This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

SEON is giving away its fraud prevention tools for free.

The free tier will include up to 2,000 API calls each month at a rate of two queries per second.

“We’re determined to tackle fraud head on,” said SEON CEO and Co-founder Tamas Kadar. “This version will help us to serve a greater number of online businesses than ever before, and it is a major step towards building a truly fraud free world.”

Online fraud prevention platform SEON‘s mission is to democratize the fight against online fraud for businesses of all sizes. Today, the Hungary-based company is furthering its efforts toward this goal by giving away fraud prevention tools for free.

The Forever Free version of its online fraud prevention software will support up to 2,000 API calls each month at a rate of two queries per second and includes email support from SEON’s customer service agents.

“We’re determined to tackle fraud head on,” said SEON CEO and Co-founder Tamas Kadar. “This version will help us to serve a greater number of online businesses than ever before, and it is a major step towards building a truly fraud free world.”

SEON has always offered businesses free access to its technology via a 14-day free trial. Starting today, after a user’s trial period expires, they will automatically be converted to SEON’s Forever Free plan. Businesses that want more capabilities can convert to SEON’s Pro plan, which offers more API calls and responses around 10 queries per second, for businesses with higher transaction volumes and a need for a faster speed.

“As a company, we make it tough for fraudsters by intelligently combining real-time social signals, phone, email, and IP lookup details with device intelligence and machine learning to uncover fraud patterns and discover revenue opportunities. We enable fraud prevention teams to go further with access to insightful, real-time data from one source.”

SEON doesn’t think of itself as a typical fraud prevention company. The company’s business model is based on a product-led growth (PLG) strategy via a software-as-a-service (SaaS) model, which makes the technology more accessible to a wider range of businesses.

“Sadly, for too long, this level of protection has only been available at a very high price point. That’s why for years, we’ve strived to make our service as accessible as possible. Through our ‘forever free’ option we’re able to go even further in that effort,” Kadar added.

The second half of the year has been a busy one for SEON. In the past couple of months, SEON has formed partnerships with SaaS anti-money laundering company, Lucinity and AI-powered decisioning platform, Provenir. And in the last few weeks, the company has made several updates to its system, including improving the accuracy of its IP, BIN, email, phone, and platform checks.

Sometimes “futuretech” means technology that helps ensure that we actually have a future!

This week we’re taking a look at recent initiatives in the fintech world to help promote sustainability. These efforts have been growing as more and more companies respond to customer concerns about the impact of their financial behavior on the climate. From technology that helps consumers measure and track their carbon footprint to new payment cards that eschew plastic for renewable, environmentally-friendly materials, businesses in the fintech industry have pursued a wide variety of strategies in support of “climate consciousness.”

The news that the Bank of Ireland has begun issuing new bio-sourced debit cards is one of the latest examples of this trend. The cards are made from 82% bio-source renewable materials such as field corn and decompose in months – compared to plastic, which lasts for hundreds of years. The cards will be available to both personal and business customers and the Bank of Ireland expects its entire portfolio to be switched over to the bio-sourced cards by 2026.

“The environmental credentials of these bio-sourced cards are exceptionally strong and with 60,000 already being used by third-level students, we will now radically expand the rollout across our entire cards business in Ireland and the U.K.,” Bank of Ireland Chief Sustainability & Investor Relations Officer Eamonn Hughes said.

The Bank of Ireland expects to save 17 tons of CO1 and nearly four and a half tons of plastic every year with the new initiative. The Bank first issued bio-sourced debit cards for third level students in September 2020. In addition to the new bio-sourced cards, the Bank of Ireland also announced that it was upgrading its card designs to make it easier for users to correctly insert the cards in machines and ATMs.

The decision to pursue bio-sourced cards is based in part on research the bank conducted on young shoppers over the past year. The Bank learned that 63% of those in Ireland between the ages of 18-25 have become “more aware of shopping sustainably” over the past 12 months. Additionally, more than half of those surveyed, 54%, said they were “happy to pay more for sustainable goods.”

In other fintech sustainability news, Zurich-based F10 is hosting what it calls the world’s first climate-focused fintech incubator in the Nordic region. The six-month program will feature startups from the U.K., Israel, Sweden, Lithuania, Switzerland, and Canada that are innovating in areas ranging from sustainable investing to waste trading. Head of F10 Nordics and Baltics Anders Norlin said, “the variety of climate fintech solutions presented reinforces the interest for more innovative solutions in the needed transition towards a net zero society.”

The startups participating are: Azzera (Canada), Eljun (Sweden), GreenGrowth (U.K.), OCO (Lithuania), Spritju (Sweden), SustainSME (Switzerland), Weather It Is (Israel), and Xworks (U.K.).

U.K.-based digital challenger bank Tandem launched its Tandem Marketplace this week. The new offering is a consumer-based hub for information on how to live a more sustainable life with tips on everything from retrofitting your home to keeping energy costs low. For example, among the tools available on the Marketplace are an EPC (“energy performance certificate”) checker to help U.K. homeowners understand their EPC and learn ways to improve it.

“We are in the middle of a climate crisis and a cost-of-living crisis,” Tandem Chief Impact and Marketing Officer Georgina Whalley said. “People shouldn’t have to choose between heating and eating. This is why we have created our Marketplace, people need more information and support to make greener choices.”

Tandem Marketplace is only the most recent sustainability initiative the bank has pursued. In September, Tandem Bank announced that it had joined the Coalition for the Energy Efficiency of Buildings (CEEB) sponsored by the Green Finance Institute. The coalition consists of more than 300 businesses and organizations from finance, policy, and civil society, working to develop a market for financing net zero carbon and climate resilient buildings in the U.K.

“This is a brilliant opportunity for Tandem to join leaders across a range of sectors to develop green and innovative financial products that will address the retrofit investment gap,” Tandem Bank CEO Susie Aliker said. “With over 28 million homes in need of retrofitting by 2050, collaboration is key to successfully tackling Net Zero targets.

Founded in 2014, Tandem is one of the U.K.’s original digital challenger banks.

The role of state-based organizations in helping foster fintech innovation in their communities is often overlooked. For years, one such organization, JobsOhio, has helped bring attention to the opportunities available to fintech entrepreneurs throughout the state of Ohio. The private development corporation also works to encourage investment in the state’s most innovative businesses – from advanced manufacturing to insurtech. As remote work has expanded in recent years, more and more founders and professionals have turned from Silicon Valley and New York to cities in states like Ohio to launch new businesses and begin new careers.

This year at FinovateFall we sat down with Ron Rock, Senior Director of Insurance/Insurtech with JobsOhio to talk about the organization’s role in driving fintech innovation in Ohio, and what the Buckeye State has to offer both fintech entrepreneurs and fintech investors.

On the impact of remote work on fintech and financial services

In financial services, it seems like we have the ability to be remote. We’re not a “build a building, fill it full of people” kind of industry. So being able to work remotely is very easy in the financial services space – especially when you’re stretching into some of the tech strategies that we have … On the other side, there are some banks and insurance companies that are quick to get people back into the office. They love the camaraderie. They love the collaboration.

On the rise of Ohio as an fintech innovation hub

We fund three different innovation centers in the state. We have one in Cincinnati, one in Columbus, and one in Cleveland that are being developed right now. There’s a lot of collaboration in the healthcare space, in the true IT space. So, in the financial services space, we think that being close to that innovation is very key. What I’m trying to do is recruit some of those (financial services) companies to utilize those innovation centers, get close to that innovation because, I know it’s kind of corny, but innovation breeds innovation.

On the advantages of launching new fintechs in Ohio

What you have is that you’re close to about two-thirds of the financial services sector in Ohio. So, within a day’s travel you can be anywhere you want to be within the financial services ecosystem in the midwest. What we’re also trying to do is highlight with our venture capitalists that fintech and insurtech is a space that is going to provide some really good ROI. We’ve got a lot of venture capital in the state. When you think of venture capital, you tend to think of Silicon Valley or New York. But we’re trying to get really strong in the state of Ohio, as well.

Digital banking solutions provider Moneythor launched a new engagement tool for wealth managers.

The new offering is designed to help wealth managers leverage client data to create more personalized experiences that help customers build their wealth.

Moneythor was a finalist in this year’s Finovate Awards in the “Best Fintech Partnership” category.

Moneythor, a Finovate Awards finalist this year in the “Best Fintech Partnership” category (in collaboration with Standard Chartered), unveiled a new tool for wealth managers this week. The offering is an add-on module to its data-driven personalization and digital engagement solution, and is designed to help wealth managers increase loyalty and NPS, as well as lower the costs and boosting revenues.

Moneythor’s digital engagement tool aggregates a sizable range of user data – from retail accounts and payment cards to lending products and investment portfolios, and more. This data is then processed by the Moneythor platform to generate and provide insights, recommendations, and alerts – at scale and in real-time. This gives customers the kind of contextual and actionable information they need in order to better manage and grow their finances. Customers can also take advantage of the configurable conduit to update their risk profile, compare their portfolio’s performance against model portfolios, as well as consider and incorporate investment advice.

“Adding the ability to deliver personalized experiences across investment journeys was a natural evolution of our solution aiming to address the needs of financial services customers across all segments including retail, SME and now wealth,” co-founder and CEO of Moneythor Olivier Berthier said. “We are excited by the interest we have seen from our clients and partners for these new features, and how important personalization and digital engagement are now to their wealth management strategies.”

Founded in 2013 and headquartered in Singapore, Moneythor has spent the fall of 2022 inking partnerships with the likes of Trust Bank, a digital financial institution headquartered in Singapore, and Australia’s National Australia Bank (NAB). In May, Moneythor teamed up with Finovate alum Thought Machine, which selected Moneythor among the initial partners for its Integration Library, a suite of curated integrations that are interoperable with Thought Machine’s Vault Core. Moneythor began this year announcing collaborations with The Saudi Investment Bank (SAIB) and carbon footprint tracking company Cogo.

In addition to its Singapore headquarters, Moneythor maintains offices in Paris, Sydney, Dubai, and Tokyo. The company’s solutions are used by financial institutions around the world, including in developing markets such as Indonesia, India, and Malaysia.

Open banking company MX and real-time payments player Orum have formed a partnership.

The agreement integrates Orum’s money movement API with MX’s instant account verification and balance check capabilities.

Combining these technologies will enable fintechs to embed real-time payment capabilities into their own offerings.

Open banking company MXannounced a partnership with real-time payments player Orum this week that will enable it to provide real-time payments and money movement capabilities for fintechs.

The agreement integrates Momentum, Orum’s money movement API, with MX’s instant account verification (IAV) and balance check capabilities. This combination will enable fintechs to embed instant payments capabilities for transactions in any direction, at any time.

“More than ever, fintechs and verticalized payments companies are looking for innovative solutions that automate and simplify money movement, from unlocking instant and risk-mitigated on and off ramps, to optimizing the customer experience through instant availability of funds and payouts,” said Orum Chief Revenue Officer Rouzbeh Rotabi. “By partnering with MX, Orum is further enhancing the ability to offer the best experience for developers who value simplicity and security, and end-customers who want instant funds availability.”

Orum offers a unified money movement API that uses in-house payments intelligence to manage risk and orchestrate complex, multi-rail transfers. The company offers settlement in as little as 60 seconds. This is the first partnership announcement I’ve seen from Orum, which offers use cases for crypto exchanges, brokerage firms, gig platforms, insurance companies, consumer lenders, and banks. Founded by Stephany Kirkpatrick, the company entered the market with its flagship product, Foresight, in 2020. To date, Orum has raised $82.2 million in funding from the likes of Inspired Capital, Bain Capital, Accel, Canapi Ventures, and others.

Founded in 2010, MX has positioned itself in the open finance space, offering account aggregation and data access products alongside its mobile banking and money management tools. When used in conjunction with Orum’s instant payment technology, MX’s IAV and balance check capabilities will help fintechs verify and aggregate consumers’ financial information quickly and securely.

“Orum offers fintech and financial institutions access to smarter, simpler, and faster payments,” said MX Executive Vice President, Channel Partnerships Raymond den Hond. “MX and Orum’s shared commitment to enabling best-in-class financial experiences and outcomes through cutting-edge platforms makes this a natural partnership. We are excited to grow and expand our capabilities together to meet the most pressing needs of fintechs and payments companies.”

Legal & General and Lloyds Banking Group have invested $40 million (£35 million) in open data and payments platform Moneyhub.

Along with the equity capital, Moneyhub received an additional $5.7 million (£5 million) debt facility courtesy of Shawbrook.

Moneyhub made its Finovate debut at FinovateEurope in 2015 in London. Samantha Seaton is CEO.

The $40 million (£35 million) in funding raised by open finance and payments platform Moneyhub will give minority stakes to investors Legal & General and Lloyds Banking Group. The two backers will leverage their relationship with Moneyhub to enhance their own offerings with Moneyhub’s open data technology. At the same time, the capital, along with an additional $5.7 million (£5 million) debt facility courtesy of Shawbrook, will enable Moneyhub to speed development of its products in areas ranging from pensions and payments to affordability and Data-as-a-Service. The funding will also support Moneyhub’s plans to further international expansion.

“(The) new investment helps us signal a step change in the way the financial services industry thinks about Open Data and the possibilities it presents,” Moneyhub CEO Samantha Seaton said. “Understanding and utilizing customer transaction data for the benefit of the customer’s financial wellbeing not only helps businesses fulfill their Consumer Duty regulatory obligations, but also empowers them to create further opportunities.”

Moneyhub enables companies to transform data into personalized digital experiences and initiate payments. Offering both APIs and its customizable Open Data Platform, Moneyhub serves businesses in industries from pension companies and wealth managers to banks, lenders, and insurance companies. Moneyhub boasts seamless, single source connectivity to thousands of financial institutions in 37 countries, helping ensure its clients can build a comprehensive portrait of their customers’ financial needs, habits, and goals.

Moneyhub’s largest funding round to date, this week’s capital infusion is part of a larger fundraising effort and follows a 2021 investment of $18 million led by Peter Wood, founder of Direct Line and Esure. At the time, the funding was the largest secured by a female fintech CEO in Europe that year. Moneyhub currently has more than $63 million in capital raised, according to Crunchbase.

Moneyhub made its Finovate debut in 2015 at FinovateEurope in London. Founded in 2011 and headquartered in Bristol, the company also announced this week that it was teaming up with SME health and wellness care provider MorganAsh. The support services provider will use Moneyhub’s technology to access customer financial data to enhance their ability to provide real-time consumer vulnerability assessments. The partnership will also help MorganAsh fulfill its obligations for Consumer Duty, a requirement issued by the U.K. Financial Conduct Authority in July that governs implementation of open finance/open data products.

“Consumer Duty and Open Finance herald a new era of customer-focused firms and financial resilience,” Moneyhub Business Development Director Vaughan Jenkins said. “Smart, forward-looking businesses will seize this moment and benefit from it.”

MoneyGram is enabling its customers in (nearly all of) the U.S. to buy, sell, and hold cryptocurrencies via their MoneyGram apps. Three cryptocurrencies – Bitcoin (BTC), Ethereum (ETH), and Litecoin (LTC) – are the digital assets available courtesy of the new service. MoneyGram expected to offer other cryptocurrencies in 2023.

“Cryptocurrencies are additive to everything we’re doing at MoneyGram,” Chairman and CEO Alex Holmes said. “From dollars to euros to yen and so on, MoneyGram enables instant access to over 120 currencies around the globe, and we see crypto and digital currencies as another input and output option.”

The new service is made possible thanks to MoneyGram’s partnership with licensed crypto exchange, crypto-as-a-service provider, and new Finovate alum Coinme. The company’s alliance with Coinme extends back to 2021, when the two firms teamed up to expand access to cryptocurrencies by establishing thousands of U.S. locations where consumers can use cash to buy and sell bitcoin.

Coinme demoed its crypto-as-a-service solution at FinovateSpring earlier this year. MoneyGram made a “strategic investment” in the Seattle, Washington-based company in January. The amount of the investment was not disclosed.

Revolut Enables Crypto Spending for Debit Card Holders

MoneyGram isn’t the only company busy making it easier for its customers to participate in the cryptocurrency market. Revolut debit card customers in both the U.K. and Switzerland will now be able to alternate between crypto and fiat purchases both online and offline.

“This year we have not only increased the number of cryptocurrencies available in the Revolut app to close to 100 tokens and launched Crypto Learn & Earn education courses enjoyed by millions of our customers,” Revolut crypto general manager Emil Urmanshin said. “Now we are making crypto even more mainstream by empowering people to use crypto-enabled cards to spend their tokens for everyday purchases.”

To enable the capability in the Revolut app, customers open the Cards section and select one of their existing physical or virtual cards. Customers then enter the card’s settings function and changes the setting from fiat to one of the nearly 100 supported cryptocurrencies. Once linked, a crypto-enabled card will process the transaction using the preferred digital asset. Revolut’s crypto-enabled cards will offer a 1% cashback on all purchases for a promotional period. Customers are also able to order a dedicated virtual or physical card specifically for crypto payments.

About That Blockchain … Lex Fridman Interviews Balaji Srinivasan

If you’re looking for something to listen to while on your drive from Los Angeles to San Francisco (and halfway back), then this 7+ hour discussion between Lex Fridman and former Coinbase CTO – and current angel investor – Balaji Srinivasan may be just what you’re looking for!

Failing that, skip ahead to 6:40:42 or so in this extended interview to listen to Srinivasan talk about the present and future of cryptocurrencies, AI, AR, and VR.

Blockchain Platform Paxos Gets Green Light in Singapore

Blockchain infrastructure platform Paxossecured a license from the Monetary Authority of Singapore this week. The license will enable the company to offer digital payment token services to companies based in Singapore. The license – made possible courtesy of the Payment Services Act of 2019 – also makes Paxos the first U.S.-based blockchain infrastructure platform to earn regulatory approval in both New York and Singapore.

Paxos Asia CEO and co-founder Rich Teo underscored the company’s commitment to “innovating within regulatory frameworks”. Teo said, “We believe blockchain and digital assets will revolutionize finance for everyone around the world, but development of this technology must have clear oversight and consumer protections.”

Paxos offers tokenization, custody, trading, and settlement of digital assets. The company builds enterprise blockchain solutions for financial institutions such as PayPal, Nubank, and Bank of America. Paxos launched the first regulated cryptocurrency exchange, itBit, in 2012. The company issued the world’s first regulated stablecoin, PAX (now known as USDP) in 2018.

Eswatini’s Central Bank to Explore CBDCs

Did you know that the country formerly called Swaziland is now “Eswatini”? If not, then consider this news that the Central Bank of Eswatini (CBE) has teamed up with Giesecke+Devrient (G+D) to research development of a Central Bank Digital Currency (CBDC), a twofer.

Located in southern Africa and bordered by Mozambique and South Africa, the Kingdom of Eswatini is one of a number of developing economies that has expressed interest in CBDCs in recent years. The country’s central bank inked an agreement with G+D this week that calls for research into the practicality of developing and implementing a CBDC in the country. The CBE will also explore the possibility of issuing digital Lilangeni to complement the country’s banknotes and coins, the dominant forms of payment among the nation of 1.2 million people.

The relationship between the bank and Munich, Germany-based G+D extends back to a time before cryptocurrencies were a significant part of the fintech conversation. G+D Currency Technology CEO Dr. Wolfram Seidemann highlighted the “long history of trusted collaboration” – of more than 40 years – between the Central Bank of Eswatini and Giesecke+Devrient. “The Kingdom of Eswatini is among the first African countries to take the step towards a retail CBDC and we are honored to support this journey towards digital public currency with our expertise,” Seidemann said.

Once the deal is finalized, Bluefin and TECS will serve a combined 34,000 merchants and close to 300 global partners in 55 countries. And for both Atlanta, Georgia-based Bluefin and Austria-based TECS, the acquisition will expand their geographical footprint.

“We are delighted to welcome TECS’ employees, customers and partners to Bluefin,” said Bluefin CEO John M. Perry. “This combination brings together two companies that focus relentlessly on meeting merchant needs for next-generation payment processing and management as well as the secure exchange of PHI and PII data with PCI-validated encryption and tokenization.”

Bluefin will leverage the purchase to offer its customers omnichannel payments and smartPOS capabilities, which will be integrated into the company’s existing payments and data security suite. TECS clients will benefit from added data security solutions, as well as additional resources for its TECS product and solution suite.

Founded in 2007, Bluefin offers encrypted and tokenized payments for point-of-sale transactions. Additionally, the company’s data security platform, ShieldConex, tokenizes payments, Personally Identifiable Information (PII), and Protected Health Information (PHI) entered online. Last month, the company appointed a new CRO to fuel its growth. And, earlier this fall, Bluefin partnered with commercial hardware manufacturer Sunmi.

U.S. Bank launched a new suite of embedded payments solutions within Microsoft Dynamics 365.

The collaboration embeds U.S. Bank payment capabilities across Microsoft platforms.

U.S. Bank said it plans to embed additional payment capabilities within platforms such as Microsoft Teams and Microsoft Power Platform.

U.S. Bank’s collaboration with Microsoft announced earlier this year has borne fruit: the bank has introduced a new suite of embedded payments solutions within Microsoft Dynamics 365. The integration embeds U.S. Bank payment capabilities across Microsoft platforms. It also makes U.S. Bank among the first financial institutions to take advantage of the opportunity of directly integrating into the popular enterprise resource planning (ERP) and finance solution.

Among the solutions available to businesses using Microsoft Dynamics 365 is the U.S. Bank AP Optimizer. Available directly from their business application, the technology gives treasury management teams the ability to automate invoice processing for both business and consumer payment disbursement within Microsoft Dynamics 365. This will facilitate automated accounts payable workflows, including matching and reconciliation.

“We are committed to meeting clients wherever they are in their digital journey, bringing payments to businesses in a way that’s instant, embedded and connected to the technology they use every day,” U.S. Bank vice chair and head of Payment Services Shailesh Kotwal said. “Our integration with Microsoft – which businesses rely on daily to serve their customers – opens new possibilities for U.S. Bank clients to improve efficiencies and enable faster payments.”

According to U.S. Bank, this week’s news is only the beginning. The bank announced that it has plans to embed additional payment tools within Microsoft platforms such as Microsoft Teams and Microsoft Power Platform.

“Embedded payments can deliver powerful, new ways for businesses to streamline processes, enhance visibility, deliver better experiences, and reduce risk,” Microsoft Corporate Vice President for Worldwide Financial Services Bill Borden said. “We are excited to build on our work with U.S. Bank, delivering integrated, easy-to-use digital payments capabilities to our customers through Microsoft Dynamics 365 with additional embedded solutions to come.”

The two companies have been working together closely since February, when U.S. Bank announced a “substantial investment” in the modernization of its technology by choosing Microsoft Azure at its primary cloud provider for applications. The move will give customers more tools and more options when it comes to accessing banking services and provides U.S. Bank with opportunities to grow via new partnerships and what the bank sees as an “ever-evolving financial services marketplace.”

U.S. Bank’s collaboration news comes just one month after the bank introduced a new cash flow prediction tool for small businesses. The solution gives SME owners a 90-day forecast of cash flow and enables them to factor in external client data along with data from their own U.S. Bank accounts to provide more comprehensive cash flow insights.

U.S. Bank most recently demoed its technology last September at FinovateFall 2021. At the conference, the Minneapolis, Minnesota-based bank demoed its Card-as-a-Service (CaaS) solution. The offering enables fintechs, partners, and clients to digitally extend corporate credit, and to leverage API integration to create a custom virtual payment experience in their own ecosystem. Spending limits, tokenization, and encryption are all features of U.S. Bank’s CaaS solution.

Amazon is launching a merchant cash advance tool in partnership with Parafin.

The cash advance ties repayment to a percentage of the Amazon seller’s Gross Merchandise Sales (GMS).

The program launches today for select U.S. businesses, and it will be available more broadly by early 2023.

Right on the heels of launching its own insurance marketplace, Amazon is taking another step into the fintech realm. This time the online retailer is taking aim at small business financing, unveiling a financing tool for sellers on its own platform via a partnership with Parafin, a fintech that offers a merchant capital-as-a-service for online marketplaces.

Leveraging Parafin’s technology, Amazon is launching a merchant cash advance tool that offers eligible Amazon sellers a cash advance that ties repayment to a percentage of sellers’ Gross Merchandise Sales (GMS). The service offers approved merchants capital ranging from $500 to $10 million in a matter of days, and does not limit borrowers to a fixed term, require credit checks, or charge late fees.

Because the merchant cash advance tool is based off a seller’s GMS, the financing does not work like a traditional loan. Repayment is only required when a seller makes a sale. There is no minimum payment, no interest, and no collateral required. Instead, Amazon charges merchants a fixed capital fee.

“Amazon is committed to providing convenient and flexible access to capital for our sellers, regardless of their size,” Amazon WW B2B Payments and Lending Director and General Manager Tai Koottatep. “Today’s launch is another milestone in strengthening Amazon’s commitment to sellers, and builds on the strong portfolio of financial solutions we already provide. This latest offering significantly expands sellers’ reach and capabilities, and broadens their access to capital in a flexible way—one that helps them control their cashflow, and by extension, their entire business.”

Amazon is launching the financing program to select U.S. businesses today, and it will be available to “hundreds of thousands” of eligible sellers by early 2023. To qualify, sellers must have at least three months of sales history on Amazon.

Founded in 2020 and headquartered in California, Parafin’s mission is to democratize access to growth capital. The company has raised a total of $244 million, including its most recent round of $60 million raised in August. Earlier this year, Crunchbase added Parafin to its Emerging Unicorn Board, its list of companies valued above $500 million but less than $1 billion.

For many in the fintech industry, there are few things as scary as the economy right now. High inflation, lowered investor and consumer confidence, and political tensions are all contributing to an uncertain future.

One of the largest impacts of this pullback in the fintech industry is seen in the drop in venture capital funding, the lifeblood of privately held companies. The lack of funding is giving startups of all sizes a shorter cash runway, which is leading to employee downsizing and increased exit activity.

We turned to CB Insights, which recently dropped its Q3 2022 State of Venture report, for some statistics that help tell the story of today’s funding environment in fintech and beyond. Here are some of the high-level takeaways:

71% drop in new unicorns in the third quarter of this year

Across the globe, there were only 25 newly minted unicorns in the third quarter of 2022. This is the lowest count since the first quarter of 2020, when the pandemic first began. It is worth noting that 14 of the 25 new unicorns are U.S. based. The total number of unicorns across the globe is now 1,192.

38% drop in fintech funding QoQ

Looking at the fintech sector specifically, fintech funding across the globe dropped to $12.9 billion. This dip– a 38% drop– marks the lowest quarterly funding amount in nine quarters. The last time fintech funding was this low was in the second quarter of 2020, when fintech funding totaled $12.2 billion.

42% drop in median deal size for late-stage rounds this year

So far in 2022, the median size of late-stage deals has totaled $29 million. This represents a 42% drop from last year’s total of $50 million. This year’s median late-stage deal size is similar to the median size of mid-stage deals, which totals $30 million. Interestingly, this median mid-stage deal size is on-par with the median mid-stage deal size of 2021, which also totaled $30 million.

56% fewer investments from top 3 investors

According to CB Insights, last quarter’s top three investors are quieter this quarter. Tiger Global Management, Gaingels, and SOSV made 109 investments this quarter. This figure is 56% lower than the number the investors made in the second quarter of this year. Notably, Tiger Global Management, which has been the number one investor in the past three quarters, did not even rank among the top 10 investors this quarter.

A bright light

Things are not all gloom and doom this Halloween. Looking at the bright side, while fintech funding is dropping, it is still above pre-pandemic levels.

As an example, in the first quarter of 2020, before the pandemic truly exploded, quarterly fintech funding totaled $11.3 billion. That’s $1 billion lower than today’s level. Going back even further, in the first quarter of 2018, quarterly fintech funding totaled $9.6 billion.

So perhaps it’s best to look at these drops as a market reset, instead of as the fintech world coming to an end.

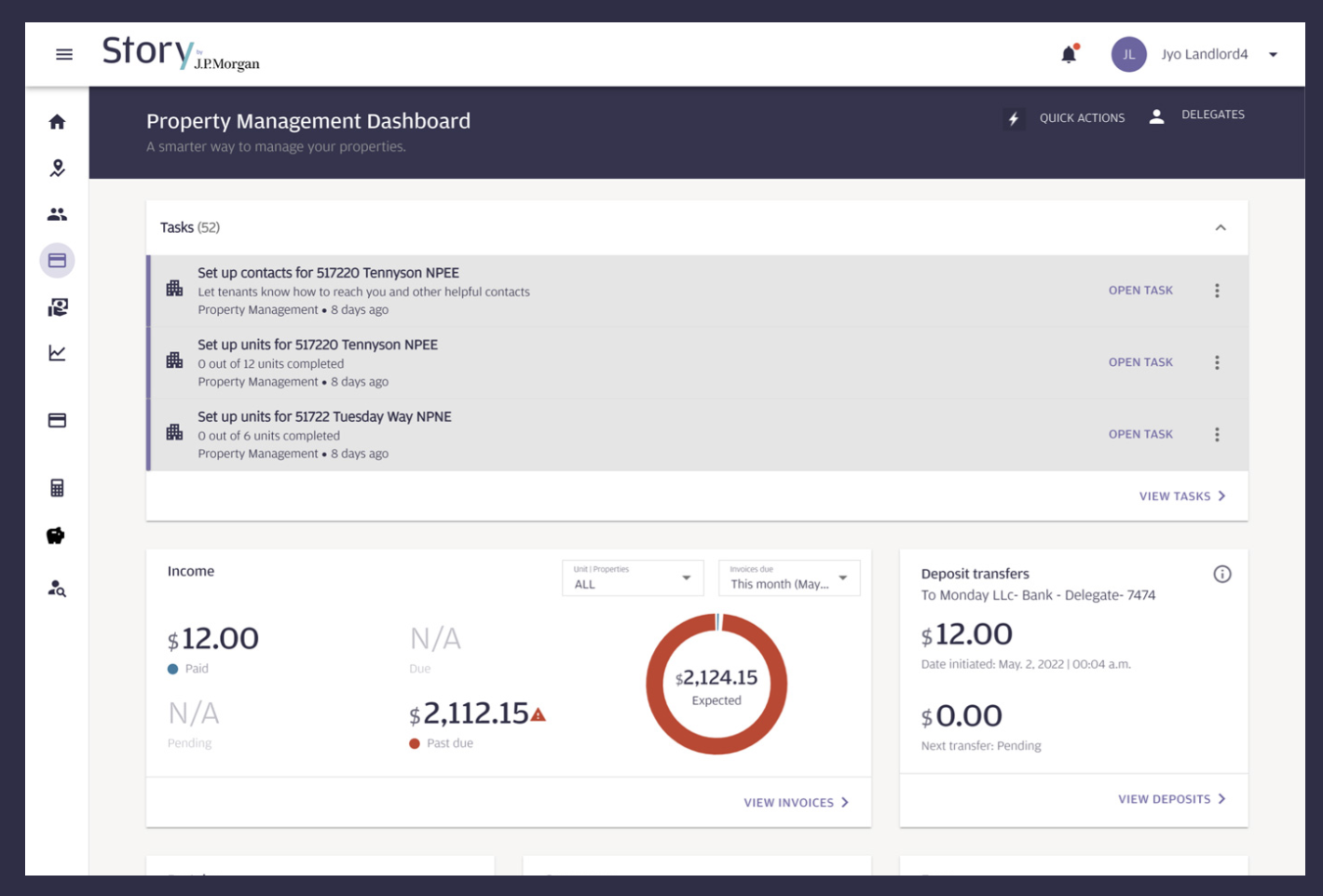

JP Morgan Chase is working on a rent management tool for owners of multi-family housing buildings.

The new tool, called Story, will enable landlords to send invoices, receive payments, track payments, view analytics, determine rent prices, and screen potential tenants.

Story is currently in beta, but is expected to be released to a broad audience in 2023.

JP Morgan Chase is piloting a platform to facilitate rent payments for tenants living in multifamily housing. The new technology, called Story, is a rent management tool for multi-family property owners.

As its core functionality, Story will enable landlords to automate rent invoices and receive rent payments. As not all tenants pay rent on time or in full, Story serves as a platform to help landlords track which tenants have paid and which still owe. Additionally, the new offering will provide property owners with analytics, help them determine rent prices, and will even offer a tool to screen potential new tenants.

As for renters, Story will remind them of upcoming rent payments, offer them multiple payment options, enable autopay, track their previous rent payments, and show a copy of their lease.

The bank has not yet set a price for the tool, but indicated that it will not charge a transaction fee for ACH, debit, or credit card payments for the first year. After that, Chase clients that hold an unspecified minimum balance will receive free ACH payments.

Story, which is currently available in 15 U.S. states, will be released to a broader set of users next year.

I’m always surprised at the lack of property tech (proptech) solutions in the fintech space. During the last decade, tenants’ rent payments totaled $4.5 trillion, and this number is set to increase massively between 2020 and 2030. Aside from insurtech, proptech is one of the last frontiers of fintech to be digitized. Now that we’re seeing a large incumbent like JP Morgan get into the game, it is only a matter of time before we see competing proptech innovations from other traditional banks.