This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Getting that signature on the contract is a great feeling reflecting weeks, months, or, sometimes, years of effort. However, this moment is only the beginning of the process of earning the confidence and realizing the mutual benefits for both parties. During the client onboarding process, you lay the foundation of trust with your customer, a crucial factor in client retention.

With a 77% customer retention rate*, optimizing the customer onboarding process is crucial. Improving your onboarding process without comprehensive data and insights is like navigating with no map. Establishing and keeping track of the right onboarding metrics is the key to accomplishing this.

In this webinar, our group of talented onboarding expert panelists will discuss the best metrics to put in place to help deliver the optimal customer onboarding experience for your organization. We’ll start with a review of the most popular metrics. Panelists will share the best practices for introducing these metrics into your company and helping make the process tracking a sustainable operating practice. We’ll also share some helpful tips and resources to help you get started.

Frost & Sullivan is a growth-focused research and consulting company that offers a wealth of expertise across more than 10 industries. Frost & Sullivan’s Information & Communications Technologies Research Team conducts an annual voice-of-customer survey that contains inputs from key decision makers across industries.

The banking, financial services, and insurance (BFSI) industry includes commercial banks, insurance companies, non-banking financial companies, and other entities.

This study uses an integrated 360-degree research methodology to provide insights from end-user organizations, IT decision-makers, and influencers within the BFSI sector.

An analyst perspective on the state of adoption and future investment plans highlights opportunities for financial services organizations to equip their workers with the advanced tools they need to achieve operational agility and interact with customers via the channels they wish to engage.

This study also discusses opportunities for improving customer and employee experiences.

Recession. Widespread staffing shortages. Increasing fraud. Customer demands — and advancements in technology like we’ve never seen. We’ve learned a lot about the current industry landscape so far in this first quarter alone, but there are still questions that loom large. Such as:

Will the threat of fraud ever go away?

Can my call center really become a revenue generator?

How will pending legislation around real-time payments and open finance affect our customers?

Should we really consider using TikTok?

Watch this Finovate webinar, in collaboration with Eltropy, on demand, and find out the top seven trends that CFIs like you should be focusing on in the coming year. You’ll discover:

Which trends are the most crucial to ensure success for your CFI this year

How the right digital strategies and tools can make or break your institution

Examples of what’s working and what’s not in financial services

You’ll hear from Jonny Manousaridis, social media & customer marketing manager, Eltropy, and banking strategy expert David Hall.

This is a sponsored post from Tim FitzGerald, EMEA Financial Services Sales Manager, InterSystems.

Innovation undoubtably will help firms keep up with market volatility, changing customer demands, and the competition – not just today, but in the future. This is reflected in the thoughts of financial services leaders themselves as almost three-quarters (73%) believe innovation is vital to their survival as a business. Yet, despite widespread recognition of the critical nature of innovation, financial services firms are facing difficulties in successfully executing their innovation initiatives.

In particular, firms cite skills gaps and integrating disparate data sets as significant barriers to innovation. With the uncertainty and upheaval of the last few years showing no signs of slowing down as we head into 2023, finding ways to better leverage their people and data to further innovation, therefore, must be front of mind.

Obtaining a 360-degree view

Data has a vital role to play in innovation initiatives. Being able to access and use accurate, real-time data from all business units to obtain a holistic 360-degree view of the enterprise and its customers will enable firms to better identify and respond to growth opportunities, address challenges in an agile manner, and make more informed, in the moment decisions. This requires firms to address the data integration challenges they are currently facing and connect their myriad data and application silos.

One way of doing this is by adopting a smart data fabric which accesses, transforms, and harmonizes data from multiple sources, on demand, to make it usable and actionable for a wide variety of business applications. Ideal for complex data environments, the smart data fabric eliminates delays which lead to errors, missed opportunities, and decisions based on stale or incomplete data.

This approach allows existing legacy applications and data to remain in place, thereby enabling firms to maximize the value from their previous technology investments, including existing data lakes and data warehouses, without having to “rip-and-replace” any of their existing technology.

By obtaining this instant insight into their organization and customers, financial services firms will be able to make better, more accurate decisions to drive innovation, improve customer experiences, and get ahead of the curve.

Power to the people

Implementing new technology alone is not enough to help firms overcome the barriers that are currently standing in the way of successful innovation. People also have a significant part to play in innovation initiatives, so giving them the capabilities to conquer current skills gaps and to use data effectively to drive innovation are also key. Firms can achieve this by implementing a holistic innovation strategy which brings together all the critical elements required for successful innovation – people, processes, and technology – and identifies how to empower business users with data.

By putting data directly into the hands of business users, firms will be able to mitigate some of the impacts of skills gaps and help people to actively contribute to innovation initiatives. Self-service analytics capabilities embedded within smart data fabrics will provide immense value here. These capabilities will enable business users to freely explore the data, ask ad hoc questions, and drill down via additional queries based on initial findings.

In doing so, not only will firms be able to leverage their data more fully, but also they will be able to mitigate the impact of skills gaps by empowering employees to read and interpret data and make the data-driven decisions needed for successful innovation. This also will reduce reliance on IT teams to surface and interpret data, while avoiding the need for business users to learn a whole host of new skills and tools.

New year, new approach

As firms look to 2023, likely with a mix of excitement and trepidation about what the year may bring, ensuring they address the barriers currently standing in the way of innovation success is essential to help them respond to whatever comes next. By addressing issues with data integration and skills gaps head on, financial services organizations will be able to make more effective use of both their data and people to drive forward innovation initiatives.

Arming themselves with a clear innovation strategy and a team of empowered and data-enabled employees will give firms the capabilities overcome any challenges that may arise, but also critically, to grow their offering, future-proof their organization, and meet changing customer demand. Ultimately, adopting this approach will help firms to set themselves up for long-term innovation success, not just for 2023, but beyond.

The financial services industry has seen a breathtaking amount of innovation over the last decade thanks to fintech applications that streamline user experiences and improve operational efficiencies. Many of these solutions incorporate third-party viewing integrations that allow people to view and manage documents, eliminating the need to switch back and forth between different software.

Implementing specialized viewing technology saves time and resources during the development process so fintechs can get their products to market faster. By selecting the right integration partner from the beginning, they can put themselves in a position to scale capabilities in the future without suffering unexpected costs or compromising performance.

Viewing Integrations and the Problem of Scale

Fintech developers often turn to API-based viewing integrations like Accusoft’s PrizmDoc because they provide the tremendous power and flexibility that modern financial services applications require. Whether it’s file conversion, robust annotation, document assembly, or redaction, fintech software must be able to provide extensive document processing features to meet customer expectations.

In order to implement those advanced viewing capabilities, the developer usually needs to set up a dedicated server as part of their on-premises infrastructure or in a cloud deployment. One of the biggest advantages of API-based integrations is that customers only have to pay for the processing resources they use, but this can also pose some challenges when it comes to scaling application capacity.

As fintech companies expand their services, they need to be able to deliver document viewing capabilities to a larger number of users. If each viewing session requires the server to prepare and render documents for viewing, costs can quickly escalate. As server workloads increase, viewing responsiveness may be affected, resulting in delays and slower performance.

While some users may still need to use server-based viewing to access more powerful imaging and conversion features, many customers simply need a quick and easy way to view and make minor document alterations. Fintech developers need a versatile solution that can meet both requirements if they want to scale their services smoothly.

Introducing PrizmDoc Hybrid Viewing

PrizmDoc’s new Hybrid Viewing feature provides fintech applications the best of both worlds by offloading the document processing workloads required for viewing to client-side devices. Rather than using server resources to convert files into SVG format and render them for display, Hybrid Viewing instead converts files into PDF format and then delivers that document to the end user’s browser for viewing.

Shifting the bulk of document processing work to client-side devices significantly reduces server workloads, which translates into lower costs for fintech applications.

For documents not already in PDF format, the PrizmDoc Hybrid Viewing feature offers new PDF viewing packages that pre-convert documents into PDF for fast, responsive local viewing. By reducing the server requirements for rendering files, fintech providers can easily scale their applications without worrying about additional users increasing their document processing costs. PrizmDoc Hybrid Viewing also eliminates the need for separate viewing solutions implemented to work around server-based viewing, which allows developers to streamline their tech stack and further optimize customer experiences.

PrizmDoc’s Hybrid Viewing feature provides FinTech developers with several important benefits that improve application flexibility and deliver greater value to their customers.

Resource Savings Hybrid Viewing minimizes server loads by offloading the bulk of the processing required to view a document to client-side devices. Reducing server requirements translates into lower costs and frees up valuable processing resources for other critical fintech workloads.

Scalable Viewing Shifting the processing work required for viewing to local devices allows fintech applications to scale their user base with minimal cost.

Enhanced Performance Offloading document preparation to the end user’s device improves viewing speed and responsiveness, especially for large documents.

Increased Productivity Diverting workloads to client-side devices allows application users to process, view, and manage multiple documents faster. Fintech developers can leverage Hybrid Viewing to provide a better user experience that helps their customers to be more efficient and productive.

Improved Storage Management For documents not already in PDF format, Hybrid Viewing can utilize PDF-based viewing packages that are significantly smaller than conventional SVG viewing files. Files can be pre-converted for fast, easy viewing without taking up extra storage space.

Enhance FinTech Applications with PrizmDoc Hybrid Viewing

PrizmDoc’s new Hybrid Viewing feature allows fintech developers to seamlessly scale their application’s viewing capabilities without having to deploy new servers or rethink their cost structure. Shifting document processing to local devices provides end-users with faster, more responsive performance, especially when viewing lengthy documents. By keeping viewing-related costs low, fintech developers can focus their resources on developing new application features that help their products stand out in an increasingly competitive market.

Faster, flexible and easy. It would be surprising if those words weren’t the top cited needs for your customers on what they expect when using your fintech app. If you can provide these obvious, yet sometimes elusive characteristics in your next release, you’ve hit the jackpot or, at the very least, met expectations!

Speaking of customer expectations, faster, flexible, and easy ARE the expectations. Any usability friction can at best annoy. At worst, it can cause you to lose customers, particularly when competition is fierce, and especially after the past few years with the rise of the “gig economy.”

What is the Gig Economy?

The gig economy is based on flexible, temporary, or freelance jobs, often involving connecting clients and customers through an online platform. But not only that, the gig economy also connects and attracts those customers who expect speed, flexibility, and ease of use.

Starting in 2020, the gig economy grew substantially as jobs were eliminated, and previous full-time workers turned to part-time and contract work for income. Many workers took delivery service jobs bringing necessities to home-bound consumers.

Thriving within the gig economy is a big opportunity for fintechs. The gig economy spans generations – from those in their first job who have added a side hustle, to those working multiple temp or freelance positions, to those in retirement who want to earn some extra income. What they all have in common is the need for services that are fast, flexible, and easy to use. They don’t have the time or patience to deal with clunky, slow services that don’t deliver to their expectations.

A recent GWI report on U.S. fintech trends shows that the widespread usage of digital financial tools offers brands a huge upside for fintech applications, particularly with the “gig economy.” 30% of Americans participate as workers in the gig economy in some way, and digital financial tools are by far the most preferred way to manage their multiple streams of income.

If You Integrate (Fast, Flexible, and Easy to Use Document Processing), the “Gig” Will Come

Fintech companies may be on the cutting edge of software innovation, but even their most sophisticated applications need the ability to accommodate a variety of document-heavy processes used in the financial services industry. That’s why 94 percent of them leverage some form of digital document management solution.

Developing or enhancing a fintech app for the gig economy is tricky, as they expect more of their software applications than ever before (faster, more flexible, easier). Piecemeal solutions that offer only a few features are being overtaken by more comprehensive platforms that deliver a fuller end-to-end experience. Developers are adjusting by making essential technology upgrades to their tech stack, incorporating more capabilities, while also building innovative features that set their solutions apart from the competition. Thanks to third-party software integrations, they’re able to do it all.

Third-party software integrations allow developers to build more cohesive software solutions that provide all the essential features a customer may require. Instead of pushing them into a separate application to interact with their documents, provide a signature, or fill out a digital form, they deliver an unbroken experience that’s easier to navigate and manage from start to finish.

Upgrading Your Fintech Application’s Potential

By turning to a partner with the right software integrations, fintechs can quickly implement powerful features while keeping their own development efforts focused on designing best-in-class capabilities and bringing them to market quickly.

With more than 30 years of experience helping fintechs enhance their integrations, Accusoft’s collection of SDK and API solutions provides a broad range of document and image processing solutions that can help improve efficiency, reduce errors, and deliver a better overall user experience. Whether you need the viewing, editing, and document processing features of PrizmDoc, or the image clean-up, conversion, and OCR capabilities of ImageGear, our family of software integrations can make it easy for fintechs to incorporate the functionality they need without having to rethink their tech stack. And most importantly, fintechs will be well prepared to meet and sustain the growing expectations of the gig economy for speed, flexibility, and ease of use while using their digital finance tools.

The following is a sponsored blog post from Finastra.

Post-pandemic recoveries stalled by rocketing energy prices are leading to calls for stalling a green transition that has already begun. But the costs to businesses due to climate-related weather events within the next four years will be over $1 trillion.

Investors and financial institutions are increasingly applying non-financial factors (Environmental, Social, and Governance) as part of their analysis process to identify material risks and growth opportunities. Also, there is a high interest coming from consumers in the sustainability of businesses and how they impact the environment.

But because of the broad range of indicators coupled with the lack of standards, transparency, and unified reporting makes it a challenge to assess and measure true, impactful ESG credentials and the sustainability of a business.

At the same time, many banks have started to embrace/experiment in the Metaverse including DBS Bank in partnership with The Sandbox with a focus on driving sustainability. Will this be an opportunity or a challenge for financial institutions keen to demonstrate their commitment to a more sustainable future?

To help navigate these challenges Finastra invited three experts in ESG and Sustainable Finance alongside Christophe Langlois, their Global Marketing Lead, Fintech & Developer Ecosystem at Finastra, who hosted this insightful conversation:

Marcus Cree, MD Financial Technology and Services, GreenPoint Global

Tanuj Pasupuleti, CEO, Bankify

Jay Mukhey, Global Director of ESG, Purpose & Impact, Finastra

They discussed the following topics:

The case of ‘greenwashing’ in 2022 and how to identify it.

The main differences in terms of sustainable finance adoption and challenges between the key regions of the world?

The opportunities that come with sustainable finance.

The essential role open/API banking plays in fostering sustainable finance.

Metaverse from a sustainable finance standpoint.

To learn about the successful adoption of ESG and sustainable finance and what solutions are available right now on the market, watch the video by visiting this page.

This is a sponsored post by Tim FitzGerald, EMEA Financial Services Sales Manager, InterSystems, Gold Sponsors of FinovateFall 2022.

In today’s fast-moving landscape, financial services firms are under increasing pressure to remain competitive and generate more revenue by developing new products and services faster, while still leveraging their existing resources.

In recent years, this has seen many financial services organisations turn to external fintech solutions to help accelerate innovation and quickly obtain new digital capabilities. And so, fintech partnerships have become critical components of financial institutions’ growth strategies, rather than the technology experiments they started out as.

To ensure innovation success, it’s vital that financial services organizations can easily leverage and provision new fintech services and applications by seamlessly integrating with their existing production applications and data sources. But the true value and potential of fintech solutions can’t be unleashed until integration is quick and easy.

As many firms will attest, arduous and costly integration can see the value of such initiatives dwindle before their very eyes – sometimes to be lost altogether. Common challenges can range from unforeseen issues tying up precious IT resources, to costs spiraling out of control and timescales sliding drastically from what was planned or what is desirable. Ultimately, these delays can result in the loss of any competitive edge as rivals launch similar solutions much faster.

Ensuring successful integration

Fintechs have become increasingly attractive as they incorporate the latest technologies, modern application methodologies, and deployment platforms. However, for banks to make effective use of these opportunities, those technologies need to be woven into its existing infrastructure, much of which is likely to be based on legacy technology.

Consequently, successful integration requires an understanding of the intricacies and idiosyncrasies of those legacy systems. It also demands knowledge of the underlying data architecture and how to connect the new technology to systems that weren’t built to be connected to in such a way. While this isn’t an unsurmountable problem, getting it right will take resources, budget, and time.

Careful consideration is also needed when undertaking the integration to ensure that the resulting architecture doesn’t become overly complex. After all, if it comprises multiple technology layers from different vendors, all with differing versions and releases, any future change could impede the bank’s ability to take advantage of the benefits they set out to achieve.

Next will be to determine how data from existing systems will be fed into the new system and in what format. To get around this, it’s all too easy to layer extraction tools upon a myriad of other tools, including transformation tools, data lineage, master data management, databases, and data lake technologies. However, what firms are then left with is a multi-headed monster that no one person truly understands. This approach to data integration is also complex and costly to design, deploy, manage, and maintain. Fortunately, adopting a smart data fabric approach, a next generation architecture, can provide a way for financial services organizations to overcome these challenges.

Achieving bidirectional connectivity

By leveraging a smart data fabric, it is possible for institutions to connect and collect real-time event data and obtain unmatched integration capabilities using just one holistic platform. This approach eliminates the complexity and inefficiencies of manual integrations and other legacy approaches to integration and enables firms to integrate applications faster and more efficiently. It does this by essentially creating a dynamic real-time, bidirectional gateway between cloud-based fintech applications and their own production applications and data assets.

The smart data fabric integrates real-time event and transactional data, along with historical and other data from the large number of different back-end systems in use by financial services organizations. It transforms the data into a common, harmonized format to feed cloud fintech applications on demand, thus providing seamless, real-time, bidirectional connectivity and integration with the bank’s existing legacy enterprise data, production applications, and data sources.

Not only does this help firms to realize faster time to value and achieve simpler implementation that is easier to maintain, but it also gives financial services institutions the agility needed to innovate faster and keep critical initiatives on track. Additionally, it helps to futureproof their architecture by making it easier to incorporate any fintech applications and technologies available in the marketplace, thereby empowering them to react to new opportunities and changes in their environments.

Ultimately, there is immense value to be unlocked from fintech solutions and applications. However, that is only possible through swift and simple integration. By implementing a smart data fabric-enabled data gateway, financial services organizations can quickly and easily integrate new solutions within their existing infrastructure to ensure they are able to keep pace in a rapidly evolving landscape.

This is a sponsored post by Strands, Gold Sponsors of FinovateFall 2022.

Nowadays, personalization has become a must in all sectors that affect consumers’ daily lives. Companies such as Netflix and Amazon have already been able to create totally customized and customer-centric experiences thanks to advances in technology, data, and analytics. Digital Banking has also faced these expectations, demanding personalization for different user bases, needs, and underserved segments. With a focus on financial wellness, banks can generate cross-selling opportunities and create personalized journeys according to the interests of their customers.

Technology advancements have enabled companies to collect, analyze, and use data from a variety of sources, including internal and external channels, enabling banks to make better decisions, offers, and actions than ever before. Unfortunately, most banks still struggle to know their customers or to interact with them timely and relevantly – to provide the right offers at the right time to the right customers.

This is what customer centricity means, which is vastly different from product or brand centricity. When a financial institution has a deep understanding of its customers, it can provide solutions that are tailored to meet their specific needs, life stages, values, and interests beyond their typical sociodemographic information.

As part of this approach, extra data sources are tapped, such as third parties, in addition to what’s available within core banking as open banking data, surveys, social media, and other data sources consented by the customers, integrating machine learning, categorized transactional data, and other customer experience solutions that can enrich the available raw data.

How to derive and use such insights is now the question. In the first stage of data enrichment and analysis, core application data can be used to understand how the customer interacts with the bank, the recency, frequency, channels, etc. Through this information and analytical models, it is possible for financial institutions to predict proactively what the customer is likely to want or need in real time.

The customer journey is vital in today’s financial services landscape and cloud-enabled business innovation is the vital ingredient.

A good user experience is a critical factor in helping consumers differentiate between firms and helping brands build lasting relationships with customers.

According to the Harvard Business Review, firms with leading customer satisfaction rankings can grow their revenues two and a half times faster than their competitors. Moreover, research by Forrester demonstrates that customers are over twice as likely to stick with a brand when their problems are solved quickly.

Yet, great digital experiences rely on intuitive GUIs and an agile, cloud native strategy, both of which are not easy to achieve. In this article, we’ll demystify how to get started with cloud computing in software engineering for banking and help you develop a leading customer UX.

What Are the Challenges of Cloud Business Innovation in Banking?

Approximately US$1.3 trillion was spent in 2020 on digital transformation, yet Deloitte data shows 70% of projects fail. That equates to over US$900 billion wasted — so what’s going wrong?

Just as an HD TV relies on good HD content, great apps need high interactivity with data, an always-on presence, security, and scalability to perform under high demand.

Eric Newcomer, WSO2 CTO, argues that cloud business innovation goes wrong when there’s a messy middle. In other words, when there’s a lack of clarity about how strategy, outcome, and skill coordinate the microservices within a platform, cloud business innovation becomes dysfunctional.

Within banking specifically, the stakes of digital transformation are extremely high. Today’s financial services firms must deal with an onslaught of cyberattacks and regulatory constraints, not to mention increased competition from new fintech entrants better-equipped to deliver excellent customer experiences. So how can financial institutions ensure they foster an innovative and successful cloud-first environment?

How to Overcome These Challenges

Great cloud computing in software engineering needs equally great cloud native practices and technology, focusing specifically on integration and APIs. Without this focus, customers lose the always-on, always integrated feel that today’s users demand.

Therefore, financial services firms require an all-in-one platform delivering accelerated and enhanced engineering processes to speed up innovation in their cloud environment. Unfortunately, building robust and agile platforms from scratch can be timely and costly.

Instead, partnering with existing solutions providers allows financial service firms to focus on developing cloud banking innovations and better deliver security, compliance, and ideal customer experiences. You can read more about overcoming challenges for banks to generate fintech innovation here.

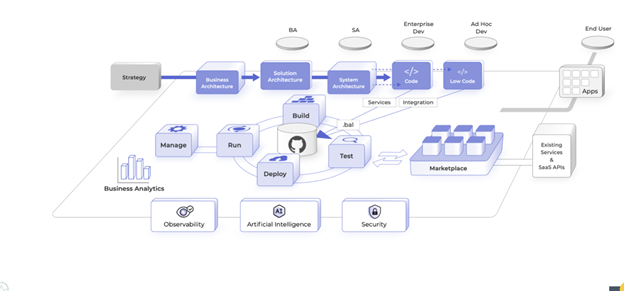

The Role of Digital Platform-as-a-Service Within Financial Services

An “opinionated” digital platform-as-a-service (digital PaaS) accelerates cloud banking innovation by tackling some of the core complexities of developing digital applications. As a result, you can build, deploy, and iterate new versions more easily.

Digital PaaS platforms enable diagrammatic and low-code functionality, providing a great developer experience. In turn, your teams can increase their productivity and attention to quality assurance for end-users.

Moreover, digital PaaS integrates with automated deployment tools using Docker and Kubernetes. As a result, you can test, develop, and deploy new user features for maximum customer satisfaction faster than ever before, using just a few clicks.

Digital PaaS solutions deliver seamless platform functionality and integration with your existing data warehouses, allowing you to leverage efficient and scalable consumer solutions.

How Low-Code Digital PaaS Enables Cloud Computing in Software Engineering

There isn’t a one-size-fits-all solution to cloud computing in software engineering, so what makes a digital PaaS-based method the most appropriate for financial services?

A digital PaaS approach provides a highly stable environment to create and manage APIs since it establishes core conventions and assumptions within your workflows. These assumptions include the programming language and dev environment, all the way to the publishing process on software marketplaces. As a result, you can remove barriers to collaboration and shorten project lead times. Similarly, as a cloud-enabled solution, you provide collaborative space for your teams to work.

Moreover, you can easily build platform microservices and provide teams with autonomy over their software output. Software teams can publish updates to critical platform elements accordingly without jeopardizing the rest of your platform or relying on slower project teams, keeping your user experience competitive.

However, the benefits don’t stop when you hit publish. Digital PaaS solutions allow you to run professional DevOps systems and make improvements in step with live user trends. Consequently, you can remain competitive and establish a close relationship with customers.

Finally, once your APIs are built, you can share them through marketplace and import or export data with other SaaS platforms. As a result, you can leverage other data sources for enhanced features. For example, you can capitalize on open banking ecosystems, enhance your security through additional identity checks, and more.

And so, with complex development and deployment tasks that are both easy to learn and use, you can deliver fresh digital services faster — and more accurately — than ever.

Introducing Choreo by WSO2

With around only three in ten digital transformations being successful and the heightened competition within banking today, financial services companies need to innovate at speed and scale.

Choreo is a digital PaaS that helps companies manage and develop APIs, services, and integrations quickly. Choreo enables developers and operations teams to go from ideation to production in hours or days versus weeks and months via a seamless environment that eliminates the complexity of cloud native computing.

Choreo provides a diagrammatic and pro-code environment side by side, allowing you to create an outline and make detailed tweaks in minutes. It includes a developer marketplace with over 400 pre-built connectors that makes it easy to discover, reuse, publish, and share.

With security and transparency at its foundation, you can easily trace code changes and root issues across your entire development history. You can also benefit from AI-assisted coding and enhanced governance features.

Find out more about Choreo and create an API with just a few clicks.

This is a sponsored post by Ann Kuelzow, Global Head of Financial Services at InterSystems.

A staggering 86% of financial services firms globally are concerned about using data to drive decision-making within their organizations, according to the latest research from InterSystems of 554 business leaders within financial services companies, including commercial, investment, and retail banks, across 12 countries globally. This lack of confidence largely stems from an inability to access data from all the needed sources and the time taken to access data. Given the wealth of data financial services firms have, this is a major concern, with the potential to open organizations up to risk and severely impede key business initiatives. In fact, more than a third of firms in the survey cite the primary impact of these challenges as being difficulty in gaining a 360-degree picture of customers.

As competition intensifies within the financial services sector, customer 360 is something that all firms must confidently be able to obtain. Doing so will empower firms to provide clients with the products, services, and hyper-personalized, real-time experiences they have come to expect across all aspects of their lives. But this relies on gaining access to accurate, consistent, and real-time data encompassing all touchpoints. Consequently, firms must first address underlying issues with their data architecture.

Solving data challenges

Gaining a holistic view of the customer requires firms to pull together all available information on each customer. As customers are likely to interact with a variety of different departments and personnel within the firm, this information can be spread across multiple systems and silos, including trading, savings, credit cards, loans, insurance, CRM, support, data warehouses, data lakes, and other applications and silos, as well as data from external sources and suppliers. The data is often in dissimilar structures and formats and follows different naming conventions and metadata. Therefore, making sense of this dispersed data typically requires significant effort and expense, and using it to make informed, accurate, and fast decisions is a major challenge.

As organizations look to solve these problems, data fabrics, a next-generation architectural approach, have emerged to provide financial services firms with a way to speed and simplify access to data assets across the entire organization. It does this by connecting to existing systems and data silos containing relevant data, both inside and outside the organization, and ingesting the relevant data on demand as it’s needed. It accesses, integrates, and transforms the data as it’s being requested, providing a real-time, consistent, harmonized view of the data from different sources, all from a single view. This allows firms to gain a complete 360-degree view of the customer.

Going a step further

A smart data fabric takes this approach a step further by providing built-in analytics capabilities which enable business users to understand customer behaviors and actions better and even to predict the likelihood of future behaviors, such as purchase of new services, churn, or response to targeted offers. It also provides the business with self-service analytics capabilities, so line-of-business personnel can drill into the data for answers without relying on IT, eliminating the usual delays associated with adding custom requests to the IT department’s queue.

This next generation approach also helps solve latency issues, as smart data fabrics lets the data reside in the source systems, where it’s accessed on demand, as it’s required.

Adopting this approach will help to restore firms’ trust in their data, ensuring that they can quickly access consistent, reliable, and accurate information on which to base decisions, fuel data initiatives, and build up a comprehensive view of the customer.

Elevating the customer experience

Being able to leverage the wealth of customer data inside and outside of the organization for customer 360 will empower firms to offer a vastly improved customer experience. For instance, with a single view of the customer, advisors, help desk, and support teams will be able to provide customers with the immediate answers and recommendations and thereby enhance their interactions with the organization.

Armed with customer 360, firms will also be able to increase revenue streams by predicting customer behavior to maximize cross-sell and up-sell opportunities. For example, incorporating and analyzing dozens of data points from different systems enables firms to determine which customers are likely to respond to a premium credit card offer and least likely to default on payments. This allows firms to identify which customers to target with particular offerings and services. Similarly, firms will be able to predict which customers are at risk of churning and take appropriate corrective actions in advance to reduce churn.

Together, these capabilities will help to elevate the experience and services being offered to customers, while also helping financial services firms to create and cement a competitive edge.

Restoring trust in data

Ultimately, by adopting smart data fabrics, firms will be able to overcome the data challenges that are currently preventing them from using their data to make better decisions by leveraging a more complete and more current 360-degree view of each and every customer. With a complete and trusted 360-degree view of the customer, firms will be in a strong position to fuel new customer initiatives, enhance the customer experience by delivering cohesive and personalized interactions and offerings across departments, and set their institution apart.

This is a sponsored article by Kim Minor, Senior Vice President Global Marketingat Provenir.

To compete successfully in our digital-first, instant gratification world, you need a risk-decisioning ecosystem designed to intelligently serve customers. A solution that not only connects every piece of credit decisioning and AI/ML software you own, but also enables you to access any external and internal data source in real time to auto optimize decisions—along with the impact of those decisions—across your entire customer lifecycle.

But many financial services providers are unable to tie all these elements together because legacy risk analytics offerings just weren’t built that way. So, as a user you’ve had to look to multiple products when you want world-class solutions for data and AI-powered decisioning. You’ve relied on vendors to make changes. You’ve relied on multiple user interfaces (UI) to keep control. You’ve waited months for solutions to go live, and… you’ve needed to replace technology a few years later when it can’t expand and scale with your business.

Whether you’re a startup with a single product line, or a unicorn offering a range of financial solutions, you need to create a financial ‘home’ for your customers, which means delivering a great customer experience from start to finish, regardless of changing dynamics.

Here are the five key features of a risk decisioning platform that will enable you to create world-class customer experiences:

No-Code Management: to integrate systems, change processes and launch new products

In a survey of 400 decision makers in fintech and financial services organizations across the globe, 78% of respondents cited low/no code UI as a feature they have or that would be most important when selecting an automated risk decisioning system. Inflexible solutions that require a vendor or your IT department to connect to a new data source, make workflow changes or launch a new product hinder time to market, increase costs, and put you behind your competitors. Look for a solution that has pre-built data integrations and a visual, drag-and-drop interface to easily and quickly make changes to respond to evolving consumer needs.

Connected Data: easy access to real-time and historical data

Through our survey of decision makers, we discovered that credit risk decisions rely more on historical than real-time data. Sixty-one percent of respondents use both historical and real-time data when making credit risk decisions yet only 11 percent mostly use real-time data. To make accurate credit risk decisions, easy access to data across the whole credit lifecycle is a must. And all teams must have access to the same data sets to ensure big picture decisioning. Without it, the insights needed to get new products and processes to market faster and to make intelligent risk decisions remain hidden in silos of data.

Centralized Control: data and AI-powered decisioning across the customer lifecycle

To power continuous innovation across the customer lifecycle, organizations need to be able to launch, learn, and iterate with ease, but separate solutions for data and AI-decisioning slow innovation down. Consumers expect their experiences to be seamless, giving them access to tailored financial services products while also protecting them from financial fraud. To support this consumer need and business strategy, financial services organizations need to combine data and decisioning into one cohesive solution that can provide the technology to access, analyze, and action data across fraud, identity, and credit decisioning processes.

Auto-Optimization: decisioning that gets more accurate every time it’s used

Do you know how your current risk models are performing? Or whether model drift is occurring and unhealthy? How long would it take you to respond to performance changes once they’re spotted? Traditional decisioning has relied on human intervention to spot model performance changes and identify efficiency improvement options, meaning improvements happen on an ad-hoc basis, if at all.

To operate at maximum efficiency and run the most accurate models possible, your AI-powered decisioning and data solution needs a centralized UI that connects all necessary data so it can be used to power a continuous feedback loop, where both historical and real-time data are used to auto-optimize performance on an ongoing basis. Model performance and accuracy can be monitored and adjusted in real time.

Grow and Expand with Confidence: Technology that scales and grows with your business

One of the biggest obstacles financial services companies face is having technology that can support their business as it evolves and grows. For example, people often find it a challenge to support decisioning as application volume grows and their offerings expand. Sometimes the impact can be from delays waiting for vendors or in-house teams to make changes; often it means procuring or building new solutions to fill in technology gaps or completely replacing existing solutions. Whatever the path forward, the impact is the same… delayed growth, limited agility, and user frustration. To preempt future technology challenges, look for options that empower you to grow, expand, and change direction.

To truly thrive in an increasingly competitive industry, you need to provide consumers with world-class customer experiences. A unified data and AI-powered decisioning platform lets you make smarter decisions, faster. Use your technology’s powerful data integration and automation capabilities to create streamlined user experiences and drive real-time decisioning.

About the Author: Kim Minor is Senior Vice President, Marketing at Provenir, which helps fintechs and financial services providers make smarter decisions faster with its AI-Powered Risk Decisioning Platform. Provenir works with disruptive financial services organizations in more than 50 countries and processes more than three billion transactions annually.