How they describe themselves: International banking group PrivatBank serves over 20 million corporate and individual сustomers in Ukraine, Latvia, Portugal, Italy, Cyprus, and Georgia. PrivatBank is the leader of the Ukrainian banking sector and one of the largest issuers and acquirers of payment cards in Eastern Europe. It is one of the most innovative banks in the world.

How they describe their product/innovation: Topless Android ATM is an ATM without an unnecessary TOP. It is equipped with an Android phone with an NFC chip, Raspberry Pi, cash dispenser, and safe. The ATM has minimum electronics and no keypad or buttons and is controlled by customers’ smartphones.

Product Distribution Strategy: Direct to Business (B2B), through financial institutions

How they describe themselves: Matchi is a privately funded company, headquartered in Hong Kong and has a global banking client base that includes UBS, Bank of Queensland (Australia), Sberbank Labs Russia, American Express, OCBC Bank Singapore, Bank Respublika Azerbaijan, Standard Chartered (Global HQ) and Standard Chartered Bank Singapore.

How they describe their product/innovation: Matchi is an Innovation Matchmaking platform for banks and innovators to establish collaborative relationships that deliver increased return on investment for innovators and banks alike. Matchi is here to open persuasive channels of communication so that both sides can benefit from the relationship.

Product Distribution Strategy: Direct to Consumer (B2C), Direct to Business (B2B)

Contacts:

Press & Sales: Philippa Newnes, Director, [email protected], +61 401 915 153

How they describe themselves: Meniga offers white-label mobile and web-based Personal Finance Management (PFM) and next generation online banking solutions to retail banks. To achieve true mass appeal and reach even people who usually avoid facing their finances, Meniga uses social curiosity, humor, and gaming concepts to engage users to think about their money.

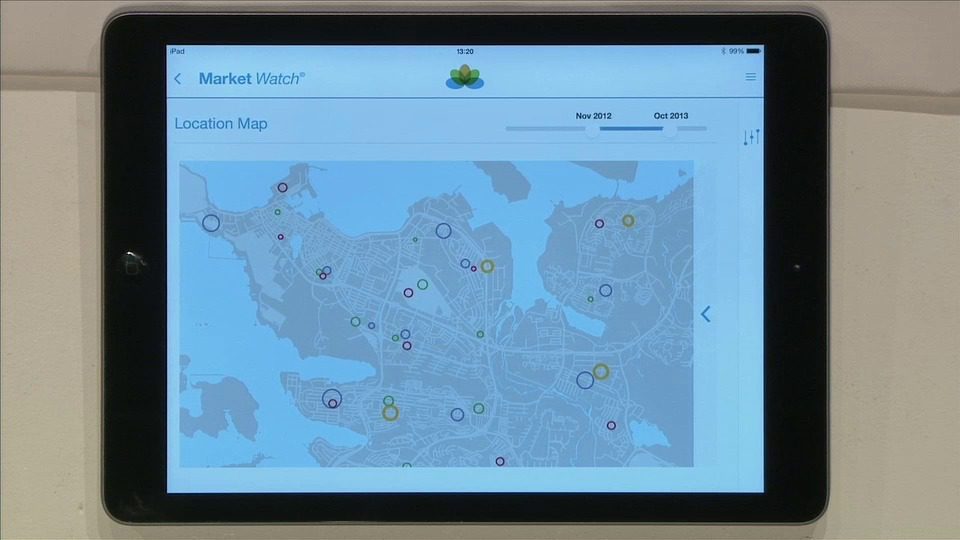

How they describe their product/innovation: The MarketWatch offers Financial Institutions a unique way to analyze financial data that lives within their systems. Complementary to Meniga‘s PFM Solution, the MarketWatch enriches the transactional data and is a real-time, transaction-based analytics platform for industry-specific market intelligence and reporting. The superior market intelligence provided by the MarketWatch can be offered by banks to retailers for competitive analysis or to improve tactical decision making thereby creating a new revenue stream.

Product Distribution Strategy: Direct to Business (B2B), through financial institutions

Contacts:

Bus. Dev. & Press: Georg Ludviksson, CEO, [email protected], +46 767822146

Sales: Duena Blomstrom, VP Sales, [email protected], +46 708620578

How they describe themselves: Misys Digital Channels (formerly IND Group) is a digital banking, PFM and payments technology software vendor for financial institutions. Focusing on customer experience, our goal is to evolve e-banking technology to web 2.0, turning it into a sales and customer engagement platform. Our unique innovations and multichannel products support banks’ in-development needs caused by the economic slowdown.

How they describe their product/innovation: To adapt to younger generations’ requirements, Misys delivers a best-in-class banking app with an innovative drive. With Misys BankFusion Digital: Mobile Banking, all services are only a few taps away – anytime, anywhere. Mobile banking has never been so comfortable and easy, yet secure. The application offers more than just transactional banking: based on customers’ life situations banks are able to deliver personal, targeted offers, turn data into relevant, visualized information, and provide a user experience like never before, turning mobile banking into their primary engagement and sales channel.

Product Distribution Strategy: Direct to Business (B2B), through financial institutions, through other fintech companies and platforms, licensed

Contacts:

Bus. Dev. & Sales: József Nyíri, Director of Innovation, Misys Labs, [email protected]

Press: Viktor Bálint, Head of Marketing, Digital Channels, [email protected]

How they describe themselves: We operate a mobile payment service that offers universal access while being totally independent from credit cards and telcos.

On the front-end, we offer an application for smartphones and a voice service for dumbphones. No special equipment is required from customers or from merchants. Integration in cash registers and vending machines is quick and easy.

For the back-end:

- In OECD countries, we connect directly with bank accounts towards real-time transactions, thereby slashing costs and risks and improving the user experience.

- In unbanked or underbanked countries, we aim to build and operate a national e-cash infrastructure on behalf of the central bank, instead of fighting with local money transfer services.

How they describe their product/innovation: The new Mobino app delivers superior convenience for customers with a seamless integration of many payment scenarios:

- Peer-to-peer money transfer

- Payment for goods and services in shops

- POS and cash register integration

- Quicker and safer e-commerce payments

- Fluid payment flow for mobile commerce

- Cheap and efficient international remittances

- Registration and KYC process for unbanked

- Cash-in/out operations at agents and ATMs

We are looking for distribution partners and investors to expand our reach in Europe and worldwide.

How they describe themselves: Money on Toast is part of CPN Investment Management, a discretionary fund manager and advisory service that has been operating throughout the UK since 1986. Money on Toast was founded by Charlie Nicholls, a young entrepreneur who spotted an opportunity to provide advice to the millions of clients who had been abandoned by other financial institutions as a result of RDR.

Money on Toast aims to revolutionise the financial services industry, providing an innovative way for consumers to receive FCA regulated financial advice online on a wide range of financial services products such as ISAs, pensions and protection policies.

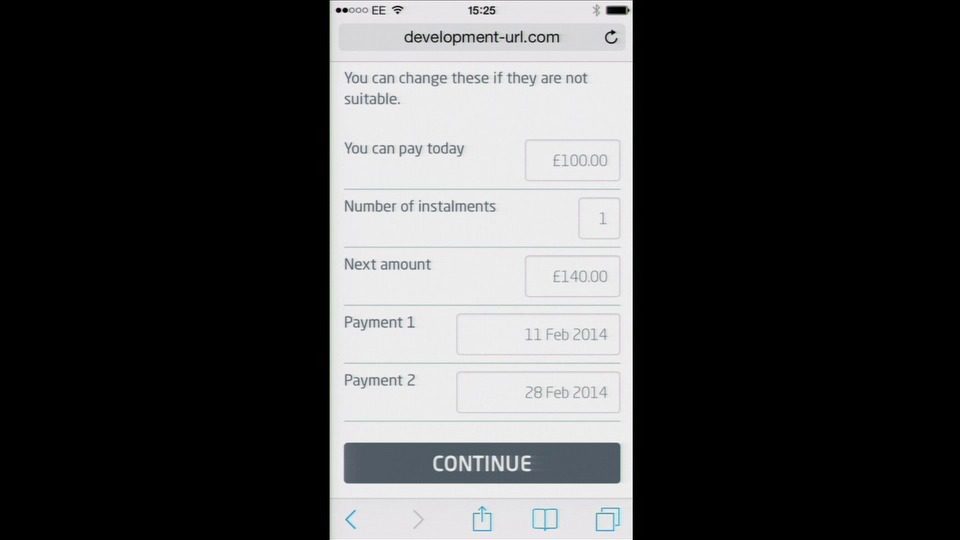

How they describe their product/innovation: Money on Toast delivers independent and whole of the market FCA-regulated financial advice online via an algorithm-powered adviser, Doughbot. Clients can obtain advice on investments, pre and at-retirement planning, protection and inheritance tax.

How it works: The online system guides the customer through a series of questions, assessing a number of different factors just as a human adviser would. Doughbot then produces a comprehensive electronic suitability report detailing what has been recommended, which is emailed to the client. Clients can then click through and buy these products directly online. All interactions are electronically tracked, providing a complete compliance trail.

Product Distribution Strategy: Direct to Consumer (B2C), through financial institutions

Contacts:

Bus. Dev.: Kay Ovenden, Business Development Director, [email protected],

01243 819101

Press: Catharine Dodd, Project Manager, [email protected], 01243 819101

Sales: Charlie Nicholls, Founder & Managing Partner, [email protected], 01243 819101

How they describe themselves: We are MyOrder. We empower and delight our customers by delivering confidence and convenience to their shopping experience.

How they describe their product/innovation: The smartest way to spend, connect, shop, browse and have fun.

Product Distribution Strategy: Direct to Consumer (B2C), Direct to Business (B2B), international distribution strategy through partners (FIƒ??s, other FinTech companies, etc.)

Contacts:

Bus. Dev.: Gertjan Rösken, CTO, [email protected]

Press & Sales: Thomas Brinkman, CSO, [email protected]

How they describe themselves: MyWishBoard.com is a social crowdfunding platform for personal dreams and wishes. The big idea behind the project is to make peoples’ wishes come true. Each user’s profile is a personal wish board, where their friends, family or fans can back any amount of money on a wish account. MyWishBoard operates as a social pinboard of desired objects and struggles allowing people to subscribe to wish boards, explore and copy new wishes filtered by tags and to keep a track of wish fulfillment.

How they describe their product/innovation: MyWishBoard.com is the first p2p platform where users can finance their wishes with the help of friends and subscribers. Once the necessary amount is raised, the money is transferred to the gift recipient’s digital account and could be further spent directly in e-stores or withdrawn on a credit card.

How they describe themselves: NF Innova is a software solutions company that specializes in creating markets’ leading Omni-Channel Customer Interaction products. A member of New Frontier Group, one of the largest System Integrator groups in Central & Eastern Europe, NF Innova has been providing the region’s prime banks and financial institutions with the most advanced solutions for the Digital Economy. iBanking, NF Innova’s flagship product, is distributed in the entire EMEA region through the network of subsidiaries and channel partners.

How they describe their product/innovation: Personal Experience Module, a part of iBanking product suite, enables banks to offer their customers a truly unique and tailored user experience. Namely, instead of static CRM-based rules used for segmentation, this module provides for the adaptive behavior of the entire system, tailoring the user interface for each individual client, without the administration by the bank’s staff. It monitors the subscribed products and services, user’s behavior on the digital touch points (portal, mobile devices, etc.), and automatically provides the exact mash up of functionalities that are most appropriate for the specific customer at the given time and the communication device.

Product Distribution Strategy: Direct to Business (B2B), through other fintech companies and platforms, licensed

Contacts:

Bus. Dev. & Sales: Vasa Segrt, Director of Sales & Operations, [email protected]

Press: Aleksandar Lenov, Pre-Sales, [email protected]

How they describe themselves: Nostrum provides technology to make lending cheaper, faster, and safer. Our technology is used by an increasing number of high profile lenders to make faster, more informed credit decisions, reducing their credit defaults and facilitating cheaper credit. High level of customer self service and automation reduce lender operating costs and interest rates whilst also providing exemplary customer service. Emerging regulatory requirements focus on transparency and treating customers fairly – these principles being embedded within our software. The software is provided on a fully managed SaaS basis through dual secure, high availability data centres.

How they describe their product/innovation: Nostrum’s mission is to provide a fully automated lending platform, enabling lending to be performed cheaper, faster and safer.

Whilst innovation in certain sectors of the lending industry have addressed the auto approval of applications and now provide loan funds rapidly, no business has adequately considered how delinquency management activity can be redesigned to ease the customer experience and reduce the risk of compliance failure. The functionality demonstrated will replace the traditional call centre operator who manages in and outbound calls to customers to discuss their delinquent payments and either takes a payment or puts an arrangement in place.

Product Distribution Strategy: Direct to Business (B2B)

Contacts:

Bus. Dev. & Sales: Richard Carter, CEO, [email protected]

Press: Deana Aldridge, Marketing Manager, [email protected]

How they describe themselves: Nous operates a free trading simulator paying weekly cash prizes, with the goal of finding and retaining the world’s best trading talent across all exchange-traded asset classes. The predictions generated by our tens of thousands of traders are condensed into simple real-time feeds that help you understand and predict the financial markets.

How they describe their product/innovation: Nous’ “Spark Feed” is a real-time financial data service that helps you understand and predict the markets. Uniquely, Spark Feed uses the intuitive and analytical capabilities of tens of thousands of real people, not software algorithms. Their predictions are segmented by proven trading skill and then quantitatively blended.

This product is an exciting combination of natural human talents and quantitative finance techniques. Our belief in persistent, dependable predictive skill is supported by securities companies’ practices, recent findings in academia — and by our own massive data set.

Product Distribution Strategy: Direct to Consumer (B2C), Direct to Business (B2B), through other fintech companies and platforms

Contacts:

Bus. Dev. & Sales: [email protected]

Press: [email protected]

How they describe themselves: payworks is the provider of a mobile POS Software-as-a-Service platform that lets developers quickly build payment functionality into their shopper and merchant apps. The mobile SDKs and APIs of payworks make it very easy to build both solutions for face-to-face payments with Chip & PIN card readers as well as solutions for shoppers to pay directly with their phones via in-app payments and wallets. By working with payworks, developers can spend their time to focus on building a product that solves real merchant problems rather than fighting with complex payment integration. payworks’ technology is the basis for many major mobile POS initiatives throughout Europe, including payment acceptance solutions for micro merchants.

How they describe their product/innovation: We are showing how easy it is to build innovative payment solutions on top of the payworks platform and showcase stunning checkout options.

Product Distribution Strategy: Direct to Business (B2B), through financial institutions

Contacts:

Bus. Dev.: [email protected]

Press: [email protected]

Sales: [email protected]