This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

From AI in the service of greater personalization and sales performance to innovations in voice authentication and fraud prevention, the latest round of interviews on the Finovate Podcast provide fascinating insights into how fintechs are helping financial institutions meet their most demanding challenges.

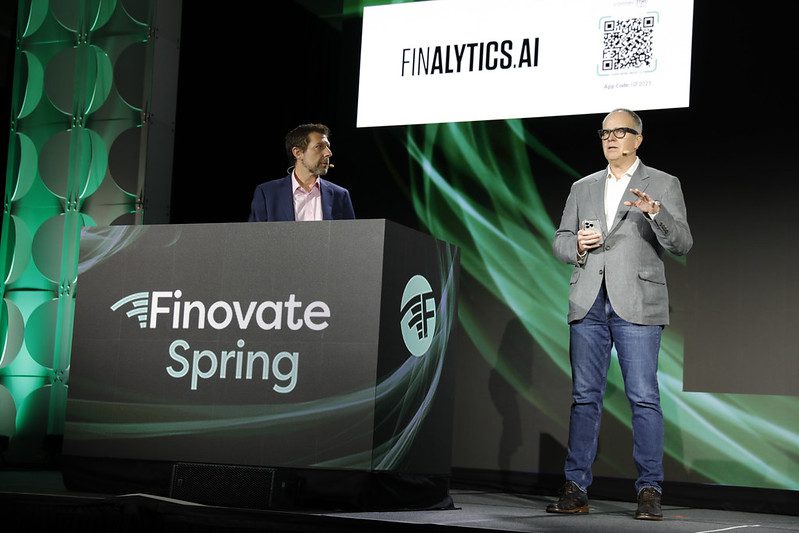

Finovate Podcast host Greg Palmer interviews Finalytics CEO Craig McLaughlin and CSO Baron Conway.

The three discuss how the Finalytics platform provides real-time, cross-channel, AI-driven personalization that combines behavioral data with transactional and third-party data to create unique, relevant experiences for customers of financial institutions.

Andrew Reese, US go-to-market lead for Solda.ai, joins Greg Palmer and the Finovate Podcast to talk about the company’s AI-powered sales agents that help financial institutions increase revenue and reduce costs by mirroring their best sales representative.

The technology helps scale sales operations, lower costs, reduce burnout and inconsistent performance, all while retaining a human connection.

Greg Palmer and Milind Borkar, founder and CEO of Illuma talk about the firm’s evolution from an authentication specialist to a more comprehensive fraud prevention company.

A two-time Finovate Best of Show winner, Illuma specializes in voice authentication and fraud prevention solutions for mid-market financial institutions, including credit unions and community banks.

Account-to-account (A2A) payment infrastructure company Token.io has received a strategic investment from HSBC. The amount was not disclosed.

The investment underscores the two companies’ history of collaboration, which includes Token.io’s support for HSBC’s Open Payments solution.

Token.io made its Finovate debut at FinovateSpring 2015 and returned to the Finovate stage two years later for FinovateEurope in London.

Token.io, an account-to-account (A2A) payment infrastructure innovator, secured a strategic investment from HSBC this week. The amount of the funding was not disclosed. The two firms have been partners since 2019, when Token.io helped the bank launch its HSBC Open Payments solution.

“We are excited to deepen our partnership with HSBC as we embark on this collaboration,” Token.io CEO Todd Clyde said. “This investment will not only accelerate Token.io’s growth and innovation, it will also advance our shared vision of making Pay by Bank a mainstream payment method—delivering benefits for HSBC’s customers across the region.”

Pay by Bank is a payments service that gives customers a secure, fast, and convenient way to conduct peer-to-peer payments, account deposits, and loan repayments, as well as securely authenticate transactions via their banking app. Supported by open banking and real-time payment infrastructure, Token.io’s technology makes the service available to anyone with a UK or European bank account. In a statement, the company noted that analysts believe in the future growth of Pay by Bank, predicting that three-in-four Europeans will be regular Pay by Bank users by 2029. In fact, by 2030, analysts estimate that use of Pay by Bank for e-commerce transactions in Europe will become more popular than all other digital payment options, with the exception of digital wallets.

HSBC’s Open Payments solution is based on this infrastructure. The technology enables businesses to connect their checkout pages with online apps or mobile platforms used by customers. Purchasers are given a request for pre-populated payments and, once the payment is authorized, the seller is granted an “instant and irrevocable credit” to their account. The new offering helps businesses get working capital faster and keeps both the risk of fraud and the cost of collections low.

“Our investment in Token.io reflects the trust and confidence we have in their team and technology, and our firm belief in the role that innovative Open Banking solutions play in transforming the payments experience for both corporates and consumers,” HSBC Head of Global Payments Solutions Manish Kohli said.

Founded in 2015 and headquartered in San Francisco, California, Token.io made its Finovate debut at FinovateSpring 2015 and returned two years later to demo its latest technology at FinovateEurope in London. A major account-to-account payment infrastructure provider for banks and other financial institutions, Token.io’s partners include three of the largest financial institutions in Europe as well as companies such as Global Payments and fellow Finovate alums Mastercard and ACI Worldwide.

Last month, Token.io became the first third-party provider to be admitted to the giroAPI scheme. This will enable the company to provide account-to-account payment solutions to its partners—including micropayments that are exempt from Strong Customer Authentication (SCA) requirements. Launched by the German Banking Industry Committee associations—BVR, DSGV, VÖB, and the Association of German Banks—at the beginning of the year, the API scheme is built on the Berlin Group’s openFinance API framework and provides a standardized, secure, and commercially governed interface to connect banks with third-party providers such as Token.io.

“By joining giroAPI, Token.io is enabling the next wave of premium, API-driven payment services—making it easier for businesses to offer innovative payment options and for consumers to benefit from seamless, secure experiences,” Token.io Chief Product Officer Charles Damen said. “We are proud to lead the way in bringing the full potential of open banking-enabled payments to the European market.”

Embedded ERP banking innovator FISPAN secured $30 million in Series B funding.

The round was led by Canapi Ventures and featured participation from existing investors, including Rhino Ventures.

FISPAN most recently demoed its technology at FinovateEurope 2022 in London.

In a round led by Canapi Ventures, embedded ERP banking specialist FISPAN has raised $30 million in Series B funding. Existing investors, including Rhino Ventures, also participated in the round. In a statement, the company said that the funds will help FISPAN expand the set of ERP platforms it supports, add actionable insights to its Accounts Payables solution, and launch a new Accounts Receivables automation product. In addition to accelerated product development, FISPAN noted that the capital will help the firm scale its go-to-market efforts and expand its market reach as well as support strategic talent acquisition.

FISPAN helps businesses integrate banking services directly into their enterprise resource planning (ERP) systems and accounting software. The company helps banks maximize their investments in host-to-host and API platforms that have enabled large businesses to experience greater productivity by connecting to their financial institutions directly. FISPAN’s technology packages these connectivity capabilities to empower banks to deliver their treasury products to mid-market and smaller businesses by way of an easy-to-install, out-of-the-box, in-ERP plugin. This empowers banks to offer integrated client experiences via financial and banking capabilities that are embedded directly into their existing ERP systems. This facilitates centralized financial workflows, automated processes, and fewer manual errors for businesses.

“This Series B funding is a pivotal moment for FISPAN, empowering us to significantly scale our innovation and market reach,” FISPAN Founder and CEO Lisa Shields said. “Canapi quickly distinguished themselves through their understanding of the embedded ERP banking landscape and our unique opportunity within it. With an LP network of over 75 financial institutions—and partners with banktech operating expertise—Canapi is a natural partner for our next chapter. We’re excited to work with Canapi to help more treasury teams optimize their operations.”

A multi-stage venture capital firm, Canapi Ventures invests in fintech and enterprise software and is backed by the Canapi Alliance, whose network of leading financial institutions stretches across the US. As part of its investment in FISPAN, Canapi Ventures’ General Partner Tom Davis will join the company’s board of directors.

“FISPAN is at the forefront of a fundamental shift in how businesses interact with their banks,” Canapi Ventures General Partner Tom Davis said. “Their proven ability to deliver highly sought-after embedded finance solutions positions them for tremendous growth. Our investment reflects our confidence in their visionary team and their capacity to build a leading platform that drives efficiency and value for both financial institutions and their corporate clients.”

Founded in 2016 and headquartered in Vancouver, British Columbia, Canada, FISPAN made its Finovate debut in 2017 at FinovateFall in New York and most recently demoed its technology at FinovateEurope 2022 in London. The company counts the world’s largest banks and nearly 5,000 businesses throughout North America among its customers. FISPAN began 2025 announcing that partner BMO had launched its embedded banking solution, BMO Sync. The new offering will enable businesses to automate payments, streamline workflows, and achieve enhanced cash flow visibility to simplify the payments process.

Feedzai has launched Feedzai IQ, a fraud intelligence solution that uses anonymized, distributed data to deliver real-time risk assessments without compromising customer privacy.

Key features include TrustScore and TrustSignals, which provide network-wide fraud risk scores and indicators to improve accuracy and payment acceptance.

Early adopters like Jack Henry and Novobanco are piloting the solution, signaling a growing industry shift toward collaborative, AI-driven fraud prevention.

Risk management provider Feedzaiunveiled today that it has launched Feedzai IQ, a new fraud intelligence layer that uses anonymized, network-wide data to detect financial crime in real time without compromising privacy.

Unlike traditional data-sharing models that raise privacy and compliance concerns, Feedzai IQ uses anonymized, distributed data to generate real-time fraud insights without sharing raw customer data. This allows financial institutions to tap into the collective intelligence of the network while protecting sensitive information.

“We’ve always believed that the true power of AI is only unlocked through access to meaningful, high-quality data,” said Feedzai Chief Product Officer Pedro Barata. “While AI is surrounded by hype today, Feedzai has led the way in applying real AI to real problems—and now, with Feedzai IQ, we’re combining our AI expertise with secure, network-wide intelligence. It’s a breakthrough that takes fraud prevention to an entirely new level.”

Key elements to Feedzai IQ are TrustScore, which offers a real-time fraud risk score based on network-wide intelligence; and TrustSignals, risk indicators that increase accuracy and improve payment acceptance.

Among the firms piloting Feedzai IQ are industry leaders Jack Henry and Novobanco, signaling growing demand for fraud intelligence tools that balance security and customer experience. “Technology is enabling increasingly sophisticated fraud threats,” said Matt Riley, President of Complimentary Solutions at Jack Henry. “Innovations such as Feedzai IQ contribute significantly to the industry’s ability to adapt to emerging threats and enhance operational effectiveness.”

Feedzai was founded in 2011 as a risk operations platform specializing in identity verification, fraud prevention, and financial crime detection. The company’s AI-powered solutions span KYC, AML, watchlist screening, and transaction fraud monitoring to help financial institutions stop fraud in real time without compromising the customer experience. Today, Feedzai protects over one billion consumers in more than 190 countries and safeguards over $8 billion in transactions annually.

Financial crime compliance innovator ThetaRay announced a strategic partnership with cross-border payments platform Spayce.

The collaboration will combine ThetaRay’s Cognitive AI Transaction Monitoring solution with Spayce’s payments infrastructure to enhance the platform’s financial crime detection capabilities.

ThetaRay made its Finovate debut at FinovateFall 2015 in New York.

Cognitive AI financial crime compliance company ThetaRay is working with cross-border payments platform Spayce to bring enhanced security and fraud fighting ability to payments. The strategic partnership will combine ThetaRay’s Cognitive AI Transaction Monitoring solution with Spayce’s global payments infrastructure to give the platform better financial crime detection capabilities.

“Financial crime is evolving rapidly, and the technology used to combat it must evolve even faster,” ThetaRay CEO Peter Reynolds said. “Our partnership with Spayce unites robust payment infrastructure with ThetaRay’s Cognitive AI to deliver proactive risk mitigation, greater transparency, and the trusted cross-border transactions needed to power global growth.”

ThetaRay’s Cognitive AI technology analyzes transaction data to accurately identify suspicious activity and complex financial crimes. The company’s offering helps institutions better combat the growing sophistication of criminal networks who are able to thwart traditional rule-based anti-money laundering (AML) systems. Spayce will leverage ThetaRay’s AI-first solution to ensure regulatory compliance and scale securely.

“Partnering with ThetaRay empowers us to stay ahead of increasingly sophisticated financial threats, while continuing to deliver seamless, trusted payment experiences for our customers worldwide,” Spayce Co-Founder and Partner Debra LePage said.

Operating in more than 200 countries and territories, Spayce is a cross-border payment platform that enables secure and scalable global transactions. The company offers real-time payments via its Spayce Real-Time Payments solution, ACH via its Spayce ACH Payments solution, as well as Open Banking services. Use cases for Spayce’s solutions include vendor payouts, global payroll, ecommerce settlements, and real-time B2P and B2B payments via a combination of APIs, a hosted checkout solution, and a merchant portal.

Founded in 2013, ThetaRay made its Finovate debut at FinovateFall 2015 in New York. Today, the company offers transaction monitoring, dynamic customer risk assessment, and real-time transaction and customer screening to financial institutions around the world including Santander, Mashreq Bank, and Travelex. ThetaRay leverages Cognitive AI to help financial institutions distinguish legitimate customers from fraudsters, and its SaaS-based solutions provide companies with shorter implementation lifecycles as well as the ability to scale faster.

ThetaRay began 2025 with news that it had formed a strategic partnership with New York-based private and commercial bank, IDB Bank. The institution, a wholly owned subsidiary of Israel Discount Bank, deployed ThetaRay’s AI-powered transaction monitoring solution to “enhance (its) operational fortitude and core competencies” in the words of bank president and CEO Ziv Biron. “In leveraging ThetaRay’s next generation technology,” Biron added, “we hope to introduce an innovative solution that will allow IDB to continue providing strong protections within the financial services industry, for our customers and operations against financial crime.”

Digital wealth management and investing platform Scalable Capital has raised €155 million ($175 million). The largest funding round in the company’s history, the investment was led by Sofina and Noteus Partners, and featured participation from existing investors Balderton Capital, Tencent, and HV Capital. The funding brings Scalable Capital’s total raised to more than €470 million (more than $535 million).

Among Europe’s leading digital investment platforms, Scalable Capital enables traders and investors to buy and sell stocks, exchange-traded funds (ETFs), bonds, cryptocurrencies, derivatives, private equity, and other products. More than €30 billion is held on the Scalable Capital platform by more than one million customers. The company also offers Scalable Wealth, a digital wealth management service that provides clients with professional ETF portfolio investment. The service is also available as a white-label solution via Scalable Capital’s B2B partners.

“Noteus Partners and Sofina perfectly complement our global investor base. The recent funding round is a clear endorsement, and an important step on our path to becoming the leading retail investment platform in Europe,” Scalable Capital Founder and Co-CEO Erik Podzuweit said. “Through our investment platform and additional new products, we’ll be able to offer even more people in Europe the best options for their investments. We have a firm focus on wealth creation and saving for retirement for the whole family.”

Scalable Capital began the year with the launch of its private equity offering courtesy of a partnership with BlackRock. Available to Scalable Capital’s qualified investors in Germany via Scalable Broker, investors will be able to access the BlackRock Private Equity Fund, and invest with one-off investments of as little as €10,000. Scalable Capital is the first digital investment platform to offer the private equity solution from BlackRock, which is also available as a savings plan once the initial investment is made.

More recently, Scalable Capital announced that its clients can invest in Swiss stocks as of May 2, 2025. Tradable via the European Investor Exchange, gettex, and Xetra, access to Swiss stocks comes after more than five years of suspension from EU stock exchanges. Previously, EU investors were only able to invest in Swiss shares indirectly through products such as American Depository Receipts (ADRs) or by way of over-the-counter trading options. Revocation of this regulation went into effect at the beginning of the month.

“The Swiss stock exchange has much more to offer than the three big dividend aristocrats,” Scalable Capital Chief Economist Christian Röhl said, referring to Nestlé, Roche, and Novartis, three of the largest stocks in the Swiss stock market. “In addition to many financial stocks and special stocks such as mountain railways, there are numerous highly specialized market and technology leaders—such as the hearing aid manufacturer Sonova, the dental technician Straumann or the sanitary product manufacturer Geberit.”

Scalable Capital made its Finovate debut at FinovateEurope 2016 in London. Headquartered in Munich, Germany, and London, UK, the company was founded in 2014.

We’re halfway through 2025, and with two Finovate events in the books, there are clear themes emerging around the future of financial services and fintech.

In this edition of the Finovate eMagazine, we bring you insights from both sides of the Atlantic, featuring key learnings from FinovateEurope and FinovateSpring.

Fill in the form and discover the trends shaping the future of financial services and fintech. Explore:

The latest approaches to innovation

Hear from David Barton-Grimley and Bhoomika Ghosh on how to make innovation meaningful and impactful. Plus, David Penn brings us insight into how credit unions want to digitise and partner.

How to navigate global growth in today’s economy

Julie Muhn brings us the key regulatory shifts on both sides of the Atlantic and David Grace from SHAZAM explores the importance of partnerships to face the upcoming challenges

The Finovate Library on Streamly

This eMagazine brings you insights to inspire your business strategy and your future endeavours.

KeyBank has partnered with Personetics to integrate AI-driven financial wellness tools that offer real-time, personalized advice based on customers’ spending.

The bank will use Personetics’ Engage platform to deliver insights that help users make smarter financial decisions.

The move will help boost engagement and foster long-term customer loyalty.

KeyBankannounced this morning that it has partnered with Personetics to bring financial wellness to its customers. The Ohio-based bank will leverage Personetics’ Cognitive Banking platform, which analyzes consumer transactions and delivers advice.

Specifically, KeyBank will use Personetics’ Engage, a client experience that offers customers spending insights and recommendations based on their spending and savings habits.

KeyBank will implement Personetics’ Engage solution, which uses AI to deliver real-time, personalized insights based on customers’ spending and saving patterns. By identifying trends and anticipating future needs, Engage offers timely, actionable advice to help users make smarter financial decisions and reach their goals in order to transform the banking experience from transactional to advisory.

By embedding Personetics’ cognitive banking tools into its digital offering, KeyBank will help improve customer engagement, reduce attrition, and create new revenue opportunities through better financial outcomes.

“KeyBank’s mission is to help clients and communities thrive. A large part of that mission centers in helping clients move forward on their financial journeys and reach their financial goals,” said KeyBank Head of Consumer Digital Emily Gessner. “By leveraging Personetics’ platform and experience, we will address the financial burden and stress consumers face by empowering our clients with real-time insights and guidance to help them effectively manage their financial futures.”

KeyBank was founded in 1825 and has 1,000 branches across the US. The bank has acquired AQN Strategies, HelloWallet, First Niagara Financial Group, EverTrust Financial Group, Leasetec, and most recently BaaS provider XUP. Among the company’s strategic partners are AvidXchange, BillTrust, and Bill.com.

Headquartered in New York, and with offices in London, Tel Aviv, and Singapore, Personetics counts more than 150 million bank customers across the globe. The fintech was founded in 2010 and strives to help banks create “self-driving finance” experiences for its customers. Under this concept, banks leverage AI to proactively act on behalf of their clients to help them achieve their financial goals.

“This partnership isn’t just about innovation—it’s about using intelligent technology to forge deeper human relationships between banks and the people they serve,” said Personetics CEO Udi Ziv. “Cognitive Banking redefines how banks understand and support their customers and, as a result, fosters customer loyalty.”

The calendar turned over to June yesterday, which means that there’s just one month left until the summer news slowdown. Here’s your jumpstart on June’s fintech news. We’ll continue adding news to this post throughout the week, so stay tuned!

Block is launching Bitcoin for Businesses, a new feature that enables Square merchants to accept bitcoin payments via the Lightning Network, starting in late 2025.

The feature builds on Block’s existing Bitcoin Conversions tool, which allows merchants to automatically convert a portion of sales into bitcoin and offer seamless QR code payments.

This move reinforces Block’s commitment to bitcoin adoption and helps integrate crypto into everyday commerce.

Block is bringing bitcoin to the point of sale. The company behind Square announced this week that it will launch Bitcoin For Businesses, enabling merchants to accept bitcoin payments directly on Square hardware using the Lightning Network, a decentralized network using blockchain smart contracts for instant, low-cost payments.

The new offering on Square’s Point of Sale app leverages the Lightning Network to facilitate near-instant, low-cost transactions. Square’s integration calculates the real-time exchange rate and sends confirmation notifications.

This new functionality builds on Bitcoin Conversions, a feature Block launched in 2024 that allows merchants to automatically convert a portion of daily sales into bitcoin, accept bitcoin payments via QR code, and benefit from real-time exchange rates and instant confirmation. Combined, Bitcoin For Business and Bitcoin Conversions will create a more seamless experience for merchants, letting customers pay with bitcoin by scanning a QR code at checkout.

“Block has long been a champion of bitcoin, focused on making it more accessible and usable in our everyday lives,” said Block Bitcoin Product Lead Miles Suter. “Rolling out a native bitcoin experience to millions of sellers brings us one step closer to that goal. When a coffee shop or retail store can accept bitcoin through Square, small businesses get paid faster, and get to keep more of their revenue. This is about economic empowerment for merchants who like to have options when it comes to accepting payments.”

Bitcoin For Business will roll out in the second half of 2025 and is expected to reach all eligible Square sellers in 2026, subject to applicable regulatory approvals.

With Bitcoin For Businesses, Block is turning Square into a crypto-native payment network that offers merchants more payment flexibility while embedding bitcoin into everyday financial activity. The launch is another step toward Block’s long-term vision of turning Cash App, Square, and its open-source tools into the default platform for both traditional and decentralized finance.

Block, which rebranded from Square in 2021, offers a host of other bitcoin-based tools, including Cash App’s bitcoin buy, sell, and transfer capabilities; Bitkey, a bitcoin wallet; Proto’s bitcoin mining products and services; and Spiral, which builds and supports open-source bitcoin projects that promote economic empowerment.

Block is also well known for its purchase of Afterpay in 2022. The company rebranded Afterpay to Cash App Afterpay earlier this year. Block anticipated the name change to fully integrate Afterpay into Cash App, helping Block to turn Cash App into a one-stop financial platform.

This week’s edition of Finovate Global looks at fintech headlines from companies headquartered in North Africa.

Fayda wallet goes live in Ethiopia

Designed to revolutionize the way Ethiopians access digital services, Ethiopia’s National ID Program (NIDP) has launched its FaydaPass wallet. The solution, developed in partnership with TECH5 and Visa, will help promote financial inclusion and address the need for verified electronic Know Your Customer (eKYC) services throughout society.

The wallet makes it easier for Ethiopians to secure a digital copy of the Fayda credential by enabling them to download the official app and request their digital ID credentials via the wallet. The Fayda ID system uses its data to generate the secure credential, which is delivered directly to the user’s mobile device as a verifiable credential (VC). The verifiable credential supports secure on- and offline verification for a wide range of use cases including payments and digital access to government services.

“A credential wallet would be a container for government and private sector issued standardized verifiable credentials,” NIDP Executive Director Yodahe Zemichael said. “It’s an exciting new way of delivering value to citizens and extending the functionality of Fayda Digital ID.”

Ethiopian digital-first Coopbank announced that it would leverage the Fayda app and its advanced biometric eKYC verification to enable customers to open new bank accounts. The institution’s CEO Deribie Asfaw said that the new offering will help it “reach financially marginalized communities who have long been excluded from the formal financial system due to the absence of such robust infrastructures.” Asfaw added, “This brings us one step closer to the community and reinforces our commitment to leaving a meaningful mark on the country’s digital transformation journey.”

Founded in 2005, Coopbank (Cooperative Bank of Oromia) was established by farmers and still counts farmers as more than half of its shareholders. With a focus on the country’s micro, small, and medium-sized farming and agricultural sector businesses, the institution has assets of ETB 139.56 billion ($1.04 billion), operates 745 branches, and has more than 14.5 million accountholders.

TerraPay, Wave Mobile Money partner on remittances to Mali

A partnership between international money movement company TerraPay and African mobile money provider Wave Mobile Money will enhance cross-border remittances services in Mali. The collaboration will enable Malians to receive funds from family and friends living and working abroad directly into their Wave mobile wallets. This will provide for a faster, more accessible, and cost-effective international remittance experience.

Mobile phone penetration in Mali is high, with more than 80% of the population using the technology. Many Malians rely on mobile phones for mobile money and digital wallet services, making the devices a key component of financial inclusion in the country for millions—especially the un- and underbanked. The partnership between TerraPay and Wave Mobile Money will facilitate remittance flows from Money Transfer Operators (MTOs) through the US, Canada, and Europe to Mali via a single integration.

“Our partnership with Wave Mobile Money marks a significant milestone in our mission to power borderless money movement,” TerraPay Vice President—Sub Sahara Africa, Willie Kanyeki said. “By enabling instant, cost-effective, and fully compliant remittances from key markets like the US, Canada, and Europe, we are simplifying financial access and driving financial inclusion in Mali.”

TerraPay enables payments to 150+ receiving countries and 210+ sending countries. The company’s platform facilitates payments to more than 3.7 billion mobile wallets, 7.5 billion bank accounts, and more than 12 billion cards. Founded in 2014, TerraPay is headquartered in London. Co-founder Ambar Sur is CEO.

Founded in 2018 and operating in Mali since 2021, Wave Mobile Money offers domestic and cross-border transfers, bill payments, and business services to customers in Senegal, Côte d’Ivoire, Uganda, Gambia, Sierra Leone, Mali, and Burkina Faso. Headquartered in Dakar, Senegal, Wave Mobile Money is on a self-described mission to make Africa “the first cashless continent.” Drew Durbin and Lincoln Quirk are Co-Founders.

Tunisia’s Konnect Networks secures investment

Tunisia’s Konnect Networks has raised an undisclosed amount from Attijariwafa Ventures. The investment was part of a wider fundraising effort that featured Utopia Capital Management, 54 Collective, Visa, Plug and Play Tech Center, Renew Capital, Digital Africa Ventures, and Sunny Side Venture Partners as investors. The company said it would use the capital to help fuel both its continued expansion and further innovation in payments technology.

Founded in 2021 by Amin Ben Abderrahman, Konnect Networks provides payment links, e-commerce plugins, and APIs. Serving both retail and business customers, the firm’s payment orchestration platform covers online and point-of-sale payments, payment aggregation, and real-time transaction capabilities. The company’s funding news comes in the wake of it being approved as a Payment Facilitator (PayFac) by Tunisia’s central bank. Konnect Networks currently has 2,000 users of its technology in Tunisia.

Griffin has opened access to its MCP (Model Context Protocol) server, enabling developers to build AI-powered agentic applications that can simulate tasks like account opening, payments, and financial analysis.

The MCP server is currently available in a sandbox environment, allowing users to prototype autonomous finance workflows.

Griffin acknowledges that the launch is still in its early stages, but says that it shows what’s possible when it comes to agentic AI.

UK-based BaaS fintech Griffinannounced today that it is opening up access to its MCP server. The new server, which is currently in beta, offers a new way for users to build agentic applications directly on the banking system.

Griffin customers can use the MCP server to have an agent open accounts, make payments, and analyze historic events. They can also use it to build prototypes of their fintech applications on top of the Griffin API. Griffin acknowledges that it’s still early days for development in the agentic applications space, but adds that its new MCP server shows what’s possible.

“There have been a few test cases floating around of people getting AI agents to engage in financial transactions, but these are generally limited to proofs-of-concept like getting an agent to buy a cup of coffee,” the company said.

While agent access is limited to the company’s sandbox environment, some of the potential future use cases will allow AI to serve as an end-to-end wealth manager, enabling AI to handle administrative tasks, and allowing customers to build their own personalized agent to handle their money in a tailored and relevant way.

Griffin’s MCP server launch will offer developers tools to simulate autonomous financial workflows and marks a step toward turning agentic finance from theory into action. While many AI tools for financial services are currently limited to narrow use cases like chatbots, Griffin is building infrastructure that could allow agents to directly open accounts, initiate payments, and manage money autonomously. If agentic applications mature, the MCP server could evolve firms’ AI use from chatbots to fully autonomous wealth managers.

Griffin was founded in 2017 and offers BaaS tools that include client onboarding, regulatory compliance safeguards, client money accounts, and payments. The company’s direct banking tools include operational accounts, credit, and lending. It also offers embedded bank accounts, client accounts, API-enabled payment options, and client onboarding tools.

Last year, after receiving a $24 million (£19 million) Series A extension round, Griffin revealed that the UK Prudential Regulation Authority (PRA) and Financial Conduct Authority (FCA) granted it approval to launch as a fully operational bank.