Second Life, the alternate reality with four million members worldwide, has a surprising driver, capitalism. According to Second Life Insider, US$1.5 million changed hands yesterday (link here). And if there's money changing hands, there are opportunities for banks and financial scammers (not necessarily in that order).

Second Life, the alternate reality with four million members worldwide, has a surprising driver, capitalism. According to Second Life Insider, US$1.5 million changed hands yesterday (link here). And if there's money changing hands, there are opportunities for banks and financial scammers (not necessarily in that order).

In a March 6 search, Second Life Insider found ten banks operating in Second Life (SL) (post here). Several operate only in Second Life, raising numerous questions about the legitimacy of these non-regulated entities.

But what most interests us are the six real-world banks that have set up shop in Second Life such as ING's Virtual Holland (see inset above and screenshot below).

Here's a banks in Second Life timeline:

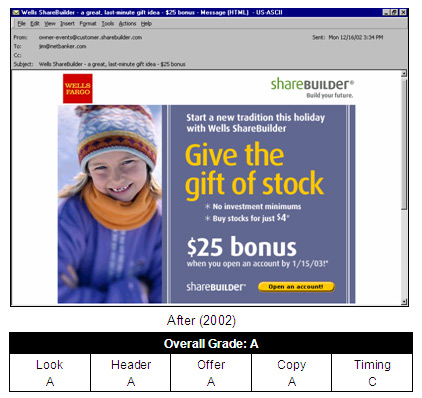

Sep. 2005: Wells Fargo is the first real-world bank with a presence in Second Life (SL)

Dec. 2005: Wells Fargo leaves SL, moving its Stagecoach Island to a new platform (see previous coverage here)

7 Dec 2006: ABN Amro becomes first European bank in SL (press release here)

7 Jan 2007: BNP Paribas opens a small test area (post here)

7 Feb 2007: Swiss bank BCV opens its doors in SL (press release here)

21 Feb 2007: ING Bank launches website and blog to get users involved in building what it calls Our Virtual Holland <ourvirtualholland.nl>

2 Mar 2007: Danish Saxo Bank announces plans to create trading platform in SL (Reuters article here)

Analysis

It's hard to predict whether banking will ultimately become a transactional business in Second Life or other virtual realities (note 1). However, with four million registered users and an inordinate amount of press attention, leveraging a Second Life presence for marketing purposes looks to be a winner.

But if you are going into SL, make sure you mirror the effort with a Web presence that lets the other 1 billion Internet users see what you are up to. And there is no one doing that better than ING, who's taken a Zen approach to its SL strategy. They've made the process of building a SL presence more important than the actual result. Their Web 2.0-inspired website ourvirtualholland.nl involves the community with blogs, suggestions, and an email list (see screenshot below).

Note

1. For the record, we believe that full banking capabilities, including transactions, lending, currency exchange, will eventually be conducted in virtual communities such as Second Life. Whether it will ever be more than just a niche play, is unknown.

Last week, ING Group's U.S. unit (note 1) made a splash with two major promotional efforts:

Last week, ING Group's U.S. unit (note 1) made a splash with two major promotional efforts: