This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Fall is officially here! A favorite season for many, autumn also marks a likely acceleration in fintech and financial services news and activity. Be sure to check Finovate’s Fintech Rundown all week long for the latest in headlines and news updates!

Nasdaq Verafin announces enhancements to its Targeted Typology Analytics suite to add detection capabilities for terrorist financing and drug trafficking activity.

This week, we turn to Uzbekistan, a Central Asian nation and former Soviet republic with a population of just over 37 million. The doubly-landlocked country (one of only two in the world) has been transitioning toward a market economy for years and has been credited by the Brookings Institution for its high economic growth and low public debt. A major producer and exporter of cotton, Uzbekistan has leveraged major natural gas supplies to be one of the largest electricity producers in the region. HSBC has predicted that the country will have one of the fastest-growing economies in the next few decades.

We interviewed Oliver Hughes, former CEO of Tinkoff and current Head of International Business for TBC Bank Group – which recently expanded to Uzbekistan. In our extended conversation, we discussed TBC’s goals in Uzbekistan, nature of banking in Central Asia, what key financial services are in the most demand, as well as how enabling technologies are helping financial institutions in the region better serve their customers.

You joined TBC a few years after the bank expanded to Uzbekistan. First, what drew you to TBC?

Oliver Hughes: Joining TBC in Uzbekistan was a great opportunity for two reasons. First, the market itself is full of potential and ripe for disruption. A young, growing population of 37 million people, of which 59% are under the age of 30, economic reforms and liberalization, a favorable macroeconomic environment and an under-penetrated digital banking market create huge demand for world-class online banking services, so I could see a clear path to success.

Second, I knew that TBC Uzbekistan would be a great place to work and an environment that would allow me to make an impact. Since coming to Uzbekistan in 2019, TBC has built a world-class team, secured a banking license, reached profitability within two years, and outlined a vision that aligns with my previous experience of building and scaling a best-in-class, profitable digital banking ecosystem.

Uzbekistan was TBC’s first international market outside of its native Georgia. Why Uzbekistan?

Hughes: Uzbekistan is a hidden gem, previously largely overlooked by the international investment community, but slowly getting on the radar of investors and fintech heavyweights. It is Central Asia’s largest country by population, which is young and getting younger each year. This supports demand for modern digital financial services. The country has also embarked on a large-scale program of economic reform and liberalization, empowering the private sector and starting to attract more international investment.

TBC Uzbekistan is part of London-listed TBC Bank Group and we are proud to play our part in attracting major global investors to the country. Through TBC, large global investment funds like Fidelity, JPMorgan Asset Management, Schroder, BlackRock and Vanguard have been investing in Uzbekistan, and more investors are coming in every month.

The macroeconomic picture is strong, with GDP expanding at an average annual rate of around 6% for the past decade and forecast to almost double to $160 billion between 2023 and 2030.

In addition, Uzbekistan has a deep tech talent base. It’s both because of its highly educated domestic workforce – a product of a strong education system, and also because Uzbekistan is benefiting from an influx of returning expats and a broad range of international tech specialists from neighboring countries.

What does the financial services ecosystem look like in Uzbekistan? What is the level of interest in fintech innovation there?

Hughes: The financial services sector is still largely dominated by major state banks, which command around 70% of the market. However, competition is increasing as the government continues its drive for privatization and other reforms. A recent example of this was with Hungary’s OTP, which in June 2023 became the first international player to participate in the privatization of the Uzbek banking sector, acquiring former state-owned Ipoteka Bank. And recently, Kaspi announced its intention to participate in the privatization of Humo, Uzbekistan’s second largest open-loop domestic payment system.

TBC Uzbekistan is part of London-listed TBC Bank Group PLC, which also operates Georgia’s leading tech-enabled commercial bank. Despite being part of a multinational group, we consider ourselves to be a local player because we operate as a standalone company in Uzbekistan with a separate tech stack and separate team purpose-built for this country.

In terms of the ecosystem as a whole, it is a mix of state banks, international operators, and local Uzbek players, as well as a developing fintech scene covering everything from payments to crypto.

The level of innovation in the local fintech market is very advanced, thanks to open banking. The key development, which has not yet been replicated in developed markets, is the full banking interoperability that open banking enables in Uzbekistan. In practice, it allows customers to seamlessly interact with multiple financial institutions.

For instance, when a customer of one bank opens an account with another institution, the new bank gains visibility into the customer’s transaction history and account balances from their original bank, while the new bank is also able to initiate fund transfers or debit transactions from the customer’s account at the original institution. This helped TBC enter the market in 2019 via the acquisition of the leading P2P payments app Payme to quickly achieve profitable growth and access to a huge customer base.

Let’s talk a little more specifically about TBC Uzbekistan. How is it structured? What is its mission?

Hughes: Our mission is simple – to make people’s lives easier. As I described earlier, the financial services sector has been and is still to some extent dominated by state institutions that operate in a traditional fashion. We see that there is demand for modern, digital banks that provide a great, convenient user experience and that is what we are building.

At present, there are three components to TBC Uzbekistan: TBC Bank Uzbekistan (TBC UZ), a mobile-only bank; Payme, a digital payments app for individuals and small businesses; and Payme nasiya (Payme instalments), an installment credit business. London-listed TBC Group owns 100% of both Payme and Payme nasiya and is the major shareholder of TBC UZ, with a 60% stake. The other 40% stake in TBC UZ is split between two institutional investors: the European Bank for Reconstruction and Development (EBRD) and the International Finance Corporation (IFC), part of the World Bank Group.

What are some of the biggest areas of opportunity in your opinion?

Hughes: We see some really exciting opportunities in Uzbekistan. At present, we are focused on consumers and specifically consumer lending. Despite over 45 million cards in circulation across the country, product offerings remain limited and retail lending is especially underdeveloped, representing just 12% of GDP.

Demand from consumers for financial services is already significant and continuing to grow, with point-of-sale (POS) digital payment volumes tripling to over $22 billion in the three years ending in 2023, with the number of POS terminals and bank cards in circulation doubling over the same time period.

There are interesting opportunities in other areas as well, including a new, product-rich debit card, financial services for SMEs, insurance and brokerage, with the latter two being at a fairly nascent stage of development in Uzbekistan. So, we plan to leverage those as well in the future.

TBC Uzbekistan recently raised a significant amount of capital. How will the new funding help the bank?

Hughes: Our business in Uzbekistan is scaling rapidly, but there is still significant potential for further growth, including through diversifying our offering to address market demand. The recent funding is being used to increase our loan book — which we are currently doubling year-on-year — advance financial inclusion, and accelerate our progress in launching new product lines.

In addition to powering our growth, new funds help us to continue to diversify our funding base.

What are some things about Uzbekistan that those of us on the outside may be surprised to learn?

Hughes: Uzbekistan is a country that largely exists outside the mainstream consciousness in the West. Some people might have their preconceptions, and would be surprised to learn about the advanced state of open banking in the country. Building on that, the level of innovation in financial services is pretty impressive in Uzbekistan. The fintech sector is thriving and strongly supported by the government and the wider ecosystem that is fueled by local and international tech talent.

In terms of other things that may surprise you about Uzbekistan, it’s the food scene. The food here is incredible, so I urge everyone to come over and try it!

There is a lot of talk about enabling technologies such as AI. Are any of these major areas of innovation in Uzbekistan’s fintech scene?

Hughes: Artificial Intelligence is a key innovation area and one that I am proud to say that TBC is leading among peers by integrating AI into our services.

Our plans are ambitious. We are building an AI Virtual Assistant that takes customer service to the next level. The most common customer service solution right now is chatbots, but we’re skipping that stage and going straight to an interactive voice assistant. What’s more, we’re enabling functionality in the Uzbek language and, in the future, in other local languages such as Tajik and Karakalpak, which tend to get overlooked by major tech giants.

We ultimately envision this Virtual Assistant being able to guide our users across all of our product offerings within TBC Uzbekistan, including the ones we plan to launch in the future, such as insurance, brokerage, travel and ticketing.

How do you see TBC Uzbekistan growing over the next two-to-three years?

Hughes: Since launching in 2019, TBC Uzbekistan has scaled significantly and established itself as a leading player in the market. As disclosed in our recent half-year results, we have grown our user base to 16 million unique registered users and achieved an operating profit of $61 million, up 87% year-on-year, with TBC Uzbekistan accounting for 7% of total profit for the group, as well as 13% of revenue and 44% of consumer loans on the group level. This is a very significant contribution, which is set to expand further.

We plan to continue to grow rapidly over the next 2-3 years, launching new product lines and gaining an increased percentage of market share. This is reflected in the guidance we have issued to the market: a net profit for TBC Uzbekistan of $75 million for the full year of 2025, with 30% of the Group’s loan book coming from TBC’s operations in Uzbekistan.

Where might TBC expand next? Are there any areas of special interest?

Hughes: We’re not yet at the stage where we can point to a specific market. However, I can tell you the types of markets we are considering. Our attention is on emerging markets with a population of around 30 to 70 million people, scope for growth and other favorable characteristics. For now, we still have a lot of exciting things to do in Uzbekistan.

Here is our look at fintech headlines around the world.

Sub-Saharan Africa

South African fintech Happy Pay locked in $1.8 million in pre-seed funding in a round co-led by E4E Africa and 4Di Capital.

Ghanaian crypto platform, Mybitstore, went live in Nigeria this week.

Nigerian fraud detection company Regfyl raised $1.1 million in funding.

Central and Eastern Europe

Germany’s Commerzbank partnered with Deutsche Börse subsidiary, Crypto Finance.

Instanbul, Turkey-based fintech Colenda AI launched new AI solution to help financial institutions enhance decision-making and boost loan performance.

Bulgaria-based Paynetics teamed up with tell.money to launch its Confirmation of Payee (CoP) service.

Middle East and Northern Africa

UAE-based B2B payments platform Xpence teamed up with Egypt-based Paymob to enhance digital payments in the region.

Egyptian fintech SETTLE raised $2 million in pre-seed funding.

Mesh integrated with digital asset trading platform CoinMENA FZE to enhance crypto transfers and account management for customers in the MENA region.

Central and Southern Asia

India-based insurtech Onsurity raised $21 million to power expansion plans.

ZaakPay, the payment gateway arm of India’s MobiKwik, partnered with Meta to provide an embedded payment option via WhatsApp.

Indian financial services platform Kaleidofin secured $13.8 million in funding.

Latin America and the Caribbean

Uruguay-based MercadoLibre secured $250 million in financing from JPMorgan.

JMM Group and Liberty Latin America launched microlending service MYNE Lend for Jamaican customers.

dLocal, a cross-border payments platform based in Uruguay, forged a partnership with MoneyGram.

Asia-Pacific

Vietnam Maritime Commercial Joint Stock Bank (MSB) teamed up with TerraPay.

Paysend launched instant cross-border payouts to China UnionPay cards for enterprise customers.

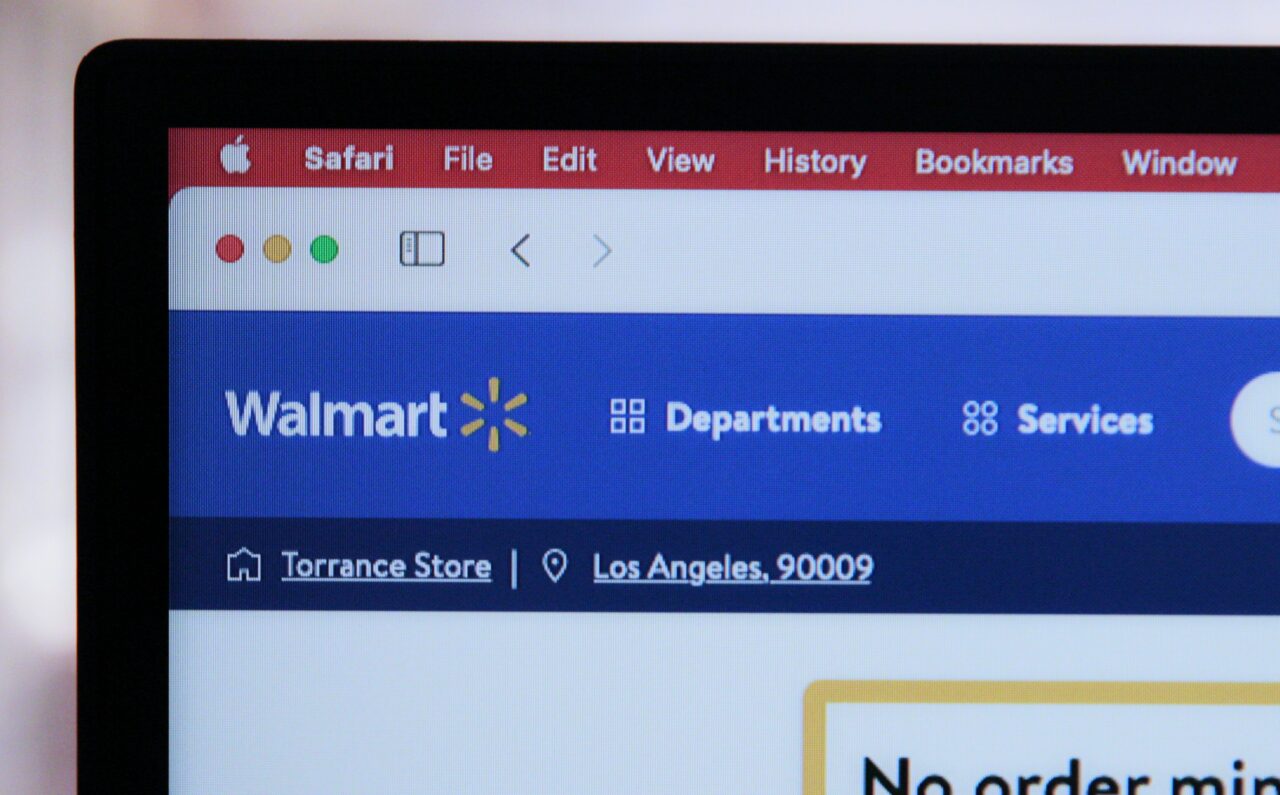

Walmart is partnering with Fiserv to enable pay-by-bank payments for online purchases starting in 2025.

Benefits to Walmart include lower transaction costs, faster settlement, reduced fraud, and fewer payment declines, while customers can avoid stacked pending transactions.

Consumers may face challenges like added friction and lost credit card rewards, but early pilot results have exceeded Walmart’s expectations for pay-by-bank adoption.

Walmart made its latest move in the fintech space this week after announcing it has partnered with Fiserv to offer pay-by-bank for online purchases.

Bloomberg unveiled this week that, while the retailer has offered pay-by-bank via Walmart Pay for a few months now, the payments were routed through ACH payment rails and still took days to clear. Beginning in 2025, however, Walmart will leverage Fiserv’s NOW Network, which will route the payments through The Clearing House’s Real Time Payments network and the Federal Reserve’s FedNow. Launched in 2014, Fiserv’s NOW Network aims to reach as many banks as possible to provide consumers and businesses the ability to send, receive, and access funds immediately while supporting credit push payments.

Starting next year, customers will be able to make online purchases using pay-by-bank by connecting their bank account through Fiserv’s AllData platform. The platform will facilitate authentication and securely link bank accounts. This will be done through integrations with Plaid, MX, Akoya, and Finicity, ensuring a seamless and secure connection to customer accounts.

Leveraging Fiserv to power real time payments is an important move for Walmart as it enters the pay-by-bank game. As Fiserv Head of Digital Payments Matt Wilcox told Bloomberg, “As an industry we believe we need to create this connectivity. FedNow and RTP, they don’t necessarily talk to one another. The NOW Network can play that role in the industry of bringing all these networks together to enable applications like pay-by-bank.”

Walmart stands to receive multiple benefits when consumers choose to pay-by-bank. The retailer will face lower transaction costs by bypassing credit card networks; increased cash flow, since bank transfers settle faster than card transactions; reduced fraud and fewer declines, since the pay-by-bank payments offers direct access to and will authenticate a customer’s bank account; and the potential to reach more consumers who may not have a credit or debit card.

From a consumer perspective, the benefits of pay-by-bank are more difficult to find. Unlike the merchant, they don’t experience any cost savings for opting for pay-by-bank, there is added friction involved in connecting their bank account to Walmart’s platform, they lose out on credit card rewards, and in the event their account is hacked, fraudsters will have the option to make purchases directly from their account, instead of on a credit card that would offer an extra layer of protection while the customer disputes the transaction.

That said, Walmart is touting the ability for pay-by-bank to help consumers avoid stacked pending transactions. “When the transaction processes as a real time payment, customers get immediate access to see that payment come through, I see it hit my account and I can properly budget,” said Walmart Vice President of Emerging Payments Jamie Henry. “It’s not as if I’ve got this phantom payment out there that’s going to take place a couple days down the road.”

And while I remain skeptical on the mass consumer adoption of pay-by-bank, perhaps Walmart’s customer base is more well suited for these types of transactions. Henry said that the initial pilot of pay-by-bank was surprising. “It’s certainly surpassed our expectations of the amount of customers that have registered and actually use the payment type,” he said.

Could 2024 turn out to be the Year of the Regtech?

As more and more processes in financial services become AI-enabled, the impact of AI on regulatory technology and compliance solutions has been profound. From automating manual processes to more comprehensively engaging data, AI is helping regtech firms better serve their customers at a time when their customers – in banking, in fintech, in financial services in general–need it most.

We caught up with one such regtech, Tennis Finance, and its Co-Founder and CEO Jake Pimental. Headquartered in San Francisco, California and founded in 2022. Tennis offers an automated AI compliance and risk management solution to help businesses better manage customer complaints and external communications.

At its Finovate debut at FinovateSpring earlier this year, the company demoed Rally, its solution that enables financial institutions to intake customer complaints and data to automatically identify compliance issues as well as uncover trends in customer conversations.

What problem does Tennis Finance solve and who does it solve it for?

Jake Pimental: Tennis Finance addresses the growing complexity of compliance and risk management for banks, financial institutions, and debt collectors. As regulations tighten and customer complaints rise, these organizations face significant challenges in handling compliance effectively and efficiently. We specifically focus on automating the processing and analysis of customer communications to prevent regulatory breaches and lawsuits, while also optimizing customer service and operational efficiency.

How does Tennis Finance solve this problem better than other companies or solutions?

Pimental: We leverage AI-driven technology to analyze calls and customer interactions, providing actionable insights that streamline workflows. Our platform parses customer communications, automatically categorizing and tagging them for compliance risk. This automation reduces overhead by 80%, increases regulatory safeguards, and improves customer retention, giving our clients a significant competitive edge. Unlike other solutions, we don’t just automate tasks – we provide a comprehensive view with tailored action plans, ensuring our clients not only meet regulatory standards but exceed them.

Who are Tennis Finance’s primary customers, and how do you reach them?

Pimental: Our primary customers include banks, accounts receivable companies, and financial institutions that are heavily regulated and at risk of non-compliance. We reach them through industry conferences like Finovate, strategic partnerships, and referrals through consulting networks. We also work closely with compliance officers and decision-makers, demonstrating how our platform can save time and reduce compliance risk.

Can you tell us about a favorite implementation or deployment of your technology?

Pimental: One of our most impactful deployments was with a major debt collection agency that was struggling with complaint handling and agent oversight/coaching. Our AI solution reduced their operational overhead by 80% and helped them identify risks early, preventing costly litigation.

What in your background gave you the confidence to tackle this challenge?

Pimental: Before founding Tennis Finance, I was a compliance officer at SoFi, where I helped launch their investments arm and navigated complex regulatory environments. This experience, along with my background in compliance strategy and risk management across multiple startups, gave me a deep understanding of the challenges financial institutions face. My track record of building solutions that solve these problems, combined with the ability to scale AI-driven technologies, gave me the confidence to build Tennis Finance.

There has been a great deal of interest in regtech and compliance in recent years. Is this a trend you saw coming? What is driving it and where is it going?

Pimental: Yes, the rise in interest was anticipated, given the increasing complexity of financial regulations and the growing number of customer complaints. What’s driving it is a mix of stricter regulatory scrutiny, rising operational costs, and the need for faster, more efficient compliance processes. The future of regtech is all about automation and AI – providing real-time risk management, reducing manual tasks, and enabling institutions to stay ahead of the regulatory curve while improving customer experiences.

You demoed at FinovateSpring earlier this year. How was your experience?

Pimental: FinovateSpring was an incredible experience. It allowed us to showcase the unique capabilities of our platform in front of an audience of industry leaders, investors, and potential clients. The feedback we received was overwhelmingly positive, especially around our AI-driven approach to compliance automation. It was also a great platform to build valuable partnerships and foster industry connections.

What are your goals for Tennis Finance? What can we expect to hear from you in the months to come?

Pimental: Our primary goal is to scale our platform to serve more financial institutions and expand into new markets. In the coming months, you can expect to see us deepening our partnerships, launching new features focused on advanced predictive analytics, new AI workflows, AI coaching, and exploring new use cases beyond just compliance. We’re committed to pushing the boundaries of what AI can do in the financial services space.

Open banking solutions provider Neonomics is streamlining and enhancing the deposit experience for customers of Oblinor.

Oblinor offers a digital real estate investment platform that enables users to build a portfolio of secured property loans.

Based in Oslo, Norway, Neonomics made its Finovate debut at FinovateEurope 2020 in Berlin, Germany.

Digital real estate investment platform Oblinor has turned to open banking solutions provider Neonomics to streamline and enhance the deposit experience. Oblinor, founded in 2018 and headquartered in Norway, has integrated Neonomics’ checkout offering, which will facilitate a faster, more secure process for investors when they deposit funds for their accounts.

“We’re excited to integrate open banking into our platform,” Oblinor Lead Engineer Christopher Maxwell said. “Neonomics has made the transition smooth and effortless, allowing us to offer a faster, more secure, and incredibly user-friendly way to fund investments. This is just the beginning, and we’re excited about the potential to continue driving innovation in financial services alongside Neonomics.”

Oblinor enables individuals to invest in loans to Norwegian property companies and to build a portfolio of secured property loans. Its partnership with Neonomics will enhance the deposit experience by instantly populating details such as account numbers, amounts, and KID numbers, reducing the amount of manual work typically required to enter transaction data. In addition to accelerating the deposit experience, the partnership with Neonomics will provide greater security and less risk of fraud, as well.

“Neonomics is a perfect fit for what Oblinor is building,” Neonomics CEO Christopher Andvig said. “By integrating open banking, we’re adding real value for their users–making it easier, more secure, and more efficient to invest. As the potential of open banking continues to grow, we’re excited to see what’s next in this partnership.”

Founded in 2017, Neonomics made its Finovate debut at FinovateEurope 2020 in Berlin. At the event, the Norway-based fintech showed how its technology can be used to facilitate instant payments and bank transfers directly from an app or website. Today, the company unifies access to more than 2,500 banks and 150 million bank customers across Europe. A licensed payments institution authorized by the Norwegian FSA, Neonomics provides payments initiation and account information services for customers ranging from banks to fintechs to payment service providers and more.

Earlier this month, Neonomics introduced new Head of Growth and Interim Country Manager for Finland, Panu Poutanen. Most recently, Poutanen was General Manager of Finland for European cloud-based payment services provider Viva.com. In August, Neonomics announced a partnership with charitable giving platform company Støtte. The company will leverage Neonomics’ open banking technology to facilitate account-to-account payments for its micro-donation offering.

CSI announced plans to acquire deposit growth firm Velocity Solutions.

CSI will integrate Velocity’s solutions that drive revenue, service, and compliance for community banks and credit unions into its existing offerings.

Financial terms of the deal were undisclosed.

Community bank technology provider CSI announced plans to acquire deposit growth firm Velocity Solutions. Financial terms of the deal were undisclosed.

Velocity Solutions was founded in 1995 to offer tools that help drive revenue, service, and compliance for community banks and credit unions. The company’s Velocity Intelligent Platform powers its solutions, among which are a Retail Performance Engine, Consumer Liquidity Engine, and Digital Business Lending. These tools leverage machine-led intelligence to help firms manage risk, drive revenue, increase engagement, and boost non-interest income.

Velocity Solutions, which demoed its Akouba cloud-based lending platform at FinovateFall 2021, services more than 30 million consumers and business owners.

“Our customers rely on us to provide the advanced tools and software that drive revenue, efficiency and cost savings,” said CSI CEO and president David Culbertson. “Velocity’s data-driven approach to deposit management and its intelligent overdraft decisioning engine are each designed to deepen relationships with account holders while minimizing risk exposure for financial institutions.”

CSI plans to integrate Velocity’s solutions into its existing financial services suite, which includes everything from core banking to lending to managed IT and cybersecurity, advisory services, and more. “We’re eager to identify more opportunities to evolve the differentiated financial software and technology solutions that make CSI the first choice for community and regional financial institutions nationwide,” added Culbertson.

“The CSI and Velocity teams are united by the same mission to empower community and regional financial institutions to compete and win against the largest banks in the country,” said Velocity Solutions CEO Christopher Leonard. “Our customers are facing increasing pressure to grow in a challenging rate and deposit environment and require innovative ways to acquire and serve their account holders. We are eager to tap into CSI’s deep expertise and development prowess to expand our banking management platform and support customers in meeting their goals.”

CSI expects that today’s purchase will complement the acquisition of community bank loan servicing platform, Hawthorn River, the company made in December of last year.

CSI, which recently launched an expanded developer portal, was founded in 1965. The company received an investment of an undisclosed amount from private equity firm TA Associates in January 2024.

You’ve likely been following the fallout from Synapse’s bankruptcy earlier this year. BaaS provider Synapse filed for Chapter 11 bankruptcy in April, leaving its clients, including Evolve Bank & Trust and multiple others, unable to verify and manage funds. In all, around $85 million in consumer funds are missing due to discrepancies in Synapse’s records.

Adding to the confusion, the dispute is ongoing in court, and because Synapse is a fintech and is thus unregulated, regulatory bodies are unable to protect consumers, many of whom are still missing their funds.

As a result of this nightmare, the FDIC has advanced a notice of proposed rulemaking for what it is calling Requirements for Custodial Deposit Accounts with Transactional Features and Prompt Payment of Deposit Insurance to Depositors. The regulatory body is currently taking public comment on the rule.

As it currently stands, the rule applies to bank accounts that fit into three categories:

The account is established for the benefit of beneficial owners

The account holds commingled deposits of multiple beneficial owners

A beneficial owner may authorize or direct a transfer through the account holder from the account to a party other than the account holder or beneficial owner

Here are five things banks with accounts that fit these categories should know about potential implications the rule may have on them.

Strengthened recordkeeping requirements

Advanced recordkeeping should already be part of a bank’s routine. However, the proposed rule is specific in its requirements, stipulating that banks working with non-bank entities (as in a BaaS partnership) must maintain accurate records that identify the beneficial owners of custodial deposit accounts that are held on behalf of consumers, which is typical in a BaaS agreement. Maintaining records of custodial accounts will help regulators ensure that deposit insurance can be quickly and accurately provided in the event of a bank failure.

Continuous third-party records access

The proposed rule states that if banks rely on non-bank companies to manage custodial deposits and their records, the bank must have continuous, direct access to records held at the third party organization. This requirement aims to prevent disruptions to operations, as what we saw in the Synapse bankruptcy case earlier this year. Ultimately, if banks have transparent access to third party records, they can help customers maintain access to their funds.

Annual compliance and validation

Under the new rule, FDIC-insured, BaaS-enabled banks will be required to conduct an annual, independent validation to verify that their third party partners are maintaining accurate deposit records. Banks will send the records, which must be accurate and compliant with the FDIC’s standards, to the FDIC and to the bank’s primary federal regulator. The purpose of this stipulation is to ensure consumers are able to access their funds without delays and to increase the reliability of custodial funds arrangements.

Consumer protection and transparency

Consumer protection is the underlying reason behind the new proposed rule. A large piece of this provides clarity about FDIC insurance. As such, BaaS-enabled banks will be expected to ensure that their consumers fully understand the coverage and protections of their deposited funds, particularly when dealing with non-bank custodians.

Heightened money laundering

The document also emphasizes that banks must exercise strengthened internal controls and anti-money laundering (AML) compliance requirements. Notably, the ruling also emphasizes that banks must ensure that their third-party partners do not facilitate financial crimes.

This week’s proposed rulemaking highlights two truths in financial services. First, the additional requirements can potentially add burdens on banks that are already weighed down by multiple reporting responsibilities. Yesterday, Vice Chairman Travis Hill voiced his concern, saying, “I recognize that certain types of pass-through arrangements have become much more complex in recent years, exacerbating the potential risks…” Hill said, however, that he is voting in favor of the proposal, explaining that, “improving recordkeeping and reconciliation practices (1) can reduce the likelihood of another Synapse-like disaster in the event of a third-party failure, and (2) may result in a more orderly resolution in the event the bank fails.”

The second truth today’s proposed rulemaking underscores is that the financial services industry needs a national fintech charter that can monitor, regulate, and enforce third parties that manage and handle consumer funds. Banks have long been subject to strict regulations and reporting requirements. But should banks that have conducted the proper due diligence be held responsible for the actions (or inaction) of their third party partners? It is time for fintechs to step up and share the responsibility.

Identity verification specialist ID-Pal announced a global strategic partnership with CLOWD9.

The partnership will integrate ID-Pal’s AI-powered identity verification technology into CLOWD9’s payment solutions portfolio.

ID-Pal made its Finovate debut at FinovateFall 2024 in New York.

Fresh off its Finovate debut at FinovateFall this month, identity verification specialist ID-Pal has announced a global strategic partnership with CLOWD9. Courtesy of the partnership, CLOWD9 will offer ID-Pal’s AI-powered identity verification technology via its payment solutions portfolio.

“This strategic partnership will allow CLOWD9 clients to access both a compelling end-to-end identity solution and an AML screening solution with advanced AI-fraud detection capabilities,” CLOWD9 CEO and Co-Founder Suresh Vaghjiani said.

Using a combination of document, database, and biometrics checks, ID-Pal enables businesses to verify the identity of their customers in real-time. Available via API, SDK, or through the Salesforce App Exchange, ID-Pal’s technology detects AI-generated documents, deepfakes, and injection attacks, providing advanced fraud detection without requiring direct access to customer data. ID-Pal also streamlines OFAC, AML, and KYC processes into a single compliant workflow to ensure a comprehensive audit trail.

“We’re delighted to be adding our award-winning identity verification solution to the CLOWD9 technology portfolio,” ID-Pal Enterprise Sales Manager Mark O’Hara said. “Together we can help financial institutions adapt and thrive in a new world of digital payments and enhanced security by democratizing secure, robust fraud prevention tools.”

The partnership with CLOWD9 advances the company’s mission to revolutionize the payment industry through a combination of advanced payment processing and AI-powered identity verification. Founded in 2021 and headquartered in London, CLOWD9 was among the first B Corp certified payments companies. The firm offers a cloud-native, decentralized issuer payments processing platform that serves challenger, consumer, and SME banks; e-wallets and crypto exchanges; virtual and corporate card programs; and more.

ID-Pal is not the only Finovate alum that CLOWD9 has teamed up with in 2024; the company announced a partnership with reconciliation and reporting services provider Kani Payments in June. Like ID-Pal, Kani is a relative newcomer to Finovate, debuting at FinovateSpring last year. Additionally, this week’s news from CLOWD9 comes just days after the company introduced new Chief Technology Officer Paul Hansford. Hansford comes to CLOWD9 after six years as head of software engineering for payment company Thredd.

Founded in 2016 and headquartered in Dublin, Ireland, ID-Pal made its Finovate debut at FinovateFall 2024. At the conference, company CEO and Founder Colum Lyons demoed ID-Pal’s technology that uses “pure AI, not people,” to provide real-time identity verification. In his remarks, Lyons highlighted the fact that many legacy vendors in the space rely as much on people for identity verification as they rely on technology. In contrast, he said, ID-Pal’s 100% AI-powered platform leverages 160+ trusted data sources and 7,000+ identity documents to provide more accurate results and greater efficiency.

Xero announced plans to acquire Syft Analytics, a collaborative reporting tool.

Financial terms of the agreement were not disclosed, but the deal is expected to close between October and December of this year.

Xero plans to integrate Syft’s technology into its existing accounting offering, and it will also continue to maintain Syft as a standalone company.

Small business accounting software company Xero has announced plans this week to acquire collaborative reporting tool Syft Analytics. Financial terms of the deal were not disclosed.

South Africa-based Syft was founded in 2017 to help small businesses leverage their financial data. In addition to automated, customizable reports, businesses can also create financial reports and disclosures. The tool can also consolidate financial information from any accounting software, trial balance, transaction list, or ERP.

“We’ve worked closely with Xero’s teams and customers over the past seven years,” said Syft CEO Vangelis Kyriazis. “Having met Xero’s senior leadership team over the past few months, we knew that joining Xero was a natural fit and would advance our shared goal of helping small businesses succeed.”

Xero has worked with Syft since February of 2018. The two first partnered when the New Zealand-based company added Syft to its App Store, which allowed Xero customers to leverage Syft’s custom reporting features.

Once the acquisition is finalized, Syft will continue to operate as a standalone offering for small businesses, accountants, and bookkeepers – regardless of whether they are Xero clients or not. Xero also plans to embed Syft’s functionality into its existing platform, aiming to enhance its own analytics and reporting capabilities.

“We look forward to bringing this exciting vision to life by strengthening our insights, advanced reporting and analytics offerings through capabilities such as benchmarking, long term cash flow forecasting and multi-entity reporting,” the company said in a blog post. “Our goal is to bring the power of premium insights and advanced reporting functionality to our customers so they can reap the value for their business.”

The acquisition is expected to close between October and December 2024.

Founded in 2006, Xero listed on the New Zealand Stock Exchange (NZX) in 2007 and the Australian Securities Exchange (ASX) in 2012. In January 2018, the company consolidated to list solely on the ASX and now boasts a market capitalization of $22.58 billion. The company counts 4.2 million subscribers.

Earlier this year, Xero launched new inventory management software called Xero Inventory Plus, which it anticipates will help goods-based small business owners track and manage their inventory across different channels.

MoneyLion will integrate TransUnion’s data and credit solutions into its hosted enterprise credit-decisioning platform and direct-to-consumer finance tools.

Leveraging TransUnion’s data will help MoneyLion deliver more personalized and relevant financial offers, and ultimately improve the user experience.

TransUnion also offers marketing, fraud, risk, and advanced analytics tools. The company showcased its Enchanced BreachIQ tool at FinovateSpring earlier this year.

Mobile banking platform MoneyLion will be adding personalized touches to its consumer-focused products and services thanks to a partnership with TransUnion.

Under the agreement, MoneyLion will integrate TransUnion’s data and credit solutions into its hosted enterprise credit-decisioning platform and direct-to-consumer finance tools. By using the data from TransUnion, MoneyLion will be able to deliver more personalized and relevant financial offers to its clients, which it expects will improve the user experience. For its part, TransUnion will see its credit solutions expand their reach into not only the MoneyLion platform, but also to its partner network.

TransUnion Executive Vice President and Head of Financial Services Jason Laky said that the partnership will drive efficiency and innovation in the industry. “By integrating our comprehensive credit data with MoneyLion’s innovative digital acquisition platform,” he added, “we can offer a more robust experience to consumers and our partners alike, ensuring informed decision-making and greater consumer satisfaction.”

TransUnion was founded in 1968 and entered into the consumer credit reporting industry in 1969. Since then, the Illinois-based company has expanded its services to offer marketing, fraud, risk, and advanced analytics. As part of its risk portfolio, TransUnion offers Enhanced BreachIQ, which it demoed earlier this year at FinovateSpring. The technology behind BreachIQ originated from Breach Clarity, a fintech founded by Jim Van Dyke that won Best of Show honors at FinovateSpring 2020.

New York-based MoneyLion, which was founded in 2013, offers both direct-to-consumer banking tools as well as a marketplace of embedded banking tools, called Engine, for businesses. This enterprise technology suite serves as a marketplace for financial products, enabling financial services and non-financial services companies alike to add embedded finance to their business leveraging MoneyLion’s API.

“This partnership with TransUnion exemplifies MoneyLion’s commitment to creating a dynamic digital consumer finance ecosystem where consumers can seamlessly access the financial tools and insights they need, while also enabling financial institutions to engage with customers more effectively,” said MoneyLion Co-Founder and CEO Dee Choubey. “By integrating our leading platform with TransUnion’s credit data solutions, we can offer consumers more personalized and relevant financial products that meet their unique needs at every stage of their financial journey.”

The Streamly Fintech Insights series provides analysis and discussion on major issues impacting banks, credit unions, fintechs, and financial services providers of all kinds.

Featuring senior leaders in fields ranging from banking to venture capital to media strategy, the Streamly Fintech Insights series offers a look into the innovative technologies that are helping financial institutions turn challenges into opportunities for themselves and their customers.

This week, we’re showcasing four new discussions from Streamly’s Fintech Insights series.

Embedded Finance with Eric McCabe, Head of Embedded Finance, Citizens Bank; and Amber Gerstung, Senior Managing Director, Head of Embedded Payments, SVB.

What’s Hot and What’s Not at FinovateSpring with Jason Henrichs, CEO, Alloy Labs; Alenka Grealish, Co-Lead Generative AI Research, Celent; and Charles Elkan, Professor of Computer Science, University of California.

Financial services software provider Finastra has teamed up with onboarding specialist Prelim.

Courtesy of the partnership, Finastra will integrate Prelim’s technology into its Finastra Phoenix core solution to enhance the account opening experience.

Finastra was formed via a merger between Misys and D+H in 2017. Prelim made its Finovate debut in 2022.

Financial services software company Finastraannounced a partnership with onboarding specialist Prelim. Finastra will integrate Prelim’s technology into its Finastra Phoenix core solution to enhance the deposit account opening experience for both retail and commercial accountholders.

“In a digital-first society, consumers and businesses expect their financial solutions to be agile and transform as needed to keep pace with their needs,” said Peter Longo, VP of Product Management for U.S. Mid-Market Banking Solutions at Finastra. “As we look to continuously enhance our offerings, Prelim is a trusted partner to support this transformation and our Open Finance ecosystem. We look forward to working together to deliver the innovations community banks and credit unions across the United States need to stay ahead of the competition.”

Prelim’s technology automates the application process, as well as internal processes such as reviewing, processing, underwriting, and servicing. This accelerates account opening and simplifies complex back-office operations. Prelim integrates seamlessly with Phoenix APIs, and newly created accounts are reflected in the digital banking solution, ensuring a cohesive, user-friendly experience.

“Customers expect an easy-to-use, real-time onboarding process when applying for a new financial product or service,” Prelim CEO and Co-Founder Heang Chan said. “We’re excited to be partnering with Finastra to help accelerate retail and commercial deposit account opening for financial institutions around the world.”

Finastra was forged in 2017 as a result of the integration between Finovate alum Misys and D+H. Headquartered in the U.K., the company provides financial services software applications for payments, lending, treasury, capital markets, and both retail and digital banking. Finastra has more than 8,100 clients in 130 countries, including 45 of the world’s top 50 banks.

In recent months, Finastra has forged partnerships with technology consultancy and digital solution provider Tech Mahindra, supply chain finance platform CredAble, and full-cycle verification platform Sumsub. The company’s technology powered new offerings like cloud-first ORO Bank of Bhutan and Bank Midwest’s digital-only OnePlace.bank. Finastra introduced Mike Stawchansky as its new Chief Technology Innovation Officer in March.

Prelim made its Finovate debut at FinovateSpring 2022. At the conference, the San Francisco, California-based fintech demonstrated its white-labeled platform that helps banks build more than 100 financial apps and digital experiences for customers and members. Prelim’s clients use the platform to add deposit accounts, treasury services, credit cards and more to their offerings. Point-to-point integrations enable Prelim to orchestrate and automate KYC, KYB, and AML in real time.