This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

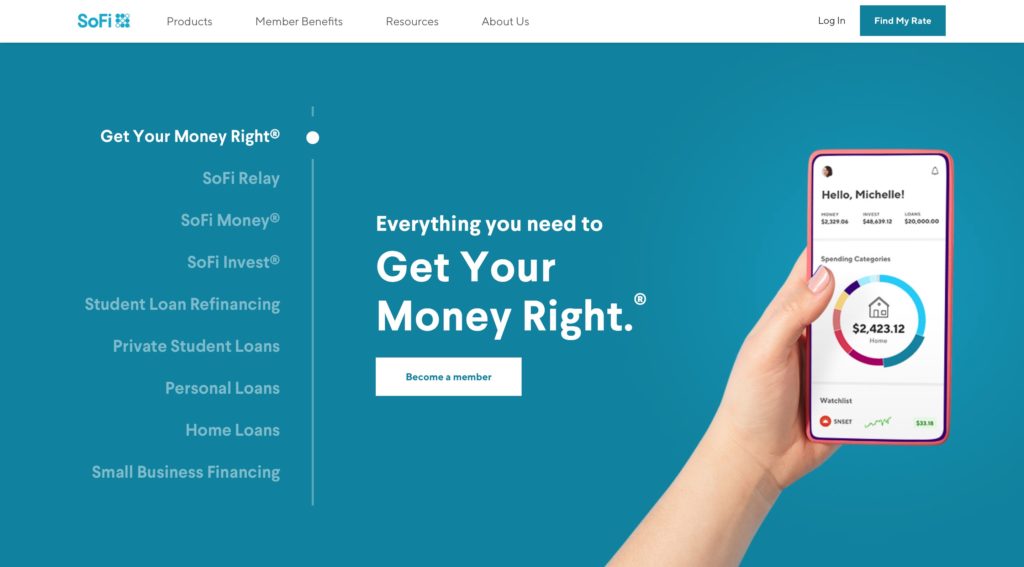

In a cash and stock deal valued at $1.2 billion, online lender and personal finance innovator SoFi has agreed to acquire financial services API and payments platform, Galileo Financial Technologies.

Galileo enables companies to build innovative consumer and B2B fintech services via its suite of open APIs. The company’s technology powers a variety of functions including:

account set-up

funding

direct deposit

ACH transfer

IVR

early paycheck deposit

billpay

transaction notifications

check balance

point of sale authorizations

Galileo processed $53+ billion in annualized payment volume in March of this year, more than doubling its September 2019 tally of $26 billion. Notably, SoFi and Galileo are already quite familiar with each other; SoFi’s Sofi Money solution is currently integrated with Galileo’s payments platform and leverages a number of the platform’s account and events functionalities.

Together, the two companies will further combine their efforts to create value for customers of both firms, who will benefit from a feature set that enables them to participate in the transition from “physical-only to a multi-channel digital and physical platform.”

“SoFi has established itself as a leader in the fintech sector, providing our more than one million members a full array of financial products to help them get their money right,” SoFi CEO Anthony Noto said. He credited SoFi’s members for motivating the company to continue innovating, and for encouraging “bigger, bolder, and more expansive” thinking. “Together with Galileo, we will partner to build on our companies’ strengths to drive even greater financial technology innovation, making those products and services available to both current and future partners.”

Galileo will operate as an independent subsidiary of SoFi, post-acquisition, with Galileo CEO Clay Wilkes remaining on board to continue leading the company. Praising SoFi’s suite of solutions for borrowing, saving, spending, and investing, Wilkes said, “these are products that many of our leading fintech clients are asking for. Distributing products through our enterprise class API is the vision behind this combination. I think it’s very powerful.”

SoFi made its Finovate debut in 2017, partnering with Quovo to presentHow Quovo and SoFi Perfected Bank Authentication at our developers conference, FinDEVr Silicon Valley. The company, based in San Francisco, California and founded in 2011, has raised $2.5 billion in funding, earning a valuation of $4.3 billion as of May of last year.

What does it mean to be financially literate? Is it more important to be able to balance a checkbook or to understand the power of compound interest? Does a financially literate person pay down student debt or consumer debt first? And does a truly financially literate person even take on debt in the first place?

A growing number of fintechs – many of them Finovate alums you’ll meet below – have devised innovative ways to help young people in particular, become better earners, savers, spenders, and investors. The majority of these innovations leverage rewards and gamification to make the educational medicine go down easier. These strategies use everything from gift cards to actual cash to encourage users to successfully complete lessons on personal finance or watch videos on common sense money management.

As companies, these fintechs partner with financial institutions – community banks and credit unions in particular – to help make their financial literacy offerings available to their customers and members. In some instances, companies have successfully partnered with educational institutions which have used their solutions as part of their financial education curricula.

April is financial literacy month. And as the coronavirus-induced economic slowdown – and potential recession – has everyone reconsidering the stability of their financial circumstances, now seems like an especially good time to be reminded of the importance of a solid – contemporary – financial education.

As recently as last fall, Finovate audiences were ranking financial literacy among the top of fintech’s most important themes. Zogo Finance, a Durham, North Carolina-based fintech that made its Finovate debut at FinovateFall, took home a Best of Show award for its Teen Financial Literacy app. Zogo’s solution pays users cash rewards – in the form of gift cards from leading brands – for successfully completing lessons on topics such as budgeting, credit, and investing.

The platform’s more than 300 educational modules were designed by educators at Duke University and ensure that users meet national standards for financial literacy. Zogo has teamed up with more than 11 community banks and credit unions in 12 states since its inception in 2018. The company began this year announcing a new partnership with fellow Finovate alum Bankjoy.

EVERFI, a Washington, D.C.-based company founded ten years before Zogo Finance, is another recent Finovate alum that has made a commitment to promoting financial literacy. The company powers community-oriented financial education for more than 850 financial institutions and 3,500+ partners in all 50 states of the U.S., as well as in Canada and Puerto Rico.

EVERFI, which offers workplace training and other educational programs as well as financial literacy, demonstrated its Achieve solution at FinovateSpring last year. The financial wellness technology enables financial institutions to offer personalized financial education to customers, employees, as well as to small business and corporate banking clients. From savings for college to navigating the homebuying process, EVERFI’s Achieve platform offers financial education that is as relevant as it is comprehensive.

Last fall, EVERFI announced a partnership with Zelle parent Early Warning Services to provide free financial education coursework to more than 1,000 high schools and 50,000+ students. The company began this year working with the MassMutual Foundation and the Washington Wizards NBA team to host the FutureSmart Challenge – an interactive financial literacy event for middle school students. Named to Fast Company’s 2020 World’s Most Innovative Companies roster, EVERFI unveiled a new financial education website earlier this month dedicated specifically to the financial challenges of the coronavirus pandemic.

Plinqit is another platform that made its Finovate debut last year and combines being an actual savings app with financial literacy features. Developed by Ann Arbor, Michigan-based HT Mobile Apps (HTMA), Plinqit leverages its Build Skills feature to pay users for engaging with its educational content. Once users sync their Plinqit account with their bank or credit union checking account and set up as many as five savings goals, Plinqit will help the user set aside a pre-determined amount of money on a customized schedule. Users can earn Plinqit cashback rewards (of approximately 1%) by reaching savings goals, referring friends and family to Plinqit, or by viewing articles and videos on personal finance and financial wellness topics.

A partnership with Arkansas-based First Community Bank ($1.5 billion in assets) put Plinqit back in the fintech headlines at the beginning of the year. The 26-branch bank teamed up with Plinqit parent company HT Mobile Apps in order to provide HTMA’s savings and financial literacy solutions to its customers. More recently, HTMA brought its financial education solutions to ChoiceOne Bank and Marquette Savings Bank.

Provo, Utah-based Banzai is another fintech oriented around financial literacy that made a major splash in its FinovateFall debut in 2018. The company picked up a Best of Show award for a demonstration of its turn-key, Community Reinvestment Act-eligible solution to enable organizations to add personal finance-based educational content – including interactive online simulations – to their websites.

Partnerships with community banks and credit unions enable Banzai to offer its financial literacy solution free of charge. The company provides three tiered courses for youth – Junior, Teen, and Plus – to ensure that the information provided and real-world scenarios are age-relevant and appropriate. Banzai’s curriculum has been used by 60,000 teachers across the U.S. and can be accessed from desktops, tablets, and mobile devices, as well.

In launching a new financial education resource for adults last fall, Banzai Coach, the company made a significant addition to its financial literacy offerings. Banzai Coach provides adult users with financial advice and instruction on how to get out of debt, how to manage basic business finances, and how to maximize their tax-advantaged investments such as retirement accounts, health savings accounts (HSA), and flexible spending accounts (FSA).

“Kids in schools love knowing that their decisions in the game actually have an impact,” Banzai’s Bryce Peterson wrote on the company’s blog announcing the availability of Banzai Coach. “As adults, we have quite the opposite concern: just about every decision we make has some kind of impact we didn’t predict or control.”

One of the most immediate impacts of the worldwide effort to combat the COVID-19 virus is social distancing. And however effective social distancing is in limiting the ability of the coronavirus to spread, it is equally effective in crushing the revenues of businesses large and small.

To help small businesses in the retail sector cope with this challenge, small business cash flow solution provider Kabbage has partnered with Facebook. Together, the two companies will help merchants continue to generate revenue at a time when their customers – for sound reasons based on public health – are largely staying away.

Via the partnership, small businesses can sign up on a new website sponsored by Kabbage: www.helpsmallbusiness.com. This will enable them to sell online gift certificates through Kabbage’s KabbagePayments portal and automatically list them on Facebook. These offers will be visible to Facebook users through their Facebook mobile app; Facebook users can then purchase gift certificates from the www.helpsmallbusinss.com website.

The integration makes it easy for small businesses to sell online gift certificates and place them where they are most likely to be seen by consumers increasingly resorting to online shopping in lieu of traveling to brick and mortar stores. It’s also a way for consumers to support their favorite retailers.

“Now with the powerful reach of Facebook, small business owners have greater opportunity to share gift certificate offers to the community that rely upon them,” Kabbage CEO Rob Frohwein said. “Small businesses are the most impacted in this crisis and this is one way Kabbage is applying its technology and resources to save them.”

The initiative with Facebook is only a small part of Kabbage’s participation in the effort to help SMEs survive the economic consequences of the coronavirus pandemic. The company is one of many helping facilitate relief funding to SMEs via the Small Business Administration’s Paycheck Protection Program (PPP). The PPP provides funding up to 2.5x average monthly payroll, and the SBA forgives the portion of the loan that is used for critical business operations such as payroll, rent, mortgage interest, or utilities if all employees are kept on staff. Kabbage reports that it has received more than 37,000 applications for the PPP, totaling more than $3.5 million.

“The smallest businesses in America are always the hardest hit, the most vulnerable, and the most in need when a crisis strikes, and together with our bank partner, we are working tirelessly to support them,” Frohwein said.

Founded in 2009 and headquartered in Atlanta, Georgia, Kabbage has been a Finovate alum since 2010 when the company debuted its Kabbage Loan at FinovateSpring.

Open banking platform for Fortune 500 companies like IBM, Yapily has picked up $13 million (€12 million) in Series A funding. The round was led by Lakestar and takes the company’s total capital to $18 million. Also participating in the funding were existing investors HV Holtzbrinck Ventures and LocalGlobe, as well as angel investors including TransferWise’s Taavet Hinrikus and Twilio’s Ott Kaukve.

This week’s funding comes a year after the company’s last capital infusion – a seed investment of $5.4 million. Yapily will use the new funds to help support adoption of open banking by institutions across Europe.

Based in London and founded in 2017 by former Goldman Sachs executive Stefano Vaccino, Yapily helps drive open banking adoption by connecting banks to fintechs and other financial services providers. The company notes that its recurring revenues have grown by more than 5x over the past six months. Yapily also has increased the size of its London office to 45 employees, and expanded into Italy, Ireland, and France.

“We believe open banking is a force for good. Using our API and infrastructure, we’re not only providing our partners with strong and powerful connectivity to boost their user experiences,” Vaccino said. “But we’re also giving their customers, whether they be customers or businesses, greater control of their finances, through the creation of products and services which can fuel greater financial management and accessibility.”

Vaccino added that this flexibility for institutions and developers was especially valuable “during this period of uncertainy.” This point was echoed by Lakestar partner Stephen Nundy who cited the COVID-19 outbreak in crediting Yapily’s technology as being “best placed” to support financial innovation that drives business growth “across the financial ecosystem.”

In addition to IBM, Yapily includes GoCardless and Intuit Quickbooks among its customers.

With a global pandemic reshaping the way we live and work, Finovate VP Greg Palmer and his Finovate Podcast turned to two of our industry’s most insightful observers this week to help put the current challenges to fintech in context.

Ron Shevlin, Managing Director of Fintech Research at Cornerstone Advisors, is one of the world’s top fintech influencers. Author of the book Smarter Bank and a columnist for Forbes, he has provided keynotes and moderated panels at industry events including FinovateFall.

On the challenges facing business leaders during the COVID crisis

We’re wrestling, all of us, with three major concerns: our physical health, our mental health, and our financial health. And if you’re an executive at a fintech company, a bank, a credit union, whatever it might be, you’re wrestling with those things in multiple dimensions: your personal physical, financial, and mental health; your family’s physical, financial, and mental health, your employees’ three areas of health and your customers’. You add that up and it’s pretty daunting …

Alyson Clarke is a Principal Analyst with Forrester Research. Among our Analyst All-Stars at FinovateFall 2019 last year, she is a specialist in digital business transformation, creating digital and customer “obsessed” cultures, and digital strategy and innovation.

On how a likely post-COVID-19 recession will affect fintechs and financial services firms

I think we’re clearly going to see fintech funding slow – especially for new or less established startups. In fact, I think it will slow across the board from VCs to corporate funding. I think that will be some of the downside for the fintechs.

In terms of financial services and banks, they’re going to do what they naturally do and that’s focus on cost-cutting and making the operations more efficient. Sadly, some of that focus will be on automation and things like that for the sake of reducing headcount. The problem with that is that they really need to be focused on productivity, not just cost-cutting, because (managing) recessions is about preparing for the upturn.

IdentityMind Global Acquired by Acuant – The deal offers Acuant access to IdentityMind’s digital identity product, a SaaS platform that builds, maintains, and analyzes digital identities and helps companies perform risk-based authentication, regulatory identification, and detect and prevent synthetic and stolen identities.

Vymo Offers Work From Home for Sales Professionals – Vymo, the company whose intelligent sales assistant makes life easier for on-the-go sales pros, has unveiled a new enhancement to help sales teams at this time when customer engagement is even more challenging.

Azimo Partners with Siam Commercial Bank – SCB clients will benefit from Azimo’s digital money transfer program that uses RippleNet, a blockchain-based money transfer service. Using RippleNet, Azimo will be able to instantly deliver payments from Europe to SCB client accounts.

CRIF to Acquire Strands – The union will bring Strands’ personal financial management and business financial management solutions to CRIF’s client base that includes 6,300 banks, 55,000 businesses, and 310,000 consumers across 50 countries.

EVO Payments Raises $150 Million to Help Manage COVID-19 Crisis – Merchant acquirer EVO Payments, the parent company of EVO Snap, has secured $150 million in cash to help fortify the company’s balance sheet, retire debt, and provide funding for future investment opportunities during the COVID-19 crisis.

How Lending-as-a-Service Can Impact Small Businesses in Need – One of the brutal facts of the COVID-19 outbreak is that it will be difficult for small businesses to survive. The self-distancing and shelter-in-place orders, while temporary, are taxing for already cash-strapped merchants.

The world continues to grapple with the COVID-19 pandemic and financial services and fintech companies are no exception. We’ve taken a look at how lenders are working to help small businesses struggling with cash flow challenges, and how firms are offering their services free of charge during the crisis to help businesses continue operating with as little interruption as possible.

Beyond this, a number of institutions around the world have taken more innovative approaches to helping manage the dislocations caused by COVID-19. Stockholm, Sweden-based Swedbank, for example, has supported hackathons in Latvia and Lithuania dedicated toward finding solutions to help businesses and individuals deal with COVID-19 related issues. The firm announced today that it is sponsoring a global hackathon in April, called “The Global Hack” to broaden the effort to get fintechs involved in the effort.

Swedbank is specifically sponsoring the economy track of the hackathon, which Swedbank Head of Digital Banking and IT Lotta Lovén said would help drive innovation in products designed to help keep markets moving.

“We not only dive into topics that will help our customers and industry through these unprecedented times, but the results will also support the local communities and the society as a whole,” Lovén said.

The Global Hack event is also supported by the European Commission, the World Health Organization, The World Economic Forum, and LinkedIn, among others.

The Fintech Times has just published its special edition on Asia – guest edited by The Finanser’s Chris Skinner. And while the timing does not allow for much consideration of the impact of the coronavirus pandemic on China’s fintech industry, a handful of articles nevertheless feature worth-reading insights on what that industry might look like on the other side of the current public health crisis.

Foremost among them – and having the most relevance for Western audiences – may be Jim Marous’ article, Tomorrow’s Model for Banking Exists Today. Marous, publisher of The Financial Brand, credits “big data, advanced analytics, modern digital technology and an innovation culture” for what he calls “the spectacular growth of innovative financial services in China.” The fact that this innovation is accompanied by – instead of being ahead of – successful financial inclusion makes the achievements of China’s techfin and fintech enterprises all the more worth learning from.

Here is our weekly look at fintech around the world.

Central and Eastern Europe

Payments platform Paysafe launchesPaysafecash in Latvia.

Russia’s second-largest bank, VTB Bank, announces big data joint venture with telecom Rostelecom.

Polish payments processor KIR partners with Danish authentication solutions provider Cryptomathic.

Middle East and Northern Africa

PayBy, a fintech based in Abu Dhabi, begins mobile payment services in the UAE.

Dubai-based Rise, which provides banking services to underbanked migrant workers in the UAE, raises $1.4 million in funding.

Mobile banking services provider Khazna secures seed funding in round led by Egyptian VC Algebra Ventures.

Central and Southern Asia

Recko, an Indian fintech that leverages AI to reconcile digital transaction plans, raises $6 million in Series A funding.

Fortune India looks at the impact of COVID-19 on India’s fintech industry.

Uruguayn-Mexican fintech Mozper, which specializes in helping parents financially educate their children, raises pre-seed investment of $770,000.

Mexico-based digital payment processor Kushki locks in Series A funding in round led by DILA Capital.

Brazil’s Cora adds cash flow boosting feature to its SME platform that enables customers that are observing quarantines to purchasing vouchers today from their favorite merchant for goods and services to be picked up later.

Asia-Pacific

Japanese digital banking startup Kyash raises $45 million in Series C funding.

Hong Kong virtual bank Airstar Bank pilots its virtual banking service.

Ripple to power cross-border payments for Thailand’s Siam Commercial Bank.

Sub-Saharan Africa

South African fintech TaxTim teams up with PwC to support expansion to Nigeria.

Zeepay Ghana wins approval for mobile money license.

Bank of Zimbabwe inks memorandum of agreement with Apollo Fintech to build a gold-based digital currency.

As the current COVID-19 pandemic reminds us, technology has a critical role in helping us respond to unforeseen events. Whether it is development of treatments and vaccines in the case of public health emergencies, or the ability to offer services and solutions to keep businesses running and workforces productive, technological innovation takes on an entirely different light at times of crisis.

One of the major themes of our FinovateEurope conference in February had to do with the ethical deployment of these financial technologies in areas like emerging markets and the frontier. These are regions where challenges from public health crisis to financial inequality can be all the more acute.

Mel Tsiaprazis, Group Chief Operating Officer at Crown Agents Bank, is one of the women who helped lead that conversation at our event in Berlin. A financial services specialist with international experience in markets such as Europe, Asia, and Oceania, Tsiaprazis believes that the combination of financial inclusion and financial education is key to ensuring financial wellness for future generations. Much of her support for diversity in financial services is revealed in the work she does as an angel investor and advisor for fintech startups.

We caught up with Ms. Tsiaprazis to discuss her work at Crown Agents Bank, the importance of ethics in fintech innovation, and the challenges of banking on the financial frontier.

Finovate: You are relatively new to the post of COO at the bank – What have been some of your early priorities?

Mel Tsiaprazis: It’s my nature to dive straight into a new challenge, so while it’s only been a year I feel like we’ve already made great progress. My priority when joining was to help drive the bank’s ambitious plans for digital transformation, so making sure we have the right infrastructure and passion to build on our technology focus has been really important. Joining at the same time as the Segovia acquisition was announced, then running with the integration, was really exciting. You can feel that becoming more technology-driven has helped keep us agile and pushing for more.

Finovate: Can you tell us a little about Crown Agents Bank and the markets it serves?

Tsiaprazis: In simple terms, Crown Agents Bank moves money to, from, and across developing, emerging, and frontier markets. We really pride ourselves on serving markets that most other players can’t. Many players don’t have the adaptability of a boutique bank like CAB or the unique relationships and expertise that we have built up over nearly two centuries, which is part of why it’s crucial we continue to serve these territories. For many countries, we provide vital access to the international market, by offering cross-border payments and FX solutions.

Our coverage spans the Caribbean, Central and South America, Asia Pacific, and our knowledge of Africa is particularly high. Within these regions, there are countries that are particularly vulnerable to natural disasters or political and economic volatility, so our services are often essential for enabling aid to reach the people who need it most.

Finovate: You participated in our FinovateEurope Power Panel on AI and Data Management in February. What were the key points you emphasized in that discussion?

Tsiaprazis: That was a really fantastic discussion! One of the key points I emphasized on the panel was how AI can help to solve societal challenges. A lot of governments worldwide are rushing to foster AI investment and develop formal AI frameworks to help spur economic and technological growth, and we need to pay close attention to the positive impact that this boom can have.

The other thing that I think is important in every AI discussion is to talk about how we can shift from fear to acceptance. What many people don’t realize is how ingrained AI already is in our daily lives – and how helpful it is – so as an industry we need to help people recognize the benefits of AI and build trust.

Finovate: You’ve spoken before about the challenges of developing or frontier markets when it comes to the lack of liquidity in local currency and the lack of financial services infrastructure. Are there ways that technology can respond to these concerns?

Tsiaprazis: Technology is an absolutely crucial part of the solution to these issues. Low liquidity and poor or absent financial infrastructure have been an issue in frontier markets for generations, but the strides we’ve made in technology over the last few years have and will be transformational.

For example, automation has already made a considerable difference in trading currencies in terms of reducing the time and cost of transactions. For markets where a large volume of cash inflow comes from remittance payments, minimizing the cost for the sender is really vital.

We’ve already seen how mobile wallets can transform access to financial services for a population. M-Pesa in Kenya is still a fantastic example of how technology leapfrogs a lack of infrastructure to reach consumers. Our payments gateway, powered by Segovia, enables International Development Organizations, for example, to reach individuals directly by allowing them to pay into mobile wallets.

Technology provides optionality in markets where financial infrastructure is considered to still be developing. We are proud to be able to offer FX to last mile delivery payment options from ACH to mobile transactions.

Finovate: One of the interesting things I’ve heard you discuss is the mutually-reinforcing relationship between financial inclusion and the need for better knowledge of local markets. Can you explain the importance of this mutually-reinforcing relationship?

Tsiaprazis: The lack of local knowledge of emerging and frontier markets can make it exceptionally difficult to serve those with limited infrastructure in the right way. A strong understanding of local financial processes and more complex environments are vital to providing financial services in hard-to-reach territories. It also helps to build trust and relationships with key organizations in that region.

Where the relationship becomes mutually reinforced is when financial inclusion increases and we get more data on people within the market. As we understand consumer behaviors and markets are better understood, more players are willing to serve them and we are able to reach more people with financial services. When the two complement each other well, we can make a real difference in improving access to these services.

Finovate: You champion gender diversity in the financial services industry through angel advice and investment in startups that support this cause. Who are some of these companies – especially in financial services? Why do you think it is an effective way to bring about the change you seek?

Tsiaprazis: Diversity is vital in all forms. It comes in numerous guises including but not limited to race, age, gender, and work experience. It is all important to the future profitability and health of an organization. Gender challenges more specifically though, within the world of startups are exacerbated. When looking for investments, I factor in BCG research which showed startups launched by women are significantly better financial investments. For every dollar of funding, startups launched by women generate 78 cents, while male-founded startups generate less than half of that at just 31 cents. Sadly, I am also very alert to the fact that only 3% of the total capital invested in 2018 in U.K. fintech companies went to firms with female founders. This challenge isn’t only in startups, we see this gender fragmentation in the top VC firms that invest in startups with only 7% of partners in the top 100 VC firms are women, according to research by Crunchbase.

While 72% of founders say that diversity in their startup is extremely or very important, only 12% of startups are diversity leaders in practice. With only 1 in 10 startups having diversity leaders, I place greater emphasis on this 10% portion not because of their background, but because startup track record shows these are sound investments. The question remains, how do we actively change the distribution of investment? How do we encourage a broader more diverse group of co-founders/startup colleagues? In my experience, the latter is answered by not only focusing on recruitment, but on retention strategies for diverse backgrounds (perhaps targeted at working/single parents, apprenticeship-like approach for high school leavers or non-degree colleagues). Encouraging a workforce reflective of your client base starts with recruitment but ends with retention.

There is no magic bullet to solve this challenge. My advice to those thinking of starting a startup is to remember you may be a superhero and a brilliant SME, but you can’t do it alone. Be wise on diversity recruitment, prioritize retention even more, and embrace lateral thinking that sets you apart.

Automated workflow and portfolio management solutions provider Teslar Software is partnering with Liberty National Bank. The Oklahoma-based bank will use Teslar’s technology to boost productivity, increase transparency, and streamline its commercial lending process.

“By leveraging our advanced portfolio management tools,” Teslar CEO and founder Joe Ehrhardt said, “Liberty National Bank will benefit from stronger data and increased visibility in the commercial lending process, helping them carry out their growth plans with confidence.”

Specifically, the bank will use Teslar’s technology to enhance its exceptions tracking, reporting, and portfolio management. This will give Liberty National Bank’s loan officers better access to more customer information, enabling them to both better engage customers as well as take advantage of potential cross-selling opportunities.

“We’re confident that through our partnership with Teslar, we’ll be able to boost efficiencies, improve accuracy of information, and provide better customer service, ultimately helping us rise above the competition,” Liberty National Bank Chief Credit Officer Michael Bucher said. “Our bank appreciates that Teslar’s platform is built by former bankers who understand our unique challenges and goals.”

With seven branches in five counties in Oklahoma, and a new loan production office in Oklahoma City, Liberty National Bank has nearly doubled its asset size over the past ten years. Founded in 1902 as the Bank of Elgin before Oklahoma had been granted statehood, the institution became Liberty National Bank in 2002. Currently serving customers in Oklahoma and North Texas, the bank has assets of $456 million as of last summer.

Teslar provides community banks and credit unions with a lending and credit management SaaS solution that enables them to manage all stages of the loan lifecycle, from pipeline and call activity to loan review. The company behind the technology, 3E Software, was founded in 2008 and is headquartered in Springdale, Arkansas. Teslar has been a Finovate alum since 2015.

There are two things that the COVID-19 crisis is teaching us. Be careful of what you touch. And be careful of who you are near.

Neither one is a good message for the future of cash nor the bank branch, two staples of 20th century financial life whose demise analysts and prognosticators have been anticipating for decades.

Could a global pandemic that forces society into “social distancing” prove to be the final straw that breaks the back of both our commitment to cash and what’s left of the bank branch?

Cash: The Irresistible Force

For all the innovations in digital payments, and the increasing adoption of these technologies by younger generations, the persistence of cash in modern economies has been impressive. In part, this is because technology has not yet been able to outperform cash where it performs best: convertibility, convenience, and anonymity.

Of late, however, one of cash’s biggest – and probably least considered – downsides has become impossible to ignore: cash is dirty. At the end of the day, regardless of whatever hero, politician, or artistic talent adorns it, cash is a slip of cotton paper passed from hand to hand, over and over again. In a article published in Scientific American three years ago, Dina Fine Maron noted:

The fibrous surfaces of U.S. currency provide ample crevices for bacteria to make themselves at home. And the longer any of that money stays in circulation, the more opportunity it has to become contaminated.

And bad news for those who limit their cash exposure to a “just couple of bucks” for tips and tiny purchases.

Lower-denomination bills are used more often, so studies suggest our ones, fives and tens are more likely to be teeming with disease-causing bacteria. Some of these pathogens are known to survive for months …

Countries around the world have already begun a coronavirus-induced assault on cash, with South Korea’s central bank both quarantining and even burning bank notes, as well as resorting to a “high-heat laundering process” to help stem the spread of the virus. Paper money has faced a similar fate in China, and even the U.S. Federal Reserve is getting into the act (albeit with currency imported from China).

Not everyone believes that COVID-19 will herald the beginning of the end of cash. Maybe it is because of doubts that, as dirty as cash is, paper money may not be a reliable transmitter of viral infection. Possibly, like young revelers at beaches in Florida well into last month, we are just too accustomed to our habits to change.

But again, the emphasis on which “we” is being discussed is probably what matters. While there is a tendency to equate people’s willingness to use digital payments as one of many options with a desire to use digital payment method exclusively, the generational trends away from cash are clear. For those who grow up in a world in which cash is increasingly under assault from one source or another, it may simply be the passage of time that ends up accomplishing what neither global pandemic nor technological innovation – combined – could not.

Branches: The Immovable Object

As thousands of traditionally on-premises employees find themselves working from home, businesses all over the world are seeing a version of themselves that is far less dependent on a brick and mortar presence – let alone multiple ones. In banking, where the value of the local branch office with lobby, tellers, and loan officers is hotly debated, it seems like the COVID-19 crisis will make the case for branches that much more of a challenge to make.

Although essential businesses that are allowed to remain open in most instances during the pandemic, banks have dramatically cut back on access to their physical locations. Often, as is the case with my bank, access is limited to a drive-through window – complete with gloved and masked teller who has you to sign your withdrawal receipt with a branded pen she asks you not to give back.

As someone who still regularly visits his bank branch – and has for decades – I actually found the experience no less impersonal than the ATMs I’ve avoided for years. Could our social distancing response to the coronavirus pandemic encourage a long-time branch-lover like me to stay away? Asked whether the COVID crisis will accelerate the trend toward fewer bank branches, KeyBank EVP and head of digital banking Jamie Warder told The Financial Brand’s Jim Marous that more “thoughtful consolidation” wouldn’t surprise him. But Warder suggested that the world still had a need for the branch, even as it “continue(d) to morph and become more digitized.”

Many innovations in the branch designed to accommodate a more digitally-savvy customer, for example, could survive the demise of the branch. Self-service kiosks that enable bank customers to perform a number of routine banking tasks without the intervention of a human teller could find homes in locations ranging from fitness centers to restaurants and other recreation hubs. The ubiquitous bank branch in any U.S. supermarket of even middling size is a reminder of how compatible these banking kiosks could be with a wide number of environments.

Unfortunately, those innovations that are geared toward making the branch itself a more enjoyable place to spend your time may struggle in the current public health climate. More luxurious accommodations – including addition of full-service cafes – could be a weak draw in a world in which we are conditioned to keep our distance.

The strain between distancing and the branch will be most acute for those who live in communities where the bank branch serves as the center of everyday financial activity. Often this consists of bill payments, check cashing, money transfers, but notably does not include short-term personal loans, a major source of financial activity in many of these communities. While a great deal of time is spent envisioning a Branch 2.0 that would appeal to the digitally-savvy and already well-banked, it may be the case that the future of the branch – to the extent that there is one – is best geared to the real needs of these communities above all others.

Merchant acquirer EVO Payments, the parent company of EVO Snap, has secured $150 million in cash to help fortify the company’s balance sheet, retire debt, and provide funding for future investment opportunities during the COVID-19 crisis. Private equity firm Madison Dearborn, a major shareholder in the company, led the investment.

“While EVO’s global portfolio represents a diversified mix of merchants across Europe and North America,” the company explained in a statement, “many of these merchants operate in markets that are subject to broad governmental restrictions on movement and commerce, resulting in substantial reductions in merchant transaction count and volumes.”

In addition to the funding, EVO Payments has launched initiatives to lower fixed costs and capital expenditures over the balance of fiscal 2020. The company’s CEO James G. Kelly said that the “long-term fundamentals of EVO’s business remain strong” and that the current strategies will enable the company to continue to grow.

Founded in 1989 and currently active in 50 markets around the world, EVO Payments acquired the technology that powers the EVO Snap development platform in 2013. EVO Snap makes it easy for developers, independent software vendors, and merchants to develop omni-channel and cross-border payment solutions. The company participated in our developers conference, FinDEVr Silicon Valley, offering a presentation and workshop on building customized loyalty programs, card-linked offers, and real-time POS rewards.

EVO Payments is publicly-traded on the Nasdaq under the ticker EVOP. The company, headquartered in McLean, Virginia near Washington, D.C., has a market capitalization of $1 billion. EVO services more than 500,000 merchants in North America and Europe, processing 900+ million transactions in the former and 1.7 billion transactions in the latter each year.

Vymo, the company whose intelligent sales assistant makes life easier for on-the-go sales pros, has unveiled a new enhancement to help sales teams at this time when customer engagement is even more challenging. The company has introduced a new Work From Home enhancement to its sales assistant solution which enables secure, 24/7 access to critical data via an app instead of requiring a desktop or on-premises hardware.

“Considering Vymo supports over 100,000 remote users already, this is a logical extension,” Vymo CEO Yamini Bhat explained. “We are seeing very encouraging signs in several of the deployments that have gone live over the past week. This social and economic situation is unlike anything we have seen before, and so our team at Vymo is committed to helping organizations adapt to this new paradigm.”

Available as an upgrade to the Vymo app, the new offering is a way for organizations to maintain business continuity during the Covid-19 crisis, and to ensure accurate communication with customers. The solution features secure calling and video conferencing, broadcasts and targeted notifications, and a central hub that provides a comprehensive view of KPIs such as agent adoption and customer coverage.

Sandeep Kumar Mishar, SVP and Head -HDFC Bank Relationship for Aditya Birla Sun Life Insurance, led the implementation of Vymo’s technology at his firm. He praised the analytics available via Vymo’s platform, and credited them for “enabling me to manage my team’s productivity better and turnaround the WFH (Work From Home) challenges positively.”

An alum of both FinovateAsia and FinovateFall, Vymo was founded in 2013 and is headquartered in Bangalore, India. The company has raised $23 million in funding from investors including Sequoia Capital India and Emergence.

Updated: 4/3/20: Added Paystand’s $20 million fundraising from February.

Finovate alums raised more than $1.3 billion in the first quarter of 2020, matching their best, first quarter performance to date from two years ago. In some ways, this year’s haul is even more impressive in that Q1 of 2020 featured half the horses as Q1 of 2018.

It is hard to not be aware of the shadow that the current coronavirus pandemic is casting over funding prospects for fintech ahead of the second quarter of the year. With regard to Finovate alums in specific, the $1.8 billion in funding they brought in for Q2 2019 would be a hard mark to beat in any year – let alone one with the sort of historic challenges we are facing in 2020.

Far and away, the $500 million raised by Revolut was the biggest fundraising of the quarter by our alums. But the nine-digit investments picked up by Tradeshift, Flywire, and Tink would put these companies at the top of any of our quarterly equity investment lists in recent years, as well. And with only a baker’s dozen of alums getting funding this quarter, it is no surprise that the top ten equity investments shown below comprise the vast majority of the quarter’s total at $1.2 billion or more than 99%.

Top Equity Investments

Revolut: $500 million

Tradeshift: $240 million

Flywire: $120 million

Tink: $100 million

Thought Machine: $83 million

Currencycloud: $80 million

Fenergo: $80 million

Lendio: $55 million

Arkose Labs: $22 million

Trusona: $20 milllion

Here is our detailed alum funding report for Q1 2020.

January: More than $440 million raised by four alums

If you are a Finovate alum that raised money in the first quarter of 2020 and do not see your company listed, please drop us a note at [email protected]. We would love to share the good news! Funding received prior to becoming an alum not included.