This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Identity proofing and fraud detection company AuthenticIDlaunched a new solution today to detect deep fake and generative AI injection attacks.

An injection attack occurs when a fraudster injects a deepfake– which could be a synthetic document, video, facial image, or audio representation– into an identity verification workflow to spoof the system. This works to bypass traditional fraud detection and identity verification methods.

The company noted that it uses three, proprietary algorithms to prevent the majority of digital injection attacks that leverage AI-generated content. The three algorithms include visual fraud algorithms that detect counterfeit and synthetic elements, text fraud algorithms that detect errors within false documents, and behavioral algorithms that focus on activity during the ID capture and submission.

AuthenticID’s automated approach limits human bias and lag time from interfering in the detection and decisioning process. This enables the new solution to stop injection attacks and deep fake attacks in a matter of milliseconds.

“The widespread availability of inexpensive, easy-to-use tools allows bad actors to create highly convincing fake identity documents and biometrics,” said AuthenticID VP Product Management Alex Wong. “Recent news stories have shown just how devastating these attacks can be to any organization. Our deep fake injection attack solution meets a critical need to determine the legitimacy of a user in this new era of technology.”

Despite the new technology’s level of sophistication, the company notes that its new algorithms are not a “silver bullet” to defend against injection attacks. That’s because fraudsters are perpetually evolving their tactics to circumvent new security methods.

Founded in 2001, AuthenticID offers identity proofing, ID verification, biometric authentication, and fraud shield tools to support the fight against cybercrime. Additionally, the company’s Identity Fraud Taskforce continuously develops new algorithms to improve AuthenticID’s identity decisioning engine to help identify and stop fraud.

Munich, Germany-based Hawk announced an extension of its Series B funding round this week.

The amount of the extension was not disclosed. But the anti-financial crime regtech said that the investment did increase its valuation.

Hawk made its Finovate debut at FinovateSpring in 2022.

Germany-based regtech Hawkannounced an extension of its Series B funding round. The amount of the extension was not disclosed, but the company noted that the investment did significantly boost its valuation. The extension included funding from Rabo Investments, and also featured participation from existing investors BlackFin Capital Partners, Sands Capital, DN, Picus, and Coalition. Hawk will use the additional capital to fuel international growth and to help the firm meet growing demand for its AI-powered anti-financial crime solutions.

“We’re honored that Rabobank has recognized the significance of our technology and joins us in building a global market-leading enterprise, while also benefiting first-hand from our solutions and experience,” Hawk CEO Tobias Schweiger said. “I would also like to gratefully thank our existing investors for their ongoing support and look forward to continuing our partnership.”

Hawk, which rebranded from “Hawk AI” earlier this year, offers anti-money laundering (AML) and counter-the-financing-of-terrorism (CTF) technology that leverages explainable AI to detect more financial crime and reduce false positives. In fact, the company’s AI-powered technology delivers a 3x to 5x increase in risk detection and a 70% average reduction in the number of false positives. Banks, payments companies, and other financial services firms benefit from the ability to combine AML transaction monitoring, payment screening, and (Perpetual KYC) pKYC in a single solution that also includes powerful fraud prevention capabilities.

“Rabobank has been working with machine learning applications for many years,” Rabo Investments Managing Director Martijn Scholtes said. “What impressed us most about Hawk is that they’re delivering compelling results using explainable AI. Their advanced screening, detection, and monitoring capabilities align very well with our mission to build a more secure and robust financial ecosystem.”

Founded in 2018 and headquartered in Munich, Germany, Hawk AI made its Finovate debut at FinovateSpring 2022. At the conference, the company demoed its AML Surveillance Suite, which leverages traditional rule-based models and AI to provide financial institutions with next generation AML compliance. “AI should be used to achieve three major outcomes,” Hawk GM of North America Steve Liú explained at the event, “one, finding suspicious and risky behavior that peer rule systems simply cannot; two, decrease the number of false positives drastically by using behavioral profiling on top of existing rules; and third, that all of this is fully explainable for operators and auditors, and available to our users on a platform allowing for secure information sharing.”

Hawk began the year by appointing former HSBC executive Michael Shearer as its Chief Solution Officer. Less than a month later, the company introduced new APAC General Manager Robin Lee, formerly of Napier. In February, Hawk won the XCelent Advanced Technology 2024 award and, in May, the company earned a spot on the 2024 FinTech Global Fincrime Tech 50.

Austin, Texas-based cybersecurity firm SpyCloud has raised $35 million in financing.

The capital will be used to expand the company’s solutions to help businesses investigate and defend themselves against cybercrime in general and account takeover fraud in specific.

SpyCloud won Best of Show in its Finovate debut at FinovateFall 2017 in New York.

In a round led by CIBC Innovation Banking, Texas-based cybersecurity company SpyCloud has secured $35 million in growth financing. The investment follows SpyCloud’s $110 million Series D fundraising from August 2023, and will be used to expand the firm’s solutions to help businesses investigate and defend themselves against financial crime.

“As the threat landscape continues to evolve, it’s imperative that digital identities are well protected since they’re the entry point for so many targeted attacks,” SpyCloud CEO and Co-Founder Ted Ross said. “Building automated solutions that combat cybercrime has been our vision since day one, and the financing we received from CIBC Innovation Banking will allow us to continue innovating and growing.”

SpyCloud’s total capital raised stands at more than $203 million, according to Crunchbase. CIBC Innovation Banking is the investment division of Canadian Imperial Bank of Commerce.

SpyCloud specializes in helping firms combat account takeover. The company’s platform scans and analyzes data from breaches, devices infected with malware, and the dark web to find employee login credentials that have been exposed. SpyCloud leverages this data to provide companies with actionable insights to enable them to blunt fraud losses, stop ransomware attacks, and fully investigate cybercrime incidents as they occur.

With customers ranging from Uber, Zscaler, and Samsonite to LendingTree, Canva, and the University of Oklahoma, SpyCloud recaptures 40 million exposed assets every week. The company’s technology seamlessly integrates into a variety of identity response and orchestration systems including Active Directory, Okta, Microsoft Sentinel, Splunk, and more.

Founded in 2016, SpyCloud won Best of Show in its Finovate debut at FinovateFall 2017 in New York. Headquartered in Austin, Texas, the company has more than 550 customers around the world and has recaptured more than 560 billion identity assets. This spring, SpyCloud released its 2024 SpyCloud Identity Exposure Report, which indicated that more than 60% of all data breaches in 2023 were malware related.

“Threat actors are linking together identity records from hundreds of sources to impersonate their victims,” SpyCloud Chief Product Officer explained, “making it extremely difficult for platforms to differentiate between legitimate users and criminals.”

To this end, the report indicates that there is plenty that individuals can do to make it harder for them to be the victim of stolen credentials. Foremost among these strategies is better password hygiene. SpyCloud recaptured nearly 1.8 billion passwords from dark web sources in 2023 alone – a year-over-year increase of more than 80%. Unfortunately, it is not difficult to see how. Beneath a subhead titled, “The U.S. government continues to struggle with bad password practices,” the report observed “the most common passwords associated with .gov emails were password, pass1, and 123456.”

This week’s edition of Finovate Global takes a look at recent developments in the fintech industry of the United Arab Emirates (UAE).

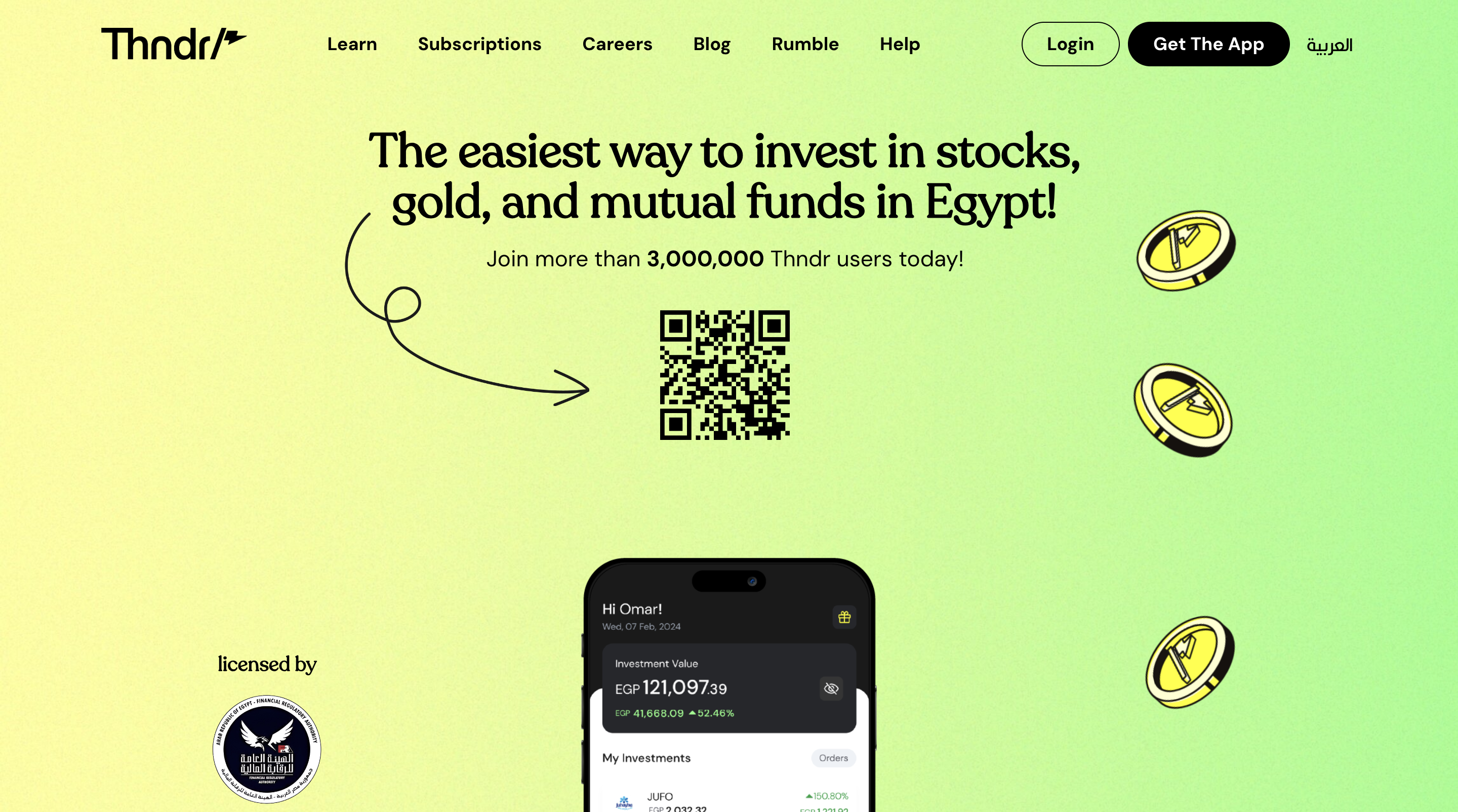

Thndr, a digital investment platform based in Egypt, announced an expansion to the United Arab Emirates (UAE) this week. The expansion comes after the company secured a Category 3A license with retail endorsement from the Abu Dhabi Global Market (ADGM) Financial Services Regulatory Authority (FSRA). Thndr will initially offer investors in the UAE direct access to U.S.-listed securities, such as stocks, including fractional shares, as well as exchange-traded funds (ETFs).

“We at Thndr are thrilled to announce our official entry into the UAE market,” Thndr UAE General Manager Salah Kaddoura said. “We’d like to express our sincere gratitude to the FSRA for their openness and for welcoming Thndr to the UAE’s dynamic financial landscape.”

Founded in 2020 and a graduate of the Y Combinator accelerator, Thndr got its start as a commission-free, mobile trading platform for stocks, bonds, and funds. That year, Thndr became the first firm to earn a brokerage license in Egypt since 2008. The company went on to launch a new solution to enable trading in mutual funds and, in 2022, raised $20 million to fuel regional expansion.

With more than three million downloads and 500,000 active monthly users, Thndr notes that Egyptians traded $1.8 billion on its platform in 2023. As of this April, Thndr accounted for 8.5% of all retail transactions in the market. The company also reported that 87% of its users are first-time investors. “I take pride in seeing how our commitment to these principles has democratized investing to all Egyptians,” Kaddoura said, “and can’t wait for what we have in store for the UAE.”

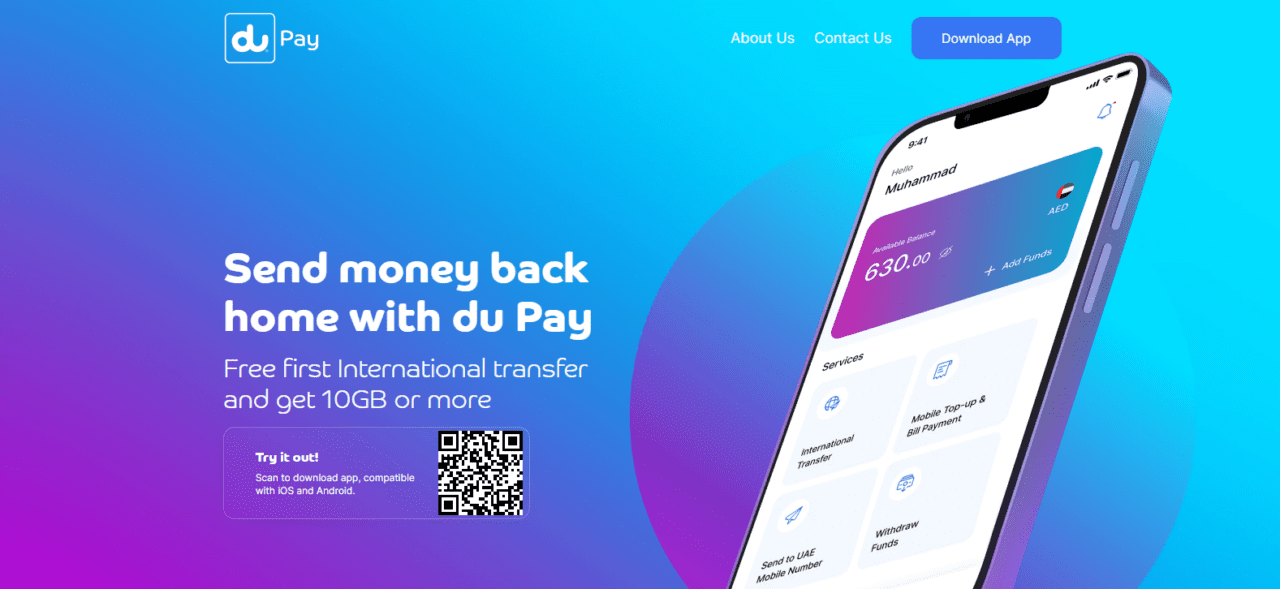

du Pay, the digital payments division of UAE-based telecommunications company du, has formalized a partnership with digital payments giant Visa. The partnership will enable du Pay to issue Visa cards, grow its suite of financial solutions, and bring greater versatility to the du Pay platform.

“We are committed to making payment processes faster, simpler, and more secure while simultaneously enhancing financial inclusion,” du Pay CEO Nicholas Levi said. “The strategic collaboration is poised to accelerate digital empowerment with a focus on inclusivity and serve the needs of those without traditional banking services, ensuring simplified access to products.” For its part, Visa highlighted the impact of the partnership – and du Pay’s new prepaid Visa card – on the growth of digital commerce in the region.

du launched its du Pay solution earlier this year. The technology, available in six languages, offers international money transfers, P2P transfers, billpay, and a unique IBAN for each customer. The company plans to add a card feature “soon.”

Clarity on the role of Open Finance in the fintech and financial services industry of the UAE has arrived in the form of a new, comprehensive framework issued by the country’s Central Bank (CBUAE). The framework provides guidance on how to regulate licensing, supervision, and operation of Open Finance and has already received positive reviews from industry participants.

The CBUAE earned especially high marks for its emphasis on security and customer consent. One observer, Women in Crypto Arabia founder Zina Ashour said the framework “puts power back in the hands of the consumer.” Others, such as Tarabut Gateway CEO Abdulla Almoayed, were grateful for the regulatory clarity and certainty, adding that the “reduction in ambiguity” will enable his firm “to invest in the UAE with supreme confidence.”

Still further plaudits came for the comprehensive nature of the CBUAE’s decision. The UAE’s Open Finance Regulation includes, for example, both Open Banking and Open Insurance, as Global Ventures partner Said Murad observed. Murad also appreciated the fact that the regulation requires all entities licensed by the CBUAE to comply with its requirements for data sharing and service initiation.

Here is our look at fintech innovation around the world.

Middle East and Northern Africa

Brokerage-as-a-Service innovator DriveWealthforged new partnership with Turkish fintech Papara.

Crédit Agricole Next Bank has launched a new lead management platform and CRM courtesy of a partnership with InvestGlass.

The new offering will help the bank deal with new customer growth and increasing linguistic diversity among its clients and employees.

Switzerland-based InvestGlass most recently demoed its sales and compliance automation technology at FinovateEurope in February.

Courtesy of a partnership with sales and compliance automation solution provider InvestGlass, Crédit Agricole Next Bank has launched its new lead management platform and CRM. The offering, unveiled this spring, will help the institution enhance the customer experience as well as automate internal processes for employees.

“The deployment of InvestGlass within Crédit Agricole Next Bank represents more than just a technical improvement,” Crédit Agricole Next Bank Deputy Director of Development Maxime Charton said. “It’s a cultural transformation that allows the bank to continue innovating and improving its digital journeys for the benefit of its clients.”

One of the key ways that Crédit Agricole Next Bank will leverage its new technology is to help the firm deal with the linguistic diversity that characterizes both its customers and staff. With more than four languages to contend with, the institution will benefit from InvestGlass’s flexibility and automation capabilities, which will enable Crédit Agricole Next Bank to provide personalized experiences even as its clientele grows.

Additionally, InvestGlass will help the institution fulfill its goal of digitalizing the lead management process, with appointment scheduling, prospect flow automation, and mailing tools integrated into the platform. This will make it easier for Crédit Agricole Next Bank to monitor and manage its communications more effectively across multiple channels.

“InvestGlass allows us to optimize our operational efficiency while significantly improving our clients’ experience,” Crédit Agricole Next Bank Director of Online Agency Stephane Graeffly said.

Headquartered in Geneva, Switzerland, InvestGlass made its Finovate debut at FinovateEurope in 2016 and returned to the Finovate stage most recently for FinovateEurope earlier this year. At the conference, the company demonstrated its automation solution for sales and compliance that helps banks, brokers, government agencies, and crypto companies become more productive with a non-U.S. CRM option.

InvestGlass’s partnership announcement comes a month after the company unveiled a pair of new AI solutions, Copilot and Mistral, to help businesses convert unstructured data into conversational knowledge and actionable insights. Copilot is the cloud-based option that allows companies to use their OpenAI API key. Mistral is InvestGlass’s local server/on-premise offering.

InvestGlass was founded in 2014. Alexandre Gaillard is CEO.

U.K.-based insurtech Eleos has secured $4 million in seed funding.

The round was led by Fuel Ventures and Indico Capital. Early-stage investor APX also participated.

Eleos made its Finovate debut earlier this year at FinovateEurope in London.

Eleos, an insurtech and income protection provider based in the U.K., has raised $4 million in seed funding. Fuel Ventures and Indico Capital led the round, with Berlin-based early-stage investor APX also participating. Eleos made its Finovate debut earlier this year at FinovateEurope in London.

“With our new funding we will launch more lines of insurance in the life and disability verticals and strike more distribution partnerships in the U.K.” Eleos CEO and Co-Founder Kiruba Eswaran said. “Part of the funding is also earmarked to launch operations in the U.S.”

Eleos embeds white-labelled life insurance and income protection into the online journeys of financial brands. These services and products give Eleos’s partners the ability to benefit from new revenue streams as well as more thorough customer engagement and greater customer retention. Eleos’s FCA authorization also provides its partners – companies like Loqbox, CreditSpring, and Updraft – with full regulatory coverage. Eleos customers also get a variety of free benefits, including 24/7 remote GP services and mental health support.

Fuel Ventures founder Mark Pearson credited Eleos for its experience, understanding of the industry, and access to a substantial market. “With Eleos we’ve found all three and we believe their products encapsulate our thinking about the insurance space – giving people easy access on familiar platforms.”

Founded in 2023, Eleos has already served more than 20,000 customers in the U.K. The company offers personalized and dynamic quotes for its insurance product, and enables potential customers to choose an affordable monthly payment plan and buy their insurance policy in minutes. Additionally, Eleos’s income protection solution helps individuals cover their essential expenses in the event of an illness or injury that requires long-term sick leave. Currently offering embedded insurance for brands, Eleos is planning to offer insurance policies directly to individuals in the future.

“The insurtech market has plenty of room to grow and Eleos is targeting areas which are not only sizable but overlooked by other current players globally,” Indico Capital Partners Managing General Partner Stephan Morais said.

AMLYZE, a regtech specializing in combating financial crime that made its Finovate debut at FinovateEurope earlier this year, has forged a strategic partnership with Aura Cloud. Headquartered in Lithuania, AMLYZE offers anti-financial crime solutions for a variety of financial services providers, including fintechs, banks, and cryptocurrency firms. The company’s partnership with Sweden-based Aura Cloud will combine the latter’s expertise in financial crime prevention with the former’s digital banking solutions.

AMLYZE Co-Founder and Head of Partnerships Jekaterina Govina praised Aura Cloud for its “commitment to agility and innovation” which Govina said “aligns perfectly with our mission to provide AML/CFT solutions, built by regulatory insiders who understand customer pain points from the inside out.” Govina added, “Together, we will empower financial institutions to stay ahead of the curve in the fight against financial crime.”

AMLYZE leverages AI, synthetic data, and the power of the network to offer a paradigm-shifting approach to AML. The AMLYZE platform’s use of synthetic data and privacy enhancing technologies (PETs) enables aggressive adoption of AI and machine learning techniques and strategies that do not violate confidentiality or breach data privacy. The company’s technology can be deployed to provide real-time and retrospective transaction monitoring, customer risk assessments, AML/CFT investigations, and PEP, sanctions, and negative media screening. Moreover, AMLYZE’s model facilitates not only effective financial crime detection, but also AI model training, testing of automated solutions, and AML staff training.

“(AMLYZE’s) automated transaction monitoring and customer risk assessment solution provides additional possibilities for our core banking platform customers to have (a) state of the art solution to minimize financial crime and enhance compliance,” Aura Cloud CEO Prem Bhagwat said. “We see this partnership as an excellent addition to our current partnership ecosystem in Northern Europe and beyond.”

Headquartered in Vilnius, Lithuania, AMLYZE made its Finovate debut earlier this year at FinovateEurope 2024 in London. The company has raised $1 million (€1 million) in pre-seed funding, courtesy of an investment round led by Practica Capital, a major venture capital firm based in the Baltics, and FIRSTPICK, a Baltics-based accelerator and venture capital fund.

Trulioo and Mastercard have partnered to help clients streamline onboarding while combatting fraud.

Trulioo will leverage Mastercard’s identity solutions to gain insight into identity and risk scores.

Mastercard will tap Trulioo’s global business identity verification services to enhance its Onboard Risk Check product by adding a layer of assurance to merchant and consumer onboarding solutions.

Global identity platform Truliooannounced today it has teamed up with Mastercard to help merchants streamline digital onboarding while helping them combat fraud.

Under the agreement, Trulioo will leverage Mastercard’s identity solutions to power two of its products– Person Match and Risk Intelligence. This will offer Trulioo insights into identity and risk scores through a customizable, intuitive dashboard, extending the company’s offerings beyond API-based products and further enhancing its onboarding processes.

“Trulioo is proud to partner with Mastercard and shares their dedication to industry-leading business verification and fraud prevention,”said Trulioo CEO Steve Munford.“As organizations navigate the complexities of the digital payments industry, fraud and business identity theft are constant threats. This is a pivotal milestone in our joint endeavor that will pave the way for a more secure global digital landscape.”

Mastercard will also see benefits from the strategic partnership. Trulioo’s global business identity verification services will enhance Mastercard’s Onboard Risk Check product by adding a layer of assurance to merchant and consumer onboarding solutions, helping to mitigate risk, reduce fraud, and increase trust in payments made across the globe.

“The digital economy thrives when people trust it and trust each other,” said Mastercard executive vice president, Identity Products, and Innovation Dennis Gamiello. “The ability to verify people are who they say they are instills confidence on both sides of digital interactions. Together with Trulioo, we are fueling the connections that make a vibrant digital economy possible.”

Canada-based Trulioo was founded in 2011 to help organizations navigate compliance by offering real-time verification of more than 13,000 ID documents and 700 million business entities across the globe, while checking against more than 6,000 watchlists. The company has raised $475 million.

Customer engagement company JRNI has integrated with bank technology innovator Backbase.

The integration will bring new appointment scheduling functionalities to users of Backbase’s Engagement Banking platform.

Headquartered in Amsterdam, Backbase has been a Finovate alum since 2009.

JRNI, a leader in global customer engagement for financial services, has integrated with Backbase, adding new appointment scheduling functionalities to the Backbase Engagement Banking Platform.

“We believe that the banking experience is enriched by building trust through personal connections,” Backbase general manager of ecosystems Roland Boojien said. “This partnership aims to seamlessly provide convenient personal connections in banking and wealth management, effortlessly uniting customers and trusted advisors at their preferred time and location.”

Backbase’s Engagement Banking Platform provides financial institutions (FIs) with a range of digital solutions for customer onboarding, servicing, financing origination, loyalty, and more – all from a single platform. Courtesy of the integration, financial institution customers on the platform will be able to book both virtual and in-person appointments seamlessly and securely. JRNI’s Self-Scheduling Appointment booking solution will give FIs the ability to offer an end-to-end embedded experience that begins with initial customer contact and continues through the customer’s entire journey with ongoing relationship management and support.

The Self-Scheduling Appointment booking solution will be available as an out-of-the-box add-on integrated within Backbase’s Digital Assist offering. Digital Assist provides a unified solution that helps customer-facing teams at FIs resolve customer service issues quicker, as well as upsell additional products and services easier.

“Backbase Digital Assist helps make interactions more efficient, effective, and of higher value,” JRNI CEO Phil Meer said. “JRNI’s engagement capabilities complement Backbase’s offering to drive trusted connections and relationships. Backbase shares our vision and its global platform prioritizes customer engagement as a critical pillar.”

Founded in 2008 and based in Boston, Massachusetts, JRNI offers a customer engagement platform that helps companies improve both customer acquisition and retention, as well as promote brands, drive hyper-personalization, and better engage target audiences. The company’s enterprise-grade event management platform handles scheduling, queuing, and analytics to provide customers with a personalized experience whether in-person or virtual.

Headquartered in Amsterdam, Backbase has been a Finovate alum since 2009. Most recently demoing its technology at FinovateFall 2021 in New York, the company has won Best of Show on four separate occasions. With more than 150 customers and 2,000+ employees around the world, Backbase provides a platform that enables financial institutions to offer their customers the latest fintech innovations without having to abandon their existing core banking systems.

Backbase’s JRNI announcement comes just days after the firm announced that Malaysia’s Bank Muamalat Malaysia Berhad (Bank Muamalat) had agreed to a long-term partnership designed to “revolutionize” the bank’s digital Islamic Banking offerings. Also participating in the partnership is fellow Finovate alum, Mambu.

FintechOS received a $60 million investment, boosting its total funding to over $151 million.

FintechOS will use the new funds to accelerate its global expansion.

In the announcement, FintechOS revealed it experienced 40% year-over-year revenue growth in 2023 and said it expects to break even in 2024.

Financial product management platform FintechOS recently announced it received a $60 million Series B+ investment, boosting its total funding to more than $151 million. Molten Ventures, Cipio Partners, and BlackRock led the round, while existing investors EarlyBird VC, OTB VC, and Gapminder VC also contributed.

FintechOS serves up technology that helps organizations launch and manage financial products and services without having to replace their existing core infrastructure. The company offers low-code/ no-code tools to help organizations extend the capabilities of their existing core, launch new products, improve their customer experience, and optimize back-office workflows across lending, savings, insurance, investment, and embedded finance operations.

While FintechOS will use the funds to accelerate its global expansion, the New York-based company has already made significant progress towards global growth. The company operates globally, with a presence in Europe, North America, and Asia. FintechOS is available in the U.K., the U.S., Canada, Germany, France, the Netherlands, Romania, Spain, Italy, Poland, Belgium, Australia, Singapore, and others.

“Securing this investment is a testament to the confidence our investors have in our vision and execution,” said FintechOS Co-founder and CEO Teo Blidarus. “Our rapid growth and operational improvements reflect the demand for our next-generation financial product management solutions. We are revolutionizing the financial services industry by providing technology that enables core modernization and drives innovation.”

Since Blidarus co-founded FintechOS in 2017, the company experienced 40% year-over-year revenue growth in 2023 and has seen a 170% increase in operating margins. The company expects to break even in 2024. Following its recent $15 million funding round in early 2022, FintechOS has achieved over 300% growth, expanding its client base to 50 global clients. This growth includes high-profile additions such as Société Générale, Admiral, Benenden Health, Avant Money, and Vibrant Credit Union.

“FintechOS’s growth trajectory is a clear indicator of their potential,” said Cipio Partners Managing Partner Roland Dennert. “We are delighted to be part of this journey and look forward to seeing the transformative impact they will make in the financial services sector. Their commitment to modernization and innovation aligns perfectly with our investment strategy.”

As organizations struggle to adapt to changing consumer expectations and new technologies while maintaining their legacy core infrastructure, technologies such as FintechOS’ will see increasing growth. That’s because many traditional players in the space continue to operate using old computer languages such as COBOL, which was developed in 1959 and does not interface easily with modern fintech solutions.

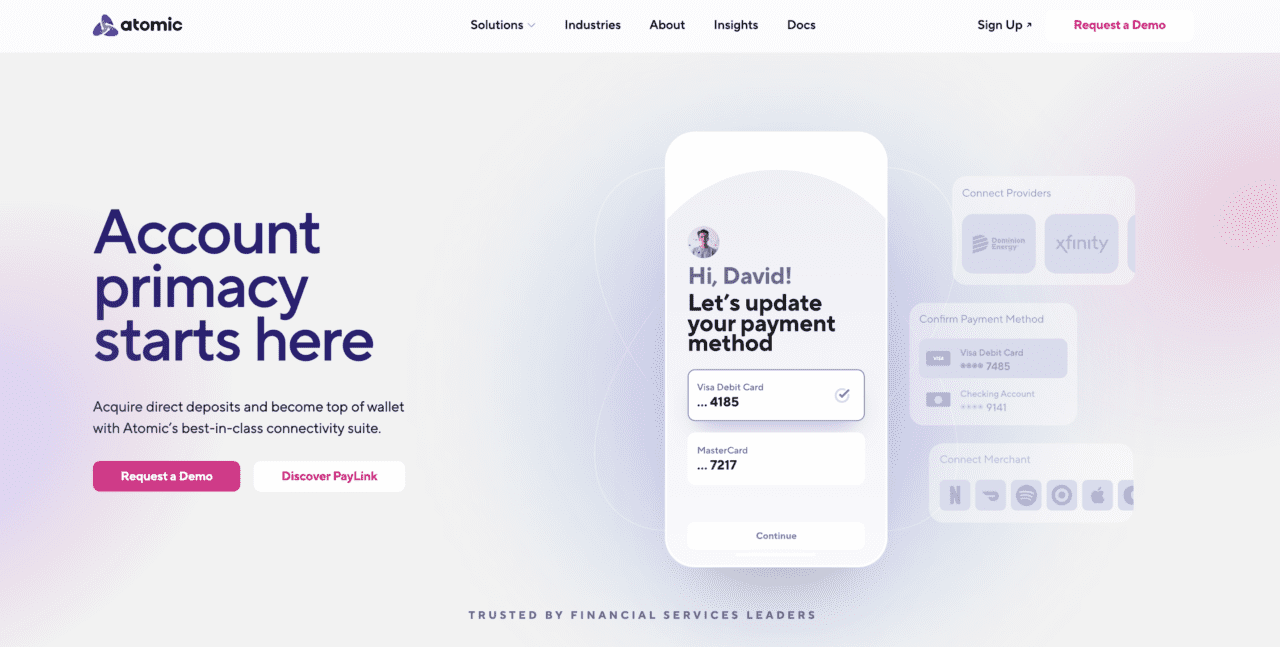

The new offering for financial institutions enables users to monitor recurring payments and make real-time changes from within their banking app.

Atomic most recently demoed its technology earlier this month at FinovateSpring in San Francisco.

Payroll connectivity innovator Atomicunveiled its latest offering: PayLink Manage. The new solution is an actionable subscription management tool for financial institutions that enables users to monitor recurring payments and make real-time changes from within their banking app.

“By integrating PayLink Manage, banks can not only improve their service offerings and increase engagement, but also can solidify themselves as the primary banking relationship,” Atomic CEO and Co-Founder Jordan Wright said. “When banks help their account holders with innovative insights that are actionable, everybody wins.”

PayLink centralizes and automates oversight and control of recurring payments. Users can connect, view, and track a variety of payment types from subscriptions and bills to streaming services and mortgage payments. PayLink Manage also enables users to make real-time changes to their subscriptions directly within the banking app. Additionally, courtesy of Atomic’s direct connectivity, financial institutions can gain insights into usage data, itemized receipts, and other key subscription information. This facilitates deeper analysis, driving more personalized guidance that helps users save money.

“PayLink leverages Atomic’s proven technology, which has already facilitated millions of secure connections across financial platforms,” Atomic Chief Product Officer Andrea Martone said. “With this launch, we are extending our trusted, robust connectivity framework to subscription management, providing financial institutions with a tool to enhance customer engagement and improve retention by helping people take action to improve their financial outcomes.”

Headquartered in Salt Lake City, Utah, Atomic made its most recent Finovate appearance earlier this month at FinovateSpring in San Francisco. At the conference, the company demoed its subscription management technology, which leverages its access to payroll, HRIS systems, and merchants to support a range of financial services, including direct deposit switching, income and employment verification, and more. Founded in 2019, Atomic has raised more than $68 million in funding from investors, including ATX Venture Partners and Portage Ventures.

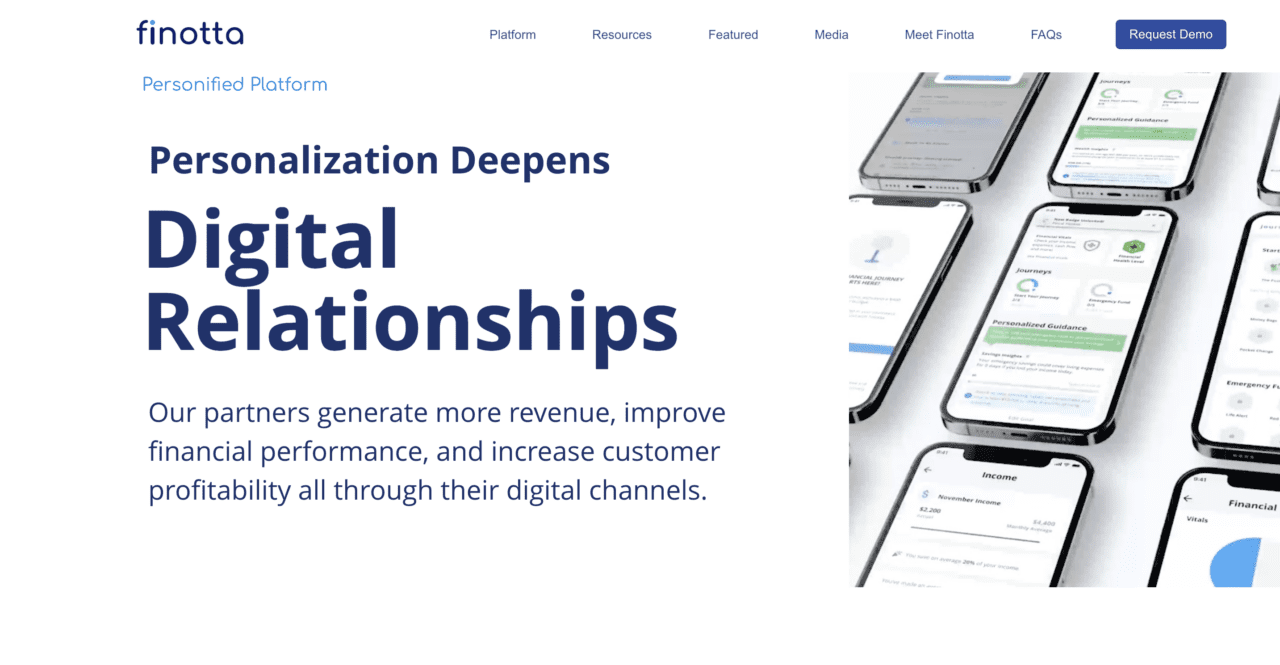

Embedded finance and digital banking solutions provider Finotta has announced a strategic partnership with Constellation Digital Partners (Constellation).

Constellation will integrate Finotta’s Personified platform into its own solution to help credit unions offer personalized financial guidance to their members.

Finotta made its Finovate debut at FinovateFall 2022 in New York.

Embedded finance and digital banking solutions provider Finottaforged a strategic partnership with Constellation Digital Partners (Constellation). A cloud-native digital banking services provider, Constellation will integrate Finotta’s Personified platform into its own solution to give credit unions new resources to boost member engagement and satisfaction, as well as drive digital growth.

“More than 90% of consumers expect their financial institution to offer a modern digital banking platform, but this is table stakes,” Finotta Founder and CEO Parker Graham said. “The key is differentiating the experience based on what members need and want, which is financial guidance. Unfortunately, this is also where massive missteps are made. Many traditional PFMs inadvertently shame consumers for poor financial habits rather than encourage positive behavior, killing the overall experience. As a result engagement is down considerably.”

Founded in 2018 and headquartered in Overland Park, Kansas, Finotta made its Finovate debut at FinovateFall 2022 in New York. At the conference, the company demoed Personified, a suite of products that enable FIs to provide personalized financial guidance via their mobile banking apps. Personified helps financial institutions anticipate member and customer needs, increase product conversions, and deliver actionable financial guidance – all in a single solution. The platform helps banks and credit unions leverage the digital channel to generate more revenue, improve financial performance, and boost profitability for members and customers.

Last year, Finotta noted that its Personified platform had increased user engagement compared to other mobile banking apps, with an average use of 13 minutes per month per user. According to Graham, this compares favorably to the “less than one minute per month” that users spend on the average mobile banking app. Not only does this reflect a significant lack of engagement from users, it also limits the FIs ability to cross-sell other products and services. Finotta also pointed to a study from Oracle that suggested as much as 40% of customers believe that independent PFM apps are superior to the offerings provided by most financial institutions.

“Embedded (Finotta’s) technology into our platform will equip credit unions with the tools they need to thrive in the digital age while delivering personalized, seamless, and exceptional service to their members every step of the way,” Constellation SVP and Head of Product Aaron Oplinger said. “We look forward to the value this will bring our industry.”

Founded in 2017 and headquartered in Raleigh, North Carolina, Constellation Digital Partners is a leading provider of mobile and digital banking solutions for community-based financial institutions. The company is dedicated to empowering both credit unions and community banks with innovative solutions for mobile banking, online account management, personalized financial insights, and more. The company has raised $17 million in funding via a Series A round completed in 2020. Kris Kovacs is President and CEO.