network, Zegin.

Sub-Saharan Africa

Stanbic Bank Kenya, in partnership with Mastercard, has launched a pair of new credit cards designed to serve the institution’s affluent customers.

Nigeria-based fintech Moniepoint achieved unicorn status after raising $110 million in new funding.

Côte d’Ivoire-based investment platform Daba Finance won the Ecobank Fintech Challenge.

Central and Eastern Europe

Lithuanian identity verification and fraud prevention company iDenfy partnered with O2Factoring.

Erste Group teamed up with Neterium to help the firm bring its transaction screening solution to markets in Central and Eastern Europe.

Tech Times profiled Germany fintech billionaire and founder of Black Banx, Michael Gastauer.

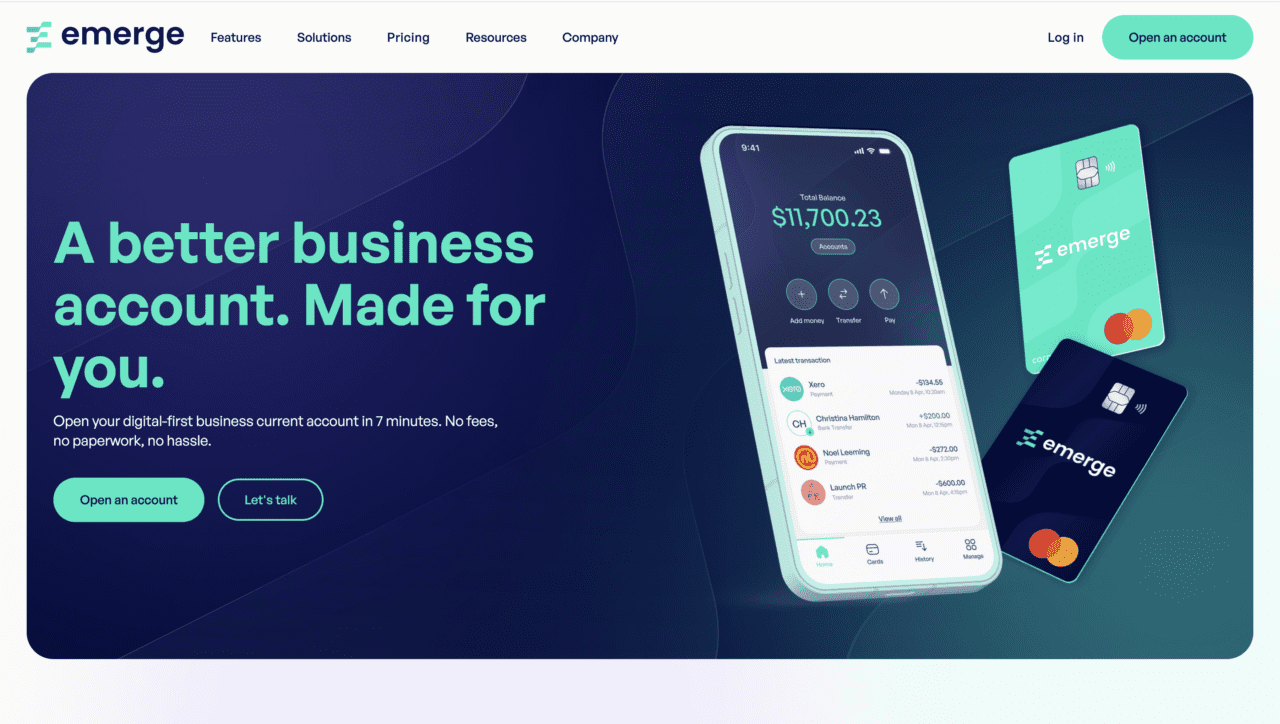

The round also featured participation from Icehouse Ventures, K1W1, NZ Fintech Fund, and Hard Yaka, a venture capital firm based in the U.S. Emerge will use the capital to support adding talent in marketing, sales, and product development. The company will also use the funds to accelerate its go-to-market strategy, including offering banking services to startups.

“Emerge was built to help Kiwi businesses do more, faster, better,” Emerge Co-founder Jovan Pavlicevic said. “In just a few minutes, you’ve opened as many Emerge accounts as you need, with features better than the banks, and team cards ready to go.”

A digital-first banking alternative, Emerge offers companies a single platform to manage their business finances. Emerge’s technology simplifies expense tracking, enables the creation of debit cards — including an unlimited number of virtual cards — and allows users to make and receive payments with a New Zealand business banking account backed by ANZ. Emerge provides bookkeeping and reporting tools and makes it easier for companies to track and manage their finances with a centralized view of their data. The company has also launched a service called EmergePay that converts a smartphone into a payment terminal.

Emerge evolved from a children’s financial literacy app called SquareOne that Pavlicevic and co-founder Jamie Jermain founded in 2020. Emerge was developed in January 2024, as the company shifted its focus toward providing banking services for SMEs, with the ultimate goal of becoming a neobank.

Headquartered in Auckland, Emerge was named to the Forbes Asia “Top 100 to Watch” in August.

FirstCape deploys wealthtech from InvestCloud

New Zealand’s largest wealth advice and asset management company, FirstCape, has partnered with InvestCloud to enhance the wealth management experience for advisors and clients alike. The deployment will help FirstCape increase the efficiency of its advisors, as well as provide a single platform for client engagement, experience, and advice at scale.

“We formed FirstCape with a stated intention of enhancing our client offering,” FirstCape CEO Malcolm Jackson said. “Integrating InvestCloud’s tools that streamline portfolio management and order execution is part of delivering on that promise. We continue to be focused on providing a complete suite of services tailored to every client’s unique needs at whatever stage of their investment life cycle.”

With more than 120 advisors and more than $30.3 billion (NZ $50 billion) in assets under management, FirstCape was forged earlier this year through the combination of four entities: JBWere NZ, Jarden Wealth, Harbour Asset Management, and BNZ Investment Services. The company has already deployed two InvestCloud solutions: Portfolio Manager and Order Capture. Portfolio Manager enables advisors to manage client portfolios with deeper insights that lead to tailored investment proposals. Order Capture provides a seamless interface for trading across asset classes, boosting operational efficiency by enabling advisors to act faster in response to client needs.

“We are thrilled to see the tangible success of our partnership with FirstCape as they embark on this modular digital transformation,” InvestCloud President of Digital Wealth International Christine Mar Ciriani said. “By leveraging our full suite of innovative front-office solutions, we are helping FirstCape create a robust digital backbone that will drive their growth, streamline advisor efficiency, and elevate client experiences.”

A global wealthtech company, InvestCloud serves wealth and asset managers, wirehouses, banks, RIAs, and insurers. InvestCloud’s clients represent more than 40% of the $132 trillion in total assets globally. A provider of digital wealth management and financial planning solutions since 2010, InvestCloud was named a CNBC “World’s Top Fintech Company” earlier this year. The firm is headquartered in West Hollywood, California.

International payments specialist Ebury arrives in New Zealand

Ebury, a specialist in international payments and collections, opened new offices in New Zealand this week. The move is designed to help the company provide a range of services to SMEs in the country, including cash management strategy and foreign exchange risk management.

“At Ebury, we embrace the complexity and risk of daily cross-border payments that enable business growth, in a way that traditional banks do not, or cannot,” Ebury Managing Director for APAC, Rick Roache said. “We make the sophisticated products and services that banks typically reserve for their biggest clients accessible to SMEs.”

The New Zealand office represents Ebury’s 40th office worldwide, and comes six years after Ebury expanded to neighboring Australia. The move to New Zealand also supports the company’s presence in nearby Shanghai and Shenzhen in China.

“Right now there are few options for SMEs looking for cross-border payment solutions and local advice in New Zealand,” Roache added, “so we’re really excited to bring our innovative technology platform into the market supported by a ‘boots on the ground’ team that differentiates us from other providers.”

Headquartered in London and founded in 2009 by a pair of Spanish engineers, Ebury serves primarily SMEs and mid-cap companies with payments, collections, and foreign exchange services in more than 130 currencies. Santander acquired a minority stake in the company for $459 million (£350 million) in 2020, and added to its stake two years later. With more than 1,700 employees across 25 countries, Ebury is reportedly preparing for an IPO in 2025 that would value the company at as much as $2.2 billion (£2 billion).

Here is our look at fintech innovation around the world.

Latin America and the Caribbean

Warburg Pincus acquired a minority stake in Brazilian accounting-based fintech Contabilizei for $125 million.

PXP Financial teamed up with Latin American payments platform Kushki.

Brazilian paytech Barte raised $8 million in Series A funding in a round led by AlleyCorp.

Asia-Pacific

Singapore-based finance platform for businesses, Aspire, secured in-principal approval for the Major Payment Institution license from the Monetary Authority of Singapore (MAS).

Bank of Hangzhou teamed up with Malaysia’s Maybank to support Chinese businesses as they expand operations in Southeast Asia.

Vietnamese private bank VPBank partnered with customer engagement platform CleverTap.

Sub-Saharan Africa

Somalia’s Premier Bank has teamed up with Mastercard and Tappy Technologies to launch Tap2Pay, a tokenized-passive payment wearable.

Fintech provider Flutterwave partnered with 9jahotel.com to launch a point-of-sale system to enhance hotel management in Nigeria.

Nigerian cryptocurrency exchange Yellow Card secured $33 million in Series C funding.

Central and Eastern Europe

Romanian payment service Pago secured $2.5 million (€2.3 million) to fuel expansion.

Budapest, Hungary-based B2B payment solutions provider, PastPay, raised $13 million (€12 million) in Series A funding.

Fingular, a neobank based in Singapore, launched a new digital lending business in Bangladesh.

TBC Bank Uzbekistan secured a $10 million line of credit from Switzerland’s responsAbility Investments AG. Read our Finovate Global interview with TBC Bank Uzbekistan’s Head of International Business Oliver Hughes.

This week’s edition of Finovate Global features news from the fintech scene in Hong Kong.

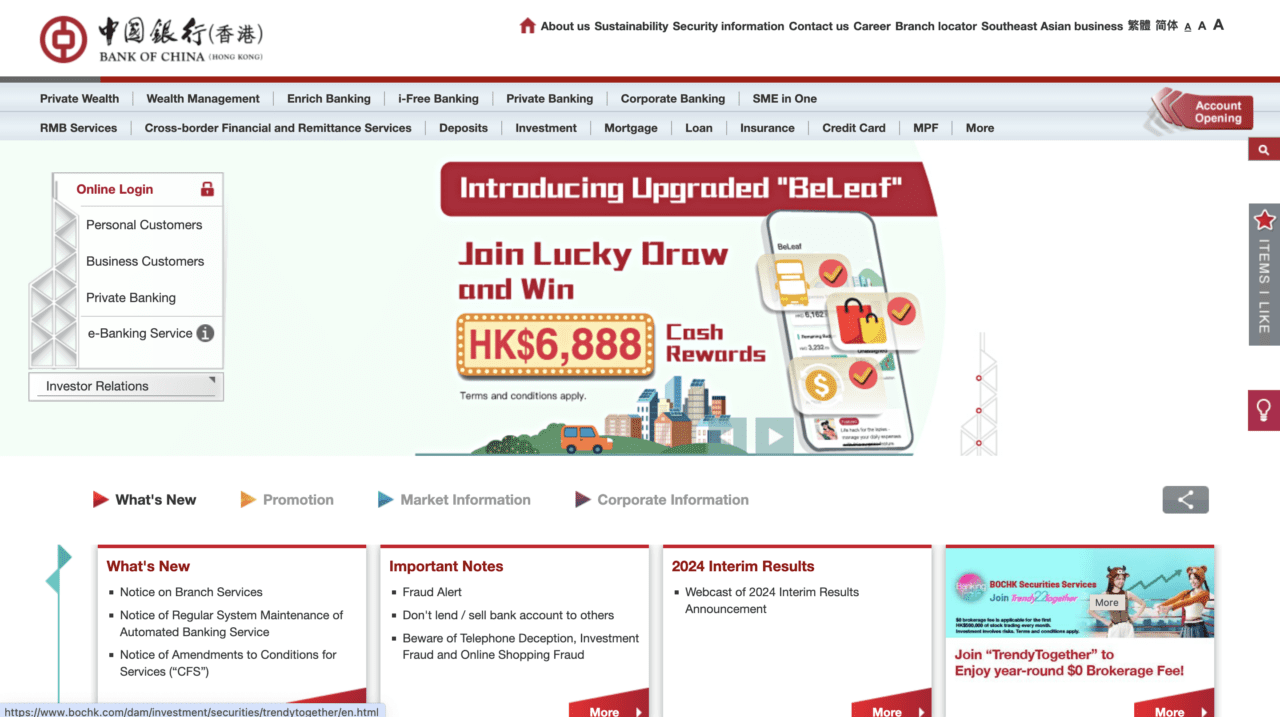

Worldline partners with BOCHK

International payment services company Worldline has forged a partnership with the Bank of China (Hong Kong), also known as BOCHK. The partnership makes the bank the first Hong Kong-based customer of Worldline’s open platform card solution, Paysuite Essential Edition. Previously called “Cardlite,” the solution will enable BOCHK to enhance the customer experience with new offerings, including its multi-currency Mastercard debit card.

“We are excited to partner with BOCHK, a prestigious bank in the region, to launch our new innovative Paysuite Essential Edition in Hong Kong,” Worldline’s Head of Financial Services Asia-Pacific, Noel Chow, said. “The partnership highlights the trust and confidence from leading financial institutions in our innovative open platform solutions. We believe the partnership paves the way for other banks to modernize their card systems and migrate from legacy systems to open systems.”

BOCHK’s partnership with Worldline reflects the trend in the payments industry toward open platform solutions. Already available in other markets, Worldline’s Paysuite Essential Edition offers issuing, acquiring, authorization, switching, and routing functionality. The technology supports Mastercard’s multi-currency card, and provides an infrastructure that accelerates time-to-market and deployment of new products and services.

Additionally, Worldline will provide a local support team with local expertise to assist BOCHK as it scales its operations in the future. This team will also help ensure the institution will meet Hong Kong banking industry compliance requirements.

“As open platform solutions are the future in digital payments, BOCHK is pleased to partner with Worldline, known for its comprehensive innovative fintech solution and unparalleled local support it offers, to provide our customers with the Mastercard multi-currency debit card powered by its Paysuite Essential Edition,” said Daniel Li, Chief Digital Officer of Personal Banking & Wealth Management, BOCHK. “This collaboration marks a significant step forward in our commitment to delivering seamless payment experiences to our valued customers and promote the wider use of digital payments.”

Worldline made its Finovate debut at FinovateEurope 2017. At the conference, the company demoed its Connected Piggy Bank, which helps parents provide financial education for their young children via a “playful” end-to-end savings solution. Today, Worldline processes more than 43 billion payment transactions a year, serves more than 14 million merchants, and is active in 170 countries. Founded in 1972, Worldline is headquartered in Bezons, France.

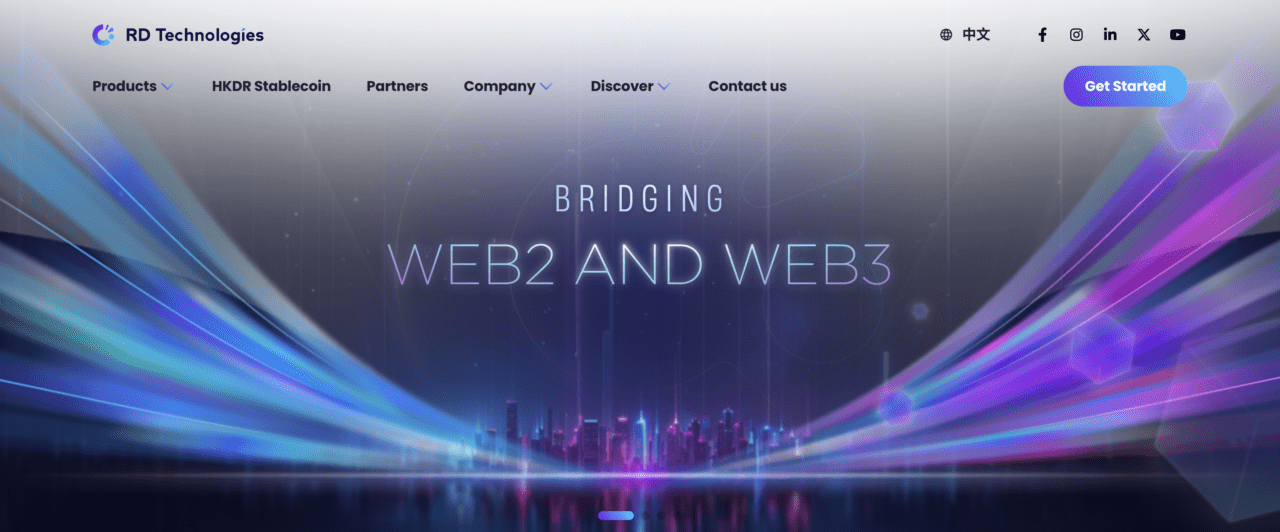

RD Technologies secures $7.8 million investment

RD Technologies, a Hong Kong-based financial platform that seeks to “bridge the worlds of Web2 and Web3,” has raised $7.8 million in Series A1 financing. Participating in the round were HongShan, Hivemind Capital, Aptos Labs, Hash Global, SNZ Capital, Solana Foundation, Anagram, and Upward Capital. The company will use the funds to further build out its financial platform and help encourage the development of the Web3 ecosystem in Hong Kong.

“The legacy payment industry is ripe to be disrupted using blockchain technology and stablecoins to provide more efficient and cheaper cross-border payment networks,” RD Technologies CEO Rita Liu said. “Hong Kong is leading the world in virtual asset regulation. We are confident that compliant and transparent stablecoins will invigorate the market and address the pain points of traditional payments and finance to bring in institutions and help Hong Kong become a global Web3 hub.”

Founded in 2020, RD Technologies offers two primary solutions via its subsidiaries: the RD Wallet and the HKDR stablecoin (HKDR). RD Wallet is a licensed Stored Value Facility that enables businesses around the world to open multi-currency fiat accounts via mobile device anywhere and at any time. The wallet supports eight currencies — HKD, CNY, USD, JPY, SGD, EUR, GBP, and AUD — that are commonly used in the region, offers fund transfer via TT and CHATS, and provides competitive FX rates with a 0% fee.

Issued by RD InnoTech Limited, the HKDR stablecoin is backed 1:1 by the Hong Kong dollar, with high-quality, liquid assets kept in segregated custody accounts with licensed financial institutions. In July, the firm was one of the first companies to be admitted to the stablecoin issuer sandbox by the Hong Kong Monetary Authority.

“Hivemind is thrilled to support RD Technologies as they seek to lead the future of stablecoins and cross-border payments,” Hivemind Partner and Head of Asia Stanley Huo said. “We believe regulated stablecoins are a critical growth area in crypto, offering real product-market fit, particularly as global demand for regulated stablecoins rises among enterprises and institutions.”

Checkout.com launches Octopus in Hong Kong

London-based Checkout.com is the first international payment services provider (PSP) to offerOctopus, the leading payment method in Hong Kong, as a payment option at checkout.

With 98% penetration in a region with 7.5 million residents, Octopus is Hong Kong’s first, “homegrown” fintech. Octopus was launched in 1997 as a contactless card for multimodal transportation. In the years since, the solution has grown into a popular and versatile payment system, used for retail and shopping as well as food and beverage transactions both in Hong Kong and abroad. The company introduced its mobile app in 2012 and now reports that there are more than 4.5 million Octopus digital wallets.

“At Octopus, we pride ourselves (on) making everyday life easier,” Octopus Head of Business Development and International Business Edwin Lai said. “This partnership with Checkout.com will enhance and broaden the payment experience not just for our customers, but also merchants within Hong Kong and beyond. We anticipate robust demand from global and local businesses eager to access Hong Kong’s consumers. We hope this collaboration will help support the growth of the city’s digital commerce.”

“Catering to local payment preferences is crucial for success in the Hong Kong market,” Checkout.com General Manager of APAC Brian Sze said. “Our strategic partnership with Octopus underscores Checkout.com’s commitment to investing in our Asia footprint, delivering localized payment solutions that empower merchants to thrive in this dynamic region.”

Founded in 2012, Checkout.com processes payments for thousands of companies around the world. The company’s international digital payments network supports more than 145 currencies, and processes billions of transactions a year. Checkout.com’s technology helps merchants increase acceptance rates, lower processing costs, fight fraud, and transform payments into a significant source of revenues. The company has raised $1.8 billion in funding, most recently closing a $1 billion Series D round in January 2022. Guillaume Pousaz is founder and CEO.

Hong Kong’s fintech celebration only weeks away

Some of the biggest fintech news in Hong Kong is likely less than three weeks away. Hong Kong Fintech Week begins on October 28 and extends through November 1. The event expects to host 30,000 participants and feature 800 speakers and 500 startups. Finovate participated in the city’s Fintech Week back in 2018 as part of FinovateAsia.

We’ll have more to say about fintech in Hong Kong in the wake of the city’s conference. For now, check out this interview with Lareina Wang, who was appointed chair of the FinTech Association of Hong Kong (FTAHK) in August. In this interview, Wang — who is also executive director, head of digital and innovation at DBS Bank Hong Kong — talks about some of the major issues facing both the growth of the association as well as fintechs in Hong Kong.

“We have some of the world’s best universities in town, while, overall, the fintech industry is short of fintech talent,” Wang told FinanceAsia. “Advocating for policies and reaching collaborations might not appeal to them, but they are interested in being educated around fintech topics.”

Founded in 2017, the FTAHK has 300 corporate members.

Here is our look at fintech innovation around the world.

Central and Southern Asia

86400, a payments technology firm based in India and formerly known as Mobileware Technologies, raised $1.8 million (INR 15.6 crore).

The New South Wales (NSW) government teamed up with Indian incubator Afthonia Labs to help NSW fintech startups enter the Indian market.

An industry organization consisting of fintech lenders, Fintech Association for Consumer Empowerment (FACE), secured “self-regulatory organization” status from the Reserve Bank of India.

Latin America and the Caribbean

Brazilian paytech Barte raised $8 million in Series A funding in a round led by AlleyCorp.

Norway’s MeaWallet partnered with Peru-based neobank B89.

Grupo Bancolombia’s crypto platform, Wenia, launched its WeniaCard that lets users pay with cryptocurrency at any merchant that accepts Mastercard.

Asia-Pacific

Singapore-based fintech Surfin announced a $12.5 million Series A investment from Insignia Ventures Partners.

JCB enabled Google Pay for customers in Japan starting on September 6.

Checkout.com added Octopus as a payment method in Hong Kong.

Sub-Saharan Africa

Mastercard and ACI Worldwideteamed up to bring real-time card payments to South Africa.

Network International went live with new payments services in Kenya.

Nigerian’s Securities and Exchange Commission (SEC) announced a crackdown on fraud in the country’s fintech industry.

Central and Eastern Europe

INDEXO Bank partnered withMambu as part of its launch in Latvia.

Austrian payment orchestration platform IXOPAY introduced new CTO Ronnie Thomson.

Croatia-based fintech Fonoa acquired PwC UK’s GITC product to faciliate management of partial tax exemptions.

Middle East and Northern Africa

Calcalist interviewed former CEO of Bank Leumi and current Managing Partner at Team8 Rakefet Russak-Aminoach on the current state of fintech in Israel.

The UAE announced that cryptocurrency transactions will be exempt from value-added tax (VAT) effective November 15.

American Express Middle East forged a partnership with Dubai-based payment gateway Telr.

This week’s edition of Finovate Global features recent fintech news and headlines from the Netherlands.

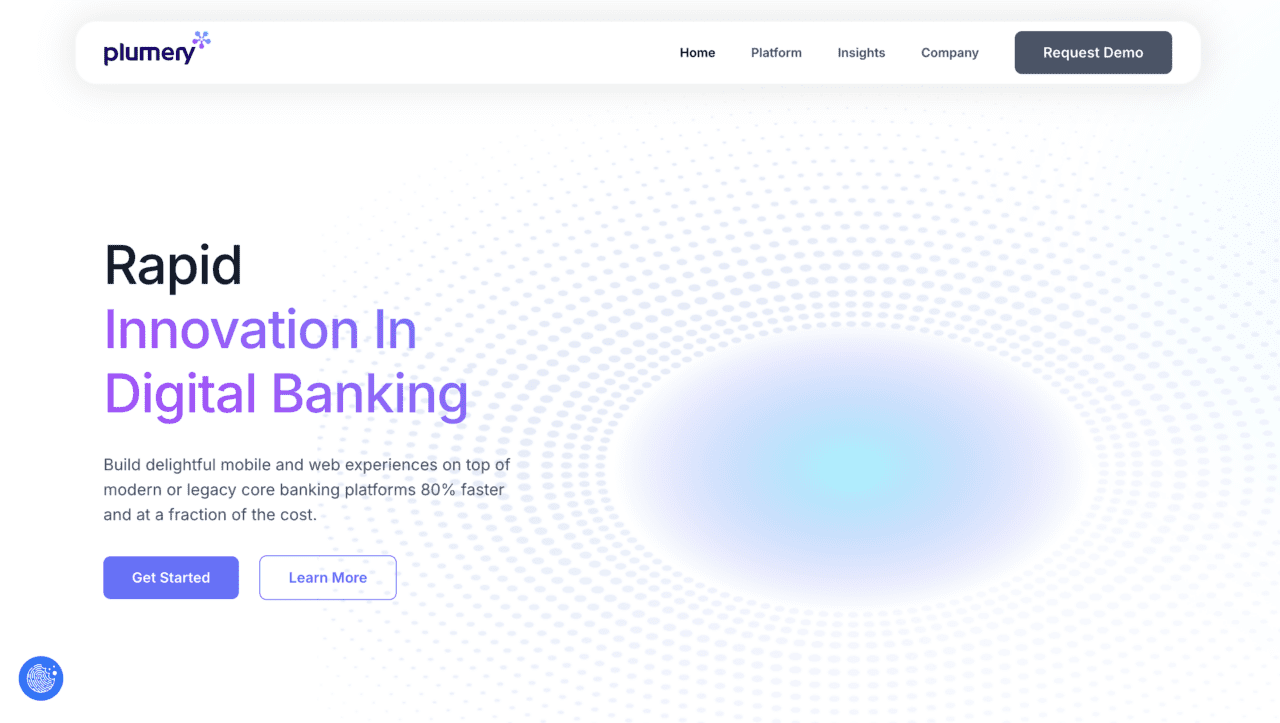

Netherlands-based digital banking platform Plumerysecured $3.3 million in funding this week. The investment came from of early-stage investor DN Capital and Fontes, managed by international VC firm QED Investors, and raises the company’s total funding to date to $7.8 million. Plumery added that it is preparing for a larger Series A round next year.

“Our commitment to product excellence and expansion into key markets (are) central to our roadmap, and this funding will propel us even further,” Plumery Founder and CEO Ben Goldin said. “We look forward to working with our partners in this next phase of our evolution and sustained growth in today’s competitive market.”

Plumery will put its new capital to work in a variety of ways. The company plans to expand its sales and marketing efforts, bolster international partner management, and enhance its platform’s capabilities for SMEs, consumers, lenders, and microfinance companies. Plumery will also look to add talent, particularly in product, engineering, and commercial roles.

Founded in 2022, Plumery offers a digital banking platform that enables businesses to rapidly customize and deploy their banking operations. The firm’s platform enables mobile and online banking interfaces and experiences to be built on top of legacy core platforms at a lower cost and at up to 80% faster than traditional methods. In its funding statement, the company noted that it plans to launch additional features including conversational banking and AI-driven automation and insights as part of its expansion plans.

It’s hard to imagine a Finovate Global look at fintech in the Netherlands that didn’t include a nod to Engagement Banking Platform Backbase. Especially upon hearing news that the company has moved to new headquarters in Amsterdam.

This week, Backbase celebrated the grand opening of its 5,000 square-meter, international headquarters at Oosterdoksstraat 114. Backbase CEO and Founder Jouk Pleiter said in a statement that the new HQ was “more than just a building,” noting that “it represents the outcome of a 20-year journey fueled by entrepreneurship, perseverance, and focus on innovation and customer success — all driven by our people.”

And at a time when many companies are struggling to encourage workers to spend more time in the office, it is hard not to be touched by the comments of Carolien Roos, partner at Firm Architects and designer of Backbase’s new headquarters. “Our vision was to create a space that not only inspires innovation but also brings people together,” Roos said. “The design encourages the kind of serendipitous encounters and discussions that often lead to groundbreaking ideas — a key ingredient in Backbase’s recipe for success.”

Backbase has been putting that recipe to good use of late. Also this week, the company announced that it was teaming up with business identity platform, and fellow Finovate alum, Middesk to enhance KYB verification for both banks and credit unions. Backbase’s Engagement Banking Platform, integrated with Middesk, will give financial institutions access to real-time verification data sourced from multiple databases including the offices of all fifty Secretaries of State, the IRS, the USPS, OFAC, and more.

“Businesses today want a seamless verification process that meets compliance standards while limiting delays during the onboarding process,” Backbase VP of Product Robert Soetens said. “Together with Middesk, Backbase is continuing to implement modern, flexible, scalable, and API-first solutions (for) banks and credit unions, helping them deliver the best-in-class digital experiences to their business clients.”

Headquartered in San Francisco and founded in 2019, Middesk made its Finovate debut at FinovateFall 2022. At the conference, the company demoed its Verification solution that provides a complete and accurate view of customers — from entity names to watchlist screening. Middesk counts Affirm, Brex, and fellow Finovate alums Plaid and Gusto among its customers. Kyle Mack is CEO and Co-Founder.

In addition to forging new partnerships, Backbase launched its Intelligence Fabric Layer last week. The new offering is a set of data/AI infrastructure and development capabilities that embed natively in the Enterprise Banking Platform. These capabilities, which include Agentic AI, help banks realize “significant productivity gains” in both customer servicing and sales. The Intelligence Fabric leverages Backbase’s Grand Central Integration Platform-as-a-Service, which unifies data from multiple sources, including core banking systems, payment gateways, fintechs, and non-fintech systems such as CRMs.

“We see a future where AI Agents will work autonomously in the background, handling tasks, managing processes, and collaborating with customers and employees,” Pleiter said. “The adoption and evolution of these new-gen, super-powerful agents will dramatically reduce internal and external labor spend on overheads such as sales, marketing, customer service, and compliance operations.”

A Finovate alum since 2009, Backbase most recently demoed its technology at FinovateFall in 2021. The four-time Finovate Best of Show winner was founded in 2003 and counts more than 150 financial institutions around the world as users of its Engagement Banking Platform.

For more on Agentic AI, check out our primer from Senior Research Analyst Julie Muhn.

Finovate has been happy to introduce our audiences to a number of fintech innovators based in the Netherlands over the last decade-plus. Check out this roster of Dutch fintechs that have demoed their innovations on the Finovate stage.

Indian neobank Jupiter is reportedly in talks to acquire a stake in SBM Bank India, according to TechCrunch.

Latin America and the Caribbean

Binance secured Virtual Asset Service Provider (VASP) license to operate in Argentina.

Trinidad and Tobago inked an agreement with NPCI International Payments to build a real-time payments system based on India’s UPI.

Paysendpartnered with Mastercard to launch Paysend Libre in Mexico to promote financial inclusion.

Asia-Pacific

Malaysia’s Maybank partnered with China’s Bank of Hangzhou to enhance cross-border financing and innovation in AI.

Worldline teamed up with Bank of China Hong Kong to launch an open platform card solution for customers in Hong Kong.

A coalition of banks and other financial institutions in Malaysia have launched a new, integrated platform, the National Fraud Portal (NFP), to fortify the capabilities of the country’s National Scam Response Centre (NSRC).

Sub-Saharan Africa

Kazang Pay launched its card acceptance solution for merchants in Zambia.

African payment infrastructure company Fincra secured a Third Party Payment Provider (TPPP) license in South Africa.

This week’s edition of Finovate Global looks at recent developments in the fintech scene in Canada.

First up, we head over to Toronto, Ontario, where embedded payroll software company Nmbrhas secured $5.6 million (CAD$7.6 million) in seed funding. The round featured investors Panache Ventures, Golden Ventures, Motivate Venture Capital, and Luge Capital. In a statement, the company indicated it will use the funding to fuel growth and accelerate product development. And while focused presently on the Canadian market, Nmbr believes the investment will enable the firm to explore expansion opportunities in other countries.

“We’re incredibly grateful for our investors’ support and their confidence in our mission to empower businesses across the country with embedded payroll solutions,” Nmbr Co-Founder and CEO Simon Bourgeois said. “With these integrated systems already gaining traction in the U.S., we’re excited to extend these proven strategies to Canada.”

Founded in 2023, Nmbr simplifies complex financial products like payroll. The company’s technology enables businesses to embed Canadian payroll within their offering in days or weeks, rather than in years as is often the case with traditional payroll systems. Companies partnering with Nmbr have added payroll alongside operations such as AP/AR automation, employee scheduling, e-commerce, employee benefits management, and more. In addition to its funding announcement, Nmbr also reported that RBCx, the technology and innovation arm of Royal Bank of Canada, will serve as the company’s banking partner.

Staying in Ontario, but traveling 300 or so miles east, takes us to Ottawa and the home of Salt Edge, an open banking solution provider for banks, lenders, and other fintechs. This week, the Canadian fintech announced that it is helping Multitude Bank enhance its loan repayment processes to enable instant loan repayments.

“Salt Edge’s solution stood out due to its flexibility, competitive pricing, extensive coverage, and readiness to adapt to Multitude’s specific needs,” Multitude Bank CBO and Deputy CEO Dario Azzopardi said. “These factors were pivotal in choosing Salt Edge as a partner in this initiative.”

A core subsidiary of the Multitude Group, Multitude Bank will leverage Salt Edge’s technology, specifically using open banking method Pay-by-Link to provide customers with timely notifications about upcoming installments. The bank will use Salt Edge’s Payment Initiation solution to enable its customers to make instant loan repayments instead of relying on traditional online banking methods. The new process reduces transaction costs and connects bank clients with more than 2,300 banks across Europe.

“Open banking offers flexibility, and we’re happy to assist Multitude in supporting its clients with a safe and faster payment solution powered by open banking,” Salt Edge VP of Sales Erica Virlan said.

Salt Edge’s partnership with Multitude Bank comes just days after Moldova-based Victoriabank announced it was teaming up with Salt Edge to help ensure compliance with impending national legislation that will transpose European 2nd Payment Services Directive (PSD2) into Moldovan law. Also this month, the Canadian company forged new partnerships with international financial services company Ebury and Moldova’s Comertbank.

Salt Edge made its Finovate debut at FinovateEurope 2018 in London. The company offers an Open Banking Gateway that enables financial institutions to secure instant access to accounts in 5,000 banks across Europe, GCC, APAC, and the Americas for account information and payment initiation. Salt Edge also offers an Open Banking and Compliance Solution that helps banks and Electronic Money Institutions (EMIs) become compliant with PSD2 and open banking requirements.

Canada has a well-deserved reputation as a welcoming country. As of 2023, with more than eight million immigrants earning permanent residence status in Canada, immigrants currently make up approximately a fifth of the country’s population.

With this in mind, it is heartening to read news that Scotiabank has expanded its partnership with Canadian cross-border credit bureau Nova Credit. The two entities will work together to help newcomers from countries including Australia, India, Kenya, Mexico, and Nigeria to leverage their credit history from their home country to help them access higher credit limits when applying online for financing in Canada.

“Canada relies heavily on the success of our immigrant population and the contributions they make to our economy,” Scotiabank SVP for Retail Customers, Tanya Eisener said. “In an increasingly digital world, a person’s history doesn’t have to start over when they move to a new country. Being able to access their foreign credit report through Nova Credit’s credit service allows us to get a better understanding of their credit risk and ultimately help them settle in Canada faster.”

The expanded partnership between Scotiabank and Nova Credit is designed to tackle the challenge of “credit invisibility” or the absence of a credit record. In Canada, based on data from 2015 through 2019, more than 25% of those considered “credit invisible” were immigrants. Further, more recent immigrants, those who had been in the country for less than two years, were nearly twice as likely to be credit invisible compared to native-born Canadians.

Scotiabank is a multinational banking and financial services company based in Toronto, Ontario. The bank offers a range of services including personal and commercial banking, wealth management, private banking, corporate and investment banking, and capital markets. The institution has more than 90,000 employees and assets of more than $1.3 trillion as of April 2023.

Headquartered in San Francisco, California, Nova Credit is a consumer-permissioned credit bureau that specializes in helping businesses make informed decisions on thin-file, no-credit history, and new-to-country credit applicants. Founded in 2016, Nova Credit expanded to Canada in 2023 as part of its initial partnership with Scotiabank.

Here is our look at fintech innovation around the world.

A partnership between Mastercard and ZOOD will bring virtual Buy Now, Pay Later cards for consumers in Uzbekistan. Read more about fintech in Uzbekistan in our Finovate Global interview with Oliver Hughes of TBC Uzbekistan.

Latin America and the Caribbean

Uruguayan cross-border payment platform dLocal teamed up with Asia-based mobile wallet ShopeePay.

Proclaiming itself the first digital bank dedicated to customers with disabilities, Brazil’s Parabank partnered with Dock to launch a new suite of credit and prepaid cards.

Payments innovator NETSTARS teamed up with ACI Worldwide to boost development of cashless payments in Japan.

Singapore-based Bybit introduced new Shariah-compliant cryptocurrency accounts for Muslim investors.

HSBC launched new financing plan for SMEs in Hong Kong.

Sub-Saharan Africa

Africa-focused investment firm Helios Investment Partners led a $100 million Series D funding round in Banking-as-a-Service (BaaS) and infrastructure API provider M2P Fintech.

Coming to America! African paytech Flutterwave has expanded its Send App remittance service to 49 states in the U.S. courtesy of a partnership with MainStreet Bank.

PayZeep, a Nigerian fintech startup, partnered with the Amalgamated Union of App-based Transporters of Nigeria (AUATON) to bring new payment options to drivers.

This week, we turn to Uzbekistan, a Central Asian nation and former Soviet republic with a population of just over 37 million. The doubly-landlocked country (one of only two in the world) has been transitioning toward a market economy for years and has been credited by the Brookings Institution for its high economic growth and low public debt. A major producer and exporter of cotton, Uzbekistan has leveraged major natural gas supplies to be one of the largest electricity producers in the region. HSBC has predicted that the country will have one of the fastest-growing economies in the next few decades.

We interviewed Oliver Hughes, former CEO of Tinkoff and current Head of International Business for TBC Bank Group – which recently expanded to Uzbekistan. In our extended conversation, we discussed TBC’s goals in Uzbekistan, nature of banking in Central Asia, what key financial services are in the most demand, as well as how enabling technologies are helping financial institutions in the region better serve their customers.

You joined TBC a few years after the bank expanded to Uzbekistan. First, what drew you to TBC?

Oliver Hughes: Joining TBC in Uzbekistan was a great opportunity for two reasons. First, the market itself is full of potential and ripe for disruption. A young, growing population of 37 million people, of which 59% are under the age of 30, economic reforms and liberalization, a favorable macroeconomic environment and an under-penetrated digital banking market create huge demand for world-class online banking services, so I could see a clear path to success.

Second, I knew that TBC Uzbekistan would be a great place to work and an environment that would allow me to make an impact. Since coming to Uzbekistan in 2019, TBC has built a world-class team, secured a banking license, reached profitability within two years, and outlined a vision that aligns with my previous experience of building and scaling a best-in-class, profitable digital banking ecosystem.

Uzbekistan was TBC’s first international market outside of its native Georgia. Why Uzbekistan?

Hughes: Uzbekistan is a hidden gem, previously largely overlooked by the international investment community, but slowly getting on the radar of investors and fintech heavyweights. It is Central Asia’s largest country by population, which is young and getting younger each year. This supports demand for modern digital financial services. The country has also embarked on a large-scale program of economic reform and liberalization, empowering the private sector and starting to attract more international investment.

TBC Uzbekistan is part of London-listed TBC Bank Group and we are proud to play our part in attracting major global investors to the country. Through TBC, large global investment funds like Fidelity, JPMorgan Asset Management, Schroder, BlackRock and Vanguard have been investing in Uzbekistan, and more investors are coming in every month.

The macroeconomic picture is strong, with GDP expanding at an average annual rate of around 6% for the past decade and forecast to almost double to $160 billion between 2023 and 2030.

In addition, Uzbekistan has a deep tech talent base. It’s both because of its highly educated domestic workforce – a product of a strong education system, and also because Uzbekistan is benefiting from an influx of returning expats and a broad range of international tech specialists from neighboring countries.

What does the financial services ecosystem look like in Uzbekistan? What is the level of interest in fintech innovation there?

Hughes: The financial services sector is still largely dominated by major state banks, which command around 70% of the market. However, competition is increasing as the government continues its drive for privatization and other reforms. A recent example of this was with Hungary’s OTP, which in June 2023 became the first international player to participate in the privatization of the Uzbek banking sector, acquiring former state-owned Ipoteka Bank. And recently, Kaspi announced its intention to participate in the privatization of Humo, Uzbekistan’s second largest open-loop domestic payment system.

TBC Uzbekistan is part of London-listed TBC Bank Group PLC, which also operates Georgia’s leading tech-enabled commercial bank. Despite being part of a multinational group, we consider ourselves to be a local player because we operate as a standalone company in Uzbekistan with a separate tech stack and separate team purpose-built for this country.

In terms of the ecosystem as a whole, it is a mix of state banks, international operators, and local Uzbek players, as well as a developing fintech scene covering everything from payments to crypto.

The level of innovation in the local fintech market is very advanced, thanks to open banking. The key development, which has not yet been replicated in developed markets, is the full banking interoperability that open banking enables in Uzbekistan. In practice, it allows customers to seamlessly interact with multiple financial institutions.

For instance, when a customer of one bank opens an account with another institution, the new bank gains visibility into the customer’s transaction history and account balances from their original bank, while the new bank is also able to initiate fund transfers or debit transactions from the customer’s account at the original institution. This helped TBC enter the market in 2019 via the acquisition of the leading P2P payments app Payme to quickly achieve profitable growth and access to a huge customer base.

Let’s talk a little more specifically about TBC Uzbekistan. How is it structured? What is its mission?

Hughes: Our mission is simple – to make people’s lives easier. As I described earlier, the financial services sector has been and is still to some extent dominated by state institutions that operate in a traditional fashion. We see that there is demand for modern, digital banks that provide a great, convenient user experience and that is what we are building.

At present, there are three components to TBC Uzbekistan: TBC Bank Uzbekistan (TBC UZ), a mobile-only bank; Payme, a digital payments app for individuals and small businesses; and Payme nasiya (Payme instalments), an installment credit business. London-listed TBC Group owns 100% of both Payme and Payme nasiya and is the major shareholder of TBC UZ, with a 60% stake. The other 40% stake in TBC UZ is split between two institutional investors: the European Bank for Reconstruction and Development (EBRD) and the International Finance Corporation (IFC), part of the World Bank Group.

What are some of the biggest areas of opportunity in your opinion?

Hughes: We see some really exciting opportunities in Uzbekistan. At present, we are focused on consumers and specifically consumer lending. Despite over 45 million cards in circulation across the country, product offerings remain limited and retail lending is especially underdeveloped, representing just 12% of GDP.

Demand from consumers for financial services is already significant and continuing to grow, with point-of-sale (POS) digital payment volumes tripling to over $22 billion in the three years ending in 2023, with the number of POS terminals and bank cards in circulation doubling over the same time period.

There are interesting opportunities in other areas as well, including a new, product-rich debit card, financial services for SMEs, insurance and brokerage, with the latter two being at a fairly nascent stage of development in Uzbekistan. So, we plan to leverage those as well in the future.

TBC Uzbekistan recently raised a significant amount of capital. How will the new funding help the bank?

Hughes: Our business in Uzbekistan is scaling rapidly, but there is still significant potential for further growth, including through diversifying our offering to address market demand. The recent funding is being used to increase our loan book — which we are currently doubling year-on-year — advance financial inclusion, and accelerate our progress in launching new product lines.

In addition to powering our growth, new funds help us to continue to diversify our funding base.

What are some things about Uzbekistan that those of us on the outside may be surprised to learn?

Hughes: Uzbekistan is a country that largely exists outside the mainstream consciousness in the West. Some people might have their preconceptions, and would be surprised to learn about the advanced state of open banking in the country. Building on that, the level of innovation in financial services is pretty impressive in Uzbekistan. The fintech sector is thriving and strongly supported by the government and the wider ecosystem that is fueled by local and international tech talent.

In terms of other things that may surprise you about Uzbekistan, it’s the food scene. The food here is incredible, so I urge everyone to come over and try it!

There is a lot of talk about enabling technologies such as AI. Are any of these major areas of innovation in Uzbekistan’s fintech scene?

Hughes: Artificial Intelligence is a key innovation area and one that I am proud to say that TBC is leading among peers by integrating AI into our services.

Our plans are ambitious. We are building an AI Virtual Assistant that takes customer service to the next level. The most common customer service solution right now is chatbots, but we’re skipping that stage and going straight to an interactive voice assistant. What’s more, we’re enabling functionality in the Uzbek language and, in the future, in other local languages such as Tajik and Karakalpak, which tend to get overlooked by major tech giants.

We ultimately envision this Virtual Assistant being able to guide our users across all of our product offerings within TBC Uzbekistan, including the ones we plan to launch in the future, such as insurance, brokerage, travel and ticketing.

How do you see TBC Uzbekistan growing over the next two-to-three years?

Hughes: Since launching in 2019, TBC Uzbekistan has scaled significantly and established itself as a leading player in the market. As disclosed in our recent half-year results, we have grown our user base to 16 million unique registered users and achieved an operating profit of $61 million, up 87% year-on-year, with TBC Uzbekistan accounting for 7% of total profit for the group, as well as 13% of revenue and 44% of consumer loans on the group level. This is a very significant contribution, which is set to expand further.

We plan to continue to grow rapidly over the next 2-3 years, launching new product lines and gaining an increased percentage of market share. This is reflected in the guidance we have issued to the market: a net profit for TBC Uzbekistan of $75 million for the full year of 2025, with 30% of the Group’s loan book coming from TBC’s operations in Uzbekistan.

Where might TBC expand next? Are there any areas of special interest?

Hughes: We’re not yet at the stage where we can point to a specific market. However, I can tell you the types of markets we are considering. Our attention is on emerging markets with a population of around 30 to 70 million people, scope for growth and other favorable characteristics. For now, we still have a lot of exciting things to do in Uzbekistan.

Here is our look at fintech headlines around the world.

Sub-Saharan Africa

South African fintech Happy Pay locked in $1.8 million in pre-seed funding in a round co-led by E4E Africa and 4Di Capital.

Ghanaian crypto platform, Mybitstore, went live in Nigeria this week.

Nigerian fraud detection company Regfyl raised $1.1 million in funding.

Central and Eastern Europe

Germany’s Commerzbank partnered with Deutsche Börse subsidiary, Crypto Finance.

Instanbul, Turkey-based fintech Colenda AI launched new AI solution to help financial institutions enhance decision-making and boost loan performance.

Bulgaria-based Paynetics teamed up with tell.money to launch its Confirmation of Payee (CoP) service.

Middle East and Northern Africa

UAE-based B2B payments platform Xpence teamed up with Egypt-based Paymob to enhance digital payments in the region.

Egyptian fintech SETTLE raised $2 million in pre-seed funding.

Mesh integrated with digital asset trading platform CoinMENA FZE to enhance crypto transfers and account management for customers in the MENA region.

Central and Southern Asia

India-based insurtech Onsurity raised $21 million to power expansion plans.

ZaakPay, the payment gateway arm of India’s MobiKwik, partnered with Meta to provide an embedded payment option via WhatsApp.

Indian financial services platform Kaleidofin secured $13.8 million in funding.

Latin America and the Caribbean

Uruguay-based MercadoLibre secured $250 million in financing from JPMorgan.

JMM Group and Liberty Latin America launched microlending service MYNE Lend for Jamaican customers.

dLocal, a cross-border payments platform based in Uruguay, forged a partnership with MoneyGram.

Asia-Pacific

Vietnam Maritime Commercial Joint Stock Bank (MSB) teamed up with TerraPay.

Paysend launched instant cross-border payouts to China UnionPay cards for enterprise customers.

This week’s edition of Finovate Globalfeatures an in-depth interview with Nacho Díaz de Argandoña, Chief Product Officer with Spain-based fintech, GPTAdvisor.

Founded in 2023 and headquartered in Madrid, GPTadvisor made its Finovate debut earlier this year at FinovateEurope 2024 in London. GPTadvisor offers a Gen AI platform that is specifically built to boost the productivity of financial advisors and wealth managers, as well as enhance client engagement.

This year, GPTadvisor announced that it has successfully completed a capital expansion round that featured support from two major Spanish venture capital firms, Kfund and JME Ventures. The company also announced that has launched a version of its GPTadvisor solution in the GPT Store by OpenAI. This launch made GPTadvisor the first portfolio management app available in the OpenAi store.

We caught up with Nacho to talk about current trends in wealth management and what AI can bring to the industry.

What problem does GPTadvisor solve and who does it solve it for?

Nacho Díaz de Argandoña: GPTadvisor addresses a critical challenge in the wealth management sector: the need for increased efficiency and productivity to remain competitive in an increasingly complex financial landscape. Financial advisors often face time-consuming, repetitive tasks such as investment research, portfolio management, and compliance. These tasks can detract from their prime objective, which is increasingly harder to accomplish: to nurture strong relationships with their clients and provide them with truly personalized and strategic advice.

GPTadvisor solves this context by providing advanced AI-driven tools that automate and streamline many of these processes, in a secure, private and controlled environment. Our wealth management platform uses the latest generative AI technology to assist financial advisors in quickly finding the right investment product, analyzing and comparing portfolios, elaborating comprehensible narratives to excel in client engagements and, ultimately, helping their clients reach their financial goals. By dramatically improving productivity, GPTadvisor allows advisors to focus more on client relationships and strategic decision-making.

The primary beneficiaries of our solutions are wealth management entities, including financial advisory firms and independent financial advisors. We see this product as a truly global proposition, where advisors anywhere around the globe can really start engaging in a new way of working.

How does GPTadvisor solve this problem better than other companies or solutions?

Díaz de Argandoña: GPTadvisor emerged during the generative AI wave with a clear objective: to apply this groundbreaking technology specifically to the wealth management sector. This focus distinguishes us from many other tech companies that, while experienced in general AI, are now struggling to adapt to the fundamentally different approach required by generative AI. Our foundation in this new paradigm allows us to harness its full potential in ways that others find challenging.

Having said that, we take AI very cautiously. We acknowledge there is a lot of noise and over-reliance in the industry where we expect AI to solve all our problems, and that is not the case. We focus on the use cases that provide the biggest gains in productivity, but without putting compliance at risk. This is why we proactively collaborate with regulators – FCA in the UK and CNMV in Spain – to explore the risks this technology involves and frame the guidelines to follow in order to successfully implement these capabilities.

Our core team brings over 40 years of collective experience in the wealth management industry. This deep expertise has enabled us to develop an innovative product from the ground up, in close collaboration with key industry partners. We work closely with numerous wealth management entities worldwide to ensure that our solutions are aligned with industry needs, making them both relevant and impactful.

Who are GPTadvisor’s primary customers. How do you reach them?

Díaz de Argandoña: GPTadvisor’s primary customers range from big commercial banks, private banks, and wealth management firms, to financial advisory entities and independent financial advisors. We work with entities that are seeking innovative solutions to enhance their productivity, streamline their processes, and ultimately provide more value to their clients by leveraging the latest technology in the market.

Interestingly, we’ve been receiving considerable inbound interest from various industry entities, driven in part by the growing enthusiasm for generative AI. As a result, we are actively engaging these entities and incorporating them into our aggressive generative AI product roadmap. This roadmap is designed not only to meet current market demands, but also to anticipate and continuously bring the benefits of this technology that is moving at unprecedented velocity.

We’ve also had the opportunity to pitch and present our work in numerous industry events, just like what we did with you last February at FinovateEurope in London. These platforms allow us to demonstrate the unique capabilities of our solutions to a wide audience that has generated very interesting conversations for us.

By capitalizing on the current momentum around generative AI and maintaining a strong and cold focus on the needs of wealth management professionals, I think we are successfully positioning GPTadvisor as the go-to solution for entities looking to stay ahead in this rapidly evolving landscape.

Can you tell us about a favorite implementation or deployment of your technology?

Díaz de Argandoña: One of our most exciting recent implementations is our quick portfolio analysis tool. This innovative function allows advisors to simply take a picture of a client’s portfolio with their phone and receive an instant, comprehensive analysis, thoroughly explained. The analysis includes generated insights on performance, risk, fees, and even comparisons with model portfolios. All in one go. This feature exemplifies the kind of intuitive, productivity-boosting tools we aim to deliver, making sophisticated portfolio analysis as simple as taking a photo.

Another feature we’re particularly proud of is our fund documentation auto-read feature. This tool is going to be a game-changer for GPTadvisor users globally, as they are now going to be able to instantly find and chat about key data and information in the documentation of thousands of investment funds. Whether they need details on fund performance, fees, or any other critical information, this tool streamlines the process, saving valuable time and enhancing decision-making capabilities.

These features are just the tip of the iceberg. We’re seeing new productivity functions like these arise on a weekly basis, as our team is able to move in sync with the fast-paced advancements in generative AI. Our ability to rapidly bring ready-to-use features to the wealth management space is one of the key strengths that sets GPTadvisor apart. It’s incredibly rewarding to see these innovations in action, transforming how wealth managers spend their valuable time and providing them with the tools they need to stay competitive.

What in your background gave you the confidence to tackle this challenge?

Díaz de Argandoña: The confidence to tackle challenges at GPTadvisor stems from the extensive experience and proven track record of our CEO, Salvador Mas. Before founding GPTadvisor, Salvador served as the Chief Digital Officer at Allfunds for five years, where he played a pivotal role in the company’s digital transformation and its successful public offering. Prior to his tenure at Allfunds, Salvador founded several startups at the forefront of innovation in wealth management. His most recent venture, Finametrix, a portfolio management platform, was eventually acquired by Allfunds.

This entrepreneurial experience, coupled with his leadership in a global financial powerhouse, has provided Salvador with deep insights into the challenges and opportunities within wealth management. It has also equipped him with the expertise to leverage technology in creating innovative solutions that address real-world problems in the sector.

Under Salvador’s leadership, we have fostered a highly talented, agile, and focused team at GPTadvisor, which has successfully grown the product and its capabilities since its inception just over a year ago.

With this strong foundation, we are confident that we are well-positioned to lead the way in bringing cutting-edge generative AI solutions to the industry.

What is the fintech ecosystem in Spain like? What is the relationship between fintechs, banks, and traditional financial services companies in the country?

Díaz de Argandoña: The relationship between fintechs and traditional financial services companies in Spain is characterized by a mix of competition, collaboration, and co-opetition.

In the specific case of wealthtech, traditional institutions have maintained their market share despite some success stories (such as the robo-advisor Indexa Capital and the neobank MyInvestor). However, the majority of advisory services continue to be provided by traditional institutions like Santander, BBVA, or CaixaBank, which have successfully embraced digital transformation.

At GPTadvisor, we are collaborating with both types of entities, introducing generative AI in both traditional and disruptive institutions.

Left to right: Nacho Díaz de Argandoña and GPTadvisor CEO Salvador Mas at FinovateEurope 2024.

You demoed at FinovateEurope earlier this year. How was your experience?

Díaz de Argandoña: FinovateEurope was an excellent experience for us. The event was professionally and thoughtfully organized, making us, as demo participants, feel like true protagonists. It provided a valuable platform to connect with a wide range of wealth management professionals, investors, and industry stakeholders, which allowed us to test our proposition with real prospects in London—one of the world’s premier fintech hubs.

As we prepare to demo our solution again, this time in New York, it feels like a natural next step in our journey. Entering the U.S. market is a key priority for us, as we believe our solution can significantly enhance the day-to-day operations of financial advisors across the country.

We’ve been steadily growing our platform, adding a host of new features and enhancements, and we can’t wait to showcase these developments on stage. We’re confident that the New York demo will be another great experience for us, helping us to further expand our presence in a critical market.

What are your goals for GPTadvisor? What can we expect to hear from you in the months to come?

Díaz de Argandoña: Over the past year, we’ve focused intensely on refining and validating our proposition in the market. We’ve been building a next-generation AI-native platform from the ground up, one that evolves in tandem with the rapid advancements in AI technology. Our approach has involved close collaboration with leading financial entities worldwide, ensuring that we stay connected to the real-world challenges and opportunities that need solving.

I believe we’re now at a tipping point where the product is ready for greater scale. GPTadvisor is now ready to support thousands of financial advisors work more productively and deliver more value to their clients. Our plan is launching our SaaS model at global scale through the second half of the year to reach more clients and gain more leadership in the market.

As we continue to explore the full potential of generative AI and its applications within our sector, I can’t imagine a more exciting time to be involved in shaping the future with GPTadvisor. We’re just getting started, and there’s much more to come.

This week’s edition of Finovate Globalhighlights recent fintech headlines from Ireland.

Dublin-based regtech Fenergo has inked a partnership with Caribbean-based PROVEN Bank. The financial institution will leverage Fenergo’s transaction monitoring solution to enhance and streamline its anti-money laundering (AML) compliance operations.

PROVEN Bank Deputy Chief Executive Officer Nikita Kissoon underscored increasing regulatory pressure on financial institutions as one of the reasons the bank sought the partnership with Fenergo. Kissoon praised the company’s “excellent reputation for expertise in both AML regulations and cutting-edge compliance technology,” and said that enhanced AML compliance “aligns with our commitment to combat financial crime and remain future-proofed against fast-evolving regulatory changes across our offshore locations.”

Fenergo’s technology will help boost operational efficiency for the Caribbean-based financial institution. PROVEN Bank will benefit from the automation of multiple manual AML processes, which will reduce the number of false positives and free up compliance resources to focus on more complex situations and higher-risk customers. The bank will begin deploying the technology at its Cayman Islands location and subsequently expand the solution to its offices in St. Lucia and its affiliate company, PROVEN Wealth, based in Jamaica.

The partnership is especially timely. The Cayman Islands, where PROVEN Bank is based, was only recently removed from the Financial Action Task force’s AML grey list and the European Union’s black list earlier this year.

Fenergo Chief Strategy Officer Stella Clarke pointed out that banks like PROVEN that operate in multiple jurisdictions often struggle to keep up with local regulations with regards to AML. “Our transaction monitoring solutions offers PROVEN Bank the flexibility to seamlessly adapt to fast-evolving regulatory environments, while empowering it to more effectively cross-sell services to existing customers based on rich data insights,” Clarke said.

Fenergo made its Finovate debut 12 years ago at FinovateEurope in London. The company has raised more than $760 million in funding, and includes TLG Capital and Bridgepoint among its investors. Fenergo’s partnership news comes at the same time that the firm announced that it had formed an alliance with Deloitte Ireland to help deliver Fenergo’s CLM solutions to financial institutions throughout EMEA.

The Bank of Ireland wants you!

If you are a technology specialist looking to drive fintech innovation in the Republic, that is.

The Bank of Ireland just announced that it is recruiting for 100 technology roles in a variety of digital projects, including fighting fraud and advanced data analytics. The Bank is specifically looking for talent with experience in data, delivery management, engineering, resilience and cybersecurity. Open banking, cloud computing, APIs, and AI are also among the areas of emphasis.

“We continue to invest in our talent, technology, and infrastructure to ensure customers have the very best banking services,” Bank of Ireland Group Chief Operating Officer Ciarán Coyle said, “We’re currently progressing a range of innovative digital projects across the Group and we want to recruit talented specialists who can enhance the banking experience for our customers.”

The bank’s search for tech talent comes as the institution has increased its investment in financial technology. After making more than 60 enhancements to its mobile banking app, including biometrics and fraud monitoring, the bank saw an 18% year-on-year increase in active digital users. The bank announced the largest single investment in ATMs in the last decade earlier this year, as well as an investment of €15 million on new fraud prevention technology.

“We are looking for the very best talent to join our technology team as we continue to deliver improvements for customers and colleagues across the organization,” Coyle said.

Ireland’s PTSB has extended its agreement with Worldpay, giving the bank’s customers access to an additional range of services from the company, including e-commerce and ePOS. PTSB will also gain access to Worldpay DCC, a dynamic currency conversion solution that allows cardholders to pay in the currency of their choice.

PTSB Head of Personal Banking at PTSB Jeff Harbourne said that the ability to offer “a best-in-class merchant services solution” was key to the bank’s “ambition of becoming Ireland’s best personal and business bank.” Harbourne added, “By partnering with Worldpay, we’re offering a competitive advanced payments solution to our existing and new customers that enables them to grow their businesses and accept payment across all channels.”

With more than 1.2 million customers, PTSB has a presence in 98 locations throughout Ireland. Founded in 1816, the financial institution rebranded from Permanent TSB last fall following its acquisition of a sizable portion of Ulster Bank, including the firm’s Retail, SME, and Asset Finance businesses.

A Finovate alum since 2015, WorldPay today is a major payments technology and solutions company that processes more than 40 billion transactions across 146 countries and 135 currencies. Headquartered in Cincinnati, Ohio, and founded in 1971, WorldPay announced an extension of its strategic partnership with fellow Finovate alum ACI Worldwide in July, and inked a new partnership with another Finovate alum, American Express, in May.

Here is our look at fintech innovation around the world.

Latin America and the Caribbean

Colombian payment orchestration platform Yuno teamed up with Medellin-based financial services app Nequi.

Mexico City-based cryptocurrency exchange Bitso partnered with blockchain company Coincover for its non-custodial disaster recovery service.

Peruvian investment and asset management arm of Credicorp, Credicorp Capital, went live with Temenos’Multifonds accounting and investor servicing solution.

Financial Times profiled Kim Beom-su, founder of Kakao and one of the richest men in South Korea, who was recently arrested on stock manipulation charges.

Digital identity verification provider ADVANCE.AI signed an agreement with the Credit Information Corporation (CIC) to become the newest credit bureau in the Philippines. Read more about fintech in the Philippines in last week’s edition of Finovate Global.

Estonian payments and e-commerce solution provider Montonio introduced its new CEO Johan Nord.

Payments infrastructure company Kevin has been blocked from serving new clients by the Bank of Lithuania, which has also appointed a “temporary representative to oversee” the firm’s activities.

Middle East and Northern Africa

Singapore’s Prytek bought a controlling stake in Israeli fintech Tip Ranks, giving the company a valuation of $200 million.

This week’s edition of Finovate Global highlights recent fintech news from the Philippines.

Philippine mobile payments company Mynt, the firm behind super app GCash, has secured an investment of $393 million courtesy of an investment from Mitsubishi UFJ (MUFG). The funding comes at virtually the same time as the company reported another $393 million investment, this one from Philippines-based conglomerate Ayala Corporation.

“We are thrilled to welcome MUFG as a new strategic partner,” said Mynt President and CEO Martha Sazon. “With their global expertise and reach within the financial inclusion space, they will be instrumental in further expanding GCash’s social impact, especially to the underserved. Alongside this, Ayala’s unmatched commitment to Philippine economic growth and development, and its expertise in multiple industries will accelerate GCash’s mission.”

The investments give the Filipino firm a valuation of $5 billion, and gives MUFG an 8% stake in the company. Ayala’s share climbs to approximately 13%.

A subsidiary of Globe Telecom, Mynt’s GCash is used by more than 90 million individuals to buy prepaid airtime, pay bills, send and receive funds, transact with merchants, and access savings, credit, insurance, and investment products.

“GCash is an indispensable infrastructure for everyday life of Filipinos and we are delighted to join Mynt as a strategic investor to support the growth of the company,” MUFG Senior Managing Corporate Executive, Head of Global Commercial Banking Business Group Yasushi Itagaki said. “With our investment, we are excited to expand our contribution to the ongoing development of the Philippines’ digital economy and financial inclusion.”

MUFG’s investment comes at a time when the banking group has been funding a range of regional fintechs that are helping bring financial services to the underbanked. Among these fintechs are Ascend Money, a super app based in Thailand, as well as Grab of Singapore and Akulaku of Indonesia.

Earlier this year, Globe Telecom suggested that the super app may launch as a public company in the Philippines next year. This week, Bloomberg reported that the company may pursue a Philippine digital banking license, as well.

Mynt’s GCash is a big deal in the Philippines when it comes to mobile fintech apps. But how big are mobile fintech apps in the Philippines? A new report from UnaFinancial noted that among Southeast Asian nations mobile fintech app adoption has been strong overall, but nowhere more so than in the Philippines where mobile fintech app penetration reached 63% by May of this year. Malaysia was second at 55%. Interestingly, fintech powerhouse Singapore registered 45%, tied with Thailand and behind Indonesia’s 49%. Vietnam showed 32% mobile fintech app penetration.

Why such a strong performance for mobile fintech apps in the Philippines? The UnaFinancial analysts cited a handful of factors including the large number of unbanked Filipinos; regulatory support for developing digital financial technologies; a sizable, tech-savvy youth population; and growing rates of Internet adoption. Digital wallets and payment apps remain the most popular mobile fintech apps, with mobile banking apps making a strong second place showing. One area of particular growth is lending apps, which increased their share of mobile fintech apps from 1% to 5% between 2019 and 2024.