This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Social trading and investment network eTorounveiled that it will begin rolling out its stock lending program in the UK. The capability, which is available in Europe and the UK, enables eligible users to lend out their stocks.

Stock lending isn’t new. In fact, it has long been a passive revenue generator for large brokers and hedge funds. Bringing this capability to an alternative platform like eToro gives the fintech a competitive edge as it brings more transparent, value-added services to the retail trading market. As investor expectations increase, platforms that provide passive-income engines, improved liquidity, and greater control over their portfolios may gain more interest in an ever-crowded market.

Facilitating the launch are global financial services company BNY and stock lending program EquiLend. Under these partnerships, BNY is acting as custodian and clearing provider, while EquiLend identifies borrowers and facilitates the lending process. eToro anticipates that the new program will allow its investors to put their portfolios to work while retaining their investments.

As with most stock lending programs, borrowers post collateral, and investors can still sell their positions at any time. By partnering with institutions such as BNY and EquiLend, eToro aims to ensure operational safeguards that offer retail users institutional-grade risk management.

“Launching stock lending in the UK is a key step in our mission to make passive income opportunities available to every investor,” said eToro VP of Execution Services Yossi Brandes. “With the ability to lend not just US but also global stocks, we are maximizing the potential for our clients to generate additional revenues, and this rollout sets the stage for further expansion into new markets.”

Launching in the UK expands eToro’s partnership with BNY, which it leverages for clearing and custody services for its stock and ETF offering across 19 global exchanges.

“We are delighted to extend our relationship with eToro, delivering an integrated solution encompassing clearing, settlement, custody, foreign exchange and cash management to UK investors,” said BNY Executive Platform Owner of Global Clearing Victor O’Laughlen. “By combining the capabilities of eToro and EquiLend with the scale and deep expertise of BNY’s leading Global Clearing platform, this initiative aims to equip retail investors with an institutional-grade solution to support their investing journey.”

Israel-based eToro said that the move marks the next step in the company’s plan to expand stock lending access to retail investors worldwide.

For eToro, today’s launch is more than a feature. The expansion is a signal of the company’s strategic move into deeper monetization and institutional-grade services. Leveraging BNY’s clearing and custody infrastructure places eToro closer to the operational standards of traditional brokers while maintaining its core social-trading product. Adding features like these in partnerships with traditional financial institutions could help eToro attract more sophisticated retail investors looking for passive-income tools and greater flexibility.

Founded in 2007, eToro has since raised $693 million in funding. With more than 35 million registered users and investors on its trading and investing platform, the company offers trading and investing tools that are more accessible and collaborative. eToro launched in the US market in 2019, entering a space where Robinhood had already established a six-year presence.

eToro began 2025 with its public debut in May. The company is now listed on Nasdaq Global Select Market under the ticker ETOR. eToro has a current market capitalization of $3.5 billion.

Airwallex has raised $330 million at an $8 billion valuation, boosting its total funding to $1.5 billion and setting up a major US expansion with a new San Francisco headquarters.

The company’s business performance is rising, with annualized revenue surpassing $1 billion, transaction volume doubling to $235 billion, and half of its customers using multiple Airwallex products.

The company is positioning itself as the backbone of global, AI-powered finance, expanding regulatory coverage to 80 licenses worldwide.

Global commercial payments and financial platform Airwallex has captured fintech’s attention with its new funding round today. The Singapore-based company closed a $330 million Series G round at an $8 billion valuation, which is 30% higher than its valuation six months ago at its Series F round.

Led by Addition with participation from T. Rowe Price, Activant, Lingotto, Robinhood Ventures, and TIAA Ventures, the round boosts Airwallex’s total funding to $1.5 billion and will allow the company to create AI agents and fuel product development. The company will also use the investment to fuel its global growth, including in the US.

As part of this, Airwallex has established a second headquarters location in San Francisco and will invest $1 billion from 2026 to 2029 to scale its US operations, attract new employees, and expand its physical footprint and brand awareness.

“We believe the future of global banking will be borderless, real-time, and intelligent,” said Airwallex CEO and co-founder Jack Zhang. “Legacy providers are fundamentally incompatible with how modern businesses operate, and our investors understand that we’re pulling ahead in the race to define this category. We’re building a modern alternative, a single platform that powers global banking, payments, billing, treasury, and spend on top of proprietary financial infrastructure. This capital will accelerate our growth, extend our technical leadership, and strengthen our position in the U S and across key markets worldwide.”

Airwallex’s new round comes during a time of not only geographical expansion, but also significant growth in business performance and platform adoption. The company’s annualized revenue surpassed $1 billion in October, marking 90% year-over-year growth, while its annualized transaction volume doubled to more than $235 billion. Product depth is also increasing, with approximately half of all customers now using multiple Airwallex products, a sign of expanding product-market fit and stickiness.

Airwallex has also strengthened its global regulatory footprint, holding 80 licenses and permits that enable customers to operate in 200+ countries and regions and support multi-currency checkout at scale. In 2025 alone, the company extended its regulated and local capabilities across 12 new markets, securing licenses and launching products in France, the Netherlands, Israel, Canada, Korea, Japan, New Zealand, Malaysia, Vietnam, Brazil, Mexico, the UAE, and more.

As Airwallex scales its infrastructure, footprint, and product suite, investors see the company as a foundational layer for the next era of global business banking. Addition’s Lee Fixel captured this shift, noting that “Airwallex is reshaping the global business banking landscape. The traditional financial system wasn’t built for borderless businesses, and Airwallex is uniquely equipped to solve this challenge. With its global financial infrastructure, software and AI capabilities, the company is exceptionally well positioned to lead the future of global business banking.”

As mentioned earlier, part of today’s investment will help Airwallex build a team of AI agents for financial workflows to eventually create a fully autonomous finance department. The agents will leverage behavioral and transactional data to automate multi-step operations such as expense approvals, policy checks, and end-to-end task orchestration. The company estimates that it will employ hundreds of agents across its platform.

“As AI lowers software costs, infrastructure and data become the ultimate differentiator,” Zhang added. “Airwallex connects the full spectrum of a customer’s financial operations – money in, money out, and everything in between, giving our agents the contextual data to execute with precision. This proprietary visibility, built on our scalable financial infrastructure, is what powers agentic finance.”

The year may be winding down, but fintech is still winding up. This morning brings news of Airwallex’s $333 million round, valuing the company at $8 billion. Grab yourself a warm cup of cheer and settle in for this week’s top fintech news. We’ll continue to add more announcements as the week progresses.

Trulioo has joined Google’s Agent Payments Protocol (AP2) to provide its Digital Agent Passport and Know Your Agent (KYA) framework, creating a trusted identity layer for AI-driven, agent-led payments.

AP2 establishes a common standard for how AI agents transact, and Trulioo ensures every agent interacting in the ecosystem is authenticated, authorized, and accountable before executing a payment.

Agentic payments remain early but are poised to scale quickly as identity layers like KYA mature and combine with programmable settlement rails such as stablecoins and tokenized deposits, enabling safe, real-time autonomous transactions.

Agentic payments are on the rise this season, and digital identity platform Trulioo is stepping up to help protect agent-led transactions. The Canada-based company has joined Google’s Agent Payments Protocol (AP2) initiative.

With the launch, Trulioo is deepening its long-standing ties with Google, which leverages Trulioo’s Global Identity Platform for Know Your Customer (KYC) verification.

Google launched AP2 in September 2025 to provide an open, standardized framework for digital payments. AP2 connects banks, fintechs, and merchants with its protocol that creates a common language for how AI agents can transact on behalf of users.

Trulioo will bring its Digital Agent Passport and KYA framework to AP2. Together with Trulioo’s KYA framework, the Digital Agent Passport creates a verifiable trust layer within AP2, ensuring every digital agent is authenticated, authorized, and accountable before transacting.

“The future of commerce belongs to agents that can think, act, and transact independently, but only if they can be trusted,” said Trulioo CEO Vicky Bindra. “By joining AP2, we’re helping define the identity backbone for autonomous payments, where verified agents transact transparently, responsibly, and at machine speed. This is the architecture, and the future, of trusted agentic commerce. We’re proud to be working with Google to bring verified identity to agentic payments.”

Headquartered in Canada and founded in 2011, Trulioo has raised $475 million. The company offers global verification for both businesses and customers in 195 countries and with the ability to verify more than 14,000 ID documents and 700 million business entities while checking against more than 6,000 watchlists. Trulioo has demoed at 10 Finovate events, most recently showcasing its identity platform at FinovateEurope 2023.

Trulioo launched its Know Your Agent (KYA) solution in August 2025. “KYA is a new identity layer designed for agent-led digital interactions, bringing trust and compliance to agentic commerce without compromising speed or user experience,” the company said. “This isn’t just technical infrastructure—it’s a real-time trust layer that quietly safeguards the ecosystem while letting everything move at machine speed.”

Agentic payments are still in their early stages, largely because true autonomy requires more than intelligent agents. For the ecosystem to work, agentic payments require a secure, verifiable system for authorizing transactions without human intervention. As identity layers like KYA mature, consumers and businesses will become more comfortable allowing AI agents to initiate payments, execute purchases, manage subscriptions, or even negotiate transactions on their behalf.

The shift becomes even more notable as agentic payments intersect with programmable settlement rails such as stablecoins and tokenized deposits. These payment methods enable real-time, programmable, and low-cost transactions that will help autonomous agents operate safely at scale. When combined, trusted agent identity plus programmable money could bring agent-led commerce into mainstream markets rapidly, especially if security layers like Trulioo’s are already in place.

This week’s edition of Finovate Global features news from fintechs headquartered in Sweden.

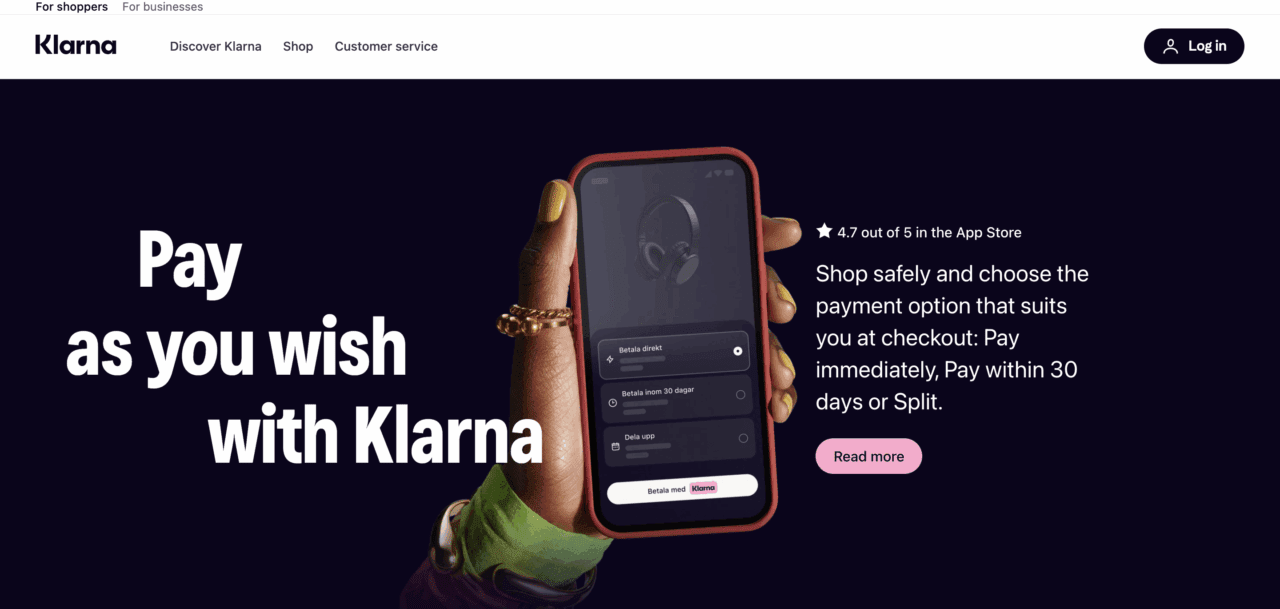

Klarna Brings Tap to Pay to 14 Markets in Europe

Swedish digital bank and payment provider Klarna has introduced Tap to Pay across 14 markets in Europe. The new features bring flexible payments to the brick-and-mortar retail world at scale, and help to transform Klarna’s app into a contactless wallet ready for everyday use.

“Tap to Pay brings us closer to our vision of Klarna being everywhere for everything,” Klarna Chief Product & Design Officer David Fock said. “Now you can set up a flexible payment plan and tap to pay in seconds, all inside the Klarna app. It makes everyday shopping moments significantly smoother for our Klarna customers across Europe, giving them even more flexibility and choice at checkout.”

At a time when 80% of shopping in Europe is still conducted in physical stores, Klarna’s Tap to Pay solution offers consumers the seamless experience of online commerce when shopping at brick and mortar retailers. Tap to Pay is currently live for Klarna customers in Germany, Italy, Spain, France, the Netherlands, Finland, Belgium, Austria, Ireland, Portugal, Norway, Poland, Denmark, and Sweden.

Klarna’s Tap to Pay announcement follows the introduction of the company’s stablecoin, KlarnaUSD, in late November. Klarna is the first bank to launch a stablecoin on Tempo, the new independent blockchain purpose-built for payments, that was started by Stripe and Paradigm. Currently live on Tempo’s testnet, KlarnaUSD is scheduled to launch on Tempo’s mainnet in 2026.

“With 114 million customers and $118 billion in annual GMV, Klarna has the scale to change payments globally: with Klarna’s scale and Tempo’s infrastructure, we can challenge old networks and make payments faster and cheaper for everyone,” Klarna Co-Founder and CEO Sebastian Siemiatkowski said. “Crypto is finally at a stage where it is fast, low-cost, secure, and built for scale. This is the beginning of Klarna in crypto, and I’m excited to work with Stripe and Tempo to continue to shape the future of payments.”

A Finovate alum since 2012, Klarna is headquartered in Stockholm, Sweden.

Tink Brings Pay by Bank Top-Ups to Fidelity International Investors

As Senior Analyst Julie Muhn reported earlier this week, Fidelity International has partnered with Sweden-based open banking platform Tink. The partnership will enable Fidelity to offer account top-ups via Pay by Bank, making it easier for investors to fund their ISAs, SIPPs, cash management, and general investment accounts.

A two-time Finovate Best of Show winner that was acquired by Visa in 2021, Tink enables financial institutions, fintechs, and merchants to leverage financial data to design and create personalized financial management tools, products, and services. With a single API, Tink empowers its customers to access aggregated financial data, use smart financial services, including risk insights and account verification, and build personal financial management tools.

Pay by Bank is one of the fastest-growing use cases for open banking. With analysts anticipating that total open banking users will top 645 million worldwide in 2029—a 3.5x increase from 2025’s 183 million users—options such as Pay by Bank are likely to become increasingly widespread as a modern, secure payment alternative with reduced friction.

“Pay by Bank represents the next evolution of open banking payments, delivering a fast, secure way to pay directly from your bank account,” Tink Head of Payments Ian Morrin said. “As adoption accelerates, we’re thrilled to see leading institutions like Fidelity put open banking at the heart of their payment experiences to make topping up investment accounts more seamless.”

Founded in 2012, Tink is headquartered in Stockholm, Sweden. The fintech offers 3,000+ connections to the major banks across Europe, processes more than 10 billion transactions a year, and boasts 10,000 developers using its platform. Co-Founder Daniel Kjellén is CEO.

Swedish VC Incore Invest Secures €15 Million Second Closing

Incore Invest, an investment firm based in Stockholm, has raised €15 million in a second closing of its Incore Invest II fund. The fundraising brings the fund’s total capital to €40 million to help SaaS and fintech companies throughout Europe grow.

“Incore Invest’s strategy has always been to back proven tech companies with strong growth potential,” Incore Invest Founder and CEO Nicolai Chamizo said in a statement. “Investors’ continued confidence in Incore Invest is very encouraging and with this second close, the round is fully equipped with capital to back the most promising European technology companies. It allows us to continue identifying and supporting the next generation of category-defining technology companies shaping the future of the industry.”

Incore Invest’s successful fundraising comes at a time when a number of European venture capital firms, especially those that have targeted growth-stage or early-stage technology companies, are raising or closing new funds. For example, four funds alone—Backed VC, Notion Capital, Armilar Venture Partners, and henQ—have raised more than €300 million in capital combined this year.

Among the companies in Incore Invest’s portfolio are several of innovative fintechs including Brite, a Swedish payments platform that leverages open banking to process instant payments; Mynt, a Swedish fintech that simplifies expense management via smart company cards; and Froda, a Swedish fintech and embedded finance company.

Here is our look at fintech innovation around the world.

Sub-Saharan Africa

Kenyan fintech Jahazii raised $400,000 to provide earned wage access and payroll infrastructure technology for Africa’s informal economy.

Wisesecured conditional regulatory approval to go live in South Africa.

Business AM looked at how Nigeria’s FairMoney Microfinance Bank expanded beyond digital lending into a full-service bank.

Central and Eastern Europe

Embedded finance infrastructure company YouLend announced a strategic partnership with digital financial management solution Qonto to help the firm enter the German market.

Salt Edgeteamed up with Romanian financial management platform, Finlayer, to bring open banking to small businesses in the country.

Former Polish President Andrzej Duda joined the board of fintech firm ZEN.COM.

Middle East and Northern Africa

Developed in partnership with Mawarid Finance, UAE-based fintech platform Huru launched its microfinance solution, Quick Cash.

MoneyGram is partnering with Fireblocks to introduce stablecoin-based settlement across its global payments network, enabling faster, lower-cost transactions and real-time liquidity management.

Fireblocks’ blockchain infrastructure will power a programmable settlement layer that streamlines reconciliation, reduces pre-funding needs, enhances treasury operations, and supports large-scale stablecoin flows.

As a legacy payments giant adopts digital-asset rails, fiat-backed stablecoins are becoming core infrastructure for cross-border payments and corporate treasury.

Cross-border payments network MoneyGram is taking a step toward modernizing its global settlement infrastructure by partnering with Fireblocks to bring stablecoin-based settlement into its core treasury processes. The collaboration aims to enable faster payments, lower costs, and real-time liquidity across MoneyGram’s worldwide network.

Fireblocks is a blockchain infrastructure and security platform designed for storing, transferring, and issuing digital assets. Founded in 2018 and headquartered in New York, the company’s suite of digital asset tools includes treasury management, wallets-as-a-service, payments, and tokenization. Fireblocks also offers stablecoin infrastructure that enables institutions to seamlessly move, hold, manage, and issue stablecoins with enterprise-grade security.

Founded in 1940, MoneyGram serves 50 million clients annually with its payment network that connects over 200 countries and territories, 20,000 corridors, and close to 500,000 retail locations.

“We are leading the next era of money movement by enabling money to move instantly across any channel—fiat or stablecoin,” saidMoneyGram Chairman and CEO Anthony Soohoo. “Fireblocks accelerates this vision by giving us the secure, programmable infrastructure to transform global payments at scale.”

The company will use Fireblocks’ stablecoin infrastructure to create a programmable settlement layer to help reduce capital requirements with pre-funding partners through continuous funding, receive stablecoin payments at scale from its partners, improve access to liquidity pools across global entities, streamline reconciliation and financial reporting for stablecoin operations, and improve treasury operations. MoneyGram will also use Fireblocks to help introduce programmable money and more resilient liquidity pathways.

“MoneyGram is rebuilding the rails of cross-border settlement in real time,” said Fireblocks Co-Founder and CEO Michael Shaulov. “By moving to a multi-chain, programmable infrastructure, it’s upgrading the speed and reliability of global payments at the foundation layer—where it matters most for the people who rely on these payments every day.”

For a long-standing, traditional player like MoneyGram, teaming up with Fireblocks pivots the company from traditional correspondent-bank rails toward a modern, agile payments infrastructure. Today’s partnership is an example of how fiat-backed stablecoins are becoming core plumbing for global payments and corporate treasury operations. It shows that stablecoins could provide instant, reliable, low-cost cross-border value movement at scale, while bypassing legacy banking delays and costs.

Financial data network Plaid and real-time clearing and embedded banking enabler ClearBank announced a new partnership this week.

The partnership will enable Plaid to leverage ClearBank’s virtual accounts and UK Faster Payments Service (FPS) access to enhance the sending, receiving, and reconciling of open banking payments.

Founded in 2013, Plaid has been a Finovate alum since its debut at our developers conference, FinDeVR Silicon Valley 2014.

A new partnership between ClearBank and Plaid will deliver faster, more secure, and friction-free Pay by Bank experiences for both businesses and customers throughout the UK. Courtesy of the collaboration, ClearBank‘s virtual accounts and direct access to the UK Faster Payments Service (FPS) will enable Plaid to enhance the sending, receiving, and reconciling of open banking payments. This includes making it easier for companies to match incoming payments to specific users or transactions, enhancing the reconciliation process and reducing reliance on manual effort.

“ClearBank and Plaid share a commitment to modernizing financial services through transparency, security, and innovation,” ClearBank Group Chief Executive Officer Mark Fairless said. “By combining ClearBank’s cloud-native infrastructure with Plaid’s open banking connectivity, we’re unlocking potential for businesses to deliver faster, more reliable, and secure payment experiences.”

An enabler of real-time clearing and embedded banking, ClearBank will provide a regulated, real-time, cloud-native infrastructure that will benefit consumers with faster, more predictable bank payments. The partnership will enable Plaid to offer faster, more reliable pay-ins and payouts that will empower companies to provide better customer experiences at checkout and during account funding.

“Pay by Bank is no longer a niche option,” Plaid Head of Product, Europe, Zak Lambert said. “Adoption is rising quickly, especially among younger consumers who expect instant, secure, and low-friction ways to pay. To meet that demand, businesses need reliable real-time payment infrastructure. ClearBank’s technology helps Plaid deliver instant, secure, and cost-efficient bank payments so companies can better serve their customers’ needs.”

Plaid’s partnership announcement with ClearBank comes as Plaid announced a new AI-enhanced transaction categorization capability that delivers up to 10% greater accuracy on primary categories and 20% greater accuracy on detailed sub-categories. The result is fewer missed transactions and more accurate data labeling. In addition to AI-assisted label generation and targeted human review, Plaid also noted that it would deploy an expanded category taxonomy with more than a dozen new subcategories to help differentiate income types, repayments, disbursements, bank fees, and transfers.

A Finovate alum for more than a decade, Plaid made its Finovate debut at FinDEVr Silicon Valley 2014. Today, the San Francisco-based fintech offers a data network that covers more than 12,000 financial institutions across the US, Canada, the UK, and Europe, making it easier for people to connect their financial accounts to the products and services they want. Plaid works with thousands of companies, including Fortune 500 firms and many of the world’s largest banks.

Plaid was founded in 2013. Co-founder Zack Perret is CEO.

As cyber threats become increasingly sophisticated, companies that once relied on simple firewalls must now face a new reality. For a major telecom like T-Mobile, the stakes are especially high, as networks, customer data, and identity services are all at risk. To protect both its assets and its customers, T-Mobile is rethinking its cybersecurity strategy at every level, from workforce authentication to real-time detection to a “human-first” culture.

Mark Clancy, SVP, Cybersecurity, Information, Technology at T-Mobile joined me in front of the camera at FinovateFall earlier this year to offer up what T-Mobile is doing to combat fraud. In our conversation, he discussed how SIM-based authentication is eliminating the friction in financial services while keeping clients’ money safe. He talked about why making security invisible doesn’t mean making it weaker, shared how banks can put customers first without compromising protection, and described T-Mobile’s network authentication tool, T-Secure.

Network authentication, what we call T-Secure, simply embeds the authentication process into the SIM card that’s already in your phone. We have 130 million customers, and we already know who they are. We use that to bind the transaction they’re performing to their identity and authenticate invisibly in the background using certificate-based authentication.

Mark Clancy leads cybersecurity at T-Mobile as Senior Vice President of Cybersecurity, Information, and Technology. Under his watch, the company has shifted from traditional reactive security practices to an identity-first, zero-trust model.

T-Mobile is one of the largest wireless carriers in the US, serving millions of customers nationwide. Historically a telecom company, T-Mobile has increasingly expanded into identity services, digital authentication, and mobile-based financial and communication products. The company runs a centralized Cyber Defense Center, employs zero-trust authentication protocols, and subjects all devices to rigorous security vetting before they go to market.

First-party fraud is a growing problem for financial institutions and retail businesses. But relative to other fraud threats—from deepfakes to account takeover—first-party fraud is often overlooked when it comes to major fraud challenges faced by businesses. Nevertheless, this type of fraud, which takes place when an individual claims to have not made a purchase they have actually made, is a problem that has only increased as ecommerce has expanded.

In this interview, conducted at FinovateFall earlier this year, I spoke with Shanti Shanmugam, Co-Founder and CEO of Casap, about the challenge of first-party fraud and dispute resolution. Shanmugam explains how AI enables Casap to instantly distinguish legitimate disputes from fraudulent claims, reducing dispute resolution costs by 90% and reducing fraud losses for clients by 51%. Shanmugam discusses why trust is at the center of both banking relationships and the dispute resolution, and how a poor dispute resolution experience can impact how much business a customer decides to do with their primary financial institution in the future.

The true cost of disputes is in trust. You are saying ‘Hey, I really did not buy this TV at Best Buy, and I really need you to have my back.’ Right now, most financial institutions, especially if they’re not working with us, take on average 90 days to resolve your case. And you’re kind of waiting in the dark the whole time. Maybe they give you a credit up front, but at the end, if they don’t get that money back from the merchant, they’re going to be clawing that money back from you 90 days later. And that’s a very trust-breaking experience. It’s the number-one reason why people are leaving their institution as a primary financial relationship: because of a negative dispute experience. So that’s the hidden cost of a dispute.

Founded in 2022 and headquartered in New York City, Casap won Best of Show in its Finovate debut at FinovateFall 2025. The company’s dispute automation and first-party fraud prevention platform automatically resolves disputes, enabling financial institutions to intelligently manage first-party fraud. The technology also transforms the dispute resolution process into an opportunity to build lasting loyalty and trust. Casap’s solution increases recovery rates, identifies and prevents fraud patterns, and delivers fast, frictionless, low-cost dispute and chargeback resolution.

Fraud is growing more sophisticated and has become supercharged by generative AI, deepfakes, and increasingly organized social-engineering networks. The changing dynamics have forced both banks and fintechs to rethink their defenses as criminals adapt faster, more frequently, and with more personalized attacks. Across fintech, it is clear that traditional fraud controls are no longer enough to protect customers.

But while the entire industry is facing the same escalating threats, fintechs have been especially creative in rolling out new layers of protection. Over the past year, a handful of standout features have emerged that combat fraud by proactively shaping customer behavior, interrupting social-engineering tactics, and closing gaps that legacy systems can’t reach. Here are three unique new innovations worth watching (and borrowing).

Revolut’s geolocation restrictions

Revolutreleased a safety feature yesterday that allows users to restrict money transfers to specific, user-approved geographic areas. If a transfer request is made from the customer’s device, but takes place at a location that the customer has not listed, the app blocks the transaction automatically, even if the fraudster has the user’s credentials. The feature uses both device GPS and Revolut’s internal risk engine to reduce account takeover losses.

Why banks should care: Geolocation locking adds a low-friction layer to fraud defense, especially for reducing authorized push payment fraud (APP) and account takeovers. By having the user determine their restricted, “safe” locations, banks could offer users more granular control over how and where their money can move.

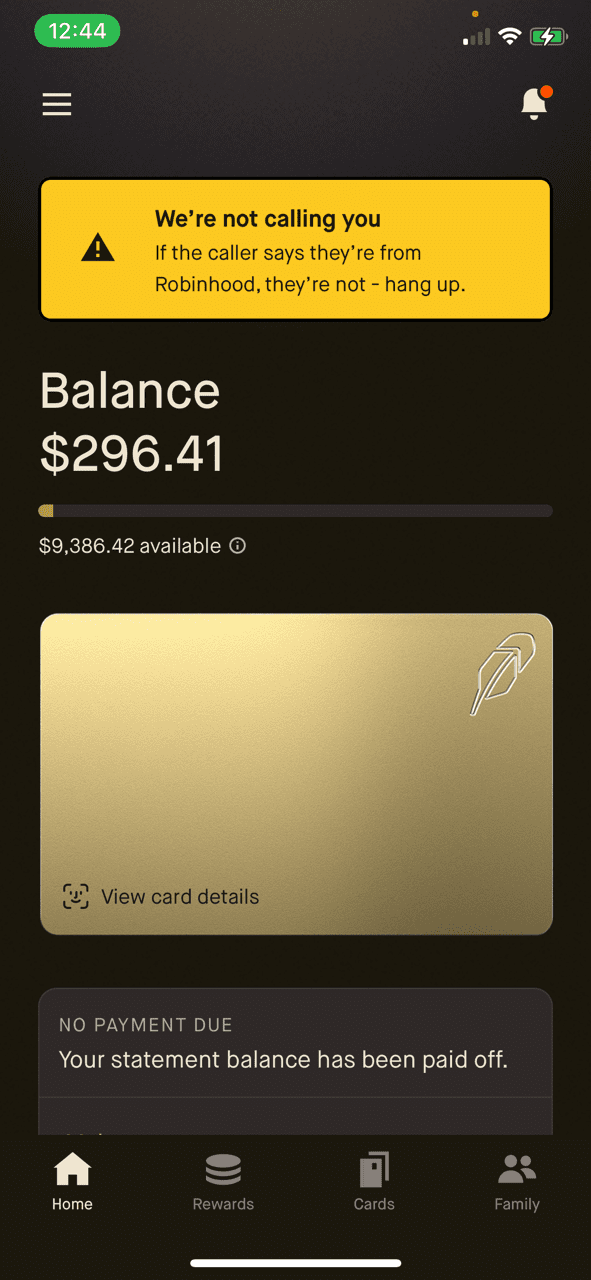

Monzo’s and Robinhood’s in-app scam warnings

Both Monzo and Robinhood help users determine whether an inbound call claiming to be from the bank is legitimate. When a customer is on a call and opens their mobile app, the app displays a banner that clearly communicates that the call they are on is not with the bank. In Robinhood’s case, the message states, “We are not currently trying to call you. If the caller says they’re from Robinhood, they are not. Hang up.”

Why banks should care: Impersonation scams are one of the most expensive forms of APP fraud. Adding an in-app, real-time verification banner is an extremely simple but effective way to interrupt fraudsters.

iProov is fighting deepfakes with biometric verification that detects AI-generated faces and synthetic video spoofing. The company analyzes pixel-level light reflections, which it calls “liveness assurance,” and uses deepfake-detection models to identify whether a live user is present. This is becoming essential for remote KYC, account recovery, and high-risk authentication.

Why banks should care: Banks increasingly rely on remote onboarding and passwordless authentication, but deepfakes are now able to defeat many of the legacy selfie-verification systems launched in the past decade. Deploying deepfake-resistant biometrics is becoming essential to prevent fraudulent account opening and social-engineering-driven account resets.

Each of these features has one thing in common: they put friction in exactly the right place. The friction isn’t applied to every transaction, and they won’t deter honest customers, but they will help stop fraud in common places. By using smarter triggers, real-time context, and design choices, fintechs are able to interrupt fraudsters. And while each solution won’t stop all fraud, they take care of some of the heavy lifting while minimizing the burden of friction on end consumers.

Embedded income protection and life insurance provider Eleos has launched its AI Voice Agent.

The new offering is designed to provide customers with always-on, around-the-clock assistance, backed by human customer service professionals.

Eleos made its Finovate debut at FinovateEurope 2024 in London. Kiruba Shankar Eswaran is Co-Founder and CEO.

London-based insurtech Eleos recently unveiled its AI Voice Agent. The new solution will provide always-on, 24/7 customer service, including the ability to make outbound calls to prospective clients. The AI Voice Agent draws answers from actual Eleos policy documents to address customer queries regarding issues such as policy coverage updates, claims information, how to cancel existing policies, and more.

“We’re committed to making protection simple, accessible, and always available,” Eleos Life CEO and Co-Founder Kiruba Shankar Eswaran said. “Our voice agent extends this mission by giving customers the support they need, exactly when they need it—whether that’s at midnight or mid-afternoon. We’re removing barriers to access and empowering our customers to manage their protection with confidence.”

Eleos emphasized that its new AI Voice Agent is designed to support, not replace, human customer service professionals. Rather, the AI agent will serve customers with basic queries, as well as those who have difficulty reading online content or writing emails. In all instances, customers will have ready access to a human agent via phone, email, or WhatsApp.

Eleos’ AI Voice Agent is the latest iteration of the company’s ongoing investment in AI-powered technology. In August, Eleos unveiledTheea, an intelligent chatbot that guides customers through their insurance application with step-by-step instructions and personalized coverage calculations.

“Life insurance is one of the most important financial decisions people can make, but too often it feels out of reach,” Eswaran said when Theea was launched. “With Theea, we’re changing that by building awareness through clear, jargon-free guidance, improving access with on-demand, multilingual support, and driving engagement by giving people the confidence to explore and choose coverage in their own time. Our mission has always been to make protection simple and inclusive, and Theea is a powerful step in that direction.”

An insurtech specializing in embedded term life insurance, disability insurance, and income protection in both the US and UK, Eleos made its Finovate debut at FinovateEurope 2024. At the conference, the company showed how it partnered with consumer brands to embed life insurance and income protection into their online journeys. Eleos demonstrated how the company leverages partner data to raise awareness of the importance of life insurance and income protection, provide quotes on various insurance products, and expedite the application process.

Fidelity International is partnering with Visa-owned Tink to offer pay by bank account top-ups, giving investors a faster, more seamless way to fund ISAs, SIPPs, cash management accounts, and general investment accounts.

Tink’s pay by bank enables real-time, secure bank-to-bank transfers, settling in under 40 seconds and reducing friction, fraud risk, and costs associated with manual transfers or card-based payments.

Pay by bank adoption is accelerating across Europe, driven by lower fees, faster settlement, and open banking growth.

Global asset manager and retirement savings firm Fidelity International has teamed up with Visa’s open banking platform Tink. Fidelity will leverage Tink’s pay by bank tool to enable account top-ups for its personal investing customers and advised clients.

Adding the account top-up capability will allow Fidelity International users to quickly add funds to their ISAs, SIPPs, cash management accounts, and general investment accounts. With Tink’s pay by bank, users can send funds directly from their bank accounts using their secure bank log-in details. The funds are sent on fast rails that settle the transaction in less than 40 seconds on average and offer real-time payment confirmation.

“Fidelity’s focus is always on making investing as accessible and straightforward as possible. Partnering with Tink to offer pay by bank gives both our personal investors and our advised clients a fast, convenient way to fund accounts—reducing friction and improving the overall customer experience,” said Fidelity International Chief Digital Officer, Global Platform Solutions, Ian Hood. “By integrating pay by bank, we’re expanding our digital payments infrastructure to offer a modern, secure alternative to traditional methods like manual bank transfers, helping users move money quickly and safely.”

Founded in 2012, Tink was an early player in Europe’s open banking ecosystem. The Sweden-based company was acquired by Visa in 2022 for $2 billion and today offers a wide variety of products ranging from payments to account data to risk decisioning and finance management. With 3,000+ connections to all major banks across Europe, Tink processes 10 billion transactions per year across 19 geographical markets.

Pay by bank is one of Europe’s fastest-growing payment methods, driven by lower transaction costs, faster settlement times, and a shift toward open banking–powered digital payments. For merchants, direct bank-to-bank transfers eliminate interchange fees and reduce chargeback risk, making the payment experience both cheaper and less prone to fraud. Consumers benefit from a smoother checkout flow, fewer authentication steps, and greater security due to strong customer authentication.

According to Juniper Research, there are currently 183 million open banking users worldwide, a number expected to surpass 645 million by 2029. The combination of cost efficiency, real-time settlement, higher authorization rates, and improved fraud controls positions it as one of the most strategically important payment innovations in the market today and offers the potential for it to become a mainstream payment option.

For Tink, Fidelity’s rollout is another signal that pay by bank is moving from early adoption into mainstream financial services. As Tink Head of Payments Ian Morrin noted, “Pay by bank represents the next evolution of open banking payments, delivering a fast, secure way to pay directly from your bank account. As adoption accelerates, we’re thrilled to see leading institutions like Fidelity put open banking at the heart of their payments experiences to make topping up investment accounts more seamless.”