This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Data-driven marketing company Cardlytics is reinforcing its troops for the new year. The Atlanta-based company has appointed Sathish Gaddipati as Chief Technology Officer.

Gaddipati has been promoted to the new role, having previously served as Cardlytics’ Senior Vice President and Head of Technology. As CTO, Gaddipati is charged with leading platform engineering, technical product management, software development, data engineering, quality assurance, and IT operations.

Gaddipati, who has been with Cardlytics for a year, said that he realized the company “was the perfect fit for me.” He added, “It’s incredibly gratifying that our combined efforts have allowed us to continue providing sophisticated technology to leading financial institutions, and I look forward to working on exciting future developments.”

Prior to joining Cardlytics, Gaddipati, who has an MS in Industrial Management from the Indian Institute of Technology, held roles at The Weather Channel, The Walt Disney Company, NCR Corporation, InterContinental Hotels Group (IHG), Sun Microsystems, and Omnitracs.

Founded in 2008, Cardlytics has raised $203 million in funding. The company demoed its geolocation application at FinovateFall 2013. In 2016, Cardlytics analyzed approximately $1.3 trillion in U.S. purchase spend. Scott Grimes is CEO and cofounder.

If the idea of a hacker getting access to your bank account is scary, imagine learning that a cybercriminal has hacked into your 401(k).

That’s the kind of anxiety independent robo advisor blooom is guarding against with the introduction of its new Suspicious Activity Alerts feature. The technology continuously monitors user’s 401(k), 403(b), and similar employer-sponsored retirements accounts for withdrawals or loans. If suspicious activity is detected, the solution sends the customer an alert by text message.

“The 401(k) is often a person’s single largest financial asset,” blooom CEO and co-founder Chris Costello said. “bloom is committed to safeguarding your right to retire. Whether it’s exposing and minimizing hidden investment fees or identifying suspicious activity, blooom serves one person: the individual.”

Founded in 2013, blooom demonstrated its robo advisory platform at FinovateFall 2014. Geared specifically for the employer-sponsored retirement market, Blooom provides free 401(k) analysis and charges a flat fee of $10 a month for basic 401(k) management and monitoring – including the Suspicious Activity Alerts feature. Additional 401(k)s can be added for $7.50 per month. Blooom automatically rebalances and adjusts the investment allocation based on the user’s general investment preferences (i.e., stock vs. bond mix) and goals (i.e., time-until-retirement). The company also offers access to human financial professionals to provide planning advice beyond the 401(k).

Blooom’s approach seems to be working. The company announced last fall that it surpassed the $1 billion assets under management milestone, doing so faster than any other independent robo advisor including both Betterment and Wealthfront. In a blog post discussing the milestone, Costello pointed to the application of readily available technology to the often-overlooked world of employer-sponsored retirement accounts as key to blooom’s growth and success.

“There has been ‘off-the-shelf’ technology that has existed for upwards of 10 years that can automate things like the construction of a portfolio allocation, rebalancing a portfolio, and even tax-loss harvesting,” Costello wrote. “But nothing existed to perform this kind of automation when it comes to the 401(k) space – where accounts are spread out over dozens and dozens of different financial institutions. Until now.”

With more than $13 million in total funding, blooom includes QED Investors, Industry Ventures, Commerce Ventures, Allianz Life Insurance, TTV Capital, and Nationwide Insurance among its investors. The company is based in Overland Park, Kansas.

SynapseFiannounces support for interchange processing for debit and credit card transactions.

This post will be updated throughout the day as news and developments emerge. You can also follow all the alumni news headlines on the Finovate Twitter account.

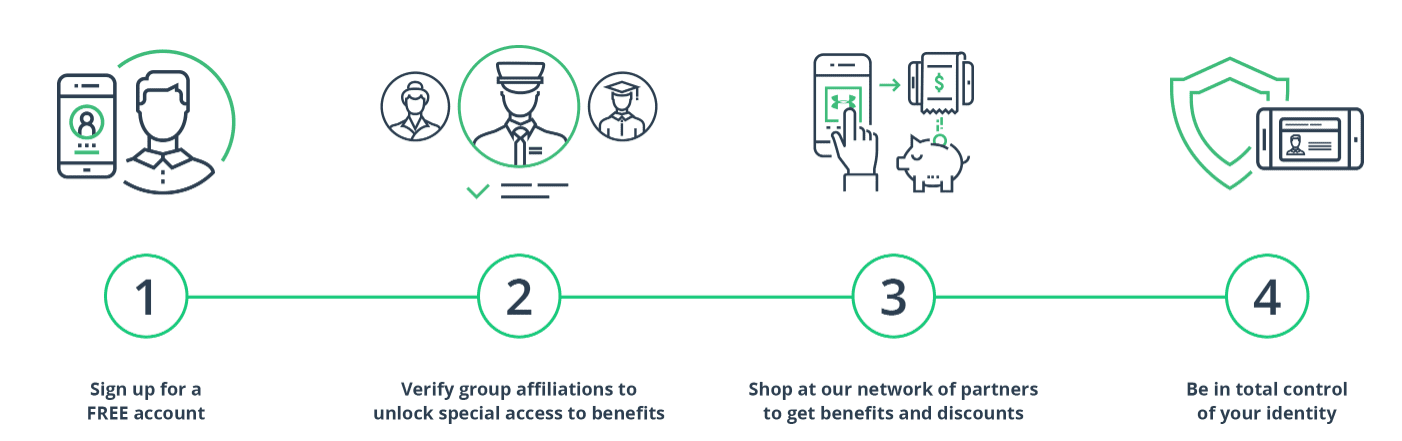

Identity management platform ID.me has landed a new client this week. Veterans for Foreign Wars of the U.S. (VFW) can now offer its members a more streamlined and secure online experience with ID.me’s single-sign on capabilities.

After VFW members sign up for an account at ID.me, the Virginia-based company issues them a single username and password. Members use these credentials to log in to the VFW Online Membership System, access VA benefits on Vets.gov, and gain access to military discounts from 200+ retailers.

This is a sizable win for ID.me, whose founder and CEO Blake Hall is a third generation soldier, former Army Ranger, and graduate of West Point. With this new client, the company has access to VFW’s 1.7 million members, all of whom stand to benefit from a simplified sign in process and secure way to prove their veteran status. The announcement of this client comes just a month after the company teamed with General Motors to support its military discount program.

“Trying to remember the login information for several different online accounts is difficult, and further, verifying your identity online can be a cumbersome process,” said VFW National Commander Keith Harman. “So we’re glad to be able to provide our members with a simple solution.”

At FinovateSpring 2017, Hall showcased how ID.me streamlines account opening, regulatory compliance, and customer support for banks and fintechs using identity that is accredited by the federal government. Last month ID.me surpassed 5 million users and in October, the company partnered with Finovate alum ThreatMetrix to deliver ID verification for government and commercial digital services. The company has raised a total of $45.8 million.

Accounting software provider Aplos has teamed up with payroll processing specialist Gusto to offer an integrated, back office financial and HR solution for Aplos’s nonprofit and faith-based organization client base.

“We are thrilled to expand our support of nonprofits by partnering with Aplos,” Gusto Head of Partnership Development Mike Triantos said. “Gusto and Aplos share the same vision by making it simpler to manage nonprofits and churches so they can focus on their core mission.”

The strategic partnership between the two companies will enable Aplos customers to import Gusto payroll runs into their accounting without requiring a manual export/import process. The cloud-based solution calculates, pays, and files federal, state and local payroll taxes, and manages W2, 1099, and new hire forms. In a statement, Aplos CEO Tim Goetz pointed out that Gusto was even able to factor in pastoral housing allowances and other more esoteric church financing arrangements

“When you are trying to change the world you don’t want to get stuck doing paperwork,” Goetz said. “This partnership with Gusto eliminates countless hours of administrative time.” He added that nine out of ten Aplos customers preferred Gusto over other payroll solutions. “I truly believe our nonprofit and church customers will feel this partnership makes their jobs easier so they can put their focus back on their mission.”

Founded in 2011 as ZenPayroll, the company demonstrated its payroll processing technology at FinovateSpring 2014. Rebranding as Gusto a year later, the San Francisco, California-based fintech has since partnered with firms like Capital One, raised more than $176 million in funding, and now serves more than 40,000 companies across the U.S. Gusto was named to CB Insights’ Fintech 250 list in June, and was featured in Business Insider as one of “3 startups to bet your careers on in 2017” last January.

Russia’s largest commercial bank is making bitcoin waves today. Alfa-Bankannounced that it has initiated a collaboration with HashCash, a private, permissionless, digital cash system.

Through the partnership, HashCash will create a payment router and clearing house where all transactions are sent to Alfa-Bank on the blockchain. Alfa-Bank will clear transactions, forward them to the receiving bank in real-time, and log supporting documents. The transfers will operate on the Open Source Blockchain, HC NET, which uses fiat currencies for settlement.

Raj Chowdhury, Managing Director of HashCash Consultants said that the implementation “creates a clearing house solution that combines the liquidity efficiency of a netting system and the intra-day finality of a real time gross settlement system.” He added, “The result is a safe, secure, reliable, fast and final payment system for all transacting parties.”

This isn’t Alfa-Bank’s first foray into the blockchain. Last year, the bank partnered with S7 Airlines for blockchain-based ticket payments. It also collaborated with Sberbank on Russia’s first Blockchain Payment.

At FinovateFall 2015, Alfa-Bank debutedSense, a predictive marketing solutions product for financial institutions.

Blockchain solutions innovator Ripple announced plans to team up with remittance services company MoneyGram.

This announcement comes at a time when both Ripple and MoneyGram have been in the news headlines. Many outlets have reported on Ripple for the volatility of XRP, its digital currency (and for the rumored rise of its founder, Chris Larsen, as one of the richest persons in the world). And last week, an attempted purchase of MoneyGram by Chinese firm Ant Financial was blocked by the U.S. government.

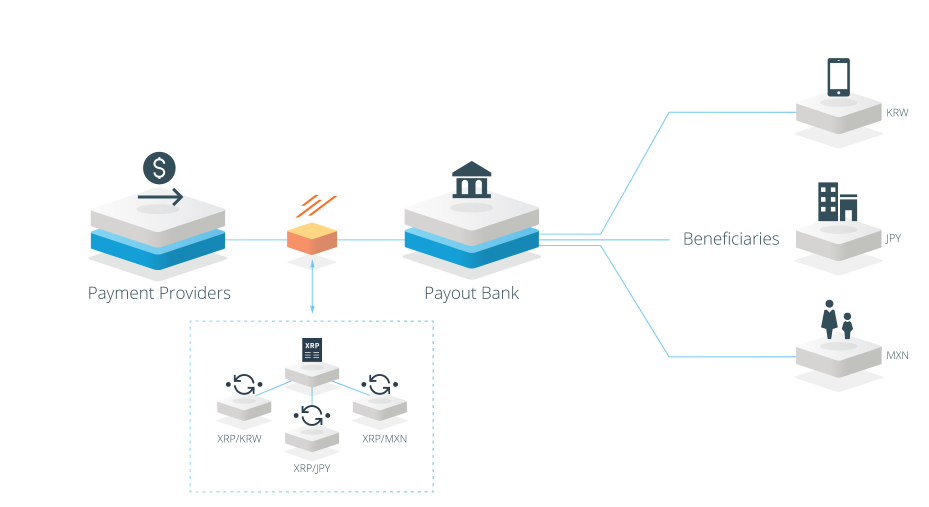

Ripple’s xRapid transfer flow

As a part of the partnership, MoneyGram will use XRP through Ripple’s xRapid, a service that aims to provide liquidity to financial institutions. Touting the practicality of leveraging XRP for remittances, Ripple noted that transactions can be made for fractions of a penny and in two-to-three seconds. This is favorable compared to Bitcoin’s fees of $30 per transactions and wait times of up to an hour.

Through agreement, the companies will also explore MoneyGram’s integration into Ripple’s xVia, an API for businesses, payment providers and banks to send payments across various networks using a standard interface.

MoneyGram’s current model requires the sender’s account to be pre-funded before they are able to send currency. Leveraging blockchain technology, MoneyGram can simplify cross-border transfers, making them more efficient. Ripple CEO Brad Garlinghouse said, “Money transfer companies are incredibly important because they help people get money to their friends and loved ones…. By using a digital asset like XRP that settles in three seconds or less, they can now move money as quickly as information.”

MoneyGram is the second largest money transfer company in the world, competing not only with traditional companies such as Western Union, but also with the likes of fintechs such as Azimo, TransferWise, and CurrencyCloud. Leveraging the blockchain for cross-border remittances and transactions is not new to fintech. At FinovateFall last year, we saw nanopaydemo its cross-border payments platform that enables the banks to provide instant fund transfers, without intermediaries, at a 60% cost reduction. Similarly, in 2015 CoinJarshowcased its platform that lets users buy, sell, send, receive, and spend digital and traditional forms of currency using the blockchain.

Ripple has offices in San Francisco, New York, London, Luxembourg, Mumbai, Singapore and Sydney, and counts more than 100 customers across the globe. At FinovateSpring 2013, company co-founder Chris Larsen debuted Ripple (originally known as OpenCoin). Last fall, Ripple teamed with AmEx and Santander to support blockchain-powered international B2B payments. And in December of last year, the company’s XRP currency reached a milestone, boasting availability on 50 exchanges worldwide.

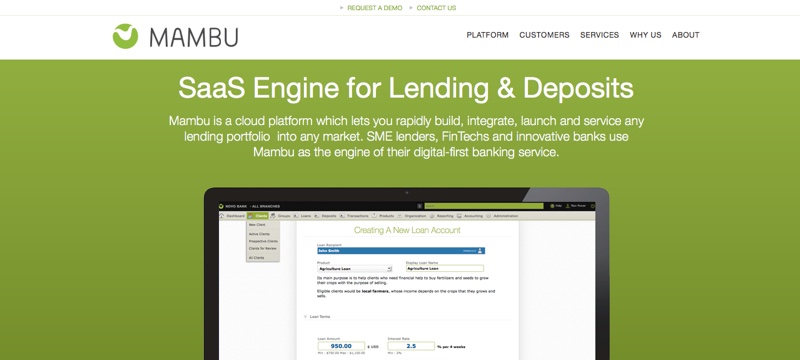

Kreditechhas selectedMambu’s Software-as-a-Service (SaaS) banking engine for its push into India’s lending market, reports Antony Peyton of Banking Technology (Finovate’s sister publication.)

The firm currently operates in Europe and Latin America and said it will expand into the sub-continent in early 2018, together with its partner PayU, a payments provider and a Mambu client in Latin America.

The engine will let Kreditech launch a short-term lending product tailored to local consumer and regulatory needs.

Alexander Graubner-Müller, CEO of Kreditech, said by using “alternative data and self-learning algorithms, we are able to evaluate consumers whose credit history is difficult for banks to gauge” – and it offers them “access to loans and thereby help them to gain economic independence”.

He added that Mambu’s cloud-native solution “easily integrates into our architecture, allowing us to quickly scale and adapt to market and consumer demands”.

The loan product is expected to go live in the first quarter of 2018, all data will be hosted by Amazon Web Services (AWS) India.

Founded in 2012 and headquartered in Hamburg, Germany, Kreditech covers more than five markets, including Russia, Mexico, Spain and Poland. Up until now, the company says it has processed more than five million loan applications through its subsidiaries. Kreditech demonstrated its the effectiveness of its Kreditech algorithm that assesses client creditworthiness in less than a minute at FinovateSpring 2014.

A FinovateAsia alum, Mambu demonstrated its native cloud Saas banking application at our Singapore conference in 2013. Based in Berlin and founded in 2011, Mambu has forged partnerships with a number of FIs and fintechs in recent months including a deal with ABN Amro’s new fintech firm, New10 in October, and a deployment with German challenger bank, N26 announced in September.

Scalable Capital is saying, “Gruetzi mittenand” to Switzerland today. The U.K.-based robo advisor has launched its services in Switzerland, the fourth country to which Scalable Capital has expanded, following launches in U.K., Germany, and Austria.

Describing Switzerland as “an interesting market for every wealth manager,” Scalable Capital Co-founder Simon Miller said that the company made the move knowing it could offer real value to Swiss retail investors. Miller added, “We are the only independent robo-advisor in Europe using three key building blocks to build a truly customer-centric product: professional risk management for every individual portfolio, low cost, and a comprehensive digital service with unparalleled transparency.”

With a Swiss customer phone hotline, as well as a website aimed specifically to serve Swiss customers, the startup has an E.U.-wide approval and can offer its services across the E.U. without having to go through additional application processes. Scalable Capital’s German custodian bank partner, Baader Bank AG, will provide tax reporting and will serve as the custodian bank for all Swiss customers, managing their portfolios in euros.

Scalable Capital was founded in 2014 and now serves more than 20,000 clients with $810 million (£600 million) assets under management. The company holds partnerships with BlackRock, Siemens Private Finance, and Germany’s third-largest retail bank, ING-DiBa.

Scalable Capital most recently presented at FinovateEurope 2016. The company has 70 employees and has raised $49 million. Last spring, Scalable Capital was the only European startup to be recognized on CNBC’s Upstart 25 list.

This post will be updated throughout the day as news and developments emerge. You can also follow all the alumni news headlines on the Finovate Twitter account.

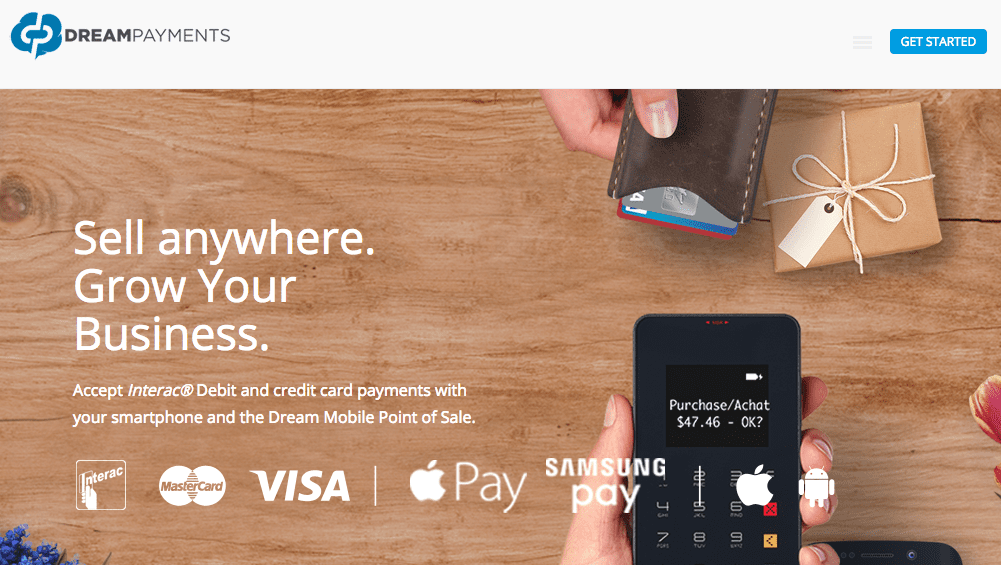

Cloud-based payment platform Dream Payments has teamed up with Quickbooks, and First Data’s Clover to bring QuickBooks capabilities to U.S. merchants this week.

This comes three months after Dream Payments first initiated a partnership with First Data last year, launching the Dream Payments POS for merchants using First Data’s Clover. It also follows Dream Payments’ successful pilot of a QuickBooks integration in Canada.

The partnership will allow Dream Payments’ business clients using any POS device in Clover’s line to sync with QuickBooks. After a purchase, QuickBooks will automatically and in real time record the sale, update inventory, collect and close invoices, and import sales tax.

CEO of Dream Payments Brent Ho-Young said that the integration will help businesses succeed. He added that, by combining QuickBooks and Clover in the Dream Payments POS, “we’re unlocking the cloud and simplifying the most complex aspects of running a successful business — customer experience, payments and accounting. Now businesses of any size can access a powerful commerce platform that traditionally only the largest retailers could afford.”

Founded in 2014 and with operations in Stamford, Connecticut, Dream Payments helps small businesses accept all payments, including chip cards, contactless cards, and mobile wallets. In addition to ties with Quickbooks and First Data, the company also counts TD Merchant Solutions and Chase Paymentech in its partnership ecosystem.

At FinovateSpring 2015, Dream Payments debuted its mobile POS device. Last fall, the company partnered with IBM to leverage its cloud and security capabilities. Dream Payments has raised $14.9 million. Brent Ho-Young is CEO.

Less than two weeks into 2018, most of us are already running to catch up. But there are a couple deadlines you should not let pass you by: demo application deadline this Friday, January 12 and ticket deadline next Friday, January 19 ($800 savings).

With its expansion to four days this year, FinovateSpring moves to the Santa Clara Convention Center on May 8-11. The first two days will continue featuring Finovate’s signature single-track demo format, while the next two days will focus on deeper dives and insights from keynotes, panels, breakout sessions and more. All the fintech bang for your buck consolidated into just four days.

Companies selected to demo on May 8-9 will receive 7 minutes on stage to demo their latest fintech innovation, a booth in the exhibition area, ability to connect with 1,500+ C-level financial execs, venture capitalists, entrepreneurs, and influential press, analysts, and bloggers, plus many other perks.

If you’re thinking about applying to demo, now is the time. Earlier applicants may receive faster selection and are also eligible for lower pricing. This next deadline, which guarantees you the lower cost, is this Friday, January 12. More information on demoing is available here.

And if you would rather check out the event with an eye towards applying next year,get your ticket before Friday, January 19 and save $800.