Techniques: Email, Web inquiry, chat, instant

messaging, call back, co-browsing

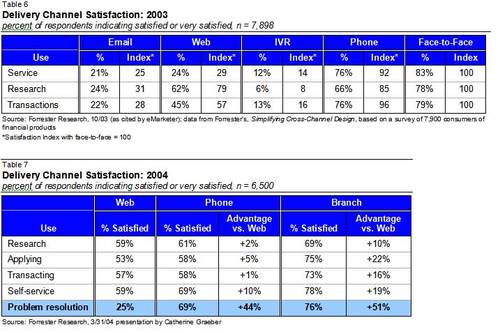

Web self-service may be the key to cutting servicing costs online, but

email support is the key to retaining customers. Responsive support (chat,

email, and telephone) is preferred by about 70% of online banking users

according to Vividence . Concerned, distraught, or impatient customers

aren’t about to wade through FAQs looking for answers. They want immediate

assurances that their concerns are valid and will be addressed. Typically

that’s required a telephone call, but more and more users are turning to

chat and email options. What’s holding back email today is poor service. In

a recent Forrester survey, only 25% of respondents expressed satisfaction

with email service, a satisfaction rate barely one-third that for

traditional branch and phone channel.

Once financial institutions provide a user experience on par with

telephone and branch, email will dominate as the primary medium for service.

Fifteen years from now, telephone and branch service support will be distant

memories. The vast majority of users will fire off an email, instant

message, or Web inquiry without even considering any other option. There is

absolutely no question that electronic channels will eventually dominate,

providing many advantages for both consumers and financial institutions.

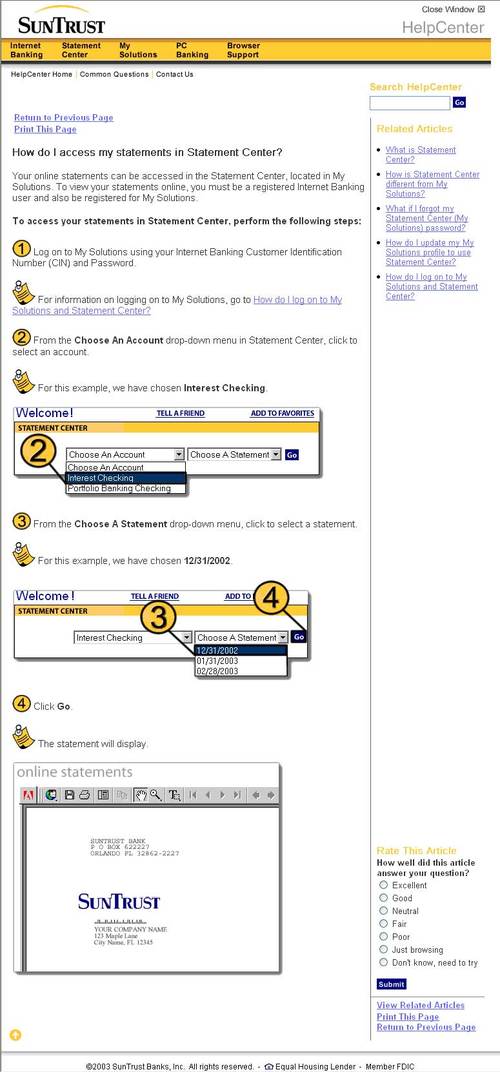

Web-inquiry Form

The design of the form used for customer inquiries

can impact the timeliness, effectiveness, and cost of your online support.

Make sure you’re not missing an opportunity to make future solicitations to

online customers with an opt-in question. You should also consider tagging

customers with cookies so you can better track future Web activity. Table

21, below, provides more details on form design.

Email Deflection

Not only can you deflect phone calls from your

call center and branches by the way of a Web-based inquiry form. You can use

the same form to actually deflect email messages as well. The key is having

the ability to parse likely search terms out of free-form text inquiries. In

the example below, Cloudmark, a provider of consumer spam filters,

applies search algorithms to the free-form question, “Is there a way to make

Cloudmark catch more spam?” (screen 1, below). Rather than sending

the query directly to customer service, the company first provides possible

answers to the question (screen 2, below). Users who still want to

ask the company the question can complete the longer Request for Help form

According iPhrase, which supplied the search solution, Cloudmark has

been able to reduce email volume dramatically.

Responding to emails or Web inquiries should follow a three-step process as

outlined in Table 22 below:

Table 22

Making Email Responses More User-Friendly

Phase 1: Immediate Autoresponse

- Include bank name in subject field and from

field

- Thank customer for using e-service and explain the process

and typical response time

- Provide response-time estimates based on averages for that

time of day and/or day of the week/month;

extra credit: provide custom response-time estimates based on current

email queue

- Include links to appropriate FAQ sections

- Reference telephone numbers for immediate support

Phase 2: Actual Answer

- Use good formatting:

– indent

– physically separate ideas

– white space

– bullet points, lists, tables

- Keep paragraphs and sentences short

- Include “time received” and “time answered” date stamps

- Include service rep name/email address for more personal

feeling and to encourage customer to engage in a conversation until

their question has been answered to their satisfaction

- Include bank name in subject field and from

field

- Provide tracking number for the customer inquiries

- If responses go to a secure mailbox within the online

banking program, send an additional email to the user’s Internet

mailbox(es) telling them that an answer is waiting (with a link to it)

- Archive customer questions and your answers so users can

refer to them later

- Include intuitive URL and/or email address for customer

comments and feedback, such as <comments.yourbank.com>, or

[email protected]

- Don’t forget to say, “Thanks for using our e-service.”

- Add a telephone number for additional discussion

Phase 3: Follow-up

- Follow-up with the customer at least once to ascertain

their satisfaction with the answer and whether they have additional

questions

- Include a two- or three-question customer-satisfaction

survey to quantify the work done by your e-service department as a

whole, and each e-service rep as individuals

- The simplest approach is to have the followup message

originate from the service rep who handled the original message; an

alternative approach is to have the followup come from a supervisor or

“quality assurance rep;” you may want to test both approaches to see

which works best

- Encourage comments and feedback, either by responding to

this message or entering comments anonymously at <comments.yourbank.com>

- Telephone number for additional discussion or to make

comments

Source: Online Banking Report, 3/04

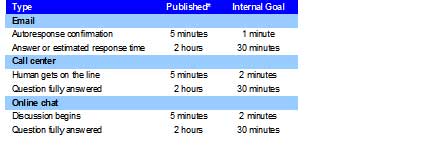

The Importance of Response Times

Even though most online transaction times are measured in seconds, users

will still become frustrated if your system is slower than what they are

accustomed to. Search engines, the most widely used Web application, set the

expectations early on. Even as early as 1995 and 1996, search engines were

able to cull through millions of pages of data and deliver results in less

than 20 seconds. With the faster connections used today, search times have

shrunk even more. Banking information, secured behind various log-in

schemes, can take three to four times longer to access, but unless you

forget your password, retrieval times are still under a minute, an

acceptable information-retrieval wait period for most Web users.

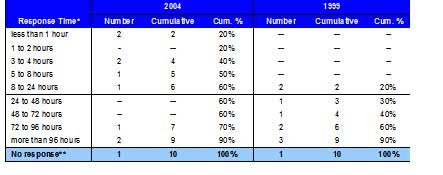

Table 23

Acceptable Wait Times for eService

acceptable wait time in hours for an online

retailer’s customer service department to respond to an email or website

inquiry; survey conducted during holiday shopping season, n = 1019

|

Use |

% of Total |

% of Those with Answer |

Top 10 Bank Results |

| 4 hours or less |

45% |

53% |

4 |

| 1 hour |

24% |

28% |

2 |

| 2 hours |

12% |

14% |

2 |

| 3 hours |

6% |

7% |

— |

| 4 hours |

3% |

4% |

— |

| 5 to 24 hours |

38% |

45% |

2 |

| 5 to 10 hours |

4% |

5% |

1 |

| 11 to 23 hours |

5% |

6% |

— |

| 24 hours |

29% |

34% |

1 |

| More than 24 hours |

n/a |

— |

1 |

| Don’t know (no answer) |

15% |

— |

3 |

Sources: Harris Interactive, 11/03 (as cited by eMarketer); research

commission by RightNow Technologies; telephone survey fielded Oct. 2003,

respondents included 1019 U.S. adults age 18+ (511 men and 508 women)

Top-10 Banks: Online Banking Report tests 4/04

Acceptable wait times for human help online are quite different. Web users

have been relatively tolerant of slow responses to email queries, likely

because they use Web-based inquiries for less urgent questions. However,

users are beginning to become more demanding. A recent Harris Interactive

survey (see Table 23, right) found that more than one-third

(36%) of Web users expected a response from customer service within two

hours. If you remove the 15% who said “didn’t know,” the number is close to

half (42%).

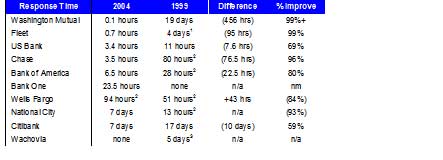

In our April 2004 test of the top-10 banks, only two returned an answer

within three hours. Washington Mutual, head and shoulders above the

rest, answered the question within four minutes, Fleet was second at

41 minutes. We received some response from all ten banks, although only

seven answered the question. The three non-answers: Wells Fargo

referred us to their call center; Citibank, apparently playing

Jeopardy provided an answer and made us guess what the question was, because

it clearly wasn’t the one we asked; and Wachovia sent an autoresponse

confirming receipt of the question, but we never got an answer. Most

surprisingly, not a single bank has followed up to see if we needed

additional assistance or perhaps wanted to apply for the account we inquired

about.

Overall, the banks have made great strides in the 4.5 years since our

last test. In 1999, the fastest response time was US Bank at 11 hours

(3.4 hours in 2004); this year the fastest response was Washington Mutual at

4 minutes, quite an improvement over its 19 days in 1999, where its

response was a snail-mailed packet.

In our most recent test, five (50%) returned an answer within 8 hours,

none did in 1999. This year, six (60%) beat the 24-hour threshold, only two

(20%) did so in 1999. Also, the quality of response was much better on

average. In 1999, only two banks emailed us an answer (three if you count

BankBoston), the rest either referred us to other departments or sent a

brochure in the mail. This year, six responded with answers, and only one

(Wells Fargo) tried to pawn us off on the phone center.

One area that needs improvement, identifying the bank name in the message

from and subject lines. Only five of the ten banks identified

themselves in the message header, the remainder used generic subject and

from lines making the messages look suspiciously spam-like.

8

Table 24

Large Bank Email Response Times

Source: Online Banking Report, 3/04 (questions submitted April 9, Good

Friday and Easter weekend)

and 10/99 (questions submitted Oct. 8-11, Columbus Day holiday weekend)

The question asked of each bank varied in the two tests:

In 2004: “Do you have a checking account that includes unlimited no-fee

transfers from an overdraft line of credit?“

In 1999: “I am relocating to [your city] soon and would like checking

information including pricing.”

*Time shown is elapsed time until an actual response was received, not

including autoresponses;

in both years, 3 of the 10 banks sent an autoresponse

**after 10 days

Table 25

Top-10 Banks: 2004 vs. 1999 Performance

Source: Online Banking Report, 3/04 and 11/99

Notes: (1) BankBoston answered the question in 22.5 hours; (2) Did not

answer question, referred to other sources of info

(3) No response from First Union

Source: Online Banking Report test conducted between 11 am and 1 pm

Pacific Daylight Time, on Friday April 9 (Good Friday);

Question: “Do you have a checking account that includes unlimited no-fee

transfers from an overdraft line of credit?

Columns: Home Location = location of Contact Us link;

Clicks Away = number of clicks to the inquiry form, starting from the

homepage; Complete Time = time to find and complete the

inquiry form, starting from the homepage; Popup = is the inquiry form

displayed in a popup window; Verify Email = is the user required to

enter their email address twice; Confirm = is user given a final look

at their info and question before submitting; Opt-in = is the user

given the option to opt in or out of future email marketing/service

messages; Required Fields = the fields that must be completed in

order to submit a question; Auto time = how long after we pressed

submit did it take to receive an autoresponse from the financial institution

(blank means no autoresponse received); Time to Answer = how long after

pressing submit before receiving an answer to the question; Quality of

Answer = our subjective evaluation of the answer including tone,

content, layout, and next steps

Legend: E = Email, N = Name, A = mailing address, T = Type of question,

Su = Subject of question, St = state of residence,

Z = zip code, A = complete mailing address; Customer = Customer or

non-customer, How = How did you find us?

Notes: (1) Wells Fargo’s contact page was very slow to download,

increasing the time by 30 seconds

(2) An extra click on one of the screens required to scroll down to the

desired area (only 3 screens to go through)

(3) Washington Mutual does not have a Contact Us link on its home

page; however if you click Search, you’ll see a Contact Us button in

the upper right hand corner

(4) Fleet does not have a Contact Us link on its home page;

however if you click Personal Financial Services, there is a Customer

Service tab on the far right, but still no Contact Us link

(5) Did not specify which fields were required

(6) Subjective evaluation of answer: A = accurate response and what to do

next; B = reasonably accurate response;

C = vague or incomplete answer; D = misleading answer; F = no answer or

wrong answer

(7) Wells Fargo made no attempt to answer the question, just referred

user to someone in the call center

(8) Citibank’s response 7 days later made almost no sense, having nothing

to do with my question; at first I thought it was a bad

phishing attempt; either it was automation gone awry, a service rep having a

very bad day, or I got an answer meant for someone else

Table 27

Example Service Standards

Source: Online Banking Report, 3/04

Example #1: Generic Normal Autoresponse

To: Customer

From: Yourbank Ebanking <[email protected]>

Re: Your question to Yourbank

Thanks for using our online service department.

This is an automatic message to tell you that we received your message at

10:12 AM Sept. 29 and have forwarded it to the proper department for a priority

response.

Most questions are answered within a few hours, but it could take up to 24

hours in certain instances.

Regards,

Ebanking Customer Support

(800) 123-4567

http:/www.yourbank.com/support

Example #2: Personalized VIP Autoresponse

To: Customer

From: Pat P. Smythe <[email protected]>

Re: Your question to Yourbank

Thanks for using online VIP service.

This is an automatic message to tell you that I received your message at

10:12 AM and we are currently working on a response. Within an hour you will

receive a either a complete answer or a preliminary response (depending on the

complexity of the request).

Please email or call if you have further questions. Regards,

Pat Smythe, VP – VIP Service

Phone Direct: (415) 555-1234 Toll-free (888) 555-9876

http:/www.yourbank.com/vip_service/pat_smythe

P.S. If for any reason you are not satisfied with my response, please feel

free to contact

Kim Bradford, VP & Manager VIP Service, (415) 555-6789, or [email protected].

Example #3: Referral to Web-based form

To: Yourcustomer <[email protected]>

From: E-Service <[email protected]>

Re: Your Question to Yourbank

Dear Customer:

Thanks for your email question received a few minutes ago. This is an

automatic response to let you know that we appreciate your interest in

yourbank.com. However, due to the volume of junk mail and spam coming to our

public mailboxes, we can only respond in a timely manner to questions submitted

via our Web-based form. Click here to go directly to that form (if you can’t

click on it, then type this address into your browser):

http://www.yourbank.com/askus/

Or if you prefer, customer service specialists are currently awaiting your

call at 1-800-yourbank. Generally, wait times are less than two minutes except

during the peak hours of 8:00 AM to 9:00 AM.

Thanks again for your interest in yourbank.com. Based on current volume, we

should be able to respond to your question within 24 hours. Thanks for your

patience.

Yourbank.com E-Service

(800) 123-4567

Putting a Face on E-Service

We are not enamored with the idea of video conferencing for customer

service. Even with ubiquitous broadband, we’re not sure users really want to

look at the customer service rep as he or she works through a problem (and

we are certain users don’t want anyone looking at them). There may be some

big-ticket sales situations, such as mortgage applications or other

large-dollar investments, where user confidence is increased by seeing the

salesperson.

However, we do think there is a place for static personal information

such as name*, direct email address, and individual Web area where e-reps

can put a human touch on e-service and build rapport with his or her client

base.

________________________________________________________

*For privacy reasons, reps may want to use pseudonyms, an acceptable

practice online.

to front of mind for most banks, and why there is no silver bullet to solve poor customer experiences. Success, he explains, is a medley of understanding your customer, deploying new technology, and keeping your staff happy, too.

to front of mind for most banks, and why there is no silver bullet to solve poor customer experiences. Success, he explains, is a medley of understanding your customer, deploying new technology, and keeping your staff happy, too.