For the third year in a row, I traveled from Seattle to the L.A.-area to drop off my son at college. And for the third year in a row, Bank of America declined my card at Target, buying groceries and incidentals for him. And this time it was an EMV chip-card. Thank goodness I had my trusty Capital One card along, because it seems to do a far better job minimizing false positives (for fraud), at least for my account.

For the third year in a row, I traveled from Seattle to the L.A.-area to drop off my son at college. And for the third year in a row, Bank of America declined my card at Target, buying groceries and incidentals for him. And this time it was an EMV chip-card. Thank goodness I had my trusty Capital One card along, because it seems to do a far better job minimizing false positives (for fraud), at least for my account.

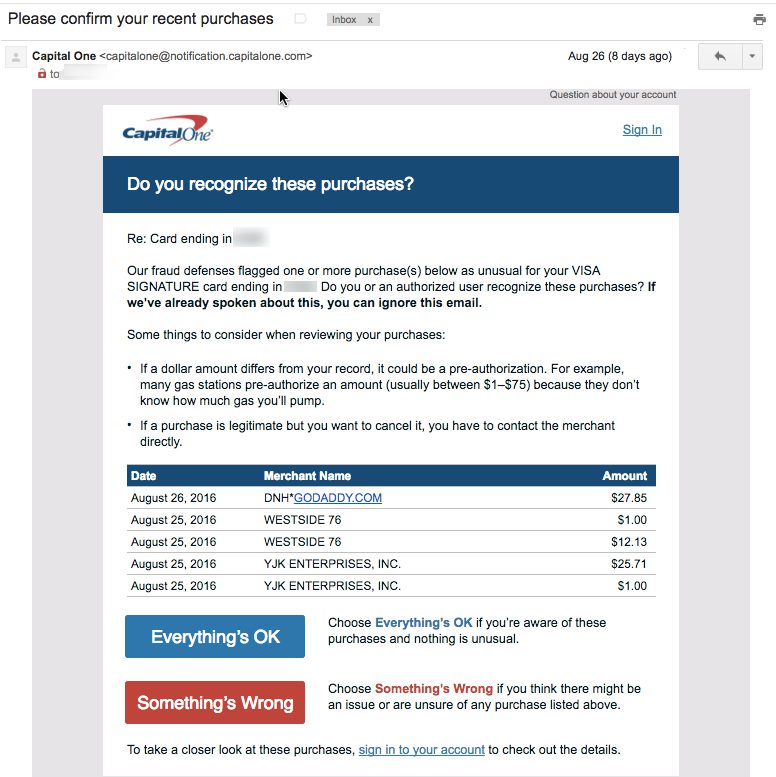

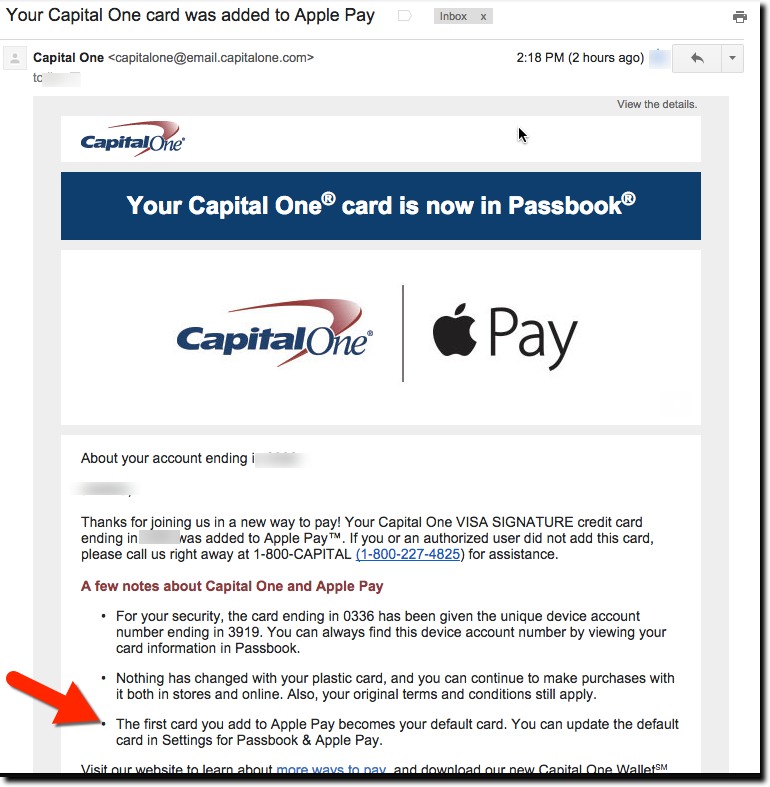

Capital One did have its concerns along the way, though. They sent the following email asking for confirmation that these gas-station authorizations were mine. And even though I didn’t respond right away, perhaps 12 to 18 hours later, they never shut off my card.

Bank of America also sent a similar email, but it arrived AFTER the card was declined. I understand the bank’s need to terminate suspicious transactions, but is it really that suspicious? For three years running, I’ve shown up in Los Angeles the last week of August (along with visits in between) and gone on a bit of a spending spree to stock my son’s dorm and now apartment (you’re welcome, boys!). Furthermore, I had already used the card to book an L.A. hotel, make some low-level but consistent charges along the way, coffee at Seatac, lunch in West L.A., and so on. But when I try to buy $150 in groceries at Ralph’s or Target, the card is declined, and worse, completely shut off from further purchasing.

Bottom line: My point here isn’t to complain about one issuer’s fraud-handling (although it felt good to get that off my chest), but to implore once again for more integration with smartphones to reduce false negatives. Specifically:

- Talk to me on the most immediate channel. Both banks sent emails, but I’m on the road, not checking emails. Pop a notification on the screen and send me a text message. Also, in instances of two account holders, make sure fraud alerts go to both (BofA emailed only my wife).

- Know me better. I get that Target in Tustin is outside my normal spending bubble. But I have a history of making charges in that area for 2+ years, so cut me a little slack.

- Better yet, know where I am. How many hundreds of millions could BofA save by tracking cardholder whereabouts in the background? I let Starbucks, Google, Yelp, and so on track my location. The benefits of them knowing where I am outweigh the privacy risks. The same goes for my bank.

——————–

Note: Looking forward to seeing everyone at Finovate this coming week. Let me know if there is anything you want to discuss ([email protected]).

Note: Looking forward to seeing everyone at Finovate this coming week. Let me know if there is anything you want to discuss ([email protected]).

Last week, Capital One launched a national marketing promotion with Uber that provides a 20% rebate on rides for one year. And unlike many (most?) card offers, it’s good for both new and existing Capital One customers. However, the ride-rebate applies only to the bank’s Quicksilver cash-back card, so I’m out of luck with my Capital One Venture card.

Last week, Capital One launched a national marketing promotion with Uber that provides a 20% rebate on rides for one year. And unlike many (most?) card offers, it’s good for both new and existing Capital One customers. However, the ride-rebate applies only to the bank’s Quicksilver cash-back card, so I’m out of luck with my Capital One Venture card.