This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Ohio-based KeyBank made its sixth acquisition today. The bank purchased Banking-as-a-Service company XUP, a platform that helps banks take control of the merchant experience. Terms of the deal were not disclosed.

Founded in 2018, XUP connects merchants, third party financial service providers, and acquirers across channels to help banks offer a more integrated and seamless payments experience. KeyBank will use XUP’s technology to improve its embedded banking strategy and improve the user experience for its commercial users. The bank describes the move as the “next step in providing digital innovation at scale.”

Today’s news is only the latest development in the relationship between KeyBank and XUP. The bank contributed to XUP’s $3 million Seed round closed in February and the two were strategic partners. According to KeyBank, XUP helped accelerate the volume growth of its merchant payments capabilities. The bank now counts 150 million card transactions each year, accounting for $13.6 billion in annual card volume.

“We’ve long embraced the software innovation that’s sweeping through the financial services industry, and the acquisition of XUP allows us to continue to be a leader in this space,” said KeyBank’s Head of Enterprise Payments & Analytics Ken Gavrity. “XUP’s highly experienced team has accelerated us on the journey to build connectivity across our systems, our partners, and our customers, to make it easy to do business with Key.”

XUP will continue to operate as its own entity and support its customer base. “Our end-to-end software solutions, combined with Key’s scale and deep financial services expertise, will perfectly blend to provide clients a best-in-class payment experience,” said XUP President Chris May.

KeyBank was founded in 1825, has $187 billion in assets under management, is headquartered in Cleveland, Ohio, and has 1,000 branches across the U.S. The bank’s other acquisitions include AQN Strategies, Finovate alum HelloWallet, First Niagara Financial Group, EverTrust Financial Group, and Leasetec. Among the company’s strategic partners are AvidXchange, BillTrust, and Bill.com.

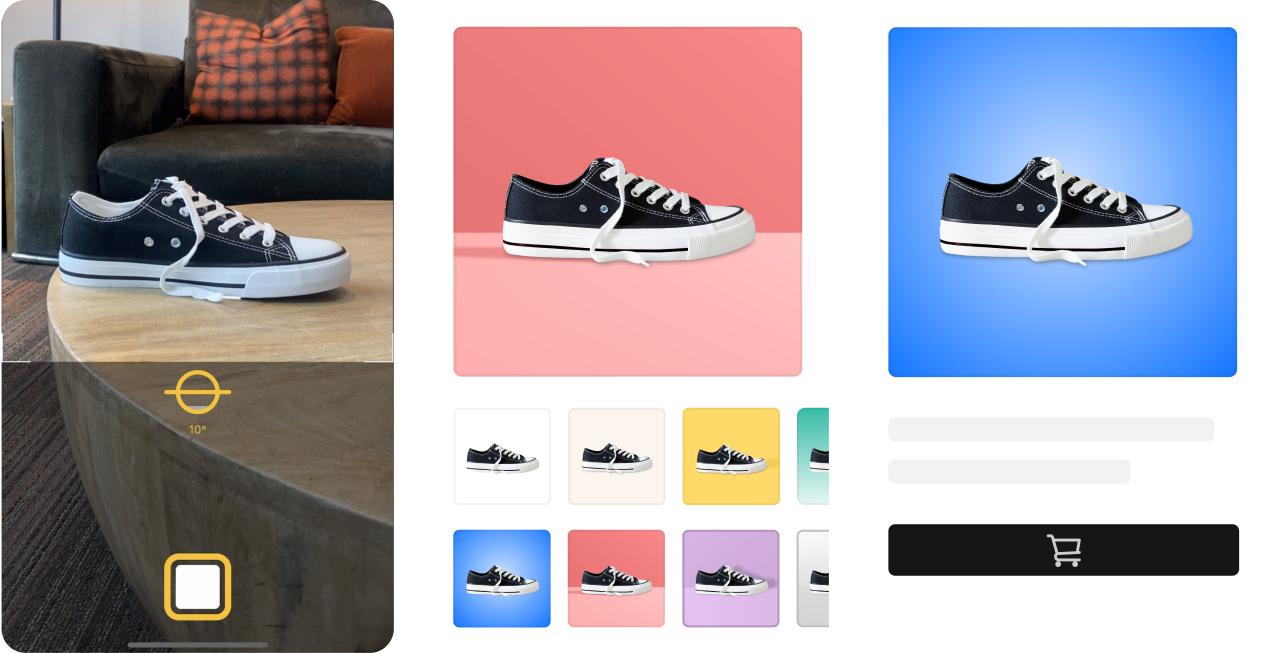

Merchant services aggregator and mobile payments company Square is making online merchants’ lives easier with a new launch today.

The Square Photo Studio app helps sellers take high-quality pictures of merchandise and sync them to their online store.

The app, which is available to both Square sellers and anyone with a Square Online Checkout link, guides merchants through easy-to-follow prompts to help them take the best photo. The photo studio automatically isolates the product from the background then helps users stylize the photo with backgrounds, shadows, and colors.

Once the seller has optimized their photo, they can connect their images to the corresponding items in their Square catalog or create a new item. After merchants list items in the catalog, they can start selling immediately.

“It’s no secret that products with professional-looking photos perform better than those without,” said Head of eCommerce at Square David Rusenko. “Unfortunately, the cost, skill set, and labor involved with taking those photos was often prohibitive. Now, with Square Photo Studio, sellers can give their items the look of a professional photo studio shoot from the comfort of their home, the office, or on the go.”

The Square Photo Studio app is available to everyone in the Apple App store, which creates a lower barrier to entry for anyone who wants to sell physical goods. Because the app is very accessible and easy-to-use, it has the potential to increase the number of transactions from Square sellers.

Buy Here, Pay Here (BHPH) crowdsourced securitization firm Agora Data is coming out with a new financing tool this week. The Texas-based company is introducing a reducing interest rate line of credit for BHPH dealers and small-to-mid-size finance companies to offer their sub-prime borrowers more vehicle financing options.

With the new reducing rate line of credit, the interest rate decreases over time. The loans also come with other advantages not typically found with traditional financing options, including no personal guaranty or recourse, flexibility to draw cash as needed, and no origination or unused line fees.

“With AgoraCapital, we remove the obstacles dealers confront in traditional lines of credit and empower them with the same secret sauce enjoyed by larger national dealer groups,” said Agora Data CEO Steve Burke. “Agora’s innovative, best-in-class financing options and robust data analytics are leveling the playing field for an underserved and underbanked industry.”

Agora Data was founded in 2017 and its team of auto retail, finance industry experts, and top data scientists leverage AI to bring BHPH car dealers a simplified experience when it comes to selling auto loans. Agora Data aids dealers in selling their auto loans to banks, finance companies, hedge funds, and private equity firms. The selling tool groups all firms’ offers together and analyzes each one in order to provide the dealer with the most competitive offer.

In addition to the selling service, the company offers AgoraInsights, a product that helps dealers maximize portfolio performance, reduce risk, and manage cashflow. “Agora is already making a positive difference for the BHPH industry by helping our members strengthen their financial footing and realize unprecedented growth, knowledge, ability to compete and ultimately build wealth,” added Burke.

News about auto financing has consistently appeared in the fintech headlines since the beginning of the COVID pandemic. However, while Agora Data’s announcement is aimed at auto financing for the underbanked community, most of the news we’ve seen in this sector has focused on digitizing and managing the loan application portion of auto loans and refinances. One such company, MotoRefi, partnered with SoFi in April of this year and received $45 million in funding in May.

The modern world has witnessed three major economies. First, there was the industrial economy in which people earned money through physical activity. Then came the consumer economy in which people made money performing services. Next, the knowledge economy enabled people to earn money through leveraging intellectual capital and insight.

In these past few years, we’ve been witnessing the birth of the creator economy, a new economy fueled by social media platforms and video sharing. This new working order democratizes the ability for anyone to become a celebrity. Here’s a look at four key facts of this new economy.

Who

While many consider the creator economy to be limited to YouTubers and Instagram influencers, it actually has a wider breadth. In essence, everyone with an online presence is a creator, since we are all making content and sharing it online in some form.

A more exclusive definition of a creator is anyone who monetizes content online. This represents not just social media influencers, but also includes those who create and sell NFTs, ebooks, podcasts, digital art, etc.

Because there are such low barriers to entry in the creator economy, even kids can do it. In fact, one of the most famous YouTube creators is Ryan, an 11-year-old with 30.9 million subscribers who posts videos of himself playing with toys. Ryan is reportedly worth $32 million.

The participation of kids in the creator economy is influencing how younger generations view their future. According to a recent study, one third of kids between ages eight and 12 want to be either a YouTubber or Vlogger when they grow up.

Size

The current size of the creator economy is over $100 billion and growing. YouTube alone expects a $30 billion stream of revenue by the end of 2021. Of the 50 million people that consider themselves a creator, around two million of these are professionals making six-figure salaries.

Where’s the money?

Just like other economies, one of the ways that creators are recognized for their contributions is by getting paid. While this payment used to come from ads, branded content, or sponsorships, today’s monetization looks different. That’s because, instead of relying on third party sponsorships and brands to receive payments, creators now receive payments via subscriptions, tips, and even by payments directly from the user.

One of the latest examples of this is TikTok, which recently introduced the concept of in-app tipping. Users with more than 100,000 followers can apply to begin receiving tips from their fan base. When they receive a tip, 100% of the compensation goes to the creator; TikTok doesn’t take a commission.

Creators aren’t just getting paid in dollars. Owners and creators of non-fungible tokens (NFTs) receive payment in cryptocurrencies in exchange for their work. For more on how NFT compensation works, check out our piece 7 Things to Know about the NFT Craze.

How to leverage the opportunity?

The most important part about the creator economy for banks and fintechs is knowing how to leverage the opportunity. The future of this economy is unlike any we’ve ever seen in that payment and monetization may not rely on traditional banking infrastructure. In fact, many participants’ future revenue will be decentralized.

What we know for sure, however, is that personalization and customer experience matter and will continue to reign, even when payments are thrown off the rails. Many digital banks are already capitalizing on this opportunity. Just take a look at Nerve, a bank for musicians; Karat Financial, a bank for digital creators; and Willa, an invoicing tool for creators.

These financial services firms are different from banks in that they understand the unique challenges that come with being a creator. For example, creators experience many of the same difficulties as the self-employed, such as difficulty qualifying for a loan. They also often times have lumpy cashflow and need help with budgeting and financial planning.

There is still time for traditional banks to come up to speed in the creator economy. The key to serving this unique customer base will be to expand your existing resources for self-employed customers by offering new services such as revenue-based financing and on-demand wage access. As with most things in today’s digital banking era, the only way to properly serve this new user base will be through partnerships.

MoneyLion made a move today that will help it catch the eye of prospective customers and retain its existing ones. The digital bank acquired MALKA, a creator network and content platform, to help it better engage with consumers and connect with communities.

MALKA was founded in 2012 and works with creators to develop content across digital mediums including advertising campaigns, original branded content, e-gaming livestreams, podcast series, feature length documentaries, sports representation, and marketing. One of MALKA’s differentiating factors is that it maintains a talent base of 170 employees in-house in order to maintain relationships instead of working with different freelancers on different projects.

MALKA will help MoneyLion, which already offers MoneyLife content, in its mission to become a daily destination by bringing evergreen content to educate, inform, and support customers’ financial decisions. Ultimately, integrating MALKA’s content into MoneyLion will support the digital bank’s marketing and brand-building efforts.

“Through this acquisition, which we anticipate will be accretive and cash flow positive in 2022,” said MoneyLion Co-Founder and CEO Dee Choubey, “we will now be able to fully leverage MALKA’s capabilities so that the MoneyLion brand can truly live wherever our customers are investing their attention.” CMO Bill Davaris added, “This fundamental shift will allow us to own and not rent the relationships we are cultivating with new and existing MoneyLion customers.”

At face value, a tie-up between a digital bank and a content creation company seems a bit odd. The acquisition, however, can be seen as MoneyLion simply buying its own creative marketing and content department. No matter how you look at it, the acquisition is a hat tip to the new creator economy and speaks to how content-driven today’s consumers are.

MALKA will operate independently from MoneyLion and the company’s Founder and CEO Louis Krubich and Co-Founder and President Jeff Frommer will continue to lead daily operations. “This partnership will allow us to exponentially grow our creator network and engage with millions of more fans,” said Krubich.

MoneyLion launched in 2013 and offers a full-service platform that delivers mobile banking, lending, and investment solutions. Earlier this year the company teamed up with Zero Hash to launch the ability for users to buy, sell, and hold cryptocurrencies. The company went public on the New York Stock Exchange in September via a SPAC merger with Fusion Acquisition Corporation.

Analytics and decision management technology company FICOlaunched a loan origination tool called FICO Originations Solution that automates the entire customer journey leveraging the FICO platform.

The cloud-based tool leverages FICO’s enterprise intelligence network to streamline and personalize loan originations. The new tool helps financial services providers do two key things. First, it helps remove friction from the customer experience. Second, it empowers loan originators by helping them make more precise origination decisions and better manage risk, ultimately helping them grow more profitable portfolios.

This enhanced decision-making is thanks in part to FICO’s data library that offers lenders access to 130+ global data sources. The ever-increasing data source helps firms make faster and better customer decisions.

The FICO Originations Solution starts with a completely digital onboarding experience. The tool considers an organization’s goals, including the types of borrowers they want to attract, their ideal conversion rate, and profitability goals. FICO offers simulation capabilities to test the user experience to determine if decreased friction results in increased fraud or if changing an application question increases the conversion rate.

FICO Originations Solutions’ customers have access to FICO’s suite of tools that includes interactive messages, fraud prevention capabilities, and pricing optimization.

“Financial services providers today need data-hungry, analytics-ready, agile, extensible systems in order to compete in a digital-first economy,” said FICO VP and Head of Product Management Tim Van Tassel. “FICO Originations Solution, Powered by FICO Platform provides the digital and analytic sophistication that enables financial institutions to offer the safety, convenience, and personalization that customers look for during the account opening process through their chosen channel, while closely managing customer-level risk.”

FICO was founded in 1956 and is headquartered in California. The company is best known for the consumer FICO score that is calculated based on information in credit reports maintained by Experian, Equifax, and TransUnion. The company also offers fraud and compliance as well as debt collection and recovery solutions.

Alternative credit provider and digital bank Upgradeannounced a $280 million investment this week. The Series F round brings the company’s total funding to $600 million and boosts its valuation to $6 billion, which is almost double its last valuation of $3.3 billion in August.

The round was led by Coatue Management and DST Global with participation from Dragoneer Investment Group, Gopher Asset Management, G-Squared, Koch Disruptive Technologies, Old Well Partners, Ribbit Capital, Sands Capital, Ventura Capital, and Vy Capital.

Upgrade was founded in 2016 and offers a variety of low-cost personal loans and credit cards that come with rewards ranging from Bitcoin cashback to 3% cashback. Earlier this year the company debuted a checking account with a debit card that pays 2% cashback for common expenses.

The company differentiates its card, which is issued by Sutton Bank, from traditional credit cards by combining monthly charges into installment plans that the borrower repays over 24 to 60 months. Upgrade structures the repayment this way to get its users into the habit of paying down their balance every month and avoid getting trapped in a continuous cycle of debt.

The funding news comes four months after Upgrade closed its $105 million Series E round. Company CEO Renaud Laplanche said that the round “demonstrates Upgrade’s rapid growth and commitment to delivering innovative financial products that benefit consumers.”

The “rapid growth” Laplanche references has been seen in recent acclamations. Earlier this year the Financial Times selected Upgrade as the fastest growing company in the Americas and the Nilson Report recognized the Upgrade Card as the fastest growing credit card in America, placing Upgrade among the top 50 U.S. credit card issuers.

Since launching its credit card in 2017, Upgrade has delivered $10 billion in total credit to customers via the company’s credit cards and loan products. The majority of this credit has been issued this year alone; the company is on track to deliver $8 billion in credit in 2021.

Upgrade is headquartered in California with an operations center in Arizona and a technology center in Canada. The company is partnered with Cross River Bank and Blue Ridge Bank for credit lines and banking services, NYDIG for Bitcoin rewards, and Sutton Bank for card issuance.

Can we stop naming AI as a trend in fintech? Probably not yet, but we should. That’s because trends ebb and flow, but AI isn’t going anywhere. Banks and fintechs aren’t going to let up on leveraging AI within the decade. In fact, the number of times we’ve seen the adjective “AI-powered” has only increased.

Depending on how you define it, fintech has been in existence for around 20 years. That’s a long time for themes to rise and fall. Below is a look at transitory trends, lasting trends, and AI’s place in the mix.

Fleeting trends

As regulation, technology, and consumer habits and tastes have changed throughout the years, so have fintech trends. However, many ideas in fintech never took off. While some were overhyped, others were simply a solution looking for a problem or were an idea before their time, offered to the market too soon.

A recent example of a transitory trend is card-linked offers (CLO) Also called merchant-funded rewards, these customer loyalty and rewards tools reached their peak in 2012. Similar to the buy now, pay later craze that is happening right now, there were multiple launches of new CLO companies each month. Even large banks were getting on board. In fact, in 2012 Bank of America debuted a CLO product, BankAmeriDeals, powered by Cardlytics.

It’s worth noting that card-linked offers are still around. It is only the growth rate and hype around CLOs that have decreased. In fact, Cardlytics, Cartera Commerce, Cachet Financial Solutions, and others still exist and serve customers today.

Lasting trends

The list of lasting trends in fintech is short. In fact, there are only a handful of trends that have been introduced over the last two decades that have become table stakes for every bank and fintech across all sub-sectors. Not surprisingly, because these lasting trends are now standard throughout the industry, they all seem quite obvious.

Three solid examples of these stronghold trends include having a digital presence, providing a mobile app, and offering digital payment/money transfer capabilities. The evolution began, at the dawn of fintech, with banks just starting to establish their online presence. The next adaptation of that was SMS banking, which evolved into to mobile apps and digital money movement.

Today, the application of AI is becoming so standard across the fintech industry that it can be added to the fintech trend hall of fame.

The current state of AI

In case you haven’t been paying attention, AI is being used across the entire fintech industry. Its applications are almost limitless, but here are a handful of current examples.

Lending– Underwriters can use AI to enhance the decisioning process to reduce risk, as well as to monitor for unseen biases in the lending process.

Payments– AI can enable biometrics-activated payments and can also create smooth payment processes by analyzing past transactions before approving or declining transactions on an issuer’s behalf.

Wealth management– Wealthtech companies can empower users with self-driving money, a concept that describes moving funds into and out of different accounts and investments based on fund performance, cash flow, and bill due dates.

Insurtech– AI can enhance predictive data modeling to create better pricing models around policies.

Security– Fraud detection in financial activity relies heavily on AI, as do both identity detection and verification.

Funding for AI fintechs has been on the rise since 2016. According to CB Insights, the total amount of funding in 2021 for AI startups in fintech is at the same level as last year’s year-end total, with $3.1 billion raised across 161 deals. This year, the average investment size clocked in at $25 million. There has also been an increase in M&A activity for fintech AI startups. So far this year there have been 12 mergers and acquisitions in the space, compared to eight last year and two in 2016.

Float, a Canada-based startup that offers a corporate card and spend management solution, landed $30 million (C$37 million) in funding this week. The Series A round was led by Tiger Global and brings the company’s total funding to $34 million (C$42 million).

The funding will help Float with its mission to deliver an end-to-end spend management platform for SMBs. “We want this platform to enable businesses and teams to focus on investing in their growth and eliminate the need to use different banking and software tools to make day-to-day payments… Float’s mission is to simplify spending for companies and teams,” the company explained in a blog post.

Float was founded in 2019 to offer Canadian SMBs a high-limit, no personal guarantee corporate card that is available in three business days or less. This turnaround is impressive when compared to the average four+ week wait time most businesses face to receive their corporate spending cards. Businesses can set custom spending limits, assign cards to employees, and review and approve transactions in real time.

In addition to the card capabilities, Float also offers spend management software that natively integrates with accounting software such as QuickBooks and Xero. The dashboard helps employers track real-time spending and provides an overview of individual, departmental, and categorical spending.

The investment comes at a good time for Float, which has seen significant growth since launching to the public in March of this year. The company now has hundreds of small business clients and continues to experience increased engagement. Float’s total payment volume has increased ~20x since June and its average monthly customer spend has increased more than 6x since March.

Float offers a freemium pricing model with varying features. All tiers come with 1% cashback, 0% FX fees, unlimited users, automatic top-ups, and a $100,000 spending limit. The paid tiers provide custom integrations, team management, and more.

Mexico-based Storilanded $200 million this week in combined debt and equity. The investment, which bring the company’s total funding to almost $250 million, will help the fintech provide financial services to its region’s underserved customers.

The $125 million in equity was co-led by GGV Capital and GIC with contributions from General Catalyst, Goodwater Capital, Tresalia Capital, Lightspeed Venture Partners, Vision Plus Capital, BAI Capital, and Source Code Capital. The $75 million in debt financing comes from Community Investment Management.

The investment echoes Stori’s success in the region. The company has become one of Mexico’s top issuer of new credit cards since February of this year. In fact, more than 2 million Mexicans have applied for a Stori credit card, and that number has grown by more than 10 times in the last twelve months.

And there is still plenty of room for growth. The broader Latin American region has 400 million underserved consumers. “Our mission – empowering financial inclusion for millions of hard-working people – is amazingly meaningful and challenging at the same time,” said Stori CEO and co-founder, Bin Chen. “We are progressing at an unprecedented pace by combining technology, machine learning, data-driven underwriting and an intuitive mobile-based user experience. A lot more will come in our journey to become a top consumer financial franchise in Latin America.”

Stori plans to use today’s funds to triple in size and broaden its product offerings to better suit customer needs, ultimately providing much-needed financial services to Mexico’s underserved citizens. The fresh capital will also help Stori grow its team and double down on training and development opportunities.

While Stori is focused on the Mexico region, the company boasts a global team with offices in Washington D.C., Mexico, and Asia. “Our success since launch is a direct result of having a team who is passionate about our mission to empower upward financial mobility for the underserved population,” said company Co-founder Marlene Garayzar.

Wealthtech company Atomicannounced its company launch along with a $25 million in a Series A funding round today. The round, which was co-led by QED Investors and Anthemis with participation from Softbank and Y Combinator, will help fuel the company’s investing API that allows fintechs and banks to integrate investing into their existing products.

With Atomic’s API, companies can launch investing experiences such as direct indexing, ESG investing, and multi-currency trading across 60 global markets with no account minimums. The “investing-as-a-service” nature of the new offering means that companies can launch investing tools in a matter of weeks without relying on in-house experiences. In fact, Atomic takes care of not only the investing experience, but also the details around regulations, brokerage operations, and compliance.

“What we see is that fintechs and other consumer-facing companies want to offer savings and investment, but most have come to market with very limited product offerings — only single stock trading or only ETF investing,” said QED Investors Partner Amias Gerety. “Atomic provides cutting edge solutions so that their partners can offer both of these products easily, but also offer advanced features like ESG, direct indexing, and tax loss harvesting that are usually only available for accounts with hundreds of thousands of dollars in them.”

Atomic helps companies retain customers by broadening their existing offerings to include investing– a financial tool that generally creates long-term customer loyalty. “Any fintech or bank that wants to become their end-customers’ primary financial relationship will need to offer investing on their platform to remain competitive,” said Atomic CEO David Dindi. “As an accelerant in the rapidly evolving ecosystem of unbundled financial services, Atomic enables these businesses to offer investing in a frictionless way as a means to deepen their relationships with customers.”

Among Atomic’s client base are fintechs such as Upside, a student loan innovator. Upside is leveraging Atomic’s API to build a wealth management offering that allows its users to refinance their student loans and reinvest the savings.

Dindi, along with the company’s CTO Marco Alban are both Stanford graduates and serial entrepreneurs.

Veterans Day in the U.S. is a day to remember and honor the sacrifices our military veterans have made to preserve the freedom we enjoy on a daily basis. How can banks and fintechs give back by connecting and serving this niche clientele in return?

We interviewed Dennis Cail, co-founder and CEO of Zirtue, who shared his experience as a U.S. Navy veteran-turned-fintech entrepreneur. Cail told us how his military experience impacts his work at Zirtue and what banks and fintechs can do to give back.

Tell us the basic idea of Zirtue.

Dennis Cail: Zirtue is the world’s first relationship-based lending application, simplifying loans between friends, family, and trusted relationships by turning informal promises into structured agreements and automating the repayment process. Zirtue’s mission is to drive financial inclusion and freedom, one relationship at a time.

Headquartered in Dallas, Texas, Zirtue sits at the nexus between two major pain points: a person needing a financial lifeline to pay their bills and a company struggling with bad debt. Corporate partners use Zirtue as an alternative payment solution, allowing individuals with past-due accounts to request loans from friends or family members in order to pay their bills. Zirtue has raised $6 million of VC funding and more than $10 million in loans have been processed on the platform to help users keep their lights on, pay their rent, and get access to critical healthcare.

How did you come up with the idea of Zirtue? What was the impetus?

Cail: Growing up in Louisiana, I lived in public housing and neighborhoods often surrounded by payday lenders and check cashing services; the same was true of the areas surrounding the naval bases I lived on. It wasn’t until college when I saw how different communities attract different types of neighborhood businesses such as banks, and that many neighborhoods didn’t have traditional banks.

Looking back, I saw how clearly and deliberately predatory lenders target those with few financial options and no access to traditional banking services, like my neighborhoods in Monroe and the Navy. These experiences led me to creating a loan option for these unbanked and underbanked folks that provided them with necessary loans and empowered them through the process. We all need a little help sometimes, and that is what Zirtue is all about. I also have experienced the challenges of loaning friends and family money myself. Even though I wanted to help my loved ones out, it made things awkward. I saw the impact that these friendly loans could have on my loved ones in terms of helping them achieve their dreams or simply make ends meet, without having to pay the high fees of predatory payday lenders who are the only available option for many.

As someone who has always wanted to found a company and had a background in finance, I knew I could create a solution for this problem that formalized these friendly loans, while simultaneously driving financial inclusion. Ultimately, this solution became Zirtue, and we’ve now processed more than $10 million in loans to-date and plan to continue until Zirtue is a payment option at every retailer you visit in-person and online.

You are one of a handful of military veteran fintech founders. First off, thank you for your service. Can you tell us about your military experience?

Cail: As a Systems Engineer in the US Navy working with hardware and software to ensure we had ship-to-ship and ship-to-shore communications, my military experience gave me the technical foundation I needed to start a successful career in technology. The military is also a place that either makes or breaks you. At the very least it reveals who you are at your core and I learned a lot about myself during my military experience.

Funny, but true story… I didn’t know how to swim when I joined the Navy and when I shared this information with my civilian friends after I left the Navy, they would naturally ask me, “why did you join the Navy if you couldn’t swim?!” The answer is that I joined the Navy to learn how to swim and to serve my country. This may sound a bit extreme. However, entrepreneurs have to be extreme on some level if they are going to achieve what most people would consider impossible or too risky. Long before I became an entrepreneur and a fintech founder, I had the spirit of an entrepreneur with a high tolerance for calculated risk. My military experience only amplified that entrepreneurial spirit.

How does your military experience impact your work at Zirtue?

Cail: The military has absolutely influenced my career and led me to found Zirtue. First of all, the military taught me how to be a strong leader and how to navigate stressful situations – which are both imperative to founding a company and handling the complexities of entrepreneurship. Further, the military taught me to always look out for your partner, or in my case shipmate, and that we either win together or lose together. This concept has shaped the way I interact with my team, our customers, partners, and other entrepreneurs – we have to take care of each other.

Finally, being in the military taught me about the importance of structured, detailed plans, which has helped me integrate further structure into entrepreneurship and supported business growth for Zirtue. Looking back, I am incredibly thankful for my military experience for shaping me into the man I am today and forming a solid foundation as an entrepreneur and CEO.

What advice do you have for banks and fintechs looking to connect with and serve military veterans as clients?

Cail: It’s extremely important that banks and fintechs alike do all they can to help military veterans transition back into civilian life so that we can put them in the best possible position to be successful with skills that are highly transferable. Given the sacrifices made by these men and women, my advice is simply to be intentional about their DEI efforts to connect with military veterans with formal programs that include military veterans.

At Zirtue we actively recruit from this amazing source of talent and encourage military veterans to apply for any open jobs we may have. I would also like to call out that banks like USAA and Navy Federal Credit Union are very active in their efforts to support veterans and their families with financial products and customized lending options. Their efforts should be applauded and replicated.