This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Affirm has extended its partnership with Walmart to offer buy now, pay later (BNPL) tools at self-checkout stands.

Shoppers can use Affirm to pay for non-grocery purchases ranging from $144 to $4,000 in monthly installments.

Affirm also recently landed partnerships with Amazon and Google.

BNPL heavyweight Affirm ended 2023 announcing an expansion of a partnership with one of its major customers. The California-based company announced that Walmart will use its buy now, pay later (BNPL) technology at select self-checkout locations.

Reuters reported late last year that more than 4,500 Walmart stores in the U.S. will offer Affirm’s BNPL as an option to shoppers whose non-grocery purchases range between $144 to $4,000. Consumers will have the option to pay back their purchases in monthly installments spanning three months to 24 months.

To keep things simple at the point-of-sale kiosks, the BNPL onboarding process will take place on the user’s phone. Shoppers that opt to use BNPL to pay for their purchase will need to use their phone to log into Affirm’s mobile app or website and enter credentials, including the last four digits of their social security number. Once Affirm approves the customer, they will receive a barcode on their phone that they scan at the physical self-checkout register to complete the sale.

Walmart, which ended its layaway program in 2020, has offered Affirm’s BNPL technology to U.S. shoppers since 2019 at in-person checkout locations. Expanding the alternative payment option to the self-checkout and moving the onboarding process to the customer’s own mobile device reduces the friction that may occur when shoppers onboard to BNPL with the help of a cashier. This may result in an increased use of Affirm’s BNPL at Walmart’s point-of-sale.

The expansion of its collaboration with Walmart is the latest in a string of major partnerships for Affirm. Amazon tapped Affirm for Amazon Pay option in June of last year, and five months later, the ecommerce giant launched Affirm’s BNPL as a payment option for small businesses. Additionally, last month, Google announced it is using Affirm and its competitor Zip to provide BNPL options for shoppers using Google Pay.

Affirm is one of a handful of Walmart’s existing financial services partners. The retailer is also teamed up with Capital One, which offers a rewards credit card; Western Union, Ria, and MoneyGram for money transfer services; and Green Dot for its prepaid card. Interestingly, Walmart has been in the process of building its own neobank, One, since 2022, and many of One’s offerings compete with those of Walmart’s current partners.

HSBC announced the launch of a new money transfer and currency conversion app and debit card, Zing, this week.

Available in both iOS and Android, the app enables users to hold up to 10 different currencies and make transactions in local currency, avoiding point of sale currency conversion fees.

Zing was founded by HSBC head of FX and Payments James Allan.

Get ready Revolut and watch out Wise. There’s a new money transfer app coming to market courtesy of HSBC.

The new solution is an app and debit card combo called Zing. The money transfer and currency conversion solution will go live in the U.K. initially. But HSBC has international intentions for the technology. Nuno Matos, CEO of HSBC’s global wealth and personal banking business, noted in an interview with Bloomberg that Zing was part of HSBC’s ambition to be a platform for international payments. As such, Matos said that HSBC has a “global ambition” for Zing and expects to see the technology deployed in Asia, the Middle East, and Europe.

Available in both iOS and Android, Zing will be available this week in at the Apple Appstore and via Alphabet’s Google Play platform. Zing will enable users to hold up to 10 different currencies on the app, giving them the ability to lock in conversion rates and spend in local currency without having to deal with the cost of point-of-sale conversion fees. Users will also be able to send money internationally across more than 30 currencies.

HSBC has offered a currency transfer service, Global Money, since 2020. The company says that Global Money has served “hundreds of thousands” of customers to date and processed approximately $11 billion in transactions in 2022. That said, because HSBC customers and non-HSBC customers alike can use the app, the company hopes that Zing will help encourage non-HSBC customers to do more banking with HSBC.

Zing was founded by James Allan, head of FX and Payments at HSBC. In a statement, he referenced a company study that underscored the frustration many people have with money transfer and currency conversion services. “That’s why now is the time for a new kind of international payments solution,” Allan said, “one that combines cutting-edge innovation with the support of an experienced global bank.”

Our final Finovate Global column of 2023 celebrates the conversations we’ve had this year with fintech innovators from around the world.

Stay tuned in 2024 for more interviews with some of the most interesting founders, entrepreneurs, and thought leaders in fintech and financial services.

“We developed BehaviorQuant because every financial decision is ultimately made by a person or a team. BehaviorQuant solves a core problem that underlies the entire investment industry: we don’t have systematic knowledge about the people and teams behind investment decisions. And that’s true for financial professionals and clients alike.” Dr. Thomas Oberlechner, founder and CEO of BehaviorQuant. Interview.

“Moniepoint solves the problem of fragmented, inaccessible, and low-quality financial services for businesses in emerging markets. It is a full-service business banking platform seeking to provide all the digital financial services a typical business needs.” Tosin Eniolorunda, founder and CEO of Moniepoint. Interview.

“Eight hundred million voice conversations are recorded daily in Europe and many more worldwide. A tiny 1% of these conversations are checked for quality control, employee training, and business results improvement. Ender Turing is a conversations intelligence and automation platform to close 99% of the conversation gap for business growth.” Olena Iosifova, CEO of Ender Turing. Interview.

“Capital raising is broken. Private companies spend months and even years in the fundraising process, learning how to raise capital and repeating the same mistakes, approaching the wrong investors and often spamming them with irrelevant investment opportunities.” Ulyana Shtybel, CEO of Quoroom. Interview.

“At Refine intelligence, our mission is to help banks regain that superpower of really knowing their customers’ life stories, so their financial crime teams can quickly clear AML or scam alerts triggered by legitimate customer activity. We work with Risk, Financial Crime, BSA and AML teams. Fraud teams look at our technology to help with scam operations.” Uri Rivner, co-founder and CEO of Refine Intelligence. Interview.

“It was an honor to be ranked by CB Insights in its Fintech 250 list and, as one of only seven African start-ups featured, it speaks to the pioneering approach we are introducing to the world – revolutionizing payments and creating a financial services ecosystem for Africa.”

“As sub-Saharan Africa gains recognition on the global stage, we are seeing innovative and pioneering products emerge and rise in popularity amongst consumers, diversifying the products they can choose from.” Tayo Oviosu, founder and CEO of Paga. Interview.

Here is our look at fintech innovation around the world.

Asia-Pacific

Singaporean fiat-to-crypto payment gateway Alchemy Pay forged a partnership with Worldpay from FIS.

Indonesian P2P fintech JULO added insurance coverage with the launch of its JULO Cares solution.

Hungary’s OTP Bank partnered with Intellect Global Consumer banking (iGCB), the consumer banking arm of Indian banking technology copany Intelltect Design Arena.

Join Finovate VP and host of the Finovate Podcast Greg Palmer as he wraps up 2023 and gets us ready for 2024 with a quartet of conversations about the latest trends in fintech and financial services.

From life stories about women and men who became fintech converts, founders, and innovators later in their professional careers to discussions on enabling technologies like Generative AI, the Finovate Podcast is a great place to hear some of the smartest voices in our business talk about what matters most.

Podcast host Greg Palmer sits down with Barry Kirby and Dave Buerger of Union Credit, winners of the “Best Emerging Technology” category of the 2023 Finovate Awards. EP 197.

Greg Palmer interviews Dhairya Dholiya, Vice President of Growth & Innovation at Celtic Bank, on his transition from innovator to banker. EP 196.

Greg Palmer talks with tech founder, venture investor, and Head of Innovation for Better, Nneka Ukpai, on the lessons learned from a recovering lawyer turned innovator. EP 195.

Host Greg Palmer and Experian VP of Strategy, Global ID and Fraud David Britton discuss Generative AI and fraud – why it’s so scary and what you can do about it. EP 194.

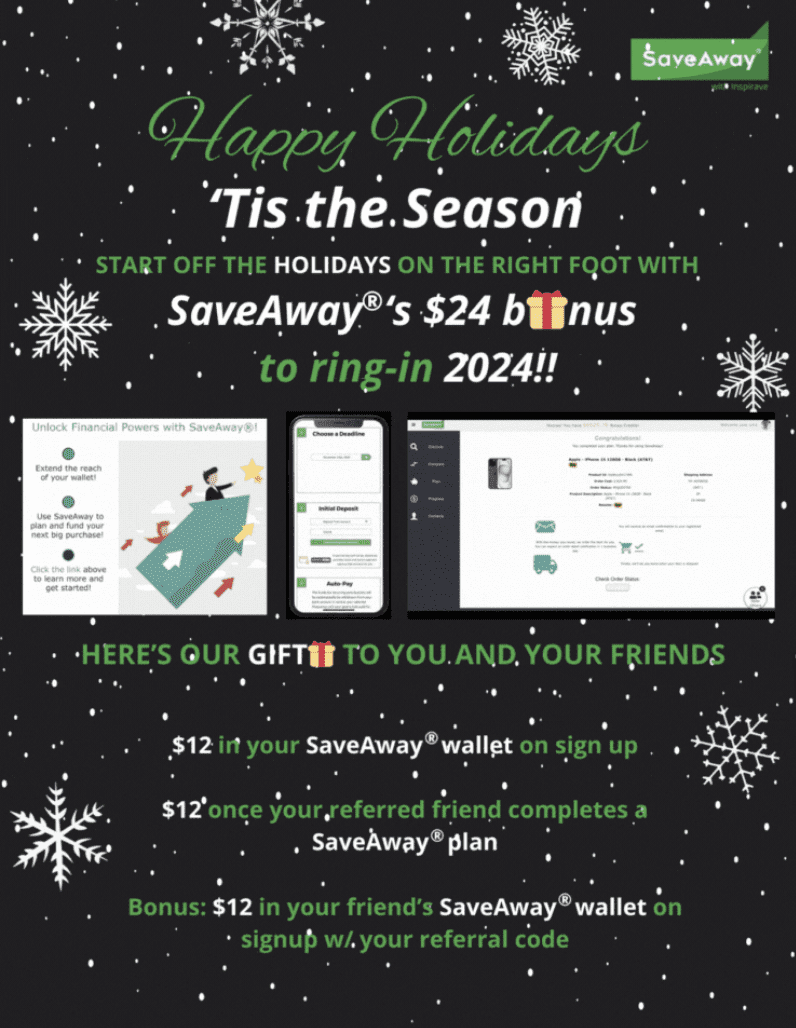

SaveAway is celebrating the season with its “$24 to Ring in ’24 program. The new offering, timed for the New Year, will put $12 in the SaveAway wallet of new sign ups and another $12 for any referral who signs up and completes a SaveAway plan. That’s $24 for new users who bring along a referral now through January 2024.

In an email, CEO and founder Om Kundu explained the thinking behind the “$24 to Ring in ’24” plan. “The $24 to ring in 2024 initiative is a recognition for those joining the remarkable company of our pioneering users and partners who have seen the merits of SaveAway first-hand,” Kundu said.

“SaveAway is social by design, as well as its proprietary engineering – $24 to Ring in ’24 is the celebratory spirit to recognize, and make the opportunity for our users to refer other SaveAway users that much more rewarding.”

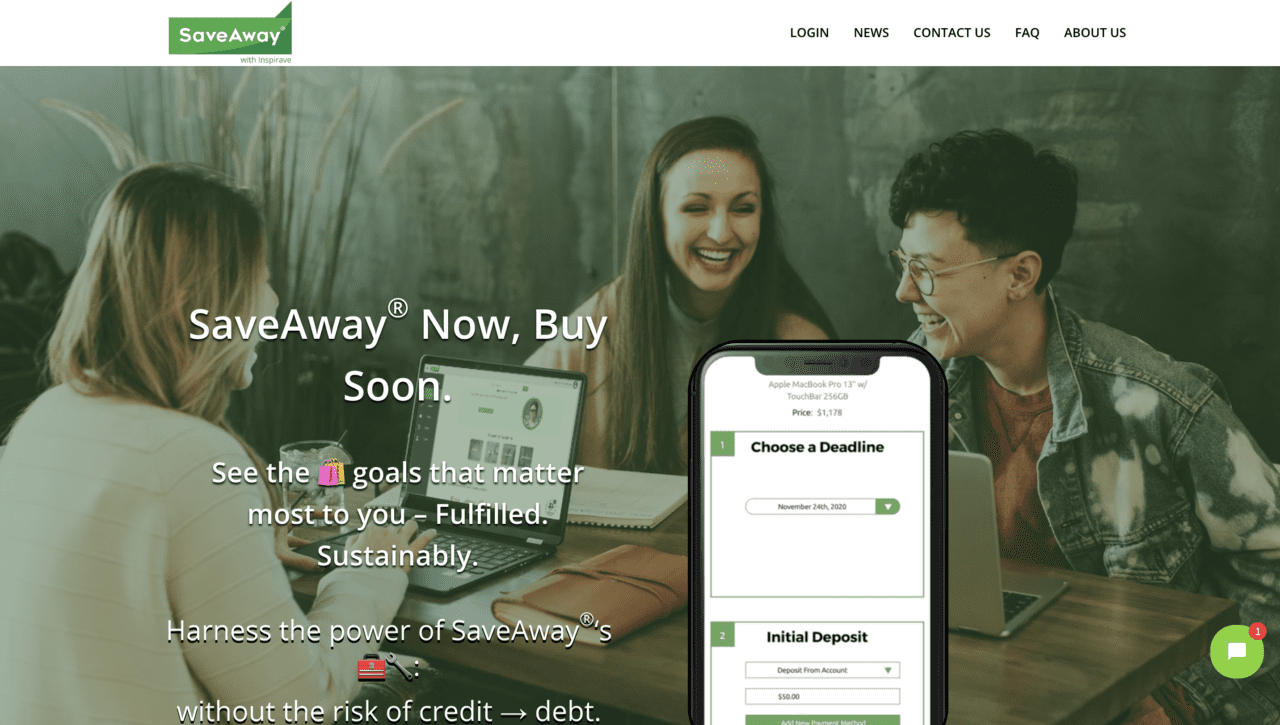

The company’s “SaveAway Now, Buy Soon” approach offers a departure from the world of Buy Now, Pay Later. The social saving and retail e-commerce platform enables consumers to buy important purchases responsibly, without having to rely on credit.

In this way, the solution combines intelligent financial planning with a sustainable path-to-purchase. The platform’s social gifting functionality enables members of the user’s trusted social network of friends and family to both support sensible spending as well as help users make purchases that they cannot afford on their own.

Users have praised the ease with which they can invite friends and family to participate in the spending process – voting on options and gifting toward the eventual purchase. The SaveAway platform also lets users see the progress they are making toward their purchase goal based on their personalized savings plan.

SaveAway made its Finovate debut at FinovateFall 2016. Earlier this year, Kundu facilitated the Fintech and E-Commerce Meetup at the SXSW conference, and the Retail Transformation+Evolution at the NRF Big Show Table Talk. Also this year, NYCEDC tapped SaveAway as a recipient of its Founder Fellowship. The fellowship offers resources for technology entrepreneurs from historically underrepresented backgrounds.

SaveAway will begin 2024 as a presenter at VentureCrushFGX having been selected to the 14th cohort of the VentureCrushFG Pod. Run by the Tech Group at legal firm Lowenstein Sandler, VentureCrush offers programs and events for startup founders and investors. The Wall Street Journal ranked Lowenstein Sandler as one of the top five most active law firms in the U.S. in terms of the number of VC/PE deals completed.

With a spot Bitcoin ETF expected in 2024, crypto investors, traders, and enthusiasts are likely feeling as optimistic about digital assets as they have in awhile.

As the trauma of Sam Bankman-Fried and FTX fades further into the background, the digital asset community has been able to refocus its energies on a number of positive developments in the space – from the surging price of crypto assets like bitcoin to the increasing interest in cryptocurrencies from major financial institutions.

So with the year drawing to a close, here are a few recent crypto- and blockchain-oriented headlines that you might have missed.

Coindesk’s reporting is based on a published memo from the SEC’s Office of Market Supervision, Division of Trading and Markets. The memo notes the subject of the meeting as “Meeting with BlackRock re: iShares Bitcoin Trust”, lists the meeting participants, and indicates that the conversation “concerned The NASDAQ Stock Market’s proposed rule change to list and trade shares of the iShares Bitcoin Trust under NASDAQ Rule 5711(d).”

What does this mean for a Bitcoin ETF in 2024? Rule 5711(d) refers to a variety of specific criteria required for listing and trading shares on the Nasdaq exchange. But especially noteworthy are aspects of this rule has to do with market integrity and protections against potentially fraudulent activity. We’ve covered the “surveillance-sharing” issue before in 5 Tales from the Crypto, so it is no surprise to find that the SEC is still looking to dot “i’s” and cross “t’s” as we move closer to a potential new ETF product for crypto investors and traders.

Saylor on Bitcoin: “Biggest Wall Street Development in 30 Years”

Michael Saylor, former CEO and current Executive Chairman of MicroStrategy, was interviewed on Bloomberg TV earlier this week. Asked about the potential of a Bitcoin ETF in 2024, Saylor said that the launch of a Bitcoin ETF next year could be “the biggest Wall Street development in 30 years.” He went on to say that he thought that the launch of an institutionally supported Bitcoin ETF could ignite a major bull market in crypto assets as a new surge in demand confronts current (inadequate) supply.

In his comments Saylor compared the emergence of a Bitcoin ETF to the launch of the S&P 500 ETF, popularly known as the SPY, more than 30 years ago.

Headquartered in Tysons Corner, Virginia, and founded in 1989, MicroStrategy is a long-time Finovate alum. The company made its Finovate debut in 2013 at FinovateSpring in San Francisco. MicroStrategy is a public company, trading on the Nasdaq under the ticker MSTR. The firm has a market capitalization of $8 billion.

Blockchain-based micropayments company raises seed funding

Swiss-fintech Centi, which offers blockchain-based micropayment solutions, announced the completion of a seed funding round this week. The amount of the investment was not disclosed. The round was led by Archblock and Bloomhaus Ventures, with current shareholders and founders also participating. The company will use the funds to help fuel global expansion.

Centi leverages blockchain technology to address two significant challenges in the payments industry: the inefficiency of micropayments and the issue of financial inclusion. Centi responds to these problems with its proprietary stablecoin technology that facilitates transactions as small as a cent. This creates new opportunities in digital content monetization for merchants, creatives, and others.

The Swiss firm also offers a direct-to-consumer stablecoin that can be purchased with fiat currency. This technology supports financial inclusion by giving unbanked consumers a pathway to digital payments.

“We founded Centi driven by the potential of blockchain for micropayments and financial inclusion,” Centi co-founder Bernhard Müller said. “The name ‘Centi’ itself, derived from our capability to process transactions as small as one cent, encapsulates this focus.”

Connecting crypto and banking pays for Fiat Republic

Europe continues to be the source of crypto funding news this week as Fiat Republicannounced a seed extension round of $7 million (€6.4 million). The investors include first-timers Kraken Ventures, Fabric Ventures, Arca, and Inovo Ventures. Existing investors Speedinvest, Credo Ventures, and Seedcamp also participated in the funding. Fiat Republic will use the capital to support growth and expansion, as well as make strategic hires and fortify banking partnerships.

London-based Fiat Republic helps crypto platforms connect with crypto-friendly banks. The company’s platform allows crypto firms to create accounts in multiple currencies and access local payment rails and FX via a single API.

Fiat Republic’s funding announcement comes as the company reports that it has been granted a full electronic money institution (EMI) license by the Netherlands’ De Nederlandsche Bank (DNB). This license will enable Fiat Republic to offer regulated financial services throughout the European Economic Area (EEA). These services include the ability to offer payment services and issue e-money to EEA crypto platforms courtesy of its API. The Dutch license is the second earned by the company; Fiat Republic has held an EMI license in the U.K. for more than a year.

Fiat Republic CEO and co-founder Adam Bialy said that the addition of the Dutch license was a major step for the two-and-a-half year old startup. “Passporting from the reputable and credible jurisdiction of the Netherlands not only boosts our legitimacy in the traditional finance world, but also highlights our commitment to high compliance standards, security, and close collaboration with regulators.”

Crypto Comeback? Looking back and leaping forward

There’s a lot for crypto investors, traders, and observers to be excited about as 2024 draws near: renewed bullishness in assets like Bitcoin and Ethereum, continued interest in crypto from institutional players and financial services incumbents … But before we go, here are a few last looks at crypto in 2023.

Payment provider Ping Payments has forged a partnership with open banking technology company Neonomics.

Via the partnership, Neonomics will manage end-user consents and account-to-account payments for Ping Payments.

Neonomics made its Finovate debut at FinovateEurope 2020 in Berlin. The company is headquartered in Oslo, Norway.

Ping Payments has announced a partnership with open banking technology company Neonomics. The Swedish payment provider will leverage its new relationship with Neonomics to enhance its account-to-account payment capabilities, identity verification, and compliance operations.

“Reach, market insight, and technical viability were paramount in our selection of a partner for expanding our services,” Ping Payments CEO Petter Sehlin said. “Neonomics has consistently demonstrated high quality throughout our relationship, and we are excited to expand our offering outside of Sweden across the Nordics with Neonomics.”

Courtesy of the partnership, Neonomics will manage end-user consents and account-to-account (A2A) payments for Ping Payments. Additionally, the partnership will feature open banking powered identity verification, a significant value-add when combined with account-to-account payment functionality. A specialist in providing payment solutions for platforms, SaaS companies, and marketplaces, Ping Payments will gain from Neonomics connections to Nordic-area banks, leveraging the company’s open banking API platform to reach FIs in Norway, Denmark, and Finland.

Neonomics founder and CEO Christoffer Andvig spoke to this aspect of the partnership in his comments. Andvig said, “With our advanced account verification solutions designed to mitigate risks and safeguard transactions, we will together strengthen payment and compliance processes across all customer touchpoints – bringing a future where transactions are inherently secure and seamless for all participants in the Nordic markets.”

Neonomics made its Finovate debut at FinovateEurope 2020 in Berlin, Germany. At the conference, the company demoed its technology that enables users to trigger instant payments and transfers from their bank, directly from an app or website.

Neonomics’ partnership news with Ping Payments comes just weeks after the company announced another collaboration, this time with Carbon Centrum. The goal of this partnership is to leverage open banking to help reduce carbon emissions. Also this year, Neononics announced that it was working with BetterNow to use open banking to enhance digital fundraising.

Both Ping Payments and Neonomics were founded in 2017. Ping Payments is based in Örebro, Sweden. Neonomics is based in Oslo, Norway.

Looking to demo your latest fintech innovation? Apply now to demo at FinovateEurope in London, February 27 and 28, 2024. Visit our FinovateEurope hub for more information.

Agency execution specialist Liquidnet has turned to investment technology company bondIT to give new tools to traders on its Fixed Income electronic trading platform. Liquidnet will leverage bondIT’s Scorable Credit Analytics to help traders better anticipate market trends. The technology will also help them mitigate credit risk and make more informed decisions quicker.

“With this integration, our goal is to give access to crucial information to investment firms of all sizes,” Liquidnet Global Head of Fixed Income Product and Partnership Programs Nicholas Stephan explained. “Our members will have seamless access to a wide range of credit data giving them an extra edge ahead of making their trading decisions.”

Scorable Credit Analytics leverages data science, Explainable AI, and machine learning to help fixed income investors anticipate changes in credit ratings and spreads. The solution predicts downgrade and upgrade probability for 3,000+ rated corporate and financial issuers worldwide. Using insights such as these, traders can spot investment opportunities earlier and outperform peers. Courtesy of explainable AI, Scorable ensures transparency and allows users to understand the reasons behind the predictions. The integration will benefit Liquidnet’s 700+ member firms that access the platform’s primary and secondary market trading protocols for corporate bonds.

“Bonds are back, but so is risk,” bondIT Head of Global Client Business Dr. David Curtis said. “Technology becomes an ever more important ally in this dynamic financial landscape. The synergy between bondIT’s AI-driven Scorable Credit Analytics and Liquidnet’s platform empowers traders with actionable insights, enabling them to stay ahead in today’s volatile markets.”

Founded in 1999, Liquidnet is an institutional trading network headquartered in New York. More than 1,000 institutional investors in 49 markets across six continents use Liquidnet’s technology. Interdealer broker TP ICAP acquired the company in 2021 for $700 million.

Note that Liquidnet is not the first company this year to deploy bondIT’s Scorable solution. Wealth management solution provider First Rate announced a strategic partnership with bondIT in June. The Arlington, Texas-based firm integrated Scorable Credit Analytics into its own AI-driven reporting tool.

bondIT made its Finovate debut at FinovateFall in 2016. In the years since, the Israel-based fintech has grown into a 50+ person team, and partnered with some of the world’s leading asset managers, banks, and technology firms. In addition to Scorable Credit Analytics, bondIT offers two other solutions: Frontier and Embedded. Frontier provides data-driven, personalized, fixed income portfolio management. Embedded is bondIT’s end-to-end, integrated portfolio construction, research, and trading solution.

Finovate alums raised more than $1.2 billion in equity funding in 2023. The total funding for the year reflects the continued slowdown in fintech funding that began in 2022.

In the fourth quarter of 2023, eleven Finovate alums raised more than $307 million in equity funding. Note, however, that this sum does not include the equity portion of the investment secured by SumUp, for example. The quarterly total also does not include the investment received by Icon Solutions, the amount of which was undisclosed.

Previous Quarterly Comparisons

Q4 2022: More than $380 million raised by 15 alums

Q4 2021: More than $1.2 billion raised by seven alums

Q4 2020: More than $472 million raised by 17 alums

Q4 2019: More than $876 million raised by 21 alums

Q4 2018: More than $800 million raised by 19 alums

Nevertheless, the fourth quarter alumni fundraising total approximates that of both last year’s Q4 and the final quarter of 2020.

Top Quarterly Equity Investments

Adlumin: $70 million

Paysend: $65 million

Scalable Capital: $64.7 million

Three investments in the fourth quarter of 2023 stood out among the others: Adlumin, Paysend, and Scalable Capital all announced fundraisings of more than $60 million in Q4. Also noteworthy was the $40 million raised by Stash in October.

Combined, the top three quarterly equity investments from our alums represent more than 65% of the total alum funding haul for Q4 2023.

Here is our detailed alum funding report for Q4 2023.

If you are a Finovate alum that raised money in the fourth quarter of 2023, and do not see your company listed, please drop us a note at [email protected]. We would love to share the good news! Funding received prior to becoming an alum not included.

Digital conversations platform Eltropy announced a partnership with Magnifi Financial.

The two companies will work to build and launch Generative AI-based solutions for employees, customers, and members of community financial institutions.

Eltropy most recently demoed its technology at FinovateFall 2022 in New York.

Digital conversations platform Eltropy and Magnifi Financial are working together to launch Generative AI solutions to enhance employee training and improve the customer/member experience. Eltropy’s Generative AI tools are powered by large language models (LLMs) that are specifically designed for community financial institutions (CFIs). These tools have enabled CFIs to bring new efficiency to their operations and greater personalization to the products and services they offer. Speaking about the partnership in a statement, Magnifi Financial SVP for IT and Digital Brad Shafton highlighted the fact that Eltropy’s technology is especially geared toward the needs of community financial institutions.

“What sets Eltropy apart is not just their technology but also their dedication to understanding the credit union industry and their commitment to community financial institutions like ours,” Shafton said. “They continue to evolve, and that’s why we consider them a long-term partner, including for AI.”

Magnifi will deploy Eltropy’s technology in a number of ways, including enhancing the firm’s mortgage and lending operations. Additionally, Eltropy’s ChatGRT-style Employee Assistants enable customer-facing financial services workers – from contact center agents to tellers – to access vetted, verified customer data. The technology also automates tasks like e-mail response generation, using natural conversational language.

To this end, Eltropy co-founder and CEO Ashish Garg said that solutions based on Generative AI have the potential to provide credit unions and community banks with new “innovative ways to thrive.” Garg added, “Eltrophy’s generative AI tools are empowering forward-thinking CFIs to achieve this by accelerating and enhancing employee knowledge training, improving the member experience and ultimately fueling growth.”

Eltropy made its most recent Finovate appearance last year at FinovateFall 2022. The company’s partnership with Magnifi Financial follows news of a collaboration with fellow Finovate alum Jack Henry from earlier this month, and an integration with Fiserv’s full-service account processing platform Portico in November. In August, Eltropy teamed up with yet another Finovate alum, Alkami, to enhance digital conversations for financial institutions.

Headquartered in Milpitas, California, Eltropy has raised $25 million in funding. The company includes K1 Investment Management and Curql among its investors.

Headless checkout company Bold Commerce launched a dynamic payment feature for Bold Commerce.

The feature allows merchants to show only the payment options relevant to therm.

Bold Commerce has raised $44 million and is headquartered in Canada.

Headless checkout company Bold Commerceannounced the launch of its dynamic payment feature for its Bold Checkout product this week.

Bold Checkout is the company’s tailored checkout solution that aims to help businesses increase conversion, lifetime value, and average order value, ultimately driving more revenue. The newly launched dynamic payment feature offers companies the ability to expand and manage multiple different payment options, including digital wallets, buy now, pay later (BNPL) and account-to-account payments. By offering a wider range of payment methods, brands can reach more consumers and convert shoppers into buyers.

The dynamic payment feature complements Bold Checkout’s Payment Booster, which helps brands deliver payment options tailored for individual shoppers based on their profiles, the device they’re using, and past purchasing behavior. Bold Checkout harnesses extensive data to enable brands to deliver hyper-personalized experiences to their customers. By displaying only the payment methods pertinent to each individual, it ensures a tailored approach, preventing information overload by streamlining the available options at checkout.

“The only way to offer shoppers flexibility in payment methods–without going overboard on options–is to carefully curate and personalize options to them based on who they are, how they shop and where they’re shopping from,” said Bold Commerce CEO Peter Karpas. “The ability to personalize payments for individual shoppers rounds out a fully tailored checkout experience powered by Bold–from when shoppers enter the checkout to payment to even post-purchase. This not only increases conversion for brands, but increases average order value and customer lifetime value as well.”

Bold Commerce was founded in 2012 and is headquartered in Canada. Earlier this year, the company teamed up with PayPal to offer the payment technology among its options at checkout. And last month, Bold Commerce partnered with open banking technology company Link Money to help its merchant clients offer more payment options in the checkout experience for their end customers.

Bold Commerce has raised $44 million and has been named to Deloitte’s Tech Fast 50, E&Y’s Entrepreneur of the Year, and CBInsights’ Retail Tech 100.

Meniga has raised $16.5 million (€15 million) in Series D funding, bringing its total raised to $60.5 million (€55 million).

The round will be used to fuel the company’s new strategy that focuses on creating hyper-personalized insights and enabling payments capabilities that leverage open finance ecosystems for financial services companies.

Meniga is pursuing the new strategy after appointing Raj Soni as new CEO earlier this year.

Personal finance solutions fintech Meniga has landed $16.5 million (€15 million) in Series D funding.

Today’s round boosts the U.K.-based company’s total funding to $60.5 million (€55 million). Contributors include major European banks, Groupe BPCE and Crédito Agrícola, Omega ehf, and several existing shareholders.

Just as notable as the investment is what the funds will be used for. Meniga plans to use the round to fuel the company’s new strategy that focuses on creating data enrichment and hyper-personalized insights for financial services companies. Meniga will also shift to emphasize enabling payments capabilities that leverage open banking and open finance ecosystems for financial services firms.

The new strategy hatched after the company appointed Raj Soni as the new CEO earlier this year. Soni’s aim to simplify Meniga’s product portfolio, diversify into verticals beyond banks, target new customers in emerging markets, and create new operational hubs to drive growth and offer customer support.

“We are looking forward to seeing [Meniga’s] continued focus on enrichment as well as personalized insights,” said Groupe BPCE Chief Digital Officer Emmanuel Puga Pereira. “These capabilities are critical for all BPCE banks to effectively engage with their end users and we have seen firsthand how Meniga’s solution is a key component for banks to succeed.”

Meniga notes that part of today’s funding will also be used for clearing the company’s debt, which will make Meniga almost debt-free.

Founded in 2009, Meniga empowers digital banking experiences for 10 million end users and serves more than 100 million banking customers across 30 countries in Europe, North America, the Middle East and Asia. Among the company’s clients are UOB, UniCredit, Groupe BPCE, Crédito Agrícola, Swedbank, and Commercial Bank of Dubai.

Meniga is among many fintechs and financial services firms that are shifting their focus to operate in the new open finance economy, where accessibility, data-driven insights, and personalized experiences reign supreme. Meniga’s strategic pivot underscores the industry-wide recognition that open banking and open finance will transform financial services for the better. It also sets a precedent for customer-centric developments going forward into 2024.