This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

It’s been a busy summer for Finovate VP Greg Palmer and the Finovate Podcast. If you’ve missed an episode or two, now is a great time to join Greg and his guests as they talk about some of the most pressing issues in fintech today.

From the challenge of optimizing the customer experience to strategies to make fintech-bank partnerships thrive, the Finovate podcast is a great source for insightful conversation on the key trends and opportunities in our industry.

Greg Palmer talks with Rachel Lyubovitzky, CEO and Chairwoman of Setuply, on transforming new clients into brand champions with seamless onboarding. Episode 188.

Greg Palmer interviews Kevin Brown, CMO and Head of Corporate Development at Onbe, on the importance of an excellent payments experience on customer retention and growth. Episode 187.

Greg Palmer explores alternatives to equity-based growth models and the broader fintech ecosystem with Neil Kenley, Principal with Vistara Growth. Episode 186.

Greg Palmer interviews Bryon Guerra and Herb Berkley of Lone Star National Bank on tech priorities, tips for engaging with banks, and how to make a partnership work. Episode 184.

What do you as an investor know about the people who manage your money? If your answer to this question is “not very much,” then imagine the challenge of banks and other financial institutions who invest millions of dollars with hundreds, if not thousands of investment professionals.

This is an underdiscussed problem in the investment world: the lack of systematic knowledge about the individuals and teams making investment decisions for millions of individuals, families, and organizations. This can lead to underperformance in terms of investments, as well as inefficient financial advisory.

To this end, we caught up with Thomas Oberlechner, CEO and founder of BehaviorQuant. The company he founded in 2018 gives financial institutions predictive information about the people behind investment decisions. BehaviorQuant leverages behavioral science, machine learning, and automation to learn and analyze the behavior of investment professionals and teams – as well as customers. The insights derived from BehaviorQuant’s automated survey technology enables fund managers to improve their performance and better customize their services to their customers.

Headquartered in Vienna, Austria, BehaviorQuant demoed its technology at FinovateEurope earlier this year.

What problem does BehaviorQuant solve and who does it solve it for?

Thomas Oberlechner: We developed BehaviorQuant because every financial decision is ultimately made by a person or a team. BehaviorQuant solves a core problem that underlies the entire investment industry: we don’t have systematic knowledge about the people and teams behind investment decisions. And that’s true for financial professionals and clients alike.

Financial players – for example, banks, funds, financial advisors – are used to having access to vast amounts of financial data and information. But without BehaviorQuant, they don’t have systematic knowledge and data about the people and teams behind this data. Yet it is the people and teams behind the visible financial results that play the key role in investing. You can see this everywhere — in the performance of investment teams, in the selection of fund managers, in the efficiency and success of wealth advisors.

For example, in our research we found that 37% of the performance of top decision makers at world-leading financial institutions is based on their behavioral characteristics. However, there is no product to easily measure and quantify the behavioral characteristics of decision-makers. This lack of insight into the behavioral aspects and decision-making tendencies leads to underperformance of asset managers, missed profit opportunities for investors, unrecognized fund manager selection risks, costly staffing mistakes, and churn among dissatisfied clients.

How does BehaviorQuant solve this problem better than other companies?

Oberlechner: Our behavioral finance technology combines the highest level of expertise in behavioral science, personality and decision research with machine learning. For the first time ever, we are capturing the people and teams behind the visible investment decisions. And we give our customers predictive knowledge about themselves and about others – about their own investment teams, about the fund managers they allocate their money to, about their clients. Our solutions solve three distinct problems: first, they help asset managers to improve their performance; second, they help allocators choose the best fund managers; and third, they enable advisors to tailor their advice highly efficiently to each individual client.

As we all know and often forget, markets are made up of people. And financial decision makers have very different ways of processing information, personalities, values, goals, and decision paths. Before BehaviorQuant, there was no systematic knowledge of these aspects. But it is exactly these aspects that are critical to how successfully you steer your course through the rough waters of financial risks and returns.

So BehaviorQuant enables you to efficiently personalize your client advice, optimize your investment decisions, and avoid invisible risks in capital allocation and manager selection.

Regardless of how experienced you are as a financial professional, you will always benefit from a system that gives you systematic, quantitative knowledge about people. Our clients receive predictive knowledge about asset managers, investment teams, and clients. And they make far better decisions — whether they want to interact more effectively with their clients, optimize their team’s decision-making, hire promising professionals, or select compatible external fund managers. BehaviorQuant effortlessly makes them a master of these tasks.

Who are BehaviorQuant’s primary customers. How do you reach them?

Oberlechner: The lack of knowledge about the actual decision makers is pervasive, and it affects three kinds of financial companies in particular. These companies are also our main customers. First, we work with financial companies and asset managers who actively invest in the markets and who want to optimize the returns they generate by improving their own decision processes. Second, we work with family offices and other allocators who use BehaviorQuant to evaluate and select fund managers. And thirdly, we cater to banks and investment advisors who want to excel in advising their clients. They want to advise in a highly personalized way that is truly aligned with their clients.

How do we reach these customers? We’re proud that our first clients found us, not the other way around. Of course, in the meantime, we have grown our sales and marketing team and expanded our outreach efforts by maintaining an active presence on social and other media and attending of relevant conferences — like Finovate. And we’re finding that word of mouth from customers who love our solutions is increasingly supporting our efforts to win new customers.

Can you tell us about a favorite implementation or deployment of your technology?

Oberlechner: We have been receiving enthusiastic feedback from users on both sides of the Atlantic. It makes me and the team happy when they tell us that BehaviorQuant should be a mandatory tool in any decision-making process, when they emphasize how BehaviorQuant’s solutions help them to make better decisions in a systematic and sustainable way, and when they express their enthusiasm about how it helps them deepen their customer relationships.

But my personal favourite deployment of our technology is something that has only very recently come to market. It allows us to impact many more customers without them having to contact our friendly sales team first. Just in time for the 2023 fall season, we’ve introduced an all-new, self-service option for our financial and wealth advisors. They can now effortlessly get detailed information on our website and actively try out BQ Advisory. Then they can purchase single product uses for their work with clients. They can do this directly on the website, on a credit-by-credit basis. This self-service option and the ability to join on a credit basis alongside our attractive licensing offerings have made the of BQ Advisory much easier, especially for the many independent advisors who advise a limited number of clients. And it’s also great for advisors in large institutions who use us already and now want to easily show their colleagues what BehaviorQuant can do.

What in your background gave you the confidence to respond to this challenge?

Oberlechner: I was initially trained as a clinical psychologist in Vienna and always have been fascinated by the differences between people and the way they make decisions. As a university professor for many years, I have focused on how people actually make financial decisions — and the fact that we are all different financial decision makers. I have been fortunate to work with dozens of the world’s leading financial institutions for my research, from Goldman Sachs to Merrill Lynch to UBS. My female cofounder, Dr. Gerlinde Berghofer, and I both have PhDs and strong backgrounds in behavioral science. We have spent years doing research at Harvard, MIT, and Columbia University. We have worked with and studied hundreds and thousands of investment decision makers, from top fund managers to banks, advisors, and financial clients. From academia, we moved first to Silicon Valley and now to Vienna to translate this research into turnkey behavioral technologies for investment professionals.

Our solutions are therefore based on our many years of scientific work with many of the world’s leading investment institutions. And we have gone to great lengths to empirically test their benefits. For example, we have systematically tested the predictive power of BQ Performance with professional portfolio decision makers. While their average annual performance was about 10%, the annual performance of those whom the system predicted would outperform was more than twice as high. To give another example, in a comprehensive study of wealth advisory clients, BQ Advisory identified clients at risk of churn with 90% accuracy. Compare this to the 50% accuracy without BehaviorQuant!

Left to right: Dr. Thomas Oberlechner (CEO, Founder) and Gerlinde Berghofer (COO, Co-founder) of BehaviorQuant at FinovateEurope 2023.

What is the fintech ecosystem like in Austria? What is the relationship between techs, fintechs, and traditional financial services companies?

Oberlechner: Austria and Vienna have proven to be a fertile breeding ground for the specific type of fintech that BehaviorQuant offers. Vienna historically has played a large role in the sciences that generate a better understanding of individual and collective behavior, from Freud’s psychoanalysis to the Austrian School of Economics. After spending many years in San Francisco developing fintech, we felt very fortunate that the Austrian government offered us a generous grant to bring BehaviorQuant here.

I would describe the fintech industry as friendly and highly innovative, with some already well-known international players with roots in Austria like n26 and Bitpanda. Collaboration between traditional financial institutions and fintech startups has been a major driver of innovation in the Austrian market. Established banks are turning to fintech partnerships to expand their service offerings, improve the customer experience, and stay competitive in the digital age. Vienna has become a bit of a fintech hotspot, attracting both local and international talent and investment. Fintech companies benefit from Vienna’s consistently high rankings in international surveys of capitals’ attractiveness. The city offers an ecosystem of co-working spaces, incubators, and accelerators that foster collaboration and help fintech startups succeed.

At BehaviorQuant, we maintain close personal relationships with many of Austria’s “traditional” financial firms and banks, and we also have a very active bridge to the U.S. based on our history and our strong network on both the East and West coasts.

You demoed at FinovateEurope in London earlier this year How was that experience?

Oberlechner: Wow! We are absolutely thrilled by the incredible response we’ve received for our products! The interest and the number of new connections we’ve made were really overwhelming. We received amazing support from the organizers throughout the conference, as well as during in the preparation stage for our participation and presentation. The feedback from participants gave us an incredible boost of confidence and motivation. Thanks again to the team for a great and wonderfully rewarding experience!

What are your goals for BehaviorQuant and what can we expect in the months to come?

Oberlechner: Our goal with BehaviorQuant is simple: we want financial decision makers around the globe to become better decision-makers though our systematic behavioral data and decision support. And we want to become the world’s leading provider of predictive behavioral data for financial professionals and investment companies.

I briefly mentioned that we recently launched a self-service payment option for our advisory solution. In the coming months, exciting new self-service options are in the queue for the analysis of financial professionals with BQ Performance. This will allow individual investment professionals to easily get started with a comprehensive analysis of their personal untapped performance potential, as well as possible behavioral bias and performance blockers — before using it in the wider context, for example, with their entire team or company. So stay tuned for our upcoming releases!

Credit union marketplace Union Credit has announced a collaboration with financial resource network Your Money Further.

The partnership will enable users of Your Money Further to access the Union Credit Marketplace of pre-approved financing offers.

Union Credit made its Finovate debut earlier this month at FinovateFall.

Fresh of its debut at FinovateFall in New York last week, marketplace for credit unions Union Credit has announced a collaboration with financial resource network Your Money Further.

“This collaboration with Your Money Further demonstrates our commitment to expanding our reach to communities and creating a level playing field for credit unions, while also empowering consumers to accomplish their financial goals,” Union Credit Chief Revenue Officer and co-founder Barry Kirby said.

A CU Awareness company, Your Money Further helps consumers find the credit union that best suits their needs. Courtesy of the firm’s collaboration with Union Credit, credit unions in Your Money Further’s network will be able to access the Union Credit Marketplace. This will give the more than 12 million consumers who visit Your Money Further every year access to financing options from nearly 300 credit unions that are now eligible to join.

“Union Credit’s marketplace … (provides) our users wth firm, pre-approved offers of credit,” CU Awareness Executive Director Chris Lorence said in a statement, “eliminating the hassle and guesswork that comes with applying for a loan and empowering consumers to take commands of their finances.” Lorence added that the rising interest rate environment was a challenge that was making consumers increasingly anxious about their financial decision-making.

Union Credit gives consumers access to one-click credit offers embedded in their daily activities. The company’s marketplace enables credit unions to enter new markets both at the front end of purchases as well as part of a financing experience. Additionally, the marketplace gives credit unions the opportunity to boost loan volume and brand-awareness. Your Money Further users will be able to compare and choose offers and rates for home purchasing, equity loans and personal loans, and refinancing, as well as new and used auto loans – all from local credit unions looking to serve new credit-worthy members.

“Your Money Further is dedicated to empowering consumers to make financial decisions with confidence,” Lorence said, “and we’re here to help them learn more about the unique benefits of joining a credit union.”

CU Awareness is a subsidiary of Credit Union National Association (CUNA). Recall that CUNA announced just last month that it would merge with the other major credit union organization in the U.S., the National Association of Federally-Insured Credit Unions (NAFCU).

Headquartered in Santa Rosa, California and founded in 2022, Union Credit demoed its Always Approved Marketplace at FinovateFall 2023 this month. The startup has more than 130 million consumers in its publisher network and approved loan offers can be activated within 90 seconds. There is no cost to credit unions for participating in Union Credit’s marketplace. Co-founder Dave Buerger is Union Credit’s CEO.

Of all the takes I’ve heard about open banking over the past week, here is a great one I did not hear courtesy of The Finanser’s Chris Skinner: open banking is bad branding.

The core issue is that banking and finance is being ripped open by technologies to ensure better service, data enrichment, machine learning, more knowledge … but to achieve this, the service is no longer delivered by one company: a bank. It is delivered by multiple service providers through apps, APIs and analytics. That’s what Open Banking is all about. It just has the wrong name. We don’t want Open Banking. We want Closed Banking.

A typically heterodox take from Skinner and a prompt I would have loved to put to our open banking panelists at FinovateFall last week.

As it turned out, our conversation revolved around other issues – from the role of regulation to the differences in the evolution of open banking between countries and regions. But the same issues raised by Skinner this week were not far away. See for yourself in our brief summary of the top takeaways from our FinovateFall discussion.

User Experience Matters

One area of major agreement on the panel was that user experience was an undervalued aspect of the appeal (or lack thereof) of open banking. Imran Haider, Director of Product, Intuit Data Exchange, noted that the user experience for a customer connecting to their bank via an open banking flow can vary significantly. He cited the occurrence of everything from cumbersome flows to basic performance issues as obstacles to wider acceptance of open banking. “If we really want to unlock the power of customer permissioned data sharing,” Haider said, “then we need better standards and approaches on the UX side.”

Location Shapes the Market

Appreciating the way open banking is evolving differently across geographies was another key takeaway from our conversation on open banking. Florencia Ardissone, Head of Product, Customer Insights & ChaseNet Analytics, JP Morgan Chase, led with this insight. In places like the U.K., Europe, and Australia, open banking has evolved courtesy of a highly-engaged regulatory authority. By contrast, in countries like India, market forces have tended to lead, with the drive for greater financial inclusion often fueling innovation. As such, we should expect the evolution of open banking in the U.S. – however slow and sluggish – to develop based on the unique features of the U.S. banking system – including the massive number of players.

Open Banking Demands Identity Management

Skinner’s skepticism about consumer appetites for “open” banking is also a great way to understand another key takeaway from our Open Banking conversation: the idea that open banking is integrally linked to identity management. Sasha Dobrolioubov, Head of Partnerships at Persona, made the point that it critical that those financial institutions involved in open banking – the banks, the fintechs – need to have a “strong identity presence” to foster trust between would-be open banking consumers and providers.

Regulation Defines the Opportunity

The funny thing about the evolution of Open Banking in the U.S. is that has taken both the route of market-driven innovation as well as the path laid by regulators, particularly the CFPB. Kevin Jacques, Partner at Cota Capital, noted that the access to account data component of open banking evolved ahead of regulations. Jacques cited innovators – and Finovate alums – like Plaid, MX, and Finicity as examples.

That said, with pending CFPB regulations potentially limiting and restricting collection of account data based on a narrower view on consumer consent, innovation in this aspect of open banking is likely to be impacted.

iProov and Ping Identity announced a partnership that will bring liveness detection to Ping Identity’s DaVinci digital identity verification platform.

Liveness detection is a key component of facial biometric authentication to ensure that the person seeking access is both the right person and a real person.

Both iProov and Ping Identity are Finovate alums. iProov has won Finovate Best of Show awards on three separate occasions.

Per the partnership, iProov will deliver a DaVinci connector that integrates with its iProov Biometric Solution Suite. This will enable businesses and organizations to deploy technologies like liveness detection as part of their identity access and customer identity access management processes. Liveness detection is a key feature of facial biometric verification and authentication. It ensures that the individual seeking access is both the right person and a real person – not the product of spoofing techniques used by fraudsters and cybercriminals, techniques that range from simple photographs to deepfakes created by Generative AI.

iProov’s biometric verification solutions have been deployed by organizations from the U.S. Department of Homeland Security to UBS Group AG.

“Many organizations across the globe are already using iProov facial biometric technology to verify the online identity of citizens, workforces, and customers more securely and effortlessly than ever before,” iProov Chief Product and Innovation Officer Joe Palmer said. “Partnering with Ping Identity will help us to expand our reach even further and we’re delighted to be bringing this integration to PingOne DaVinci.”

A Finovate alum since 2017, iProov has earned Finovate Best of Show awards on three separate occasions. The company most recently demoed its technology at FinovateEurope in 2021. At the conference, iProov showed how its Flexible Authentication solution combined two of the company’s innovations – Genuine Presence Assurance and Liveness Assurance – to ensure that organizations apply the appropriate level of verification for a given situation.

Founded in 2003 and headquartered in Denver, Colorado, Ping Identity made its Finovate debut in 2012. The company’s PingOne DaVinci solution is a vendor-agnostic, no-code, identity orchestration service. DaVinci streamlines the process of integrating and deploying identity verification solutions from a variety of vendors. The solution currently has more than 100 out-of-the-box connectors to services ranging from identity to automation.

Earlier this week, Ping Identity launched its PingOne for Customers Passwordless solution. The new offering helps companies migrate toward a secure, seamless, password-free digital experience for their customers.

How can greater transparency in financial services help improve underwriting, lower risks, and create more opportunities for banks and small businesses alike?

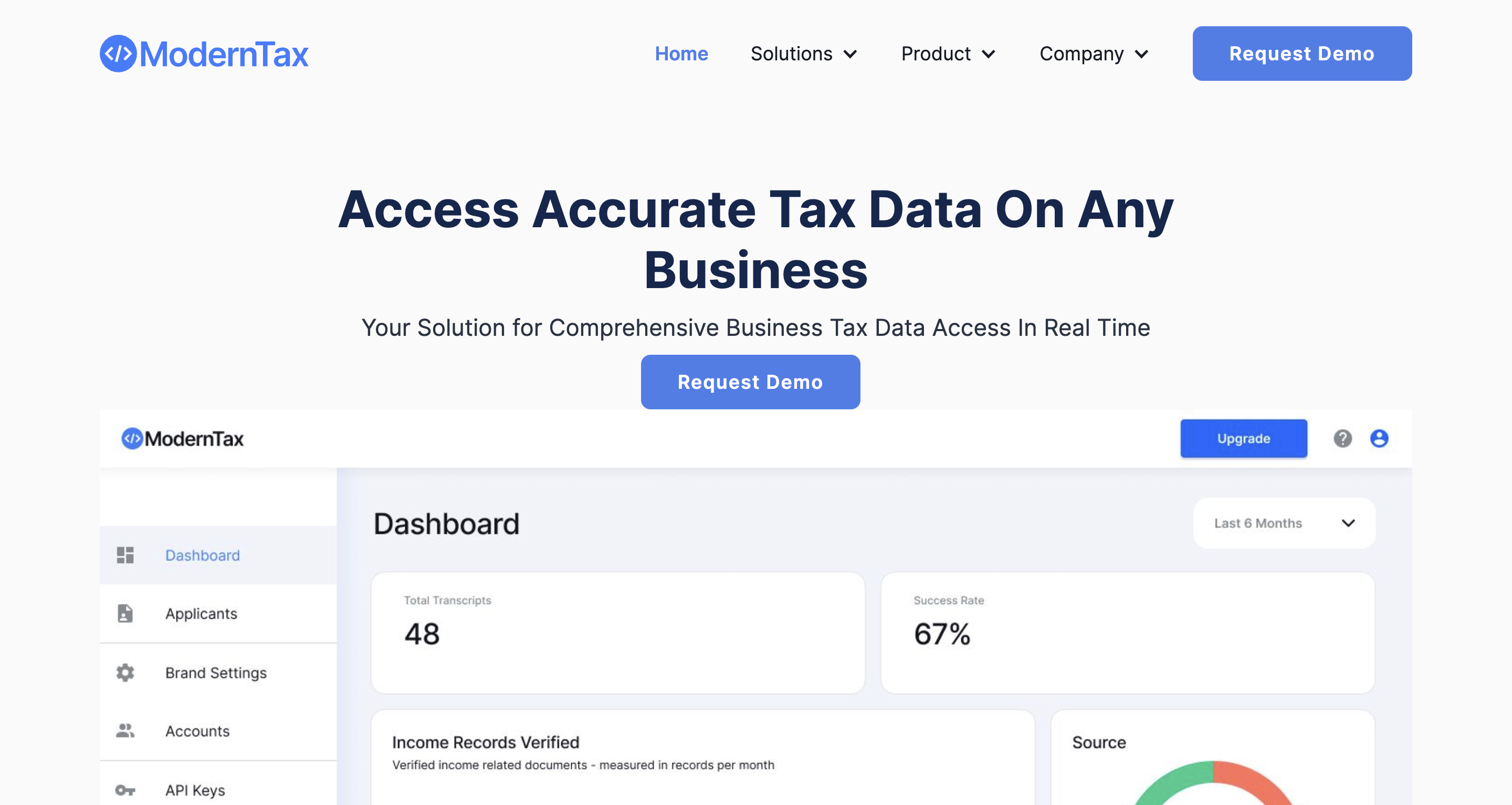

We caught up with Matthew Parker, founder and CEO of ModernTax, to discuss how bringing more transparency to areas of finance like taxation can help credit providers make better decisions.

Founded in 2021 and headquartered in San Francisco, California, ModernTax made its Finovate debut earlier this year at FinovateSpring. At the conference, the company demoed its Business Verification Platform and Verifier API, a secure solution that enables fintechs and banks to verify tax records, business standing and KYC data.

Last month, ModernTax launched its Live Contributory Network for on-demand tax verification. The solution connects licensed tax professionals with ModernTax customers to provide on-demand, secure, and reliable tax verification services.

To start off, what is it about taxes that interests you? Of all the areas of finance, what’s special about taxes?

Matthew Parker: My first job out of college was in social services, specifically working in child support. My responsibilities included calculating the combined income of two people with misaligned incentives. This experience opened my eyes to how broken the world of tax, income, and finance can be at the ground level.

A few years later, I worked in consulting, helping banks understand what went wrong with the mortgage crisis. I then stumbled into my first entrepreneurial endeavor: a franchise tax preparation company. Over three years, I grew from one office to five and learned the ins and outs of the tax preparation business.

In 2017, I caught the technology bug and bought a one-way flight to San Francisco with the goal of starting a tax startup that utilized all of the tax data I had been accessing through my tax preparation business as alternative data to underwrite loans.

Six years later, I am building ModernTax to make use of this data to help underwrite, decrease risk, and create a more transparent financial ecosystem for U.S.-based small businesses.

Can you elaborate on that?

Parker: One thing that has consistently bothered me is the black box of tax information that lives outside of our bank feeds and accounting feeds. There is an entire business that helps accountants export accounting data into tax software (they are a customer), but that is a niche market.

The real problem we are solving is financial transparency. Many businesses that provide financial services are locked out of access to critical financial records, and 99% of U.S. businesses are not required to report any financials. This results in a massive transparency gap. Tax records are one way to fill this gap, with 15 million unique entities and 160 million individual tax returns filed annually in the U.S. alone.

How does ModernTax solve this problem better than other companies, or other solutions?

Parker: ModernTax aims to solve the problem of financial transparency by providing tax information on all U.S. small businesses, which can level the playing field and create a more transparent financial ecosystem. The commercial credit market in the U.S. alone is worth $8.8 trillion annually, and the average company in this industry generates approximately $7 billion in yearly revenue.

By utilizing tax records, which are filed by 15 million unique entities and 160 million individuals annually in the U.S. alone, ModernTax’s strategy revolves around transparency and eliminates the need for countless hours of back-and-forth communication and manual data entry to collect this information, saving commercial providers time and money, and making it easier to evaluate businesses.

What is your primary market? What has the response to your technology been like?

Parker: We primarily sell to commercial credit providers such as banks, online lenders, and other data providers that assist companies in underwriting, fraud prevention, and verifying financial documents for their customers.

We have received positive responses from data providers such as D&B, Experian, and Transunion, as well as from our first paying partner, Enigma Technologies. Moreover, ModernTax has been well-received by direct carrier insurance companies for both underwriting and claims processing on income-related products.

Are there any deployments or features of your technology that are especially noteworthy?

Parker: In the past month, we have added 14 new features. One notable observation is the need for a robust platform that allows our contributors to efficiently provide us with data. Unfortunately, the IRS does not provide adequate tools to help companies maintain transparency in their reporting. We are constantly learning from our contributors on how we can build tools to address this issue.

ModernTax is headquartered in San Francisco and was founded in 2021. What is it like to be a young startup in San Francisco today?

Parker: Personally, it feels surreal to me. I moved to San Francisco in 2017, lived through the pandemic, and experienced the boom of 2021 and the correction of 2022. Nevertheless, San Francisco is resilient. Although there are political and socioeconomic problems that come with being a high-stakes, high- reward city, founders can arrive here with nothing and become paper billionaires and liquid millionaires faster than anywhere else in the world.

This creates a tale of two cities. To be a young startup, you have a ton of resources right in your backyard, but you also realize how competitive it is. There was a new billion-dollar company born every day for a certain amount of time and now, with AI, we are seeing history repeat itself. It’s important to keep your momentum but also not get too distracted.

We also wanted to talk with you as a Black founder and entrepreneur. What advice would you give to other potential founders-of-color?

Parker: Starting a company is hard, full stop. I even joke with my wife that I don’t mind telling my 18-month-old son “no” a lot because it’s just the nature of life in general. As a black founder, I have experienced both ups and downs. George Floyd’s murder created a domino effect of predominantly white people at large institutions feeling guilty, which led to a lot of initiatives that were half-baked and more PR moves than anything. That sentiment wore off pretty quickly, especially as markets turned for the worst in 2022.

If you built your brand “how hard it is to be a black founder”, you are likely bitter right now because we learned that the market didn’t care about you being black or about what happened with George Floyd. We are now seeing pushback with the rollback of affirmative action, the lawsuit impacting Fearless Fund, and I think more challenges will come. So, I would say focus on your business, focus on your customers, and build products. If you play the victim in a game that is already hard, you decrease your chances of winning.

You demoed your technology at FinovateSpring earlier this year. What was that experience like for you and your team?

Parker: This demo helped us think about how our product helps financial institutions and we were able to demonstrate the capabilities that companies can experience by getting access to this information in real-time.

What are your goals for ModernTax? What can we expect from the company over the balance of 2023 and into next year?

Parker: ModernTax aims to provide near-instant access to verified tax and financial information through a network of licensed tax agents to create a more transparent verification process for their customers. Over the balance of 2023 and into next year, the company plans to add eight new customers, launch new features for its contributor portal and business user features, and attend various business development events and in-person client meetings.

How will AI help drive fintech innovation? How can digital transformation power greater financial inclusion? Where is the smart money investing in fintech? What will be the Next Big Thing in financial services?

FinovateFall wrapped up just days ago – and much of the three days of fintech demoes, keynote addresses, and panel discussions was dedicated to providing answers to these questions.

Here we’ll reflect of those responses and highlight some of the key takeaways from our mainstage fintech experts, our innovative demoing companies, and Finovate attendees themselves.

What we learned from the experts

Our invitation-only, Leaders+ session held the evening before the conference began featured a number of insights on the present and future of fintech. The lead-off address on major fintech themes set a tone for our invitees that foreshadowed much of what the rest of our attendees would see and hear once FinovateFall got underway the following morning.

Analyst and expert Alex Johnson of Fintech Takes provided one of the more surprising insights of the night in his keynote on top trends in banking and fintech. Johnson suggested that the relatively unglamorous areas of the industry may turn out to be the “Coming Attractions” in terms of fintech innovation over the near term. Much of the fintech revolution to date, Johnson explained, involved solving consumer problems – many of them bearing an uncanny resemblance to the problems of the company founder’s themselves.

As innovation in this space runs its course, opportunities in other, neglected areas can emerge. Johnson encouraged invitees to keep an eye on “the boring stuff” like payments infrastructure and the B2B world when gauging the overall level of innovation and opportunity in the fintech and financial services industry.

Johnson also observed that we should continue to see fintech deployed to solve problems that are not necessarily considered to be financial problems. Our own Finovate research team has noted the increased news flow from companies looking to help small businesses survive supply chain financing challenges. It was heartening to hear Johnson use the example of fintechs providing financing to SMEs caught in supply chain snafus in that part of his presentation.

The other major topic of conversation in our Leaders+ session was AI and the metaverse. This was another discussion that extended over the balance of FinovateFall. The jury may still be out on the impact of the metaverse in banking. But the potential of AI in fintech and financial services seems clear.

From greater personalization of services to more efficient, more secure, and more innovative financial products, banking and financial services are ready to find roles for AI.

Start with Generative AI. One commonality between keynote speakers on AI was to compare the adoption rate of a Generative AI solution like ChatGPT to the adoption rate of previous popular technologies from the past. Think everything from Napster to LinkedIn to TikTok. GenerativeAI was clearly in a class of its own. This sentiment – that AI is here to stay – was echoed in virtually every discussion of the technology – from Leaders+ and keynote speaker Tomas Chamorro-Premuzic to Analyst All-Star Tiffani Montez of Insider Intelligence. At one point, even David Letterman’s classic skewering of the Internet in an interview with Bill Gates back in 1995 (“Does radio ring a bell?”) was deployed to remind our FinovateFall audience that we’ve underestimated innovation before.

What we learned from the innovators

There is no better way to feel the pulse of fintech innovation than by attending the Demo Days at a Finovate event. And there is no better distillation of what direction fintech innovation is going than the companies that take home Finovate Best of Show awards.

FinovateFall was no exception. Of the six companies that won Best of Show last week, we saw three companies demo solutions in areas that observers long have said are ripe for innovation. Chimney demoed a solution for homeowners that gave them actionable advice on their home’s value and equity, their borrowing power, and the availability of relevant pre-qualified offers. Trust & Will demonstrated technology that streamlines and simplifies estate planning and settlement with attorney approved, legally valid documents. Wysh, an innovator in the insurance space, demoed a deposit solution that provides micro-life insurance coverage of up to 10% of the account holders balance.

Best of Show winning companies like eSelf.ai showed fintech to be at the cutting edge of enabling technologies like AI, as well. The Israel-based company, whose founder helped launch three-time Finovate Best of Show winner Voca.ai, demoed eSelf.ai’s AI-powered client interaction solution that provides human-like conversation and engagement. Mahalo Banking, headquartered in Michigan and also winning Best of Show in its Finovate debut last week, demonstrated fintech’s commitment to diversity and inclusivity. The company leverages innovative technology to deliver online and mobile banking solutions for credit unions that help them serve neurodiverse customers with visual, cognitive, and other challenges.

And the return of Debbie to the Best of Show winner’s circle is a reminder that solutions that respond to the basics of financial wellness – saving and reducing debt – remain critical components of the fintech ecosystem. Having won Best of Show in its Finovate debut last fall, Debbie was back with new tools to help users manage debt, including a credit card refinancing marketplace for credit unions.

Where we go from here

There were a few dogs that did not bark – at least not as loudly as they once did. Cryptocurrency and digital assets, for example, did not draw as much attention this year as they have in previous years. We’ve seen more from mortgagetech, as well. It is hard not to wonder what the impact of higher interest rates will have on this industry and other consumer-facing, interest-rate sensitive sectors and services from lending to Buy Now Pay Later.

Therein lies the opportunity. The problems may seem more intractable and the solutions not as sexy as they used to be. But the eagerness of founders and financial institutions to embrace both new technologies like digitization, automation, and AI – as well as new causes like financial inclusion and sustainability – is a strong sign for the future of our industry.

They are cheering in Times Square tonight as the winners of Best of Show at FinovateFall 2023 are crowned. After two days of live fintech demos from more than 60+ innovative fintechs, our delegates have decided. Here are the winners of Best of Show for FinovateFall 2023.

Chimney for its Chimney Home solution that gives homeowners actionable advice about their home value, equity, borrowing power, and pre-qualified offers. Video.

Debbie for its rewards app for debt payout and its new credit card refinance marketplace for credit unions. Video.

eSelf.ai for its technology that delivers the next generation of client-financial institution interaction, enabling human-like conversations and efficient personalization. Video.

Mahalo Banking for its intuitive and neurodiverse-inclusive online and mobile banking solutions for credit unions with tight core integrations. Video.

Trust & Will for its technology that simplifies estate planning and settlement with attorney-approved, legally valid documents. Video.

Wysh for its innovative deposit solution called Life Benefit that provides micro-life insurance coverage up to 10% of an accountholders’s balance onto an existing deposit account. Video.

We want to thank our demoing companies, our partners, our sponsors, and – last but not least – our valued attendees whose engagement continues to make Finovate a must-attend event on the fintech conference calendar. We look forward to seeing you again next year in The City That Never Sleeps for FinovateFall 2024!

Notes on methodology:

1. Only audience members NOT associated with demoing companies were eligible to vote. Finovate employees did not vote.

2. Attendees were encouraged to note their favorites during each day. At the end of the last demo, they chose their six favorites.

3. The exact written instructions given to attendees: “Please rate (the companies) on the basis of demo quality and potential impact of the innovation demoed.”

4. The six companies appearing on the highest percentage of submitted ballots were named “Best of Show.”

5. Go here for a list of previous Best of Show winners through 2014. Best of Show winners from our 2015 through 2023 conferences are below:

Temenos unveiled a new solution, based on Generative AI, that automatically classifies customers’ banking transactions.

The new offering will help banks offer more personalized insights and recommendations to their customers.

Temenos’ Generative AI solution is part of the company’s strategic AI roadmap. Other use cases for the technology include chatbots and guiding customer journeys.

How will financial services companies take advantage of Generative AI? One way, courtesy of a new solution from Temenos, will be to leverage the technology to automatically classify customers’ banking transactions. This functionality will make it easier for banks to offer personalized insights and recommendations to their customers.

While traditional AI and machine learning technologies have been deployed by financial services firms in a variety of contexts, generative AI and Large Language Models (LLMs) offer these companies the ability to enhance both operations and customer experiences even further. This is due to the fact that Generative AI and LLMs outperform traditional AI and machine learning approaches when it comes to understanding language, images, sound, video, and code – and then leveraging these inputs into a variety of solutions for customers.

Temenos’s new Generative AI-based offering enables banks to automatically classify and label customer transactions. The technology has a high degree of accuracy and operates in multiple languages. The automatic customer transaction capability has a number of use cases including cashflow prediction, customer attrition analysis, next best product, and more.

“We have continually invested in embedding Explainable AI and ML capabilities into our banking platform and making available all products through an easy-to-use interface or APIs,” Temenos President of Product and COO Prema Varadhan said. Varadhan referred to the new offering as part of the company’s strategic AI roadmap and underscored the value of transparency and explainability when it comes to deploying AI.

Temenos has deployed explainable AI in a wide variety of use cases ranging from wealth management, AML, credit scoring, smart money management, collection optimization, and more. However, transaction classification is the first instance of leveraging Generative AI in a Temenos product. The company said in a statement that it plans to extend the technology to chatbots and customer interfaces, as well as in guiding customer journeys and responding to customer queries.

A Finovate alum since 2013, Temenos was founded in 1993 and is headquartered in Geneva, Switzerland. The company serves 3,000 customers and its open platform enables more than 1.2 billion individuals to conduct their daily banking activities. Two-thirds of the top 1,000 banks in the world and more than 70 challenger banks in 150+ countries use Temenos’ technology. Max Chuard is CEO.

Loan origination, risk management, and analytics company Baker Hill forged a new partnership with Oakworth Capital Bank.

The bank will leverage Baker Hill NextGen to enhance its loan origination and portfolio monitoring for commercial and private client lending.

Baker Hill most recently demoed its technology on the Finovate stage at FinovateFall in 2021.

Carmel, Indiana-based Baker Hillannounced a new partnership with Oakworth Capital Bank this week. The partnership is the first new alliance from the mortgagetech since private equity firm Flexpoint Ford acquired the company in June. Oakworth Capital Bank will deploy Baker Hill NextGen, a unified solution for loan origination and portfolio monitoring for both commercial and private client lending.

“Our bank’s mission is focused on delivering a personalized experience for our clients, which often means challenging the status quo and reimagining how financial services are delivered,” Oakworth Capital Bank chairman and CEO Scott B. Reed said. “The team is always looking for new, better ways to help our clients achieve their financial aspirations and Baker Hill NextGen will help us continue to do that.”

The new technology will enable Oakworth Capital Bank to enhance its commercial relationships, as well as automate the entire consumer loan origination process. The bank will also leverage Baker Hill NextGen Client Portal. This solution enables clients to submit loan documents online. Applicants also can track the status of their loan all the way to closing, bringing more transparency to the origination process. Additionally, the bank will integrate TruStage (formerly Compliance Solutions) with Baker Hill NextGen in order to automate loan document preparation and ensure compliance.

“With Baker Hill NextGen, Oakworth Capital Bank can optimize their entire loan origination process and continue surpassing their clients’ expectations with a world-class borrowing experience,” Baker Hill chairman and CEO John Deignan said.

Founded in 1983, Baker Hill most recently demonstrated its technology on the Finovate stage at FinovateFall in 2021. In the time since, the company has forged partnerships with a sizable number of banks and fintechs. These alliances include partnerships with financial institutions like Arvest Bank, Salem Five Bank, and TowneBank. Also among the company’s recent partners are tax workflow automation software company FlashSpread, and regional financial services company BOK Financial.

Digital ID verification company IDVerse will help embedded finance platform FutureBank enhance its onboarding processes with fast and secure digital identity verification (IDV). The new partnership will let FutureBank customers to use IDVerse software and also allow IDVerse customers looking for a middleware platform to connect their API credentials take advantage of FutureBank’s technology.

An integration platform for core banking providers that features embedded financial services, FutureBank operates as a middle layer between banks and third-party providers. As such, the company helps banks and fintechs launch new solutions faster, more efficiently, and more securely. IDVerse brings not only its Identity Service Provider status to FutureBank – status that comes with 20 certifications from the U.K.’s Digital Identity & Attributes Trust Framework (DIATF). The identity verification specialist also offers technology to help businesses combat the problem of deepfake accounts, a problem made all the more challenging by the way fraudsters are exploiting tools like generativeAI.

“Generative AI is breeding many different fraud types,” FutureBank CEO Sergio Barbosa said. “With ChatGPT, fraudsters can create very authentic documents and profiles for people at a low cost.” Barbosa called cybercrime “the third biggest economy in the world.”

Adding to Barbosa’s sentiments, IDVerse General Manager EMEA Russ Cohn underscored the challenge of deepfakes. Cohn agreed that “synthetic media is becoming the new tool of choice for fraudsters looking to make money” and added: “Our fully automated identity verification system can offer FutureBank customers a reliable solution to spot deepfake accounts that fraudsters are increasingly trying to create.” Cohn explained that IDVerse’s technology can detect subtle shifts and patterns in a person’s face that the unaided human eye cannot see, such as the way a person’s heartbeat slightly changes the color of their skin. These “natural yet invisible patterns,” Cohn said, enable IDVerse’s technology to distinguish real human images from deepfakes.

IDVerse’s platform also features Zero Bias AI-tested technology that leverages generative AI to train deep neutral networks to resist race, age, and gender-based discrimination.

Introducing itself to Finovate audiences in 2016 as OCR Labs Global, the company rebranded as IDVerse earlier this year. Founded in Australia in 2018, IDVerse is headquartered in London, and maintains offices in North America, Asia, and Europe. The company provides identity verification services in more than 220 countries and territories.

IDVerse has raised $45 million in funding from investors including Equable Capital and OYAK. This year, the company has forged partnerships with fellow Finovate alum Experian, bank verified digital identity service provider OneID, and cryptocurrency platform Coinmetro. John Myers is CEO.

FinovateFall is right around the corner (September 11 through September 13). If you still haven’t registered for our annual autumn fintech conference in New York this month, there’s no better time than the present. Visit our FinovateFall 2023 hub today and save your spot.

This week’s edition of Finovate Global highlights companies headquartered outside of the U.S. that will be demoing their latest innovations on the Finovate stage in just a few days. Get to know them here, then join them in New York live and in person for FinovateFall!

Connect Earth

Founded in 2021 and headquartered in the United Kingdom, Connect Earth enables financial institutions to offer their retail and SME customers insights into the environmental impact of their spending. LinkedIn.

Engage People

Headquartered in Toronto, Ontario, Canada, Engage People is a loyalty network that enables program members to pay with points directly at checkout. The company was founded in 2015. LinkedIn. X (Twitter).

eSelf

eSelf is building the next generation of client-financial institution interaction, enabling human-like conversations and efficient personalization. Founded in 2022, eSelf is headquartered in Israel.

FinTech Insights

Fintech Insights offers a comprehensive digital banking research platform. The company’s technology helps FIs build strategies and launch new features faster. Headquartered in London, the company was founded in 2010. LinkedIn. X (Twitter).

Flybits

Founded in 2013, Flybits enables FIs to deliver personalized digital banking experiences across mobile, web, and the Metaverse. The company is headquartered in Toronto, Ontario, Canada. LinkedIn. X (Twitter).

Fundica

Headquartered in Montreal, Quebec, Canada, Fundica is a government funding platform used by some of the largest FIs in North America to acquire and retain clients at scale. Fundica was founded in 2017. LinkedIn. X (Twitter).

Jaid

Jaid is an AI-powered platform build to enable the intelligent automation of business communications. Founded in 2018, Jaid is based in London, U.K. LinkedIn. X (Twitter).

LemonadeLXP

Headquartered in Ottawa, Ontario, Canada, LemonadeLXP is a digital growth platform that helps FIs and fintechs create effective training and support tools to maximize their investment in their technology. The company was founded in 2019. LinkedIn. X (Twitter).

MacroMicro

Founded in 2016 and headquartered in Taipei, Taiwan, MacroMicro empowers over three million investors worldwide to make personalized investment decisions through dynamic and insightful charts. X (Twitter).

NayaOne

NayaOne gives banks a single point of access to hundreds of fintechs, digital sandboxes, fintech-as-a-service offerings, and datasets. Headquartered in London, U.K., NayaOne was founded in 2019. LinkedIn.

SESAMm

Headquartered in Metz, France, and founded in 2014, SESAMm is an AI insight and ESG risk detection specialist serving the financial services industry. LinkedIn. X (Twitter).

Zero Bank Design Factory

Zero Bank Design Factory is developing and operating a banking system for Japan’s first digital bank, Minna Bank. Founded in 2019, the company is headquartered in Fukuoka, Japan. X (Twitter).

Here is our look at fintech innovation around the world.

Central and Southern Asia

India-based PhonePe Wealth Broking, a subsidiary of mobile payments app PhonePe, launched a stock broking app, Share.Market.

A new report from Elevation Capital and McKinsey India indicated that India’s fintech ecosystem could reach $70 billion in annual revenue by fiscal year 2030.