Doug Parr, Vice President, D3 Banking reveals the features that banks and credit unions should include in the products and services that they offer for small business owners’ unique needs.

Doug Parr, Vice President, D3 Banking reveals the features that banks and credit unions should include in the products and services that they offer for small business owners’ unique needs.

As bankers juggle strategic issues and priorities such as compliance, mobile banking, channel strategy, etc., it’s easy for small business banking to be put on the back-burner. However, if ignored for too long, banks and credit unions risk missing out on the benefits to be gained from serving this important segment of their customer base.

Only 39 percent of small businesses have full-time staff to manage bookkeeping, accounting, and finance, while only 42 percent have the staff to manage payments and cash flow, leaving small business owners largely without help. There are 29 million small businesses in the United States, representing an engine that drives a significant amount of the nation’s economic growth.

Many institutions today simply offer a ‘lite’ version of their treasury management solution for small business, or expect owners to ‘make do’ with the features available in their consumer banking option, neither of which fit small businesses’ needs.

Because small business owners are beginning to vote with their feet – one institution I know is seeing more than 10,000 of these individuals leave annually – more banks and credit unions are looking for ways to offer products and services specifically designed for small business owners’ unique needs. The following is a list of the kind of features small business owners have identified as priorities.

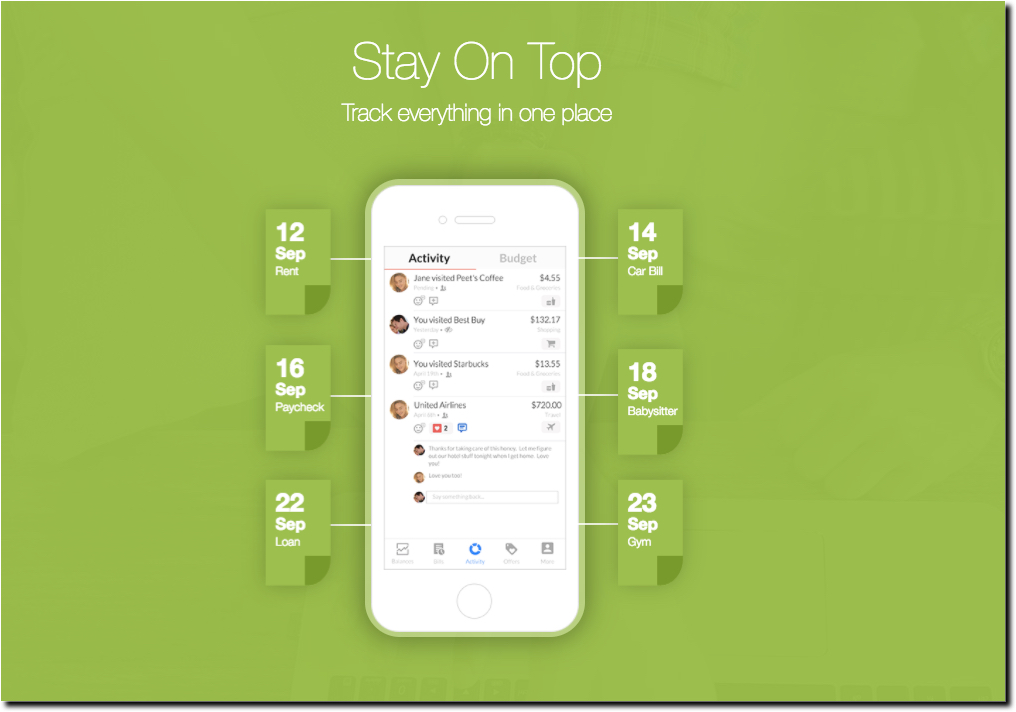

A single, convenient view

One thing most small business owners are consistently lacking is time, making it especially important for small business offerings to be mobile friendly as possible. These offerings should also include time saving elements that make the experience optimally quick and easy.

For example, small business owners often have more than one account at their primary bank or credit union between numerous business and personal accounts. A single integration view that allows small business owners to toggle between all accounts without the friction of repeated logins provides a quicker way for them to move between accounts. This capability also gives more incentive for small business owners to use a single institution for all of their banking needs, strengthening relationships and creating additional revenue opportunities for the financial institution.

Advanced entitlement options

Small business owners typically will delegate more administrative aspects of banking to their employees. However, because current offerings largely lack secure permissions, owners are often hesitant to share these duties.

This makes entitlement options another necessity for small business offerings. Allowing small business owners to determine who has access to financial details, payroll information and bill pay functions gives them a way to divide tasks while avoiding risk. These entitlements should include the proper limits, controls and alerting options to notify owners when activities must be approved.

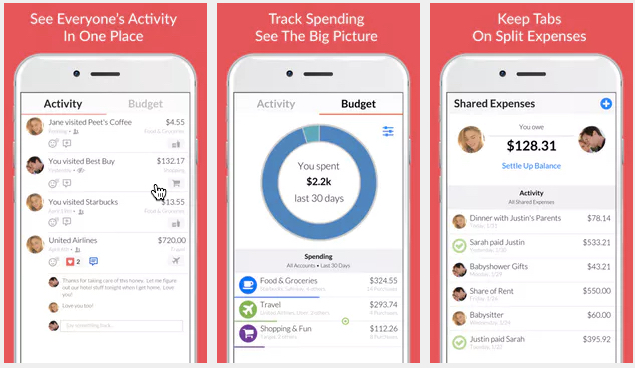

More automated reporting and actionable information

The most common cause of small business failure is the lack of time and knowledge to run operations successfully. Financial institutions should help small businesses with this pain point by providing comprehensive, easily digestible information about these organizations’ financial positions to help them allocate resources and plan for the future. This includes categorizing a business’s financial activity to provide detailed insights about income and expense trends.

Income, cash flow and balance sheets should be automatically populated for review and exported as needed. This data can also be leveraged for banks to provide predictive cash flow and push proactive alerts for potential red flags.

Simplified money movement options

Small businesses depend on successful and timely payments, but they shouldn’t be burdened with having to understand the specific money movement route, or the accompanying parade of acronyms such as P2P, A2A, ACH, etc. Banks and credit unions must offer simple money movement options that only require the customer to know where to send the money, how much to send and when it should arrive. This method of moving money is similar to shipping a package via UPS, quick and easy.

The small business segment has the potential to be a profitable and loyal customer base if banks and credit unions stop repackaging services that do not fit small business owners’ needs, and start tailoring services built specifically for them. Failure to do so will result in these organizations continuing to head for the exit, taking their money and loyalty with them.