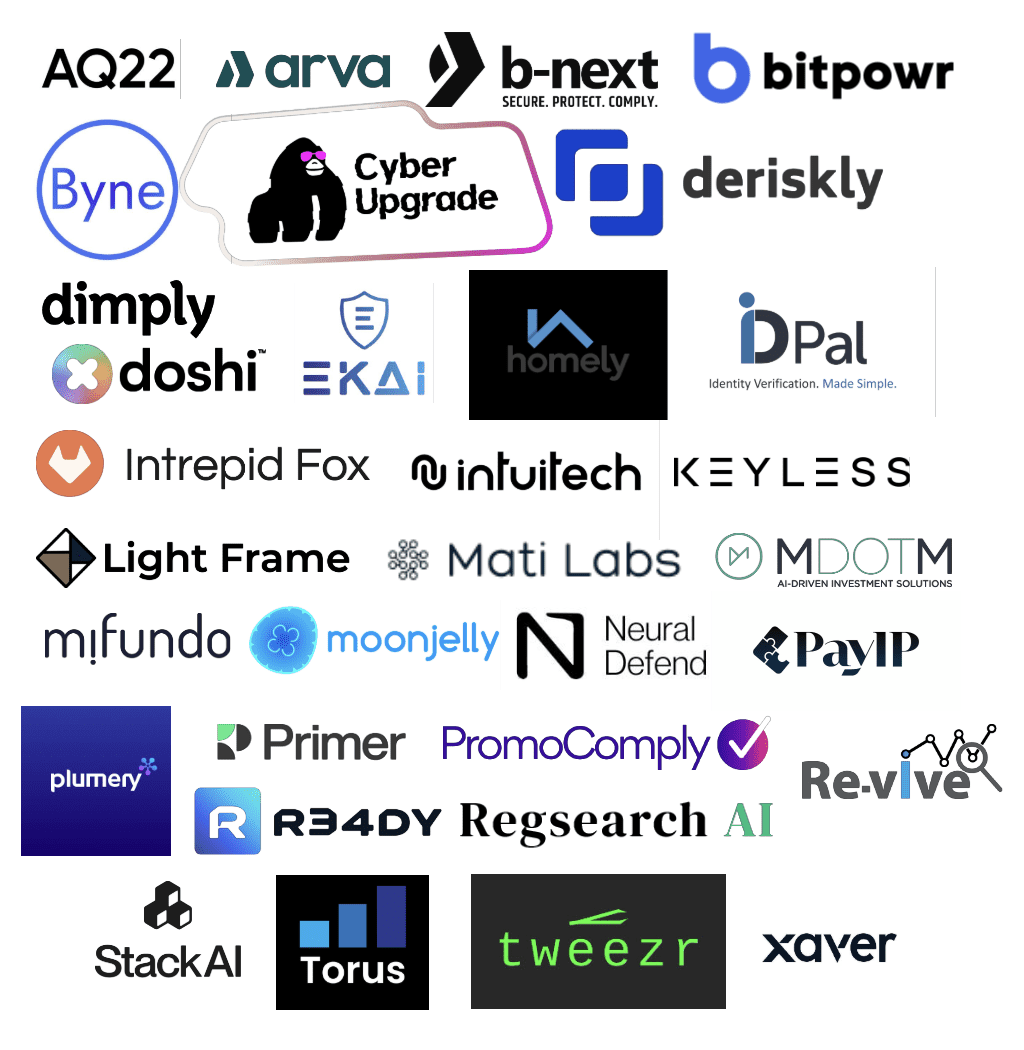

This year at FinovateEurope 2025, our 32 demoing companies represent a baker’s dozen of countries from around the world. Of the 32 companies, nine are headquartered in the UK, and seven of them are making their Finovate debuts this year.

Last year, FinovateEurope featured companies from 15 different countries. This year, we’re thrilled to see a similarly diverse group. Here’s where the rest of our FinovateEurope 2025 demoing companies are based.

- Arva AI – United States

- AQ22 – Lithuania

- Bitpowr Technologies – United States

- b-next – Germany

- CyberUpgrade – Lithuania

- Dimply – Ireland

- ID-Pal – Ireland

- Intuitech – Hungary

- Light Frame – United States

- Mati Labs – United States

- Mifundo – Estonia

- Moonjelly – The Netherlands

- Neural Defend – India

- PayIP – South Africa

- Plumery – The Netherlands

- PromoComply – Canada

- R34DY – Hungary

- Regsearch AI – Luxembourg

- RE-ViVE – United States

- Stack AI – United States

- Torus – Lithuania

- Tweezr – Israel

- Xavier – Germany

FinovateEurope is right around the corner: 25-26 February at the Intercontinental O2 in London. Friday, 14 February is the last day to take advantage of big, early-bird savings on the price of your ticket. If you haven’t registered yet, visit our FinovateEurope hub today and save your seat!

Here is our look at fintech innovation around the world.

Middle East and Northern Africa

- Tabby, a financial services and shopping app in MENA, announced a $160 million Series E funding round that brought the company’s valuation to $3.3 billion.

- Qatar-based Islamic financial institution Al Rayan Bank partnered with financial software application provider Finastra to launch its new Islamic core banking solution.

- Israel fintech BitStock raised $400,000 in seed funding.

Central and Southern Asia

- The Banker featured Golomt Bank and the rise of open banking in Mongolia.

- Indian digital payments firm ToneTag secured $78 million in new funding.

- TBC Uzbekistan announced successful deployment of its AI-based, proprietary Uzbek language models.

Latin America and the Caribbean

- Ripple teamed up with Portuguese currency exchange provider Unicâmbio to support cross-border payments between Portugal and Brazil.

- Brazilian payments and banking technology provider Dock introduced new Chief Technology Officer Thiago Teixeira.

- Latin American global collections firm Takenos launched its Spicy Card, enabled by Pomelo, in Argentina.

Asia-Pacific

- Malaysian Earned Wage Access (EWA) specialist Payd raised $400,000 in an extension of its seed funding round.

- New Zealand’s Inland Revenue service issued a Request for Information (RFI) as part of an effort to influence the growth of open banking in the country.

- Bangladesh-based commercial bank Trust Bank teamed up with TerraPay to help students pay tuition fees.

Sub-Saharan Africa

- Nigeria-based multi-currency accounts platform Raenest secured $11 million in Series A funding in a round led by QED Investors.

- South African fintech Stitch acquired ExiPay, a company that enables brick-and-mortar stores to securely accept in-person payments via point-of-sale (POS) terminals.

- Advanced Television looked at the evolution of South African fintech marketing.

Central and Eastern Europe

- Berlin-based invoicing and payables automation management platform Monite unveiled iFrame solution to help SMB platforms deliver financial products and services.

- UK-based supply chain finance provider Orbian announced plans to acquirer Czech payment institution Roger.

- German accounting, taxation, and payroll startup Integral raised $6.5 million (€6.3 million) in pre-seed funding in a round led by General Catalyst and Cherry Ventures.