This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

A look at the companies demoing at FinovateFall on September 13-15, 2021. Register today and save your spot.

Cinchy dataware platform’s unique approach of decoupling data from applications removes data silos and the need for integration.

Features

Delivers change 5x faster

Reduces IT overhead by 50%

Includes flexible data models that can evolve with business needs

Why it’s great Dataware is a new concept whose benefits are already being leveraged by leading financial services organizations and the top global banks by moving from an app-centric to a data-centric approach.

Presenter

Dan DeMers, CEO & Founder DeMers is CEO & Founder of Cinchy, the dataware platform that makes integration obsolete. For over a decade, DeMers has built large IT systems for FIs worldwide. LinkedIn

A look at the companies demoing at FinovateFall on September 13-15, 2021. Register today and save your spot.

IMPESA is a software developer fintech. Monibyte is a P2P payments app that offers customers card controls and offers banks new revenue opportunities.

Features

Integrated finance controls that include transaction controls

P2P plus in-app split transactions with social experience

Affordable for small financial institutions

Why it’s great Monibyte is an affordable and time-to-market solution for small financial institutions. It creates a new revenue channel and leadership in innovation and benefits for clients with minimum investment.

Presenters

Mario Hernández, CEO & Co-Founder Hernández is an expert in payments solutions focusing on new technologies and innovation. He has had a successful trajectory in the financial sector in several countries. LinkedIn

Gloriana Carballo, PR & Marketing Director Carballo has extensive experience in marketing, retail, and market strategy. At roughly 28 years, she was named one of the ‘Top 5 Oustanding Women in Business in Costa Rica’ by EKA magazine in 2017. LinkedIn

A look at the companies demoing at FinovateFall on September 13-15, 2021. Register today and save your spot.

Informed.IQ automates the consumer loan verification process for lenders using AI.

Features

Faster funding

Ability to free up staff to work on higher-order functions

Greater accuracy and reduced fraud

Why it’s great Informed.IQ is used nation-wide across major consumer lenders such as Ally Bank and Westlake Financial to turn their applicants’ documents and data into decisions.

Presenter

Justin Wickett, CEO & Co-Founder Prior to founding Informed.IQ, Wickett led product management at Credit Karma, Lyft, and Zynga. He has a bachelor’s in Computer Science from Duke University and holds several U.S. patents. LinkedIn

A look at the companies demoing at FinovateFall on September 13-15, 2021. Register today and save your spot.

Directlink is an AI-powered conversational banking platform built to transact, deal, and direct seamless experiences for bank and credit union customers – whenever and wherever they like.

Features

Control dialog and content in an easy-to-use portal

Transform and test customer experiences across channels

Take action on data insights in real-time

Why it’s great Directlink makes it easy for banks and credit unions to devise, deploy, and maintain intelligent automated banking experiences for their customers without burdening their human team members.

Presenters

Mark Vanderpool, President Vanderpool is a leader and team builder with enterprise, channel and on-demand, and SaaS success. In addition to true operational experience, he has extensive experience with omni-channel communications. LinkedIn

Ben Nichols, Head of Product Nichols leads the product and technology departments at Directlink by IMS. He has over a decade of experience building data-driven software for both large financial institutions and SaaS startups. LinkedIn

A look at the companies demoing at FinovateFall on September 13-15, 2021. Register today and save your spot.

Income Discovery increases a client’s retirement paycheck by as much as 30% by using AI to optimize strategies and simplify execution of the strategy.

Features

Maximum paycheck in retirement – increase by as much as 30%

Powerful one-click AI based optimization engine

Scalable paycheck disbursals for planned and unplanned spending

Why it’s great Income Discovery solved the “nastiest, hardest problem in finance” by using AI to simplify the solution for increasing a client’s retirement paycheck by as much as 30%.

Presenter

Manish Malhotra, CEO & Founder Prior to forming Income Discovery, Malhotra was a Senior VP at Citigroup Global Wealth Management, leading the application architecture function for strategic initiatives. LinkedIn

A look at the companies demoing at FinovateFall on September 13-15, 2021. Register today and save your spot.

Thinknum provides a real time alternative web data index for CIOs.

Features

Generate real-time insights about private and public companies via UI and API

Access 5+ years of history of alt web data on 500,000 companies updated daily

Visualize your insights and share dashboard

Why it’s great Thinknum democratizes access to alternative data with an easy-to-use interface and API deployment at scale.

Presenter

Marta Lopata, Chief Growth Officer Lopata is the Co-Founder and Chief Growth Officer at Thinknum Alternative Data and KgBase – a no-code knowledge graph tool. LinkedIn

A look at the companies demoing at FinovateFall on September 13-15, 2021. Register today and save your spot.

BANYAN creates an at-scale network that allows retailers to share receipt data with banks and fintechs through both API calls for individual transactions and batch calls for unlimited records at a time.

Features

The individual receipt gets matched to a transaction

The Scale of BANYAN today

The integrations are super clean and easy

Why it’s great We get you SKU level data, and you can use it for any use-case within your organization as long as you conform with our data rights.

Presenters

Jehan Luth, CEO & Founder Luth has a background touching receipt level data from multiple verticals. He worked in CPG while at Campbell’s Soup and fintech/OCR while building receipt capture apps for clinical trials at med school. LinkedIn

Wil Schobeiri, CTO Schobeiri brings over 15 years of technology, product management, and leadership experience to BANYAN, including CTO. He also had CPO roles at MediaMath and Revantage (a Blackstone company). LinkedIn

Our Women in Fintech Series continues with an interview featuring Kathryn Petralia, co-founder of Kabbage, an American Express Company.

We caught up with Kathryn Petralia to discuss her journey to success as the co-founder of Kabbage, an American Express Company, how alternative lending is democratizing access to financial services, and the importance of advocating for inclusion for every employee and end user.

Can you tell us how you got involved in fintech?

Kathryn Petralia: I was always interested in technology, its possibilities and impact, but I never considered it a career until much later. I was on track to earn a masters degree in English when a family friend asked me join a tech company he had invested in at the time. I ended up ditching the graduate program to take advantage of the opportunity.

From there I spent close to 15 years working in the credit, payments, and e-commerce industries, leading strategy and corporate development, as well as founding multiple companies. When my co-founder, Rob Frohwein, approached me about the idea of Kabbage, I immediately saw the potential to help small businesses gain access to capital via real-time data.

What drew you to the world of alternative lending?

Petralia: I’ve been in alternative lending since the late ’90s, and my passion for helping small businesses has always been a driving force.

I was drawn to alternative lending as it’s a very interesting area of financial services that was ripe for disruption as new technologies paved a path to give customers a better experience.

At the time, I could see that automation and access to real-time data could do away with the lengthy, manual processes which were the status quo in the industry, and democratize access to financial services.

Where did you find support as you were starting out?

Petralia: It’s important to have a strong partner and support system at home and in the office. I’ve been fortunate that my husband has been an at-home dad for our kids. And I’m an advocate of having a co-founder in business, someone that compliments one another’s strengths and weaknesses, and I’ve been lucky to have Rob a part of this journey.

Kabbage has grown into a hugely successful company. Can you share some of the challenges you have faced on your journey?

Petralia: It was very challenging to raise money when we first launched Kabbage, especially in Atlanta where the venture community was small and there was not a lot of competition at the time. This unfortunately tends to drive down company valuations. It was hard to get Silicon Valley investors behind Atlanta businesses, but we ultimately succeeded and really raised the profile of Atlanta as a fintech and startup hub.

What advice do you have for small businesses coming through the pandemic?

Petralia: While businesses were forced to adapt their processes to stay afloat during the pandemic, it’s crucial for them to continue evolving for long-term success. According to our Small Business Recovery Report, 77 percent of small businesses agreed they’re more open than ever before to replace old systems and adopt new technologies to run their company more efficiently.

Be nimble in the face of uncertain circumstances and adopt new technologies that will aid in the success of your business.

Where do you see fintech heading in the next 12 months?

Petralia: The pandemic highlighted where small businesses have cash flow gaps and operational blind spots, so fintechs should shift their focus and offer more comprehensive solutions that address these concerns. Offering a full suite of solutions and integrated platforms can provide business owners with the tools they need to solve their immediate needs while instilling more confidence in how they run their company with data.

What more do you think can be done to support women in fintech?

Petralia: There is so much more we can do to create equality in fintech. The gender disparity in fintech is due, in part, to the tendency of white-male-dominated industries to invest in other white-male-dominated businesses (which is of course true for technology companies generally). We can ensure this situation doesn’t endure by building inclusive products and encouraging leaders to make diverse hires. It’s crucial that we continue promoting policies and products that minimize biases and create a more inclusive industry.

What advice would you give to women starting their careers in the industry now?

Petralia: Women in Fintech must advocate for inclusion not just for leadership, but also for every employee and end user. But as for those women—or men, frankly— just joining the industry or pursuing their goals, I always advise to really take the time to be the smartest about your field, job, or industry. That will earn you seats at tables and trust among executive teams that will help propel you and your career.

Courtesy of Blackhawk Network, championship-winning professional athletes aren’t the only ones headed to Disneyland. The branded payments solution provider announced late last week that it is leveraging its proprietary ScanIt solution to power retail ticket purchases using QR codes. Moreover, among the first customers of this new offering is none other than Disneyland, which will offer QR code ticket sales in major retailers throughout the state of California.

“Shoppers’ comfort with QR codes exploded in the last year,” Helena Mao, VP of global product strategy at Blackhawk explained. “Now, as consumers return to in-person entertainment, we are pleased to continue the innovation around QR codes with the introduction of entertainment and amusement park ticketing.”

Amusement parks are only one use case of Blackhawk’s technology. The company’s solutions can also be applied to other experiences that have historically relied on paper tickets, such as music concerts, museums, zoos, and other forms of live entertainment. Contactless, QR code-based payments also support the public’s growing preference for purchasing goods and services in the analog world the same way that they do in the digital world. Research conducted by Blackhawk, for example, suggests that 73% of consumers surveyed would prefer “online” payment methods – even when shopping “in-store.”

“Our technology affords retailers the luxury of a content selection that is no longer hindered by physical space,” Mao added. “And it gives shoppers access to a broader selection of digital content, such as e-tickets and digital gift cards, within a convenient purchase experience.”

To this end, Blackhawk Network has spent 2021 forging partnerships with a variety of companies. This year, the firm has teamed up with eGifting company Givingli, supermarket Tops Friendly Markets, digital asset marketplace Bakkt, and apparel retailer UNTUCKit. Most recently, technology from Blackhawk Network has been deployed to enable both PayPal and Venmo bring additional digital payment options to leading supermarket retailer Giant Eagle.

Blackhawk Network was founded in 2001, and has been a Finovate alum for almost ten years. A publicly traded entity on the NASDAQ – under the ticker “HAWK” – Blackhawk Network has a market capitalization of $2.5 billion. This year has featured a number of C-suite changes for the Pleasanton, California-based company, appointing former Google executive Nikhil Sathe as Chief Technology Officer in February, Cory Gaines as Chief Product Officer in May, and David McLaughlin as Chief Financial Officer in June.

A look at the companies demoing at FinovateFall on September 13-15, 2021. Register today and save your spot.

Signal Intent is reimagining financial guidance for the digital age. The company’s innovative platform transforms how banks and lenders engage customers at scale.

Features

Financial tools to engage and convert more customers

Shift from reactive to proactive marketing

Powerful customer data to prequalify and send relevant offers

Why it’s great With millions of customer interactions happening every month, we’re building data models that empower banks to deliver personalized marketing and build stronger customer relationships.

Presenter

Matthew Covi, CEO & Co-Founder Previously the Head of Growth at Stash, a fintech unicorn, Covi is now focused on reimagining financial guidance for the digital age. LinkedIn

A look at the companies demoing at FinovateFall on September 13-15, 2021. Register today and save your spot.

DocFox is a SaaS business serving over 200 banks, fintechs, and credit unions helping them to onboard and perform ongoing due diligence for business and complex accounts.

Features

Seamless omni-channel account opening lets new clients interact online or in-branch

Document collection and review, allowing you to open accounts smoothly

Incredible client experiences

Why it’s great DocFox is onboarding technology that creates incredible client experiences with ZERO manual effort and can intelligently read ANY document enabling automated business account opening.

Presenter

Ryan Canin, CEO Canin is the CEO of DocFox, a digital tool which enables rapid account opening, customer onboarding, and automated complex workflows for business and commercial banking. LinkedIn

A look at the companies demoing at FinovateFall on September 13-15, 2021. Register today and save your spot.

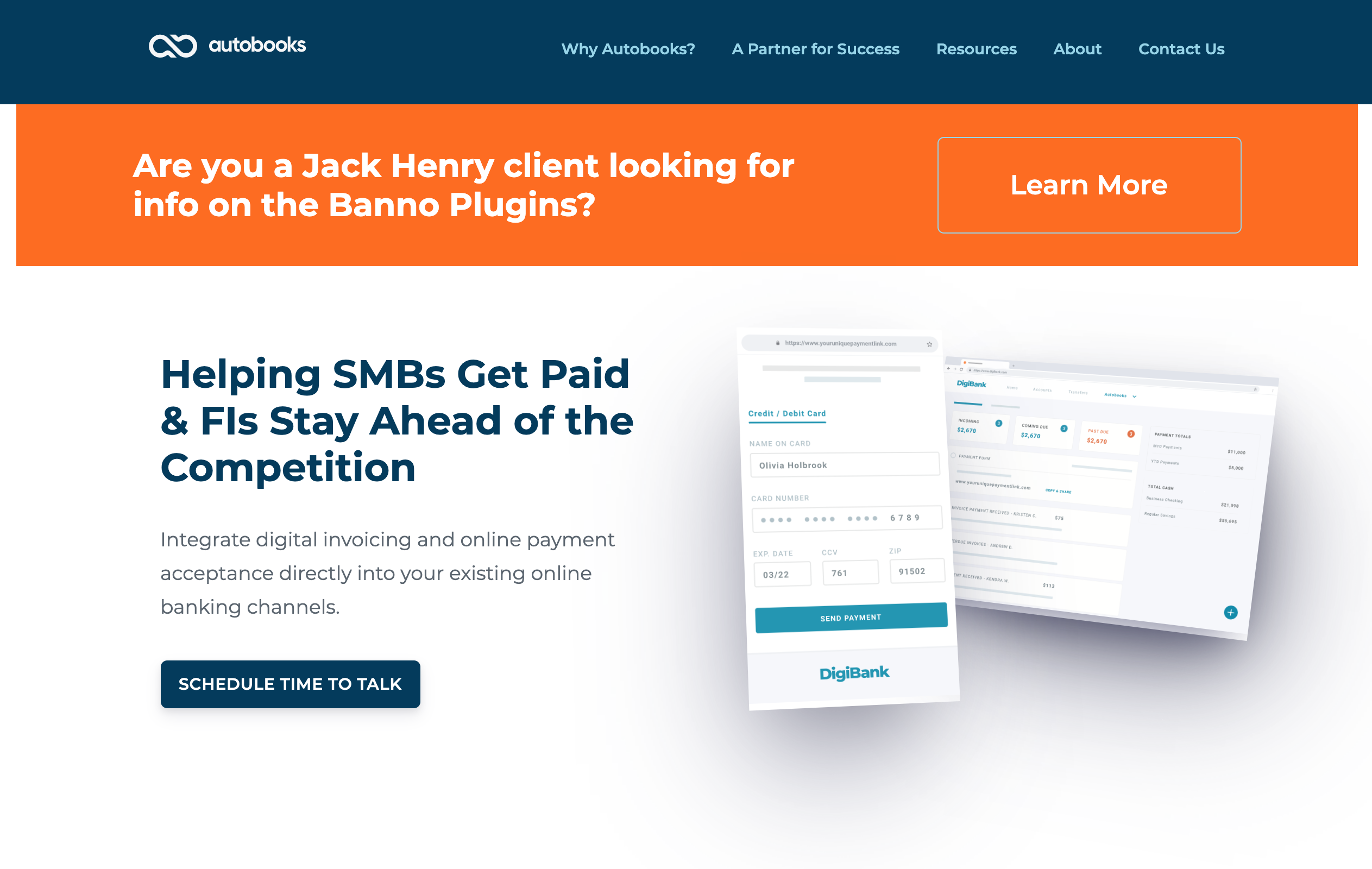

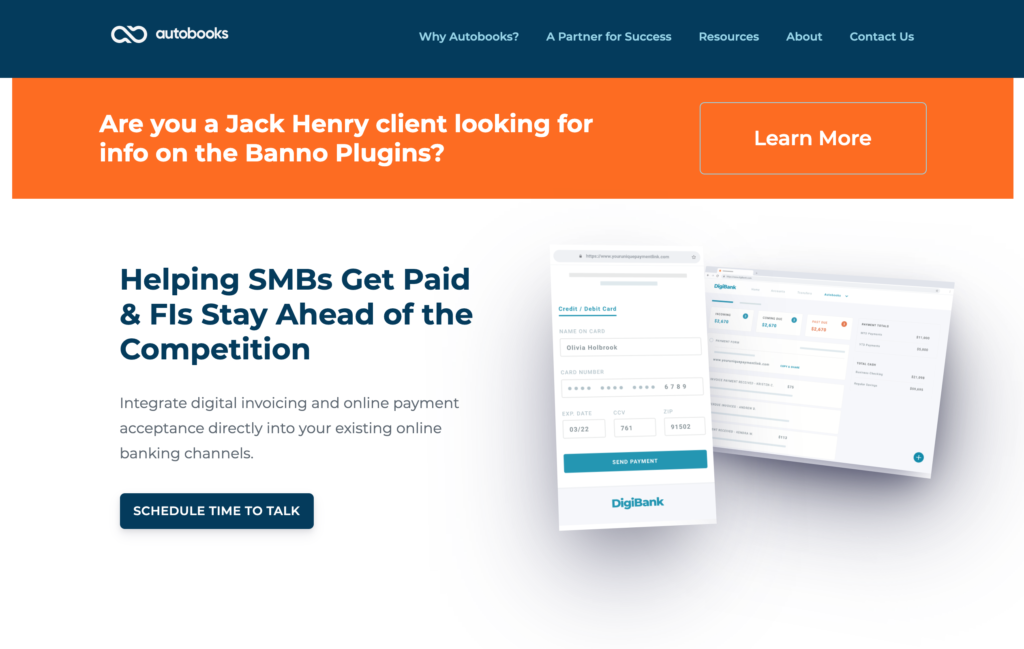

Autobooks‘s embedded modules for small businesses allows them to send digital invoices and accept online payments directly from a financial institution’s mobile or online banking application.

Features

Digital Invoicing

Online payment acceptance

In-app payment acceptance

Why it’s great This new innovation directly integrates within the banking channel.

Presenters

Steve Robert, CEO & Founder Robert is an accredited investor, adviser, and board member, who actively coaches, speaks, and blogs about start-ups, technology and entrepreneurship. LinkedIn

Jo Jagadish, Head of Corporate Products, Services, & Innovation Jagadish is the Head of Commercial Products and Innovation for TD Bank including Deposits, Cash Management, Global Trade Finance, Revenue Management, Product Sales Support, Servicing, and Implementations. LinkedIn