This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Velmie added a card module to its updated white-label BaaS solution.

The new card module will help businesses offer their own customized physical or virtual payment card.

Velmie’s new release also enables businesses to issue physical and virtual corporate cards to their employees.

Mobile e-wallet platform Velmiereleased an updated white-label solution that offers the addition of a card module. The new BaaS offering will help companies build and launch their own fintech business.

The card module is a new feature of Velmie’s white-label solution and will offer businesses a comprehensive tool set to launch their own customized physical or virtual payment card product. The solution integrates with both Apple Pay and Google Pay, and includes 3D Secure to protect against fraud.

Additionally, Velmie enables businesses to issue physical and virtual corporate cards to their employees. Doing so offers businesses visibility and control over expenses, enables them to set spending limits, and provides them control over transaction types.

“Velmie built white-label solutions not only to speed up time to market for new fintech products but to make them scalable and future-proof,” said Velmie Founder and CEO Slava Ivashkin. “We’re excited to release our upgraded Velmie application. We believe it will be valuable for fintech companies and banks looking to create innovative solutions that meet the changing needs of their customers.”

Facilitating this week’s launch are Velmie’s recent fintech partners, including payment, open banking, and sustainability services fintech Enfuce and all-in-one business financial platform ConnectPay.

Velmie was founded in 2010 and its technology helps traditional banks and mobile wallet companies provide compliant and scalable mobile banking, e-wallets, remittance platforms, payroll solutions and more to their end customers. With three office locations spanning from the U.S., the U.K., and Lithuania, Velmie serves customers across four continents.

News that Venmo is now accepting transfers of cryptocurrency is among the top stories in crypto of late. Here are some of the other stories making the crypto headlines.

Paxos Partners with Fierce Finance

Blockchain infrastructure platform Paxos has forged a partnership with financial services app, Fierce Finance. Paxos’ technology will be leveraged to power Fierce Finance’s new digital asset experience. This new offering will combine an FDIC-insured checking account, a no-fee debit card, and fractional stock, ETF, and cryptocurrency trading all in a single app.

“We are the qualified custodian managing the licensing, trading, and technical complexity so that our clients can focus on building a seamless user experience,” Paxos Chief Revenue Officer Michael Coscetta said. “By integrating with Paxos platform, Fierce ensures its users get the best prices with the proper consumer protections in place so that their assets always remain safe and accessible.”

Headquartered in New York, Paxos was founded in 2012. The company reached a major milestone at the beginning of last month when it surpassed ten million active end user digital wallets globally. Earlier this year, Paxos launched an engineering R&D Center in Israel focused on “security and cryptography excellence.” The center will serve as a hub for cryptography researchers and security specialists to develop secure solutions on top of the blockchain.

Paxos has raised more than $540 million in funding. The company’s investors include Oak HC/FT, Declaration Partners, and PayPal Ventures.

Tax on Cryptocurrency Mining Proposed

If the Biden administration gets its way, the electricity used in mining cryptocurrencies could get a lot more expensive. The White House is proposing a 30% tax to offset the impact of cryptocurrency mining on the environment.

A statement from the Council of Economic Advisors (CEA) argues that the “high-energy consumption” of cryptocurrency mining “has negative spillovers on the environment, quality of life, and electricity grids” wherever they are located. A report from the White House released last fall suggested that cryptocurrency mining devours more electricity than the country of Australia. In the U.S., cryptocurrency mining represents between 0.9% and 1.7% of all electricity use. The U.S. is home to approximately a third of the world’s cryptocurrency mining.

Some critics of the proposal believe less in the administration’s concerns over the climate and more in its antipathy toward the cryptocurrency industry in general. Other observers suggest that taxing greenhouse gas emissions from cryptocurrency mining makes more sense than simply taxing electricity use – which can come from clean sources.

If enacted, the tax could yield $3.5 billion over 10 years.

Coinbase Launches International Exchange

Hot on the heels of securing a license to operate in Bermuda, U.S.-based cryptocurrency exchange Coinbase has launched its Coinbase International Exchange. The new exchange will give institutional market participants in eligible jurisdictions outside the U.S. the ability to trade perpetual futures.

Perpetual futures are similar to futures contracts in other assets. But there are important differences. Perpetual futures do not have an expiration period – unlike traditional futures contracts. This enables traders to hold on to their positions for longer periods – or even indefinitely. Trading in perpetual futures is not allowed in the U.S. But the market for perpetual futures is sizable. Almost 75% of cryptocurrency trading worldwide last year was in perpetual futures.

Coinbase International exchange listed perpetual futures contracts for both Bitcoin (BTC) and Ethereum (ETH) this week. The contracts provide 5x leverage and all trades are settled in USDC.

New Digital Asset Venture Fund Coming from Fineqia

Digital asset and fintech investment company Fineqia will launch a new venture capital fund to invest in startups in the digital asset space. The new fund, Fineqia Glass Slipper Ventures (FGSV), will focus on investments in early and growth-stage technology companies. Among Fineqia’s current investments in the industry are digital asset manager Wave Digital Assets LLDC, and blockchain gaming platform company Forte Labs. The fund has identified blockchain infrastructure, decentralized finance, and the metaverse as areas of particular investment interest.

“We have a proven track record of investments that are generating extraordinary returns,” Fineqia CEO Bundeep Singh Rangar said. “An investment fund will give us more firepower to invest in the most promising firms among the scores we see monthly and take advantage of entry valuations not frothy as they were 18 months ago.”

Deloitte Leverages the Blockchain for KYB, KYC

Will the next big thing in decentralized finance come from the underlying blockchain technology or from products like cryptocurrencies? The latest entry in the “innovative blockchain use case” competition comes courtesy of Deloitte Consulting. The firm announced that it has partnered with BOTLabs GmBh to use its KILT protocol to support KYC and KYB processes.

“By offering re-usable digital credentials anchored on the KILT blockchain, Deloitte is transforming verification processes for individuals and entities,” Head of Deloitte Managed Services Micha Bitterli said. “Digital credentials that are convenient, cost-effective and secure have the potential to open new digital marketplaces, from e-commerce and DeFi to gaming.”

Re-usable credentials are stored on the customer’s wallet on their own device. Customers have full control over whom they share their credential with. They can also control which data points on the credential they grant access to. Deloitte digitally signs the credentials and is able to revoke credentials via the blockchain if a customer’s circumstances change.

PayPal-owned Venmo is continuing its journey into DeFi this month. Late last month, the California-based company unveiled a new peer-to-peer crypto transfer capability. The new feature enables users to transfer crypto to friends and family using Venmo, PayPal, and external wallets and exchanges.

Venmo first introduced crypto to its users in 2021, but the capabilities were limited. Within the Venmo app, users could only buy, hold, and sell cryptocurrency. This month’s development adds to the company’s crypto wallet capabilities, rounding out the utility from saving and investing into spending and giving.

The company reports that, over the past year, more than 74% of its crypto customers have continued to hold crypto in their accounts. “In addition,” today’s announcement said, “since the beginning of 2023, nearly 50% of customers with existing crypto balances have added to their crypto holdings on Venmo.”

To send their crypto to friends and family, customers use the Crypto tab within the Venmo app and use the transfer arrows to transfer a select amount of their crypto to a Venmo account, or to a recipient’s PayPal wallet address or other external wallet. To receive crypto, users show their unique crypto address QR code with other users.

Select Venmo customers will have the ability to send crypto transfers starting this month. The company will roll out the new capability to more users over the coming months.

A look at the companies demoing at FinovateSpring in San Francisco on May 23 and 24. Register today and save your spot.

FinTech Insights by Scientia is a competitive analysis tool for banks and fintechs that provides all the data a company needs to outsmart their competition in one powerful, user-friendly platform.

Features

Reveals gaps in a company’s market faster

Eliminates the risk of releasing an obsolete feature or user journey

Imports a product roadmap and benchmarks the projected self against any competitors

Why it’s great

Some digital banking teams develop with limited view of the market, and FinTech Insights allows them to quickly identify unmet customer needs and market opportunities.

Presenters

Nickolas Belesis, VP of Growth Belesis is a fintech growth and digital banking specialist, assisting c-suite executives in utilizing FinTech Insights to skyrocket their digital banking and maximize their NPS scores. LinkedIn

Konstantine Pappas, Account Executive Pappas is an experienced fintech executive who is empowering digital banking teams to improve their UX and product offerings. LinkedIn

A look at the companies demoing at FinovateSpring in San Francisco on May 23 and 24. Register today and save your spot.

PayTic provides a SaaS solution for card issuers and program managers that automates network fee analysis, reconciliation, dispute submission, exceptions management, and reporting.

Features

Efficiency: Program management processes live in a single platform

Accuracy: Modules update each other

Savings: Elimination of unnecessary fees and data related to compliance issues

Why it’s great

Saving time and money is possible while managing card programs. By automating processes and data flows, PayTic can reduce network fees and increase compliance efficiency.

Presenters

Imad Boumahdi, Founder & CEO Boumahdi founded PayTic to help card programs modernize and manage their day-to-day operations and compliance. He has 15+ years of experience in payment cards processing. LinkedIn

Kate Firuz, Director of Product Over the past nine years, Firuz has directed company growth by acquiring and issuing businesses, while launching card programs in U.S. markets and Canada. LinkedIn

A look at the companies demoing at FinovateSpring in San Francisco on May 23 and 24. Register today and save your spot.

ModernTax provides fast and secure access to millions of financial data points for businesses to verify tax filings and wage and income reports. It delivers coverage of over 7 million unique entities in the US.

Features

Includes fast and secure access to millions of financial data points in minutes, not days

Offers coverage of over 7 million unique entities and every U.S. taxpayer

Provides a comprehensive solution for verifying U.S. tax filing

Why it’s great

ModernTax offers fast, secure access to financial data for tax verification, reducing the risk of fraud – valuable for financial institutions, insurers, and others.

Presenter

Matthew Parker, CEO Parker is the CEO of ModernTax, a startup offering API and no-code solutions for tax data to financial institutions and fintech platforms. He is a 3x founder and former D1 college athlete. LinkedIn

A look at the companies demoing at FinovateSpring in San Francisco on May 23 and 24. Register today and save your spot.

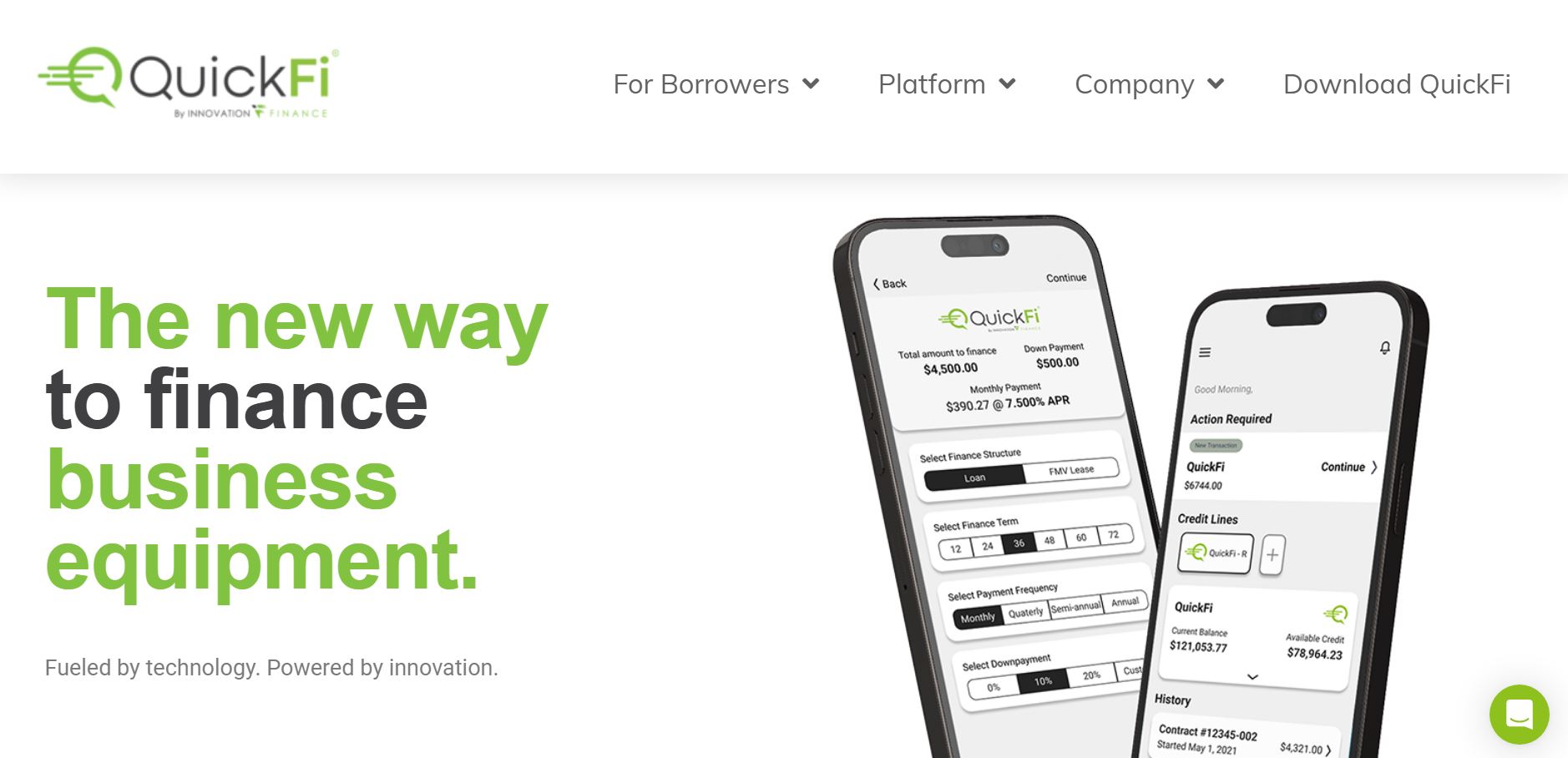

QuickFi’s latest e-commerce technology allows business borrowers to shop and consummate financing for business equipment – all within minutes, instead of days or weeks.

Features

Easily embeds into lender or manufacturer’s website

100% digital, borrower self-service, and accessible 24/7

Automated credit, contract structuring, and business verification

Why it’s great

With this latest technology, banks and manufacturers can now offer a combined online shopping and financing experience that is 100% digital, fully self-service, and able to be completed in minutes.

Presenters

Nate Gibbons, CXO Gibbons oversees QuickFi’s customer experience strategy, leveraging automation and technology to enable dramatic improvements to the borrower experience. LinkedIn

Jillian Munson, VP, Process & Automation Munson leads core technology projects at QuickFi. She develops seamless user experiences for both internal and external business processes. LinkedIn

Behavioral biometrics and fraud detection innovator BioCatch has raised $40 million in funding.

The investment gives Permira a “significant minority stake” in the Tel-Aviv-based company.

BioCatch made its Finovate debut at FinovateFall 2014.

Behavioral biometrics innovator BioCatch has raised $40 million in funding courtesy of an investment from Permira Growth Opportunities. The capital gives Permira a “significant minority stake” in the New York and Tel Aviv-based company. In fact, along with Bain Capital and Maverick Capital, this week’s capital infusion makes Permira BioCatch’s third largest shareholder.

“Permira is one of the leading global private equity firms in the world, with particularly strong experience in the technology space,” BioCatch CEO Gadi Mazor said. “We believe its deep sector expertise and company-building capabilities will help us to expand our business and strengthen our global position.”

The funding takes BioCatch’s total capital raised to more than $213 million. No new valuation information was provided. BioCatch will use the capital to help support geographical expansion, product development, and potential M&A.

BioCatch is a pioneer in behavioral biometric intelligence and advanced digital fraud detection. Its technology leverages AI and machine learning to collect thousands of data signals to analyze the cognitive intent of users. This enables BioCatch to provide highly accurate insights into the legitimacy of a user’s identity and behavior. Financial institutions using BioCatch’s technology have been able to better fight fraud, accelerate digital transformation efforts, uncover new revenue opportunities, and boost customer satisfaction.

Founded in 2011, BioCatch made its Finovate debut at FinovateFall in 2014. In the years since, the company has grown into a fraud detection leader with a global footprint of 22 countries. More than 100 international banks rely on BioCatch’s technology to fight financial crime and defend themselves against fraud. BioCatch announced early this year that 2022 had been the firm’s “most successful” – with annual recurring revenue growth of more than 40%. BioCatch also revealed that the company added more than 100 leading global banks as customers in 2022 and detected more than $1.5 billion in fraud, saving banks nearly $1 billion.

Global financial services innovator Revolut is becoming a bit more global today. The London-based company announced today it has expanded into Brazil. Today’s move of launching multi-currency account and crypto investments in Brazil, marks Revolut’s first expansion into a Latin American country.

Revolut’s expansion efforts into Brazil began last March. The company not only brought on Glauber Mota as CEO of its Brazil operations, but it also opened up a waitlist in the region. “There’s a lot of appetite for Revolut and digital banking services in Brazil,” said Mota. “Recent surveys show that more than 45% of Brazilians already use digital accounts as their primary account, and use more than five different applications to manage payments, transfers, and investments.”

The company will begin its Brazil expansion via a phased rollout, during which time it will continue adding to its waitlist. In addition to being available in Brazil, Revolut’s accounts are available to residents of the European Economic Area (EEA), Australia, Singapore, Switzerland, Japan, the U.K., and the U.S.

Revolut counts 29 million retail customers across the globe making 330 million transactions each month. The company debuted its multi-currency account at FinovateEurope in 2015 and also offers a peer-to-peer trading, an early wage access tool, an account for users under the age of 18, stock trading, business cards, commercial spend management tools, and more.

Revolut has raised around $2 billion since it was founded in 2015. While the company was once considered one of Europe’s most valuable fintechs, Revolut took a hit last week when company shareholder Schroders Capital Global Innovation Trust disclosed a $5.8 million (£4.7 million) writedown, shaking the value of its stake from $12.6 million (£10.1 million) in 2021 to $6.7 million (£5.4 million) in 2022.

Despite the valuation woes, however, Revolut continues to expand. The company launched credit cards for its Ireland user base earlier this year and is planning to launch a car insurance service in the region. Additionally, Revolut is working on expanding to more geographies, including Ecuador, Mexico, India, New Zealand, and Oman.

Retail software company Celerant Technology has partnered with BNPL innovator Sezzle.

Celerant will integrate Sezzle’s SezzlePay solution into its platform. SezzlePay enables consumers to pay for purchases in four, interest-free installments over six weeks.

Sezzle made its Finovate debut at FinovateSpring 2016.

Retail software provider Celerant Technology announced a partnership with consumer financing solutions company Sezzle. The partnership will enable retailers who use Celerant eCommerce to add Sezzle Pay to their payment choices. This option gives consumers the ability to take advantage of Sezzle’s buy now, pay later (BNPL) financing, with 0% APR. Retailers will also benefit from engagement with potentially millions of Sezzle users, an opportunity that could lead to increased online sales and new customers.

“We’re excited to partner with a leader in the retail software industry and to bring Sezzle’s Buy Now, Pay Later financing to the millions of consumers that shop at Celerant’s diverse ecosystem of brands,” Sezzle co-founder and Chief Revenue Officer Paul Paradis said.

Paradis underscored the popularity of BNPL financing among millennials and Gen Z consumers. He pointed to the fact that BNPL financing charges no interest and no fees when purchases are paid for on time, as well as the ability to use BNPL to build credit, as two factors in favor of the financing option. “It’s a runaway hit,” Paradis said.

Celerant’s eCommerce platform enables retailers to offer Sezzle to customers directly from their website. The process is straightforward. Customers select SezzlePay as their payment option during checkout. This will enable them to split the cost of the transaction into four interest-free payments over six weeks. Sezzle pays the merchant in full at the time of the transaction; funds are direct deposited in the merchant’s account within one-to-three business days. Sezzle also assumes full risk of any missed payments.

“With more consumers turning to instant credit apps to make ends meet, it was important to expand our technology with additional consumer financing options,” Celerant President and CEO Ian Goldman said. “As a popular ‘buy now, pay later’ solution in the industry, partnering with Sezzle provides more options for our retailers to offer their customers payment flexibility and help financially with larger purchases, and in turn increase our retailers’ online sales.”

Sezzle made its Finovate debut at FinovateSpring in 2016. The company returned to the Finovate stage two years later for FinovateFall. Sezzle began 2023 as the first BNPL company in Canada to offer free credit-building service to users. The firm also began the year as a profitable company, growing from a net loss of $75.2 million in fiscal year 2021 to ending 2022 with net income in Q4. The turnaround came as a result of major cost-cutting strategies. These efforts included layoffs; a retreat from potential expansion in Asia, Europe, and Latin America; and a renegotiation of merchant fees. Sezzle also benefitted from a premium membership drive that brought on more than 132,000 subscribers.

Founded in 2016, Sezzle is headquartered in Minneapolis, Minnesota.

Business budgets and digital payments platform inbanx has partnered with Corserv.

inbanx will leverage Corserv’s Payment Cards as a Service API to offer its business customers a Visa commercial credit card.

According to Juniper Research, the number of payment cards issued via digital platforms will grow 170% between now and 2027.

Business budgets and digital payments platform inbanx is boosting its offerings today by partnering with card issuer Corserv. Texas-based inbanx is integrating Corserv’s Payment Cards as a Service API (PCaaSA) into its platform to offer a more holistic business payments platform.

Integrating Corserv’s PCaaSA will enable inbanx to offer a Visa commercial credit card to its business clients. The new modern payment card solution will offer real-time, configurable spend controls and cooperative authorization for businesses that rely on hierarchical approvals and spending limits.

“Our highly configurable PCaaSA platform simplifies complex processes for inbanx to launch and embed commercial cards in a secure, compliant and flexible way,” said Corserv CEO Anil Goyal. “We are thrilled to work with inbanx to integrate with their innovative budget and expense management solution.”

Founded in 2021, inbanx helps businesses budget, manage their card program, and control spending across teams. By automatically reporting the expenses, inbanx’s solution eliminates the need for employees to fill out manual expense reports.

“We serve our customers with an innovative and easy-to-use solution that adopts the next generation of payment capabilities to allow businesses and their employees to spend efficiently,” said inbanx CEO Rob Kaczmarek. “Corserv’s payment card platform was the only solution that afforded us the customizability and flexibility to build exactly what we needed for our customers.”

Corserv has been helping banks and fintechs offer issuing processing and program management services for credit, debit, and prepaid cards since it was founded in 2009. The Atlanta, Georgia-based company has raised $2.1 million in funding and recently named Anil Goyal as its new CEO.

Modern card issuing is a hot space in the fintech realm, especially as banking-as-a-service and embedded finance becomes more popular. Juniper Research expects the number of payment cards issued via digital platforms to grow 170% between now and 2027, increasing from 500 million in 2023 to 1.3 billion by 2027. Global leaders in the modern card issuing space include Thales, G+D, FIS, Fiserv, and Marqeta.