This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Multiple benefits arose from last year’s drive to digital, including the increase in user data and more control over the user experience. But making the leap to capturing that data and enhancing control over the user experience is easier said than done.

It is this gap that led Quantum Metric to launch its platform for continuous product design. The product uses realtime data from digital customer interactions to inform the decision-making process. As a result, firms can maximize opportunities, find errors, measure engagements, and more.

Quantum Metric offers tools for a range of industries, including retail banking. Some of the company’s retail banking clients include Western Union, Bank of Montreal, Silicon Valley Bank, and Aspiration.

In the video below, Aspiration Chief Product Officer Jody Mulkey explains how his bank uses Quantum Metric to understand sticking points in its application process and better interpret how clients are using the bank’s tools.

Founded in 2015, Quantum Metric became a unicorn company earlier this year after raising $200 million in a Series B funding round. Because the company aids in the transition to digital, Quantum Metric came close to doubling both its staff and revenue in 2020.

Though there is no official word on a public offering, Quantum Metric appointed a new Chief Revenue Officer, Chief Financial Officer, and Advisory Board Member late last month. The new hires indicate the company may be poising itself for an IPO in the foreseeable future.

Quantum Metric is one of the demoing companies at FinovateEurope 2021, which will take place digitally on March 23 through 25. Register to watch the demo and network with the company during the event. Or, check out a recording of the demo on Finovate.com later this year.

Apex Clearing Holdings, a digital clearing and custody engine, announced formal plans to publicly list on the New York Stock Exchange under the ticker “APX.”

The Texas-based company is eschewing the traditional IPO route to a public launch, and instead pursuing the listing via a merger with Northern Star Investment Corporation, a special purpose acquisition company (SPAC). The deal values Apex at $4.7 billion.

Apex is the sixth fintech to use a SPAC to go public in the past few months, joining SoFi, BankMobile, Payoneer, MoneyLion, and OppFi.

“We are in the first inning of the digital revolution in financial services, and our merger with Northern Star will provide Apex with the resources and flexibility to accelerate our growth, scale our platform, and expand our offerings and market share alongside our clients,” said Apex Clearing CEO William Capuzzi.

Capuzzi, along with Apex President Tricia Rothschild, will continue to serve the company in their current roles. Northern Star Chairwoman and CEO Joanna Coles will join the combined company’s Board of Directors.

Apex was founded in 2012 and helps online brokerages, traditional wealth managers, wealthtechs, professional traders, and consumer brands with account opening and funding, execution of trades, digital asset movements, trade settlement, and the safekeeping of customer assets.

Apex has provided custody for $14 billion in new assets year-to-date and currently serves 200+ clients representing more than 13 million customer accounts. The company has already recorded impressive growth so far this year, seeing 3.2 million customer accounts and more than one million new crypto accounts opened in the past two months.

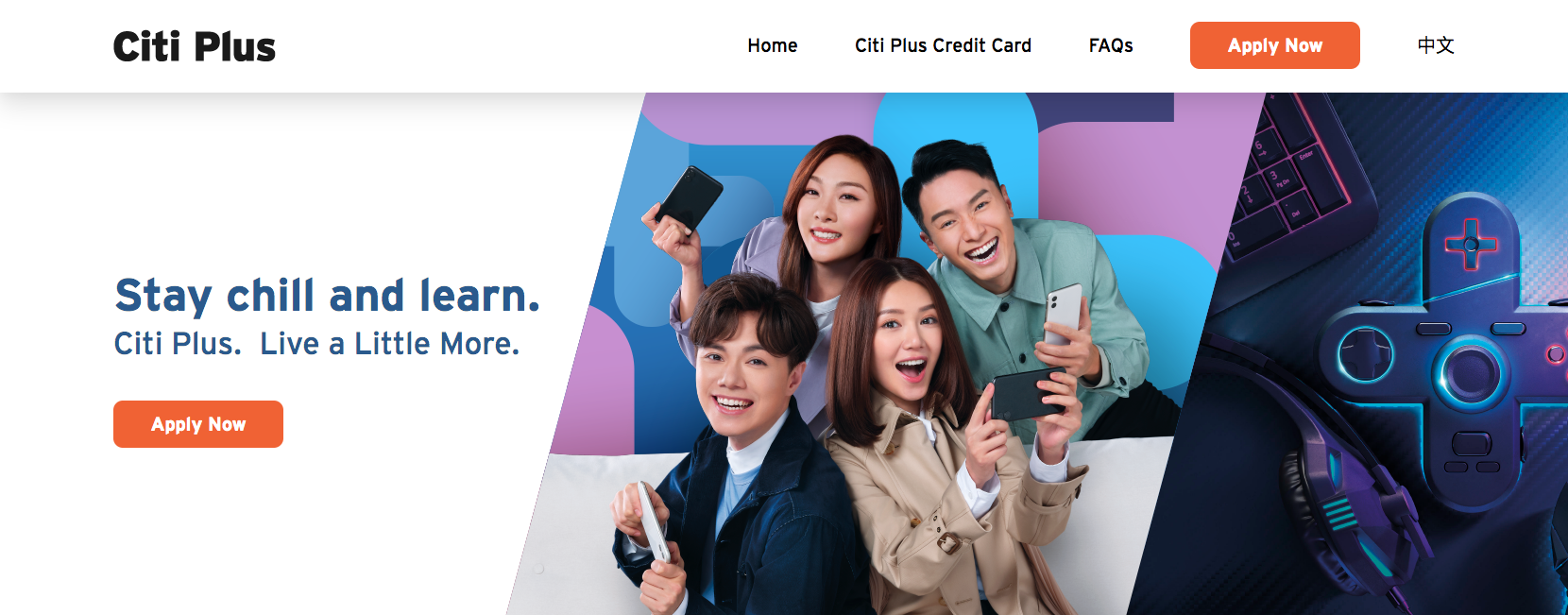

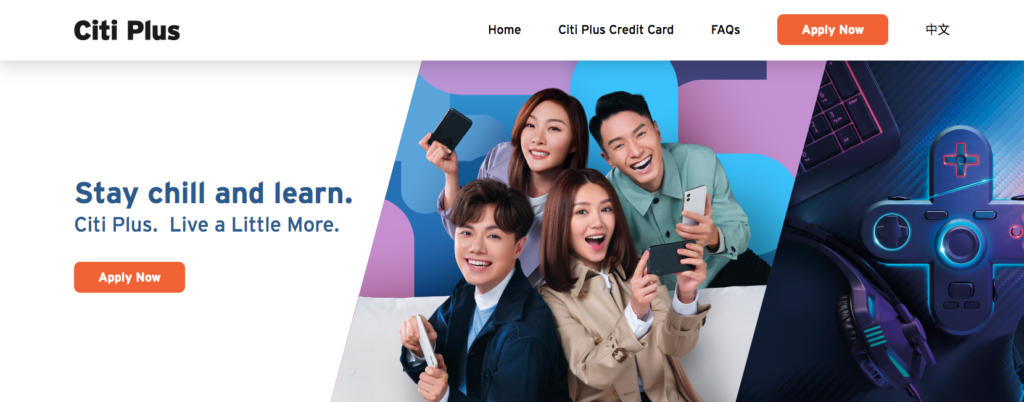

After piloting the product last year, Citibank Hong Kong formally unveiledCiti Plus, its mobile-first bank designed for digital natives.

The new offering aims to help users “level up” their banking experience by providing financial education, personalized wealth management tips, and easy access to a range of investment products.

“Citibank Hong Kong has shown strong determination in the development of digital banking in recent years. Citi Plus is our latest initiative to bring digital natives a banking experience they admire,” said Citibank Hong Kong Consumer Business Manager Lawrence Lam. “Millennials were invited to participate in research and the co-creation process, through which we could better address target clients’ pain points, and help them grow their wealth via the new service.”

The platform’s gamified user experience encourages users to build their wealth by accomplishing fun tasks. The Citi Interest Booster, for example, enables users to earn higher interest rate of up to 1.8% on their savings by completing what Citi calls “missions.” These missions include tasks such as maintaining a certain balance, funding accounts, investing, exchanging currency, and spending with their Citi Plus card.

In addition to the gamification element, Citi Plus will offer savings goals, debit and credit cards with built-in rewards, easy money transfer capabilities, and a low threshold investment platform. The investment opportunities include access to stocks, money market funds, and mutual funds from Aberdeen Standard Investments, Allianz Global Investors and Franklin Templeton.

In the first three weeks after the pilot launched, Citi received 5,000 registrants interested in Citi Plus, which is open to Hong Kong residents only.

The millennial-friendly user interface and marketing, combined with features such as low-threshold investing, financial education tools, and high interest savings accounts, help Citi compete with the increasing number of challenger banks and neobanks that are enticing young users. Unlike this group of digital banks, Citi has a slight upper hand. That’s because the bank not only has a robust existing user base from which to draw new clients, it also has an established reputation and inherent consumer trust.

This is a guest post written by Shannon Flynn, managing editor at ReHack.com.

Embedded finance has taken the financial industry by storm. What started from banking-as-a-service (BaaS) has now developed into a full-blown feature that enterprises of all kinds are integrating.

The term embedded finance refers to companies that have historically been separate from financial services that now integrate them within a platform or app. During this integration, the company still retains control over the customer experience. It could be something as simple as paying a bill or something more complex, like full-fledged credit cards.

These trends are coming on strong. While they originated with banking services, embedded finance could end up becoming a bigger industry on its own. The reason for this growth can be seen in the following sectors.

Retail

The retail world has evolved and adapted to many historic changes, from e-commerce to new payment methods. Most recently, the COVID-19 pandemic has put the spotlight on online shopping. Apps are now using embedded finance.

Delivery apps adapted as food takeout skyrocketed into popularity throughout the pandemic. Users can now save their credit or debit card information to apps like Doordash and Grubhub. Specific apps for restaurants also offer embedded finance options.

Similar things are happening elsewhere in the retail world. Shopify has connected businesses and customers quickly and efficiently with new embedded tech channels. Financial information is saved for customers so payments are a breeze. On the other side of the transaction, the embedded financial tech includes a dashboard for retailers to view and manage profits and individual orders.

These kinds of integrations cut out the need for a bank or other financial institution. Instead, consumers can do it all themselves.

Automotive

The automotive industry has always done business through banks. When someone buys or leases a vehicle, dealers will contact a financial institution to better understand someone’s standing and credit. The industry is shifting, though.

Tesla is a key example of how embedded tech trends are impacting the automotive field. Shoppers can already use car sites and apps to pay their leases, but Tesla goes a step further and offers car insurance. It monopolizes on the opportunity to provide discounts.

Ridesharing has become a massive field. Through apps like Uber and Lyft, customers can call a car in minutes. These apps have evolved over time and now offer embedded financial services where customers can pay right from the app immediately after the driver drops them off.

This form of payment adds an extra layer of convenience that other services like taxis don’t offer.

Tech

In the past several years, big tech companies have gone from prominent to all-encompassing. Notably, Google and Apple have stepped up their financial services in a short period, offering things like Apple Pay and Google Pay. Customers can also use their Apple or Google wallets to store credit and debit cards. Moreover, Apple rolled out its first credit card in 2019.

These advancements mark a shift in the big tech world. Big companies are slowly separating from financial institutions and taking on those roles themselves. For instance, if you use your Apple Card from your Apple Wallet to pay for items, none of that interaction ever leaves the company’s control.

Embedded finance changes are happening on smaller scales in the tech world, too. Data and analytics companies may use tools like machine learning to adapt to consumer behavior when making purchases. They can then better enable companies in all industries to provide more embedded tech.

What the Embedded Finance Trends Mean

These three industries are pillars of innovation around the world. Banking-as-a-service has catapulted financial technology to the forefront of these fields, and embedded finance trends have become the norm. It may even outshine BaaS soon.

Physical branch locations decreased by 7% from 2015 through 2020 due to the rise in online banking. The turn to virtual resources is slowly taking over, which seems to be the natural progression of these industries — especially as the pandemic enforces the use of remote tech.

Embedded finance allows companies and consumers to operate independently from banks and financial institutions. This dynamic gives more agency to the industries themselves, helping to boost engagement and profits.

From here, more mobile apps and websites will directly incorporate financial resources into their dynamics. Big tech companies like Apple and Google are already pushing the boundaries of what embedded tech can do. Others are likely to follow suit.

The Convenience Factor

Embedding financial resources into industries that haven’t historically worked in finance is more than just a way for companies to engage consumers. They’re also a win for customers. After all, people tend to look for the most convenient ways to do things. Having everything in one place is a financial tech trend that is only going to grow from here.

ShannonFlynn is a technology and culture writer with two plus years of experience writing about consumer trends and tech news.

One of the major players in the Buy Now, Pay Later (BNPL) game, Sezzle, is teaming up with Discover this week. Through the partnership, Sezzle will work with select players on Discover’s network to provide their customers with additional payment options.

The merchants will be able to use Sezzle’s interest-free, BNPL payment technology to process payments on Discover’s network. Sezzle anticipates the partnership will help boost its business development efforts by connecting with Discover’s established relationships.

“Our merchant partners are always a top priority and we know that providing them with additional payment options, such as a buy now, pay later structure, can be beneficial, especially in the current economic environment,” said Discover’s SVP of Global Business Development and Acceptance Jason Hanson. “We are able to leverage our unique technology capabilities and vast network of merchant relationships to provide Sezzle the ability to grow its business and provide new payment opportunities.”

Founded in 2016, Sezzle currently reaches 2.2 million active customers. Last September, the company launched a virtual payments card that helps customers benefit from Sezzle’s BNPL tech when they make purchases at brick-and-mortar stores. The company launched on the Australian Stock Exchange in the summer of 2019 and has a current market capitalization of $1.1 billion.

By now you’ve likely heard of Central Bank Digital Currencies (CBDCs). With consumers’ lives taking place increasingly online and the recent boost in cryptocurrency usage and value, much of the global economy is ready to move from discussing CBDCs to formally implementing a CBDC strategy.

But though there has been some progress in this area, there is still a lot of confusion in the broader banking and fintech community. If you’re feeling a bit behind on the CBDC discussion, here are five things to know that can help you catch up:

Six countries are currently piloting CBDCs

While much of the world is struggling to wrap their heads around CBDCs, some countries are ahead of the game and already have pilot programs in place. Of these, the most well-known is China, but Thailand, the Republic of Korea, Ukraine, Sweden, and Uruguay are also actively piloting CBDCs. Additionally, Brazil reports it plans to formally launch its CBDC next year.

A handful of countries, including Canada, Venezuela, Cambodia, South Africa, and the UAE have made key developments with their CBDC programs.

Other countries are still in the research phase or have had no development.

Check out this interactive map from the Atlantic Council to learn more about each country’s progress.

CBDCs don’t necessarily need the blockchain

Many people associate CBDCs with Bitcoin, which can be a helpful way to think of distinguishing Central Bank currencies from fiat money in digital form. But while Bitcoin leverages the blockchain, CBDCs don’t necessarily need to.

That’s because blockchains are used when there is no central party to provide trust. When central banks serve as the trustworthy authority, however, this decentralization is no longer necessary.

In fact, according to a survey conducted last February by the U.K.’s Central Banking Magazine, only one reserve bank said that they planned to use a blockchain for the structure of distributing their CBDC.

There are two types of CBDCs

Many people don’t know this, but there are actually two types of CBDCs– wholesale and retail. Wholesale CBDCs facilitate clearing operations between the central bank and its member banks, while retail CBDCs are for the general public to use, taking the place of the bank note.

There will still be room for cash

CBDCs will work alongside cash, or fiat currency. While there are both negative and positive aspects to paper money and coins, there will still be a cash economy. CBDCs simply combine the convenience of a cryptocurrency with the stability and regulation of fiat currency.

CBDCs won’t harm banks

As Chris Skinner highlighted in a blog post recently, CBDCs have the potential to disrupt banks to the point making them obsolete. Because CBDCs are issued digitally, they could technically circumvent banks.

Skinner concludes, however, “The true role of banks, whether in a digital currency or cryptocurrency world, is to store and exchange value with trust. That’s why they’re regulated the way they are and why they exist the way they do. And that isn’t going away anytime soon.”

Opera, one of the top internet browsers, announced a suite of in-browser cashback and payment tools for ecommerce. The release of the tools coincides with the launch of Dify, Opera’s new digital wallet.

Dify is a standalone mobile app that will enable users to open a Dify checking account and make purchases using a free, virtual Mastercard debit card. The account also features a special shopping mode, which protects users’ data while they shop by disabling third party extensions.

“Every day millions of people shop online and make their payments using Opera browsers,” said Opera EVP Browsers & EEA Fintech Krystian Kolondra. “Opera has a track record of growing audiences and then improving their experiences to make them more engaging. We think this is one of the highest-potential areas: With Dify, we are making the browser and a superior wallet work better, together, to improve users’ shopping experience and also make it financially rewarding.”

At launch, the main incentive to opening a Dify account is the cashback feature. Shoppers will receive cash back for purchases made on Opera’s partner websites accessed through its browser and will receive additional cashback on purchases made using their virtual Dify Mastercard.

Opera has a larger vision for Dify’s future, however. The company plans to enable more wallet services like savings management, credit products, investment opportunities, and instant cashback.

Dify is currently available to users in Spain in beta. Opera says it plans to expand to more European markets in the future.

Today’s launch follows a recent expansion of online shopping. According to research from J.P. Morgan, last year ecommerce activity reached $863 billion (€717 billion). The bank’s reports indicate that many countries in Europe will continue to have double-digit growth this year.

Australia-based financial comparison website Mozo has agreed to be acquired by British Media company Future PLC.

Future anticipates the purchase will fuel its global growth by creating a new revenue stream, adding a new financial services content arm in Australia, and growing Mozo’s market share.

Founded in 2008, Mozo is a B2C site that helps consumers compare offers on home loans, credit cards, and personal loans, as well as compare banking and insurance products. In total, the company compares more than 1,800 products from over 200 banking, insurance, and energy providers.

Monzo is also known for its personal finance resources. The company offers financial calculators and creates content to help guide readers through financial decisions and build their awareness of the finance world.

“We’re delighted to be adding Mozo to the Future family,” said Future CEO Zillah Byng-Thorne. “We are seeing the increasing convergence of content and price comparison and this acquisition supports our global growth ambition in this area.”

Mozo has raised $1.4 million (£1 million) via one round of funding. The company’s team of 45 employees works out of Sydney, Australia.

Cryptocurrencies have dominated the fintech headlines this week- from Mastercardagreeing to allow merchants to accept payments in cryptocurrencies to BNY Mellon’s announcement that it will begin custody of cryptocurrencies.

Today, after bitcoin reached an all-time high of over $48,000, marketing services company Kasasaunveiled plans to help its bank and credit union clients provide bitcoin wallets to their consumers.

The new capabilities will be powered by a partnership with New York Digital Investment Group (NYDIG), a technology and financial services firm dedicated to Bitcoin. The collaboration will help Kasasa’s bank clients stay ahead of the rapidly growing bitcoin adoption.

“Clearly, Bitcoin is here to stay, and consumers are demanding that Bitcoin offerings be made through their trusted financial institutions,” said Kasasa CIO John Waupsh. “With this new partnership, we’re looking across the product and services that Kasasa currently offers, as well as future product and service ideas. With NYDIG we can evaluate new offerings such as a buy-sell-hold wallet while also incorporating Bitcoin into our core rewards business.”

This partnership will be a major selling point for Kasasa, especially as consumer interest in cryptocurrencies rise. According to NYDIG, more than 22% of U.S. adults over the age of 18 own Bitcoin today.

This interest, combined with the creation of formal regulation like the OCC’s recent ruling that banks may use stablecoins for payment facilitation, is bringing cyrptocurrencies into the forefront of banks’ agendas. With today’s partnership, Kasasa is better positioned to help small financial institutions compete with larger players when it comes to cryptocurrencies.

If you have the WiFi, we’ll bring the content. This month, we’re hosting two FinovateFocus events– Connect and Roundtable. Both events are free to attend and will take place on February 25 from 9 a.m. to 11:45 a.m. Central Standard Time.

Register for these all-digital micro events and you’ll not only have access to great content, but you’ll also have the opportunity to check out the unique format and full roster of discussions and networking.

This month’s discussions will focus on the digital user experience. Now more than ever, your digital user experience is what your customers see; it shapes how they view your organization. Our dive into digital will help inform how you can leverage your UX to increase sales, create happy customers, and increase operational efficiency.

Here’s what to expect at each event:

FinovateFocus Connect

This event maximizes your time by bringing you nine presentations and nine meetings, all within the span of an hour. The platform will alternate between three-minute presentations and three-minute meetings, which are pre-assigned based on common interests.

FinovateFocus Roundtable

This discussion-based event includes your choice of two moderated, 30-minute roundtables with 15 minutes of networking before and after each roundtable conversation. To encourage engagement, each roundtable is limited to eight participants each.

Roundtable discussions for this month’s event include:

Earning customer trust in the digital age

Future of payments –are we turning into a cashless society?

Effective customer acquisition, engagement, and retention – the Experience Age

Boosting CX in banking with AI – conversation banking: exploring back-end technologies

Authentication, biometrics, and digital identity in digitized society

Chatbots, AI, automation as a platform for revolutionizing the CX

Personalization and customization with data in the banking and payments industry

Insights into how to support financial futures for customers in a post-COVID-19 world

Customer Service NOW

Video banking as a preferred means of customer communication

What do customers want – Meeting customer needs

APIs and Open Banking – Putting the customer in the driver’s seat

FinovateFocus starts on February 25. The Connect portion will run from 9 am to 10 am Central time while the Roundtable portion will run from 10:15 am to 10:45 am Central time. Both events are free to attend, so sign up early.

While you’re signing up, check out the deals for FinovateFocus sessions in March, April, May, and June available on the registration page. Sign up for a single event or purchase a bundle package to save.

Here are the topics we have planned for the months ahead:

Data analytics firm Moody’s announced plans to acquire data insights company Cortera this week. Terms of the deal, which is expected to close in the first quarter of this year, are undisclosed.

Moody’s anticipates the purchase will enhance its risk assessment capabilities. The move will also significantly extend Moody’s coverage in the SME market– the segment that serves as Cortera’s focus.

“Cortera plays an important role in helping businesses understand each other,” said President of Moody’s Analytics Stephen Tulenko. “Our customers will be able to leverage Cortera’s extensive information on small businesses with Moody’s proprietary analytic tools to make better decisions.”

Cortera was founded in 1993 and provides credit data and workflow solutions on North America-based public and private organizations. The Florida-based company maintains a database of credit information on more than 36 million businesses across the continent.

Cortera sources this data from thousands of resources and scrubs it using AI. As a result, the company is able to provide analytics, reports, and monitoring services to help inform businesses’ decisions.

Specifically, the acquisition will augment Moody’s Orbis database of private company information and enhance its KYC, commercial lending, and supply chain solutions.

Moody’s was founded in 1900 and provides data, analytical solutions, and insights to help businesses identify opportunities and manage risk. The company employs more than 11,000 people across 40+ countries. Headquartered in New York City, Moody’s is publicly traded on the NYSE under the ticker MCO. The company has a market capitalization of $52 billion.

Klarna is taking its Buy Now, Pay Later (BNPL) platform to a logical next step. The Sweden-based company announced today it will launch a bank account offering in Germany.

This move makes Klarna the first BNPL firm to make such a move. The company will now compete with the growing roster of digital banks in Germany, including N26 and Tomorrow.

Users will receive a Visa debit card, which is available in two colors, and will have tools on the app to track, manage, budget, and analyze their spending habits. Klarna will also reimburse users for two global ATM transactions per month.

“Our focus is to provide a superior shopping experience to our consumers at the intersection of retail and banking,” said Klarna CEO Sebastian Siemiatkowski. “And we know that there’s still massive room for improvement to the way many people bank and save their money today. Users are demanding more seamless, intuitive and transparent services to meet their daily needs, but many banks still do not cater for this.”

As Siemiatkowski points out, Klarna banking will be useful for “bundling shopping and banking in one app.” However, it is difficult to see the extra value a Klarna bank account will bring to users who aren’t big on shopping. N26 touts an integration with Transferwise for easy and inexpensive foreign money transfers and Tomorrow differentiates itself with a positive approach to sustainability and social causes. Klarna, in contrast, makes shopping a more embedded experience. This isn’t necessarily a positive attribute for one’s finances.

To counteract this “spend, spend, spend” mentality, Klarna said it has plans to add savings goals to the banking app, a feature that is already available in Sweden.

A pilot of Klarna’s bank account will initially be available to the company’s “most loyal” users and will roll out to all Germany-based users “in the coming months.”