This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Banking technology innovator Plaid is kicking off Black History Month ahead of schedule this year. The San Francisco-based company announced the launch of FinRise today. FinRise is a nine month accelerator program designed to support early-stage founders who are Black, Indigenous, or People of Color (BIPOC).

“While technology has come a long way to level the playing field, the reality is that many minority-owned businesses are still frequently denied access to some of the most basic resources needed to start and grow their businesses,” the company said in a blog post.

The program, which was developed during an internal hackathon, offers three key areas of support:

Access to capital and services Plaid is leveraging its network of venture capital firms, network service providers, and accelerators to offer startups networking opportunities, discounted services and ad credits, and pitch practice.

Resources for growth The program will kick off with a three-day virtual bootcamp led by Plaid experts and other thought leaders who will lead workshops on technical, product, and business topics. The sessions will focus on topics like communication and storytelling, engineering best practices, navigating the policy and regulatory landscapes, and designing user-centric experiences.

Mentorship and support Participants will receive support for nine months following the bootcamp. In addition to benefitting from others in the bootcamp cohort, startups will have access to a dedicated account manager, an internal skillshare network, and mentorship from Plaid leaders.

The FinRise program certainly fills a gap. Historically, much of the attention on diversity has been focused on driving more women into the fintech sector. With Black History Month starting in February and the Black Lives Matter Movement still fresh in everyone’s mind, we can expect to see more initiatives dedicated to solving the gap in ethnic diversity in fintech and the technology field in general.

The first FinRise program will take place from April to December, 2021.

Eligible startups are U.S.-based, BIPOC majority-owned businesses incorporated in the United States with two or more employees. A panel of Plaid leaders will select the participants, giving preference to those that offer a product that leverages financial data.

Founders can apply starting today and the first cohort will be announced in early March.

There’s not much room in 2021 for 2020-style pessimism. Sure, if you look, you can find plenty of things to be negative about so far this year. However, one aspect of 2021 that’s giving fintechs hope is the recent uptick in valuations across the fintech sector.

Despite last year’s global events, many fintechs received valuations exceeding $1 billion. In fact, in December 2020 alone, four fintechs, including eToro, Creditas, PhonePE, and GoCardless, received unicorn status.

This year seems to be off to a similarly bullish start, with four fintechs becoming unicorns in just the first three weeks of 2021:

Digit Insurance

India-based Digit Insurance became India’s first unicorn of 2021 after the country saw 11 new unicorns in 2020. Just 15 days into the new year, and after raising $18.5 million, Digit Insurance unveiled a new valuation of $1.9 billion.

Divvy

Spend management startup Divvy received a valuation of $1.6 billion after its Series D round on January 5. The $165 million came from new investors PayPal Ventures, Whale Rock, Schonfeld, and previous backers NEA, Insight Venture Partners, Acrew, and Pelion. The pandemic has spurred increased traffic to Utah-based Divvy; the startup has experienced a 500% increase in monthly sign-ups since March 2020.

Mambu

SaaS banking platform Mambuearned its unicorn title after landing a $135 million investment on January 7. The boost gave the Germany-based company a post-money valuation of just over $2 billion. Mambu will use the funds to increase its presence in Brazil, Japan, and the U.S.

MX

The second fintech unicorn to come out of Lehi, Utah is fintech data company MX. Founded in 2010, MX raised $300 million in Series C funding on January 13, bringing the company’s total capital to $505 billion and boosting its valuation to $1.9 billion. Company CEO Ryan Caldwell said that MX will use the funds to hire more staff and improve its data collection and enhancement capabilities.

Beijing-based ByteDance, the company behind TikTok, launched a mobile payments service for Douyin, which is China’s version of TikTok.

The new mobile payments service, Douyin Pay, will compete with the likes of Tencent’s WeChat Pay and Alibaba’s Alipay. “The set-up of Douyin Pay is to supplement the existing major payment options, and to ultimately enhance user experience on Douyin,” a Douyin representative told Reuters.

Douyin Pay will also help Douyin expand into the ecommerce scene. That’s because while users are watching short video clips of influencers promoting products on the Douyin app, they can pay using Douyin Pay instead of with competing payment services.

Helping to power the new payment service is Wuhan Hezhong Yibao Technology Co., which ByteDance purchased for an undisclosed amount in September of last year. Hezhong Yibao received a third-party payment license from China’s central bank in 2014.

Last fall, ByteDance achieved a valuation of $100 billion, making it the most valuable privately-held startup. In 2019, the company’s e-commerce and TikTok brands accounted for 17% of its total revenue. This figure is expected to expand this year as ByteDance taps into the potential of short-form video apps.

Another player vying for space in the Chinese payments arena is PayPal, which recently took full ownership of China-based GoPay. The move marks PayPal as the first foreign operator with 100% control of a Chinese payment platform. PayPal’s aim with the purchase is to provide a cross-border payments solution for Chinese consumers and merchants.

Online pension provider PensionBee is making it easier for the non-traditional workforce to save for their later years. That’s because the U.K.-based company is launching a new product designed for self-employed users.

The product will enable new users to set up a new pension in minutes. The new offering also provides a flexible contributions plan so that savers can adjust their pension contribution amounts as their income fluctuates, with no minimum contribution required.

The self-employed pension product is available to sole traders and directors of companies without an existing workplace or private pension. Users have nine investment options, including the PensionBee’s Fossil Fuel Free Plan which completely excludes fossil fuel producers and persistent violators of the UN Global Compact.

One of PensionBee’s differentiating factors is its fee structure. Instead of charging users a range of fees, the company has a more simplified fee structure that charges just one annual fee. This “all-in” fee ranges from 0.50% to 0.95%, depending on the plan. And, to encourage higher balances, PensionBee offers users 50% off their fee for any portion of their savings that exceeds £100,000.

Prompting the release of the self-employed product is the increase in self-employed workers combined with a decline in consumer savings. According to a report from the Institute for Fiscal Studies, the number of self-employed workers has grown over the past two decades while the proportion saving into a private pension has fallen from 48% in 1998 to 16% in 2018. Another study from Nest found that only 24% of self-employed workers are saving into a pension.

“Without the benefits of auto-enrollment, the self-employed are at a significant disadvantage and need access to simple and flexible products urgently if they are to avoid a shortfall in later life,” said PensionBee CEO Romi Savova. “In the absence of old workplace pensions to provide a head start, we know that the thought of saving from nothing can be daunting for many self-employed consumers, which is why we’ve made it as easy as possible for them to open a pension and put money aside whenever their business allows.”

“The self-employed currently make up 20% of the PensionBee customer base, so we know their needs well and are committed to helping many more self-employed consumers plan for a happy retirement and achieve better financial outcomes.”

Savova founded PensionBee in 2014 along with his co-founder, Jonathan Lister. The company has closed three rounds of funding; the amounts of each round are undisclosed.

Brokerage infrastructure API provider DriveWealthannounced this week it acquired Cuttone & Company, a New York-based institutional broker dealer. Terms of the deal were not disclosed.

DriveWealth has purchased Cuttone & Company specifically for its market and regulatory expertise and network of institutional trading partners. The New Jersey-based company will leverage this expertise to offer its own partners access to price discovery on its scalable, configurable, and redundant electronic trading infrastructure.

Ultimately, the acquisition will offer retail investors who trade fractional shares of U.S. equities via DriveWealth’s partners direct access to the point of sale for NYSE securities.

“These added resources, unprecedented transparency, and the ability to trade directly on the NYSE or across all U.S. equity destinations will open up greater opportunities for the retail investors we serve on our platform,” said DriveWealth Founder and CEO Bob Cortright. “Having notional trading technology connected to a flexible brokerage infrastructure allows investors to start small by investing in brands they know and care about. We’re proud to bring this new combination of Cuttone & Company’s institutional knowledge with our retail trading technology to become the most complete brokerage stack available to retail investors today.”

DriveWealth was founded in 2012 by Cortright and his co-founder Julie Coin. The company has raised a total of $100.8 million, including a $56.7 million DriveWealth closed last October.

Global card issuing platform Marqetaunveiled today that it has been tapped by Goldman Sachs to power checking accounts for its Marcus brand.

The new digital checking accounts will launch for Goldman’s Marcus clients later this year, though there is no word on the exact timing.

Goldman selected Marqeta for its open APIs and webhooks and its developer experience, which was designed to power future-proofed banking experiences. The two also have a prior relationship, as Goldman Sachs is one of Marqeta’s previous investors.

“We’re incredibly proud to work with Marcus by Goldman Sachs to help power this work, which we think is a true validation of the power of our technology,” said Marqeta Founder and CEO Jason Gardner. “Our modern card issuing platform helps digital innovators build the sorts of customer experiences that can be industry game changers, and we’re looking forward to working alongside Marcus to bring a powerful new digital banking experience to life.”

Marcus currently offers limited consumer banking tools, including savings, certificates of deposits, and loans. The bank also partnered with Apple in 2019 to serve as the banking partner behind the Apple credit card. Expanding into checking accounts will help Goldman Sachs diversify from its traditional investment banking offerings and move further into the everyday financial lives of consumers.

Goldman’s expansion into checking accounts comes as no surprise. The bank announced its intentions in February of last year. And the partnership with Marqeta is a logical one. The California-based company offers a tech-forward approach and counts fintechs such as Square and Klarna among its clients.

Should other banks– challenger banks and traditional banks alike– be worried? Jim Marous answers that question in his piece Marcus: A Digital Bank That Should Keep Rivals Up At Night. “In the future, the Marcus brand will only grow,” said Marous. “With the addition of wealth management and eventually checking accounts that are 100% supported by a mobile app, financial institutions of all sizes should take note of the potential for Goldman Sachs to be a major player in the marketplace. If banks and credit unions are not paying attention today (when there is time to react), there is a good chance Marcus will be the source of nightmares going forward.”

Shortly after expanding its offerings to include consumer banking tools, fintech innovator Blendannounced it has landed $300 million in new funding.

The series G financing round was led by Coatue and Tiger Global, and brings Blend’s total funding to $665 million. With the investment, Blend is also seeing its valuation nearly double to $3.3 billion, up from $1.7 billion just five months earlier.

In a blog post, company CEO Nima Ghamsari said that Blend will use the funds to fuel “aggressive plans” for this year. “We want to build the banking software infrastructure for the future,” said the CEO, “with an end-to-end digital experience for any consumer banking product and a complete homebuying and financing journey from start to close.”

Blend offers banks no-code, drag-and-drop workflows to help them customize the end user experience and launch new products quickly in response to consumer demand.

The company launched in 2012 with a focus on helping banks revamp the mortgage application process for consumers. Last September, Blend introduced a consumer banking suite, a set of tools to help banks focus on more than just the lending process. The suite includes modules to help banks launch their own deposit accounts, credit cards, personal loans, vehicle loans, and home equity line of credit offerings.

Last year, Blend facilitated $1.4 trillion in loans, more than double what it did in 2019. The company counts 285+ lender partners, which together are responsible for around 30% of all mortgage volume in the U.S. Partners include BMO Harris Bank, Navy Federal Credit Union, and Wells Fargo, which sees more than 75% of its mortgage applications submitted via its Blend-powered application tool.

In addition to growing its loan volume and client portfolio, Blend also grew its team. The company added more than 200 employees last year remotely via Zoom, a move that increased its team by more than 60%.

“Today’s news is just another step in Blend’s journey; we’re in it for the long haul, and we look forward to continuing to build the best lending and banking experiences for all,” said Ghamsari.

This is a guest post written by Shannon Flynn, managing editor at ReHack.com.

Financial tech and nonprofits have an opportunity to build partnerships and make the world a better place. If fintech companies want to work with nonprofits, they must establish trust and clearly outline the benefits of collaborating for the greater good.

Households in the United States are generous. According to National Philanthropic Trust, Americans gave $449.64 billion to various charities in 2019. However, people are increasingly demanding that the giving be easy and intuitive, which brings fintech into play. Even the way nonprofits manage the funds donated to them is changing.

Examples of fintech companies include Lending Club, Kabbage and Stripe. Meshing fintech and charity isn’t always an obvious choice. However, nonprofit technology is on the rise, and organizations benefit greatly from some of the advantages these brands bring to the table. Here are some of the benefits of fintech charity partnerships.

How Fintech and Charity Work Together

There is a growing move toward non-cash payments in charitable giving. Forbes reports in countries such as Sweden, cash-based payments make up 13% of transactions. This can impact traditional fundraising efforts, such as in-person collection baskets.

Fintech advances in the last decade have made it much easier for people to participate in charitable giving. There are numerous ways nonprofit technology helps organizations raise money. Rather than an in-person fundraising push, organizations raise money via social media and email campaigns. Not to mention philanthropies saw an increase in virtual fundraising campaigns in 2020, boosting the need for online financial services and resources at an unprecedented rate.

Nonprofits can only thrive because of the generosity of patrons and local businesses. A fintech business can team up with a charity, and both can develop stronger community relationships as a result. Individuals who support the organization will look to partner companies for their own fintech solutions. The charity benefits from gaining access to the business’s software for easier donations and tracking funds.

Nonprofit Technology Advances

The M + R Online Giving Benchmark Study found that online revenue grew about 10% in 2019. Facebook alone made up around 3.5% of online giving, with much of it occurring on Giving Tuesday.

In addition to ramping up the ways people give to nonprofits, financial management has gone into the cloud. Rather than keeping a paper book, nearly every organization uses some type of accounting software and big data to track giving and donors and figure out ways to increase revenue from year to year.

Benefits of Teaming Up

There are numerous benefits to fintech and charity partnerships. While some are quite obvious, others are more subtle.

More Exposure

When two companies team up, they both gain access to one another’s customer lists. For example, if a business offers an online payment gateway and it teams up with a local charity, it might send out a press release. Simply gaining exposure may bring in more donations for the nonprofit.

They also will let their members know they are using a partner’s payment system. If the software is donated, the nonprofit will offer a thank you. Some of its patrons are likely business owners who may need services. By working together, the charity and company both expand their reach.

In a study by Omnicom Group’s Cone Communications, researchers found 83% of millennials felt loyal to companies helping them contribute to causes. A partnership helps both the fintech firm and the non-profit organization.

Financial Help

Some fintech companies throw their financial support behind an organization. They offer technology advantages and also come alongside them to raise money for the cause. Businesses should care about the purpose of the charity it supports. It should tie into the company’s philosophy and help advance its own goals. Any donations can likely be written off on taxes while helping a local group.

Testing Systems

Offering software at no cost allows businesses to try out new features and work through bugs. Part of the agreement can be that it provides the nonprofit with updates first, and they’ll report issues so the company can fix them. They get the program for free, and the business receives instant feedback on what works and what needs tweaking.

Better Tracking

Most fintech companies offer better tracking features for all types of businesses. Charities will be on top of where donor funds go and if they’re being used wisely. When people give to an organization, they expect them to be good stewards of that generosity. With the right programs, the nonprofit can run reports and know in an instant how money gets spent and if they are actually making the difference they promised.

Fintech Charity Partnerships Can Improve Performance

When it comes to making a difference in the world, improved performance enhances productivity and allows volunteers to do more than they ever thought possible. Technology allows people to stay on top of tasks and ensure cash flow is never an issue. By working together, fintech and nonprofits can make a huge difference in the lives of those they serve.

ShannonFlynn is a technology and culture writer with two plus years of experience writing about consumer trends and tech news.

You’ve finally perfected your digital transformation strategy that was accelerated because of 2020’s global pandemic. What should you focus on now? Here’s an idea: stablecoin transactions.

The U.S. Office of the Comptroller of the Currency (OCC) last week published Interpretive Letter 1174 detailing that banks may use stablecoins and independent node verification networks (INVNs) to facilitate payments for customers. That is to say, banks can transfer stablecoins to other banks.

To catch you up to speed, INVS are distributed ledgers. And stablecoins are a type of cryptocurrency that minimize volatility by pegging their value to an external factor.

There are a few key things this means for traditional financial institutions.

Transactions become decentralized

Stablecoin transactions are essentially decentralized cryptocurrency transactions. Because of this, they enable banks to send and receive money without a government intermediary.

Faster payments

Stablecoin transactions do not rely on traditional payments rails, rather, they utilize public blockchains. Because of this, stablecoins, just like other cryptocurrencies can be transferred in near-real time from one party to the next.

On 24/7

Once again citing freedom from traditional payment rails, because stablecoin transactions occur outside of the traditional payments infrastructure– and because they occur instantly– they can essentially be made at any time, including on the weekends and holidays.

Compliance is still on the table

According to the letter, stablecoin transactions, “should have the capability to obtain and verify the identity of all transacting parties, including those using unhosted wallets.” So banks are still responsible to adhere to KYC guidelines.

Additionally, banks using stablecoin transactions are responsible for managing the multiple risks associated with cryptocurrency transactions. Per the letter, “The stablecoin arrangement should have appropriate systems, controls, and practices in place to manage these risks, including to safeguard reserve assets. Strong reserve management practices include ensuring a 1:1 reserve ratio and adequate financial resources to absorb losses and meet liquidity needs.”

This is positive news not only because it offers banks more options, but also because it serves as a signal that the OCC and the Acting Comptroller of the Currency Brian Brooks are bullish on cryptocurrencies.

Pay attention to the cryptocurrency/stablecoin sector this year. We’re expecting to see significant developments in the decentralized finance area, and banks’ involvement in initial cryptocurrency efforts will be crucial. There will be little-to-no room for laggards in this space.

Data and analytics company Equifaxannounced its acquisition of digital identity player Kount this week. The deal, which is pending regulatory approval, is set to close for $640 million in the first quarter of this year.

Kount was founded in 2007 and offers a range of products and solutions, including chargeback protection, account takeover and bot protection, ecommerce fraud protection, and friendly fraud prevention. The company’s identity network, the Kount Identity Trust Global Network, leverages AI to link trust and fraud data from 32 billion digital interactions, 17 billion devices, and five billion annual transactions across 200 countries and territories.

All of Kount’s products will be integrated into Equifax’s Luminate Platform, a fraud platform that combines the company’s solutions with machine learning to give clients the information they need to make better decisions about fraud.

Kount has more than 9,000 clients across the globe, including Barclays, Staples, PetSmart, and Chase. Equifax anticipates the purchase will expand its global prevalence in digital identity and fraud prevention solutions.

“The acquisition of Kount will expand Equifax’s differentiated data assets to bring global businesses the information and solutions they need to establish identity trust online,” said Equifax CEO Mark W. Begor. “Equifax is taking advantage of our strong 2020 outperformance and cash generation to make this strategic acquisition. Our data and technology cloud investments allow us to quickly and aggressively integrate new data and analytics assets like Kount into our global capabilities and bring new market leading products and solutions to our customers.”

Kount employees will continue to work from the company’s headquarters location in Boise, Idaho, and will join Equifax’s U.S. workforce.

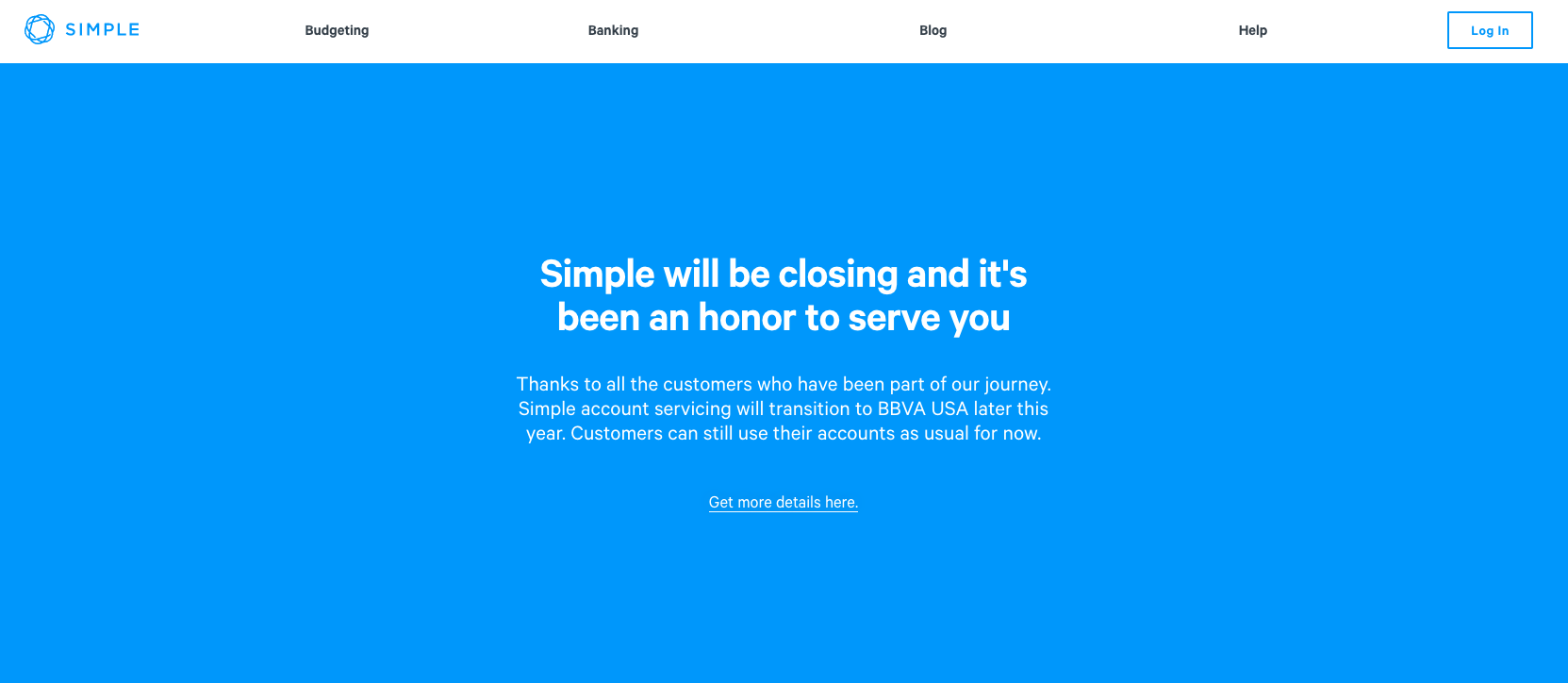

You’ve likely heard that BBVA has decided to shutterSimple, its in-house challenger bank. Yesterday, the company sent an email to accountholders stating, “BBVA USA has made the strategic decision to close Simple.”

The reactions across fintech are mixed– some say they’re not surprised, and others have expressed more nostalgia than anything.

Those who aren’t surprised cite PNC’s recent acquisition agreement with BBVA. The two may have been trying to streamline their businesses in order to minimize duplication of market coverage and services. There’s also the fact that competition in the challenger bank space is hotter than ever, and it doesn’t make sense for BBVA (or PNC, for that matter) to try to keep up with the marketing spend that others such as Chime have shelled out to acquire customers.

Since this is a eulogy, however, I’ll focus on the nostalgia. Simple was founded in 2009 as BankSimple and quickly became one of the top pioneers in the challenger banking space. I like to think of Simple as the grandfather of challenger banks (perhaps the grandmother is Moven, which closed its B2C model last year).

Simple was ahead of its time in focusing on the millennial client base that is untrusting of banks and prefers a straightforward, transparent approach. The bank also offered features that were unique at the time, such as geolocation via an integration with Google maps for every transaction, instant purchase notifications, and a “safe to spend” balance that indicated the user’s discretionary spending balance.

The bank’s young, Portland, Oregon-based staff were consistently quirky and upbeat on customer service phone calls. Simple maintained this culture even after BBVA acquired it in 2014.

Does anyone remember Simple’s catchphrase when it launched? “We don’t suck.” Hopefully the new generation of challenger banks will keep this mantra in mind as they work on creating the new wave of consumer-first banking technology.

As for what’s next, Simple’s email to clients went on to detail what to expect, stating, “In the future, your Simple account will become exclusively serviced by BBVA USA, but until then you can continue to access your account and your money through the Simple app or online at simple.com. You will receive additional information in the near future about the transition of your account servicing to BBVA USA.”

SaaS banking platform Mambu is even more prepared to support the banking-as-a service trend that’s sweeping the fintech industry. That’s because the Germany-based company received $135 million (€110 million) in new funding this week.

The investment was led by TCV, followed by new contributors Tiger Global and Arena Holdings and existing investors Bessemer Venture Partners, Runa Capital, and Acton Capital Partners. TCV General Partner, John Doran, will join Mambu’s board of directors.

The company also disclosed a new valuation of more than $2 billion (€1.7 billion), which places it in the fintech unicorn club (two-times over!).

Mambu will use the funds to accelerate growth and boost its presence across the globe. Specifically, the company announced intentions to deepen its footprint in Brazil, Japan, and the U.S.

“As an increasing number of challenger and established banks sign on to prepare themselves to thrive in the fintech era, we have, and will continue to provide them with a world-class platform on which to build modern, agile customer-centric businesses,” said Mambu CEO and Co-founder Eugene Danilkis. “This latest funding round allows us to accelerate our mission to make banking better for a billion people around the world and address one of the largest, most complex global market opportunities that’s still in the infancy of cloud.”

Mambu was founded in 2011 and emerged as one of the pioneering players to move banking software to the cloud. Since then, the company has seen success from its concept of composable banking that allows clients to build a banking experience to suit their needs without being tied to a specific vendor, product, or technology. This shift away from legacy core banking platforms, along with plug-and-play integrations, helps banks future-proof their systems to better serve their customers. Among Mambu’s customers are ABN AMRO, N26, OakNorth, Orange, and Santander.

Today’s news comes after a strong period of growth for Mambu. The company has seen around 100% YoY growth and is planning to support it by doubling its team to more than 1,000 by next year.