With FinovateSpring 2026 right around the corner—May 5-7—we wanted to take a moment here at Finovate Global to highlight the international companies that will be demoing their latest fintech innovations live on stage next week.

While both our European conference FinovateEurope and our flagship event FinovateFall tend to showcase the lion’s share of our international alums, we are thrilled to host these eight fintech innovators from Greece, India, Israel, Italy, Singapore, and Switzerland this year at FinovateSpring!

Join us next week—May 5-7—at the Sheraton San Diego Resort for FinovateSpring 2026. 1200+ senior-level fintech attendees. 600+ attendees from banks and financial institutions. 50+ live fintech demos. Save your spot. Book your room. And we’ll see you in sunny San Diego!

BankUniverse—Greece

BankUniverse delivers a privacy-first ‘intent engine’ that identifies high-value prospects and automates conversion, increasing digital sales by 20%+ without sharing sensitive customer PII. Headquartered in Greece, the company was founded in 2024.

Cobalt—Tel Aviv, Israel

Cobalt automatically maps real system dependencies across complex banking environments, enabling agentic AI, real-time visibility, safer changes, reduced risk, and confident operations. Headquartered in Tel Aviv, Israel, the company was founded in 2025.

ContexQ — Singapore

ContexQ is forensic Graph AI that detects fraud, money laundering, and hidden beneficial ownership by seeing the relationships every other AI misses. Headquartered in Singapore, the company was founded in 2024.

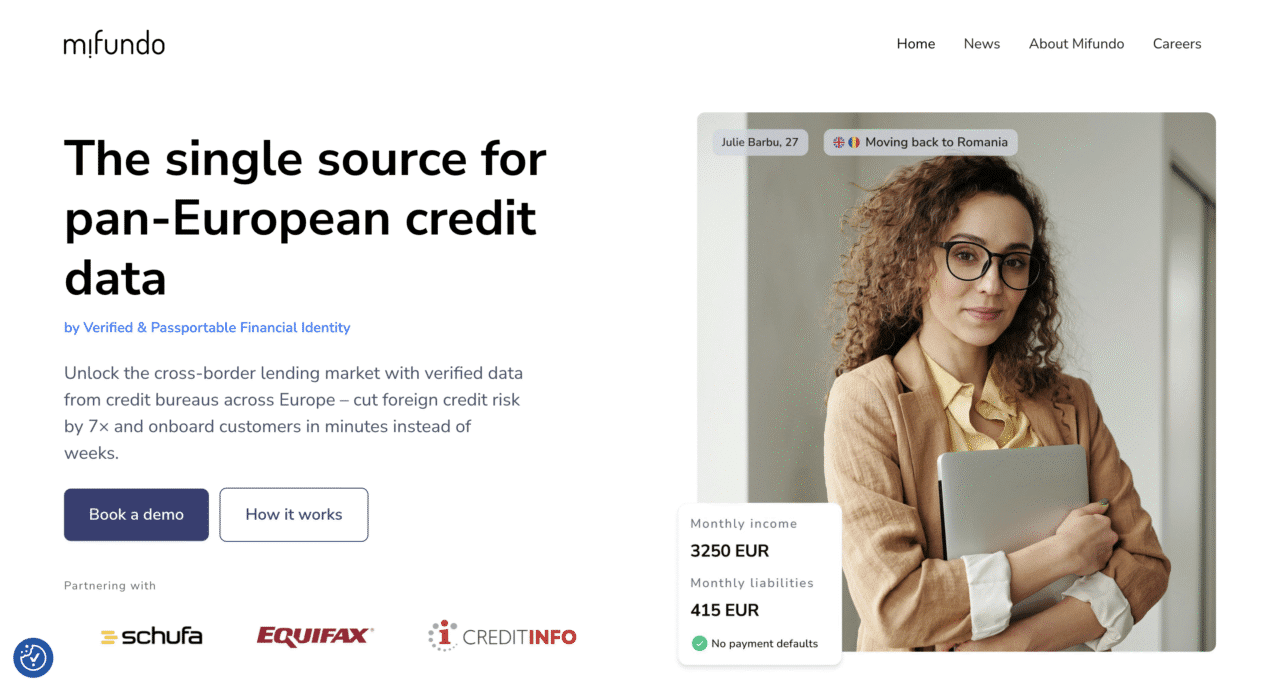

CRIF—Italy

CRIF is a global technology company delivering credit bureau services, business intelligence, advanced analytics, decisioning platforms, and digital solutions that power smarter lending and risk management worldwide. Headquartered in Italy, the company was founded in 1988.

Holdyn—Tel Aviv, Israel

Holdyn is a trust-first fintech platform enabling secure, structured transactions, and conditional payments. In addition to moving funds instantly, Holdyn also allows users to define how and when funds are released, reducing counterparty risk in both local and cross-border transactions. Headquartered in Tel Aviv, Israel, the company was founded in 2025.

Nextvestment — Singapore

Nextvestment enables safe, self-service exploration while guiding advisors to intervene at the right moments, improving client engagement and advisor productivity without changing advisory models. Headquartered in Singapore, the company was founded in 2024.

uncharted group—Zurich, Switzerland

uncharted group’s operating system turns commoditized AI into a proprietary, compounding advantage for investment firms. Headquartered in Zurich, Switzerland, the company was founded in 2024.

Yubi—Chennai, India

Yubi is India’s AI-powered debt marketplace—connecting 17,000+ enterprises with 6,200+ lenders, having facilitated over $36 billion in financing. Now they’re bringing this breakthrough technology to the U.S. Headquartered in Chennai, India and Delaware, the company was founded in 2020.

Here is our look at fintech innovation around the world.

Middle East and Northern Africa

- Saudi Arabian financial app barq introduced international cross-border QR payments in partnership with Alipay+.

- Dubai-based, B2B embedded finance platform Comfi raised $65 million in funding.

- Blockchain-based enterprise solutions company Ripple opened the doors on a new regional headquarters in the UAE this week.

Central and Southern Asia

- India-based fintech Pine Labs announced the acquisition of next-generation online checkout optimization platform Shopflo.

- Central Asian digital banking ecosystem TBC Uzbekistan launched its AI assistant Lola.

- Indian fintech Mobikwik secured approval from the Reserve Bank of India to initiate lending operations.

Latin America and the Caribbean

- Cross-border payment infrastructure company TerraPay forged a strategic partnership with Nicaraguan remittance payout services company Banco de la Producción S.A (Banpro Grupo Promerica).

- Argentina-based fintech belo secured $14 million in Series A funding in a round led by Tether.

- The IMARC Group predicted that Mexico’s fintech market size will reach $67.2 billion by 2034.

Asia-Pacific

- South Korea-based fintech RiskX secured seed funding for its technology that will enhance the pricing, risk analysis, and investor communication for structured derivatives.

- Commonwealth Bank of Australia deployed an agentic AI system designed to detect emerging fraud and scam patterns in payments and transaction data.

- Crypto payments network MoonPay joined Sungho Electronics and Seoryong Electronics in an investment in Soutk Korean fintech Finger as part of an effort to support a Korean won stablecoin ecosystem.

Sub-Saharan Africa

- South African bank Absa Group Limited improved its self-solve cases of digital and card fraud by 47% by using WhatsApp to instantly confirm suspected fraud transactions with customers.

- Nairobi, Kenya-based cross border payments company WapiPay secured approval from the Bank of Jamaica to begin operations in the country.

- PitchBook looked at the state of VC funding for African fintechs.

Central and Eastern Europe

- European paytech Nexi integrated new digital payment option, Wero, bringing it into Germany’s ecommerce system via its German subsidiary, Nexi Germany.

- Austrian cooperative banking group Raiffeisenbankengruppe Oesterreich partnered with nCino for its unified corporate lending platform

- Finom unveiled a new, standalone version of its accounting solution for freelancers and small businesses in Germany.

Photo by Andrew Stutesman on Unsplash