This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

A U.S. presidential election with, essentially, two incumbent presidents running for office. An enduring war in Europe. A new war in the Middle East. Economic instability in China. Lingering inflationary concerns and interest rate volatility.

If the fintech industry doesn’t have enough to worry about on its own, the prospect of macro economic and geopolitical events making life even tougher for fintech and financial services is enough to make your head spin. What do banks and fintechs need to know – and do – to effectively manage the current and evolving geopolitical landscape?

To help you better brace yourself for what 2024 may bring, we’ve invited Manas Chawla, founder and CEO of London Politica, to deliver both a fireside chat and keynote address at FinovateEurope in February.

With the theme, The Global Economic & Geopolitical Outlook – What Are the Five Things You Need to Know? Chawla will outline how many of our current challenges could impact the financial services industry – and what they can do about it.

We last caught up with Manas Chawla at FinovateSpring last May. Then, concerns over the impact of inflation and rising interest rates on banks were top of mind. In this interview from the conference, Chawla explained the challenges and opportunities for banks and fintechs that lie not just in black swan events, but in what he called “grey rhino” risks, as well.

Join us next month at FinovateEurope to hear more from Chawla and other insightful analysts and observers on the impact of macro trends on fintech and financial services.

While many people unplugged from their work computers last week to enjoy holiday festivities, the news in the fintech world didn’t stop moving. As you sift through the backlog of emails, voicemails, and meetings post-vacation, here’s a handy news digest we’ve curated for you.

Dive into the latest in fintech news as we unpack the biggest headlines from the past week, making it easier for you to catch up on what you missed.

1

December 18: Salesforce Signs Definitive Agreement to Acquire Spiff Utah-based compensation platform Spiff has agreed to be acquired by Salesforce. Financial terms of the deal were undisclosed. Salesforce will integrate the Spiff team into its Sales Cloud team, a group that aims to enhance Salesforce’s Sales Performance Management solutions.

2

December 19: Walmart Taps Affirm to Offer BNPL Option at Self-checkout Buy now, pay later (BNPL) heavyweight Affirm has extended its partnership with Walmart to offer its BNPL solution at select Walmart self-checkout stands. Shoppers can use Affirm to pay for non-grocery purchases ranging from $144 to $4,000 in monthly installments.

3

December 21: Circle Secures Conditional Digital Asset Service Provider Registration Massachusetts-based Circle received a conditional registration as a Digital Asset Service Provider (DASP) with the French Financial Markets Authority. The company’s goal is to have its European operations brought under comprehensive EU oversight with both a full DASP and Electronic Money Institution license. Circle also appointed Coralie Billmann as head of French operations.

4

December 21: Saudi Arabia-based Tabby Lands $700 Million Credit Facility from JP Morgan Chase Saudi Arabia-based BNPL platform Tabby received a $700 million credit facility from JP Morgan Chase. Since it was founded in 2019, Tabby has brought in a total of $1.7 billion in combined debt and equity funding. The news comes before the company’s planned listing on the Saudi Stock Exchange.

5

December 22: Blackstone Agrees to Acquire Sony Payment Services Private equity group Blackstone has agreed to acquire Sony Payment Services. The firm is acquiring Sony Payment Services from Sony Group’s Sony Bank, which will still support Sony Payment Services as a minority investor. The acquisition marks Blackstone’s first investment in a Japan-based fintech company.

6

December 25: Libyan Islamic Bank taps Backbase to Enhance Customer Experience in Digital Channels Libyan Islamic Bank partnered with Backbase to “streamline its customer service operations and enhance its customers’ digital banking experience.” The move, which is expected to reduce Libyan Islamic Bank’s friction in both onboarding and servicing, will revamp the bank’s existing mobile app for retail customers and introduce new digital apps for business users.

7

December 26: Grayscale Chair Barry Silbert Resigns CEO and Founder of Digital Currency Group Barry Silbert resigned as Grayscale Investments chairman. Digital Currency Group, which is Grayscale Investments’ parent company, is currently caught up in lawsuits from U.S. regulators. Digital Currency Group Chief Financial Officer Mark Shifke is replacing Silbert as chairman.

8

December 27: OakNorth Brings on Lord Adair Turner as New Chairman U.K. neobank OakNorth has appointed Lord Adair Turner as its Chairman. Lord Turner has previously served as Vice-Chairman of Merrill Lynch Europe, has been a Board Director of Standard Chartered, was Chair of the Financial Services Authority, and is a founding member of the Financial Policy Committee.

9

December 28: Saudi Fintech Tameed Closes $15 Million Series A Funding Round Small business lending platform Tameed received $15 million in funding. The round was led by Alromaih Group in Riyadh. Saudi Arabia-based Tameed will use the funding to fuel its growth to meet demand for its Shariah-compliant financing products.

10

January 1: HSBC Launches Money Transfer and Currency Conversion App Zing HSBC launched a new money transfer and currency conversion app with companion debit card. The new tool, called Zing, is available for both iOS and Android. With Zing, users can hold up to 10 different currencies and make transactions in local currency, avoiding point of sale currency conversion fees.

Blackstone has agreed to acquire Sony Payment Services.

The firm is acquiring Sony Payment Services from Sony Group’s Sony Bank, which will still support Sony Payment Services as a minority investor.

The acquisition marks Blackstone’s first investment in a Japan-based fintech company.

Private equity group Blackstone has agreed to take a majority stake in Japan-based Sony Payment Services (SPSV). The firm is acquiring SPSV from Sony Group subsidiary Sony Bank. Sony Bank will continue to support SPSV as a minority investor.

The acquisition marks Blackstone’s first investment in a Japan-based fintech company. The firm’s other Japan-based acquisitions have centered around the pharmaceutical industry. In 2002, Blackstone acquired AYUMI Pharmaceutical and Alinamin Pharmaceutical, a deal that marked the largest healthcare transaction in the market ever.

“We are thrilled to invest in SPSV… and expand our Japan Private Equity portfolio in ‘good neighborhoods’ – sectors with strong secular growth,” said Blackstone Japan Head of Private Equity Atsuhiko Sakamoto. “Digitization of the economy is a key trend around the world including Japan, and SPSV is exceptionally positioned to benefit with its sophisticated technology and robust customer base. We’re committed to bringing our operational and technology expertise and scale to support SPSV’s growth.”

Sony established its payment services group in 1995, and the group became a standalone company when it established SPSV in 2006. Headquartered in Tokyo, SPSV offers infrastructure for online payments processing.

“For the past 30 years, SPSV has led Japan’s cashless evolution, making payments safe and secure for customers,” said Sony Group Chairman and CO Kenichiro Yoshida. “We believe Blackstone, a long-standing partner of Sony Group, can help continue the legacy that SPSV has formed and support its next phase of growth.”

Combining Sony’s legacy and Blackstone’s expertise brings potential for SPSV to further innovate in Japan’s cashless evolution. This collaboration suggests there may be room for more strategic partnerships between traditional industry players and investment firms to foster innovation and drive advancement in the payments industry.

Founded in 1985, Blackstone counts more than $1 trillion in assets under management. The firm serves both institutional and individual investors with a wide range of portfolio companies and investment vehicles including private equity, real estate, public debt and equity, infrastructure, life sciences, growth equity, opportunistic, non-investment grade credit, real assets, and secondary funds.

Chase has teamed up with debt advice charity StepChange to build upon its own efforts to support customers with financial challenges.

Courtesy of the partnership, Chase specialists will direct vulnerable customers to StepChange for free, confidential, expert advice on debt management.

Founded in 1993, StepChange is headquartered in Leeds, U.K.

A new partnership between Chase and U.K.-based debt advice charity StepChange extends the bank’s efforts to provide support to vulnerable customers via expert advice on debt management. Chase specialists will now direct these customers to StepChange and its online debt advice solution. The online tool is free to use and will help Chase customers build a budget that will ensure they can meet their financial obligations. Customers can communicate with the tool via webchat or phone and all information submitted to StepChange is confidential.

In a statement, StepChange Director of Client Experience Gail Arkle underscored why it was important for people with debt challenges to seek assistance rather than try to solve the problem on their own. “92% of the people we support say that they wish they’d asked for help earlier,” Arkle said, “and so working closely with leading organizations like Chase is crucial to ensure we can identify and support customers who are experiencing financial difficulty as early as possible.”

According to a 2023 FCA Financial Lives survey, there has been a significant increase in what it calls “low financial resilience” as the cost of living increased in 2023. The survey defines low financial resilience as adults who are experiencing financial challenges due to missed payments on “domestic bills or credit commitments in three or more of the previous six months.” Overall, the survey revealed that just under 13 million in the U.K. have low financial resilience.

Today’s partnership is another example of how banks are becoming more involved in the financial wellness of their customers. “Financial stress can take a toll on a person’s mental wellbeing and be a constant source of worry,” Chase Managing Director for Customer Operations Alexa Collinson said. “Finding free, impartial and trusted advice is often the first step to putting an action in place.”

The largest provider of free debt advice in the U.K., StepChange works with thousands of individuals across the country. A registered charity, the company helps people improve their financial wellness via better budgeting, responsible credit card use, and debt management and repayment. StepChange has partnered with more than 900 banks, retailers, local authorities, and charities since its inception in 1993.

Last month we shared the first round of demoing companies to make the cut for FinovateEurope 2024. With more names on the way, we wanted to take a moment to highlight the return of three alums who will be demoing their latest fintech innovation live on stage in London next month, February 27 through 28.

NayaOne: De-risking innovation and facilitating partnership

A Best of Show winner in its Finovate debut last year, NayaOne offers a secure, Digital Sandbox platform that helps banks take the risk out of innovation, integration, and partnership with fintechs. Financial institutions that use NayaOne’s platform gain single key access to more than 350 technology vendors that are being actively evaluated by banks, a secure digital sandbox environment, and 2.5 billion datapoints to facilitate evaluation and review of new technologies.

NayaOne’s approach allows banks to review multiple vendors simultaneously. This helps them get their proofs-of-concept evaluated faster, saving money and enabling greater integration-induced productivity with less integration-related risk.

Among the company’s 2023 highlights are, most recently, its partnership with market network and technology platform PIMFA WealthTech. NayaOne teamed up with the wealthtech firm last fall to launch a client analytics and profiling tech sprint. The goal of the tech sprint was to explore how both unstructured and alternative data can be used to identity and attract potential clients. The sprint also examined use cases for Large Language Models in client services, such as pre-onboarding.

The partnership with PIMFA WealthTech came in the wake of NayaOne’s securing of the Digital Sandbox tender from the U.K. Financial Conduct Authority last spring. “We believe that our digital transformation platform and synthetic data technology will be a valuable asset in helping fintech companies to develop and test their products more efficiently and effectively,” NayaOne CEO Karan Jain said in April.

NayaOne also announced partnerships with Polymesh, which joined the NayaOne Network in June, and Valley National Bank, which deployed its innovation platform – powered by NayaOne – the previous month.

Headquartered in London, U.K., NayaOne was founded in 2019. The company most recently demoed its technology at FinovateFall in September.

NF Innova: Turning traditional banks into digital leaders

NF Innova will return to the Finovate stage next month at FinovateEurope. The company made its Finovate debut at FinovateEurope in 2014 and was among the alums to participate in FinovateAfrica in Cape Town four years later.

Headquartered in Vienna, Austria, and founded in 2013, NF Innova demoed its FINTENSE Omnichannel Digital Banking Platform at FinovateEurope 2023. At the conference, the company showcased its innovation in personal finance management, leveraging augmented reality to enable users to see their financial data in a new and compelling way.

In addition to augmented reality, NF Innova’s platform automates a number of customer-facing processes, including account opening. In fact, the company notes that firms using its technology have experienced efficiency increases of up to 600% thanks to NF Innova’s end-to-end automation of five different customer facing digital products.

NF Innova also reports faster times in completing common operations ranging from credit card payments to loans, as well as greater efficiency when it comes to orchestrating digital channels and segmentation.

In August NF Innova announced a strategic partnership with proactive mobile app security company Promon. The alliance will integrate Promon’s state-of-the-art technology to enhance security for users of NF Innova’s FINTENSE platform. NF Innova began 2023 by opening the doors on new offices in Čačak, Serbia, to provide workspace closer to where a number of its employees live.

Realmonitor: Helping banks benefit more from the homebuying process

Proptech innovator Realmonitor offers a white-label, AI-based property discovery mobile app designed to help address the specific pain points of the real estate market in Central and Eastern Europe. Because of the way properties are advertised in the CEE, there are often pricing discrepancies and anomalies that make the market difficult for home sellers, buyers, and agents.

Realmonitor brings transparency to this market by featuring all listings on the market from listing sites, Facebook Marketplace, Groups, and other locations. The technology conducts price comparisons to identify the best offers for advertised properties and provides instant push notifications when opportunities arise.

At the same time, banks benefit from an increase in mortgage loan prospects, as well as early engagement insofar as prospective homebuyers have used their whitelabled solution to find their properties.

Last month, Realmonitor won recognition as the most promising Hungarian fintech and Beyond Banking Solution of the Year at the FinTechShow. In its seventh year in 2023, the FinTechshow is an opportunity for fintechs and financial services companies in the country to “discuss digital transformation directions, new technological trends, and challenges.

“The application helps users throughout the entire journey of searching for, buying and selling real estate, and in relation to renovations and maintenance, with a specialist search engine,” Realmonitor founder Péter Faragó said upon receiving the award. “The greatest value of the application is that it helps save time for the user, who can handle everything related to the purchase, renovation, and maintenance of a home in one place, through one platform.”

Interested in demoing at FinovateEurope in London next month? Applications are still being accepted from innovative companies with new solutions that are ready to show. Visit our FinovateEurope hub today to learn more.

Affirm has extended its partnership with Walmart to offer buy now, pay later (BNPL) tools at self-checkout stands.

Shoppers can use Affirm to pay for non-grocery purchases ranging from $144 to $4,000 in monthly installments.

Affirm also recently landed partnerships with Amazon and Google.

BNPL heavyweight Affirm ended 2023 announcing an expansion of a partnership with one of its major customers. The California-based company announced that Walmart will use its buy now, pay later (BNPL) technology at select self-checkout locations.

Reuters reported late last year that more than 4,500 Walmart stores in the U.S. will offer Affirm’s BNPL as an option to shoppers whose non-grocery purchases range between $144 to $4,000. Consumers will have the option to pay back their purchases in monthly installments spanning three months to 24 months.

To keep things simple at the point-of-sale kiosks, the BNPL onboarding process will take place on the user’s phone. Shoppers that opt to use BNPL to pay for their purchase will need to use their phone to log into Affirm’s mobile app or website and enter credentials, including the last four digits of their social security number. Once Affirm approves the customer, they will receive a barcode on their phone that they scan at the physical self-checkout register to complete the sale.

Walmart, which ended its layaway program in 2020, has offered Affirm’s BNPL technology to U.S. shoppers since 2019 at in-person checkout locations. Expanding the alternative payment option to the self-checkout and moving the onboarding process to the customer’s own mobile device reduces the friction that may occur when shoppers onboard to BNPL with the help of a cashier. This may result in an increased use of Affirm’s BNPL at Walmart’s point-of-sale.

The expansion of its collaboration with Walmart is the latest in a string of major partnerships for Affirm. Amazon tapped Affirm for Amazon Pay option in June of last year, and five months later, the ecommerce giant launched Affirm’s BNPL as a payment option for small businesses. Additionally, last month, Google announced it is using Affirm and its competitor Zip to provide BNPL options for shoppers using Google Pay.

Affirm is one of a handful of Walmart’s existing financial services partners. The retailer is also teamed up with Capital One, which offers a rewards credit card; Western Union, Ria, and MoneyGram for money transfer services; and Green Dot for its prepaid card. Interestingly, Walmart has been in the process of building its own neobank, One, since 2022, and many of One’s offerings compete with those of Walmart’s current partners.

HSBC announced the launch of a new money transfer and currency conversion app and debit card, Zing, this week.

Available in both iOS and Android, the app enables users to hold up to 10 different currencies and make transactions in local currency, avoiding point of sale currency conversion fees.

Zing was founded by HSBC head of FX and Payments James Allan.

Get ready Revolut and watch out Wise. There’s a new money transfer app coming to market courtesy of HSBC.

The new solution is an app and debit card combo called Zing. The money transfer and currency conversion solution will go live in the U.K. initially. But HSBC has international intentions for the technology. Nuno Matos, CEO of HSBC’s global wealth and personal banking business, noted in an interview with Bloomberg that Zing was part of HSBC’s ambition to be a platform for international payments. As such, Matos said that HSBC has a “global ambition” for Zing and expects to see the technology deployed in Asia, the Middle East, and Europe.

Available in both iOS and Android, Zing will be available this week in at the Apple Appstore and via Alphabet’s Google Play platform. Zing will enable users to hold up to 10 different currencies on the app, giving them the ability to lock in conversion rates and spend in local currency without having to deal with the cost of point-of-sale conversion fees. Users will also be able to send money internationally across more than 30 currencies.

HSBC has offered a currency transfer service, Global Money, since 2020. The company says that Global Money has served “hundreds of thousands” of customers to date and processed approximately $11 billion in transactions in 2022. That said, because HSBC customers and non-HSBC customers alike can use the app, the company hopes that Zing will help encourage non-HSBC customers to do more banking with HSBC.

Zing was founded by James Allan, head of FX and Payments at HSBC. In a statement, he referenced a company study that underscored the frustration many people have with money transfer and currency conversion services. “That’s why now is the time for a new kind of international payments solution,” Allan said, “one that combines cutting-edge innovation with the support of an experienced global bank.”

Our final Finovate Global column of 2023 celebrates the conversations we’ve had this year with fintech innovators from around the world.

Stay tuned in 2024 for more interviews with some of the most interesting founders, entrepreneurs, and thought leaders in fintech and financial services.

“We developed BehaviorQuant because every financial decision is ultimately made by a person or a team. BehaviorQuant solves a core problem that underlies the entire investment industry: we don’t have systematic knowledge about the people and teams behind investment decisions. And that’s true for financial professionals and clients alike.” Dr. Thomas Oberlechner, founder and CEO of BehaviorQuant. Interview.

“Moniepoint solves the problem of fragmented, inaccessible, and low-quality financial services for businesses in emerging markets. It is a full-service business banking platform seeking to provide all the digital financial services a typical business needs.” Tosin Eniolorunda, founder and CEO of Moniepoint. Interview.

“Eight hundred million voice conversations are recorded daily in Europe and many more worldwide. A tiny 1% of these conversations are checked for quality control, employee training, and business results improvement. Ender Turing is a conversations intelligence and automation platform to close 99% of the conversation gap for business growth.” Olena Iosifova, CEO of Ender Turing. Interview.

“Capital raising is broken. Private companies spend months and even years in the fundraising process, learning how to raise capital and repeating the same mistakes, approaching the wrong investors and often spamming them with irrelevant investment opportunities.” Ulyana Shtybel, CEO of Quoroom. Interview.

“At Refine intelligence, our mission is to help banks regain that superpower of really knowing their customers’ life stories, so their financial crime teams can quickly clear AML or scam alerts triggered by legitimate customer activity. We work with Risk, Financial Crime, BSA and AML teams. Fraud teams look at our technology to help with scam operations.” Uri Rivner, co-founder and CEO of Refine Intelligence. Interview.

“It was an honor to be ranked by CB Insights in its Fintech 250 list and, as one of only seven African start-ups featured, it speaks to the pioneering approach we are introducing to the world – revolutionizing payments and creating a financial services ecosystem for Africa.”

“As sub-Saharan Africa gains recognition on the global stage, we are seeing innovative and pioneering products emerge and rise in popularity amongst consumers, diversifying the products they can choose from.” Tayo Oviosu, founder and CEO of Paga. Interview.

Here is our look at fintech innovation around the world.

Asia-Pacific

Singaporean fiat-to-crypto payment gateway Alchemy Pay forged a partnership with Worldpay from FIS.

Indonesian P2P fintech JULO added insurance coverage with the launch of its JULO Cares solution.

Hungary’s OTP Bank partnered with Intellect Global Consumer banking (iGCB), the consumer banking arm of Indian banking technology copany Intelltect Design Arena.

Join Finovate VP and host of the Finovate Podcast Greg Palmer as he wraps up 2023 and gets us ready for 2024 with a quartet of conversations about the latest trends in fintech and financial services.

From life stories about women and men who became fintech converts, founders, and innovators later in their professional careers to discussions on enabling technologies like Generative AI, the Finovate Podcast is a great place to hear some of the smartest voices in our business talk about what matters most.

Podcast host Greg Palmer sits down with Barry Kirby and Dave Buerger of Union Credit, winners of the “Best Emerging Technology” category of the 2023 Finovate Awards. EP 197.

Greg Palmer interviews Dhairya Dholiya, Vice President of Growth & Innovation at Celtic Bank, on his transition from innovator to banker. EP 196.

Greg Palmer talks with tech founder, venture investor, and Head of Innovation for Better, Nneka Ukpai, on the lessons learned from a recovering lawyer turned innovator. EP 195.

Host Greg Palmer and Experian VP of Strategy, Global ID and Fraud David Britton discuss Generative AI and fraud – why it’s so scary and what you can do about it. EP 194.

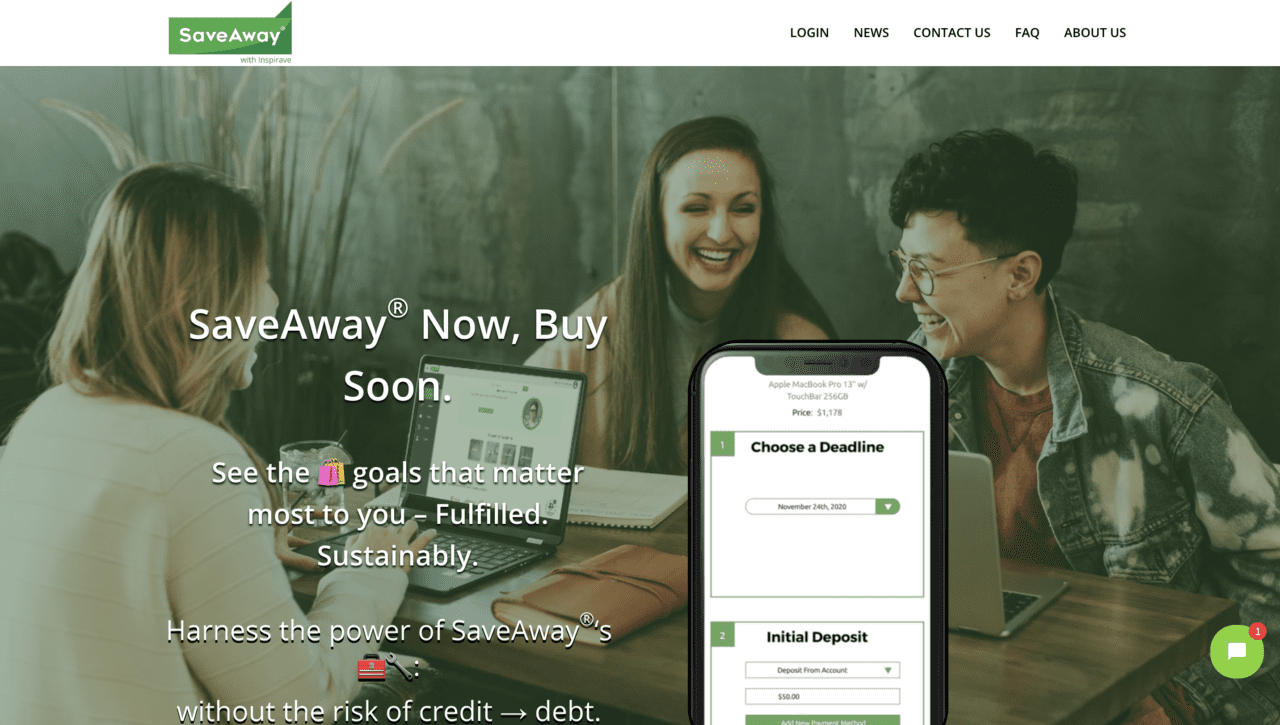

SaveAway is celebrating the season with its “$24 to Ring in ’24 program. The new offering, timed for the New Year, will put $12 in the SaveAway wallet of new sign ups and another $12 for any referral who signs up and completes a SaveAway plan. That’s $24 for new users who bring along a referral now through January 2024.

In an email, CEO and founder Om Kundu explained the thinking behind the “$24 to Ring in ’24” plan. “The $24 to ring in 2024 initiative is a recognition for those joining the remarkable company of our pioneering users and partners who have seen the merits of SaveAway first-hand,” Kundu said.

“SaveAway is social by design, as well as its proprietary engineering – $24 to Ring in ’24 is the celebratory spirit to recognize, and make the opportunity for our users to refer other SaveAway users that much more rewarding.”

The company’s “SaveAway Now, Buy Soon” approach offers a departure from the world of Buy Now, Pay Later. The social saving and retail e-commerce platform enables consumers to buy important purchases responsibly, without having to rely on credit.

In this way, the solution combines intelligent financial planning with a sustainable path-to-purchase. The platform’s social gifting functionality enables members of the user’s trusted social network of friends and family to both support sensible spending as well as help users make purchases that they cannot afford on their own.

Users have praised the ease with which they can invite friends and family to participate in the spending process – voting on options and gifting toward the eventual purchase. The SaveAway platform also lets users see the progress they are making toward their purchase goal based on their personalized savings plan.

SaveAway made its Finovate debut at FinovateFall 2016. Earlier this year, Kundu facilitated the Fintech and E-Commerce Meetup at the SXSW conference, and the Retail Transformation+Evolution at the NRF Big Show Table Talk. Also this year, NYCEDC tapped SaveAway as a recipient of its Founder Fellowship. The fellowship offers resources for technology entrepreneurs from historically underrepresented backgrounds.

SaveAway will begin 2024 as a presenter at VentureCrushFGX having been selected to the 14th cohort of the VentureCrushFG Pod. Run by the Tech Group at legal firm Lowenstein Sandler, VentureCrush offers programs and events for startup founders and investors. The Wall Street Journal ranked Lowenstein Sandler as one of the top five most active law firms in the U.S. in terms of the number of VC/PE deals completed.

With a spot Bitcoin ETF expected in 2024, crypto investors, traders, and enthusiasts are likely feeling as optimistic about digital assets as they have in awhile.

As the trauma of Sam Bankman-Fried and FTX fades further into the background, the digital asset community has been able to refocus its energies on a number of positive developments in the space – from the surging price of crypto assets like bitcoin to the increasing interest in cryptocurrencies from major financial institutions.

So with the year drawing to a close, here are a few recent crypto- and blockchain-oriented headlines that you might have missed.

Coindesk’s reporting is based on a published memo from the SEC’s Office of Market Supervision, Division of Trading and Markets. The memo notes the subject of the meeting as “Meeting with BlackRock re: iShares Bitcoin Trust”, lists the meeting participants, and indicates that the conversation “concerned The NASDAQ Stock Market’s proposed rule change to list and trade shares of the iShares Bitcoin Trust under NASDAQ Rule 5711(d).”

What does this mean for a Bitcoin ETF in 2024? Rule 5711(d) refers to a variety of specific criteria required for listing and trading shares on the Nasdaq exchange. But especially noteworthy are aspects of this rule has to do with market integrity and protections against potentially fraudulent activity. We’ve covered the “surveillance-sharing” issue before in 5 Tales from the Crypto, so it is no surprise to find that the SEC is still looking to dot “i’s” and cross “t’s” as we move closer to a potential new ETF product for crypto investors and traders.

Saylor on Bitcoin: “Biggest Wall Street Development in 30 Years”

Michael Saylor, former CEO and current Executive Chairman of MicroStrategy, was interviewed on Bloomberg TV earlier this week. Asked about the potential of a Bitcoin ETF in 2024, Saylor said that the launch of a Bitcoin ETF next year could be “the biggest Wall Street development in 30 years.” He went on to say that he thought that the launch of an institutionally supported Bitcoin ETF could ignite a major bull market in crypto assets as a new surge in demand confronts current (inadequate) supply.

In his comments Saylor compared the emergence of a Bitcoin ETF to the launch of the S&P 500 ETF, popularly known as the SPY, more than 30 years ago.

Headquartered in Tysons Corner, Virginia, and founded in 1989, MicroStrategy is a long-time Finovate alum. The company made its Finovate debut in 2013 at FinovateSpring in San Francisco. MicroStrategy is a public company, trading on the Nasdaq under the ticker MSTR. The firm has a market capitalization of $8 billion.

Blockchain-based micropayments company raises seed funding

Swiss-fintech Centi, which offers blockchain-based micropayment solutions, announced the completion of a seed funding round this week. The amount of the investment was not disclosed. The round was led by Archblock and Bloomhaus Ventures, with current shareholders and founders also participating. The company will use the funds to help fuel global expansion.

Centi leverages blockchain technology to address two significant challenges in the payments industry: the inefficiency of micropayments and the issue of financial inclusion. Centi responds to these problems with its proprietary stablecoin technology that facilitates transactions as small as a cent. This creates new opportunities in digital content monetization for merchants, creatives, and others.

The Swiss firm also offers a direct-to-consumer stablecoin that can be purchased with fiat currency. This technology supports financial inclusion by giving unbanked consumers a pathway to digital payments.

“We founded Centi driven by the potential of blockchain for micropayments and financial inclusion,” Centi co-founder Bernhard Müller said. “The name ‘Centi’ itself, derived from our capability to process transactions as small as one cent, encapsulates this focus.”

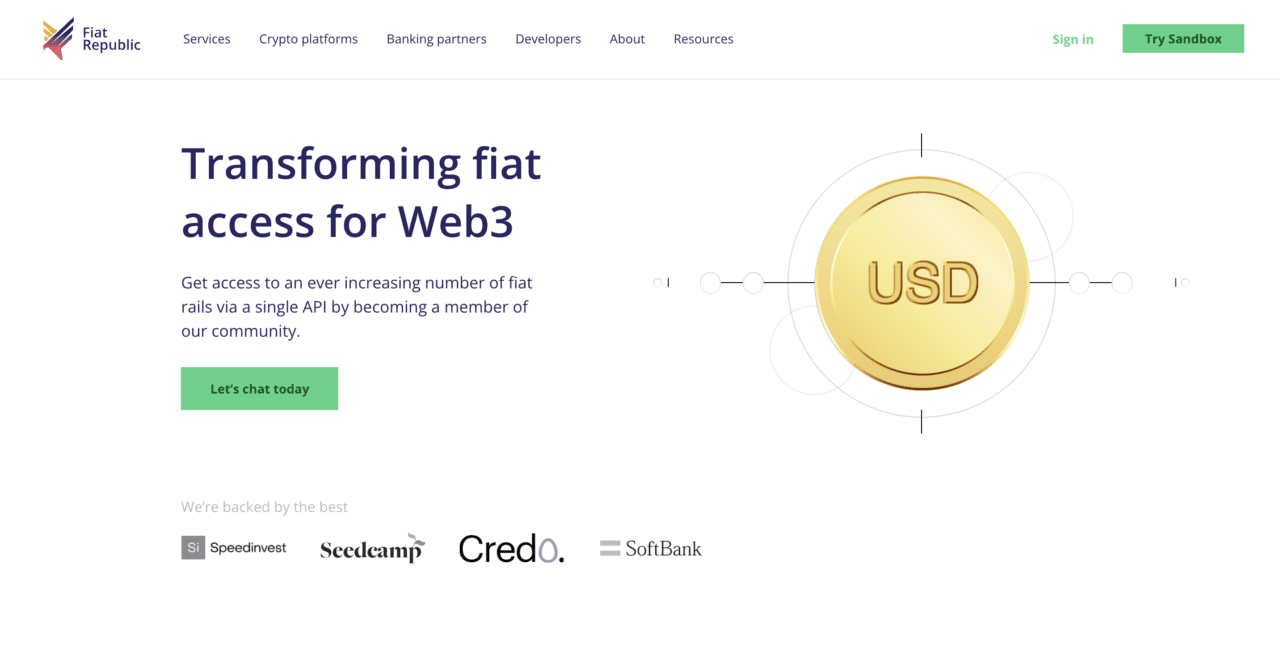

Connecting crypto and banking pays for Fiat Republic

Europe continues to be the source of crypto funding news this week as Fiat Republicannounced a seed extension round of $7 million (€6.4 million). The investors include first-timers Kraken Ventures, Fabric Ventures, Arca, and Inovo Ventures. Existing investors Speedinvest, Credo Ventures, and Seedcamp also participated in the funding. Fiat Republic will use the capital to support growth and expansion, as well as make strategic hires and fortify banking partnerships.

London-based Fiat Republic helps crypto platforms connect with crypto-friendly banks. The company’s platform allows crypto firms to create accounts in multiple currencies and access local payment rails and FX via a single API.

Fiat Republic’s funding announcement comes as the company reports that it has been granted a full electronic money institution (EMI) license by the Netherlands’ De Nederlandsche Bank (DNB). This license will enable Fiat Republic to offer regulated financial services throughout the European Economic Area (EEA). These services include the ability to offer payment services and issue e-money to EEA crypto platforms courtesy of its API. The Dutch license is the second earned by the company; Fiat Republic has held an EMI license in the U.K. for more than a year.

Fiat Republic CEO and co-founder Adam Bialy said that the addition of the Dutch license was a major step for the two-and-a-half year old startup. “Passporting from the reputable and credible jurisdiction of the Netherlands not only boosts our legitimacy in the traditional finance world, but also highlights our commitment to high compliance standards, security, and close collaboration with regulators.”

Crypto Comeback? Looking back and leaping forward

There’s a lot for crypto investors, traders, and observers to be excited about as 2024 draws near: renewed bullishness in assets like Bitcoin and Ethereum, continued interest in crypto from institutional players and financial services incumbents … But before we go, here are a few last looks at crypto in 2023.

Payment provider Ping Payments has forged a partnership with open banking technology company Neonomics.

Via the partnership, Neonomics will manage end-user consents and account-to-account payments for Ping Payments.

Neonomics made its Finovate debut at FinovateEurope 2020 in Berlin. The company is headquartered in Oslo, Norway.

Ping Payments has announced a partnership with open banking technology company Neonomics. The Swedish payment provider will leverage its new relationship with Neonomics to enhance its account-to-account payment capabilities, identity verification, and compliance operations.

“Reach, market insight, and technical viability were paramount in our selection of a partner for expanding our services,” Ping Payments CEO Petter Sehlin said. “Neonomics has consistently demonstrated high quality throughout our relationship, and we are excited to expand our offering outside of Sweden across the Nordics with Neonomics.”

Courtesy of the partnership, Neonomics will manage end-user consents and account-to-account (A2A) payments for Ping Payments. Additionally, the partnership will feature open banking powered identity verification, a significant value-add when combined with account-to-account payment functionality. A specialist in providing payment solutions for platforms, SaaS companies, and marketplaces, Ping Payments will gain from Neonomics connections to Nordic-area banks, leveraging the company’s open banking API platform to reach FIs in Norway, Denmark, and Finland.

Neonomics founder and CEO Christoffer Andvig spoke to this aspect of the partnership in his comments. Andvig said, “With our advanced account verification solutions designed to mitigate risks and safeguard transactions, we will together strengthen payment and compliance processes across all customer touchpoints – bringing a future where transactions are inherently secure and seamless for all participants in the Nordic markets.”

Neonomics made its Finovate debut at FinovateEurope 2020 in Berlin, Germany. At the conference, the company demoed its technology that enables users to trigger instant payments and transfers from their bank, directly from an app or website.

Neonomics’ partnership news with Ping Payments comes just weeks after the company announced another collaboration, this time with Carbon Centrum. The goal of this partnership is to leverage open banking to help reduce carbon emissions. Also this year, Neononics announced that it was working with BetterNow to use open banking to enhance digital fundraising.

Both Ping Payments and Neonomics were founded in 2017. Ping Payments is based in Örebro, Sweden. Neonomics is based in Oslo, Norway.

Looking to demo your latest fintech innovation? Apply now to demo at FinovateEurope in London, February 27 and 28, 2024. Visit our FinovateEurope hub for more information.