This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

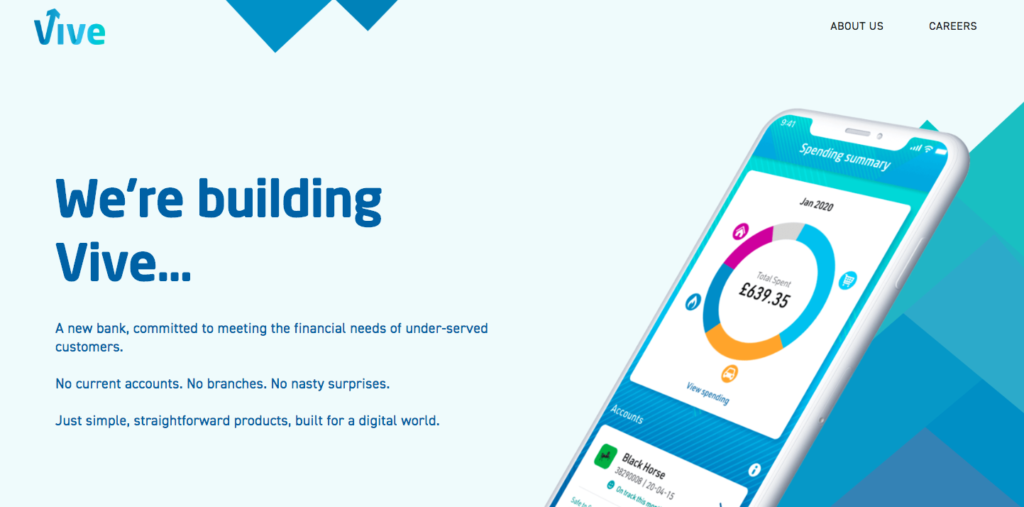

Challenger bank Vive Bank received some good news from the Bank of England today. The U.K.-based startup has been granted a banking license with restrictions.

Vive is aiming to ship its offerings in the second quarter of 2020 but unlike the region’s other challenger banks, Vive Bank will not be launching a current account. Instead, Vive Bank will focus on unsecured personal loans, a fixed-rate savings account, and PFM tools.

“It’s just not difficult to get a current account, so we want to focus on serving our customers with what they really need,” Vive CEO Nick Anthony said in an interview with AltFi. “We’re looking to serve a market where it’s more difficult for customers to get banking products. We want to make it simple and straightforward. Our unsecured personal loans, for example, will be far more than the narrow offering from high street banks, aimed at helping those with less than perfect credit scores.”

Vive Bank was founded in 2017 and has since refrained from promoting its services. While a waiting list is available on its website, the startup has intentionally remained quiet until today.

If you’ve ever been hacked, having either money or personal credentials stolen, did you stop to think about what type of person, organization, or agenda you were inadvertently supporting?

“Let’s talk about the funding of evil,” said Trusona founder and CEO Ori Eisen during his first Finovate demo. “When a bank loses $10 million, it’s not a good day for the bank. But where the money goes and what it’s being spent on is not good either.” Eisen then turned to the audience to suggest their responsibility in the matter. “You can help stop or curb the funding of evil,” he added.

At first I thought he was joking. Discussion of the “funding of evil” and “stopping the bad guys” sounded like something straight out of a kid’s TV program. However, it’s no joke and it’s unnerving to think of what these “bad guy” fraudsters do with their stolen cash.

In the demo, Eisen went on to explain that one way to curb funding these fraudsters is to make user’s accounts more secure. And in Trusona’s opinion, the best way to do that is to get rid of passwords entirely. The Arizona-based company just raised $20 million this month in support of this concept– getting rid of the password. The investment brought Trusona’s total funding to $38 million.

So what does web authentication look like without a password? The 30 second process requires the user to have their smartphone with them, but doesn’t require access to a cellular network. Upon logging in, the user clicks Login with Trusona. The web interface shows a unique QR code, and the user then opens the Trusona app on their smartphone, scans the QR code, and taps to accept. Once complete, the user can enter the website without the need for a username or password.

In addition to simple authentication, Trusona also offers solutions for ID scanning and proofing, multi-factor authentication, and VPNs.

The need for such a solution stems from faulty password management skills common among consumers and employees today. In fact, last year Trace Security reported that 81% of company data breaches were caused by poor passwords. Trusona offers an SDK that businesses can integrate into their own app to simplify logins for both employees and end customers.

With its recent funding, Trusona said it will focus on expanding its customer base as well as begin working on new product offerings.

Trusona was founded in 2015 and counts Aetna, Kleiner Perkins, and Bain Capital among its clients. The company has demoed at Finovate twice and won Best of Show awards at both of its appearances. Check out Trusona’s most recent demo below.

Community bank marketing expert Kasasaannounced a partnership with Carleton today in which Kasasa will integrate Carleton’s insurance and debt protection calculations into its Kasasa Loan, a move that will allow it to tailor loan limits.

Headquartered in Indiana, Carleton provides financial calculation software, loan origination compliance support, and document generation software. Through the partnership, Kasasa will enable its clients to add debt protection and credit insurance products to their Kasasa Loan offering.

Kasasa will use Carleton’s CarletonCalcs, which will allow it to tailor limits to each client based on their institutional, state, and federal compliance requirements. “By integrating CarletonCalcs throughout the Kasasa service platform, Carleton will ensure compliant loan computations and precise amortization schedules through Kasasa’s dashboard and mobile app,” said Carleton President and COO Matt Ruszkowski.

“We wanted to ensure the Kasasa Loan added a high level of configurability and compliance support to meet our client’s needs, in addition to providing consumers the greatest flexibility when choosing their loans,” said Chris Cohen, EVP, Product Management for Kasasa.

Kasasa debuted its Kasasa Loan in 2017 and showcased it at FinovateSpring 2018. The concept works similar to a regular loan agreement in which the borrower repays according to a regular payment schedule. However, it is unique because every month the consumer has the option to overpay on their loan repayment and at any time in the future if they need to access cash quickly, they have the option to “take-back” any portion of the overpayment.

Kasasa is an Austin-based company with 450 employees. The company counts 900 community financial institutions as clients.

We recently spoke with ITSCREDIT CEO João Pinto. Founded in 2018, ITSCREDIT is a spinoff from ITSECTOR and is a fairly new player in the digital lending space. The Portugal-based company focuses on placing the consumer in control of the lending experience by making the entire process digital.

In this interview, Pinto talks to us about the digital lending opportunity, how his company fits into the current state of this fintech subsector, and what we can expect to see next.

Finovate: There is a wide range of borrowers out there– some who may not be comfortable on digital channels and others who are digital natives. How does ITSCREDIT adapt to this variety?

João Pinto: The main focus of ITSCREDIT is to evolve the lending process so that different types of customers can perform all lending origination actions using online channels. Our aim is that the customers can perform all origination operations online with minimum data input. We do this by retrieving necessary application information from various systems (personal data, financial data, and so on). Our approach to digital lending is to provide processes that are intuitive, attractive, simple, and fast in an online environment to revamp many of the bureaucracies often associated with traveling to the banks’ physical branches.

The customer can access the ITSCREDIT platform via online channels, such as mobile and internet. ITSCREDIT provides interfaces for other channels, as well, such as branch, contact center, and backoffice, which all have access to the client and their application process. This means that the client can start an application in any channel and get information or advice and can continue the process in any other channel. This way, more traditional users that are not as comfortable using digital channels can use traditional channels either in an isolated way, or– more interestingly– in a combined way. The multi-channel approach offers them full control of their application.

Finovate: How does ITSCREDIT underwrite credit risk and how does that approach differ from incumbent players?

Pinto: The ITSCREDIT platform contains four main modules: Flowcredit (Loan Origination), Calculators, Risk Analysis,Scoring, and Collections. Each can operate in isolation or can be combined in any way. Also, the platform is open so that implementations can use as much data as is available in order to have a more complete view of customers and their financials. We believe this is a huge strength of the platform. It allows banks to garner richer information for the risk analysis from both individuals and corporations (through Risk Analysis and Scoring modules), and also makes data available from credit applications processes (through Flowcredit).

In many situations our clients have, in the past, invested heavily in building their credit application analysis. The Flowcredit module easily integrates with such systems and then adds additional information and rules to make underwriting even more accurate and tailored to suit the financial institution needs.

Finovate: Tell us about the role that open banking plays in ITSCREDIT.

Pinto: As we mentioned previously, one of our strengths is that the ITSCREDIT platform is open so that implementations can use as much data as is available in order to have a more complete view of customers and their financials. In this scenario, open banking is a key element. It not only makes much more data available from different players, but also makes integrations much easier.

On the other hand, our platform is based on a services architecture, so that it exposes services that can be consumed by third party entities. For example, the use of calculators and loan origination components can easily be used in different commerce sites and therefore originate completely new lines of business for the institutions. For example, a travel agent can have a payment method on their website for their clients based on a personal loan.

Finovate: Looking broadly at the credit and lending industry as a whole, what changes do you anticipate 2020 will bring?

Pinto: In the past years we have seen financial institutions start to approach digital lending for their clients. This journey is still in its early stages, with few institutions providing such functionalities for a few products. We are sure, though, that in 2020 we’ll see more institutions adopting full digital lending with simpler models more adequate to their clients needs. The launch of PSD2 in Europe and other Open Banking initiatives around the world make it much easier to obtain personal and financial data from credit applicants and therefore make the loan origination simpler and faster.

The other area that we foresee a great expansion is through a space we refer to as dPOS (digital Point-of-Sale). A dPOS enables merchants to provide payment methods for their ecommerce platforms with digital lending, providing lower rates on credit cards for end customers and a lower cost and even extra income for merchants.

Finovate: What’s next on the horizon for ITSCREDIT?

Pinto: ITSCREDIT is a spin-off that will be 2 years old in May. We already have 13 clients on three continents: North America, Europe, and Africa. Our journey on the commercial side is to present the advantages of our solutions to more institutions and get more implementations.

In terms of product evolutions, we are enhancing the digital lending capabilities and models and launching new versions in 2020 for brokers and merchants.

Overall, our big aim is to position ourselves as a world-class player for credit solutions, providing innovative and modern solutions for our customers to help them differentiate from their competitors and become more efficient with higher loan volumes.

You can watch ITSCREDIT demo its latest technology on stage at FinovateEurope next month. Register now to save your seat!

If you’re interested in demoing on the FinovateEurope stage this year, reach out to [email protected] or take a look at our event page for more details.

If your insurance company is offering you drone insurance, you know it’s not your grandmother’s insurance agency. Germany-based insurtech Getsafe does just that– and the company announced today it is expanding its home contents insurance offering (though, sadly, not its drone insurance offering) to users in the U.K.

Starting today, U.K. users will have access to Getsafe’s “neo-insurance” offering via its mobile app. The launch is made partially possible via a partnership with Hiscox, which will serve as the carrier for Getsafe’s U.K. contents product. The fintech’s other insurance partners include Munich Re and AXA.

Getsafe’s selection of the U.K. as its next launch site is a strategic one since U.K. residents are already comfortable with mobile-based services and payments. In fact, the U.K. is one of the leading regions of the globe for challenger banks.

The company has already proven itself as the fastest growing insurance agency for millennials in Germany. “Over the last two years, we have shown that our product meets a core need for the young, tech-savvy generation,” said CEO and founder Christian Wiens. “With our insurance delivered through your smartphone, we are developing a product that fits perfectly with the living and communication habits of this generation.”

Getsafe states that today’s move into the U.K. is “just the beginning.” The company plans to expand its offerings to all of Europe in the next few years.

Getsafe has raised $17 million and was founded in 2015. In addition to its contents and drone insurance products, the company offers ad-hoc insurance for travel, liability, bike theft, legal protection, routine care, dental care, and dental replacement. Getsafe also has plans to launch a digital life insurance company in Germany, its flagship market.

If you’re like me, you’re already experiencing 2020 fatigue. If you’ve read at least 10 posts depicting the top trends for 2020 in every fintech sub sector, you’re not alone.

Fortunately for you, this isn’t another 2020 predictions post.

Instead, we’re taking a look at the trends you can expect to see on stage next month at FinovateEurope. To keep things simple this year, we assessed the themes at a very high level and broke them down into three categories: the big, the little, and the trends in-between.

The big trends

As you can see in the word cloud above, the big topics for FinovateEurope 2020 are AI, digital identity, and customer experience. The only surprise here is that AI isn’t bigger. Since AI is an enabling technology it often pulses throughout multiple sectors across fintech. Customer experience, for example, is a topic that relies heavily on AI.

Digital identity is another trend developing throughout the fintech industry and has been rising in discussions around identity verification. However, digital identity isn’t quite as sexy as AI, so companies aren’t as quick to boast about their digital identity capabilities.

The little trends

The three smallest trends on this year’s list include blockchain, compliance, and PFM. Though its potential to disrupt traditional banking hasn’t lessened, blockchain has regressed slightly into the shadows of fintech. This may be the result of compliance complications that the blockchain brings. Other challenges to wider blockchain adoption may result from a lack of understanding of the subject or stem from the lack of ability for legacy systems to adapt.

PFM appears as a small topic because while many fintechs help users with their personal finances, they are hesitant to describe their technology as PFM. However, just because PFM is older than Twitter doesn’t make it any less relevant.

Speaking of relevance, compliance is pertinent to every subsector in fintech. However, the topic appears small in the word cloud because it is a bit of a status quo. In other words, every bank and fintech has some level of compliance measures in place.

The trends in between

Data analytics, fraud prevention, wealthtech, chatbots, lending, credit, regtech, and small business tools are all trends caught in the middle this year.

None of the topics is new and the only one I’m surprised to see on this list is fraud prevention since it is thought of more as a requirement than something firms are looking to add to their technology. However, recent evolutions in cybercriminal techniques, high-profile hacks, as well as advancements in enabling technologies adapted to the security space have made fraud prevention an even hotter topic than it once was.

If you want to not only read about the newest fintech trend transformations but also see them demoed live on stage, register for FinovateEurope. This year’s event is taking place in Berlin, Germany on 11 through 13 February.

Interested in demoing your company’s new technology on stage? There’s still room in our demo lineup. Check out more information on what it takes to demo at FinovateEurope or contact [email protected] for details.

European deposit marketplace Raisin announced today it acquired New York-based Choice Financial Solutions. Terms of the acquisition, which marks Raisin’s fourth purchase in the past year, were undisclosed.

Raisin will license Choice FS’ technology to banks in the U.S., a move that will bring the company one step closer to its U.S. launch. Last year, Raisin teased the geographical expansion with the appointment of Paul Knodel as U.S. CEO.

Raisin U.S. CEO Paul Knodel

“Joining forces with Choice Financial Solutions lets Raisin begin offering cutting-edge services to banks and customers before we even launch our U.S. platform,” said Knodel. “As a leading innovator in the deposits space, Raisin sees Choice FS as a perfect fit for our mission in the U.S. deposits market. The enthusiastic market feedback we have already received affirms how ripe the savings space is for just this type of personalization.”

Choice FS has a decade-long track record of providing banks with technology to help their clients save for long-and-short-term goals. The company’s secret sauce is customization– something modern consumers have become accustomed to in today’s era of BigTech solutions. Choice FS allows banks to customize terms, distributions, amounts, and withdrawals to maximize return on savings accounts, creating a highly-personalized savings experience with an intuitive user interface. Company founder and CEO Daniel Smith refers to this personalization as “the missing piece” for banks and depositors.

Raisin was founded in 2012 and has since brokered $20.6 billion (€18.5 billion) for 200,000 customers in 28+ European countries and 90 partner banks. The company provides a free marketplace where consumers can browse European deposit products, ETF portfolios, and, in Germany, pension products.

Supply chain payments company Tradeshift just unveiled details about a $240 million funding round today. The investment– a combination of debt and equity– comes from new and existing investors. Tradeshift’s total funding is now $672 million.

The San Francisco-based company will use the investment to boost expansion efforts and gear toward a “direct path to profitability in the near future.” The funding will also be used to grow Tradeshift’s network finance program that provides liquidity to companies in 100+ countries.

And it appears that Tradeshift is already on the right track. Last year the company tallied record expansion; growing its revenue more than 60% and closing more than 300 enterprise deals. What’s more, 40% of the total transaction volume across its platform occurred in the last 12 months.

“It’s clear that the investor community has a strong focus on growth combined with profitability and they like our plan,” said Tradeshift CEO Christian Lanng. “As a network business, growth is always going to be a key part of our story. But it’s also important that we manage that growth responsibly.”

Tradeshift’s business commerce platform connects more than 1.5 million companies across 190 countries. To date, the company has processed more than half a trillion dollars in transaction value. After Tradeshift’s most recent funding round of $250 million last spring, the company’s valuation was boosted to $1.1 billion.

As for 2020 plans, Lanng said that the company’s focus “will be about doubling down in areas where we’re seeing the greatest momentum while continuing to ensure we have the necessary balance in place to fully capitalize on the enormous opportunities in front of us.”

Risk management and advisory services firm INTL FCStone announced today that its London-based subsidiary has agreed to acquire GIROXX for an undisclosed amount.

Headquartered in Germany, GIROXX offers international bank transfers and currency hedging. INTL FCStone plans to leverage this technology to expand its current client base to small-and-medium-sized enterprises (SMEs).

As part of the agreement, INTL FCStone’s advisory services will be made available to GIROXX’s clients. GIROXX founders Klaus Hoffmann and Jörg Sonnenschein said that the deal will help the company “gain the resources to offer hedging services on a multi assets basis.” As a result, the founders anticipate that GIROXX will solidify its client base and boost company expansion.

The purchase marks INTL FCStone’s sixth acquisition and its fourth in less than 10 months. The company said that these purchases, combined with internal restructuring, are part of an effort to protect clients from negative effects of Brexit.

“Our objective is to offer SME’s the ability to hedge all parts of their production processes, and to allow these corporates to have access to a digital payments and hedging platform,” said Carsten Hils, Global Head of INTL FCStone’s Global Payments Division.

Following the deal, INTL FCStone plans to open its client base to companies with less than 1,000 employees in Europe, a market with 350+ correspondent banks. The acquisition is pending approval from BaFin, Germany’s financial regulatory authority.

Founded in 1981, INTL FCStone is publicly listed on the NASDAQ under the ticker INTL. The company has a market capitalization of $947 million.

Thailand’s biggest bank by assets, Siam Commercial Bank (SCB), announced it has partnered with blockchain solutions company Ripple. SCB will leverage Ripple’s RippleNet to power the cross-border payment offering in its mobile app, SCB Easy for the app’s 9+ million users.

RippleNet is Ripple’s global payment network that works across 40+ currencies and consists of more than 200 financial institutions. Because RippleNet leverages the blockchain, users are able to track funds, delivery time, and status.

“It is so difficult to send and receive money today. People must physically go to a bank branch, fill out long and complicated forms and wait for payments to be received—with no transparency,” said SCB’s SVP of Commercial Banking, Arthit Sriumporn. “With our service, their loved ones from abroad can transfer payment and receive money immediately.”

SCB is also working with Ripple and EMVCo to add a QR code-based payment solution to SCB Easy. Once complete, the QR codes will enable users to make payments without using the local currency.

This isn’t SCB’s first partnership with Ripple. The bank first partnered with Ripple in 2018 when it became the first financial institution using RippleNet to pilot multi-hop, a tool that enables banks to settle frictionless payments on behalf of other banks in the network.

Ripple has offices in San Francisco, New York, London, Luxembourg, Mumbai, Singapore, Sydney, and Brazil. Ripple recently closed $200 million in a Series C round, bringing the company’s total funding to $321 million and boosting its valuation to $10 billion.

Banks are facing an increased number of competitors these days. Not only are traditional banks vying for customer deposits, but fintechs and challenger banks want part of their funds, as well.

The average U.S. savings rate is just 0.09% APY, so any amount banks can offer beyond that is a differentiator. However, some banks have gone all out and are offering more than 2% interest. The highest APY we saw totaled a whopping 6.17%.

Here are the 8 financial institutions (listed in alphabetical order) we found that are offering accounts currently paying more than 2% interest:

BrioDirect

2.1% APY with a minimum balance of $25

Digital Federal Credit Union

6.17% APY on first $1,000 with a minimum balance of $5

Elements Financial

New accountholders can earn 2.1% APY for one year on a minimum of $2,500 that has been transferred from another financial institution.

Fitness Bank

Members earn 2.20% APY on a minimum balance of $100 if they walk 12,500 steps or more per day (or 10,000 steps per day for those age 65 or older) as calculated on their fitness tracker.

GreenDot

Users earn 3% APY, which is paid on a maximum of $10,000 and is held in a separate account that the consumer is unable to access until the account anniversary. The high yield savings account must be opened in tandem with Green Dot’s Unlimited Cash Back account, which pays customers a 3% cash-back bonus on all online and in-app purchases. The account charges a $7.95 monthly fee if a consumer’s purchases (excluding mobile bill payments, ATM withdrawals, and ACH transactions) are less than $1,000.

T-Mobile Money

Users earn 4% APY on balances of $3,000 or less. Any amount over the $3,000 threshold earns 1% APY. There is no minimum balance requirement but account holders must deposit at least $200 per month into the account to earn 4% APY.

TotalDirectBank

2.1% APY on balances of at least $5,000 and no more than $500,000.

Vio Bank

2.02% APY with a minimum deposit of $100

Many of these financial institutions are able to offer higher-than-average rates by keeping their operating costs low. In most cases, the lower operating cost is the result of being an online-only bank. However, two of the banks listed above (Digital Federal Credit Union and Elements Financial) have physical branch locations, as well.

Another aspect that helps with offering high interest is setting appropriate limitations. Interestingly, the two banks on this list that have branch locations (re: higher operating costs) are the two with the most stringent restrictions on their savings accounts. Setting up appropriate limits on account earnings can make banks’ offerings look attractive without costing too much. Conversely, too many restrictions will frustrate consumers and, perhaps worse, compromise trust.

The People’s Bank of China (PBOC), China’s Central Bank, announced it has accepted an application from American Express (AmEx) that expressed the company’s intention to operate in China.

Reuters reported that the PBOC announced the receipt of AmEx’s application via a WeChat post on Wednesday. The bank, however, did not disclose information about the approval timeline.

This follows the PBOC’s approval in November of 2018 for AmEx to clear card payments in partnership with China’s LianLian Pay to process payments in Yuan. This week’s announcement also makes AmEx the first U.S. card network company to gain access into the China market. In order to commence operations, however, AmEx still needs final approval from the PBOC.

China is beginning to open up its credit card payments market to foreign players after restricting access. For the past ten years, foreign payment card companies could only tap into China’s credit card market via partnership with state-run UnionPay.

Visa and Mastercard are expected to follow suit to claim their stake in China’s $27 trillion market.

Traditional players aren’t the only ones eyeing the China opportunity. Last October PayPal gained controlling interest in China-based GoPay. The move granted PayPal a license to offer online payment services in China, making it the first foreign company to be granted such license.