This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Two Canadian fintechs have struck a deal this week. Payments network and digital ID provider Interac has agreed to acquire rights to digital ID and authentication provider SecureKey’s digital ID services for Canada.

Interac, which is building a network to help Canadians digitally share and verify their identity credentials, will leverage SecureKey’s digital ID services, along with its operations, technology, and innovation. Ultimately, Interac seeks to accelerate secure online service delivery and offer strong privacy and fraud protections for the digital economy in Canada.

“At Interac, we believe that digital ID is the key to empowering all Canadians to participate equally and safely in the future of the digital economy,” said Interac CEO Mark O’Connell. “Through this acquisition, we are proud to increase our investment in leading identification and authentication capabilities as we work to support businesses and governments across Canada in delivering secure and convenient digital ID experiences for Canadians.”

Both companies will continue to operate as separate entities. Interac will implement Verified.Me, a digital ID verification network built on distributed ledger technology, and Government Sign-In by Verified.Me, a secure sign-in tool to access 280+ government services.

“As the pandemic has made abundantly clear, the way Canadians use their identity documents and how they prioritize accessing services digitally has changed forever,” said Chief Officer of Innovation Labs & New Ventures at Interac Debbie Gamble. “The need to accelerate innovation to provide secure and convenient options for people to transact with their identities is critical.”

This announcement follows Interac’s acquisition of Ottawa-based 2Keys, a company focused on creating secure digital experiences, in 2019.

Founded in 2008, SecureKey has made a couple of key partnerships recently. The company partnered with Onfido in March of 2020 to offer real-time photo ID verification and teamed up with Simplii Financial in May of 2020 to offer Simplii clients with secure access to government services.

After finalizing the deal with special purpose acquisition company (SPAC) Fusion Acquisition Corp. this week, MoneyLion is now publicly traded on the New York Stock Exchange under the ticker symbol ML.

For additional insight into this milestone, we spoke with MoneyLion CEO and Co-Founder Dee Choubey. Prior to co-founding MoneyLion in 2013, Choubey spent over a decade on Wall Street inside the largest banks learning about the inefficiencies that exist within banking. He built MoneyLion to create a private banking experience for everyday Americans by offering credit, banking, and investing in a single app.

Talk to us about MoneyLion’s journey so far. What has growth been like since the company was founded in 2013?

Dee Choubey: We founded MoneyLion with the goal of rewiring the consumer finance system, giving hardworking Americans access to previously exclusive private banking services. At MoneyLion, we bring consumer finance into the future by combining AI, machine-learning technology, and behavioral science to create a full-service, digital financial platform for our users. Since 2013, we have engaged with over 8.5 million Americans, empowering them with a digital banking platform that helps them better manage their finances today and build wealth for tomorrow.

This has been a historic year for the company. Since announcing we were going public via a SPAC in February, to listing on the NYSE on September 23rd, we’ve continued to see consistent growth and a validation of our business plan. Entering the public markets will enable us to scale our capabilities and reach even more hardworking Americans. Since the start of 2021, we’re up across all key financial and operating metrics, including 100%+ year over year growth in net revenue. Our user growth has also accelerated this year, with total customers increasing almost 60% in the first half of 2021 to 2.3 million.

Earlier this month, we raised our annual revenue guidance for fiscal years 2021, 2022, and 2023 to reflect higher projected user growth, along with expected revenue contribution of planned product launches including our new crypto and Buy Now Pay Later offerings. As a public company, we will remain laser focused on positioning ourselves for optimal execution on our well-defined growth objectives.

How did you know that a SPAC was right for MoneyLion?

Choubey: For us, we’d spent the last eight years focusing on building proprietary technology. As we saw the product market fit of MoneyLion accelerating, we knew it was time to take MoneyLion’s innovative products to more Americans, and a SPAC provided us with an entry point to enhance our public presence as well as capitalize the business. As with everything we do at MoneyLion, it ties back to our mission: to provide top-notch financial access and bespoke advice to every hardworking American.

Listing via a SPAC was the best option for us due to its efficiency in allowing us to strengthen our balance sheet. With the capital we raised through this transaction, we are now able to accelerate the execution of our growth strategy, deliver against our mission, and provide incredible value to our customers and members.

What has been the hardest part of the SPAC process?

Choubey: If anything, our biggest challenge was timing. We announced the merger with Fusion Acquisition Corp in late February, expecting to be public somewhere in June or July. It took longer than anticipated to get through the whole process, in part due to the number of deals coming to the market.

With the merger behind us and our balance sheet fortified, we’re all very excited about this next chapter in the MoneyLion journey. For the past eight years we have been focused on building our proprietary tech stack, and we think we have one of the best platforms, not only here in the United States, but globally. We’re poised to build on that strong foundation and make MoneyLion a daily destination for all hard working Americans, combining our robust financial products and services with highly personalized content and advice to help our customers take control of their finances and achieve their life goals.

What advice would you offer other fintechs considering the SPAC route?

Choubey: Find the right partner with whom to go public. And that usually entails the sponsor’s knowledge of its investor base, their willingness to do whatever it takes to accurately position the company, as well as a specific understanding of the capital markets including the pipe market. At the end of the day, the fintech needs to have public market fit and a good sponsor can help create an efficient framework.

Will anything about MoneyLion change now that the acquisition is finalized?

Choubey: We’re no longer trading under FUSE; we’ve officially taken over the ML ticker on the New York Stock Exchange. For those that remember, ML was Merrill Lynch’s ticker, an iconic American financial institution. Today, we are immensely proud to have that ticker as we grow into our own iconic American brand. As we like to say, the ‘bull has become the lion’.

In terms of what’s happening within MoneyLion, we are going to continue to work hard and deliver against our mission: harnessing the power of technology to empower millions of hardworking Americans to take control of their finances so that they can achieve their life goals.

Wealthtech company Betterment has boosted its total funding to $435 million after closing $160 million in growth capital this week. The funds include $60 million in Series F equity and a $100 million credit facility.

The new round values Betterment at $1.3 billion. The equity portion was led by Treasury with participation from existing investors Kinnevik, Bessemer Venture Partners, Francisco Partners, Menlo Ventures, Anthemis Group, Globespan Capital Partners, Citi Ventures, and The Private Shares Fund. New investors Aflac Ventures and ID8 Investments also participated.

The $100 million credit facility comes from ORIX Corporation USA’s Growth Capital group and Runway Growth Capital.

“We are thrilled to have the support of new and existing investors who believe in our business model and are excited by the opportunity to support our growth,” said Betterment CEO Sarah Levy. “We’re using these funds to further cement our category leadership with rapid innovation on top of our already differentiated product suite and unique, multi-pronged distribution model that serves retail investors, advisors and small businesses.”

More specifically, Betterment will use the funds to support its 401(k) offering for small and medium sized businesses.

Founded in 2010, Betterment manages $32 billion in assets for its nearly 700,000 clients. In addition to offering automated 401(k) and IRA options, the company also provides socially responsible investment options, retirement planning services, a checking account, and a high-yield savings account.

Today’s announcement comes after a flurry of news activity for Betterment, after the company appointed Levy as CEO in December of last year. In March, the company acquired the investment advisory business of WealthSimple, partnered with Zenefits to offer 401(k) plans on the Zenefits platform, rolled out a checking account for shared finances, unveiled a co-pilot tool for advisors, and launched pre-packaged tech stack for RIAs.

U.K. digital bank Starlingannounced plans to expand its banking-as-a-service (BaaS) solution.

Starling launched its BaaS offering, Starling as a Service, in the U.K. in 2018. The company currently has 25 BaaS customers, including Raisin, CurrencyCloud, Moneybox, and Vitesse.

Starling as a Service will expand to the European Union in the first half of this year. Specifically, Starling aims to bring the service to companies in France, Germany, The Netherlands, and Spain.

The BaaS offering will enable businesses to build their own embedded financial products. While the business client offers the financial product to its end customers, Starling handles all technical and regulatory details involved.

Starling CEO Anne Boden described the European markets as a “great fit” for Starling due to the region’s “thriving” fintech scene. “We have seen a consistent and growing demand for digital financial services, further accelerated by extended lockdowns and a shift in consumer behaviors in key European markets,” said Boden, “and it is clear that Starling can power new and exciting opportunities for businesses across Europe.”

Starling as a Service takes advantage of the embedded finance trend that has been building since last year. By leveraging third party fintech solutions, any business can itself become a fintech by offering financial services to its customers. In Starling’s case, Starling as a Service will enable businesses to provide savings and current accounts, digital wallets, data processing, and payment cards.

Today’s news comes after Starling scored $376 million in funding in March and acquired Fleet Mortgages in July of this year. Headquartered in London, and with offices in Southampton, Cardiff, and Dublin, Starling has amassed $922 million in funding since launching its digital bank in 2014.

The pandemic has not only shined a light on the inequalities of women in the workplace, it also created a larger gap, especially for working mothers. Between mandatory home schooling and a lack of childcare, the workload that women bear around the house is increasing.

There have been plenty of studies and articles stating that these demands are placed unfairly mothers, have made it difficult for them to advance in their career, and have caused many mothers to drop out of the workforce entirely.

I don’t want to minimize the headaches that moms (and truly everyone) have endured over the past 20 months. However, it’s worth pointing out a few ways that the pandemic economy has actually benefitted working mothers, specifically mothers working in fintech (myself included).

Flexible hours

The need for employees to balance work with home schooling and childcare motivated many workplaces to embrace more flexible working hours. As long as employees produce quality work, put in the necessary hours, and attend mandatory meetings, many are able to set their own schedule that works with their family.

Moms are always on call, whether to nurse a baby, help with homework, solve an argument, or change a diaper. So being able to step away from the computer to take care of pressing tasks is a huge benefit.

Remote working is the new norm

Prior to the pandemic, many workplaces were strictly against remote work, even when in-person collaboration wasn’t necessary. While commuting into an office five days a week has its benefits, it also comes with its share of difficulty. Not only does the extra time of the commute add up, but there is also more time and money spent on a professional wardrobe and makeup.

For breastfeeding mothers, long commutes are especially burdensome because the more time spent away from the baby means the more times mothers have to pump, store milk, and wash and sterilize bottles.

Meetings and conferences come to you

I included this point because of personal experience. My son was nine months old when I attended my first conference after maternity leave. Because I was still nursing, I chose to bring him with me to FinovateFall 2019 in New York. Even though I was physically at the conference, I still missed out on much of the content because I had to step out to nurse him so frequently.

In comparison, at FinovateFall 2021 last week, I was able to attend the show digitally from my home office with my newborn daughter on my lap. I was so much more present during the demos and discussions since I wasn’t running back and forth from the venue to a hotel room.

In this post-pandemic way of work, many businesses have made a point to offer digital experiences either in place of or alongside physical meetings. Now that so many more meetings and conferences offer a digital option, women do not have to miss out in the event they need to care for a sick family member or if they have a gap in childcare.

Normalizing home life

Perhaps the biggest upside of the pandemic is that it has shed a light on the full breadth of women’s duties outside of the workplace. Not only this, but colleagues are more accepting of times when family life collides with work. I’ve worked from home for 11 years, and prior to the pandemic I would have been mortified if my two-year old was audible outside of my office door on a conference call.

In this new era, colleagues and clients are much more open to home life. In fact, I’ve videoconferenced with people who not only don’t mind seeing and hearing children in the background of calls*, but they also ask me to bring them to the computer so that they can say hello to their children on the other end of the screen.

*At least within reason. Yes, children can be quite annoying sometimes.

Royal Bank of Canada (RBC) launched two new capabilities for its NOMI financial intelligence platform. Unveiled today, NOMI Forecast shows users their future cash flow. The app also has increased its security with the launch of two-step verification upon login.

“At a time when Canadians are more conscious than ever of their daily finances, and banking digitally more frequently, they expect solutions that help them confidently manage their money and safeguard their accounts and information,” said RBC SVP Digital Peter Tilton. “With NOMI Forecast, we’re giving clients next generation cash flow advice and insights to take the stress out of balancing their accounts. Equally important, 2-Step Verification will work to provide clients added peace of mind as they navigate this rapidly evolving digital banking landscape.”

NOMI Forecast works by showing users all of the pre-authorized payments they have coming over a seven-day period. By accounting for known upcoming expenses, the forecasting capability offers users better visibility of their account activity and helps them have more control over their finances.

With the two-step verification process, users can select their mobile device as the primary channel to access the account. If they attempt to login with another device, they receive an in-app notification to verify their session. Unlike two-factor authentication, there is no security code delivered via email or text. Instead, the user presses a button to continue their session.

In a press release, RBC said that the two new features demonstrate the bank’s “commitment to add value, enhance security, and create peace of mind” for clients.

Financial document automation platform Ocroluspulled in $80 million in Series C funding today. The round was led by Fin VC and included participation from Thomvest Ventures, Mubadala Capital, Oak HC/FT, FinTech Collective, QED Investors, Bullpen Capital, ValueStream Ventures, Laconia, RiverPark Ventures, Invicta Growth, Stage II Capital, and Cross River Bank.

The New York-based company now boasts $127 million in funding and is valued at over $500 million. Ocrolus plans to use the funds to expand U.S. operations and “more aggressively” build products for banking and mortgage lending.

“Our platform helps lenders automate underwriting and intelligently leverage cash flow and income data for credit scoring,” said Ocrolus Co-founder and CEO Sam Bobley. “By enabling lenders to more quickly analyze diverse sources of financial data, Ocrolus levels the playing field for every borrower, providing expanded access to credit at a lower cost.”

Ocrolus was founded in 2014 to create a document processing automation solution that helps lenders classify, capture, detect, and analyze financial documents to make better lending decisions. To accomplish this, the company leverages AI, machine learning, and human-in-the-loop (HITL) optimization. The HITL component serves as Ocrolus’ key ingredient to differentiation because it ensures an enhanced level of accuracy when analyzing data derived from documents.

The company, which won a Best of Show award at FinovateFall last week for its document analysis technology, has benefitted from the recent acceleration of digitization brought on by COVID. In today’s lending environment, FIs need to offer online options to compete. We spoke with Ocrolus’ VP of Solutions Nicole Newlin last year on the effects of this digitalization.

Ocrolus’ client list is as impressive as it is extensive, including firms such as Brex, Enova, Lending Club, PayPal, Plaid, and SoFi. Accommodating for a recent uptick in demand, the company added more than 75 employees this year and plans to boost its hiring efforts next year, focusing specifically on machine learning and data science professionals.

At FinovateFall last week, Citizens Bank of Edmonds CEO Jill Castilla described how she is leading her bank through the pandemic. In her 16-minute address, she described how her bank navigated the decision making process and leveraged fintech relationships to help their small business customers survive COVID lockdown.

Citizens Bank of Edmonds was founded in 1901, has $400 million in assets, and 55 employees. The bank aims to serve everybody and has a goal to be the best at everything. And while that sounds like a lofty goal, the bank has proven that it is up to the task by implementing unique solutions that come alongside customers to meet their needs.

So what does it take to be such a successful bank in both the eyes of competitors and customers? Here are three takeaways from Castilla’s keynote that are worth considering.

Communication is foundational

By today’s standards, Castilla is very liberal about offering up her contact information. During the pandemic, she was quick to share her cell phone number; she even tweeted it out multiple times! Providing this open line of communication to both staff and customers was key to ensure that nobody fell through the cracks. Castilla even concluded her keynote by sharing her phone number, saying, “You’re welcome to text me any time.”

But it doesn’t end there. When the pandemic hit, Castilla made sure to contact all of Citizens Bank of Edmonds’ business customers to determine their main areas of stress. And when the bank had to close its lobby, it sent employees to meet customers at the curb to schedule time slots to serve its customers and maintain the personal touch.

Look forward

Castilla watched Frozen II during lockdown and the quote, “All one can do is the next right thing” caught on. In trying to make decisions for the bank, Castilla and her team would consider “the next right thing.” In other words, they would think about what the best decision would be for the future, and not for the present moment.

Castilla offered the example of using the mantra to determine if Citizens Bank of Edmonds should host its annual block party at a time when COVID was just getting started. Thinking about the next right thing made it easy for the bank to call off the party.

And while a block party may seem trivial, consider this mantra implemented for a larger, more strategic decision making. Questions such as, “should we make an investment in AI technology?” or, “should we partner with this up-and-coming fintech?” are a bit easier to answer when filtered through the lens of the next right thing.

Focus on the needs of clients

This takeaway ties back into the first two points, because if financial institutions maintain a foundation of communication while focusing on the next right thing, they will ultimately be doing what is best for their clients.

“Doing the right thing will help you find your people,” Castilla said during her keynote, “And talking about what’s important to you out on social media and the digital space will help you connect with people.” She also noted that both banks and fintechs are trying to do what is best during this challenging time, adding, “Collectively and individually, while working together and on our own, we’re going to change the world for [consumers and small businesses], we’re going to provide greater access to credit, we’re going to have a better understanding of what their financials are, (and) we’re going to help them run more successful businesses.”

JP Morgan Chase announced this week it will replace its U.S. core banking suite with U.K.-based Thought Machine’sVault.

Founded in 2014, Vault is a cloud native core banking engine that leverages smart contracts to help banks and fintechs build in the cloud and avoid the constraints of legacy technology. Vault provides a full range of retail and small business banking capabilities, including checking accounts, savings, loans, credit cards, and mortgages.

In the future, Thought Machine plans to build Commercial and Private Wealth offerings into Vault, as well.

JP Morgan, which was in the headlines yesterday for its purchase of college planning platform Frank, will benefit from Vault. The technology’s cloud-based nature will decrease the siloed structure that comes with most large, legacy banks. Instead, JP Morgan will operate as a universal banking platform where all products run on a single system.

“JPMorgan Chase represents one of the most ambitious, powerful financial institutions in the world—and our joint work signals to the finance industry that cloud native core banking technology is the future for financial services,” said Thought Machine CEO and founder Paul Taylor. “We are delighted to be working with JPMorgan Chase on this project, delivering modern core technology to the bank, and powering the next generation of financial services in North America.”

Thought Machine, which raised $125 million last year, is said to be working on another $205 million funding round. The company has seen significant growth over the past year and has scaled up its clients base to include Lloyds Banking Group, Standard Chartered, Atom bank, Monese, and SEB. Not only that, the company added 100 employees in the first half of 2020.

Trustly, the company that helps customers pay directly from their bank account, launchedInstant Payouts for U.S. users this week.

The service helps U.S. businesses provide their clients with near-instant payouts to their bank accounts. Instant Payouts in the U.S. is made possible via a partnership with Cross River Bank, which participates in The Clearing House’s (TCH) RTP network, a real-time payments rail.

Trustly’s business users can fund payments with Cross River Bank, which will send RTP payments on their behalf to their customers’ accounts at other participating RTP banks.

“The RTP network provides a platform for financial institutions and their corporate users to create innovative new payment products for their customers,” said TCH SVP of technology and Innovation Bijan Chowdhury. “Trustly’s partnership with Cross River Bank to deliver Instant Payouts to U.S. businesses and Cross River Bank’s use of the RTP network to send instant payments to the the businesses’ customers illustrates the power of the RTP network to boost innovation in the payments industry.”

Trustly was founded in 2008 and supports card-not-present payments for online merchants to offer a secure way for consumers to transact using their online banking access credentials. Last year, the company processed over $21 billion in transaction volume in its network. At FinovateEurope 2017, the company debutedDirect Debit, a payment offering that removes the pain of entering payment card information by allowing users to transact using their current account by entering their bank login credentials.

Trustly works with more than 8,100 merchants, helping them connect with 525 million consumers and 6,300 banks across 30 countries. The company has 500 employees across Europe, North America, and Latin America.

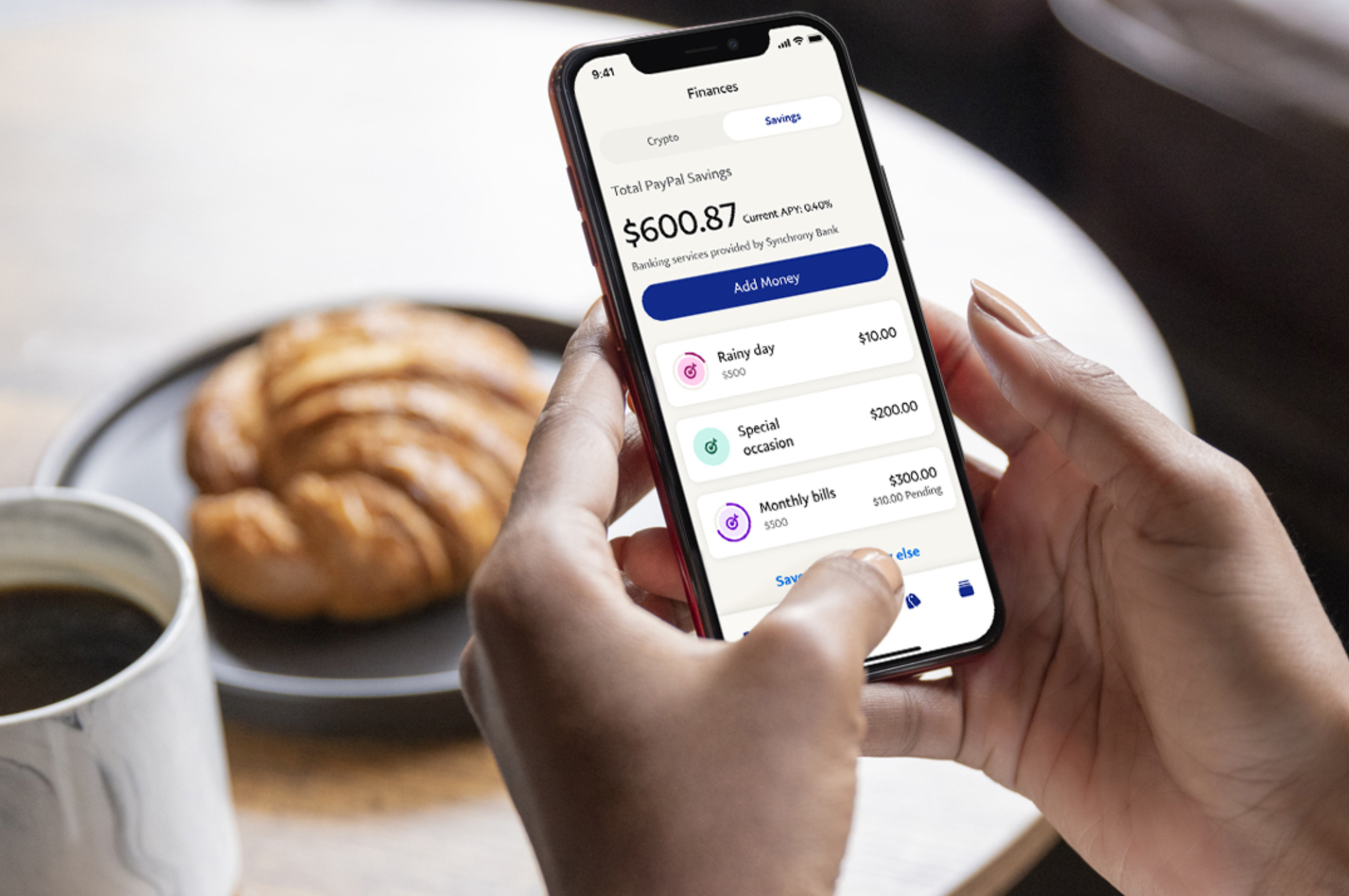

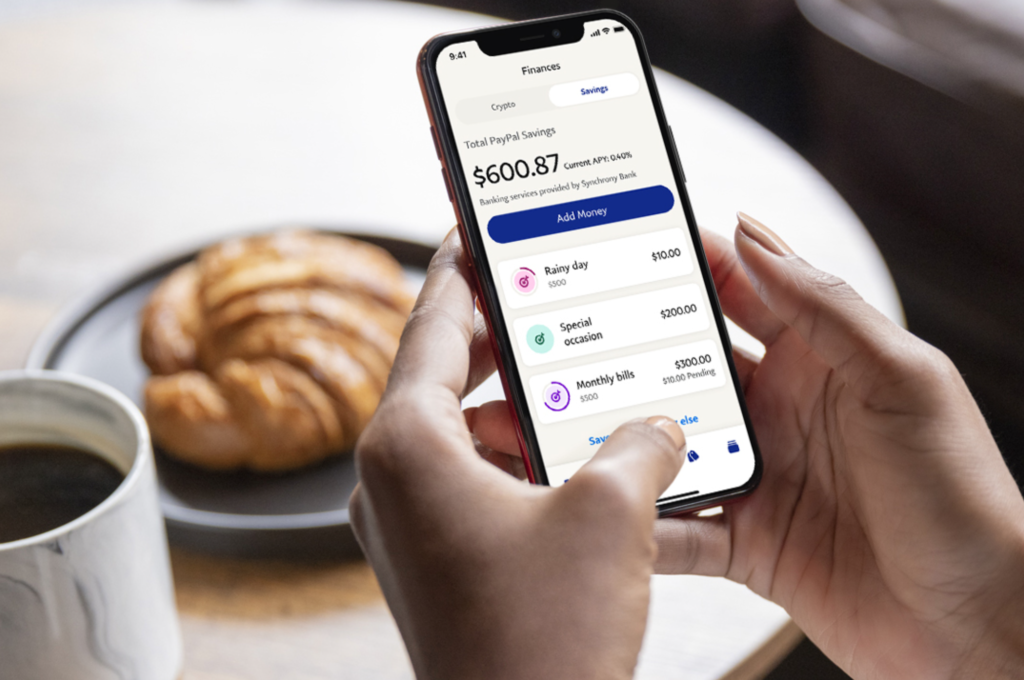

The company is adding a handful of features that bring it into “super app” territory, competing with the likes of WeChat, Alipay, and Paytm. PayPal’s app already offers a peer-to-peer payment tool, a mobile wallet, and a charity donation feature.

The new release, however, will offer more features and new banking capabilities. Here’s a rundown of what to expect:

PayPal Savings, a new, high-yield savings account provided in partnership with Synchrony Bank that pays 0.40% APY

In-app shopping tools that allow customers to discover and earn loyalty rewards

Billpay management tools that help users track, view, and pay their bills

A new Direct Deposit feature that fronts users their paycheck up to two days early

Rewards capabilities

Gift card management

Credit access

Buy Now, Pay Later services

Crypto purchasing, holding, and selling abilities

The app will show users a personalized dashboard of their account; a wallet tab to manage payments and direct deposits; a finance tab to access savings and crypto accounts; a payments tab that enables users to send and receive money, make a donation, and manage billpay; and a messaging feature built around peer-to-peer payments.

“We’re excited to introduce the first version of the new PayPal app, a one-stop destination for our customers to take charge of their everyday financial lives, with new features like access to high yield savings, in-app shopping tools for customers to find deals and earn cash back rewards, early access Direct Deposit, and bill pay,” said PayPal CEO Dan Schulman. “Our new app offers customers a simplified, secure and personalized experience that builds on our platform of trust and security and removes the complexity of having to manage multiple financial or shopping apps, remember different passwords and track loyalty rewards.”

What’s next for PayPal’s Super App? The company will add investment tools, offline QR code payments, and new shopping and deals capabilities.

PayPal is currently the closest thing the U.S. has to a super app. However, the new app is still missing some key elements that Asia’s successful super apps have, including food delivery, transportation, travel, health, insurance, government, and public services.

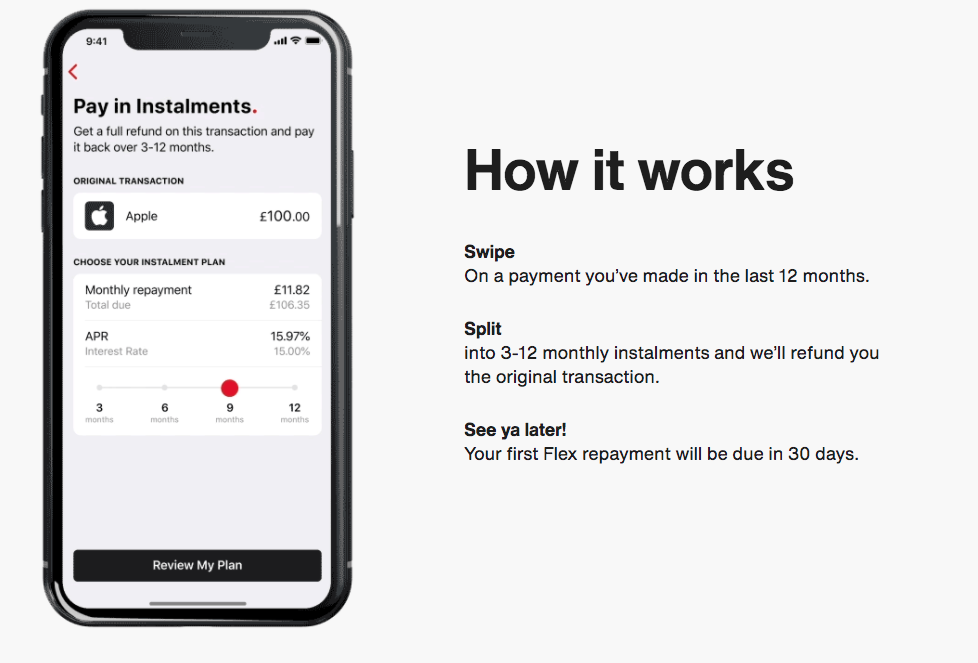

Curve, a U.K.-based payment card technology company, announced its own version of a buy now, pay later (BNPL) product this week.

The company is known for its unique payment solutions, such as its Go Back in Time feature that lets consumers switch payments from one card to another for up to 90 days after the transaction was made. Today, Curve is launching Curve Flex, a tool that builds on Go Back in Time.

Curve Flex allows consumers to convert almost any purchase from the past 12 months into an installment plan, as long as the card they used is linked in the Curve Platform. After the customer makes a purchase, all they need to do is swipe the transaction and select the number of installments. Then, Curve refunds their transaction in full almost instantly.

Unlike most BNPL tools, Curve Flex isn’t limited to specific merchants, cards, or products. It can be used on retail purchases, online orders, household bills, and more. Also unlike many BNPL tools, Curve’s offering charges interest based on the purchase amount and the number of installments.

“Curve is giving customers the unprecedented ability to convert transactions made up to a year ago into free or low-interest installment loans,” said Head of Curve Credit Paul Harrald. “Being able to Go Back in Time and Pay Later is going to forever change how U.K. customers think about managing their personal finances and cashflow.”

Curve Flex, which has been in beta for a year, already has 1,600 users that have opted to pay later on 7,000 transactions worth over $1.4 million (£1 million).