This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

A look at the companies demoing at FinovateEurope on March 22 and 23, 2022 in London. Register today and save your spot.

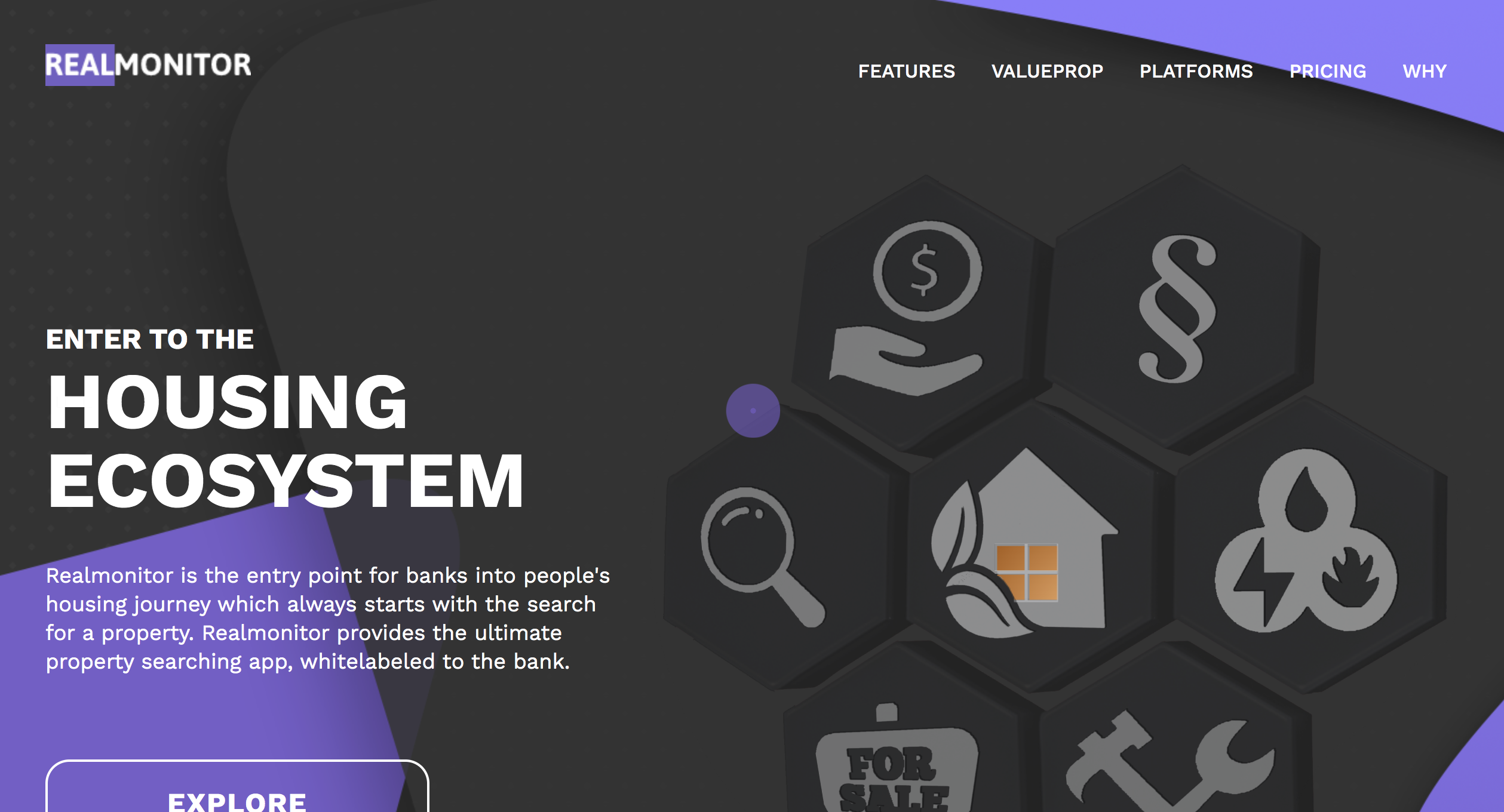

Realmonitor reduces customer acquisition cost for mortgages and significantly lowers the bank’s exposure to the agent network by providing super early customer engagement.

Features

Significantly reduce customer acquisition cost

Provide early customer engagement and super sharp customer profiling

Reduce bank’s exposure to agent networks

Presenter

Peter Farago, CEO and Co-founder Farago has spent the last 15+ years in the bank and real estate industry covering several stages of the housing ecosystem. LinkedIn

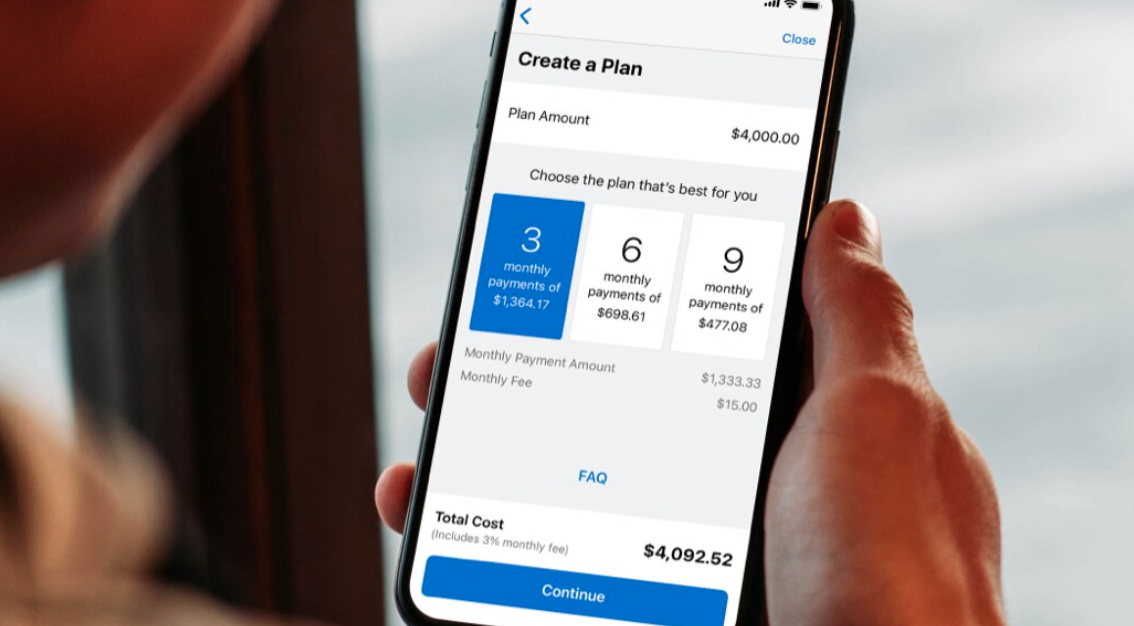

American Express partnered with Delta Air Lines to offer American Express’ buy now, pay later tool, Plan It, as a payment option at checkout.

Plan It allows users to select from one to three repayment options and charges a fixed monthly fee.

Plan It will be added as a checkout option on Delta’s mobile app this spring.

American Express and Delta Air Linespartnered this week to offer their shared customers a buy now, pay later (BNPL) option when booking flights on Delta.com’s web interface.

The partnership, which leverages American Express’ Plan It tool, enables American Express U.S. consumer card members to split up purchases of over $100 into equal monthly installments with a fixed fee.

Launched in 2017, Plan It allows customers to select from one to three repayment options, depending on factors such as the purchase amount, the cardholder’s account history, and their creditworthiness. Plan It charges a fixed monthly fee that is disclosed before the transaction.

As an added advantage over other BNPL plans, Plan It is built into the American Express card and does not require users to enroll, plus cardholders earn rewards as they usually do with their card payment. Further, cardholders do not need to keep track of additional payments, since they are included in their monthly statement.

As Anthony Cirri, Executive Vice President for Global Consumer Lending and Cobrand at American Express highlighted, the timing of the partnership is ideal. “It’s the perfect time to bring these together as people are booking long-awaited trips, and our card members can book with confidence knowing they are backed by the strong partnership between Delta and American Express.”

Plan It has benefited from the rising popularity of BNPL and alternative payment options. The volume of new plans originated in the fourth quarter of 2021 was more than double the volume in the fourth quarter of 2020. And 65% of plans originated in the last year were from new users.

Travelers will see Plan It as a checkout option on Delta’s mobile app this spring.

Clients that use U.S. Bank’s prepaid Focus Card for payroll can offer their employees access to their wages as they earn them, thanks to a new partnership between U.S. Bank and Payactiv.

Employees will not only benefit from early access to their wages, but will also have access to Payactiv’s other financial wellness tools.

“We’re proud to be on the leading edge, developing a solution that helps our business clients provide additional convenient options for their employee payroll,” said U.S. Bank Payment Services Vice Chair Shailesh Kotwal.

U.S. Bank is partnering with financial wellness company Payactiv this week. Under the agreement, U.S. Bank will leverage Payactiv’s earned wage access (EWA) tools.

U.S. Bank’s commercial clients that use U.S. Bank’s prepaid Focus Card for payroll can enable their employees to access a portion of the wages they’ve already earned. Employees can access their funds on their U.S. Bank Focus Card, via an instant deposit into their checking account, or other payment options.

In addition to benefitting from early payouts, employees will have access to other financial wellness services such as savings and bill management tools, financial education, and a discounts marketplace.

“The future of payments is one where companies may soon say goodbye to the traditional, biweekly payroll,” said U.S. Bank Payment Services Vice Chair Shailesh Kotwal. “Employers recognize that providing employees on-demand access to earned wages improves employee satisfaction and recruiting efforts. We’re proud to be on the leading edge, developing a solution that helps our business clients provide additional convenient options for their employee payroll.”

Payactiv was founded in 2011 to help companies send their employees their wages as they earn them, as opposed to bi-weekly. “We provide timely access to liquidity – so a single mother can pay for daycare between paychecks and a healthcare worker can cover an unexpected car expense,” explained company CEO Safwan Shah.

California-based Payactiv has raised $134 million in funding and earned a Best of Show award for its 2016 demo. In 2020, the Consumer Financial Protection Bureau (CFPB) approved Payactiv’s EWA program as exempt from the federal Truth in Lending Act and Regulation Z rules governing creditors. “Employers can take comfort in knowing that PayActiv continues to be the leader in responsible EWA for employees,” Shah said at the time.

When your day job keeps you busy for 40+ hours per week, it’s hard to take on new tasks or pay attention to new initiatives. But one thing 2020 taught us is that the digital initiative doesn’t take vacation days. So when enabling technologies and platforms like the metaverse come around, banks and fintechs need to pay attention.

First, let’s look at what the metaverse is and what it is not. You can think of the metaverse as immersive, collaborative internet. In some respects, the metaverse is already here. Users are already collaborating with each other on multiple platforms, and alternate realities– whether in 2D or 3D– have been around for decades. However, though the metaverse will be accessible via virtual reality, it is not the same as virtual reality.

The metaverse is at an early stage and is still not well defined. Despite this, banks and fintechs still need to be paying attention. Here’s why.

It’s not the first time fintech has tried to embrace a different reality

In 2014, many fintechs and even some established financial services companies launched mixed reality experiences in the form of Google Glass, which was released to the public in May of 2014. Top Image Systems (now Kofax), Fiserv, eBankIT, and Wallaby Financial (now Bankrate) all released tools for Google Glass in 2014.

Most are familiar with the fate of Google’s mixed reality glasses– they were discontinued in 2015. The failure of Google Glass is not the point, however. What matters is the speed at which this group developed around the new technology. We can expect the same for the metaverse.

You’re already behind

It’s easy to sleep on trends that seem like they are nothing but hype. Despite that, if you’ve been sleeping on this trend, you’re already behind. JP Morgan announced yesterday that it has joined the metaverse by opening a virtual lounge. Located in Decentraland, JP Morgan’s Onyx Lounge shows a timeline of the bank’s blockchain innovations, has three videos to watch, and has a tiger walking around.

The bank also released a white paper on opportunities in the metaverse. “There is a lot of client interest to learn more about the metaverse,” JPMorgan’s Head of Crypto and the Metaverse Christine Moy told Coindesk. “We put together our white paper to help clients cut through the noise and highlight what the current reality is, and what needs to be built next in technology, commercial infrastructure, privacy/identity and workforce, in order to maximize the full potential of our lives in the metaverse.”

In five years, you’ll wish you had paid attention

If there’s nothing to the metaverse right now, why bother paying attention? Because five years from now you’ll wish you had been paying attention.

While it’s easy to say that about any risk-laden investment such as real estate or tech stocks, you can consider the example of cryptocurrency. What if your organization had been investing in crypto research five years ago? You may have already been leveraging the benefits of stablecoins or smart contracts. The metaverse is just one more way to invest in the future of your organization.

Metaconomy

One very attractive aspect of the metaverse is that it is intertwined with the blockchain. In the metaverse, digital assets will be exchanged for digital currencies in a new economy. There is even speculation that work will take place in the metaverse. According to JP Morgan, $54 billion is spent on virtual goods each year and NFTs have a current market capitalization of $41 billion. Banks won’t want to be left out of this new metaconomy.

It’s where you’ll find your next clients

Generation Z* and Generation Alpha** are not only digital natives, many of them are mixed reality natives. They’ve grown up with virtual reality headsets and spend hours a day in parallel universes such as Fortnite. To capture the attention of this group, there is no doubt that financial services companies will need to meet these young clients where they are.

If JP Morgan’s bet on Decentraland is any indication, banks and fintechs should start planning their first move in the metaverse. However, as Cornerstone Advisors’ Alex Johnson recently pointed out, they may want to hold off on building their first bank branch in the metaverse.

Revolut has acquired India-based Arvog Forex. Terms of the deal were not disclosed.

The purchase will help Revolut launch services in India in the latter half of this year.

Arvog Forex has more than 20 branches across India and served more than 15,000 customers last year.

Global financial services innovator Revolut recently acquired Arvog Forex to deepen its roots into India, a region with a population of 1.3 billion and ripe for fintech disruption.

Arvog Forex, an international money transfer and currency exchange company, is headquartered in Mumbai. With more than 20 branches across India, the company served over 15,000 people with its remittances and other forex services last year.

Revolut, which plans to invest $25 million into the Indian market in the coming years, expects the purchase will strengthen its foundation in India. The company initiated its India expansion plans last April after hiring Paroma Chatterjee, a former Flipkart executive, to lead its India operations. Under Chatterjee’s leadership, Revolut plans to launch bespoke financial products that serve the unique needs of Indian consumers.

The company is aiming to launch services in India in the latter half of this year. The Arvog Forex acquisition should streamline this, helping Revolut offer remittances and multi-currency accounts to Indian customers.

Chatterjee calls the buy a “first step” towards the company’s aspiration to usher in a “digital financial revolution” in India. “Our significant investment plans, this acquisition, and the quality of the team we are putting together reflect our intention to rapidly roll out these innovative products and services. India is a key region in our global expansion plan and this acquisition is testament to the rapid strides we want to make here. It is an incredible time to be a fintech company in India and we plan to make the best of this opportunity,” she said.

U.K.-based Revolut was founded in 2015 and has already expanded into other Asia-based countries, including Japan and Singapore, but has yet to enter into China, a market that will prove to be highly competitive. On the other side of the globe in North America, Revolut has applied for a bank charter in the U.S., but withdrew its operations in Canada last March. The fintech plans to reenter the region later this year.

Madison Dearborn Partners has agreed to acquire MoneyGram in a $1.8 billion deal.

The deal will offer shareholders $11 per share and will make MoneyGram a privately-held company.

MoneyGram anticipates the acquisition will help it advance digital growth and compete against smaller fintechs.

MoneyGram, an 82-year-old fintech, announced today it has agreed to be acquired by private equity investment firm Madison Dearborn Partners (MDP) in a $1.8 billion deal. The transaction is expected to close in the fourth quarter of this year.

When the deal closes, MoneyGram shareholders will receive $11 per share. In addition, MoneyGram, which is currently listed publicly on the NASDAQ under the ticker MGI, will no longer be listed on a public exchange. Logistically, MoneyGram will continue to operate under its own brand. Company CEO Alex Holmes and the existing leadership team will continue to lead MoneyGram from the company’s headquarters in Dallas, Texas to continue to serve its 150 million customers.

Holmes anticipates the deal will not only deliver value to shareholders, but will also help MoneyGram as it seeks to advance its digital growth. “MoneyGram has undergone a rapid transformation over the last several years to expand our digital capabilities and adapt to the evolving needs of our customers. By partnering with MDP and becoming a private company, we will have greater opportunities to innovate and transform MoneyGram to lead the industry in cross-border payment technology and deliver a more expansive set of digital offerings, while leveraging our global platform for new customers and use cases.”

The move will place MoneyGram in a better position to compete with the onslaught of fintechs in the cross-border payments arena. And in today’s increasingly decentralized economy, this competition goes beyond cross-border payments companies of the last decade such as Azimo, Wise, Visa’sCurrencyCloud, and Payoneer. Looking ahead, MoneyGram will need to deepen its crypto roots.

The Dallas-based company dipped its toe in the crypto waters in 2018 when it initiated a partnership with Ripple to leverage xRapid for remittance payments. And last fall, MoneyGram began collaborating with Stellar to enable consumers using Circle’s USDC stablecoin to receive cash funding and payout in local currency.

“We are looking forward to applying our substantial experience growing digital businesses and deep payments knowledge to help MoneyGram further strengthen its market-leading cross-border capabilities and enhance its digital platform,” said MDP’s Managing Director Vahe Dombalagian.

IRA company Alto Solutions is partnering with P2P marketplace Prosper.

Under the agreement, Alto’s clients can now invest IRA funds in Prosper’s consumer loans.

Prosper has facilitated more than $20 billion in P2P loans to nearly 1.2 million people across America.

Peer-to-peer (P2P) investment marketplace Prosper may likely see a new slough of investors in the coming months. That’s because the California-based company just inked a partnership with self-directed IRA platform Alto Solutions.

Alto users can now invest their IRA funds in loans originated through Prosper’s online marketplace lending platform. Prosper’s alternative investment platform connects people who want to borrow money with individuals and institutions that want to invest in consumer credit. As a result, borrowers are able to secure credit outside of a traditional financial institution and investors can gain diversification along with attractive returns.

“We are extremely proud to partner with Prosper,” said Alto Chief Revenue Officer Tara Fung. “Prosper was the first peer-to-peer consumer lending marketplace in the U.S. and has given everyday Americans a first-of-its-kind investment opportunity to better diversify their portfolios. Thanks to our partnership, Alto investors can now deploy IRA funds to invest in consumer loans.”

Prosper was founded in 2006 and has since facilitated more than $20 billion in P2P loans to nearly 1.2 million people across America. In 2019, the company launched a HELOC tool that BBVA integrated into its website.

Tennessee-based Alto was founded in 2018. The company helps users access alternative investments such as real estate, crypto, startups, and more. Alto’s current investment partners include AngelList, DiversyFund, Eaglebrook Advisors, Fundr, Grayscale, Masterworks, Republic, Vint, and others.

Passwords are as frustrating as they are essential, especially in financial services. We chatted with LastPass VP of Product Management DanDeMichele to get an idea of how banks and fintechs can protect themselves, what the future of passwords looks like, and how digital identity is dictating changes.

In his role at LastPass, a password manager that offers secure password storage for millions of users, DeMichele is responsible for leading LastPass’ overall product and strategy teams. We caught up with him to get some insight on the intersection of banking, cybersecurity, passwords, and digital identity.

How are cyber threats impacting the banking industry? Is the situation improving or worsening?

Dan DeMichele: Cyber threats are decisively impacting the banking industry as attackers are constantly eyeing sensitive information. It’s a heavily targeted industry given the volume of highly sensitive data being produced and stored within it and the insider vulnerabilities that plague it. Made worse by the growing population accessing banking networks, the industry is seeing an increase in touchpoints that give hackers more opportunities to attack.

Knowing attacks have been made easier by the digitization of the sector, which was fast-tracked by the pandemic, it’s clear the situation is worsening. A recent LastPass report revealed that while 68% of individuals would create stronger passwords for financial accounts, 8% believe a password shouldn’t have ties to personal information. This means most users are creating passwords with ties to potentially public details, making it easier for hackers to access their information. To take it a step further, these credentials are being leaked on other websites through which bad actors then attempt credential stuffing, particularly into financial networks.

What are easy steps banks can take to mitigate these threats?

DeMichele: It’s critical that private banks, wealth managers, and clients themselves protect online banking sign-on and practice proper password hygiene to minimize attacks that are on the rise. The industry can work to combat threats in a number of ways, including requiring multi-factor authentication (MFA) during the login process, setting up dark web monitoring alerts, addressing general password hygiene needs and implementing password management tools, installing solutions such as anti-phishing web browsing software, and implementing policies for location and devices staff can log in from and the type of access allowed.

Beyond these basic protection measures, what should banks do to fully protect themselves?

DeMichele: The private banking and finance sectors need to focus on how they store and share sensitive data and information. By identifying weak spots and knowing how to reduce risks, banks can make attacks more difficult to accomplish and essentially less attractive to potential hackers in the first place. Cybersecurity also needs to be a concern beyond the IT department. Staff with network access need to be properly informed and trained in their role in keeping the organization secure against attacks. Organizations should also weigh the option of implementing automated solutions. With the rise of the digitization of the sector, tools that automate cybersecurity and compliance are now available to help mitigate risk.

Do you envision we’ll ever see a world without passwords as we know them today? What would that look like?

DeMichele: Over the next year, I anticipate a simplification of the tool set for administrators and the end user experience that enables efficient password hygiene. Today’s password solutions were built for the more tech-savvy crowd, but looking ahead, password management will become more intuitive for end users. In addition, within the next five years or so, VPNs will likely be obsolete and replaced by zero trust. It offers a different perspective on how devices are connecting to networks, which is critical as organizations remain remote or shift to a hybrid workforce. There will likely be one vendor that comes to market and makes it simple to implement, which is when every company will look to adopt it. I also see passwordless authentication with strong security standards such as FIDO 2.0 being adopted and triggering a slow phasing out of traditional passwords. It will be a long journey to get to that point, and password management solutions that are tackling both challenges will help users keep secure profiles.

What role does digital identity play in all of this?

DeMichele: We’re in the midst of a revolution of how individuals interact online as a result of digital identities. Unfortunately, the more we digitize ourselves without the proper protections in place, the easier it becomes for cyber criminals to learn about us and use our digital identities to their advantage. With the rise of digital wallets, vaccine codes, digital driver’s licenses, biometrics and credentials, connected homes, smart airports and much more, we’re likely going to experience more calls for supervision of these digital ID systems along with more global ID initiatives in the future. With more access to the internet via mobile, a pandemic-induced accelerated shift to all things digital-first, and an increase in demand for security, digital identity is definitely a feature of modernization processes to come.

Australia BNPL player Zip is partnering with Singapore telecommunications firm Singtel.

Singtel is integrating Zip’s Pay Later into its mobile wallet, Dash.

Over the next six months, Zip will launch new payment schemes and onboard more than 2,000 new merchants to its existing network of 51,000.

Australian buy now, pay later (BNPL) company Zip is partnering with Singapore’s largest telecommunications firm Singtel this week. Through their collaboration, Zip’s Pay Later service will be available to Singaporeans on Singtel’s Dash app.

The integration provides Dash customers with the option to pay for a purchase in full or to pay over time with Zip. Zip’s Pay Later tool enables users to pay for everyday purchases between $350 and $1,000 in interest-free installments on a flexible schedule.

“Many of our customers want greater choice and control over managing their finances and our partnership with Zip provides just that with an alternative payment method that is transparent and flexible,” said Singtel Head of Financial and Lifestyle Services Gilbert Chuah. “This collaboration adds to Dash’s rapidly growing financial services business and we are working on expanding our suite of financial products and services to meet our customers’ diverse needs.”

Dash is a Singapore-centric mobile wallet that offers users remittance services, insurance and investment products, in-person and online contactless payments, rewards, and deals. By partnering with Dash, which counts one million registered users, Zip will have a running start in Singapore, a new geography for the BNPL company. Zip initiated operations in the South East Asia region after investing in Philippine-based TendoPay, a fellow BNPL player, in May of last year.

Over the next six months, Zip will be rolling out new payment schemes and onboarding more than 2,000 new merchants to its network of 51,000– including Target, North Face, and Wrangler– that have already integrated Zip’s BNPL technology into their checkout flows.

There has been a consistent pulse of news coming from BNPL providers over the past 12 months. Just today, Bloomberg reported that Sweden-based Klarna is looking to raise new funds, while France-based Alma closed $130 million in Series C funding and $109 million in debt financing. Last fall, Marqeta announced it would help banks get in on the action. The firm partnered with Amount to offer a BNPL-as-a-service offering.

Trulioo has acquired HelloFlow, a digital onboarding startup. Financial terms of the deal were not disclosed.

HelloFlow’s no-code, drag-and-drop tools “vastly simplify” the onboarding process and will offer efficiencies to Trulioo’s GlobalGateway customers.

Trulioo will leverage Denmark-based HelloFlow to help expand its global footprint, specifically in Europe. The company plans to double the size of its team by the end of the year.

Trulioo is making an acquisition today that will boost the digital onboarding aspect of its global identity platform. The company announced it has acquired HelloFlow, a startup that enables businesses to build client onboarding, monitoring, and digital workflow solutions using a no-code, drag-and-drop interface. Financial terms of the deal were not disclosed.

HelloFlow was founded in 2020 by Mikkel Skarnager and Ciprian Florescu who set out to disrupt the onboarding process by creating a digital solution with low barriers to digitalization. They came up with a no-code solution that minimizes coding and developer costs. The Denmark-based company has raised $3.3 million.

“We set out to build a platform that businesses could leverage for digital onboarding regardless of company size, resources, market, or jurisdiction,” said Skarnager. “We’re thrilled to be joining Trulioo and continue the journey of digital innovation and inclusion.”

The purchase combines Trulioo’s GlobalGateway data and identity services network built to verify the identity of both business and individuals with HelloFlow’s suite of orchestration, onboarding workflow, and risk management capabilities. By integrating HelloFlow’s technology, Trulioo will offer a single platform that combines Trulioo’s eIDV, KYB and DocV capabilities with the orchestration solution from HelloFlow. According to the press release, HelloFlow will “vastly simplify” the onboarding process, which will offer efficiencies for Trulioo customers.

“Establishing and securing trust online is a foundational step for all digital activity,” said Trulioo President and CEO Steve Munford. “Our ability to verify both businesses and individuals globally combined with HelloFlow’s advanced orchestration delivers unmatched capabilities and helps us accelerate an end-to-end identity platform that meets the evolving needs of our customers.”

Throughout 2022, the company plans to expand its global footprint. As part of this strategy, Trulioo will leverage HelloFlow’s current locations and operations to support its European expansion. By the end of this year, Trulioo anticipates it will have doubled the size of its team.

This purchase is Trulioo’s second acquisition since it was founded in 2011. Last June, the company raised $394 million in funding, boosting its total funding to almost $475 million and increasing its valuation to $1.75 billion.

For a look at the newest technology coming out of Trulioo, check out the company’s live demo at FinovateEurope next month. Trulioo is a Platinum sponsor of the event, which is taking place in person this year on March 22 and 23 at the Intercontinental O2 in London. Book your ticket today to save.

Apple launched its Tap to Pay capability enabling merchants to accept payments via iPhone

Stripe will be the first payment platform to offer the new Tap to Pay functionality.

The new solution will compete with Block’s Square, PayPal’s contactless QR code payment offering, and others

Rumors circulated about the launch of a contactless payment acceptance tool for iPhone a few weeks ago. Today, the news is no longer a rumor; Appleconfirmed the details.

The tech giant announced plans to launch Tap to Pay on iPhone, a new capability that lets merchants use their iPhone to accept Apple Pay, contactless payment cards, and other digital wallets by tapping it to their iPhone. The new payment tool will be available as a service. Apple will allow payment platforms and app developers to integrate the new contactless payment capability into their iOS apps for business customers.

“As more and more consumers are tapping to pay with digital wallets and credit cards, Tap to Pay on iPhone will provide businesses with a secure, private, and easy way to accept contactless payments and unlock new checkout experiences using the power, security, and convenience of iPhone,” said Apple’s Vice President of Apple Pay and Apple Wallet Jennifer Bailey. “In collaboration with payment platforms, app developers, and payment networks, we’re making it easier than ever for businesses of all sizes — from solopreneurs to large retailers — to seamlessly accept contactless payments and continue to grow their business.”

Tap to Pay leverages NFC technology to enable customers to pay by holding their iPhone, Apple Watch, contactless credit or debit card, or other digital wallet near the merchant’s iPhone, to complete a purchase in person. Once the technology becomes available, merchants simply need to unlock the capability on their iPhone; no additional hardware is necessary.

Stripe will be the first payment platform to offer Tap to Pay. The fintech will offer the payment technology to its merchant customers via its new Shopify app. Additional payment platforms will be added later this year. “Whether you’re a salesperson at an internet-first retailer or an individual entrepreneur, you can soon accept contactless payments on a device that’s already in your pocket: your iPhone,” said Stripe Chief Business Officer Billy Alvarado. “With Tap to Pay on iPhone, millions of businesses using Stripe can enhance their in-person commerce experience by offering their customers a fast and secure checkout.”

The new payment acceptance tool is a direct competitor to the multiple merchant acceptance solutions that launched over a decade ago, including Block’s Square, which launched its card reading dongle in May of 2010, and PayPal, which launched its contactless QR code payment technology in 2020.

Despite this well-established competition, Apple still has more than a fighting chance to gain traction with Tap to Pay. That’s because not only is it hardware-free, it is also virtually friction-free for customers, and doesn’t require shoppers to download a new app or change their existing habits. Additionally, because it is an Apple product, we can count on it to build a customer-first user interface.

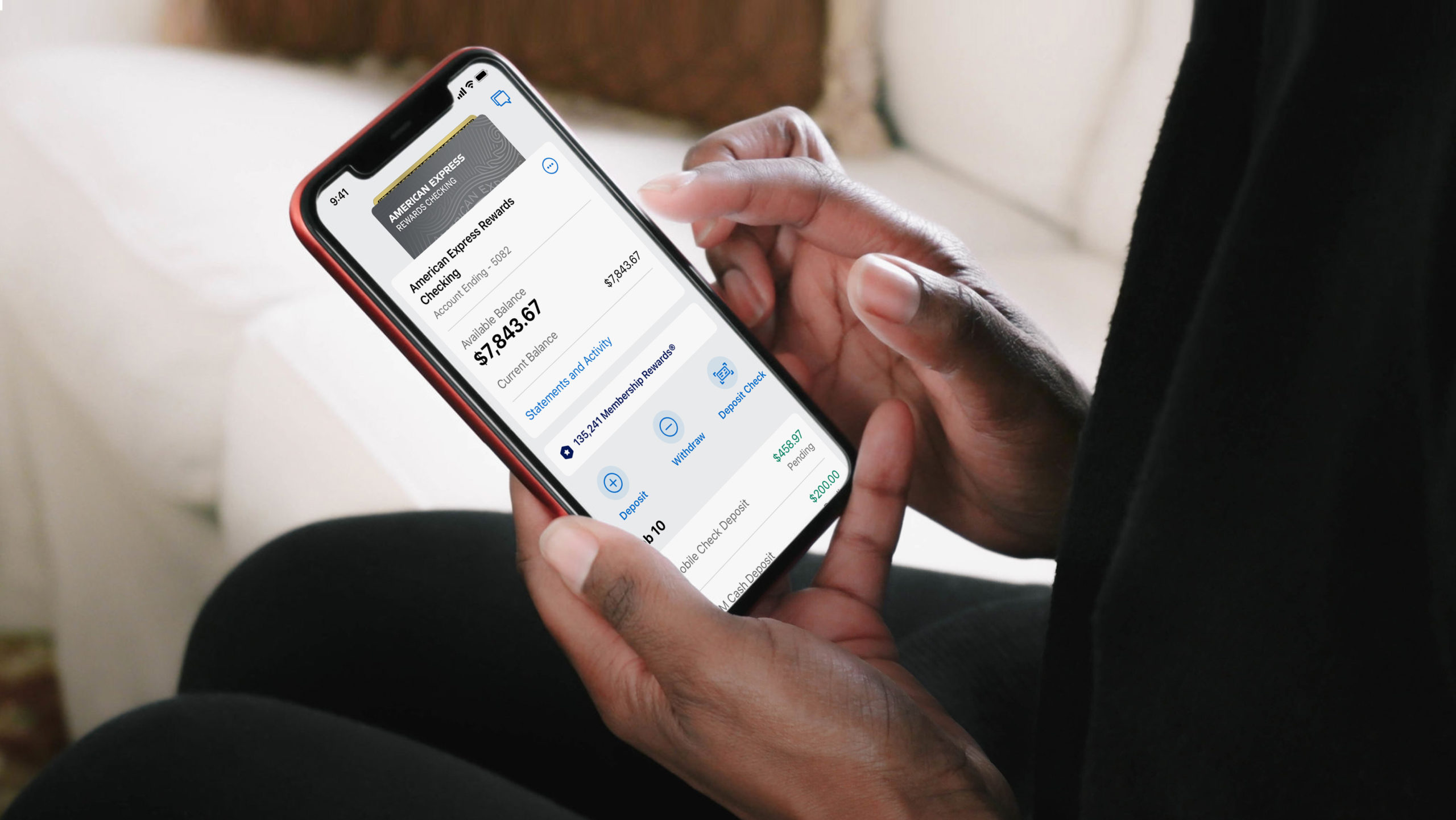

American Express is launching a new, digital checking account called Amex Rewards Checking

The Amex Rewards Checking account will offer a 0.50% high-yield APY on account balances, along with other membership rewards

The new checking account is only open to primary American Express credit cardholders and is limited to individual users.

Financial services giant American Express is expanding its horizons into the crowded world of digital checking. The company is launchingAmex Rewards Checking, an all-digital consumer checking account, for eligible U.S. card members.

As an incumbent player, American Express has multiple advantages over the many smaller digital challenger upstarts that have launched in the past two years. That’s because not only does the New York-based firm have credibility and a pre-existing large customer base, it also comes with a reputation for its rewards and perks.

“Our Members want more banking products and services from us,” said American Express Executive Vice President and General Manager of Consumer Banking Eva Reda. “And they want more from their checking account, without giving up the benefits that are important to them. That’s why we built Amex Rewards Checking to deliver more value for Members with the powerful and trusted backing of American Express. It’s digital checking without compromises.”

The checking account product will be a draw to Millennial and Gen Z users, who look for banking products with incentives and rewards. In fact, according to a study from Amex, 35% of consumers rank rewards and offers at the top when considering opening a new account. Given this, Amex packed competitive features into its new checking account. Accountholders can:

Earn 0.50% high-yield APY on their account balance, which is 10x higher than the national rate

Gain one Membership Rewards point for every $2 spent on eligible debit card purchases. Users can redeem these points for deposits into their Amex checking account

Pay no monthly maintenance fees or minimum balance fees

Receive purchase protection for accidental damage or theft on eligible purchases

Access Amex’s customer care providers 24/7 via phone or chat

Receive fraud protection and monitoring

Make fee-free ATM withdrawals at 37,000 MoneyPass ATM locations

The new Rewards Checking account is only open to primary American Express credit cardholders who have had their account for more than three months. Currently, the new checking account is limited to individuals and cannot accommodate joint accounts.

The new Amex Rewards Checking is American Express’ first checking account for retail customers. The financial services giant has offered small business checking for a little over a year now. The company acquiredKabbage in 2020 for $850 million and leveraged the purchase to launch a small business checking offering in 2021. That said, it’s worth noting that Amex’s new debit card is not available to its small business checking customers.

American Express, which presented at our developers conference in 2015, is listed on the New York Stock Exchange under the ticker AXP. The company saw $36 billion in revenue in 2020 and has a market capitalization of $149 billion. Stephen Squeri is CEO.