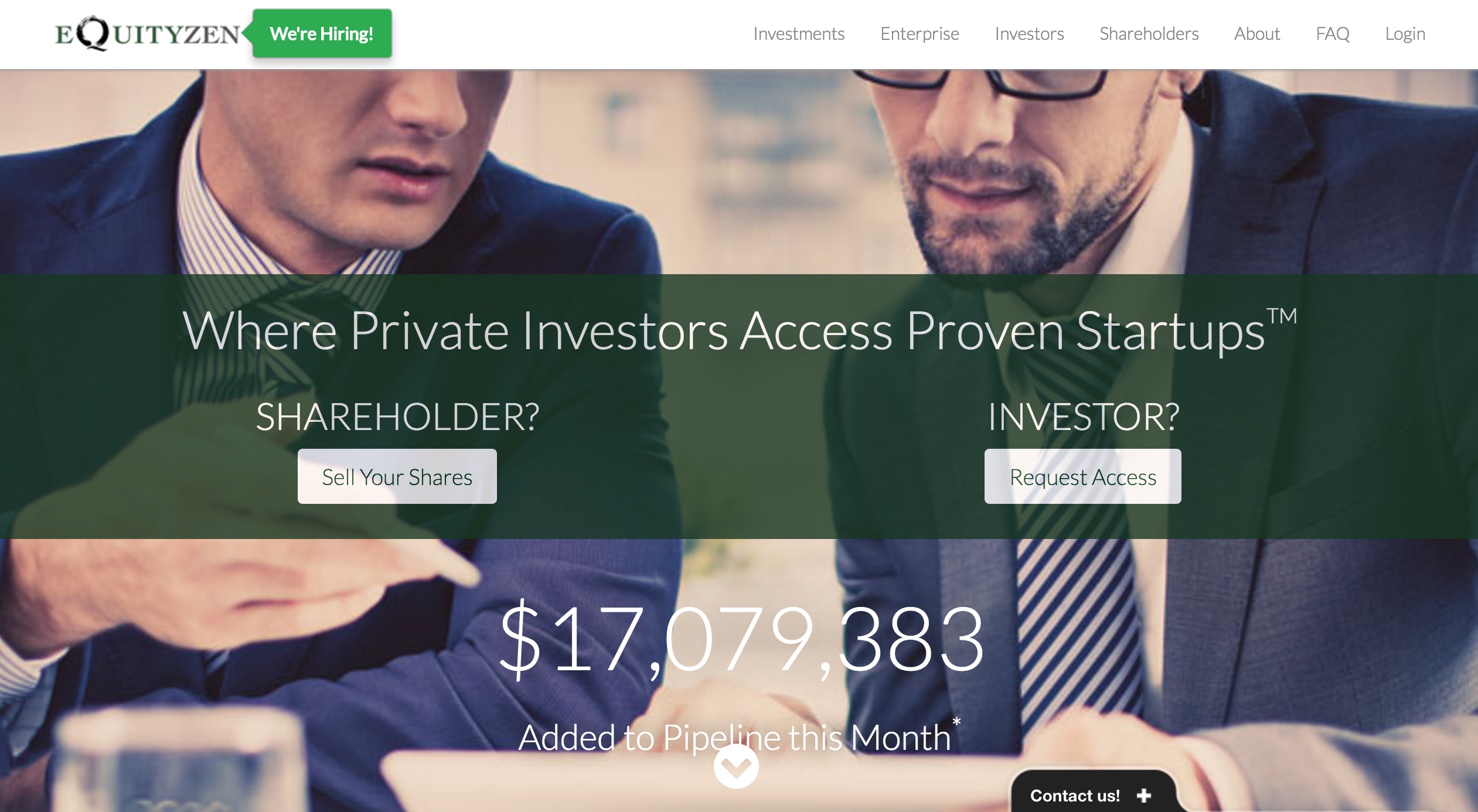

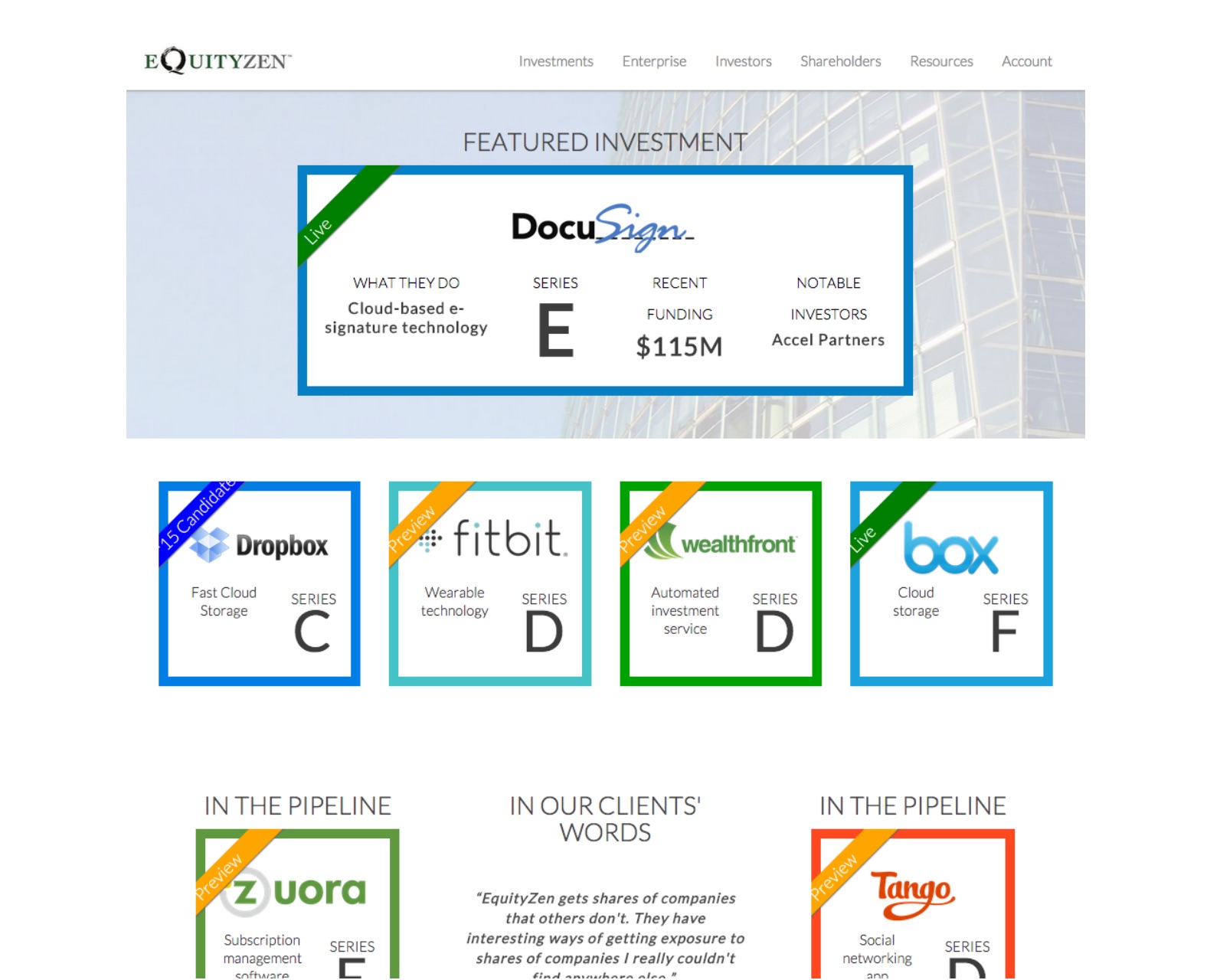

EquityZen was founded in 2013 as a platform to exchange private company shares. Its online marketplace conducts secondary transactions where users buy and sell existing shares of private companies with at least $100 million in enterprise value.

EquityZen’s roots stem from when CEO Atish Davda left his job at a hedge fund to pursue a career at a startup. Davda, who needed a down payment for a house and cash to purchase an engagement ring, wanted liquidity for his private company equity. At a time when startups are staying private longer and consumer familiarity with startups is greater than ever, this seemed the ideal time for Davda to launch EquityZen.

“We bring private markets to the public,” CEO Davda explains in his FinovateSpring demo, where the company launched EquityZen Institutional, an offering that enables professional wealth managers to offer their clients further diversification through investing in private companies.

Company facts:

- Founded in 2013

- $3.5 million in funding raised

- Headquartered in New York City, New York

- 10,000+ accredited investors from 15+ countries

- 5,000+ sellers, 80% of them from a unicorn startup

- On pace to reach $500 million of equity on its platform this year

CEO Atish Davda, founder, and Ketan Bhalla, product lead, launching EquityZen Institutional at FinovateSpring 2016 in San Jose.

CEO Atish Davda, founder, and Ketan Bhalla, product lead, launching EquityZen Institutional at FinovateSpring 2016 in San Jose.

Before his presentation at FinovateSpring last month, we chatted with Atish Davda (pictured right), the company’s CEO, for further insight on EquityZen. Davda has been featured on CNBC’s SquakBox and Fox Business News. He speaks English, Hindi, Gujarati, and Python.

Before his presentation at FinovateSpring last month, we chatted with Atish Davda (pictured right), the company’s CEO, for further insight on EquityZen. Davda has been featured on CNBC’s SquakBox and Fox Business News. He speaks English, Hindi, Gujarati, and Python.

Finovate: What problem does EquityZen solve?

Davda: EquityZen is a stock exchange for private company shares.

Amazon went public with a market capitalization of $440M at an age of four years; today, companies remain private almost until they’re teenagers before they are accepted by public markets. With the longer gestation period, there is a gap between the financing timeline of the company and that of individuals supporting the company (shareholders wanting to sell and investors looking to invest). EquityZen has filled this gap.

Finovate: Who are your primary customers?

Davda: EquityZen’s platform helps shareholders (founder, investor, employee, or ex-employee) of any private company that passes our extensive filters before they can enlist. By working directly with the company, not only does EquityZen enjoy a greater trust, but also a direct channel for future shareholders who wish to sell while the company is private.

EquityZen’s platform offers these investment opportunities to accredited investors and qualified purchasers. Investors on our platform include small institutions (asset managers, family offices) as well as retail (HNWIs, financial advisers). This investor base now spans over 15 countries, and makes way to offer other asset classes.

EquityZen has established itself as one of the hubs for educating financial advisers and investors alike regarding the risks and benefits of investing in the asset class.

Finovate: How does EquityZen solve the problem better?

Davda: While it was accepted practice to build a phone-sales brokerage, EquityZen is building a future where the days of phone broker—and the overhead they bring—are numbered. Using our technology, therefore, EquityZen is able to conduct $100,000 transactions profitably, while deriving greater profits from transactions well above $1 million.

Finovate: Tell us about your favorite implementation of your solution.

Davda: While everyone else is trying to find a way to let investors put more money into the ecosystem, EquityZen is the only platform through which folks actually get money out—liquidity!—when they need it.

Finovate: What in your background gave you the confidence to tackle this challenge?

Davda: Atish Davda, CEO; Shriram Bhashyam, counsel and shareholder relations; and Phil Haslett, investments, founded EquityZen with one goal in mind: to reinvent the private market. All three have previous experience in financial services and have collectively called New York City home for over 20 years.

Prior to EquityZen:

- Atish was product lead and first engineer at Ampush, a big-data advertising-technology firm. He began his career as a financial engineer at AQR Capital, before which he founded and operated the education-technology firm, Knolsoft.

- Shri was an attorney at Shearman & Sterling LLP, a New York-based global law firm. Shriram advised market participants on regulatory, transactional, and trading and markets issues, with a focus on U.S. broker-dealer and securities regulation. He also advised banks and other financial institutions on U.S. bank regulation, including the Dodd-Frank Act of 2010.

- Phil was a vice president at Pomelo Capital, a NYC-based hedge fund, focusing on capital structure arbitrage. After helping launch the fund (now $300mm+ AUM), he was responsible for trading, research, and operations. Phil started his career at Barclays Capital in their Proprietary Trading group trading credit and equity derivatives.

Finovate: What are some upcoming initiatives from EquityZen that we can look forward to over the next few months?

Davda: Wider adoption of EquityZen Institutional beyond the 1,000+ financial advisers on our platform that know about it. EZ Institutional is a new offering EquityZen launched at Finovate in 2016, allowing financial advisers and institutional investors to invest capital and manage alternatives portfolios on behalf of their clients.

Finovate: Where do you see EquityZen a year or two from now?

Davda: While we remain focused on the U.S. market for now, I would not be surprised if EquityZen increases our investor network reach from 15 countries to a bit more than that.

CEO Atish Davda, founder, and Ketan Bhalla, product lead, presenting EquityZen at FinovateSpring 2016 in San Jose:

We spoke briefly with Daria Dubinina and Andrey Morozov during rehearsals at FinovateSpring in May. We followed up with a few questions for Dubinina by e-mail.

We spoke briefly with Daria Dubinina and Andrey Morozov during rehearsals at FinovateSpring in May. We followed up with a few questions for Dubinina by e-mail.

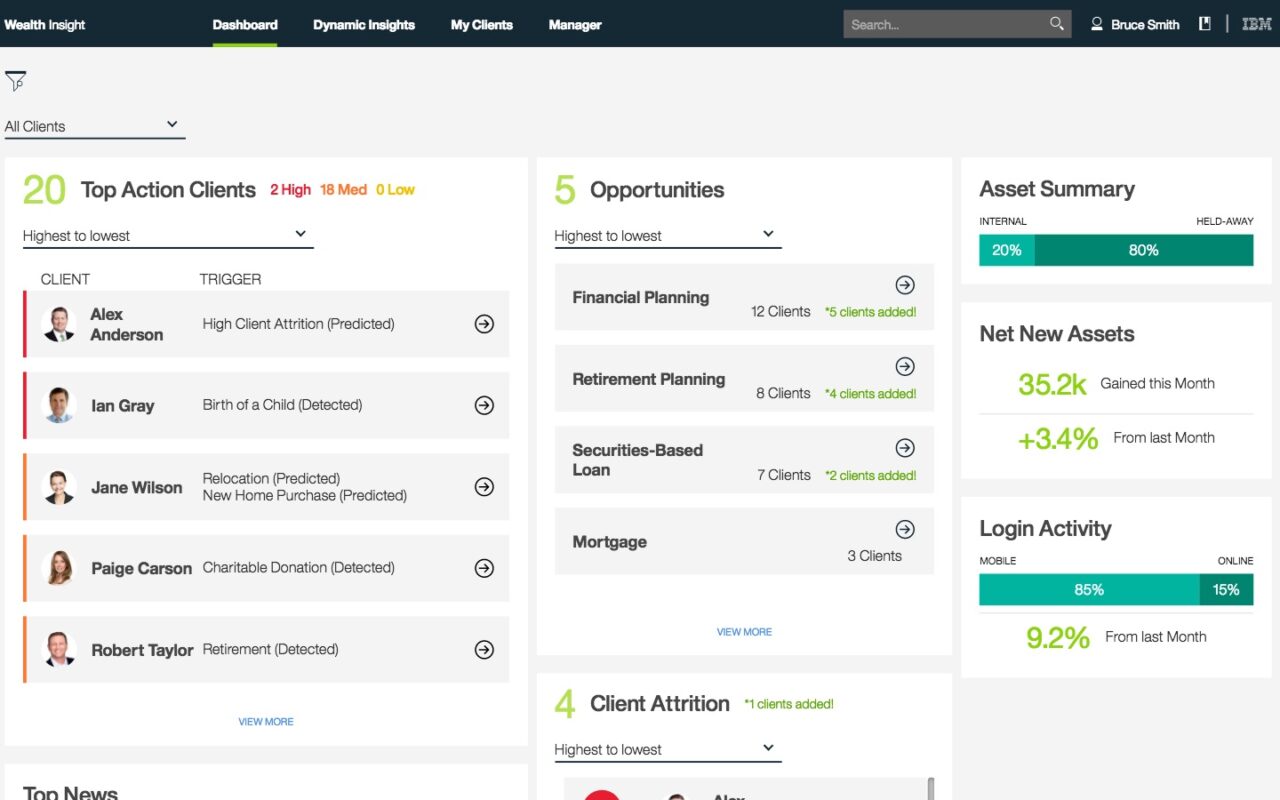

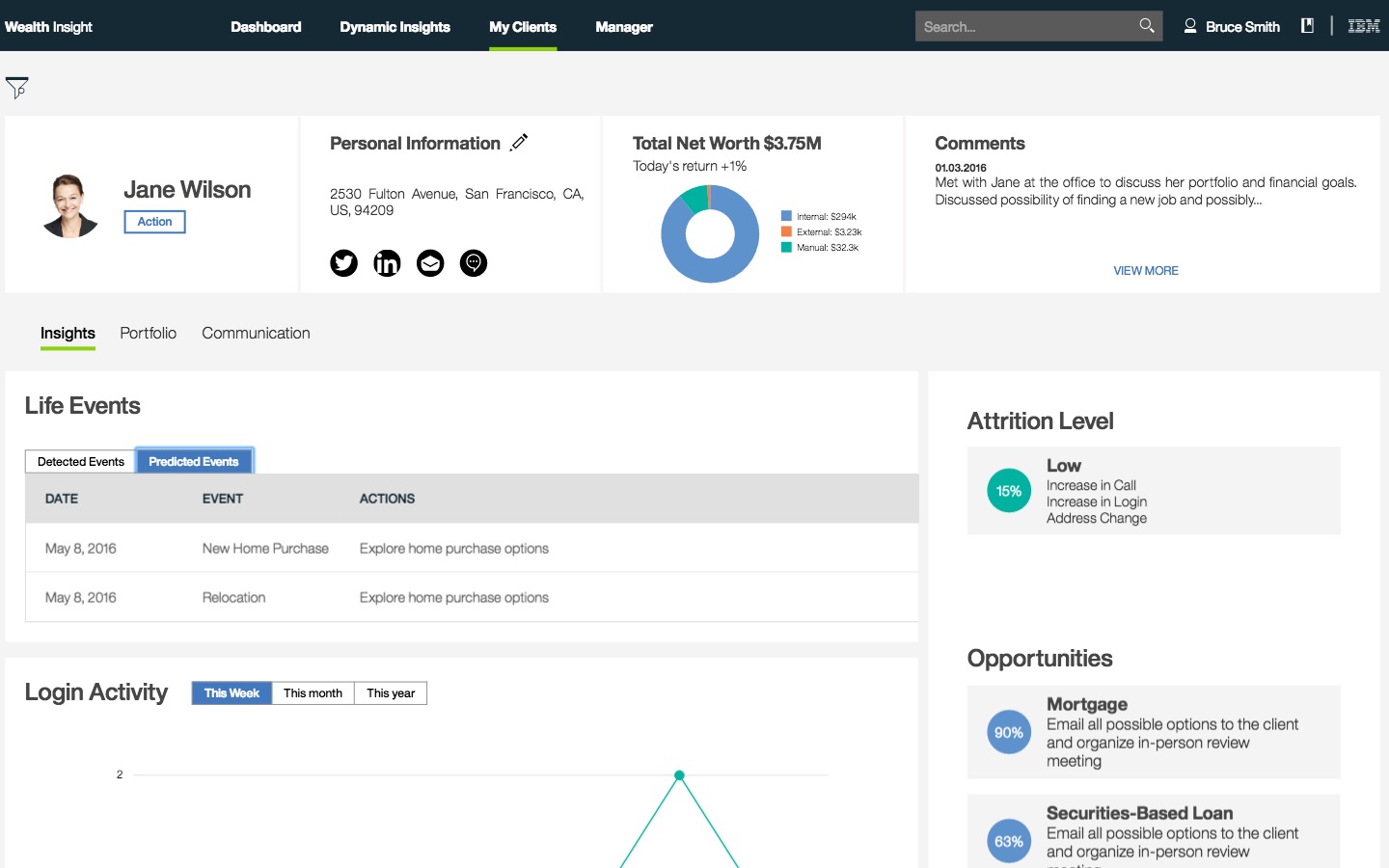

Financial adviser dashboard

Financial adviser dashboard Alex Baghdjian, senior offering associate, financial markets & wealth management, and Rob Stanich, global wealth management offering manager, presented at FinovateSpring 2016.

Alex Baghdjian, senior offering associate, financial markets & wealth management, and Rob Stanich, global wealth management offering manager, presented at FinovateSpring 2016. We chatted with Rob Stanich, IBM global wealth management offering manager, about the new offering:

We chatted with Rob Stanich, IBM global wealth management offering manager, about the new offering: Client Profile screen

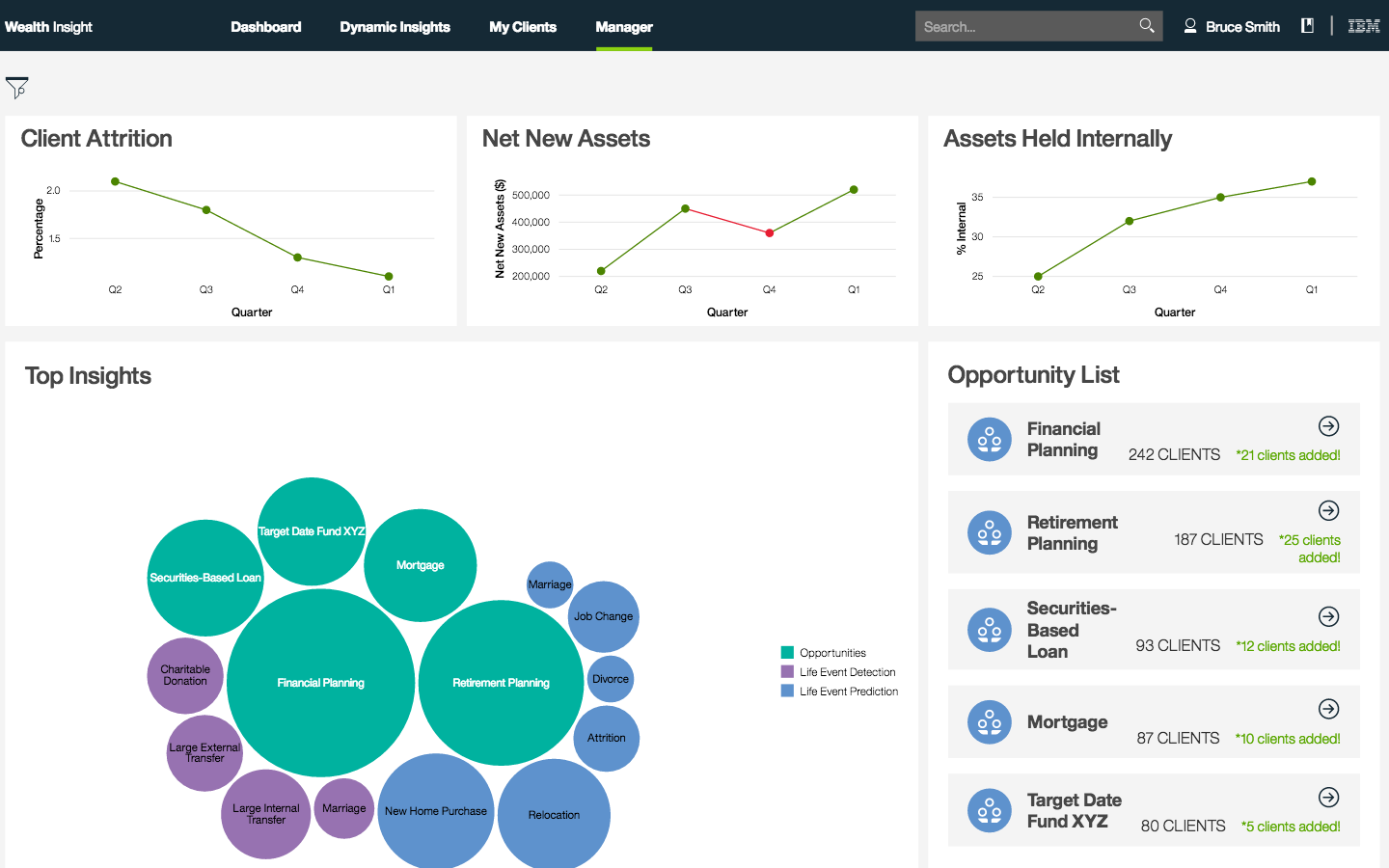

Client Profile screen The Branch Manager dashboard

The Branch Manager dashboard

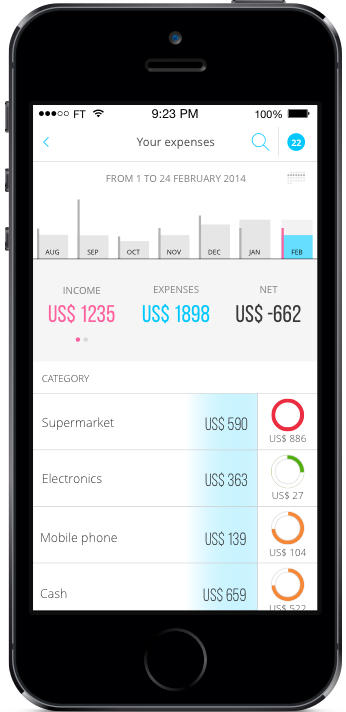

Fintonic’s

Fintonic’s CEO Sergio Chalbaud demoing Fintonic at FinovateSpring 2016 in San Jose

CEO Sergio Chalbaud demoing Fintonic at FinovateSpring 2016 in San Jose We interviewed CEO Sergio Chalbaud for more insight into the Madrid-based company. Chalbaud, who speaks three languages, has served as CEO of Fintonic since it launched in 2012. Prior to starting Fintonic, he was founder of

We interviewed CEO Sergio Chalbaud for more insight into the Madrid-based company. Chalbaud, who speaks three languages, has served as CEO of Fintonic since it launched in 2012. Prior to starting Fintonic, he was founder of

We spoke briefly with Eran Livneh, Personetics VP of Marketing, during rehearsals at FinovateEurope in February. We followed up with a few questions for CEO Sosna via e-mail.

We spoke briefly with Eran Livneh, Personetics VP of Marketing, during rehearsals at FinovateEurope in February. We followed up with a few questions for CEO Sosna via e-mail. Finovate: How does your solution solve the problem better?

Finovate: How does your solution solve the problem better? Finovate: Tell us about your favorite implementation of your solution?

Finovate: Tell us about your favorite implementation of your solution? Finovate: What are some upcoming initiatives from your company that we can look forward to during the next few months?

Finovate: What are some upcoming initiatives from your company that we can look forward to during the next few months?

Finovate: What problem does Scalable Capital solve?

Finovate: What problem does Scalable Capital solve? Finovate: Tell us about your favorite implementation of Scalable Capital.

Finovate: Tell us about your favorite implementation of Scalable Capital.

Featurespace’s Commercial Director Matt Mills and Dave Excell, co-founder and CTO, presented at FinovateEurope 2016

Featurespace’s Commercial Director Matt Mills and Dave Excell, co-founder and CTO, presented at FinovateEurope 2016

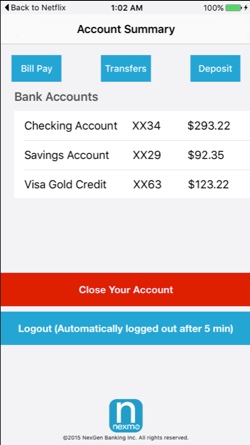

We spoke with Awasthi during conference week at FinovateEurope. Then we followed up with a few questions by email for more about Nexmo, its Verify SDK, and what to expect next from the company. Awasthi has been with Nexmo since 2014, and was previously a program manager at Microsoft.

We spoke with Awasthi during conference week at FinovateEurope. Then we followed up with a few questions by email for more about Nexmo, its Verify SDK, and what to expect next from the company. Awasthi has been with Nexmo since 2014, and was previously a program manager at Microsoft. Finovate: Who are your primary customers?

Finovate: Who are your primary customers? Finovate: What in your background gave you the confidence to tackle this challenge?

Finovate: What in your background gave you the confidence to tackle this challenge?

Advisory Service SVP Jay Hummel, Blake Wood, SVP, product management, and Molly Pandya, SVP, product management, presented Advisor Now at FinovateEurope 2016 in London.

Advisory Service SVP Jay Hummel, Blake Wood, SVP, product management, and Molly Pandya, SVP, product management, presented Advisor Now at FinovateEurope 2016 in London.

CEO Nikita Blinov, Chief Data Scientist Alexander Fonarev, and Project Manager Anna Laskovaya presented at FinovateEurope 2016 in London.

CEO Nikita Blinov, Chief Data Scientist Alexander Fonarev, and Project Manager Anna Laskovaya presented at FinovateEurope 2016 in London. At FinovateEurope 2016, we interviewed Nikita Blinov (

At FinovateEurope 2016, we interviewed Nikita Blinov (

We spoke with Chilton briefly on rehearsal day at FinovateEurope, then followed up a few weeks later with a few questions by e-mail.

We spoke with Chilton briefly on rehearsal day at FinovateEurope, then followed up a few weeks later with a few questions by e-mail. Finovate: Who are your primary customers?

Finovate: Who are your primary customers?