This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Courtesy of an investment from Thoma Bravo, personalization and customer-engagement solution provider for financial services companies Personetics has raised $85 million in growth funding. Updated valuation information was not disclosed.

Calling data-driven personalization and customer engagement “the battleground for financial institutions” worldwide, Personetics CEO and co-founder David Sosna said that banks and financial services providers are rightly moving toward a more proactive relationship with their customers. “Personetics provides financial institutions with the most comprehensive engagement platform on the market, enabling agility and differentiation with an agile delivery for quick business impact,” Sosna said.

Personetics’ technology boosts customer engagement by analyzing financial data in real-time, learning financial behaviors, anticipating needs, and then acting on the user’s behalf. The company’s enriched data, actionable insights, financial advice, and automated wellness solutions can be used by retail banks, small businesses, wealth management firms and others to increase digital customer engagement by as much as 35%, account and balance growth of 20%, and realize gains of 17% in the adoption of personalized recommendations and advice.

Making its Finovate debut in 2016 at FinovateEurope in London, Personetics raised more than $160 million in funding last year from investors including Viola Ventures, Lightspeed Ventures, Sequoia Capital, Nyca Partners, and Warburg Pincus. In the fall of 2021, the company announced a partnership with Europe-based financial services group KBC to increase customer engagement on the firm’s mobile app. Last spring, Personetics unveiled its patented, automated cash-flow based savings solution – Pay Yourself First – which has been integrated into U.S. Bank’s mobile app. Note that U.S. Bank won Best Customer Experience at the Finovate awards in 2019 for its mobile banking technology.

“Personetics’ PYF intelligent algorithms take the guesswork out of setting money aside for saving or investing and acts on behalf of customers,” Personetics President for Americas Jody Bhagat said. “It’s another example of how Personetics is helping financial institutions deliver hyper-personalized solutions for their customers, and bringing to reality its vision of Self-Driving Finance.”

FinovateFall Best of Show winner SpyCloud has launched its latest solution to combat online fraud. The SpyCloud Identity Risk Engine, unveiled this week, analyzes billions of data recaptured from the dark web to help businesses and financial institutions make faster, more accurate, real-time fraud mitigation decisions.

What’s unique about SpyCloud’s approach to fighting fraud is the company’s focus on identifying credentials that have been exposed during data breaches and are actively being traded in the criminal underground. These exposed credentials are sold to fraudsters on the black market or used by the hackers themselves to steal confidential information, access secure systems, or commit fraud. Because many of these sources of stolen credentials cannot be readily accessed by automated software tools or web crawlers, SpyCloud uses a combination of technical innovation and human intelligence to find and recapture data from online criminal communities. The company also gives businesses and financial institutions access to the kind of authentication systems that will help defend them against cyberattacks that leverage stolen credentials such as account takeover (ATO), identity fraud, and new account fraud.

With the release of its SpyCloud Identity Risk Engine, SpyCloud gives businesses in financial and ecommerce services actionable, predictive fraud risk assessments based on breach data and stolen credentials that have been recaptured from the dark web. The technology combats difficult-to-detect challenges including data harvested by malware and the use of synthetic identities. SpyCloud Identity Risk Engine also gives businesses insight into which customers have the highest risk of account takeover due to risk factors such as exposed credentials or weak password protocols.

Businesses place the Identity Risk Engine at their most critical points of potential fraud (i.e., at account opening, login, transactions, etc.). From there, all that is required is an API query using an email address or phone number. SpyCloud then scans billions of recaptured data points to deliver a risk score that enables businesses to make more accurate fraud decisions. SpyCloud has recaptured more than 145 billion breached assets, more than 30 billion email addresses, and more than 25 billion total passwords. The company’s technology collects 50+ breach sources every week.

Winner of Built In Austin’s Best Places to Work for a second year in a row, SpyCloud was founded in 2016 and made its Finovate debut one year later. The company was featured in Fast Company’s inaugural Next Big Things in Tech roster last fall and, in October, SpyCloud announced a partnership with Houston, Texas-based identity and access management solution provider Identity Automation to help schools fight ransomware threats.

“Preventing ransomware is possible by negating the top attack vector: credentials that have been exposed in data breaches,” SpyCloud SVP of Business Development Cassio Mello explained. “This service gives schools early identification of compromised accounts, enabling them to take action quickly and prevent cyber attacks that leverage recently-breached identity data.”

SpyCloud has raised $58.5 million in funding from investors including Centana Growth Partners, Microsoft’s Venture Fund M12, March Capital, and Silverton Partners. Ted Ross is co-founder and CEO.

Digital investment services and infrastructure company WealthKernelsecured $7 million in Series A+ funding to start the week. The round was led by XTX Ventures and featured participation from Digital Horizon, Big Start Ventures, and ETFS Capital. The U.K.-based company said that it will use the capital to fuel expansion across Europe.

“I’m incredibly excited to take this next step in WealthKernel’s journey,” WealthKernel CEO Karan Shanmugarajah said. “Our investors’ backing will not only help us bring our product to a wider audience and expand our platform, but also achieve our goal of becoming the leading provider of API-based wealth and investment infrastructure across Europe.”

WealthKernel offers businesses the building blocks they need to power their digital investment offering. From client onboarding and trading to portfolio management and custody, WealthKernel enables neobanks, roboadvisors, PFM apps, and embedded finance platforms to focus on building their brand and customer experience while leaving the heavy lifting to WealthKernel’s all-in-one investing API.

“We often describe what we do as the plumbing for wealth management companies,” Shanmugarajah explained. “The current industry is built on leaky legacy pipes and that leakage directly impacts the savings and pensions of millions of people, particularly those with smaller sums of money. Our mission is to enable the change that makes financial services and investing better for everyday people.”

This week’s Series A+ round is an extension of the company’s $6 million Series A round from 2020. In addition to supporting the company’s growth plans in Europe, the funding will enable WealthKernel to expand its investing infrastructure to accommodate intraday trading, as well. The company currently has $13.9 million in total equity funding according to Crunchbase.

A leading embedded investing solution provider in the U.K., WealthKernel’s platform supports more than 100,000 transactions a month, and more than 72,000 trades per month are executed using its technology. The company’s clients include U.K.-based financial coaching app Claro Money, Sharia-compliant ethical investment platform Wahed, and wealth management service provider Rosecut. More recently, WealthKernel has forged partnerships with GOODFOLIO, an ESG-based investment platform, and investment app Stratiphy, which offers personalized investment and trading strategies. WealthKernel was founded in 2015.

Latin American payments company EBANX is doubling down on its commitment to its business in Mexico, opening its first office in Mexico City and introducing a range of solutions designed to help Mexican companies offer new payment experiences for their customers in-country. These solutions include credit and debit cards, installments, OXXO and OXXOPay, SPEI, and digital wallets like Mercado Pago.

“The launch of these local solutions and the opening of the new office are part of our strategy for continuous growth in Mexico, a country where e-commerce is one of the most dynamic and relevant sectors,” EBANX co-founder and CEO João Del Valle said. “With these new initiatives, we became the ideal strategic ally to help e-merchants grow their operations in Mexico or other LatAm markets.”

For EBANX, bringing broader payment options to Mexican consumers is a way to better serve the country’s unbanked population. According to the Association of Mexican Banks, 53% of Mexican adults not have a bank account as of 2020. At the same time, the company’s own study on digital commerce in Mexico revealed that as much as 60% of the digital commerce in Mexico is conducted using payment methods ranging from digital wallets and cash vouchers to debit and credit cards. By enabling more merchants in Mexico to process both cash-based transactions as well as these methods preferred in digital commerce, EBANX believes it can help merchants in the country increase their reach and sales potential by 2x and increase their total addressable market faster.

Founded in 2012 and headquartered in Curitiba, Brazil, EBANX has been active in the Mexican market since 2015. Last year, the company grew the number of transactions processed in Mexico by 115%. Hibobi, SHEIN, Shopee, and Wish are among EBANX biggest customers in the country.

The acquisition is slated to take place in two parts. First, Itaú will acquire 50.1% of the share capital of Ideal, which was founded in 2019 and is one of the leaders in traded volume on the Brazilian stock exchange, B3. Second, the bank plans to execute its right to purchase the remaining 49.9% of the brokerage’s shares for approximately $117 million (R$651 million) securing control of the company. Stage two of the acquisition plan is reportedly not scheduled to take place for another five years.

“This investment materializes our mantra of client centrality because they are the ones who will get the most out of the transaction,” Itaú Unibanco president Milton Maluhy Filho said. “Ideal is going to help us expand and standardize the offer for different channels. Customers from various segments of the bank, such as iti, ion, or even Itaú Corretora, will be able to have access to the same products on whichever platform they prefer.”

The acquisition will add to the talent base for the 60-million customer financial institution, which bills itself as a digital bank with the convenience of physical banking. Ideal CEO Nilson Monteiro will continue to oversee operations at the company with Itaú serving essentially as one of Ideal’s financial institution clients. Itaú Unibanco’s Carlos Constantini, who runs Wealth Management and Services for the bank, underscored the importance of maintaining Ideal’s autonomy, citing the company’s market position and “well-defined strategy for its segment of activity.” Constantini added, “the company will play an important role in consolidating Itaú Unibanco’s investment ecosystem and maintaining our market leadership.”

Founded in 2008 via the merger of Banco Itaú and Unibanco, Itaú Unibanco is headquartered in São Paulo, Brazil. With total assets of more than $377 billion and 90,000 employees, Itaú Unibanco is the largest private sector bank in the country. The institution is publicly traded on the Brazilian stock exchange and has a market capitalization of $41 billion.

FinovateEurope 2022 is right around the corner. If you are an innovative fintech company with new technology to show, then there’s no better time than now and no better forum than FinovateEurope. To learn more about how to demo your latest innovation at FinovateEurope 2022 in London, March 22-23, visit our FinovateEurope hub today!

Here is our look at fintech innovation around the world.

A partnership between India-based private sector bank RBL Bank and Google will enhance the customer experience and potential for expansion for its digital platform Abacus 2.0.

FundThrough noted that the deal is designed to accelerate both its commitment to embedded finance as well as fuel expansion plans for the U.S. market. Specifically, FundThrough believes the acquisition of its American rival will enable it to increase its U.S. clientele by 2x, boosting the number of customers in the States who use its technology to turn unpaid invoices into access to working capital.

“We are committed to helping small businesses grow and thrive – especially those who sell to large customers where long payment terms and a lack of financing options stand in the way of growing a business,” FundThrough co-founder and CEO Steven Uster said. “BlueVine was one of our biggest competitors in the U.S. market, and through this acquisition we can fulfill our mission on a much larger scale.”

With growth of more than 10x since its founding in 2014 and 3x growth over the past year, FundThrough has scaled to process more than $120 million in funding each month. The company’s AI-powered funding platform, along with its partnerships with companies like Intuit and Enverus, has enabled it to cut the standard amount of time it takes for SMEs to get their invoices paid by as much as 97%.

Invoice factoring was BlueVine’s founding business – and the centerpiece of the company’s 2014 Finovate presentation. The company has grown significantly since then, adding a range of new financing solutions for small businesses and giving the Redwood City, California-based fintech the ability to choose which area of small business financing it will focus on going forward.

“Since launching BlueVine, we’ve been focused on the financial needs of small businesses and are very proud of what we’ve been able to accomplish,” BlueVine co-founder and CEO Eyal Lifshitz said. “As we evolve our products and services, we continuously examine how we can better serve our customers at scale. We determined that FundThrough is perfectly positioned to serve our factoring clients with the care and individual attention they need and deserve. Our factoring clients will be in great hands with FundThrough.”

As part of the acquisition, BlueVine’s invoice funding division employees will join the FundThrough team. The transaction will enable BlueVine to focus on other elements of its business including its BlueVine Business Checking, Payments, and Line of Credit offerings. Since inception in 2014, the Redwood City, California-based fintech has helped SMEs access more than $14 billion in financing.

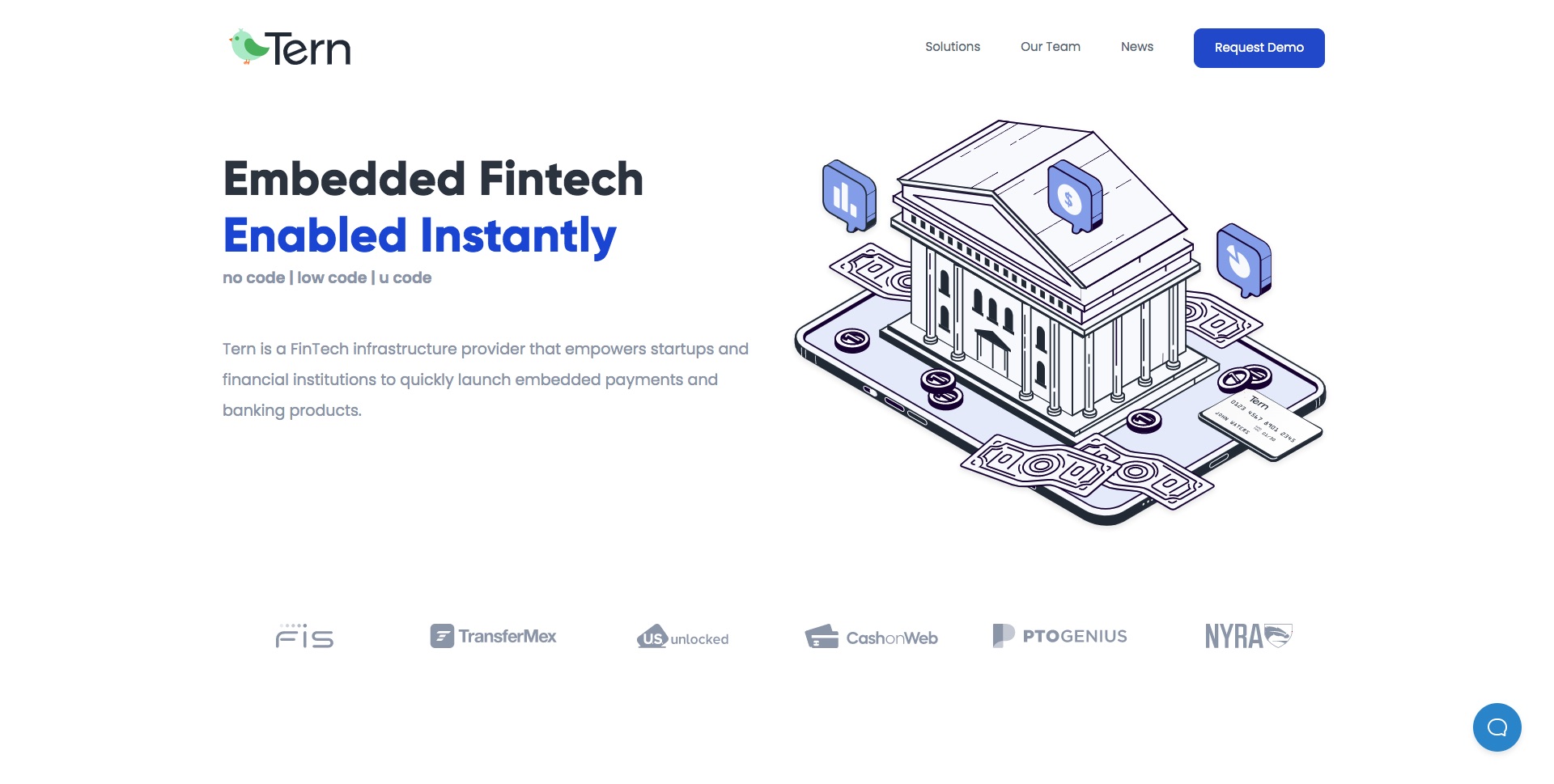

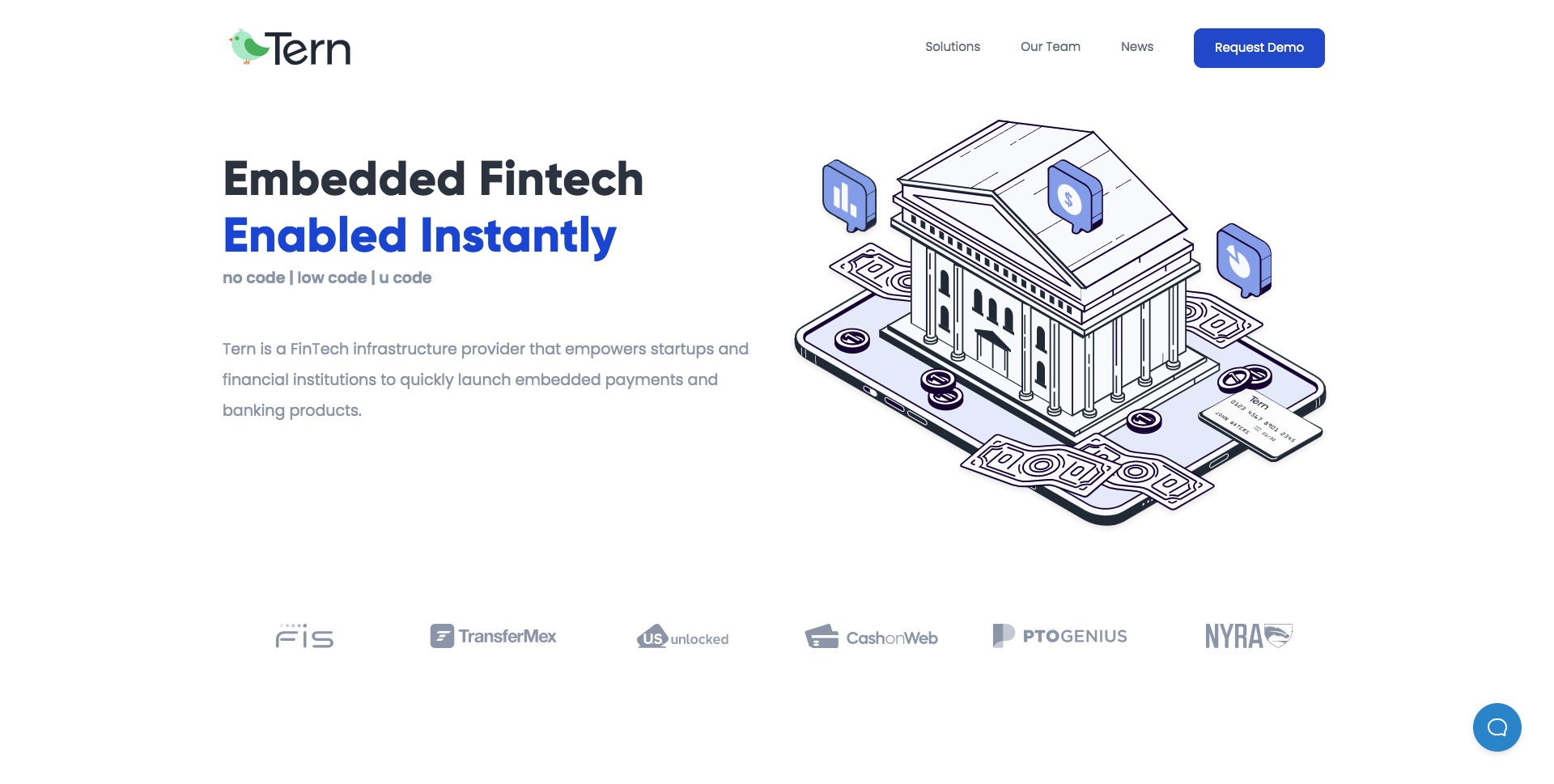

Headquartered in New York City, Tern is a fintech as a service innovator dedicated to enabling startups and established financial institutions alike to launch embedded banking and payments services products. The company, founded in 2015 by CEO Brion Bonkowski, offers a multi-currency, multi-language prepaid and stored-value platform with embedded AML, KYC, CIP, and fraud mitigation solutions.

We caught up with Brion to discuss a variety of critical topics in fintech – from the power of embedded finance and the future of neobanks, to the rise of BNPL and the challenge from Big Tech and Big Retail. We also discussed how Tern enables more companies to fulfill the promise of the banking as a service (BaaS) phenomenon.

What problem does Tern solve and who does it solve it for?

Brion Bonkowski: Tern is a fintech infrastructure company that exists to help virtually any company launch fintech products. Launching fintech products is hard and expensive. Anyone who has done it before knows the pains of contracting with banks, processors, and networks. Combined with long project timelines, these obstacles sadly prevent many programs from ever launching.

The emergence of Banking as a Service (BaaS) was the market’s initial reaction to try and serve this need. It was a way to package program management, processing, and banking under one roof. But BaaS had a narrow mandate aimed at serving startups for the most part when, in reality, the number and type of companies interested in launching financial services offerings is much broader.

Tern is the next evolution of BaaS in that we’re building tools that allow virtually any type of company to launch fintech products. This could include an early stage fintech startup, a legacy fintech, or a big global brand that wants to provide value-added financial services products to their existing customer bases. By offering no code (white labeled UX), low code (embeddable widgets), u code (API) options, we are striving to be every company’s answer to launching fintech products quickly and compliantly.

The rise of embedded finance has been one of the biggest trends in fintech of late. How do you see this trend evolving in 2022?

Bonkowski: We see a definite trend with more traditional enterprise players launching embedded finance applications, aiming to add stickiness to their service offering and additional lines of revenue to increase ARPU (average revenue per unit). The problem is, it is really hard to prototype, A/B test, and launch pilot programs to test a particular thesis in the market. We find marketing and product teams attempting to prototype and launch products quickly, however the problem is the complex compliance and regulatory oversight required. In response to this growing demand, technology providers will need to make their tools easier to deploy (with compliance baked in) to keep up with ambitious project timelines. Tern, for example, launched low code widgets to enable companies to launch core fintech services, such as onboarding, account issuance, and payouts, quickly and inexpensively.

Looking ahead, the real uptick in embedded finance will come when enterprise legacy companies, with established customer bases, realize the ROI of launching fintech services across a broad range of industries, and have a deployable vehicle to bring them to market. So, really, I would say we’re still at the beginning of this trend, and that’s exciting.

Another major trend in fintech is the proliferation of neobanks – especially those serving specific communities and consumer segments. What is driving this and how sustainable is it?

Bonkowski: New neobanks are popping up all over the place, and for good reason. Consumers have decreasing loyalty to traditional banks, so when a new online bank with messaging targeting a specific demographic appears, that demographic will typically at least test the waters, especially if motivated to do so by their peers. This is especially true if the account is free and offers services traditional banks do not, like earned wage access (EWA). Challenger banks like Chime started the wave of EWA programs and we find this function to be a big driver for neobanks to differentiate themselves and add new customers. Unfortunately, outside of EWA offerings, many of these neobanks have little to no differentiation. Many rely on celebrities and influencers to get the word out which is definitely not sustainable. Coupled with a bullish fintech venture market, we are sure to see some major casualties in the coming years.

Neobanks with specific functionality catering to their audience, however, still have a fighting chance at disruption. These differentiators vary, but even something like lowering the friction of moving funds into or out of accounts, or adding a utility like crypto or remittance to a portfolio, can be very powerful.

We’ve seen a number of different types of industries – from Big Tech to Big Retail – move into the banking services space. What kind of challenge does this represent for both “traditional” fintech providers as well as for banks?

Bonkowski: One distinct advantage that Big Tech and Big Retail have over banks and “traditional” fintechs is data. They know who their customers are, how they spend their time, and what they buy, which gives them a significant leg up in offering financial services and credit products. Traditional banks and processors see transaction data and know if you have paid your bills on time, but they haven’t a clue as to who their customers are and what makes them tick. Big data is playing an increasing role in establishing very specific cohorts of users. Within this construct, they can facilitate the orchestration of a variety of financial services, offered in different formats with cohort specific messaging, to see which one works.

The one saving grace traditional banks have is regulation and oversight, two things Big Tech and Big Retail want to stay as far away from as possible. They are already under the federal microscope, and the thought for some is that adding banking regulatory obligations could stifle growth and innovation. This has moved Big Tech and Big Retail to partner with banks, rather than compete against them…at least for now.

The Buy Now Pay Later e-commerce phenomenon seems very much in a boom phase. Is regulatory scrutiny inevitable and how might it change the way BNPL services are offered?

Bonkowski: BNPL feels like it’s the wild west of payments right now with little to no oversight. These services are, in fact, credit products and we feel they will eventually be treated as such by the CFPB. We expect new regulations and standards for things like fees, disclosures, payment due dates, penalties, etc. Our fear is these new regulations may stifle the BNPL form factor by adding steps to the process or forcing consumers to accept multiple onerous disclosures. This may increase shopping cart abandonment, the very thing BNPL is looking to obfuscate. With many products and programs, we feel the best and cleanest end use experience will prevail. BNPL providers need to remain agile and incorporate these new regulations as they come up with the least amount of end user friction possible.

This fall Tern announced a partnership with TransferMex. How did this collaboration come about and how does it help fulfill Tern’s mission?

Bonkowski: TransferMex is a great case study on the power of partnership. In 2020, Tern was approached to help an institutional Mexican labor supplier issue bank accounts for H2 Visa workers. The driver for the program was to service the employers by eliminating paper checks and, in turn, the exorbitant cost for employers to track down workers that have to leave unexpectedly to deliver their final paycheck. Looking to add value to not just the employer, but the workers, Tern suggested adding simple and inexpensive remittance capabilities to the program and TransferMex was born. The TransferMex team had limited technical resources or fintech experience so they chose to use Tern’s No Code deployment option, essentially outsourcing the entire program to Tern.

Today, the TransferMex program is live and is seeing dramatic increases in the number of workers and employers using the service. The TransferMex team does all of the marketing, onboarding, and customer support, while Tern hosts and manages all of the technology, applications, and fintech components. Tern sees growing demand for this model of issuing prepaid cards with remittance capabilities to existing brands, and will be launching two telecom companies with similar functionality in early 2022.

A fundraising round of $1 billion has given Checkout.com a valuation of $40 billion, more than 20x the valuation the company earned upon its first fundraising three years ago. The investment takes Checkout.com’s total capital raised to $1.8 billion, and the company said that it plans to use the funds to support growth in the U.S. market, launch its marketplaces solution, and strengthen its position in Web3.

“At our core, we help enterprise merchants to navigate the complexity of moving money around the world, whether in fiat currency or bridging the gap to Web3,” Checkout.com founder and CEO Guillaume Pousaz said. “By combining an elegant technology stack with industry expertise and an ‘extra-mile’ approach to service over the past decade, we’ve built deep partnerships with some of the world’s most innovative companies.” Pousaz added that while he considered this week’s investment to be a “validation” of the firm’s work to date, “we’re still in ‘chapter zero’ of our journey.”

Investors in the Series D included Altimeter, Dragoneer, Franklin Templeton, GIC, Insight Partners, the Qatar Investment Authority, Tiger Global, the Oxford Endowment Fund and “another large west coast mutual fund manager.”

With customers ranging from Netflix and Pizza Hut to fintechs like Klarna, Revolut, and Coinbase, Checkout.com offers a full-stack online platform that makes payments easier for global businesses. Enterprise merchants that face significant challenges in moving money around the world have partnered with Checkout.com for its flexible, cloud-based payment platform that offers improved authorization rates, feature parity, and direct connection to local networks in key geographies and for all major alternative payment methods.

Looking forward, Checkout.com plans to launch a solution to service both marketplaces and payment facilitators later in 2022. The new offering will combine identity verification, split payments, and treasury-as-a-service functionality with Checkout.com’s Payouts solution, which helps companies send funds to both cards and bank accounts worldwide by way of a single integration. Checkout.com reports that both TikTok and MoneyGram have taken advantage of the service, with “billions of dollars in payout transactions” processed.

Headquartered in London and founded in 2012, Checkout.com spent 2021 opening new offices in six countries across four continents and making numerous major C-suite additions. These include a new Chief Financial Officer, a new Chief Technology Officer, and a new Chief Product Officer. The company announced an extension of its strategic partnership with JCB in September, and led a $110 million funding round for Saudi Arabian-based fintech Tamara in April.

CBANC, the biggest verified professional network for U.S. commercial banking institutions – and the professionals that run and work for them – announced the launch of its new platform this week. The CBANC Marketplace will host data and information on 1,000 products from more than 450 companies – all designed to meet the unique needs of small banks and credit unions.

“Over the past 10 years, CBANC has been a place for all financial professionals to connect and discover the information they need to succeed,” CBANC CEO Tom Ferries said. “Today, the speed of technological innovation is outpacing awareness, and community banks and credit unions need a place to discover what’s available for them and feel confident in their decisions.”

The CBANC Marketplace gives companies the ability to have their solutions accessed by a verified audience of community banking and credit union professionals. Both the CBANC Community and Marketplace are free for all employees of U.S. financial institutions, and there is no cost for fintechs and other companies that want to add their product or solution. For more information, and to request inclusion in the CBANC Marketplace, visit the network’s vendor hub.

Headquartered in Austin, Texas, and founded in 2009, CBANC benefits from the collective wisdom of more than 8,600 financial institutions with a combined total of more than $22 trillion in assets. The CBANC Community consists of 65,000 verified financial professionals representing more than 80% of all financial institutions in the United States. A unique opportunity to connect and collaborate with peers in the industry who are innovating in a wide range of technologies from AI to the blockchain to cryptocurrencies, the CBANC Network earned a spot on the 2020 Inc 5000 list of the fastest growing private companies in the U.S. Ferries, who took over at CEO days before the Inc 5000 announcement, credited CBANC’s three-year revenue growth of more than 6.5x for helping the organization secure the listing.

“Our strong revenue growth is a testament to the value we deliver to our Members and Partners,” Ferries said. “Look for new and exciting product launches later this year to continue our mission of helping our Members preserve the diversity of the American banking system.”

With its acquisition of financial analysis as a service company FlashSpread, digital mortgage platform BeSmartee’s ability to deliver a complete, digital lending experience just got that much more complete.

“We are excited to welcome FlashSpread and Ariel Trybuch to the BeSmartee family,” CEO and co-founder of BeSmartee Tim Nguyen said in a statement. “This is an acquisition that not only brings new clients, technologies, and talents to BeSmartee, but one that also sparks further innovation into all lending verticals, including mortgages, consumer, and commercial.”

Founded in 2017 and headquartered in Glendale, California, FlashSpread specializes in instant tax spreading for commercial lenders and fintechs. The company’s proprietary algorithms enable lenders to convert scanned tax returns into customized and comprehensive financial reports with the click of a button. The technology brings significant efficiencies to the commercial loan process – from origination to servicing – and empowers lenders to make accurate, data-driven credit decisions quickly.

Via its acquisition of FlashSpread, BeSmartee will be able to accelerate its growth strategy, prioritizing increased automation as it expands into the commercial lending space. FlashSpread is integrated with some of the largest loan origination systems in the commercial lending industry, with more than 100 financial institutions relying on its technology to automate manual processes. Post-acquisition, FlashSpread will continue independently to serve customers as a “BeSmartee Company” with FlashSpread founder and CEO Ariel Trybuch taking on the role of General Manager.

“This partnership will provide the resources necessary to support the hyper-growth FlashSpread is currently experiencing, as well as allow us to provide our customers with an even higher level of customer support, rapidly introduce new features and functionality, and expand our ever-growing library of supported document types,” Trybuch said. The company will continue growing its document library to support a broader range of financial statements, as well as launch a no-code reporting module to offer instant custom reports, and unveil an ongoing credit monitoring tool.

BeSmartee’s acquisition announcement comes just days after the company reported a partnership with Freddie Mac. The Huntington Beach-based fintech will integrate Freddie Mac’s automated underwriting system, Loan Product Advisor, improving workflows for lenders by automating risk assessment, and both asset and income data review. The integration will also improve lenders’ ability to make smart business decisions, leveraging actionable insights from Loan Product Advisor’s rich data visualization features.

An investment of $70 million from Sumeru Equity Partners will enable online facial biometric authentication specialist iProov to expand its business in the United States, grow its worldwide partner network, and add more “top-quality staff” to its global team.

“This investment by one of America’s leading growth funds recognizes the preeminent position we have established,” iProov CEO and founder Andrew Bud said in a statement. “Our potential is enormous and we now have the resources to scale in the United States and worldwide. Our strong balance sheet will give our customers and partners confidence in our long-term ability to keep them and their customers secure.”

Updated valuation information was not immediately available. The company secured Series A funding in 2019, though the amount of the investment was not disclosed. In a statement, the company announced that it had tripled its revenues from 2020 to 2021, and processed more online verifications during a single 10-day period in 2021 than in the whole of 2020. The company added that it had completed more than one million verifications in a single day multiple times in 2021.

As part of the investment, Sumeru Managing Partner Kyle Ryland will join iProov’s Board of Directors. Ryland praised the company’s “combination of patented deep technology, exceptional customer references, and hugely capable team.”

A three-time Finovate Best of Show winner, iProov made its most recent Finovate appearance last spring at FinovateEurope 2021. At the event, iProov demonstratedFlexible Authentication which combines two of the company’s solutions – Genuine Presence Assurance and Liveness Assurance – to enable firms to choose the appropriate level of verification to be applied in a given situation.

Last month, iProov announced a partnership with high-speed passenger rail service Eurostar to test a new contactless fast-track service. The solution, SmartCheck, leverages iProov’s Genuine Presence Assurance technology to provide biometric face verification during the U.K. exit check to both streamline and better secure the travel experience. The pilot project was launched at London’s St. Pancras International station.

“This secure, convenient, and privacy-protecting technology will make life easier and safer for travelers around the world,” Bud said when the Eurostar collaboration was announced in December. “The days of rooting around in your bag for your passport or hoping that your phone battery doesn’t run out before you show your e-ticket at the gate are over. It’s effortless and convenient while also delivering the reassurance and security that travelers expect.”

The news is flying a bit under the radar. But from China to Bahrain to Jamaica, central banks are beginning 2022 having made major moves recently in support of digital assets.

We covered China’s CBDC announcement earlier this week. In short, the People’s Bank of China, the country’s central bank, made its digital yuan wallet available via both the Android and Apple app stores. Select Chinese citizens in a wide range of provinces – including Shenzhen, Shanghai, and Chengdu – will be able to download the e-CNY wallet. The Chinese government hopes that there will be significant use of the technology in the weeks leading up to the Winter Olympics in Beijing, which could represent a showcase for the digital currency.

Halfway around the world, the Central Bank of Bahrain (CBB) announced that it has successfully completed its test with Onyx by JPMorgan’s JPM Coin System. The test, the first of its kind in the MENA region, enabled Bank ABC to launch real-time payments for Aluminum Bahrain (ALBA) in the U.S. JPM Coin is a permissioned system that provides payment rail and deposit account ledger services that allow participants to transfer U.S. dollars that are held on deposit with JPMorgan.

“We at the Central Bank of Bahrain are extremely pleased to announce the success of this test which aligns with our vision and strategy to continually develop and enrich the capabilities extended to the stakeholders within our financial services sector in the Kingdom using advanced and leading emerging technologies,” Central Bank of Bahrain Governor Rasheed Al Maraj said in a statement.

JPM Coin is the inaugural product offering from JPMorgan’s Onyx, a blockchain-based platform that facilitates the exchange of value, data, and digital assets. Onyx was formed in 2020.

Several hundred miles to Bahrain’s west, the Bank of Jamaica (BOJ) announced that it also has completed a cryptocurrency pilot. Here, the digital asset is a central bank digital currency (CBDC), which has been undergoing testing in the island nation for the past eight months. The project was conducted in partnership with Irish fintech eCurrency Mint, a company with a 10+ year pedigree in innovation on CBDCs. The stated goal of the initiative was to determine “whether a central bank digital currency along with the attendant technology solution could be successfully implemented in Jamaica.”

Three specific tasks were part of the test: minting of the CBDC, issuing the CBDC to wallet providers, and distributing CBDCs to retail customers. This final component of the test involved wallet provider NCB, and the successful onboarding of 57 customers who conducted person-to-person, cash-in, and cash-out transactions with small businesses as part of an NCB-sponsored event in December called “Market on the Lawn.”

In the wake of the successful test, the Bank of Jamaica has planned a national roll-out of its new CBDC in the first quarter of 2022. The roll-out will feature the continued onboarding of new and existing customers by NCB, the introduction of two additional wallet providers, and a test of transactions between customers of different participating wallet providers to establish interoperability.

Note that Jamaica’s Caribbean neighbor, the Bahamas, launched its CBDC, the Sand Dollar, in October of 2020. The Sand Dollar is the the world’s first official central bank digital currency to reach full circulation.

FinovateEurope 2022 is right around the corner. If you are an innovative fintech company with new technology to show, then there’s no better time than now and no better forum than FinovateEurope. To learn more about how to demo your latest innovation at FinovateEurope 2022 in London, March 22-23, visit our FinovateEurope hub today!

Here is our look at fintech innovation around the world.

Among the country’s largest commercial banks, Taiwan’s Taipei Fubon Bank teamed up with Avaloq to build a wealth management platform for its private banking business in Hong Kong. Avaloq won Best of Show at FinovateAsia in 2018.

Indonesia’s central bank unveiled a new retail payments system, BI-Fast, that will reduce the cost of money transfers.

End-to-end fintech and regtech solution provider Computer Services, Inc. (CSI) has announced a pair of new partnerships to start the new year. At the beginning of the week, the Paducah, Kentucky-based company announced that Cypress Bank & Trust would deploy CSI’s NuPoint core platform to serve as the backbone for its integrated banking services. A de novo bank headquartered in Palm Beach, Florida, Cypress Bank & Trust will leverage its new platform to offer a suite of commercial and consumer banking services to new customers and expand its services to current trust and investment management customers.

“At CSI, our top priority is providing industry-leading technology and services that empower community banks to grow their businesses and innovate,” CSI Enterprise Banking Group President Giovanni Mastronardi said. “As a de novo, Cypress Bank & Trust has the opportunity to establish a modern technology foundation for their banking services.”

NuPoint is a cloud-based, core banking system that leverages seamless integration and the ability to connect to third-party APIs to enable banks to deploy customer-facing banking solutions and streamline back office operations. Cypress Bank & Trust President, CEO, and Director Dana Kilborne noted that the partnership will help the financial institution, which grew out of The Cypress Trust Company last year, to continue to evolve and build out its offerings.

“For the last 25 years, we have specialized in providing personalized trust services to meet the holistic needs of our clients,” Kilborne said. “To successfully expand into banking services, it is imperative that we work with a provider that has the technology advancements and proven experience to support our initiative.”

Computer Services, Inc. followed up its bank partnership announcement with a fintech partnership announcement a few days later. The company announced that it was teaming up with bitcoin innovator NYDIG to enable community financial institutions to offer a full suite of turnkey Bitcoin services. This includes giving banking customers the ability to buy, sell, and hold bitcoin from within CSI’s digital banking platform.

In a statement, Gerald Reiter, president and CEO of CSI core banking customer Granite Bank, noted the growing popular interest in cryptocurrencies and the importance of ensuring that consumers have a safe way to participate in digital asset trading and investing. NYDIG Chief Innovation Officer Patrick Sells underscored the point, emphasizing that safety and regulatory compliance need to keep up with customer enthusiasm for cryptocurrencies.

“Community banks are excited about offering Bitcoin services to their customers,” Sells said, “but they also know that they need to provide a secure and compliant environment to maintain the trust that their customers place in them.”

Founded in 2017 and based in New York, NYDIG ended 2021 with a $1 billion investment that gave the company a valuation of more than $7 billion. New investor WestCap Group led the round, which also featured participation from Affirm Holdings and Fiserv. Also involved in the funding were existing investors Morgan Stanley, Massachusetts Mutual Life Insurance, and New York Life Insurance.