This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

The latest chapter in Bank of Charles Town’s digital transformation was written today. The West Virginia-based financial institution announced that it is collaborating with Jack Henry & Associates to digitize its commercial lending operations.

“We selected Jack Henry’s lending platform because it supports our broader digital banking strategy,” Bank of Charles Town (BCT) Vice President Anthony J. Ranghelli said. “The platform will help us grow with scale and efficiency while improving everyone’s experience. Our immediate goal for the next few years is to expand our digital lending footprint geographically to support businesses in neighboring communities and diversify our portfolio.”

Bank of Charles Town has spent the past few years investing in digital banking solutions, including a new website, digital wallets, and mobile deposit functionality. This week’s announcement will enable the FI to move away from the manual backend processes that have governed its previous loan origination system. The new technology from Jack Henry & Associates will bring new efficiencies, an improved customer experience, and streamlined workflow for employees. Ranghelli noted that the partnership will enable BCT to better serve its small and medium-sized business customers, especially “niche industries” such as dentist offices and law firms which he called “a priority for our bank.”

Founded in 1871 by a coalition of Jefferson County, West Virginia farmers and business leaders, Bank of Charles Town has grown into a $511 million-financial institution serving communities in the Eastern Panhandle of West Virginia; Loudon County, Virginia; and Washington County, Maryland. BCT was named a Best Bank to Work For by American Banker in 2020 for a second year in a row. Alice Frazier is President and CEO.

A Finovate alum since 2011, when the company showcased its ProfitStars division, Jack Henry & Associates finished 2021 with new partners and new functionalities for its solutions. The company announced a collaboration with Envestnet | Yodlee in December and also reported that its Jack Henry Lending platform, the centerpiece of its partnership with Bank of Charles Town, has been upgraded to include tax return spreading capabilities. This move will further reduce the amount of manual work that typically burdens the lending process and will accelerate the time to loan fulfillment.

Miss an episode of the Finovate Podcast during the holiday rush? No need to fear; the Finovate blog has got your back.

From insights into the rise of embedded finance and prospects for “technosocialism” to discussions with innovators in the field of personal finance and roboadvisory, the Finovate Podcast is your one-stop-shop for fascinating, in-depth conversations between Finovate VP Greg Palmer and fintech’s finest analysts and entrepreneurs. Today we’re sharing some end-of-year episodes of the podcast that might have slipped beneath your radar as 2021 drew to a close.

Chris Karageuzian, CEO and Co-founder, Help With My Loan. Host Greg Palmer and Chris Karageuzian talk about how the Finovate newcomer is making the lending process more pleasant for borrowers.

“I was in the industry for 20+ years so I felt the frustration – that’s why I left and created this company. (There’s a) lack of technology and fragmented software – you have to use almost seven to ten pieces of software just to deal with one file. That’s really not productive in my opinion. We closely work with banks right now. We have 300+ banks signed up in our database and in our software. So deals get automated and matched and we are within an earshot of every deal.”

Vivek Krishnamurthy, Principal, Commerce Ventures. Host Greg Palmer sits down with Vivek Krishnamurthy for a conversation on “embedded finance” and an overview of the field’s opportunities and pitfalls.

“There’s a split between the infrastructure layers that enable third parties to launch financial services products. And then there are the instances in which financial services products are launched inside of other ecosystems. We think that latter aspect, that latter space of being able to turn on a financial services product in the customer journey inside of a non-financial services ecosystem, that’s what we think about as ’embedded finance.'”

Ned Phillips, Founder and CEO, and Mike Larsen, Head of Sales, Bambu. Host Greg Palmer talks about the challenges facing the automated investment business with Ned Phillips and Mike Larsen of Best of Show winning roboadvisor Bambu.

“We are a B2B wealthtech. So what does that mean? We design, build, and deploy those roboadvisor, savings and investment apps for financial institutions. So if a financial institution wants its own Betterment or its own Wealthfront, they come to us for the tech and we build it. And at Finovate, we built one on stage in seven minutes!”

Will Graylin, Chairman and CEO, OV Loop; CEO, Indigo Technologies. Host Greg Palmer chats with serial entrepreneur Will Graylin about contactless payment adoption, super apps, and the future of mobile payments.

“Why haven’t we adopted (contactless payments) in much more mass given that Apple Pay has been out for over seven years, and Samsung Pay has been out for six years, and Google Pay has been out there for seven years – eight years now? Why haven’t we adopted en masse? (Our situation is) unlike China’s WeChat/WeChat Pay/AliPay. For those solutions, they are adopted to the order of about 83% of all consumer transactions, whereas we’re still in single digits in the United States. Why?”

Brett King, Author, The Rise of Technosocialism; Founder of Moven. Host Greg Palmer and Brett King talk about King’s latest book, The Rise of Technosocialism: How Inequality, AI, and Climate Will Usher in a New World.

“When you think about why it is that we haven’t been able to tackle (climate change) and get agreement on this, part of the core problem is that we tend to be quite short-term focused in our planning as a species. We’re focused on the next quarter, the next year, in terms of financial reporting, or maybe the next two years or four years in terms of political cycles. But when it comes to planning out things for 20 years in our future or 30 years in our future, the big problem is we just ask ‘who’s going to pay for it?'”

Lindsay Holden, Co-founder and CEO, Long Game. Host Greg Palmer discusses loyalty, education, Millennials, and gamification with Lindsay Holden, founder of FinovateFall Best of Show winner, Long Game.

“Long Game is a mobile game. It’s an app that sits on top of your bank account and rewards customers for learning about financial literacy and for positive financial behaviors like saving. For banks, we are helping them have a branded experience that’s super-fun for customers, they can acquire new customers with us, and also increase their customer LTV through promoting their products, increasing savings, and increasing direct deposits.”

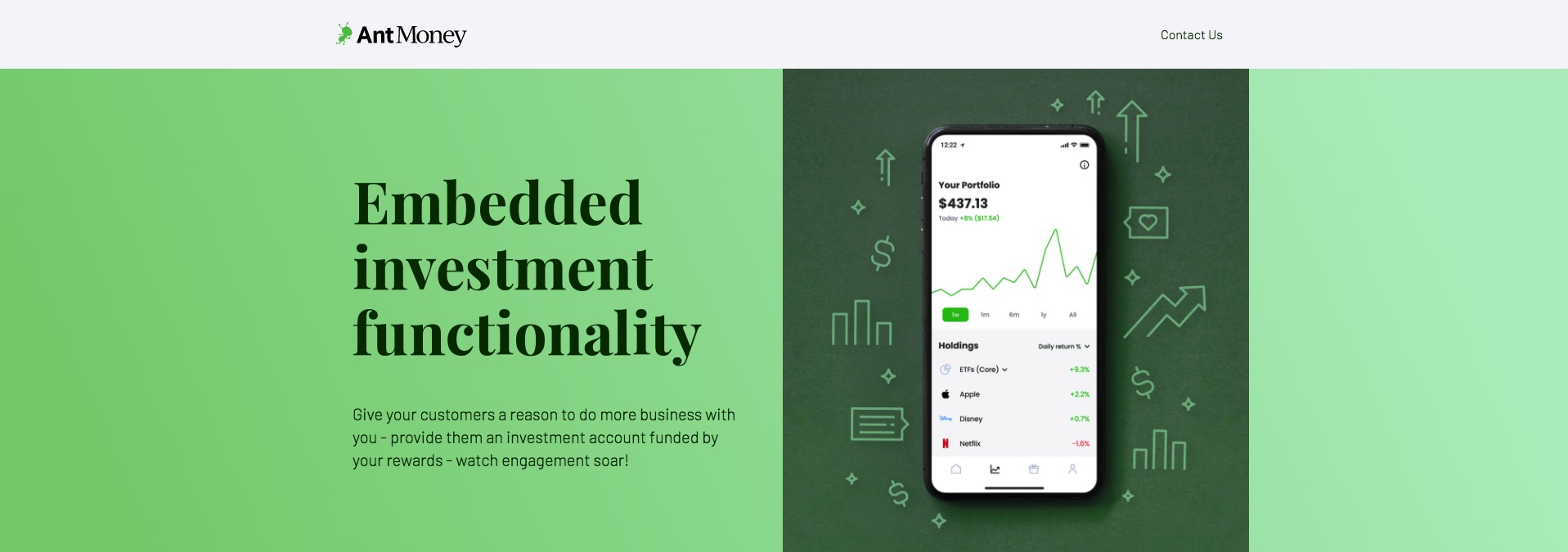

Embedded finance platform Ant Moneyhas secured $20 million in Series A funding. The round was led by Franklin Templeton’s Franklin Venture Partners, RX3 Ventures, SteelBridge Laboratories, Steelpoint Capital Partners, and Ant Money founder Walter Cruttenden. The company, whose founder also launched micro-investing platform Acorns in 2012, also completed its stock-for-stock merger with Blast. A financial services platform for gamers, Blast went live in 2018 with its Game-Based Savings technology that leverages gameplay as a way to help individuals passively fund a free savings account.

The deal brings the total number of apps on the Ant Money platform to three: ATM, Blast, and Learn & Earn. Together the trio of offerings enables users to earn money and easily fund investment accounts.

“Building an investment account early in life can help people on the road to financial success, but many people don’t start because they lack the knowledge or funds,” Ant Money’s Walter Cruttenden said. “My hope is that Ant Money, which helps people generate small amounts of money to seed accounts, can foster new growing accounts and provide increased financial security for millions.”

ATM enables users to earn micro-income by engaging anonymously with leading worldwide brands. That income can be saved or invested in the stock market via Ant Money Advisors, a registered investment company and robo advisor that is embedded in the ATM app. Users can earn a minimum of $10 for the first month of participation, and more than $100 a month afterwards if enrolled in the ATM rewards program. Learn & Earn was developed in partnership with Junior Achievement USA. The app helps users earn money by completing lessons on concepts like budgeting, launching a business, and the power of compound interest. The money earned from Learn & Earn, like the money earned via ATM, can be automatically invested in the stock market, enabling users to start saving for the future at the same time as they are learning how to be good investors.

Ant Money co-founder Michael Gleason said that the merger of the companies made sense because they shared “similar visions for helping people enter the financial investment world.” Combined with what Gleason called “overlapping management,” the companies seemed ripe for consolidation. “(It) seemed like the logical next step was to merge the companies and build a larger one together,” Gleason said.

Finovate alums notched their biggest fourth quarter fundraising since 2014, securing $1.2 billion in equity investment. The strong Q4 gives Finovate alums a 2021 fundraising total of $8.4 billion, more than double the capital raised in any previous year.

2021’s fundraising strength comes courtesy of $3.3 billion raised in Q1, $2.8 billion raised in Q2, and $1.1 billion raised in Q3. Fundraising in this year’s fourth quarter is also significantly higher than that raised in previous Q4s, and by a significant margin. The fact that Q4’s sizable fundraising totals came as a result of investments in only six alumni makes the current quarter’s accomplishment all the more remarkable.

Previous Quarterly Comparisons

Q4 2020: More than $472 million raised by 17 alums

Q4 2019: More than $876 million raised by 21 alums

Q4 2018: More than $800 million raised by 19 alums

Q4 2017: More than $730 million raised by 23 alums

Q4 2016: More than $700 million raised by 26 alums

Four of this quarter’s fundings were at or above the $200 million mark. This marks a first for Finovate alums. The biggest investment received in Q4 of 2021 was the $450 million secured by Socure, a fundraising total that has never been met by a Finovate alum in the final quarter of the year.

Top Quarterly Equity Investments

Socure: $450 million

Zopa: $304 million

Mambu: $266 million

Thought Machine: $200 million

Here is our detailed alum funding report for Q4 2021.

October 2021: More than $329 million raised by two alums

If you are a Finovate alum that raised money in the fourth quarter of 2021, and do not see your company listed, please drop us a note at [email protected]. We would love to share the good news! Funding received prior to becoming an alum not included.

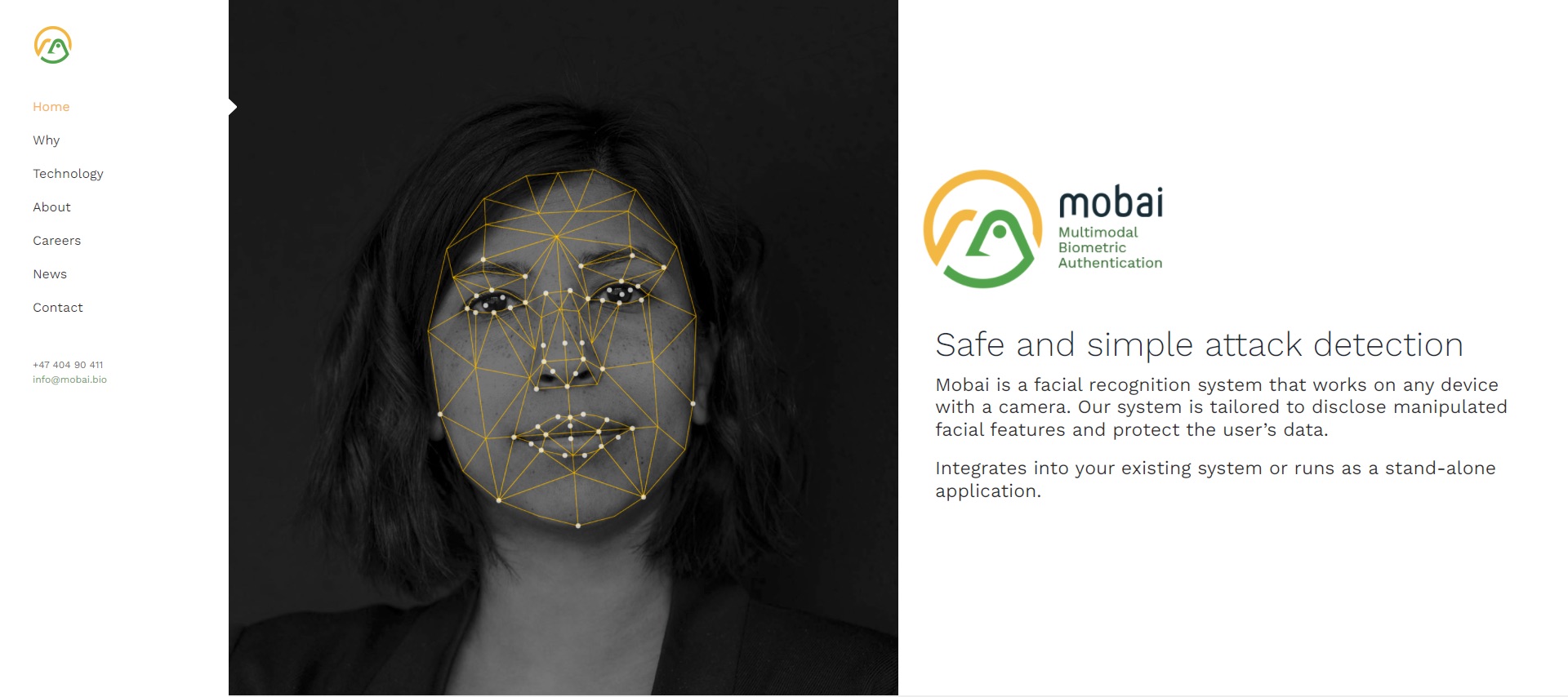

Norway-based biometric startup Mobaiwon $3.16 million (EUR 2.8 million) in funding to enhance the protection of personal biometric data in coalition with Vipps BankID, Sparebank1 Østlandet, KU Leuven, and NTNU. The project, named SALT for “Secure privacy preserving Authentication using faciaL biometrics to proTect your identity,” will bring new functionalities to Mobai’s facial recognition solution, and improve the quality of the technology to help firms meet eiDAS and AML regulations.

The project will drive innovation in the field of facial biometrics, particularly in the areas of biometric template protection, face quality assessment, and presentation attack detection. Mobai CEO Brage Strand noted in a statement that innovation in facial biometrics is especially urgent insofar as vulnerabilities in current authentication strategies such as passwords and even two-factor authentication increasingly have been exploited by fraudsters and cybercriminals.

“Our aim is to offer consumers a unique opportunity to prove who they are, as a way to combat the surge in phishing and identity theft we currently experience,” Strand said. He added the goal of the project was to move “beyond comparing a photo you store on a device with a selfie” to bring the same level of trust found in ePassports “into a digital domain.” Strand also emphasized the importance of leveraging “privacy-preserving technology” to ensure GDPR compliance and the integrity of personally identifiable information.

Mobai’s partners represent an interesting cross-section of the country’s financial services industry. Sparebank1 Østlandet is the fourth largest savings bank in Norway. Vipps is a payments and electronic ID provider with more than four million electronic ID users. NTNU is the Norwegian University of Science and Technology, the largest university in the country with more than 40,000 students; Mobai was spun out of NTNU’s Norwegian Biometrics Laboratory in 2019. Katholieke Universiteit Leuven is a research and educational institution, one of the oldest universities in Europe, with a reputation for pioneering scientific research.

“We see face recognition as a very promising and effective way to add an extra layer of security that will help combat identity theft, fraud, and money laundering,” Sparebank1 Østlandet EVP for Innovation and Business Development Dag Arne Hoberg said. “Imagine a situation where you may actually sign a mortgage electronically and use a ‘selfie’ as part of this process to confirm that your are the right person to sign.”

Meanwhile, in nearby Denmark, leading business automation software and services provider Visma announced its acquisition of expense management company Acubiz. Term of the transaction were not immediately available.

Visma will integrate Acubiz’s expense management solution into its Visma Enterprise HRM, but Acubiz will continue to function as an independent brand. The company, which has a 20% market share in Denmark and more than 200,000 users, offers solutions to help businesses better manage employee and travel expenses, as well as mileage reimbursement, invoice management, and time registration.

“I am excited to welcome another strong, Danish company into the Visma family,” Visma Enterprise A/S Managing Director Monika Juul Henriksen said. “There is no doubt that Acubiz is a perfect match not only businesswise but also in their culture and DNA. Acubiz wants to be the best – and so do we. Together, we will be even better.”

Founded in 1997 by Lars de Nully, Acubiz is based in Birkerød north of Copenhagen. This year, the company has forged partnerships with accounting firms Tal & Tanker and Tietotili, as well as with financial administration services provider Fiscales, HR software company Sympa, and Jutlander Bank.

In a year-end statement published on the Acubiz blog, the company noted that, in addition to its acquisition by Visma, it plans to unveil a new financial interface in 2022. The new UI will feature upgrades in performance, user-friendliness, and the ability to customize.

“By becoming a part of Visma, we do not only get a shortcut to new customers, markets, segments, and partners, we will also benefit from the knowledge and skills within legal, HR, marketing, and sales,” Acubiz Managing Director Henrik Malling said. “Being able to counsel with these experts is immensely valuable for us as a relatively small organization. So we honestly cannot wait to get started and to get to know all our new colleagues within Visma.”

FinovateEurope 2022 is right around the corner. If you are an innovative fintech company with new technology to show, then there’s no better time than now and no better forum than FinovateEurope. To learn more about how to demo your latest innovation at FinovateEurope 2022 in London, March 22-23, visit our FinovateEurope hub today!

Here is our look at fintech innovation around the world.

Narrative Science reported on Wednesday that its acquisition by Salesforce – and integration into Saleforce’s Tableau team is complete. First announced last month, the closing of the acquisition this week will combine Narrative Science’s automated data storytelling capabilities with Tableau’s analytics platform.

“Bringing the Narrative Science award-winning, world-leading AI in analytics team and their innovations to Tableau will help us reach millions more people who are underserved with data,” Tableau President and CEO Mark Nelson wrote on the company’s blog this week. “It will help close the data literacy gap, reimagine an entirely new analytics experience, and set people up for success in this digital-first world.”

Salesforce acquired Tableau Software in 2019 in a deal that combined “the world’s #1 CRM with the world’s #1 analytics platform” Tableau announced in a press release that August. The goal of the acquisition was to enable Salesforce customers to “unlock even greater value from their data” using Tableau’s combination of diverse visualization, analytics, and AI. By adding Narrative Science’s data storytelling technology, Tableau and Narrative Science move closer to their shared goal of “making data more available to everyone, everywhere.”

A Finovate alum since 2013, Narrative Science is a leading provider of automated business analytics and natural language communication technology. Founded in 2010 and headquartered in Chicago, Illinois, the company is an innovator in the field of data storytelling. As a strategy for delivering business intelligence, data storytelling transcends both data visualization and static dashboards by translating insights into easy-to-understand stories and giving business users a personalized data digest. The company’s Lexio solution, its latest iteration unveiled in the fall of 2020, serves both businesspeople who require data insights in order to do their jobs, but do not have the time or skills to become data analysts, as well as leaders of analytics teams who need to ensure that insights are accessible to and understandable by employees who can translate them into action.

“Unlike today’s typical BI tools, Lexio anticipates what employees need to know so they can make faster and better data-driven decisions,” Narrative Science co-founder and CEO Stuart Frankel said. “Data without context is useless, and Lexio brings that context and understanding to every single employee in plain language and in a consumer-like experience.”

As of this fall, Narrative Science has raised nearly $43 million in funding from investors including Jump Capital, Sapphire, and Battery Ventures. In October, the company earned a #1 ranking in Crain’s Chicago Business Most Innovative Companies 2021 roster. Over the summer, Narrative Science’s Lexio won the “AI-Based Analytics Innovation Award” at the AI Breakthrough Awards.

A partnership between cloud-based digital banking solution provider Alkami Technology and Idaho Central Credit Union will enable ICCU members to buy and sell bitcoin within their mobile apps and on the credit union’s online banking platform. Bitcoin services are provided by cryptocurrency technology company NYDIG with Alkami’s platform facilitating the deployment.

Claiming the mantle of both the fastest growing credit union in the state, as well as one of the best performing credit unions in the country, ICCU Chief Information Officer Mark Willden said that adding new services such as bitcoin investing are key to ensuring that the credit union maintains its “momentum” and “deliver(s) additional value.” He added, “Fully integrated bitcoin services through NYDIG and the Alkami Platform take us to the next level when it comes to the member experience.”

Idaho Central Credit Union was founded in 1940 and serves more than 480,000 members throughout the state. With 1,600+ employees, ICCU has more than $8 billion in assets.

NYDIG works with Alkami to allow financial institutions to offer their customers and members bitcoin services in a secure and compliant way. NYDIG joined Alkami’s Gold Partner Program over the summer, making it easier for financial institutions to add bitcoin products and services to their offerings and provide them to their customers and members under their own brand.

“The demand for and utilization of digital currencies have expanded exponentially in recent months, leaving many FIs struggling to keep pace and retain these deposit streams within their institution,” Alkami Chief Strategy & Sales Officer Stephen Bohanon said. “Alkami’s partnershp with NYDIG further supports our mission to enable FIs to compete directly against the megabanks and challenger banks to capture this valuable market.”

A Finovate alum since 2009, making its Finovate debut as iThryv, Alkami has grown into a leading cloud-based digital banking solution provider with more than 280 financial institution customers. The company went public this spring, earning a market capitalization of $3.4 billion in its debut on the NASDAQ. Trading under the ticker ALKT.O, the Plano, Texas-based firm raised $180 million in its IPO.

Since its public listing, Alkami has forged a number of partnerships with financial institutions including STAR Bank in November and MainStreet Bank in October. Also this fall, the company announced its acquisition of digital account opening and loan origination provider MK Decision and introduced its new Chief Executive Officer Alex Shootman, formerly the CEO of Workfront. Alkami Board of Directors Chairperson Brian R. Smith said Shootman’s experience in “growing and scaling enterprise software companies” was “essential at this stage of Alkami.”

Today’s announcement from Idaho Central CU comes as NYDIG reports a massive $1 billion growth equity round that gives the company a valuation of $7 billion. The round was led by WestCap and featured participation from Bessemer Venture Partners, FinTech Collective, Affirm, FIS, Fiserv, MassMutual, Morgan Stanley, and New York Life.

The New York-based company now has a total capital of $1.4 billion. The new investment will help NYDIG further develop its platform, taking advantage of recent changes to the bitcoin protocol to introduce functionalities such as bitcoin and lightning payments, asset tokenization, and smart contracts. The company will also use the new funding to add talent to its team worldwide.

“Our roster of partnerships and strategic investors lays the foundation for NYDIG to become the leading provider of Bitcoin solutions for businesses in any industry,” NYDIG co-founder and CEO Robert Gutmann said. “(This) new equity capital will further accelerate progress towards making this exciting network accessible – and useful – to all.”

One month after introducing its next generation development application platform, OutSystems has announced that it is entering a strategic partnership with fellow Finovate alum ieDigital. The alliance will enable ieDigital’s financial services company partners – ranging from bank to mortgage lenders – to access a suite of pre-built, low-code applications that support a variety of operations including originations, self-servicing, retention, and collections.

The goal of the new relationship is to give financial service providers new resources that will help accelerate growth, become more cost-efficient, and better manage risk. The partnership also allows for additional functionalities to be added as part of broader, future digital transformation efforts. One example of this would be enabling companies to analyze data collected during the completion of online applications for a new financial product or service.

“By pioneering the low-code market and having a vision to transform how enterprise software is delivered,” ieDigital Commercial Director Garry Larner said, “the OutSystems platform perfectly complements our existing product-offering. We look forward to working alongside them to continue delivering market-leading financial technology that makes a real impact to all that use it.”

ieDigital noted that the partnership will leverage and further build upon the Interact Application Suite, an approach ieDigital used in a previous collaboration with Cambridge & Counties Bank to help the firm combat financial crime. The result was a more streamlined customer onboarding process, enhanced automation for both middle and back office workers, and better capacity and knowledge to support the development of applications going forward – including an option for Cambridge & Counties Bank to build its own in-house development capability.

Founded in 1984 and headquartered in London, U.K., ieDigital demonstrated its Money Fitness solution at FinovateFall 2018. The technology helps credit unions effectively compete with the wave of competition from “digital-first” providers with a forward-looking personalized service that credit union members can use to better manage their day-to-day finances, make better financial decisions, and improve their overall financial health.

More recently, ieDigital launched its customer retention solution Interact Switch, which is designed to help mortgage lenders retain customers at product offer maturity. The technology enables mortgage lenders to function more efficiently by cutting down on paper-based, mortgage representative, and third-party costs. Also this fall, ieDigital announced a partnership with Darlington Building Society and a collaboration with DF Capital to help the savings and commercial lending bank to launch a new digital interactive channel for its savings customers.

An alum of our developers conference, FinDEVr NewYork 2017, Boston, Massachusetts OutSystems specializes in cloud-native, low-code app development. More than 14 million people currently use OutSystems’s platform to build solutions such as mobile apps and consumer websites, as well as extensions of core systems from Microsoft and Salesforce. The latest platform edition from the company, code named Project Neo, marries the productivity benefits of visual, model-based development with state-of-the-art container- and Kubernetes-based cloud architecture. The technology is hosted on Amazon Web Services to make it easy for any company to build customized, cloud-based apps that scale globally and can be continuously updated.

“Developers should be the artisans of innovation in their organization, but they are mired in complexity that stifles their ability to innovative and differentiate,” OutSystems CEO Paulo Rosado said. “Instead of using their talents to fix, change, and maintain code and aging systems, you can give them industry-leading tools that unleash their creativity on your business, and achieve massive competitive advantage.”

The announcement that global identity verification specialist Trulioo has signed up a sextet of cryptocurrency companies as its latest round of customers is a testament to the growing maturity of startups in the digital asset business. The six firms – Centbee, GMO Trust, Omni Matrix, Skilling, Strike Protocols, and Vintech Capital – will use Trulioo’s GlobalGateway to enable them to meet KYC and AML compliance requirements.

“The pandemic democratized the world of financial services, helping casual or novice investors explore financial trading online,” Trulioo CEO Steve Munford explained. “With cryptocurrencies becoming mainstream, digital asset issuers and exchanges understood the need to bolster their identity verification programs to securely and seamlessly onboard a huge uptick in users while meeting compliance obligations.”

Trulioo’s GlobalGateway gives companies access to more than 400 data sources to confidently and securely verify the identities of more than five billion individuals worldwide via a single API. The platform provides identity verification with real time comprehensive match results, ID document verification using intuitive image capture and automated verification technology, and AML (anti-money laundering) watchlists with extensive international coverage. This coverage includes sanction lists from law enforcement and government regulatory entities such as financial and securities commissions.

The solution also provides Business Verification, which Trulioo demonstrated during its most recent appearance on the Finovate stage last year at FinovateEurope in Berlin, Germany. At the conference, the company demonstrated its GlobalGateway Business Verification technology which provides regulated entities with certainty about their business customers and assures compliance with Customer Due Diligence (CDD) requirements. Leveraging key company data from government sources in more than 80 countries and from non-government sources in more than 195 countries, GlobalGateway Business Verification automates the complete Know Your Business workflow, enabling companies to verify business entity data, conduct watchlists reviews, and identify and verify a business’ beneficial owners.

Founded in 2011 and headquartered in Vancouver, British Columbia, Canada, Trulioo has raised more than $474 million in funding. The company’s most recent fundraising was a Series D investment in June of this year that added $394 million to the firm’s coffers. The round was led by TCV.

At a time when concerns about illegal immigration have complicated the mostly positive attitude most Americans have toward immigrants in general, it is heartening to see that innovators and entrepreneurs in the fintech space are finding ways to bring vital services to those fleeing often-horrific conditions to find better lives in another land.

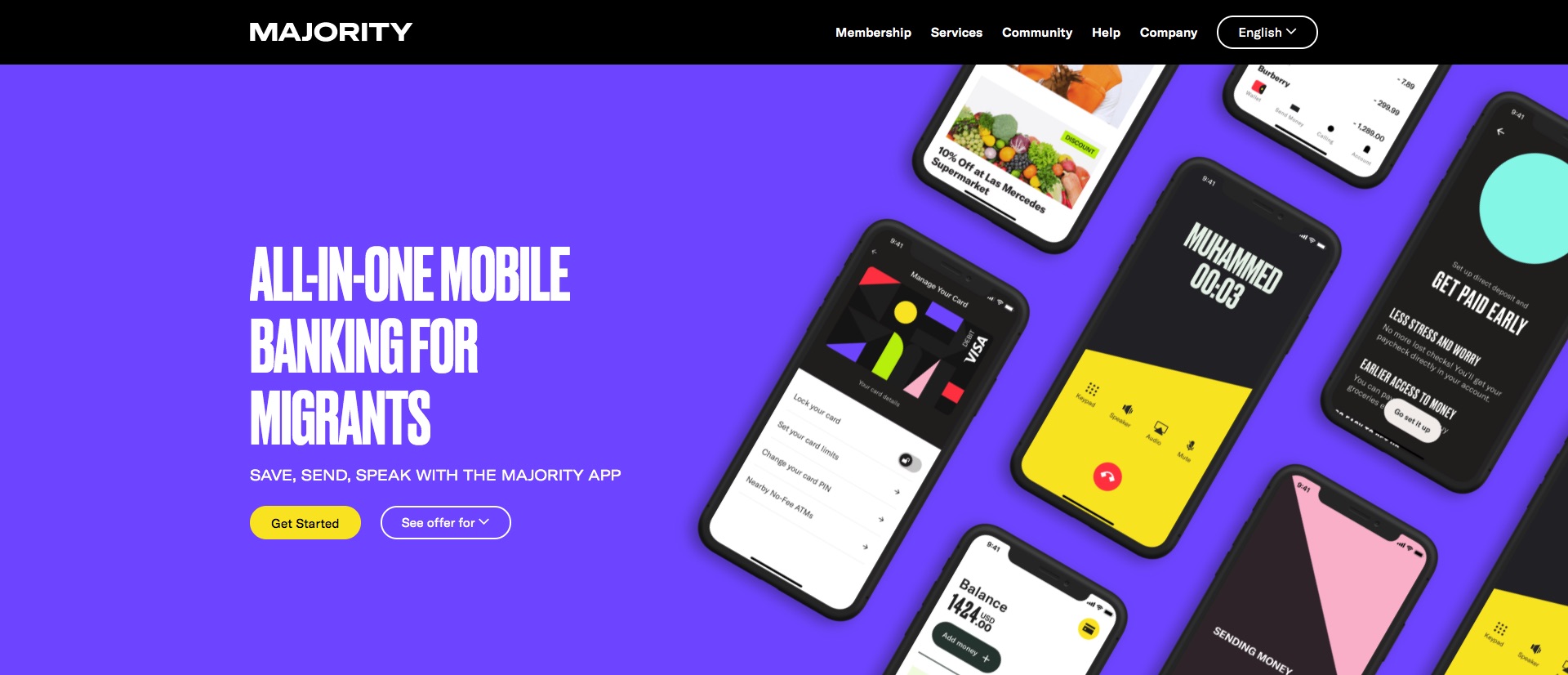

One such company is MAJORITY, a U.S.-based, mobile banking service designed specifically to serve the migrant communities in the States.

Founded in 2019, MAJORITY offers a banking app that provides an no-overdraft-fee, FDIC-insured bank account, a debit card with community discounts from local merchants, no-fee remittances, and “at-cost” international calling. The app is available for $5 a month. Company founder and CEO Magnus Larsson said that MAJORITY already has saved its Cuban members $21 a month on average and its Nigerian members $10 a month on average thanks to its “cost-efficient service offerings.”

MAJORITY also offers members the services of its hundreds of local advisors who help onboard and support new customers in their native languages. And while MAJORITY’s banking services are available in all 50 states, the company’s advisors are currently operating only in Texas and Florida.

Larsson explained the utility of the company’s human advisors in a conversation with TechCrunch. He described how a MAJORITY customer could meet up with an advisor outside of a grocery store and, within minutes, have their bank information, a Visa debit card, and the ability to use that grocery store to send money to another country.

“Migrants, by their very definition, are the most ambitious people in the world, striving for success in a new country – but they are lacking the necessary tools,” Larsson said. “Migrant-relevant financial services come with extensive fees that feel overwhelming for all people, but even more intimidating for those trying to navigate an unfamiliar system. At MAJORITY, we seek to remove the uncertainty that comes with international financial services and do our part to better facilitate a world where people are valued on their positive impact, not their country of origin.”

MAJORITY estimates that there are more than 258 million migrants worldwide, with nearly 50 million migrants in the U.S. – who are under-banked, un-banked, or otherwise experiencing “insurmountable barriers” when it comes to financially integrating into their new country. And courtesy of a $27 million investment MAJORITY announced last week, the company now has new resources to help.

“Our mission, as a migrant-led company, has always been to serve the migrant communities with the unique resources they need—financial and otherwise—and this latest funding will help us continue to perfect our services and support this community that is the backbone of America,” Larsson said.

The Series A round was led by Valar Ventures and featured the participation of Avid Ventures, Heartcore Capital, and a number of Nordic fintech founders. MAJORITY now has $46 million in total funding, which includes $19 million in seed funding the company raised earlier this year.

Accompanying its funding news, MAJORITY also announced that it is introducing a new feature that will enable migrants to sign up for a bank account without requiring a social security number. Instead, applicants will be able to use a government ID from any other country and proof of U.S. residency to access MAJORITY’s banking services.

“A bank account is the starting point to so many other things for someone moving to a new country, and American bureaucratic delays and backup shouldn’t prevent people from being able to establish themselves here,” Larsson said. An immigrant himself from Sweden, Larsson is currently waiting for visa approval in order to move from Stockholm to Miami, Florida, to further build out MAJORITY. He also looks forward to being able to grow the company from its current 65+ employees in Sweden and the U.S.

Supply chain finance company Tradeshift has raised more than $200 million in combined equity and debt funding. The San Francisco, California-based firm, which made its Finovate debut in 2012 at FinovateEurope, now has an estimated valuation of $2 billion according to Reuters. Tradeshift CEO and founder Christian Lanng, who did not confirm the valuation with Reuters, did tell the company that the new funding will help Tradeshift “refinance parts of our balance sheet focusing us on long term continued growth.”

The investment featured participation from Koch Industries, IDC Ventures, LUN Partners, Private Shares, and Fuel Capital. According to Crunchbase, the investment gives Tradeshift more than $1 billion in equity funding.

Founded in 2010, Tradeshift has become a leading B2B e-invoicing and accounts payable automation company. With more than 1.5 million companies connected on its platform, Tradeshift has processed more than $1 trillion in cumulative value since inception, a figure that has doubled in two years. The company’s offerings include its B2B marketplace for e-procurement Tradeshift Buy, its automated accounts payable platformTradeshift Pay, a supplier analytics solution Tradeshift Engage, early payment option Tradeshift Cash, and its virtual credit card offering Tradeshift Go.

By hosting all of these features on a single trade technology platform, Tradeshift enables businesses to transition from being “future proof” to “future flexible,” and to scale their operations virtually without limit. An early adherent of the value of embedded technologies, Tradeshift empowers companies to “continually digitize” their supply chain and take advantage of a dynamic, digital network of connected buyers and sellers.

“Embedding financial services directly into our product unclogs the flow of working capital across supply chains, eliminating a significant pressure point in the buyer-suppliers relationship,” Lanng explained. “As one of the first companies to recognize the potential for embedded finance in SaaS, we have been betting on the convergence of Fintech and SaaS products for awhile. We’ve built the technology and distribution channels to capitalize on what is now one of the defining trends in our industry.”

Named to Fast Company’s list of the World’s Most Innovative Companies for 2020, Tradeshift launched its cross-border e-invoicing solution last month, reducing friction in cross-border transaction flows for companies doing business in China. In October, the company announced that its Tradeshift Go virtual credit card solution was on track to process $2.5 billion in charge volume in 2021, a 6x increase over 2020. Tradeshift has forged partnerships this year with the Danish Export Credit Agency, trade and supply chain financing platform Raindew Trade, and Qatar-based Gulf Warehousing Company (GWC).

Selling nearly 290 million shares priced at $9 in its initial public offering on the New York Stock Exchange this week, Brazilian digital bank Nubank has raised $2.6 billion, reaching a market value of $41 billion. An alumni of Finovate’s developer’s conference FinDEVr in 2016, Nubank is now the most valuable financial institution in Latin America in addition to being the world’s biggest digital bank. CEO David Vélez, who co-founded the company in 2013 with an initial investment of $2 million from Sequoia Capital and Kaszek Ventures, now owns a stake in the company worth $8.9 billion at the IPO price.

“We don’t think the banking branch will survive the way it is,” Vélez said to CNBC this week. “It is too costly to serve the majority of users, especially in emerging markets where you have a very high cost of operations, so a lot of that physical infrastructure will probably disappear.” Vélez predicted that most financial services providers will transition into digital entities in the next five to ten years because of this, leading to an increased focus on customer service as well as lower costs and interest rates.

With more than 48 million customers in Brazil, Mexico, and Colombia, and onboarding more than two million new customers a month on average, Nubank offers financial products for spending, savings, investments, loans, and insurance. The company claims to have provided more than five million people with their first credit card or bank account as of September 30, and to have saved its customers more than $4 billion (R$27 billion) in bank fees and more than 113 million hours of waiting time since inception.

Vélez said that the capital from the IPO will help fuel Nubank’s expansion in Mexico and Colombia, en route to becoming a truly pan-Latin American banking services provider. “There is a lot of opportunity to build the next generation of financial services, so we will continue to invest and grow for a very long time,” Vélez said an interview with the Financial Times.

FinovateEurope 2022 is right around the corner. If you are an innovative fintech company with new technology to show, then there’s no better time than now and no better forum than FinovateEurope. To learn more about how to demo your latest innovation at FinovateEurope 2022 in London, March 22-23, visit our FinovateEurope hub today!

Here is our look at fintech innovation around the world.

CinetPay, a digital finance platform serving merchants in French-speaking Africa secured $2.4 million in seed funding from 4DX Ventures and Flutterwave.

Online fraud prevention company SEON inked an agreement with a pair of African neobanks, Carbon and FairMoney.

South African device identity and authentication solutions provider Entersektannounced a “significant investment” from U.S. private equity firm Accel-KKR.

German biometrics and digital identity verification company Passbase secured $10 million in Series A funding, as well as another $3.5 million in seed-2 investment.