This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Sila has partnered with Trice to leverage the company’s safeguards for instant payments.

Trice will help Sila’s customers eliminate insufficient funds and unauthorized debit for ACH transactions.

Sila combines FedNow and The Clearinghouse’s RTP to allow ACH transactions to be settled in seconds.

There has been some movement in the instant payments world this week. Banking and payment infrastructure-as-a-service company Sila has partnered with instant payments platform Trice.

Under the agreement, Sila will leverage Trice’s built-in safeguards for instant payments. Founded in 2022, Trice offers the ability to eliminate ACH return codes R1 and R5. For those unfamiliar with ACH return codes, R1 typically refers to “insufficient funds,” while R5 refers to “unauthorized debit to consumer account using corporate SEC code,” meaning the accountholder did not authorize the transaction. By eliminating these return codes, Trice will help Sila lower costs, reduce losses, decrease fines, and ultimately improve the customer experience.

“This partnership reflects our dedication to simplifying financial transactions and making money movement more accessible, reliable, and cost-effective for businesses of all sizes,” said Sila Co-Founder and Chief Strategy Officer Shamir Karkal. “Trice’s innovative instant payment solutions align perfectly with our mission, and together, we aim to set new industry standards for secure and efficient money transfer services.”

Oregon-based Sila launched its ACHNow product in 2018. The tool combines The Clearing House’s RTP, the U.S. Federal Government’s FedNow, and Sila’s own instant settlement product that allows all ACH transactions to be settled in seconds. When businesses submit a standard NACHA file, ACHNow routes each transaction to either RTP or FedNow. In the event the transaction cannot be routed on either of those rails, Sila uses its own instant settlement product to clear the transaction.

“With new faster payment systems becoming available, Sila is currently in a great position to create excellent payment experiences to surprise and delight their customers,” said Trice Co-Founder and CEO Doug Yeager. “Together with Sila, we’re excited to bring these groundbreaking solutions to businesses and financial institutions, further enhancing the financial ecosystem with the promise of smarter, faster, and more secure money movement.”

This week’s edition of Finovate Global takes a look at recent fintech developments in Latin America. The region was one of the few places in the world to see significant fintech funding in Q2 of 2023. Further, fintech in Latin America will be the focus of a special panel at FinovateSpring in May.

Here are a handful of headlines to help you get up to speed on the variety of fintech innovation happening in countries like Mexico and Colombia.

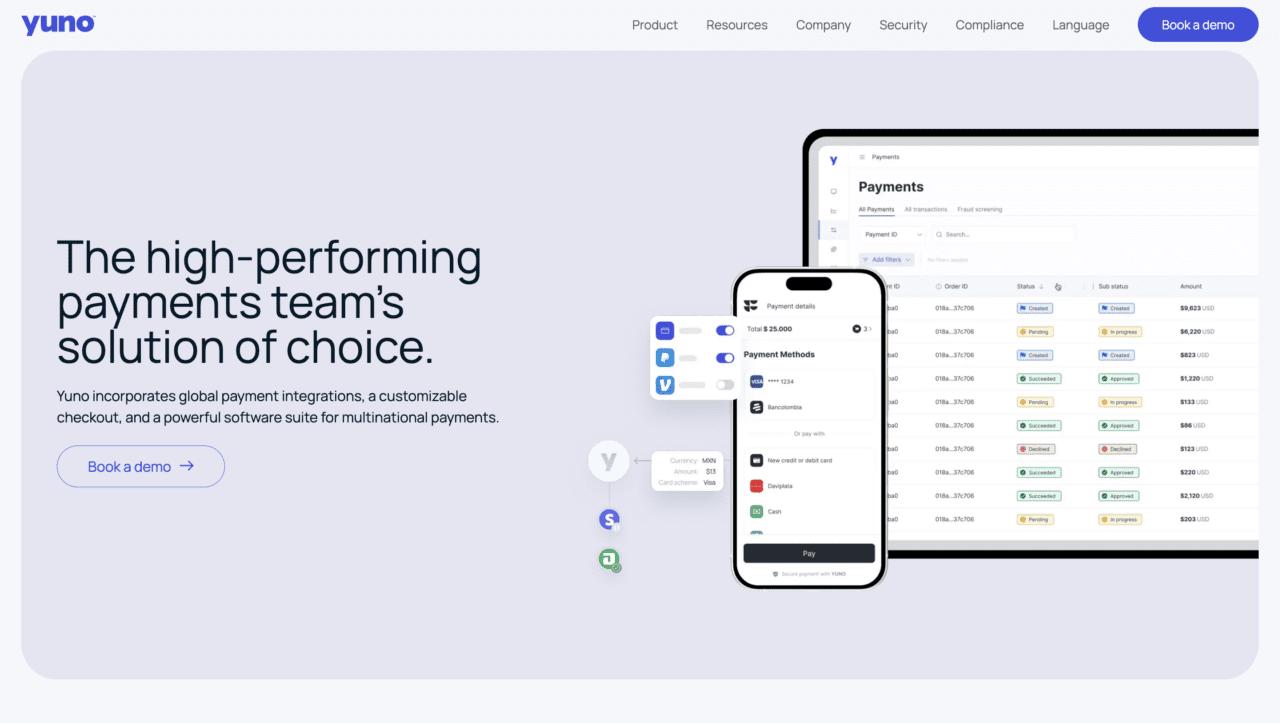

Colombian payments orchestration platform Yuno raises $25 million

Payments, as we say in the fintech business, is the gift that keeps giving. And this week, Colombian payments orchestration platform Yuno is on the receiving end. The company announced this week that it has raised $25 million in funding from a consortium of investors including DST Global Partners, Andreessen Horowitz, Tiger Global, Kaszek Ventures, and Monashees.

With customers ranging from McDonald’s to Avianca, Yuno offers fast and reliable payments orchestration for businesses in industries like e-commerce, retail, and mobility. The company’s platform offers features such as one-click checkout modifications and smart routing. Yuno also integrates data from all payment processors and anti-fraud tools into a single, unified interface. The company will use this week’s investment to support its operations in both North and South America. The investment also will help fuel Yuno’s expansion to new markets in Europe, Asia, and Africa.

“This financial backing validates our vision and our ability to take the global payments industry into the future, helping fuel positive change across many different sectors of the economy. We are thrilled to bring our cutting-edge solutions to new markets,” Yuno CEO and co-founder Juan Pablo Ortega said.

Mexico’s Ziff acquires digital lender Arrenda

Meanwhile, a few miles north, Mexican revenue-based financing company Ziffhas acquired Arrenda, a Mexico-based digital lending startup. Terms of the transaction were not disclosed. Arrenda founder and CEO Joe Merullo will take the position of Chief Technology Officer in Ziff’s C-suite.

Ziff founder and CEO Gerardo Name said the acquisition will boost the company’s product offering and “enable us to rapidly penetrate new market sectors.” Currently, Ziff’s revenue-based financing solution provides liquidity to Mexican SMEs – which often have little to no credit histories – by funding up to 36 months of receivables. The acquisition will enable Ziff to leverage Arrenda’s Adelanta digital lending platform, which enables Mexican property owners convert future rental payments into cash within 24 hours. Name added that he hopes to see Ziff distribute more than $1 billion pesos to Mexican SMEs by the end of 2027.

BBVA Technology expands to Latin America

Created in 2023, BBVA Technology announced its expansion to Latin America this week. To be headquartered in Mexico, the new entity – officially titled “BBVA Technology en América” – represents the merger of a number of technology companies that previously operated under the name BBVA Axial Tech. The goal of the nearly 600-strong body is to help advance BBVA Group’s digital transformation objectives. The company noted that in addition to a regional expansion, the creation of BBVA will help boost career opportunities for BBVA’s tech talent.

From Mexico City, Mexico, BBVA Technology will provide technology services to BBVA firms operating in Argentina, Colombia, Mexico, Peru, Uruguay, and Venezuela. Former BBVA Axial Tech CEO Robert Altes will serve as CEO of the new company.

Note that BBVA has also set up a companion entity in Europe – “BBVA Technology in Europe” – led by CEO Ricardo Jurado and headquartered in Spain.

Here is our look at fintech innovation around the world.

Asia-Pacific

Savis and Open Banking advisory firm Konsentus announced the creation of an operational structure for open banking in Vietnam.

New Zealand-based Kiwibank went live with ACI Worldwide’sEnterprise Payments Platform.

Hong Kong’s Mox partnered with Wise to enable low-cost, international payments directly from the Mox app.

Sub-Saharan Africa

South African payroll and HR software company PaySpace agreed to be acquired by HR startup Deel for $100 million.

Kenya’s Equity Bank launched instant withdrawals courtesy of a partnership with PayPal.

A partnership between Mastercard and Ethiopian commercial bank Awash Bank will bring new payment solutions to consumers in the country.

Currencycloud was offered In-Principle Approval to serve as a Major Payment Institution license holder in Singapore.

If granted the license, Currencycloud will be able to offer its full suite of intra-regional and international money movement services to Singapore businesses.

“Having the license would allow us to integrate with the robust financial network in Singapore and collaborate with valuable industry players,” said the company’s Managing Director of APAC Rohit Narang.

B2B cross-border payments fintech Currencycloud announced this week that the Monetary Authority of Singapore (MAS) offered the company In-Principle Approval (IPA) to serve as a Major Payment Institution (MPI) license holder in the region.

If the MAS grants Currencycloud the MPI license, the company will be able to offer its full suite of intra-regional and international money movement services to Singapore businesses. These additional capabilities will allow the U.K.-based company to process intra-Asia and east-to-west payments more quickly, efficiently, and seamlessly.

The MPI license will also impact Singapore-based businesses, which will be able to leverage Currencycloud to help their customers make conversions and payouts in their own time zones and local currencies. Ultimately, the license will help these local businesses launch new financial services quickly by leveraging local networks combined with its multi-currency account capabilities.

“The IPA for a Major Payment Institution License is testament to the strength of the Currencycloud brand,” said Currencycloud Managing Director of APAC Rohit Narang. “Having the license would allow us to integrate with the robust financial network in Singapore and collaborate with valuable industry players. The payments opportunity in Asia-Pacific is significant, and Singapore’s excellent infrastructure, world-class regulatory system, and strategic geographical location serve as an ideal base for accelerating future payments innovation across the region.”

Founded in 2012, Currencycloud facilitates cross-border, multi-currency transactions. In addition to offering virtual wallets, the company also enables banks, fintechs, and FX brokers to offer their users the ability to send, receive, and manage their multi-currency payments. Among the company’s clients are Starling Bank, Revolut, Penta, and Lunar.

Currencycloud was acquired by Visa in 2021. Mike Laven is CEO.

At Finovate, we are known for having companies demo their solution. Anyone can talk about their product, but showing how it works (especially in front of 1,000+ people) is difficult. Today, as we celebrate International Women’s Day– a day assigned by the United Nations— we wanted to do a demo of our own by showing three ways we are taking action on the theme for International Women’s Day, Invest in Women.

Here are three ways Finovate invests in women:

Scholarship program

We launched our scholarship program to spotlight underrepresented founders and startups tackling climate change, diversity, and financial inclusion through sustainable and equitable practices to support social and environmental change. Scholarship opportunities are available at all three Finovate events. In order to qualify for the women in fintech scholarship, the company must be either women-founded or women-owned and have less than $7 million in funding.

Equal representation on stage

Finovate’s speaker curator, Katie Gwyn-Williams, is committed to diversity, ensuring that each show features a balanced mix of male and female speakers, with at least 50% representation from each gender. As part of that she also makes a huge effort to ensure female representation on all panel discussions.

This is no small feat. Katie spends a lot of time and research to recruit the most knowledgeable females in the industry. That said, if you are a woman looking to represent your financial institution in a panel discussion, feel free to send a note her way; she’s currently recruiting for FinovateFall!

Women-centric events

Finovate is proud to feature a Women in Fintech gathering at every show. To be honest, I used to avoid sessions like these because they sounded too fluffy (who wants to talk about women when you can talk about fintech?). However, once I got over myself and began attending, I’ve found valuable discussions with actionable tips on how to uplift myself, my female colleagues, and even my daughter. Not only that, I’ve made meaningful connections with other women in the industry.

Why it matters

It is so easy to fall into discussions about the financial services industry’s insufficient efforts to invest in women. While many of the discussions are valid, let’s spend today promoting awareness about the change being made. Take action and talk about it to inspire others to make similar changes.

Payroll connectivity provider Argyle raised $30 million in Series C funding this week.

The round was led by Rockefeller Asset Management’s Fintech Innovation Fund.

New York-based Argyle made its Finovate debut at FinovateSpring 2022.

Income and employment data provider Argylesecured $30 million in new funding in a Series C round led by Rockefeller Asset Management’s Fintech Innovation Fund. Bain Capital Ventures, SignalFire, and Checkr also participated in the round. The investment consists of both equity and debt and takes the company’s total capital raised to more than $100 million. The funding will help Argyle continue to adapt and expand its automated income and employment verification platform. No valuation information was provided in the funding announcement.

This week’s news comes in the wake of a year in which Argyle notched a number of significant accomplishments and milestones. In 2023, Argyle onboarded more than 90 new customers. The company also boosted its total customer count to more than 140 firms in verticals such as mortgage, personal lending, and background screening.

To date, Argyle has processed more than 1.6 million annual verifications. This includes direct-source income and employment verifications for 90% of the U.S. workforce. Last year, the company achieved a 3.6X growth in bookings, generated cost savings for up to 80% of customers, and built integrations with lending partners ICE and nCino. Argyle also became the first consumer-permissioned provider to integrate into Dark Matter’s Empower LOS.

“Our verticalized approach and direct-source model has provided accurate data and an enhanced consumer experience for our customers,” Argyle CEO and founder Shmulik Fishman said. “With this capital from our valued investors, we will continue to tailor our solutions to priority verticals while improving the verification experience for the next wave of prospective customers that can benefit from our services.”

In an extended “Letter From Our Founder & CEO”, Fishman articulated the journey his company has made and underscored Argyle’s commitment to what he referred to as the “human side of digital transformation.” Noting that even “novel technology” is “only half the equation,” Fishman added “widespread digital transformation only happens when people trust new technologies enough to change their behavior. And change is really hard – even when it’s absolutely essential.” Calling the current moment Argyle’s “enterprise-adoption era” Fishman wrote that now was the time to ensure that “people and process take center stage.”

Headquartered in New York and founded in 2018, Argyle made its Finovate debut at FinovateSpring 2022. At the conference, company co-founder and COO Billy Marsden showed how Argyle’s Link 4.0 design update enhanced account connectivity, and decreased drop-off rates for users of its real-time income data platform. Link 4.0 also upgrades the platform’s visual style to boost consistency across Argyle’s product line.

Interested in demoing at FinovateSpring in San Francisco in May? We are happy to read applications from innovative companies with new solutions that are ready to show. Visit our FinovateSpring hub today to learn more.

FinovateSpring 2024 takes place at the Marriott Marquis San Francisco on May 21 through 23, 2024.

More than 60 innovative companies will take the stage this May, with just seven minutes to show their latest tech to the audience. The rules: No slides, no canned video. There’s no better way to quickly see the most exciting fintech – and with Finovate’s signature, live-demo format, what you’re seeing on stage is already fully functional and ready to plug in.

Take a look at the first wave of demoers for FinovateSpring 2024 – this is just the beginning! We’ll continue selecting companies for the lineup from across the fintech ecosystem, including payments, asset management, core banking, CX/UX, anti-fraud, AI, ID/KYC, regtech, retail banking, rewards and loyalty, BaaS, SMB banking, and more.

Apple began offering an API called FinanceKit in its latest iOS 17.4 update.

The new update allows developers to fetch users’ transactions and balance data from users’ Apple Card, Apple Cash, and Apple Savings accounts.

Online budgeting platforms Monarch, YNAB, and Copilot are the launch partners for FinanceKit.

In its latest iOS 17.4 update, Apple is offering an API called FinanceKit that allows developers to fetch users’ transactions and balance data from users’ Apple Card, Apple Cash, and Apple Savings accounts. The company made a similar move in the U.K. in November 2023.

Launch partners in the new update are online budgeting platforms Monarch, YNAB, and Copilot. Apple’s update will help users more easily aggregate their accounts. Instead of uploading spreadsheets of their transaction data, users will be able to see data from their Apple Card, Apple Cash, and Apple Savings in real time on the third party platforms.

“This new feature means that as you spend and save with your favorite Apple products, your transactions will appear in YNAB almost instantaneously. No manual entry required,” the company said in its blog announcement. “Imagine: when you open YNAB on your device (running iOS 17.4 or higher), all of your Apple transactions are there, ready to categorize.”

Overall, the more free flow of data will help achieve a bit of what open banking is supposed to help accomplish by allowing users to access their data how and where they want. Today’s action from Apple shows that the company believes users should own their transaction data, and it is encouraging to see the tech giant granting access to third parties.

As with most account aggregation efforts, however, bringing users’ transaction and account balance data into third party platforms will not be without friction. As PFM platform Monarch Money explained on its blog post, “For those with existing Apple Card accounts in Monarch, we recommend you sync your Apple Card again as a new account, and remove or hide the old accounts. You can also merge your history from your old Apple Card account to the new one using our merge account flows on desktop, which lets you choose whether you want to move over your old transactions and/or balances.”

What might some of the impacts be from Apple’s more open approach to users’ financial data? First, it may result in consumers increasing their usage of Apple’s financial products, such as Apple Card, as they become more integrated into users’ financial management habits. The launch of FinanceKit is also a win for PFM platforms. As more platforms are able to leverage Apple’s API to fetch consumer data, they will reduce friction and minimize consumer complaints regarding manual processes. Finally, end consumers will benefit from the launch because, not only will they enjoy decreased friction, but they will also be able to make more informed financial decisions by having their transaction and account data more readily available.

Document automation platform Ocrolus announced it has teamed up with financial data aggregation and account verification expert Envestnet | Yodlee this week.

Under the agreement, Envestnet | Yodlee will leverage Ocrolus’ technology to enhance digital document capabilities for its clients. Specifically, Envestnet | Yodlee’s 47 million customers will be able to improve their user experiences by offering their end-users the option to either submit documents or digitally connect bank accounts. Customers will also be able to automate the extraction of financial data from the documents that the end consumer uploads.

“While the financial services industry has undergone significant digital transformation, documents are still a critical source of data,” said Ocrolus Co-founder and CEO Sam Bobley. “We are thrilled to partner with Envestnet | Yodlee to provide a more comprehensive and smoother customer experience across a variety of financial services use cases.”

New York-based Ocrolus leverages AI to capture and analyze data from 1,000 different types of documents and digital forms and boasts an accuracy rate of more than 99%. The company counts more than 400 clients, including Enova, PayPal, Brex, CrossCountry Mortgage, Plaid, and SoFi, who use the solution to detect fraud, analyze cash flows and income, and streamline decisions.

With these capabilities Envestnet | Yodlee anticipates its clients will benefit from more efficient and confident decision-making. “With added document automation capabilities, Envestnet | Yodlee will improve and streamline the onboarding process for credit and lending use cases,” explained company Chief Operating Officer Arun Anur.

Envestnet | Yodlee’s client list includes more than 1,300 financial services and fintech companies, including 17 of the top 20 U.S. banks. The company was founded in 1999 as Yodlee, and changed its name to Envestnet | Yodlee after Envestnet acquired Yodlee for $660 million.

In a digital world, sharing documents can be a huge headache. However, automation platforms such as Ocrolus, this process has become much smoother. Today’s collaboration between Envestnet | Yodlee and Ocrolus marks a significant step forward in enhancing the customer experience.

U.K.-based digital bank Monzo has raised $430 million (£340 million) in a round led by Alphabet-owned CapitalG.

The funds come about a year after Monzo achieved profitability, having reached nine million customers.

Monzo’s post-money valuation is now $5 billion, up from $4.5 billion in 2022.

U.K.-based digital banking platform Monzo has raised $430 million (£340 million) in a round led by Alphabet-owned CapitalG.

Also participating in the round, which was first rumored last week, were new investors, Google Ventures and HongShan Capital, along with existing contributors Passion Capital and Tencent. The new round boosts Monzo’s post-money valuation to $5 billion (£4 billion), which is up from the $4.5 billion valuation it received in 2022. According to Crunchbase, Monzo’s total investment amount now stands at $1.5 billion.

“With backing from global investors, we have the rocket fuel to go after our ambitions harder and faster, building Monzo into the one app that sits at the centre of our customers’ financial lives,” said company CEO TS Anil. “Each milestone we’ve reached to this point has given us more strength and speed to make strides towards our mission – now we’ll scale to even greater heights and seize the huge opportunity ahead.”

Monzo plans to use the funds to fuel expansion and to help the company improve its product roadmap. The timing of the funds, combined with the company’s expansion ambitions, come at a good time. That’s because, since it was founded in 2015, Monzo has acquired nine million users– two million of which were brought on just last year. This growth, combined with higher interest rates, pushed Monzo to achieve profitability in March of last year.

Monzo originally launched in 2015, the early days of digital challenger banks. In the U.K., the company offers both personal and business accounts that feature current and savings accounts, unsecured personal loans, and investment funds powered by BlackRock. U.S. users are limited to personal and joint checking accounts, but have the option to aggregate data from other financial services providers in order to get a holistic picture of their overall financial standing.

According to Monzo’s public roadmap, the company is currently working on budgeting improvements, paying interest on savings balances, and a faster onboarding experience. For the future, the company plans to develop digital billpay, capabilities and the ability to send checks, and also has stretch goals to launch a check depositing feature, subscription management, and merchant spending rules.

Open data fintech Moneyhub is teaming up with fellow fintech providers, Rebcat and Navos Technologies.

Via the partnership, the three companies will work together to develop solutions to help large financial institutions offer personalized financial advice to their customers.

U.K.-based Moneyhub made its Finovate debut at FinovateEurope 2015 in London.

Open data fintech provider Moneyhub announced a new partnership this week. The U.K.-based firm has teamed up with fellow fintechs Rebcat and Navos Technologies to help financial institutions offer personalized financial advice and guidance to their customers. The companies will collaborate to launch a number of personalized plug-and-play services, focusing initially on closing the so-called “advice gap.” Additionally, the services will also include financial management, investments, and mortgages.

Moneyhub CEO Samantha Seaton pointed to regulatory changes in the U.K. as one of the trends that guided the partnership decision. “The upcoming changes to the Data Bill and the FCA’s proposals to relax the advice-guidance boundary highlight the significant role of digital advice businesses in the future,” Seaton said. “We have seen first-hand how advanced and robust Rebcat technology is and are delighted with this partnership and the opportunities it brings to unlock financial wellness for more people.”

The joint statement makes clear that Rebcat’s technology is at the core of the offering. The firm is a spin-out of OpenMoney, a digital adviser that Octopus Group acquired in 2023. With nearly 20,000 customers, Rebcat provides a range of B2B financial services. These include white-labeled, end-to-end investment and mortgage advice, as well as a bespoke personal finance and engagement app. Headquartered in Manchester, Rebcat leverages Open Data to help companies offer their customers personalized support and advice. Based in Bristol, Navos Technologies provides services ranging from building digital strategies to implementing effective cybersecurity. Founded in 2020, the company leverages its 120 years of combined experience at U.K. investment platform Hargreaves Lansdown to help companies reach their digital transformation goals.

A Finovate alum since its debut at FinovateEurope in 2015, Moneyhub supports seamless connections via a single source to thousands of financial institutions in 37 countries. This enables financial services companies to access a comprehensive view of their customers needs, habits, preferences, and aspirations. Banks, pension companies, wealth managers, lenders, retailers, and insurers all use Moneyhub’s open data platform to transform data into personalized digital experiences and insights – as well as initiate payments.

Headquartered in Bristol, Moneyhub was founded in 2011. The company began this year by earning a spot as a supplier on Crown Commercial Service’s (CCS) Open Banking Dynamic Purchasing System (DPS) framework for its Open Banking and Payment services. CCS is an Executive Agency of the Cabinet Office. The entity helps the public sector secure maximum commercial value when procuring goods and services.

Galileo Financial Technologies has expanded its partnership with The Bancorp Bank.

Though The Bancorp Bank, Galileo will leverage The Clearing House’s Real Time Payments network to offer real-time payments to help its retail and commercial clients transfer money in real time, 24-hours a day.

The Clearing House reported record usage of its RTP network in the third quarter of last year, when it reached 64 million transactions valued at $34 billion.

Under the scaled up agreement, Galileo and The Bancorp will leverage The Clearing House’s Real Time Payments (RTP) network to fuel real-time payments services. By offering instant money movement between bank accounts, the two will enable Galileo’s fintech clients to help their retail and commercial customers solve cash flow challenges by gaining fast access to their funds.

With the RTP network, real time money movement is available on any day of the year, 24-hours a day. This availability and speed not only solves cashflow issues, it also helps businesses deal with time sensitive transaction and ultimately enhances customer satisfaction.

“Consumers and businesses expect payments to be available instantly, and offering real-time payment capabilities ensures Galileo’s clients can deliver on that expectation,” said Galileo Financial Technologies Chief Product Officer David Feuer. “With this integration between The Bancorp and Galileo, we can offer a swift, efficient way to ensure faster money movement today.”

The Clearing House, which launched its RTP network in 2017, has seen growth in demand for real-time payments. In the third quarter of last year, the company reported that usage of its RTP network hit a record high, reaching 64 million transactions valued at $34 billion. The Clearing House competes directly with the U.S. government’s real-time money service, FedNow, which launched in July of 2023. Currently, more than 350 financial institutions enable their retail customers and 150,000+ business clients to send payments over the RTP network.

Founded in 2001, Galileo is a payment processing platform that allows third party fintechs and businesses to build and scale their own financial services offerings. The company’s client list includes DailyPay, Bluevine, Dave, MoneyLion, Monzo, and others. Galileo was acquired by SoFi in 2020 in a $1.2 billion deal.

Headquartered in Wilmington, Delaware, The Bancorp Bank provides fintechs with the people, processes, and technology to meet their banking needs. The bank is the third-largest bank by assets, has more than 75 million prepaid cards in distribution and processes 1.1 billion transactions each year. Damian Kozlowski is President and CEO.

Do you remember the parable about the blind men and the elephant? In some respects, trying to encapsulate the two days of FinovateEurope into a single conversation recalls their challenge.

It will come as no surprise that AI was top of mind. However, less than three years into this AI revolution, it was impressive to see calm heads and cautious strategies among the enthusiasm and anxiety. From AIs working with human agents to AI-enabled automation, putting the technology to practical use – on both the backend and frontend – is helping integrate AI more constructively into financial services than we might have imagined back in the days when we were first enthralled by ChatGPT.

That said, there is more to financial services and fintech in 2024 than AI. As more than one observer noted over the two days of FinovateEurope last week: AI may be king, but the kingdom is still the customer experience.

A View from the Keynote

That said, our Out of the Box Keynote address from author and Generative AI expert Nina Schick set the AI-powered tone early on Day One. From her presentation – Will AI Be More Profound Than The Invention Of The Internet? What Do Financial Institutions Really Need to Understand About Generative AI? – three points stood out to me.

First, popular opinion – and mass media news coverage – tends to treat AI and its innovations as either “dangerous” (New York Times, May 30, 2023: “AI Poses ‘Risk of Extinction,’ Industry Leaders Warn”) or “dumb” (The Guardian, March 16, 2023: “The stupidity of AI”). Thinking, or assuming, that AI will clearly be one or the other blinds us to the potential for the technology.

Furthermore, it is commonplace to suggest that AI will only be as “dangerous” or as “dumb” as its creators (not an entirely comforting thought, but …). Nevertheless, our relationship with AI will not be static; it will evolve as the technology evolves. In the process, we will become more attuned to, and aware of, the limitations of both AI as well as ourselves. In this, I am reminded of an observation by another AI expert who remarked that our experience with AI might actually help us understand more about what it means to be human. With each successive conversation about this technology, this viewpoint becomes more credible to me.

A second point from Schick is that many observers are focused on what is called “Artificial General Intelligence.” This refers to AI that is able to perform as well or better than humans at a variety of cognitive tasks, including the ability to self-teach. This is also the AI that the world is alternately anxious and excited about. Schick noted that before we get to artificial general intelligence (AGI), however, we will experience a period when what she called “Artificial Capable Intelligence” (ACI) will drive innovation.

ACI bridges the gap between the AI we see on display with large language models (LLMs) and Generative AI solutions on one hand and a potential future AGI on the other. Rather than what we can compel AI models to say or generate, ACI seeks to figure out what AI is “capable” of doing with its intelligence. As AI researcher Mustafa Suleyman wrote in an article for MIT Technology Review last July: “We don’t want to know whether the machine is intelligent as such; we want to know if it is capable of making a meaningful impact in the world. We want do know what it can do.”

As Schick elaborated on this concept, the ACI stage of AI’s evolution will not require machines that think or have achieved some level of sentience. Nevertheless, at this point, AI technology can perform highly specialized tasks – including emotional tasks – that would have been considered impossible for machines to conduct before. A recent Google study that showed its Articulate Medical Intelligence Explorer (AMIE) LLM outperforming human doctors, as well as, AI-assisted doctors, in a test of diagnostic reasoning and conversation. This is an example from health care, but the use cases in financial services – from debt resolution to wealth management – are clear.

Lastly, Schick emphasized that AI is a meta-technology rather than a single technology. As such we will be able to apply AI to a wide and growing variety of experiences and challenges. Moreover, as a meta-technology, AI will also have the ability to upskill a sizable range of activities – from the quantitative to the creative. This will cause no small measure of anxiety among many, but Schick believes that the benefits will be significant – and in many cases, surprising – enough to fuel continued engagement and innovation rather than retrenchment.

A View from the Money

What can we expect on the funding front for innovative startups in fintech? Where is the Smart Money looking – and investing – in 2024?

Our panel – Investor All Stars: Where Is The Smart Money Investing in Fintech? – is always one of the most well-attended sessions at FinovateEurope. These are the conversations that put technological innovation in the context of what’s actually possible. After a full day of watching live fintech demos, our All-Star Panel often arrives the following afternoon as a bracing tonic: what did you see? what did you like? what would you buy?

Claire Mongeau

This year, our investor panel at FinovateEurope featured Robin Scher, Head of Fintech Investment, Lloyds Banking Group; Sophie Winwood, Operating Partner, Foxe Capital; and Dallin Bills, Principal, Battery Ventures. Founders Factory Investor Claire Mongeau moderated the conversation.

If AI is the big driver for technological innovation in fintech and financial services, then the cost of money – namely, interest rate policy in the U.S. and Europe – are likely to give us the clearest indication of what to expect when it comes to investment in our industry this year.

While the panel in general was optimistic about funding in 2024, especially in the second half, they also agreed that interest rates will help determine the appetite for investment in fintech and that appetite will, in turn, help drive valuations.

Dallin Bills

There was also robust discussion of the M&A front. Capital One’s acquisition of Discover Financial in February was an early sign that 2024 might feature some welcome consolidation in the financial services space. And while the panel was united on the likelihood that M&A could be surprisingly active this year, there was debate on whether strategic transactions or private equity-fueled moves would dominate.

Bills noted, in favor of private equity, that there is $2.5 trillion in “dry powder on the sidelines”, a record amount, he said. Bills added that there are potential opportunities not only in AI and AI-powered automation, but also in niche areas like tax and accounting. Scher added that strategic M&A was “very much still in play” for 2024. “There are too many fintechs doing the same thing,” Scher observed, “and they don’t seem to realize it.”

Sophie Winwood

What do our panelists like? Winwood echoed Bills interest in the tax and accounting space. She also highlighted a “new wave of insurtechs” as worth keeping an eye on, as well as continued innovations in the wealthtech/wealth management space. With Millennials well into family formation mode, and both homebuying and saving for college becoming top agenda items for them, companies who are able to help these young families navigate these major financial challenges could be in high demand.

That, however, does not necessarily mean good times for lenders – digital or otherwise – as Bills noted. Many of these companies are still reeling from the interest rate hikes of 2023, and the prospect of interest rates remaining relatively high in the near-term is likely to encourage investors to take a hands-off, or at least wait-and-see, approach to the space.

Robin Scher

Perhaps most inspiring was Winwood’s observation that often some of the best companies are started during times of crisis and uncertainty. Further, she added, it’s never been easier to launch a new fintech. Maybe, if the previous fintech boom was characterized by a YOLO, ZIRP-fueled, free money mania, then perhaps the next boom will be characterized by greater sense and sobriety.

After all, she concluded wryly, if you’re starting a fintech today “you’re either mad or really love the problem and want to solve it.”