Can banks effectively provide their customers with relevant, personalized information about how they can best spend their money? For Personetics, an Israel-based company making its Finovate debut earlier this year, the three pillars of personalization are real-time access to transaction data, predictive analytics, and best practices, i.e., knowing what works and what doesn’t. Combine these three elements and the result is what Eran Livneh, Personetics’ VP of marketing called “making personalized guidance work for large financial institutions.”

Personetics offers a white-label solution that integrates with a bank’s mobile app or online website. As soon as a customer logs in—no registration, no signup required—the solution provides contextual tips and predictive advice, as well as flags transactions based on real-time transaction analysis, aggregation, location, and other contextual factors. Company co-founder and CEO David Sosna emphasizes that what Personetics provides “are not offers, not sales, but insights,” before explaining why insights are more valuable than traditional rewards.

“Our data shows that when banks are creating experience and content that people like to get, instead of promoting products and services at the engagement level you are going to get, … is going to dramatically improve,” Sosna said.

Pictured (left to right): CEO David Sosna, co-founder, and Sudharsan “Sid” Krishnan, solution architect, demonstrated Personetics’ Engage at FinovateEurope 2016 in London.

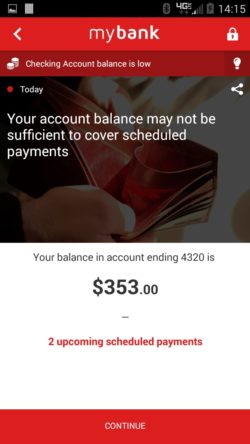

How does Personetics make a bank customer’s financial life better? Sosna used the examples of Personetics flagging a charge after a free-trial subscription lapsed, or sending “a contextual tip” on how to best use a bankcard upon arrival at an airport. Personetics also helps consumers make savings decisions based on anticipated cash flow shortfalls and provides an inbox of recent or unanswered notifications. Users are prompted to rate the tips to provide feedback on their usefulness.

“We have implemented it with some of the largest banks in the world,” Sosna said from the Finovate stage in London. “If you do good things for the customer, if you are going to partner with them using content, then they are going to come.”

Company facts:

- Founded in 2011

- Headquartered in Tel Aviv, Israel

- Total funding of $17 million

- 15 million users

- David Sosna is CEO and co-founder

We spoke briefly with Eran Livneh, Personetics VP of Marketing, during rehearsals at FinovateEurope in February. We followed up with a few questions for CEO Sosna via e-mail.

We spoke briefly with Eran Livneh, Personetics VP of Marketing, during rehearsals at FinovateEurope in February. We followed up with a few questions for CEO Sosna via e-mail.

Finovate: What problem does your solution solve?

David Sosna: We help banks meet customer expectations for a personalized digital experience. Banks have a great amount of data about their customers, and we help them transform this data into insights that can be extremely useful to the customer.

By utilizing their data assets to better serve their customers, banks can remain relevant in the digital age and compete more effectively with emerging financial services providers that are threatening their space.

Finovate: Who are your primary customers?

Sosna: We currently work with some of the largest banks and card issuers in North America and Europe, as well as some smaller institutions that have advanced digital strategies. There are millions of consumers who [daily] use our solutions, but since it’s a white-label solution that is embedded in the bank’s web or mobile application, they never know it’s Personetics that is doing the magic behind the scenes.

Finovate: How does your solution solve the problem better?

Finovate: How does your solution solve the problem better?

Sosna: Three critical elements [are necessary] to make personalized guidance work for large financial institutions.

The first is the ability to access transaction data and do it it in real-time. If the data is not up-to-date, the information conveyed to the customer could be inaccurate or even misleading. It could undermine the credibility of the solution and the bank. We have invested a great amount of effort in developing APIs that can access the bank’s data in real-time and do it directly from the core system, so the bank doesn’t have to create new data stores. Needless to say, it also has to be secure: Our solution sits behind the bank’s firewall and is fully compliant with the strictest security and privacy requirements.

Second is predictive analytics that can turn data into insights for the customer. It’s not enough to simply present information to the customer. Guidance is about proactively identifying potential issues and opportunities, providing meaningful advice that the customer can act on – much like a well-trained and highly qualified banker or financial adviser would do. For example, our analytics enables us to determine what’s the best way for an individual customer to start saving, how much should be allocated for savings, and when is the best timing to present this insight to the customer.

Last but not least is the issue of best practices. For most banks, this is new territory. We have been doing it for a few years now, and have developed a significant body of knowledge of what works better and what doesn’t. Our solutions come with a library of more than 150 pre-built user scenarios that a bank can start using right out of the box. They would typically start with 30 or 40, and then build on them over time.

So data access, analytics, and domain-specific best practices—it’s the combination of these three that makes Personetics uniquely positioned to deliver a solution that is cutting-edge for the consumer, yet practical for the bank.

Finovate: Tell us about your favorite implementation of your solution?

Finovate: Tell us about your favorite implementation of your solution?

Sosna: That’s a tough question … like asking who is your favorite child …

Our solution is very strategic to the banks, since it really impacts how the bank interacts with customers on a daily basis. Each implementation has some unique aspects based on the customer-facing strategy specific to that bank.

I can point to several things I like in a number of these implementations. For example, one of the largest banks we are working with is rolling out the solution across different countries. It’s nice to see how the solution is generating similar positive reaction from customers across cultures and languages. When you see customer satisfaction rates in the 80% to 95% range as we are seeing in these implementations, it’s hard not to feel good about it.

At the other end of the spectrum, we are working with a new challenger bank that is using our solution to turn the entire paradigm of customer communication on its head. Banks in general are still very product-centric, so when you log in to the bank application, you see a list of accounts. This bank is moving away from the product-centric approach, so the communication is contextually driven from the customer’s perspective and based on what the customer is doing, or trying to do, at the moment. It’s a different concept and one that turns the overused term of “customer-centric” into a reality.

Finovate: What in your background gave you the confidence to tackle this challenge?

Sosna: The team that started Personetics is predominately the same team that worked together at Actimize, which was a leading solution for fraud detection and compliance in the financial sector and is now part of NICE Systems. We started Personetics with the idea that if we know how to analyze bank transaction data, which we have done for fraud detection, we can use this knowledge to better serve the bank customer. Obviously we still had to learn a lot and we are still learning, but this prior familiarity with the domain and the technologies required to tackle this problem—fast and secure data access, in-memory analytics, AI, and machine learning—definitely helped us get started and quickly move forward.

Finovate: What are some upcoming initiatives from your company that we can look forward to during the next few months?

Finovate: What are some upcoming initiatives from your company that we can look forward to during the next few months?

Sosna: We have two types of solutions that nicely complement each other along the spectrum of customer interactions with their financial institution. The first is Assist, which is a personalized self-help solution for customers actively seeking advice from the bank. The second is Engage, which proactively provides bank customers with personalized, predictive, and contextualized insight and guidance.

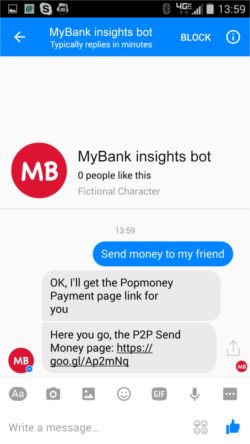

We just announced Personetics Anywhere, which is our chatbot solution that brings both Assist and Engage into messaging platforms such as Facebook Messenger. The whole chatbot scene is exploding right now, and we have a very unique offer that allows banks to quickly deploy a chatbot solution that is personal, smart, and very useful to the customer.

While I cannot get into specifics before we officially announce them, there are some interesting additional developments in the works that will be coming out in the next few months.

Finovate: Where do you see Personetics a year or two from now?

Sosna: I think the whole area of digital money management is going to evolve significantly over the next few years. As consumers feel more comfortable with digital tools, they will expect higher levels of personalized insight and advice from their banks. I believe Chatbots will play a major role and become a must for pretty much every financial institution.

We are already seeing a huge uptick in demand for our solutions, both in North America and in Europe, and I fully expect the kind of solutions we provide to become pretty much an industry standard in a few years. At the same time, as the boundaries of financial services blur, we will probably find ourselves working with a more diverse set of financial services providers that will be entering the market in various capacities.

Check out the demonstration video from Personetics from FinovateEurope 2016.